Yacht Charter Market Size, Share, Trends and Forecast by Type, Length, Contract Type, and Region, 2026-2034

Yacht Charter Market Size, Share, Trends & Forecast (2026-2034)

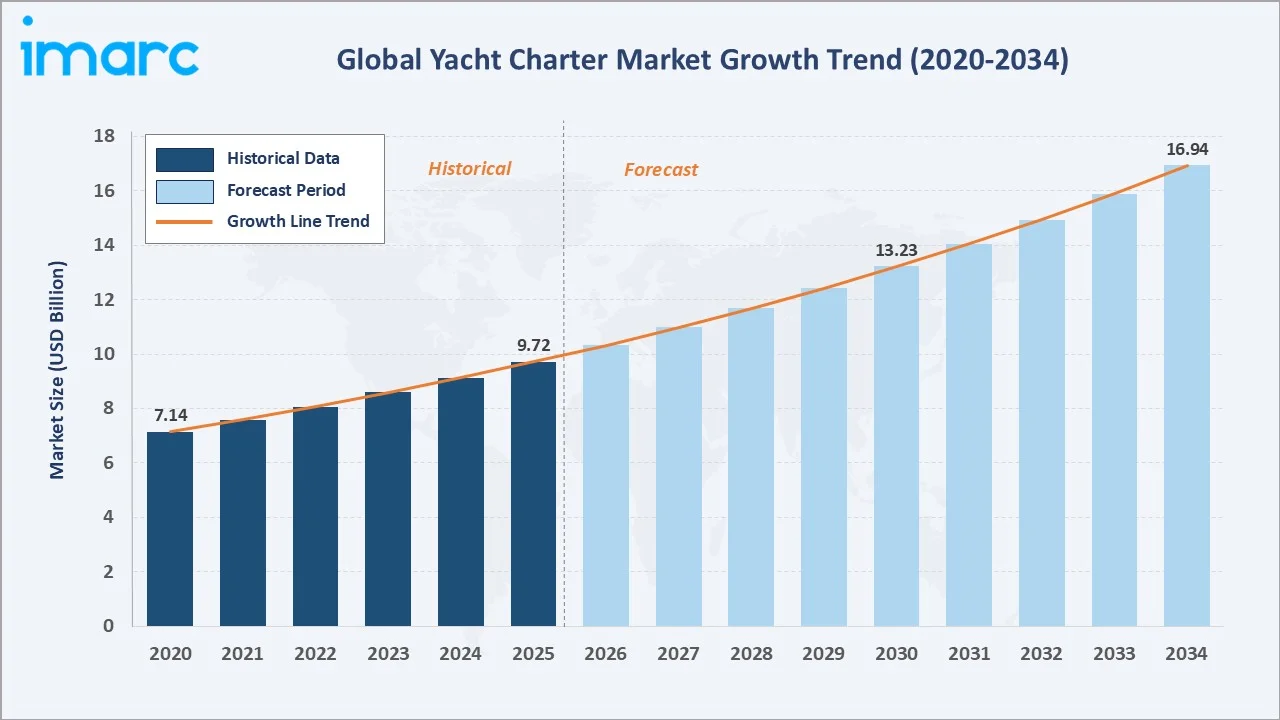

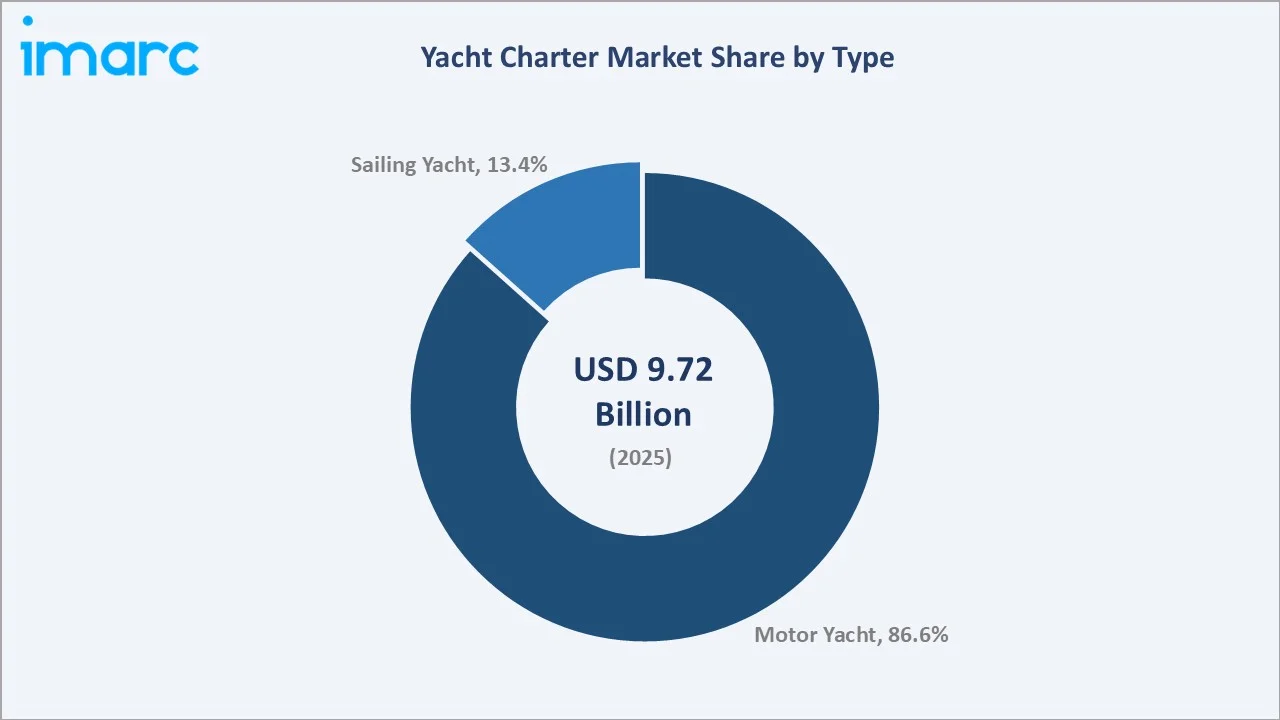

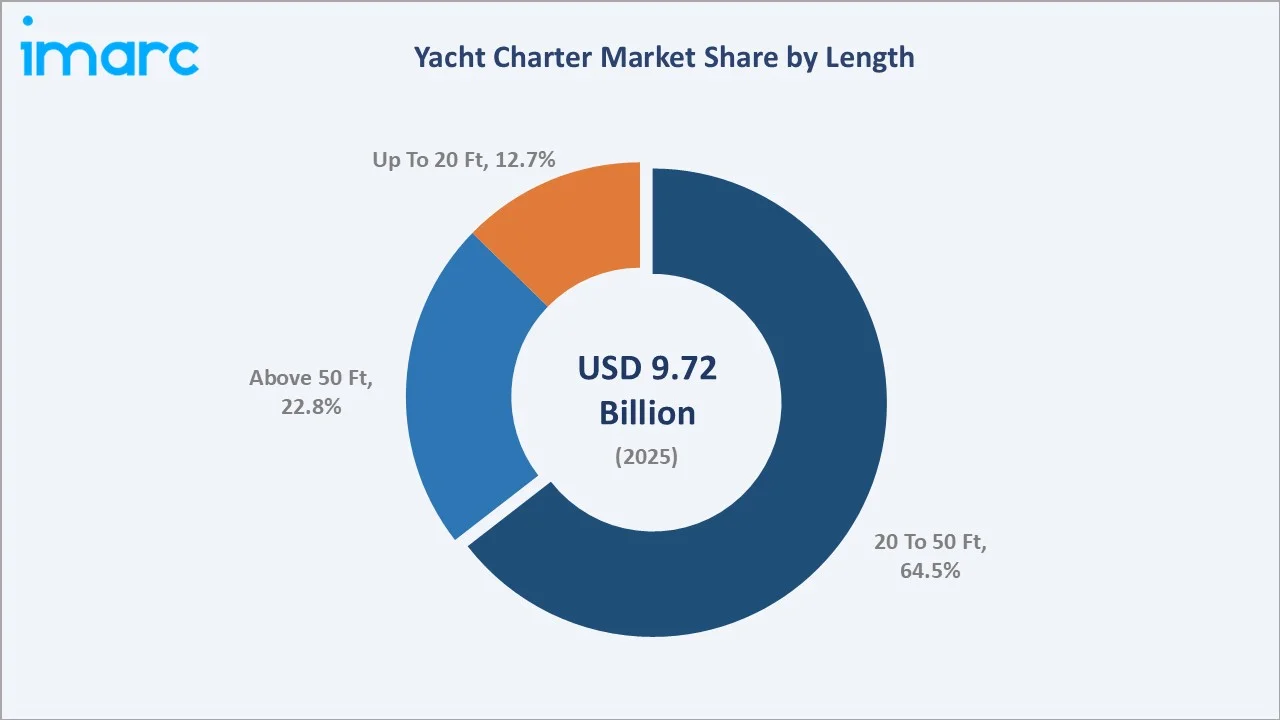

The global yacht charter market size reached USD 9.72 Billion in 2025 and is projected to reach USD 16.94 Billion by 2034, exhibiting a CAGR of 6.36% during 2026-2034. Rising