Argentina Construction Market Size, Share, Trends and Forecast by Sector and Region, 2026-2034

Argentina Construction Market Size, Share, Trends & Forecast (2026-2034)

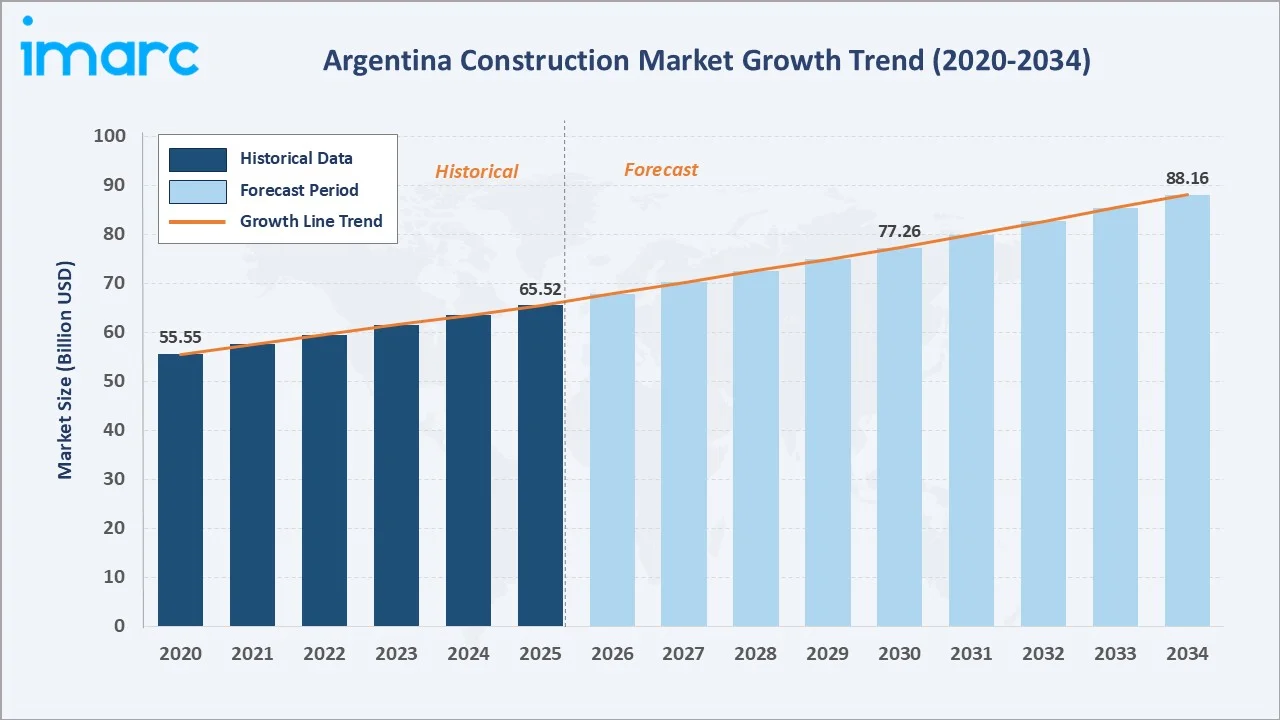

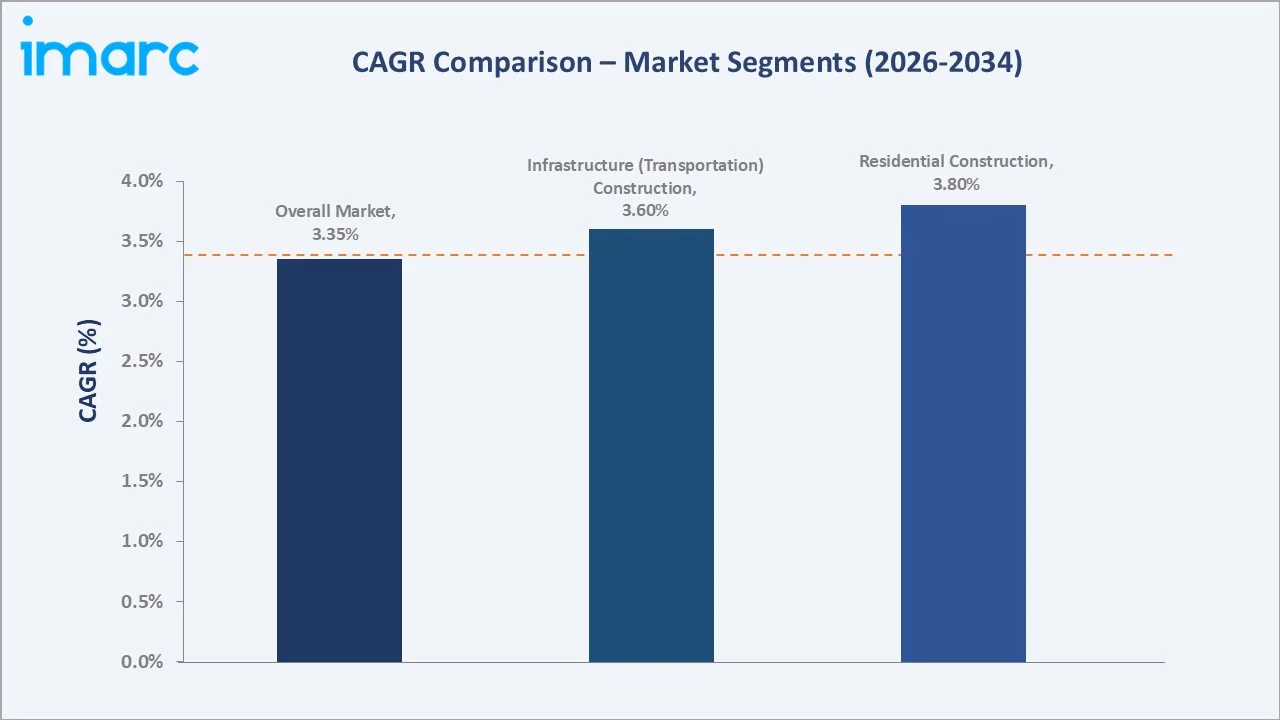

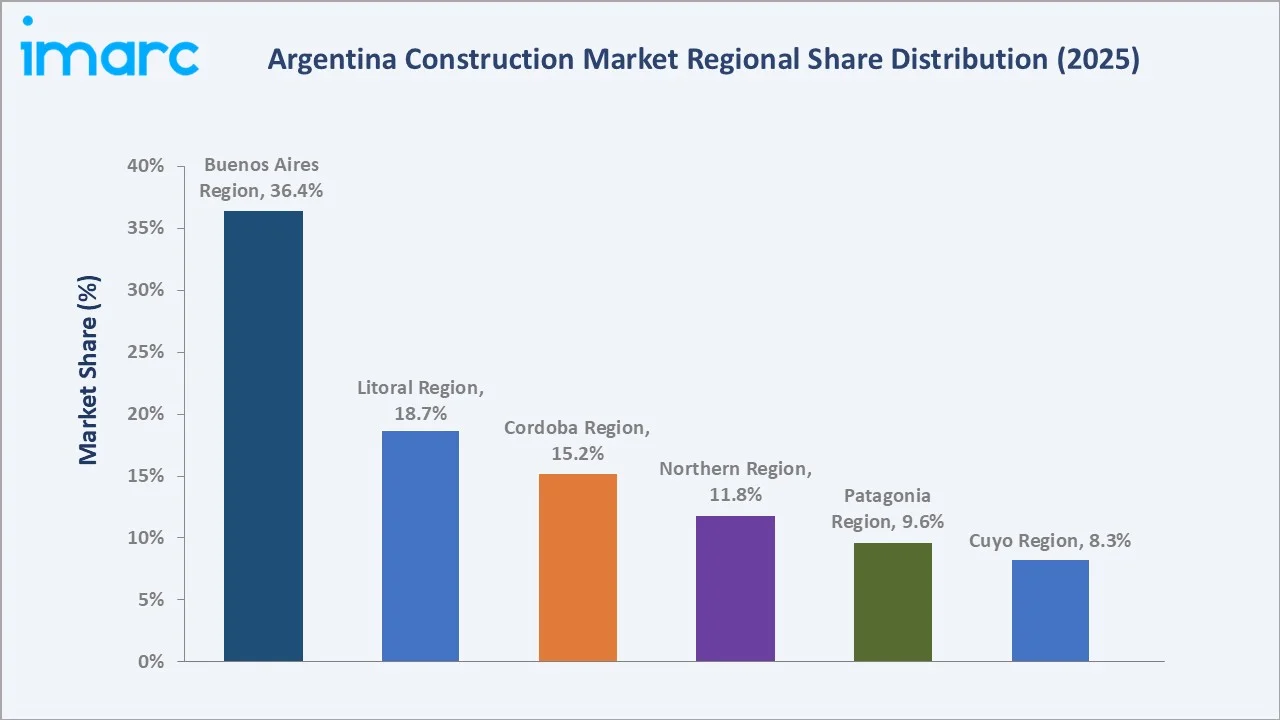

The Argentina construction market reached USD 65.52 Billion in 2025 and is projected to reach USD 88.16 Billion by 2034, growing at a CAGR of 3.35% during 2026-2034. The market is propelled by economic expansion and major infrastructure development, rising urbanization and housing demand, and increasing foreign investment and public-private partnerships (PPPs). Residential Construction dominates at 33.8%. Buenos Aires Region commands 36.4% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 65.52 Billion |

