United States Stacker Market Size, Share, Trends and Forecast by Type, End User, and Region, 2026-2034

United States Stacker Market Size, Share, Trends & Forecast (2026-2034)

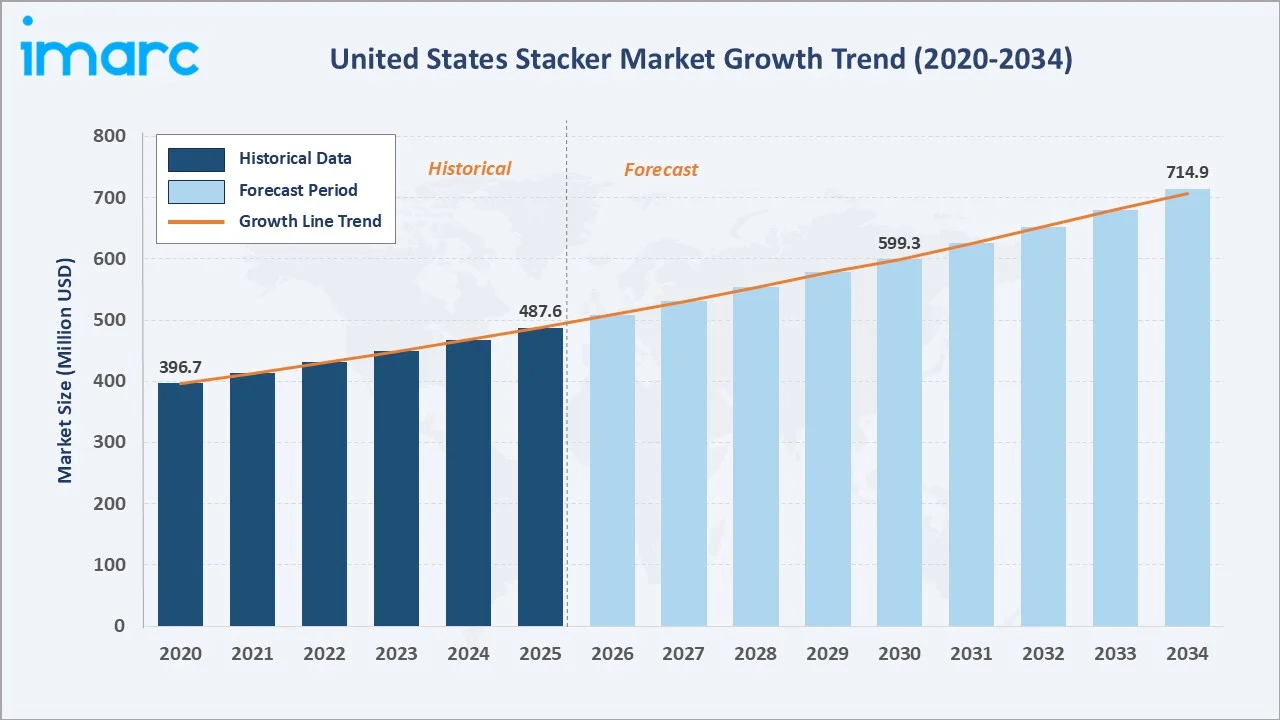

The United States stacker market reached USD 487.6 Million in 2025 and is projected to reach USD 714.9 Million by 2034, growing at a CAGR of 4.21% during 2026-2034. The rapid expansion of e-commerce is driving large-scale warehouse and fulfilment center construction, accelerating the adoption of electric stackers driven by sustainability commitments and operational efficiency advantages, integrating IoT and automation technologies in warehouse material handling, and labor cost reduction and workplace safety compliance, driving powered stacker investment are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 487.6 Million |