disposable incomes, growing luxury travel demand, and expanding maritime tourism are the primary forces shaping this market.

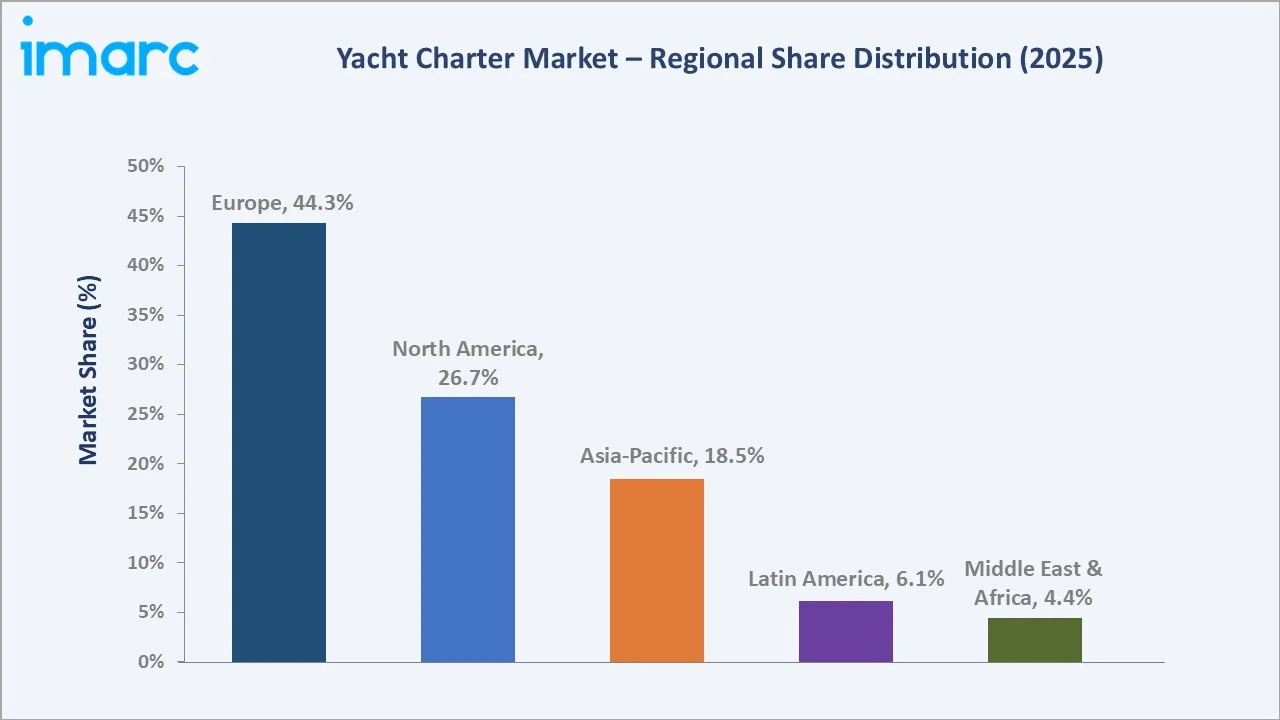

Motor Yacht leads type segmentation at 86.6% in 2025, driven by comfort, speed, and versatility. Europe commands 44.3% regional share, reflecting well-developed maritime infrastructure and iconic Mediterranean charter destinations globally.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.72 Billion |