|

Forecast Market Size (2034) |

USD 88.16 Billion |

|

CAGR (2026-2034) |

3.35% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Sector |

Residential Construction (33.8%, 2025) |

|

Second Largest Sector |

Infrastructure (Transportation) Construction (24.6%, 2025) |

|

Leading Region |

Buenos Aires Region (36.4%, 2025) |

The Argentina construction market expanded from USD 55.55 Billion in 2020 to USD 65.52 Billion in 2025, anchored at USD 77.26 Billion in 2030, and forecast to reach USD 88.16 Billion by 2034. Economic recovery, structural infrastructure investments, and sustained housing demand underpin this growth trajectory.

To get more information on this market, Request Sample

Residential Construction grows at ~3.80% CAGR driven by urbanization and government housing programs. Infrastructure (Transportation) Construction grows at ~3.60% CAGR through road, bridge, and airport expansion projects under PPP arrangements.

Executive Summary

The Argentina construction market reached USD 65.52 Billion in 2025, representing one of South America's most dynamic intersections of real estate, infrastructure, and industrial development. The market encompasses residential buildings, commercial structures, transportation infrastructure, energy installations, and industrial facilities.

Residential Construction at 33.8% dominates through sustained housing demand, government subsidy programs, and urban population growth. Infrastructure (Transportation) Construction at 24.6% reflects the government's commitment to roadway expansion, bridge construction, and airport modernization. Buenos Aires Region, at 36.4%, leads through concentration of economic activity, population, and investment.

Key Market Insights

|

Insight |

Data |

|

Dominant Sector |

Residential Construction – 33.8% share (2025) |

|

Second Largest Sector |

Infrastructure (Transportation) Construction – 24.6% share (2025) |

|

Leading Region |

Buenos Aires Region – 36.4% market share |

|

Market Opportunity |

PPP infrastructure; affordable housing; green energy construction; smart cities; industrial parks |

Key Analytical Observations Supporting the Above Data:

- Residential Construction at 33.8%: Residential construction dominates due to rapid urbanization, population growth, and government housing programs. Demand for affordable housing, combined with mortgage subsidy schemes such as Procrear, drives consistent residential investment across major cities.

- Infrastructure (Transportation) Construction at 24.6%: Infrastructure construction leads through government-mandated road, highway, bridge, and airport projects. Multilateral financing from the IDB and World Bank supports major transport corridors and connectivity programs across Argentina.

- Buenos Aires Region at 36.4%: Buenos Aires leads due to its position as Argentina's economic, financial, and population center. The region attracts the majority of real estate investment, commercial development, and infrastructure spending.

Argentina Construction Market Overview

The Argentina construction market encompasses the planning, design, financing, and execution of residential, commercial, industrial, infrastructure, and energy projects across the national territory. The market is shaped by macroeconomic conditions, government investment cycles, foreign direct investment, urbanization trends, and regulatory frameworks.

Macroeconomic factors include GDP growth, currency dynamics, inflation rates, interest rates, and government fiscal policy. In addition, demographic growth, urbanization trends, and government infrastructure programs are accelerating construction activity across Argentina's regions.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