|

Forecast Market Size (2034) |

USD 714.9 Million |

|

CAGR (2026-2034) |

4.21% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

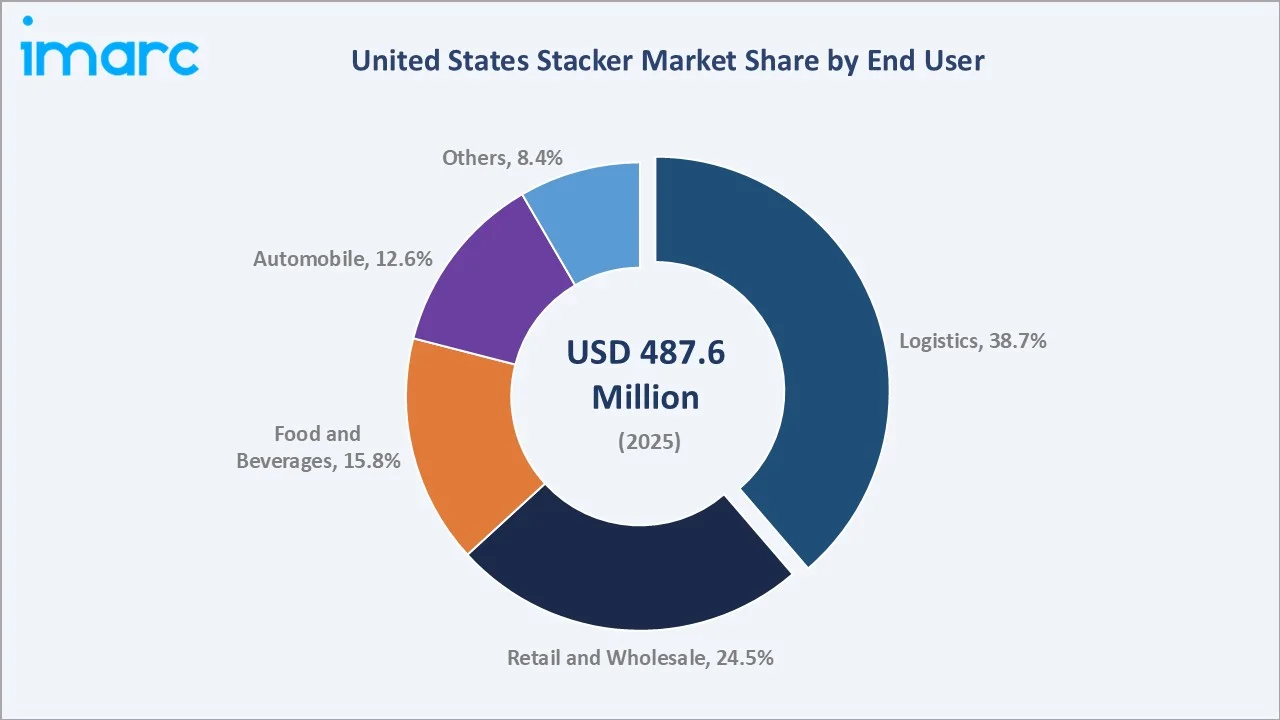

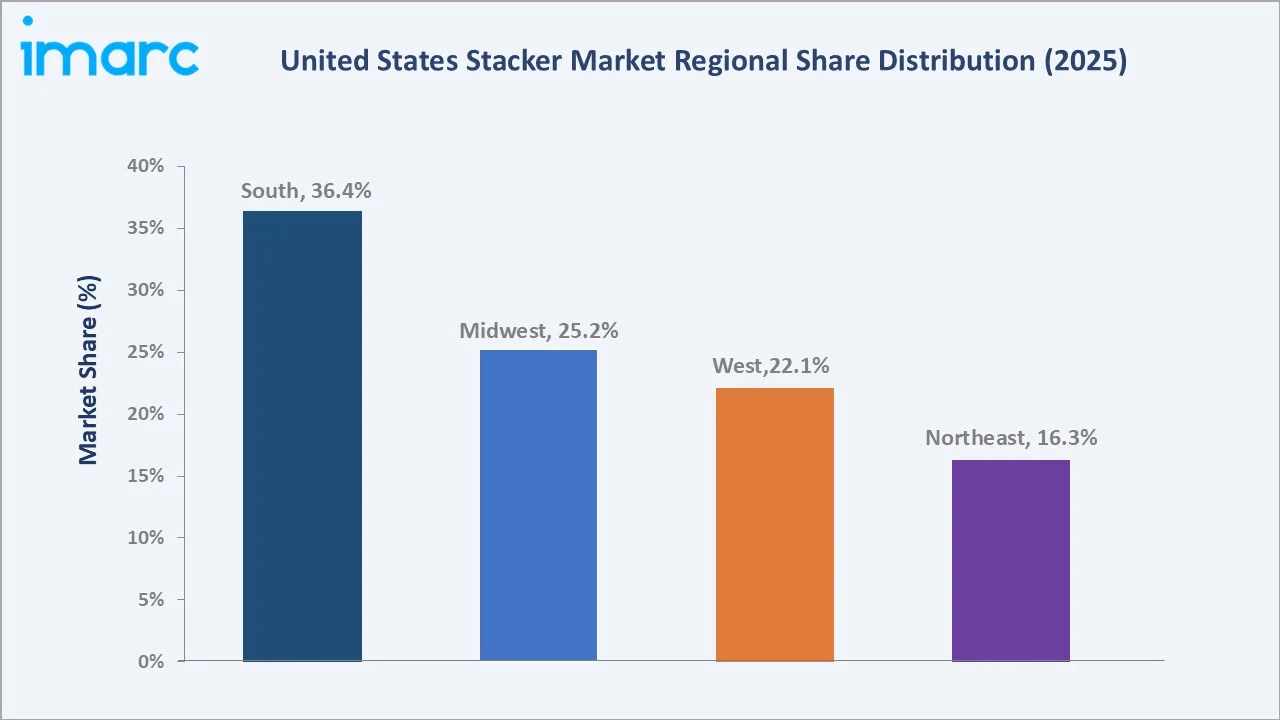

The South leads regionally with a 36.4% share in 2025, driven by the region’s concentration of Amazon, Walmart, and third-party logistics fulfilment centers, strong food and beverage manufacturing and distribution, and major automobile manufacturing and parts distribution in Texas, Tennessee, and the Carolinas. Logistics at 38.7% of the end user segment reflects e-commerce and supply chain-driven warehouse expansion as the primary stacker demand generator in the US market.

To get more information on this market, Request Sample

The US stacker market is driven by three structural demand forces: the e-commerce revolution that has created a structurally higher level of warehouse and fulfilment center construction, each deploying fleets of stackers for goods receipt, storage, and order picking operations; the electric stacker transition that is replacing legacy manual and IC engine-powered equipment with battery electric units that deliver lower total cost of ownership, zero indoor emissions, and reduced maintenance requirements; and the automation integration that is progressively converting standard electric stackers to semi-autonomous and fully automated guided vehicle (AGVs) that reduce labor dependency in high-volume warehousing operations.

Executive Summary

The United States stacker market is experiencing steady growth, underpinned by the structural transformation of US retail and logistics toward e-commerce fulfilment models that require intensive warehousing and material handling operations. Moreover, the progressive electrification of the stacker fleet, replacing aging manual and IC-powered equipment, and the integration of IoT, fleet management, and automation technologies are expanding the value proposition of electric stacker investment beyond simple unit economics to operational intelligence and labor optimization. The market was valued at USD 487.6 Million in 2025 and is forecast to reach USD 714.9 Million by 2034, growing at a CAGR of 4.21%.