|

Forecast Market Size (2034) |

USD 16.94 Billion |

|

CAGR (2026-2034) |

6.36% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Type |

Motor Yacht (86.6% share, 2025) |

|

Leading Length Segment |

20 To 50 Ft (64.5% share, 2025) |

|

Leading Region |

Europe (44.3% share, 2025) |

The yacht charter market growth from 2020 through 2034 reflects consistent demand driven by HNWI wealth expansion, digital platform adoption, and fleet modernization. The forecast to USD 16.94 Billion by 2034 captures accelerating superyacht demand and sustainable charter growth globally.

To get more information on this market, Request Sample

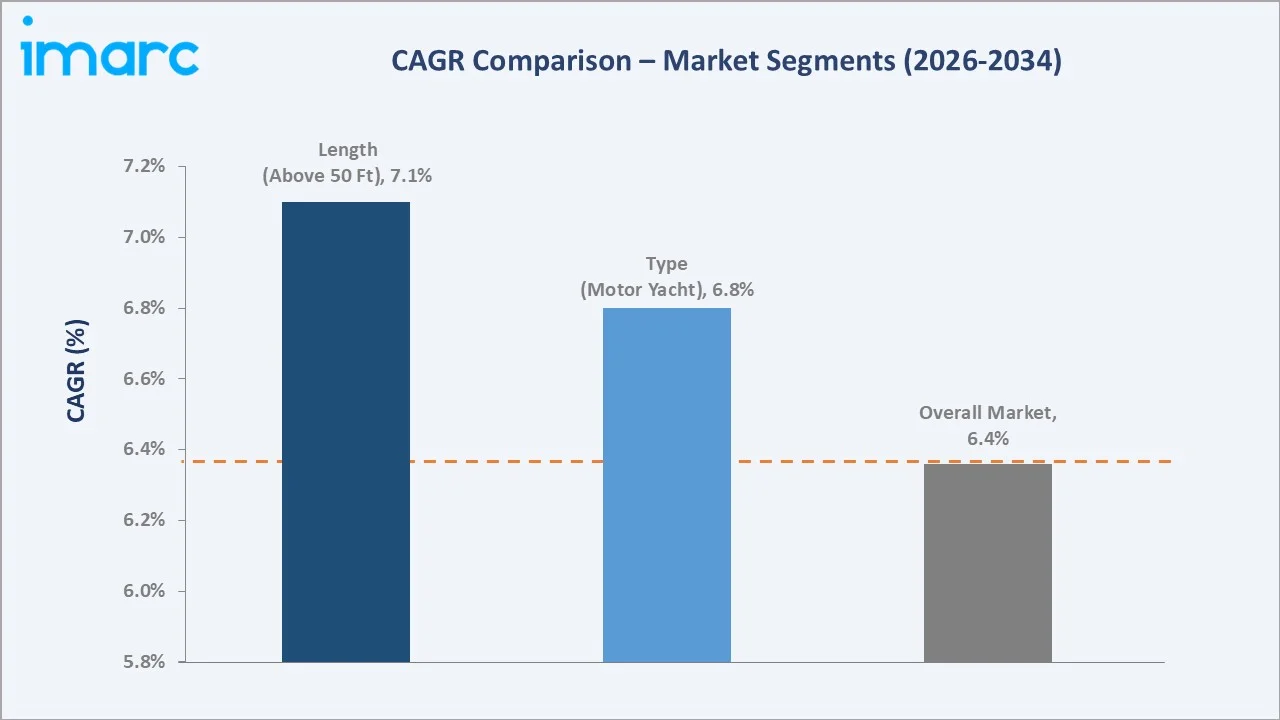

The CAGR trajectories highlight Above 50 Ft at approximately 7.1% CAGR and Motor Yacht at approximately 6.8% CAGR as the fastest-growing categories within the yacht charter market through the 2034 forecast horizon.

Executive Summary

The global yacht charter market is on a sustained growth trajectory from USD 9.72 Billion in 2025 to USD 16.94 Billion by 2034. The sector spans bareboat, crewed, and luxury charters, benefiting from rising affluence and growing premium travel demand globally.

Motor Yacht leads at 86.6% in 2025 owing to versatility across leisure, corporate, and event charters. Sailing Yacht (13.4%) retains dedicated demand among eco-conscious and adventure travelers seeking authentic maritime experiences.

20 To 50 Ft vessels command 64.5% of the length segment in 2025, favored for accessibility and cost-effectiveness. Above 50 Ft (22.8%) serves ultra-luxury demand, while Up To 20 Ft (12.7%) supports day-charter and coastal resort operators globally.

Europe dominates at 44.3% in 2025, supported by Mediterranean routes and strong marina infrastructure. North America follows at 26.7%, driven by Caribbean and US coastal charter demand and growing corporate event bookings.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Motor Yacht – 86.6% share (2025) |

|

Largest Length Segment |

20 To 50 Ft – 64.5% share (2025) |

|

Leading Region |

Europe – 44.3% share (2025) |

|

Second Largest Region |

North America – 26.7% share (2025) |

|

Top Companies |

Camper & Nicholsons, The Moorings, Argo Nautical Limited, IYC, and West Coast Marine Yacht Services Pvt. Ltd. |

Key Analytical Observations Expanding On The Above Data:

- Motor Yacht dominates at 86.6% in 2025 due to superior comfort, speed, and range versatility for diverse charter itineraries. Continued advancement in hybrid propulsion sustains Motor Yacht leadership through 2034.