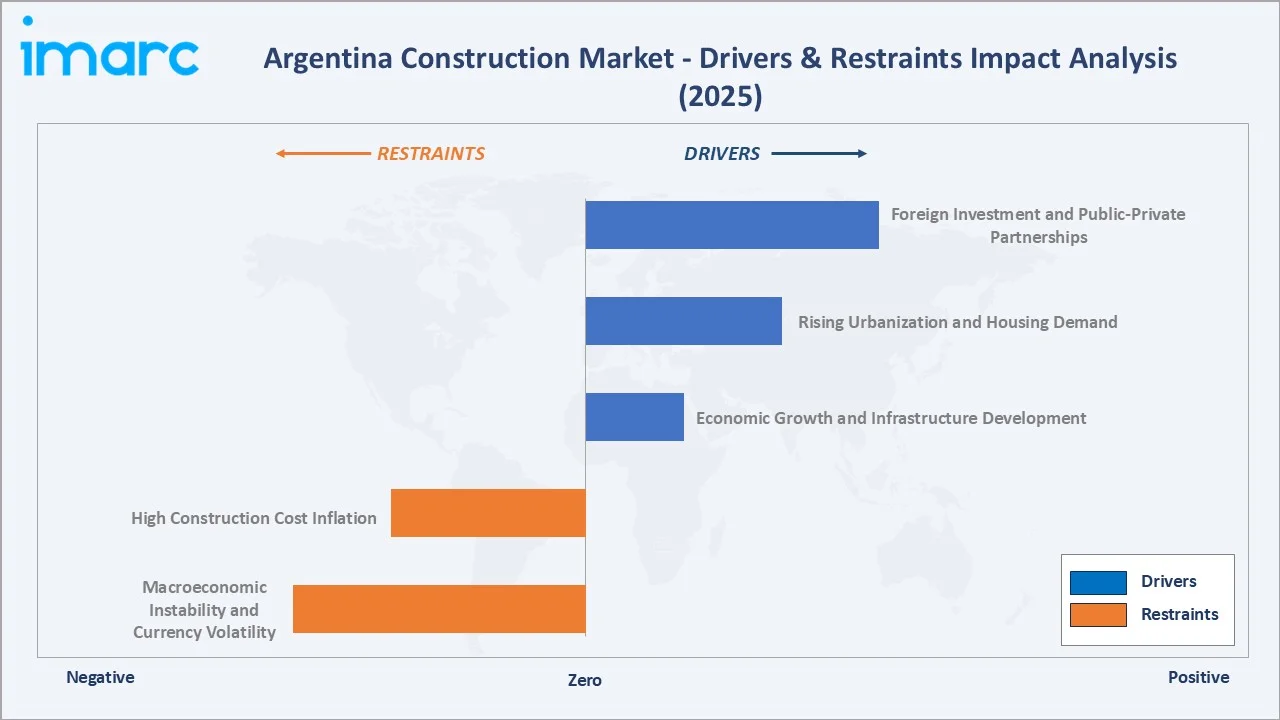

- Economic Growth and Infrastructure Development: Argentina's economic expansion and major infrastructure programs are primary growth catalysts. Government investments in road networks, energy installations, and airport expansions, along with favorable GDP growth projections, are creating sustained construction demand and encouraging private sector participation through PPP frameworks and public works contracts.

- Rising Urbanization and Housing Demand: Argentina's urbanization rate exceeding 92% of its population drives continuous residential construction activity. Urban expansion in Buenos Aires, Córdoba, and Rosario creates demand for housing developments, commercial spaces, and supporting urban infrastructure. Government mortgage subsidy programs directly stimulate affordable residential construction and private real estate investment.

- Foreign Investment and Public-Private Partnerships: Rising foreign direct investment and PPP frameworks are unlocking large-scale infrastructure and industrial construction projects. Multilateral financing from the IDB and World Bank, including major credit facilities for transport infrastructure, mobilizes private capital and construction expertise for national priority projects.

- Government Housing Initiatives and Subsidy Programs: Government-backed housing initiatives and subsidy programs are expanding residential construction volume. Procrear mortgage programs provide financing for affordable housing, while public housing schemes directly fund residential construction. The energy sector boom from Vaca Muerta is additionally driving industrial and utility construction across multiple regions.

Market Restraints

- Macroeconomic Instability and Currency Volatility: Argentina's history of inflation, currency devaluation, and economic instability creates significant uncertainty for construction investment planning. High inflation rates increase building material costs and complicate project budgeting, while currency restrictions make imported construction materials and equipment more expensive for developers.

- High Construction Cost Inflation: Persistent inflation elevates the cost of cement, steel, labor, and construction services. Construction cost indexation mechanisms complicate long-term project financing and profitability calculations. Budget overruns and delayed project completion are common consequences of cost volatility in the Argentine construction environment.

- Regulatory and Permitting Delays: Complex regulatory environments and permitting processes slow project initiation and execution. Bureaucratic inefficiencies at municipal and provincial levels create timeline uncertainty for developers and increase pre-construction costs, reducing overall investment attractiveness for domestic and international construction firms.

Market Opportunities

- PPP Infrastructure Expansion: Growing government reliance on PPP models creates significant construction opportunities for qualified firms. Transport, energy, and social infrastructure projects structured as public-private concessions represent a multi-billion dollar construction pipeline through 2034, offering stable revenue streams backed by government guarantees.