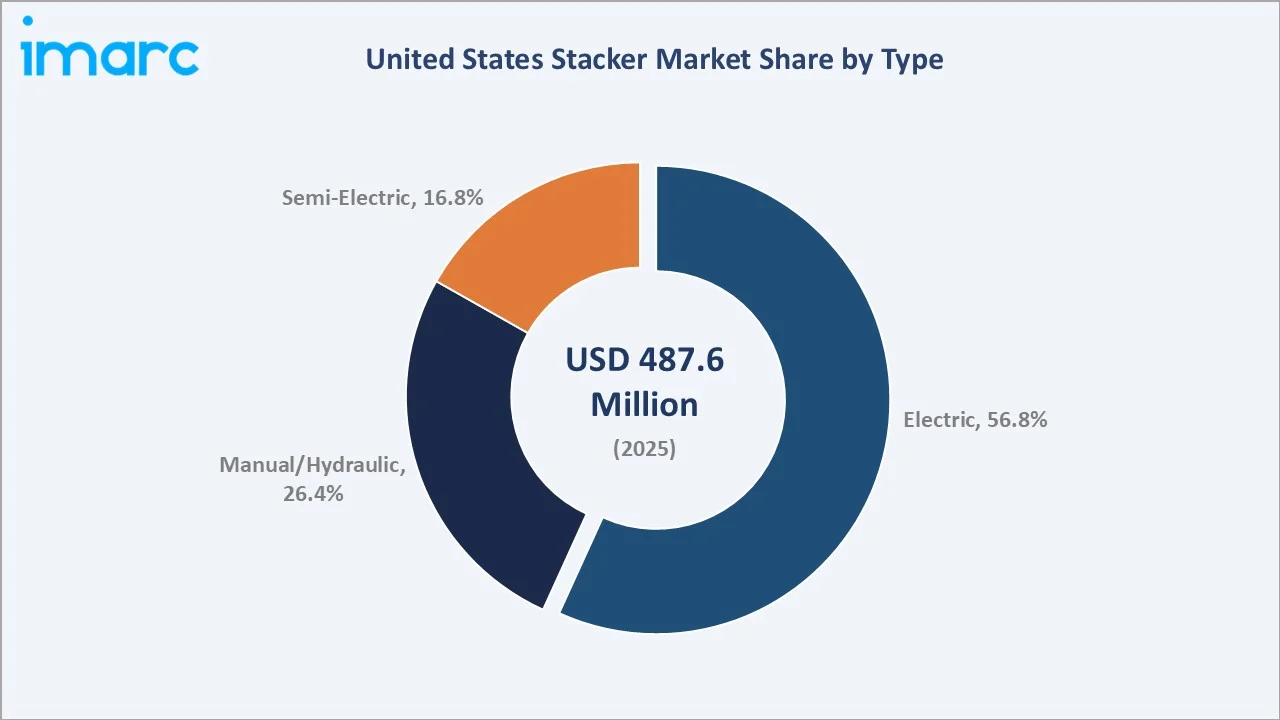

Electric vehicles at 56.8% have achieved a dominant market share in 2025, marking a structural market milestone where battery electric operation has become the default technology choice for new stacker procurement across logistics, retail, and food and beverage applications. Lithium-ion battery technology’s adoption as the premium energy storage solution is further accelerating electric stacker adoption by reducing the total cost of ownership gap versus manual alternatives. Logistics at 38.7% of the end user segment reflects the primacy of e-commerce warehouse and fulfilment center demand as the market’s growth engine.

The South leads regionally at 36.4%, driven by strong warehouse automation adoption, expanding e-commerce and retail distribution hubs, growing manufacturing activity, and high demand for material-handling equipment across logistics, food processing, automotive, and industrial facilities. Key players compete across product range breadth, electric technology capability, automation integration, and fleet management service depth.

Key Market Insights

|

Insight |

Data |

|

Largest End User |

Logistics – 38.7% share (2025) |

|

Second Largest End User |

Retail and Wholesale – 24.5% share (2025) |

|

Largest Type |

Electric – 56.8% share (2025) |

|

Second Largest Type |

Manual/Hydraulic – 26.4% share (2025) |

|

Leading Region |

South – 36.4% share (2025) |

|

Key Market Players |

Crown Equipment Corporation, Toyota Industries Corporation, Hyster-Yale, Inc., Jungheinrich AG, KION GROUP AG |

Key Analytical Observations Supporting the Above Data:

- Logistics at 38.7% share (2025) leads the end user segment as the US e-commerce market’s structural shift has created sustained growth in fulfilment center, distribution center, and last-mile delivery hub construction, each deploying stacker fleets for pallet receipt, storage racking, and order preparation operations.

- Electric at 56.8% (2025) reflects the structural transition driven by multiple converging factors: OSHA indoor air quality regulations prohibiting IC engine operation in enclosed facilities, lithium-ion battery economics delivering 20–30% lower total cost of ownership versus IC alternatives over a 5–7 year asset life, and electric stacker manufacturers’ expanded product range now covering weight capacities and lift heights previously served only by IC models.

- Retail and wholesale at 24.5% (2025) reflects the second-largest end user category, driven by grocery distribution center and retail back-of-store stacker requirements for pallet handling and high-density racking environments. The growth of omnichannel retail fulfilment is creating new back-of-store electric walkie stacker demand across major US retail chains.

- The South’s 36.4% share (2025) reflects the region’s position as the primary US logistics and fulfilment center development zone, with Texas, Florida, Georgia, Tennessee, and the Carolinas hosting the highest density of new warehouse and distribution center construction.

United States Stacker Market Overview

Stackers are powered or manually operated warehouse material handling equipment designed to lift, transport, and stack palletized loads to elevated racking positions in warehouse and distribution facilities. The product category encompasses walkie stackers, rider stackers, reach stackers, and counterbalanced stackers. The US market serves warehouse and distribution operations, retail and wholesale storage facilities, food and beverage manufacturing and cold chain operations, automobile parts and assembly logistics, pharmaceutical distribution, and industrial storage applications.

Macroeconomic drivers include the U.S. e-commerce sales reaching approximately USD 1.234 trillion in 2025, rising 5.4% from USD 1.170 trillion in 2024, creating structural warehouse capacity expansion that directly drives stacker procurement; the CBRE reporting US industrial and logistics real estate vacancy at historic lows 3.5%, driving new warehouse construction starts above 250 Million square feet annually through 2024; and OSHA’s continued enforcement of 1910.178 powered industrial truck regulations requiring operator certification and equipment maintenance standards that drive fleet replacement of aging manual equipment with compliant, inspectable electric stackers.

Market Dynamics

To evaluate market opportunities, Request Sample

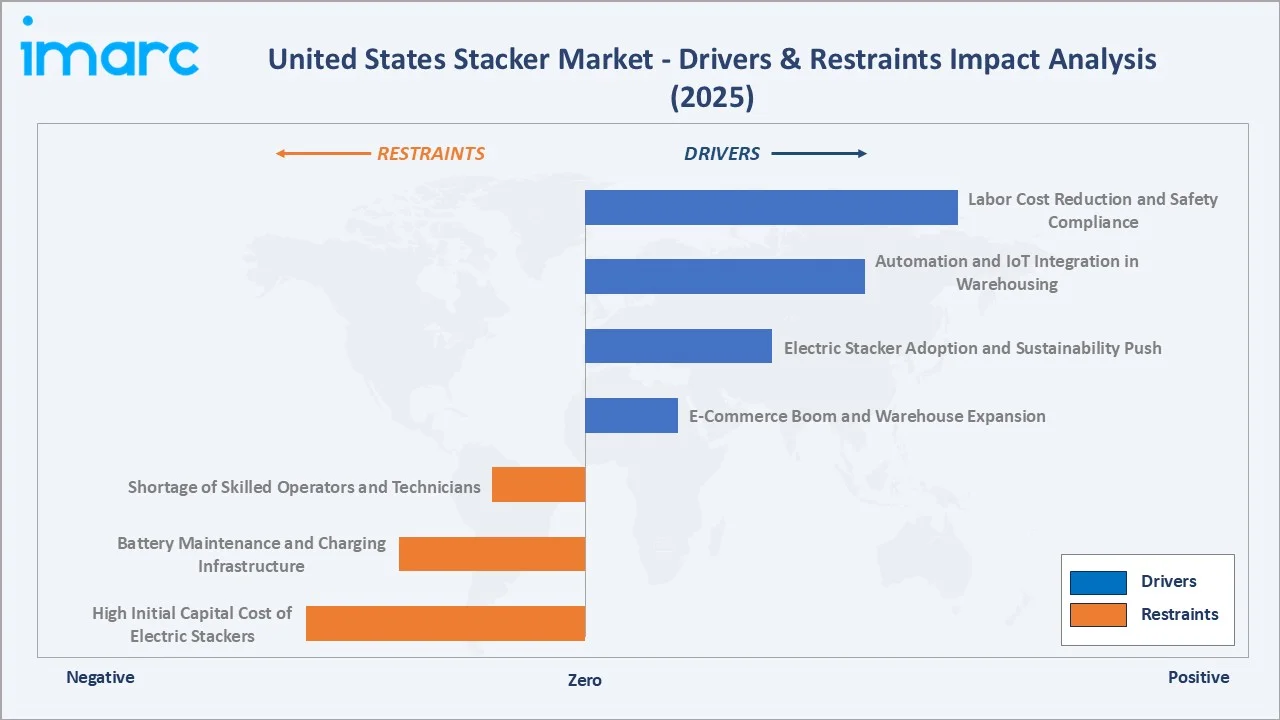

Market Drivers

- E-Commerce Boom and Warehouse Expansion: The structural expansion of US e-commerce has created an unprecedented wave of fulfilment center, distribution center, and cold storage warehouse construction that directly drives stacker fleet procurement. Each new fulfilment center of 500,000+ square feet typically deploys 50–200 stacker units, depending on the operating model.