- 20 To 50 Ft vessels command 64.5% share because they offer broad accessibility, manageable operational costs, and suitability for diverse routes, attracting both first-time charterers and experienced sailors.

- Europe's 44.3% dominance reflects extensive Mediterranean coastlines, year-round charter demand, and concentrated presence of leading operators in Croatia, Greece, and the French Riviera.

- Above 50 Ft superyacht charters, growing at approximately 7.1% CAGR, benefit from rising UHNWI populations, corporate event demand, and expanding fractional ownership and subscription charter models.

Yacht Charter Market Overview

The yacht charter market encompasses short-term rental of motor yachts, sailing yachts, catamarans, and superyachts for leisure, corporate, and event purposes. Operators range from boutique regional fleet owners to global charter brokerages serving HNWI and corporate clientele worldwide.

The ecosystem integrates yacht manufacturers, charter brokerages, marina operators, digital booking platforms, regulatory bodies, and service providers across Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa regions globally.

Market Dynamics

To evaluate market opportunities, Request Sample

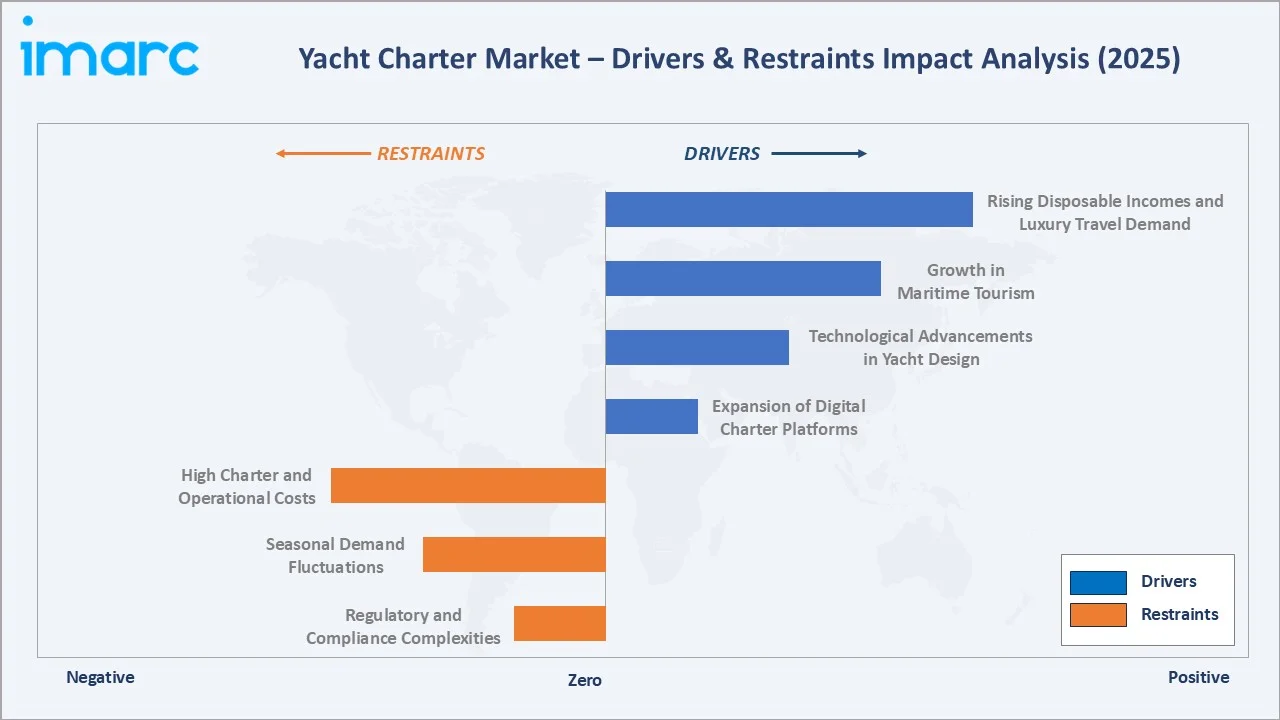

Market Drivers

- Rising Disposable Incomes and Luxury Travel Demand: Increasing global HNWI and UHNWI populations are driving demand for exclusive yacht charter experiences. Luxury travelers seek personalized itineraries, premium crews, and iconic destinations, sustaining strong charter revenue and fleet procurement growth globally.

- Growth in Maritime Tourism: Expanding global tourism infrastructure and rising interest in marine-based leisure are accelerating yacht charter demand. Mediterranean, Caribbean, and Southeast Asian destinations are experiencing record charter bookings driven by growing international tourism flows.

- Technological Advancements in Yacht Design: Innovations in hybrid propulsion, smart navigation, satellite connectivity, and sustainable materials are enhancing yacht performance and appeal. Advanced onboard technology attracts tech-savvy travelers and corporate clients, supporting fleet upgrade cycles and premium pricing.

- Expansion of Digital Charter Platforms: Online booking platforms simplify yacht charter discovery, comparison, and reservation. Digital platforms broaden market access beyond traditional brokerages, enabling real-time availability, transparent pricing, and global reach for charter operators worldwide.

Market Restraints

- High Charter and Operational Costs: Premium yacht charter pricing, crew fees, provisioning, and port charges represent substantial expenditure. High costs limit market access among mid-tier consumers, restricting the broader democratization of yacht charter experiences across developing markets.

- Seasonal Demand Fluctuations: Mediterranean and Northern European markets experience pronounced seasonal peaks, creating revenue concentration risk. Offseason underutilization increases maintenance costs and reduces overall profitability for charter businesses in key destination markets.