- Electric Stacker Adoption and Sustainability Push: Corporate sustainability commitments are driving logistics operators, retailers, and manufacturers to accelerate electric stacker conversion programs as part of warehouse emission reduction strategies. The cost economics of lithium-ion electric stackers have improved dramatically, with a 5–7 year total cost of ownership including fuel, maintenance, and productivity metrics now demonstrating parity or advantage versus IC alternatives in most indoor warehousing applications.

- Automation and IoT Integration in Warehousing: The integration of IoT fleet management, RFID tracking, and AGV capability into warehouse stacker operations is creating a new premium product category that commands above-average pricing while delivering measurable labor productivity and throughput improvements. The Raymond Corporation’s Raymond Courier 3030 Automated Stacker exemplifies the automation trend, enabling unmanned stacker operation in defined warehouse zones with automatic charging.

- Labor Cost Reduction and Safety Compliance: US warehouse labor costs have increased significantly as the e-commerce expansion has driven competition for warehouse workers, with average warehouse hourly wages rising above USD 18-20 per hour in major logistics markets. This labor cost inflation is creating a strong economic rationale for investment in electric stackers that enable single operators to handle more pallet moves per shift versus manual pallet jack alternatives, and for semi-automated and automated stacker systems that can reduce the number of operators required for equivalent throughput.

Market Restraints

- High Initial Capital Cost of Electric Stackers: Electric walkie stackers cost USD 5,000–15,000, and rider electric stackers USD 15,000–40,000 or more, versus comparable manual pallet jacks at USD 500–2,000, creating a significant capital cost barrier for small and medium warehouse operators and independent retailers who cannot justify electric stacker investment based on limited daily usage cycles.

- Battery Maintenance and Charging Infrastructure: Lead-acid battery-powered electric stackers require distilled water top-up, equalization charging, and regular battery capacity testing that add maintenance complexity versus manual alternatives. While lithium-ion batteries eliminate these maintenance requirements, the higher upfront cost of lithium-ion stacker packages creates an additional capital barrier versus lead-acid alternatives.

- Shortage of Skilled Operators and Technicians: OSHA’s 1910.178 standard requires all powered industrial truck operators to be trained and certified before operating stacker equipment, creating a recurring training cost and administrative burden for warehouses with high operator turnover rates that are common in the US logistics sector. The shortage of qualified electric stacker technicians with lithium-ion battery system expertise is constraining service capacity at OEM dealer networks.

Market Opportunities

- Automated and Semi-Autonomous Stacker Systems: The progressive automation of warehouse operations is creating growing demand for semi-autonomous and fully AGV stacker systems that can perform predefined routes and stacking operations without continuous operator input. Each automated stacker unit deployed replaces 1.5–2.0 operator shifts per day of labor cost, creating compelling ROI in high-wage US warehouse markets.

- Lithium-Ion Retrofit and Fleet Upgrade Programs: The large installed base of aging lead-acid battery electric stackers in US warehouses represents a significant fleet upgrade opportunity as operators replace lead-acid battery packs with lithium-ion retrofit systems, or replace end-of-life lead-acid stackers with new lithium-ion models. The lithium-ion retrofit market enables operators to benefit from reduced battery maintenance, faster opportunity charging, and longer service life without full stacker replacement capital expenditure, representing a growing aftermarket revenue opportunity for stacker OEMs and battery system specialists.

Market Challenges

- Chinese Manufacturer Price Competition: Chinese stacker manufacturers are aggressively entering the US market with electric walkie and semi-electric stacker products priced 20–40% below traditional models. While Chinese products initially faced quality and after-sales support concerns, ongoing product quality improvement and the establishment of US distribution networks by major Chinese manufacturers are creating price competition that is pressuring margins at premium US and European brand stacker dealers.

- Evolving Battery Technology Transition Complexity: The stacker market’s transition from lead-acid to lithium-ion battery technology is creating complexity for fleet managers operating mixed battery technology fleets, with different charging infrastructure, maintenance protocols, and battery management system requirements. Operators with legacy lead-acid stacker fleets face capital investment decisions on whether to refresh batteries on existing equipment or accelerate full stacker replacement with lithium-ion models, creating procurement decision complexity that can delay purchasing decisions and extend replacement cycles.

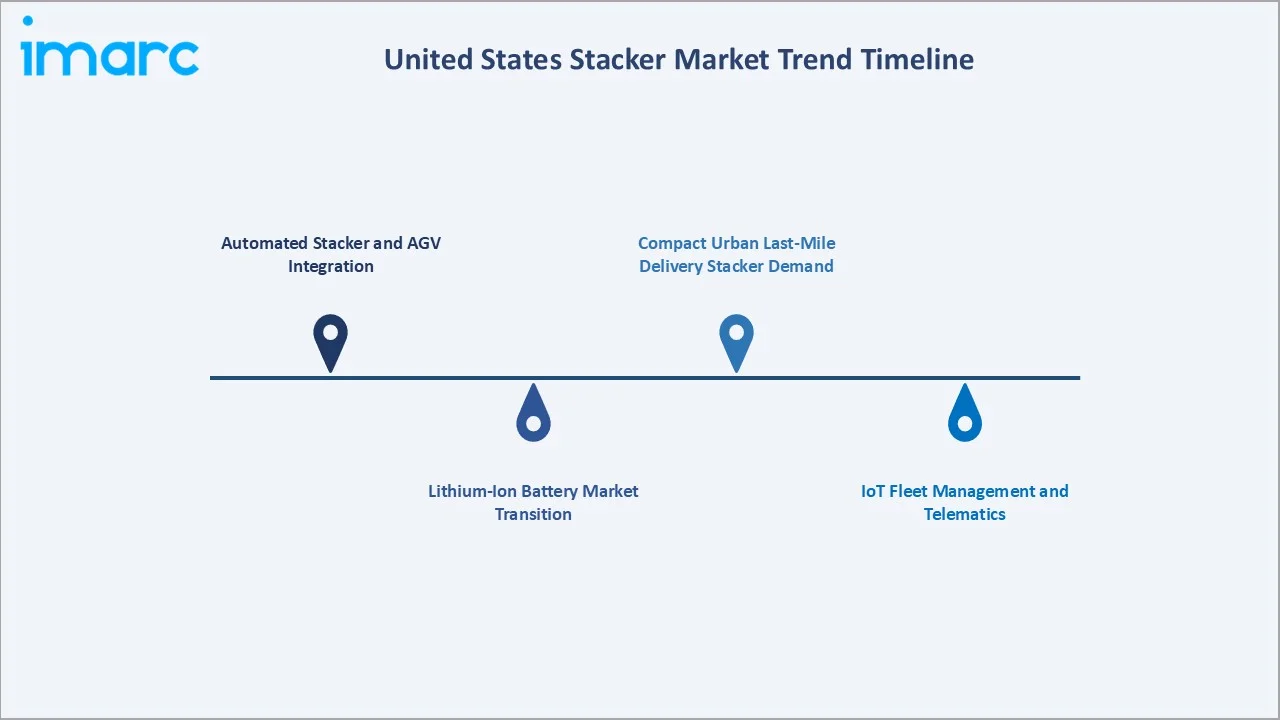

Emerging Market Trends

1. Automated Stacker and AGV Integration

The commercial launch of automated stacker and collaborative mobile robot (CMR) systems that work alongside human operators in defined warehouse zones is the most significant structural trend reshaping the US stacker market through 2034. The Raymond Corporation’s Courier 3030 Automated Stacker enables unmanned pallet stacking in defined warehouse corridors with automatic return to a charging station when idle. Jungheinrich’s automated walkie stacker exemplifies the commercial product pipeline entering the US market, targeting the high-labor-cost logistics operations where automated stacker ROI is most compelling.

2. Lithium-Ion Battery Market Transition

The stacker market’s transition from lead-acid to lithium-ion battery energy storage is accelerating from a premium option to the standard specification across major stacker OEM product lines. Lithium-ion’s advantages, including 3–5× longer cycle life, opportunity charging without memory effect, no watering or equalization maintenance, 30–40% lower weight for equivalent energy capacity, and significantly better performance at cold storage temperatures, are compelling enough to justify the 30–50% premium over lead-acid equipped alternatives in most professional warehouse applications.

3. IoT Fleet Management and Telematics

IoT-connected fleet management platforms that provide real-time data on operator productivity, battery state of charge, service due status, impact event recording, and equipment utilization rates are transforming stackers from simple physical equipment to data-generating operational intelligence tools. Crown’s InfoLink, Raymond’s iWAREHOUSE, and Jungheinrich’s FMS are each attracting software subscription revenue alongside equipment sales, creating recurring service revenue models that improve stacker OEM customer retention. These platforms also enable evidence-based fleet rightsizing that justifies additional procurement from data-informed logistics operations.

4. Compact Urban Last-Mile Delivery Stacker Demand

The growth of urban warehouse and micro-fulfilment center operations serving same-day and next-day delivery requirements is creating demand for ultra-compact electric walkie stackers and pallet movers that can operate in the constrained aisles of multi-storey urban warehouses. These compact units command pricing premiums above standard walkie stackers and are growing at above-market rates as the US urban fulfilment infrastructure buildout accelerates.

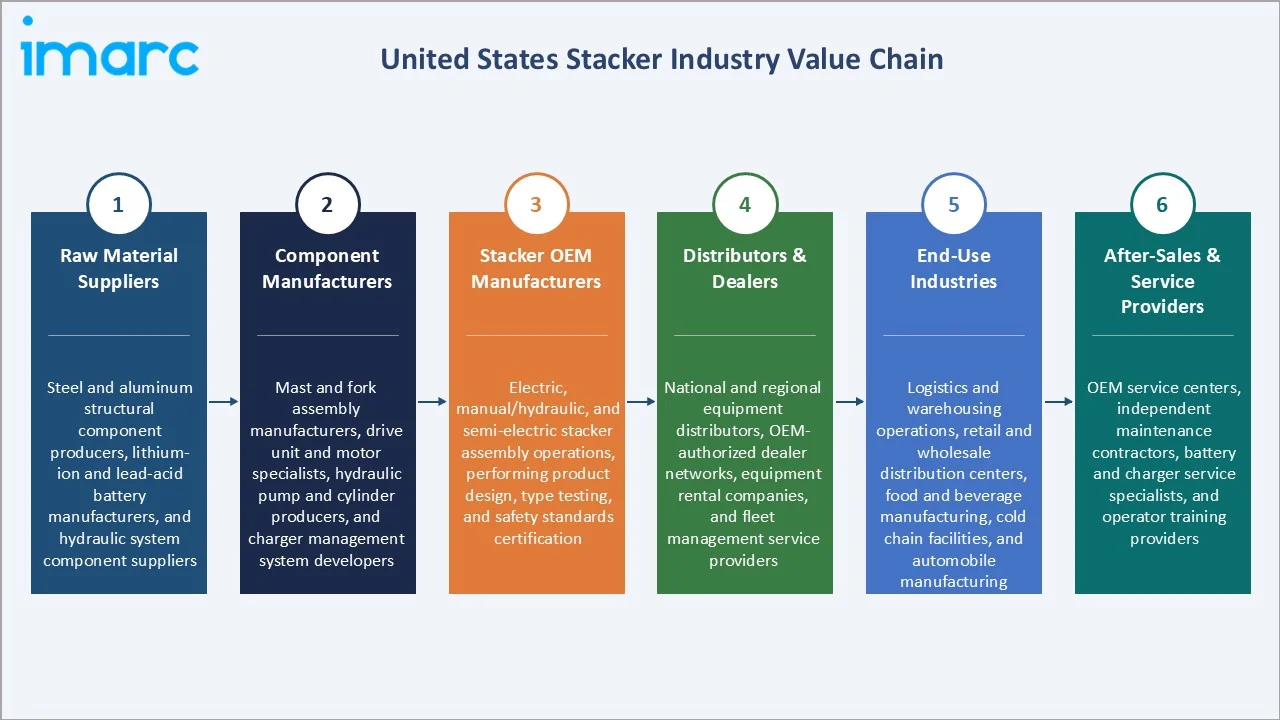

Industry Value Chain Analysis

The US stacker market value chain spans from raw material and component supply through OEM manufacturing, distribution and dealer networks, end-use deployment across logistics, retail, food and beverage, and automobile sectors, and aftermarket service and fleet management.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Steel and aluminum structural component producers, lithium-ion and lead-acid battery manufacturers, and hydraulic system component suppliers |

|

Component Manufacturers |

Mast and fork assembly manufacturers, drive unit and motor specialists, hydraulic pump and cylinder producers, and charger management system developers |

|

Stacker OEM Manufacturers |

Electric, manual/hydraulic, and semi-electric stacker assembly operations, performing product design, type testing, and safety standards certification |

|

Distributors & Dealers |

National and regional equipment distributors, OEM-authorized dealer networks, equipment rental companies, and fleet management service providers |

|

End-Use Industries |

Logistics and warehousing operations, retail and wholesale distribution centers, food and beverage manufacturing, cold chain facilities, and automobile manufacturing |

|

After-Sales & Service Providers |

OEM service centers, independent maintenance contractors, battery and charger service specialists, and operator training providers |