- Regulatory and Compliance Complexities: Varying maritime regulations, licensing requirements, and environmental compliance across jurisdictions increase operational complexity. Regulatory fragmentation poses barriers for operators seeking multi-destination or cross-border charter service expansion.

Market Opportunities

- Eco-Friendly and Sustainable Yacht Charters: Growing environmental awareness is driving demand for electric and hybrid charters. Operators investing in sustainable fleets capture premium pricing from eco-conscious travelers and access emission-regulated marina destinations.

- Emerging Market Expansion: Asia-Pacific, Middle East, and Latin America present high-growth opportunities driven by expanding HNWI populations. Government luxury tourism initiatives in these regions create significant new demand frontiers for charter operators.

Market Challenges

- Competition from Alternative Luxury Travel Experiences: Private jet travel, luxury resort experiences, and expedition cruises compete with yacht charters for HNWI budgets. Operators must continuously innovate in itinerary design and onboard amenities to maintain positioning.

- Crew Recruitment and Retention: Qualified maritime professionals are in high demand globally. Skilled crew shortages increase labor costs and affect service quality, posing operational challenges for fleet expansion across global charter markets.

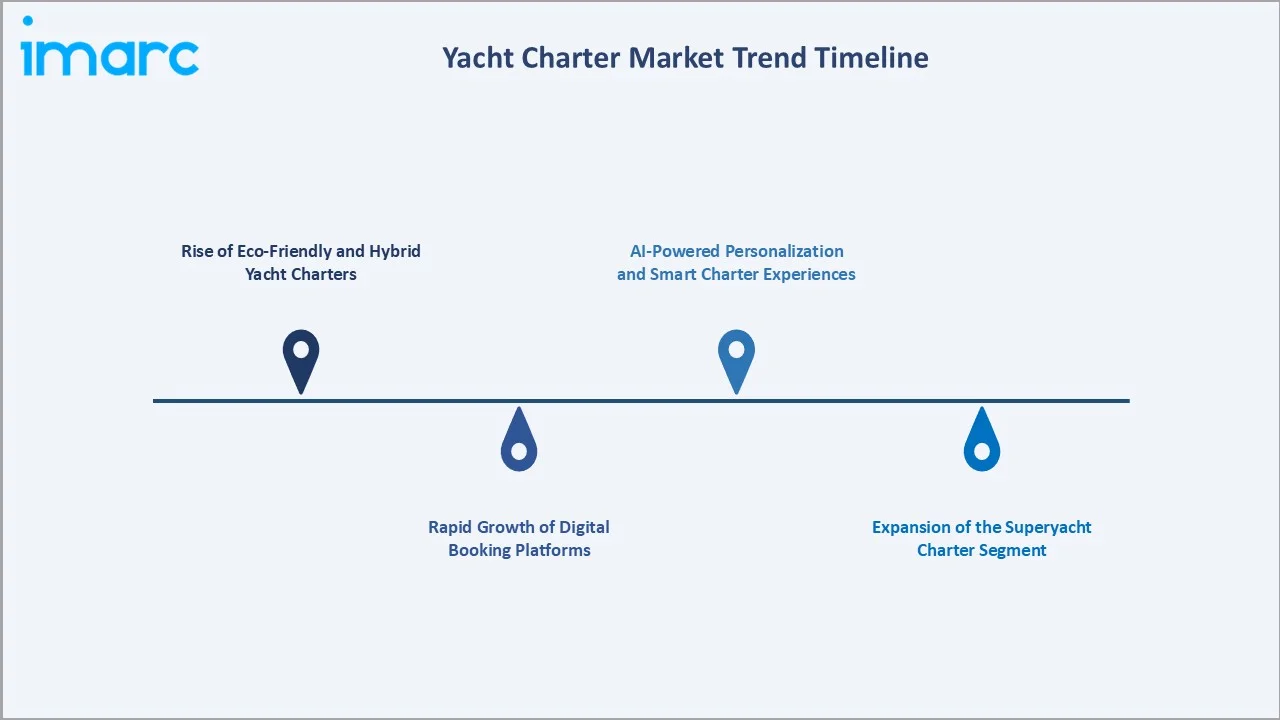

Emerging Market Trends

1. Rise of Eco-Friendly and Hybrid Yacht Charters

Electric and hybrid propulsion systems are gaining traction in the charter market. Sustainable yachts attract eco-conscious charterers and align with tightening marina emission regulations, driving fleet modernization among forward-looking charter operators globally.

2. Rapid Growth of Digital Booking Platforms

Online platforms have transformed yacht charter accessibility, enabling transparent pricing and real-time availability. Digital-first operators capture a growing share, especially among younger HNWI clientele preferring self-service booking experiences.

3. Expansion of the Superyacht Charter Segment

Rising UHNWI wealth and corporate event demand are fueling above-50-ft superyacht charter growth. New builds with advanced onboard amenities are redefining luxury standards and commanding record weekly charter rates across Mediterranean and Caribbean routes.

4. AI-Powered Personalization and Smart Charter Experiences

Artificial intelligence enables hyper-personalized itinerary recommendations, predictive maintenance alerts, and smart onboard automation. AI integration enhances guest experience and operational efficiency, positioning tech-enabled services as the premium offering through 2034.