Technology Landscape in the United States Stacker Industry

Electric Walkie and Rider Stacker Technology

Electric walkie and rider stackers represent the core technology platform of the US stacker market, with AC motor drive systems replacing older DC technologies to deliver improved energy efficiency, regenerative braking energy recovery, and brushless motor maintenance elimination. Traction control systems, electronic stability control, and automatic speed reduction in corners are standard safety technologies on premium electric stackers, reducing the incidence of tip-over incidents in warehouse environments. Integrated digital displays providing battery state of charge, service alerts, and productivity data are standard on current-generation premium electric stackers.

Lithium-Ion Battery Systems

Lithium iron phosphate (LFP) chemistry has emerged as the preferred lithium-ion battery chemistry for warehouse stacker applications, providing a favorable balance of energy density, cycle life, safety, and cost. The ability to charge LFP batteries from 20% to 80% state of charge in 30–60 minutes without battery degradation enables opportunity charging during operator breaks and shift changes, fundamentally changing warehouse charging infrastructure requirements versus lead-acid batteries that require 8-hour overnight charging cycles.

Automated Guided Vehicle and Autonomous Stacker Technology

Commercial automated stacker systems use a combination of laser navigation (LIDAR), magnetic guide tape, QR code mapping, and visual SLAM (Simultaneous Localization and Mapping) technologies to navigate predefined warehouse routes without operator input. Safety systems, including 360-degree obstacle detection using laser scanners, automatic speed reduction in proximity zones, and emergency stop activation on unexpected obstacle detection, are required safety features for autonomous stacker operation in shared human-robot warehouse environments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

End User |

Logistics |

38.7% |

2025 |

|

Type |

Electric |

56.8% |

2025 |

|

Region |

South |

36.4% |

2025 |

By End User

Logistics leads with a 38.7% share of the market in 2025, reflecting the structural primacy of e-commerce fulfilment and third-party logistics operations as the largest and fastest-growing stacker procurement category. Major logistics operators and 3PL providers collectively represent the highest-concentration stacker procurement customer base in the US market.

To access detailed market analysis, Request Sample

Retail and wholesale at 24.5% share (2025) encompasses grocery distribution center operations, retail back-of-store stacker requirements for pallet handling, and wholesale club warehouse operations. Food and beverages at 15.8% represents food manufacturing and cold chain distribution requiring electric stackers with food-grade materials and IP-rated specifications for wash-down environments.

By Type

Electric leads with a 56.8% share in 2025, reflecting the structural transition of the US stacker market from manual and IC power toward battery electric operation that has accelerated significantly through 2020–2025. Electric walkie stackers dominate new stacker sales in the logistics and retail segments, where indoor operation requirements, OSHA air quality compliance, and total cost of ownership economics collectively mandate electric over alternative power sources.

Manual/Hydraulic at 26.4% share (2025) serves light-duty, low-intensity applications where electric investment cannot be justified by usage volume, including small retail back rooms, light manufacturing, and low-frequency warehouse operations. Semi-electric at 16.8% provides a cost-effective intermediate option with electric lift and manual traction that serves medium-duty applications where battery traction system cost cannot be justified, but manual lifting is unacceptable for ergonomic or safety reasons.

Regional Market Insights

The South’s dominant position (36.4%, 2025) reflects the region’s structural role as the primary US logistics and fulfilment center development zone, driven by the combination of large available land parcels at competitive prices, favorable logistics geography connecting Southern manufacturing with Eastern US consumption markets, and lower labor costs relative to Northeast and West Coast markets.

The Midwest at 25.2% benefits from its established manufacturing and industrial base, creating stacker demand in automotive, steel, and consumer goods distribution, combined with its central logistics geography, making it a preferred location for national distribution centers serving cross-country freight networks.

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

36.4% |

Strong food and beverage manufacturing and distribution infrastructure, major automobile manufacturing and parts distribution, and rapidly growing e-commerce warehouse construction activity |

|

Midwest |

25.2% |

Strong automotive manufacturing base creating stacker demand for parts and assembly logistics, large retail distribution center networks in the Chicago corridor, and growing e-commerce fulfilment infrastructure |

|

West |

22.1% |

California’s large logistics and warehousing sector serving Asia-Pacific import activity, strong technology company warehouse and distribution operations, and growing cold chain and food distribution stacker demand |

|

Northeast |

16.3% |

Dense urban logistics and last-mile delivery warehouse demand for compact electric stackers, concentrated retail and wholesale distribution infrastructure, and pharmaceutical and healthcare product warehousing stacker requirements |