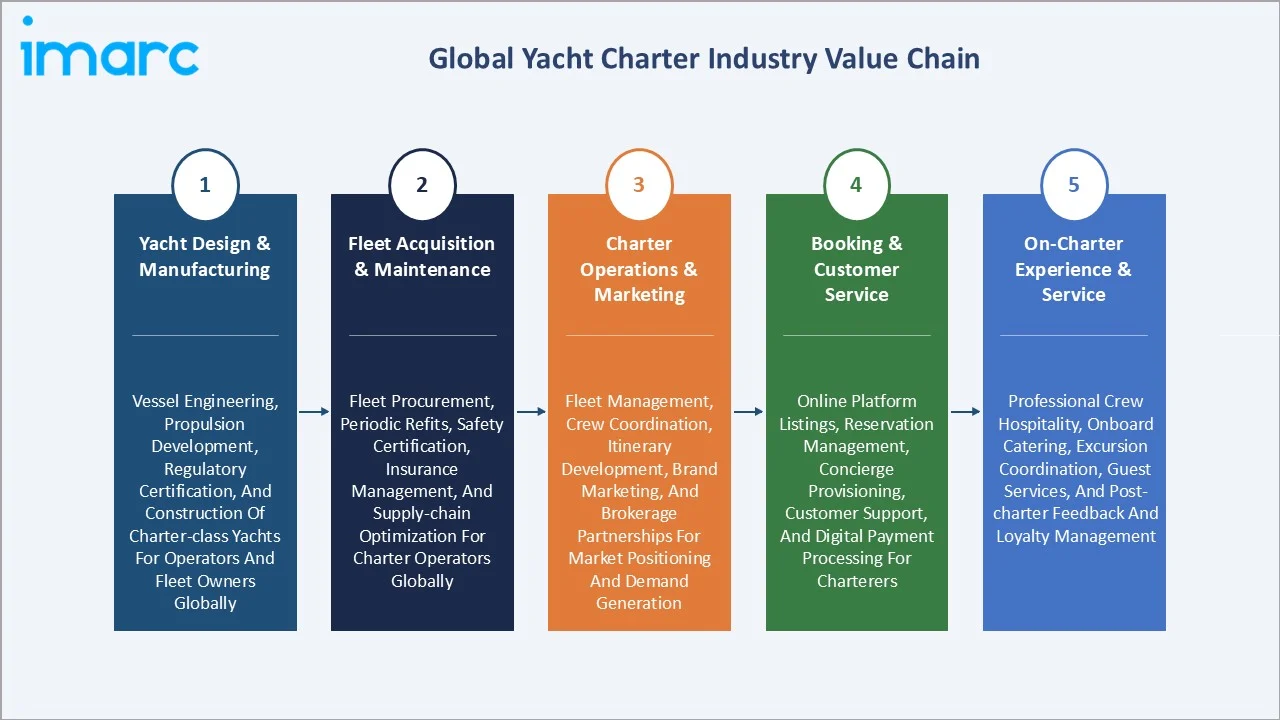

Industry Value Chain Analysis

The yacht charter value chain spans five integrated stages from design through on-charter service. Manufacturing and fleet acquisition capture primary capital value, while charter operations and digital booking platforms generate direct ongoing revenue.

|

Stage |

Key Activities |

|

Yacht Design & Manufacturing |

Vessel engineering, propulsion development, regulatory certification, and construction of charter-class yachts for operators and fleet owners globally |

|

Fleet Acquisition & Maintenance |

Fleet procurement, periodic refits, safety certification, insurance management, and supply-chain optimization for charter operators globally |

|

Charter Operations & Marketing |

Fleet management, crew coordination, itinerary development, brand marketing, and brokerage partnerships for market positioning and demand generation |

|

Booking & Customer Service |

Online platform listings, reservation management, concierge provisioning, customer support, and digital payment processing for charterers |

|

On-Charter Experience & Service |

Professional crew hospitality, onboard catering, excursion coordination, guest services, and post-charter feedback and loyalty management |

Charter operations and digital booking platforms capture the highest direct revenue, representing core competitive differentiation. Post-charter service and crew excellence generate repeat bookings and premium pricing power among loyal HNWI charterer segments.

Technology Landscape in the Yacht Charter Industry

Hybrid and Electric Propulsion Systems

Diesel-electric hybrid and fully electric propulsion technologies are reducing fuel consumption and emissions. Leading manufacturers integrate lithium-ion battery systems and regenerative charging to enhance range and sustainability across luxury charter vessel categories globally.

Smart Navigation and Connectivity

VSAT satellite systems, AI-powered route optimization, and IoT-based vessel monitoring enhance safety and connectivity. Real-time weather routing and remote diagnostics reduce operational risks and improve guest confidence across offshore and bluewater charter itineraries.

AI-Powered Booking and Charter Management Platforms

Machine learning algorithms optimize dynamic pricing, inventory management, and personalized recommendations. Digital platforms leverage behavioral data to match charterers with optimal vessels and itineraries, increasing conversion rates and customer lifetime value globally.

Sustainable Materials and Green Design

Advanced composites, recyclable hull materials, and solar panel integration are reshaping yacht construction. Green design certifications are becoming competitive differentiators, attracting eco-conscious charterers and enabling access to emission-regulated marina destinations.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Segment | Market Share | Year |

|---|---|---|---|

| Type | Motor Yacht | 86.6% | 2025 |

| Length | 20 To 50 Ft | 64.5% | 2025 |

| Contract Type | 🔒 | 🔒 | 2025 |

| Region | Europe | 44.3% | 2025 |

By Type

Motor Yacht commands an 86.6% majority share in 2025 owing to superior speed, comfort, and range versatility. Advanced diesel-electric hybrid models with premium amenities drive replacement demand across global charter fleets through 2034.

To access detailed market analysis, Request Sample

Sailing Yacht (13.4%) retains dedicated demand driven by eco-tourism, adventure travel, and traditional sailing enthusiasts. Racing-style and ocean-crossing sailing yachts serve specialized niche markets, particularly in Northern Europe and Southern Ocean charter circuits.

By Length

20 To 50 Ft vessels dominate at 64.5% in 2025, offering optimal balance of capacity, maneuverability, and cost-effectiveness. This segment attracts families, small groups, and first-time charterers across Mediterranean and Caribbean routes with broad marina availability.