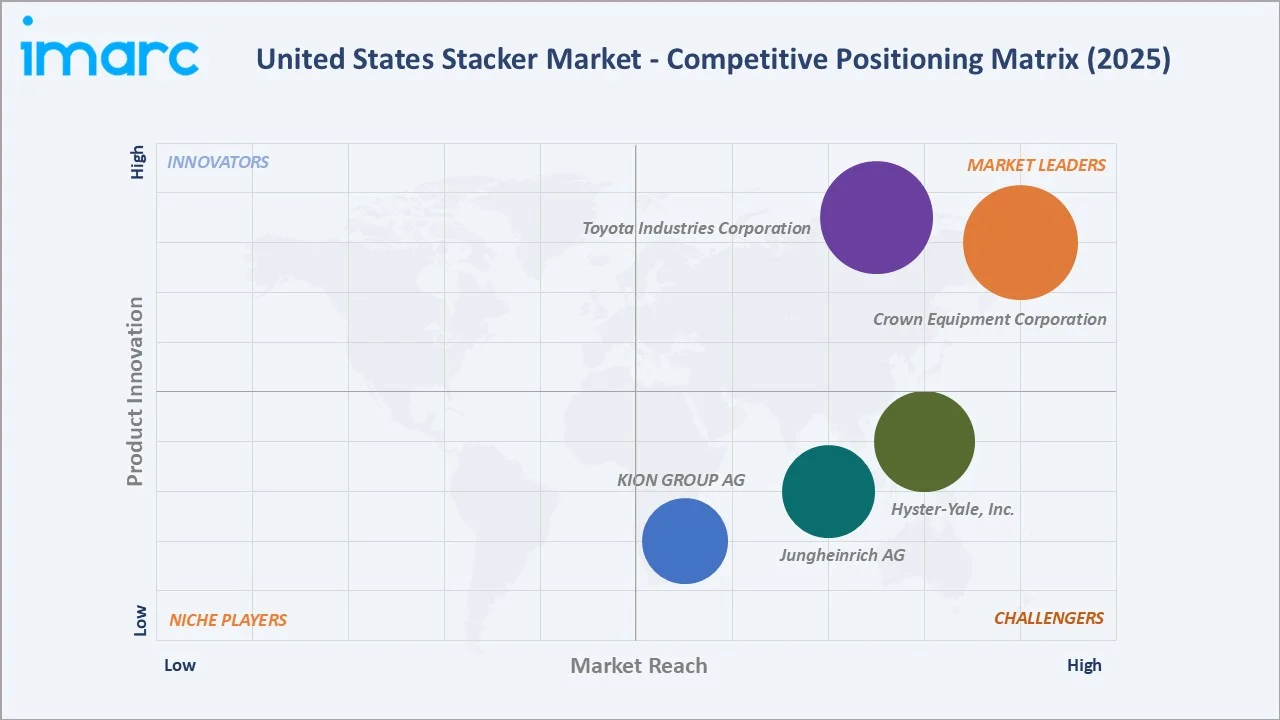

Competitive Landscape

The United States stacker market is moderately concentrated among global material handling equipment leaders with the broadest domestic dealer networks and deepest US customer relationships.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Crown Equipment Corporation |

M Series, ES Series, ST/SX Series, SHC Series, SH Series, SHR Series |

Market Leader |

Broad electric stacker portfolio; strong dealer network; advanced fleet management technology integration |

|

Toyota Industries Corporation |

6210 Walkie Straddle Stacker, 6310 Walkie Straddle Stacker, 6410 Walkie Reach Stacker, 6510 Walkie Counterbalanced Stacker, 8530 Rider Stacker |

Market Leader |

Courier Automated Stacker leader; iWAREHOUSE fleet management; strong US warehouse and logistics customer base |

|

Hyster-Yale, Inc. |

Walkie High Lift Stacker, Compact Electric Stacker, Platform High Lift Stacker, Walkie Counterbalanced Stacker, Counterbalanced Stacker |

Strong Challenger |

Broad portfolio across manual and electric stacker categories; strong US industrial and logistics dealer network; growing electrification capability |

|

Jungheinrich AG |

EJC M/EMC, EJC/EJD, ERC/ERD, ESC/ESD walkie stackers |

Strong Challenger |

European market leader with growing US presence; advanced lithium-ion stacker portfolio; IoT-integrated fleet management capability |

|

KION GROUP AG |

Linde L-series walkie and rider stackers |

Challenger |

Premium engineering quality; strong ergonomics and operator safety reputation; growing US market penetration through authorized dealer network |

The competitive landscape is evolving as automation capability becomes an increasingly important differentiator alongside traditional product quality, safety, and service network considerations. Furthermore, the transition to lithium-ion battery technology is creating a secondary competitive axis, while some Chinese manufacturers still offer predominantly lead-acid battery systems in their US market entry price points.

Key Company Profiles

Crown Equipment Corporation

Crown Equipment Corporation is one of the world’s largest electric forklift and walkie stacker manufacturers. The company’s vertically integrated manufacturing model provides product quality control and supply chain advantages that differentiate it from competitors relying on third-party component supply.

- Product Portfolio: M Series Walkie Stacker, ES Series Fork Over Pallet Stacker, ST/SX Series Pallet Stacker, SHC Series Heavy-Duty Walkie Counterbalance Stacker, SH Series Heavy-Duty Walkie Straddle Stacker, and SHR Series Heavy-Duty Walkie Reach Stacker.

- Strategic Focus: Electric stacker electrification leadership; lithium-ion battery system integration; automation and AGV platform development; InfoLink fleet management platform scale; US dealer network depth and service capability.

Toyota Industries Corporation

Toyota Industries Corporation’s subsidiary, The Raymond Corporation, is one of the leading US electric stacker and forklift manufacturers, with particular strength in warehouse automation and fleet management technology.

- Product Portfolio: 6210 Walkie Straddle Stacker, 6310 Walkie Straddle Stacker, 6410 Walkie Reach Stacker, 6510 Walkie Counterbalanced Stacker, and 8530 Rider Stacker.

- Recent Developments: In September 2025, The Raymond Corporation expanded its Raymond Basics lineup with the Raymond RBS26-F Stacker, a lithium-ion-powered forklift stacker designed for handling skids, crates, containers, and platforms without bottom boards.

- Strategic Focus: Automated stacker and warehouse AGV leadership; iWAREHOUSE connected fleet intelligence platform; lithium-ion product line expansion; Toyota-backed engineering excellence and manufacturing quality positioning.

Market Concentration Analysis

The US stacker market exhibits moderate concentration, with approximately 35–45% controlled by the dominant domestic manufacturers with the deepest dealer and service networks. Chinese manufacturers are growing from a small base toward a meaningful 10–15% share as their US distribution networks mature and product quality credentials improve.

The market’s concentration is reinforced by the importance of after-sales service and operator training in the stacker buying decision, which favors established OEMs with dense US dealer and service center networks over new entrants or importers without local service capability. The automation technology differentiation is creating a premium market segment where competitive concentration is even higher, as Chinese manufacturers do not yet offer commercial automated stacker products in the US market.