Above 50 Ft superyacht charters (22.8%) serve the ultra-luxury segment, commanding the highest weekly rates. Up To 20 Ft (12.7%) serves day-charter operators at coastal resort destinations and island-hopping circuits globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

44.3% |

Extensive Mediterranean coastlines, well-developed marina infrastructure, iconic sailing routes, and high HNWI concentration in key coastal nations |

|

North America |

26.7% |

Caribbean and US coastal charter demand, strong brokerage network, growing corporate event market, and premium destination infrastructure |

|

Asia-Pacific |

18.5% |

Rapid HNWI growth, expanding marina development, government tourism promotion, and rising luxury travel culture in key regional economies |

|

Latin America |

6.1% |

Growing private charter sector, emerging coastal destination development, and rising inbound luxury tourism across key regional markets |

|

Middle East & Africa |

4.4% |

Luxury tourism investment, marina megaprojects, superyacht charter demand growth, and government-led maritime tourism initiatives |

Europe's 44.3% market dominance in 2025 is driven by the Mediterranean's year-round appeal, iconic charter routes, and established operator ecosystems. Croatia, Greece, and the French Riviera collectively account for the majority of regional charter volume.

North America, at 26.7%, benefits from the Caribbean's year-round charter appeal, strong US coastal demand, and a growing corporate event charter segment. The British Virgin Islands and Florida remain key hubs attracting domestic and international HNWI charterers.

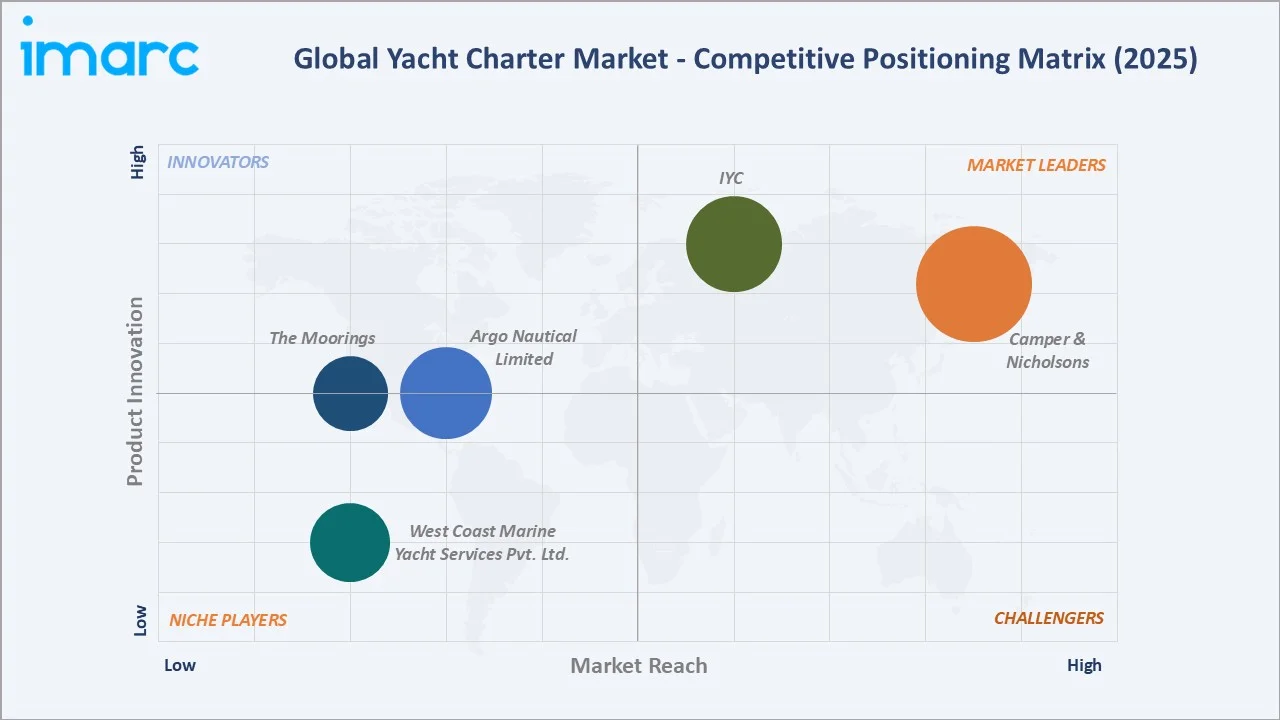

Competitive Landscape

The global yacht charter market is moderately fragmented, with global charter groups and manufacturers competing alongside regional boutique operators. Leading players differentiate through fleet breadth, digital capabilities, destination network, and premium crew service excellence.

|

Company Name |

Key Products / Operations |

Market Position |

Strategic Focus |

|

Camper & Nicholsons |

Project X, Nectar, Alfa G, Illusion V, SuRi, Emocean |

Leader |

Superyacht specialization, global brokerage, premium client relations |

|

The Moorings |

Sail Yacht Charters, Catamaran Charters, Powerboat Charters, Crewed Yacht Charters, By the Cabin Charters |

Established |

Broad destination network, bareboat expertise, digital growth |

|

Argo Nautical Limited |

Greenline Range, Galeon Yachts, Pardo Yachts, Saxdor Range |

Established |

Mediterranean specialization, yacht dealership and brokerage |

|

IYC |

Motor Yachts, Sailing Yachts, Displacement Yachts, Semi Displacement Yachts, Open Yachts, Fishing Yachts, Hybrid Yachts, Classic Yachts |

Leader |

World's largest charter fleet management, digital platform investment, global sales and charter network across Mediterranean and Caribbean |

|

West Coast Marine Yacht Services Pvt. Ltd. |

Ashena, 80 Feet Motor Yacht, 66 Feet Motor Yacht, Gulf Craft 31 WCM Express |

Niche |

Indian coastal market specialization, diversified fleet services, domestic luxury tourism and experiential charter growth |

Key players include Camper & Nicholsons, The Moorings, Argo Nautical Limited, IYC, and West Coast Marine Yacht Services Pvt. Ltd., among others.

Key Company Profiles

Camper & Nicholsons

Camper & Nicholsons is among the oldest and most prestigious superyacht brokerage and management companies globally. It provides bespoke charter, new build, and yacht management services to UHNWI clients across all major maritime regions.

- Product Portfolio: Project X, Nectar, Alfa G, Illusion V, SuRi, Emocean

- Strategic Focus: Camper & Nicholsons International Ltd. strengthens digital charter listing capabilities and expands presence in the Middle East and Asia-Pacific growth markets, with investment in experienced broker talent and exclusive charter fleet relationships globally.

The Moorings

The Moorings is a global leader in both bareboat and crewed yacht charters, operating extensive fleets across the Caribbean, Mediterranean, and South Pacific.

- Product Portfolio: Sail Yacht Charters, Catamaran Charters, Powerboat Charters, Crewed Yacht Charters, By the Cabin Charters

- Recent Developments: In January 2026, The Moorings announced the launch of a yacht charter base in Fethiye, expanding its Mediterranean operations and giving travelers access to Turkey’s scenic Aegean coastline from summer 2026. The Fethiye base will feature a fleet of sailing and power catamarans, including the TM 464PC, aimed at both experienced sailors and leisure travelers seeking comfortable charter experiences.

- Strategic Focus: The Moorings is investing in fleet modernization with fuel-efficient vessels and eco-friendly operations. Expansion of its digital booking platform and loyalty charter program drives repeat bookings and sustained revenue across destination networks.

Market Concentration Analysis

The yacht charter market is moderately fragmented at the global level. Major players, commanding leading positions, though regional operators compete effectively through destination specialization and local fleet expertise.

Geographic concentration favors Europe and North America at the revenue level, while volume growth is increasingly driven by Asia-Pacific and the Middle East expansion. Regulatory complexity creates barriers favoring established operators with existing multi-destination fleet networks.

Investment & Growth Opportunities

Fastest-Growing Segments

Above 50 Ft superyacht charters represent the highest-growth segment at approximately 7.1% CAGR through 2034, capturing investment from rising UHNWI demand and corporate events. Motor Yacht benefits from ongoing hybrid propulsion migration and fleet upgrade cycles.

Emerging Markets

Asia-Pacific and Middle East are key investment frontiers with marina infrastructure programs creating significant new charter demand. Indonesia, Saudi Arabia's Red Sea project, and Thailand represent transformative charter destination expansion opportunities.

Venture & Investment Trends

Investors are targeting digital charter marketplace platforms and eco-yacht startups. Integration of AI personalization, fractional ownership models, and subscription charter services represents an emerging high-value convergence investment theme globally.

Future Market Outlook (2026-2034)

The yacht charter market is forecast to expand from USD 9.72 Billion in 2025 to USD 16.94 Billion by 2034 at a CAGR of 6.36%, driven by rising HNWI wealth, luxury travel demand, and advancement in sustainable yacht technology and digital charter platforms.

Three structural forces will shape the market through 2034: hybrid and electric fleet adoption will drive premium pricing; AI-powered platforms will expand market accessibility; and Asia-Pacific and Middle East infrastructure investment will progressively shift global volume toward high-growth regions.

Research Methodology

Primary Research

Primary research encompassed structured interviews with charter operators, marina directors, yacht brokers, and fleet owners. Primary data validated market sizing, segment shares, regional estimates, and technology adoption trends across key geographies.

Secondary Research

Key secondary sources include maritime regulatory databases, annual reports of leading charter operators and manufacturers, IMO publications, tourism authority data, and industry association reports on luxury travel and yacht market trends globally.

Forecasting Models

Market size estimations used combined top-down and bottom-up models incorporating tourism expenditure data, HNWI wealth projections, fleet utilization rates, and macroeconomic GDP growth scenarios. Base, optimistic, and conservative scenario modelling was applied through the 2034 horizon.

Yacht Charter Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Motor Yacht, Sailing Yacht |

| Lengths Covered | Up To 20 Ft, 20 To 50 Ft, Above 50 Ft |

| Contract Types Covered | Bareboat Charter, Crewed Charter |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Camper & Nicholsons, The Moorings, Argo Nautical Limited, IYC, West Coast Marine Yacht Services Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the yacht charter market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global yacht charter market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the yacht charter industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Yacht Charter Market Report

The global yacht charter market reached USD 9.72 Billion in 2025, reflecting sustained demand driven by rising HNWI wealth, growing maritime tourism, and digital platform adoption enabling broader charter accessibility worldwide.

The market is projected to reach USD 16.94 Billion by 2034, growing at a CAGR of 6.36% during 2026-2034, driven by luxury travel demand, superyacht segment expansion, and emerging market marina infrastructure development.

Motor Yacht leads with an 86.6% market share in 2025, driven by speed, comfort, and versatility. Sailing Yacht follows at 13.4%, serving eco-conscious travelers, adventure tourism, and dedicated sailing enthusiasts globally.

20 To 50 Ft vessels dominate with 64.5% share in 2025 due to broad accessibility and cost-effectiveness. Above 50 Ft holds 22.8%, while Up To 20 Ft accounts for 12.7%, serving day-charter and coastal resort operators.

Europe leads with a 44.3% market share in 2025, supported by Mediterranean charter routes and strong marina infrastructure. North America accounts for 26.7%, Asia-Pacific for 18.5%, Latin America for 6.1%, and the Middle East & Africa for 4.4%.

Above 50ft superyacht charters represent the fastest-growing segment, with an approximate 7.1% CAGR through 2034, driven by UHNWI demand and corporate events. Motor Yacht leads type growth at approximately 6.8% CAGR through 2034.

Leading companies include Camper & Nicholsons, The Moorings, Argo Nautical Limited, IYC, and West Coast Marine Yacht Services Pvt. Ltd, among others.

Key drivers include rising disposable incomes, expanding luxury travel demand, maritime tourism growth, technological advancements in hybrid yacht design, and digital platform expansion, enabling global charter access for HNWI clientele worldwide.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)