Investment & Growth Opportunities

Fastest Growing Segments

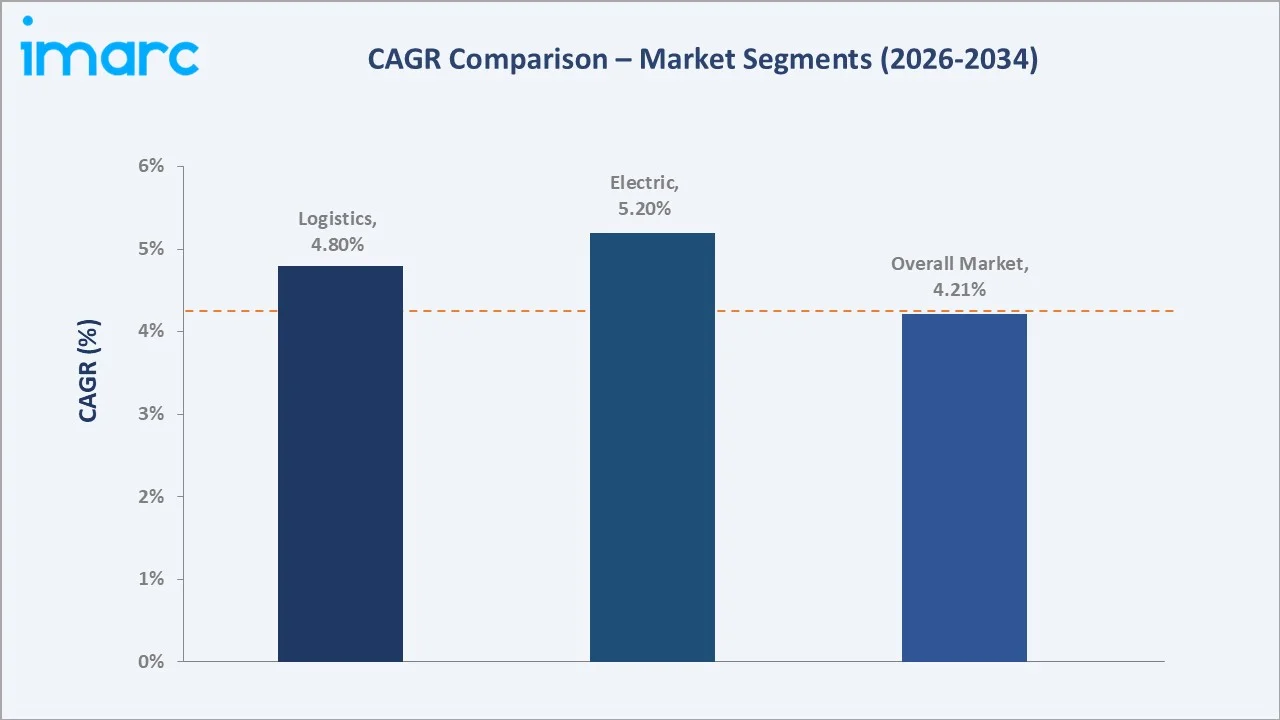

Electric stackers (~5.2% CAGR), automated and semi-autonomous stacker systems (~10–15% annual growth), cold chain and food distribution electric stackers, and lithium-ion retrofit and fleet upgrade programs represent the highest-growth investment vectors within the US stacker market through 2034. The logistics end-user segment at ~4.8% CAGR is outpacing overall market growth, driven by sustained e-commerce fulfilment center construction.

Emerging Trends

Several structural trends are creating investment opportunities in the US stacker market through 2034. Collaborative mobile robot (CMR) integration with electric stacker fleets is creating a new category of human-robot collaborative warehouse systems. Subscription and lease-to-own stacker financing models are expanding the addressable market for electric stackers among small and medium warehouse operators who cannot justify large upfront capital expenditure, with manufacturers and dealers developing monthly fee fleet access programs that include maintenance and technology upgrades.

Technology Investment Trends

- Lithium-ion battery system development for cold storage-optimized stacker applications is attracting OEM and battery supplier investment, as the standard lithium-ion battery chemistry’s temperature performance degradation below 0°C creates a specific product development requirement for cold chain stacker applications that command premium pricing.

- IoT fleet management platform development and customer data monetization are attracting software investment from major stacker OEMs, with fleet management platforms evolving from hardware-bundled features to standalone subscription software services that generate recurring revenue independent of equipment replacement cycles.

Future Market Outlook (2026-2034)

The United States stacker market is positioned for sustained growth through 2034. From USD 487.6 Million in 2025, the market is projected to reach USD 714.9 Million by 2034, representing total incremental value creation of USD 227.3 Million at a CAGR of 4.21%.

This growth is underpinned by the e-commerce-driven warehouse expansion that shows no sign of reversal as US online retail penetration continues to grow toward 25–30% of total retail by 2034, the electric stacker transition creating a sustained fleet replacement cycle as aging lead-acid battery units are retired, and the automation upgrade cycle as logistics operators invest in automated stacker systems to manage labor cost pressures.

The competitive landscape will continue evolving as Chinese manufacturers establish stronger US market positions through improved product quality, expanded dealer networks, and competitive pricing that creates sustained pressure on mid-range electric stacker pricing for established US and European brands. Automation technology differentiation will become an increasingly important competitive dimension that maintains premium pricing for technology-leading brands against lower-cost Chinese competition in standard electric stacker categories.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 55 industry participants in 2024–2025, including stacker manufacturer sales executives, US warehouse and logistics operations managers, material handling equipment distributors, fleet management technology specialists, OSHA compliance consultants, and battery technology providers. Expert input validated market sizing, segment growth rates, and regional demand estimates.

Secondary Research

Secondary research encompassed stacker manufacturer annual reports and investor presentations, Industrial Truck Association (ITA) US shipment data, Material Handling Industry (MHI) market statistics, CBRE US industrial real estate market reports, US Census Bureau e-commerce retail sales data, Department of Labor warehouse employment statistics, and industry publications including Modern Materials Handling, Material Handling & Logistics, DC Velocity, and Logistics Management.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating US warehouse square footage expansion data, stacker fleet age and replacement cycle analysis, electric stacker market share progression modelling, US e-commerce retail growth projections, and end-user sector capital expenditure trend analysis. The base-case CAGR of 4.21% reflects consensus estimates validated against stacker manufacturer revenue guidance and US industrial and logistics real estate market projections for 2026–2034.

United States Stacker Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Electric, Manual/Hydraulic, Semi-Electric |

| End Users Covered | Retail And Wholesale, Logistics, Automobile, Food and Beverages, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered |

Crown Equipment Corporation, Toyota Industries Corporation, Hyster-Yale, Inc., Jungheinrich AG, KION GROUP AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States stacker market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States stacker market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States stacker industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Stacker Market Report

The United States stacker market reached USD 487.6 Million in 2025 and is projected to reach USD 714.9 Million by 2034.

The market is expected to grow at a CAGR of 4.21% during 2026-2034, driven by e-commerce warehouse expansion, electric stacker adoption acceleration, IoT automation integration, and labor cost reduction and safety compliance demand.

The South leads with a 36.4% share in 2025, driven by the region’s concentration of e-commerce fulfilment centers, food and beverage manufacturing and distribution, automobile parts logistics, and large warehouse and distribution center construction activity in Texas, Florida, Georgia, Tennessee, and the Carolinas.

Logistics leads with a 38.7% share in 2025, reflecting the structural primacy of e-commerce fulfilment and third-party logistics warehouse operations as the largest and fastest-growing stacker procurement category driven by the sustained growth of US online retail.

Electric leads with a 56.8% share in 2025, reflecting the structural transition to battery electric operation driven by OSHA indoor air quality requirements, lower total cost of ownership, corporate sustainability commitments, and the expanded product range of electric stackers now covering applications previously served only by IC models.

Some of the key players include Crown Equipment Corporation, Toyota Industries Corporation, Hyster-Yale, Inc., Jungheinrich AG, and KION GROUP AG.

Key drivers include e-commerce expansion driving warehouse and fulfilment center construction, electric stacker adoption and sustainability push, and labor cost reduction and OSHA safety compliance requirements driving powered stacker investment over manual alternatives.

Key opportunities include automated stacker and AGV system development, lithium-ion battery system integration for cold chain applications, IoT fleet management subscription platform development, and compact urban last-mile delivery stacker solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)