- Green and Sustainable Construction: Rising demand for energy-efficient and environmentally sustainable buildings is creating a premium construction segment. Green building certification, solar energy integration, and water-efficient systems are increasingly demanded by corporate tenants, government agencies, and buyers across commercial and residential segments.

Market Challenges

- Financing Constraints and Interest Rate Volatility: High domestic interest rates and limited long-term mortgage availability constrain residential construction demand and buyer purchasing power. Project financing for commercial and industrial developments faces similar constraints, limiting the scale and pace of private construction investment across market segments.

- Supply Chain and Material Cost Volatility: Reliance on imported construction materials and equipment exposes developers to global commodity price fluctuations and currency-driven cost increases. Supply chain disruptions can delay project timelines and escalate construction costs beyond initial budget estimates, reducing profitability for developers.

Emerging Market Trends

1. PPP Infrastructure Model Driving Large-Scale Transportation Construction

Public-private partnerships are accelerating Argentina's transportation infrastructure construction through a financing model combining government guarantees with private sector execution. Road network expansion, bridge construction, and airport modernization projects across multiple provinces are structured as PPP concessions, attracting domestic and international construction firms alongside multilateral financing.

2. Vaca Muerta Energy Boom Creating Industrial and Energy Construction Wave

The Vaca Muerta shale formation's development is generating unprecedented demand for industrial and energy construction. Pipeline networks, processing facilities, and worker camp infrastructure are being built at scale across Patagonia. This energy construction wave is expected to sustain above-average growth in the Energy and Utility Construction segment through 2034.

3. Affordable Housing Programs Driving Residential Construction Scale

Government-backed affordable housing initiatives including Procrear and social housing programs continue to drive residential construction volume. These programs provide mortgage subsidies, construction financing, and direct public investment in housing development across Argentina's major urban centers, ensuring residential construction remains the dominant market segment.

4. Green Building and Sustainable Construction Gaining Commercial Adoption

Corporate occupiers, government agencies, and institutional investors are increasingly demanding, green-certified buildings with energy efficiency features. LEED certification, solar panel integration, and sustainable material sourcing are becoming differentiating features in commercial real estate development, creating a premium construction sub-segment growing at above-market rates.

Industry Value Chain Analysis

The Argentina construction value chain integrates site selection and structural planning, raw material sourcing and supply, construction and project execution, systems installation and finishing, handover and occupancy, and ongoing operations and maintenance support.

|

Stage |

Key Participants |

|

Site Selection & Structural Design |

Greenhouse site assessment firms, engineering consultants, structural design and planning service providers |

|

Raw Materials & Supply |

Cement manufacturers, steel producers, aggregates suppliers, timber and glass material providers |

|

Construction & Execution |

Civil engineering and general contracting firms, specialized subcontractors, project management companies |

|

Systems & Finishing Installation |

MEP contractors, electrical system providers, plumbing and HVAC suppliers, interior finishing companies |

|

Handover, Packing & Occupancy |

Real estate agencies, property management companies, government housing allocation agencies |

|

Distribution & Operations & Maintenance |

Facility management companies, maintenance contractors, renovation and building upgrade service providers |

The construction and execution stage is the value chain's most capital-intensive and commercially differentiated phase. Large integrated contractors with nationwide execution capabilities hold structural advantages through scale, access to financing, and established government and developer client relationships across all construction segments.

Technology Landscape in the Argentina Construction Industry

Building Information Modeling (BIM) Technology Adoption

Building Information Modeling (BIM) technology is increasingly adopted by Argentina's leading construction firms for project design, coordination, and lifecycle management. BIM enables digital construction simulation, clash detection, and cost optimization. Major infrastructure and commercial projects are mandating BIM compliance, driving digital construction capability investment among top-tier contractors.

Prefabrication and Industrialized Construction Systems

Prefabricated concrete systems, modular construction components, and industrialized building systems are gaining adoption across residential and commercial segments. Holcim's April 2024 acquisition of Tensolite, a pre-cast concrete systems manufacturer with operations in Argentina, Paraguay, and Uruguay, reflects the growing commercial importance of industrialized construction solutions in the region.

Renewable Energy Integration in Construction

Solar panel installation, energy-efficient HVAC systems, and green roofing technologies are being integrated into new construction projects. Government renewable energy targets and corporate sustainability commitments are accelerating adoption of low-carbon construction technologies, creating new technical competency requirements for Argentina's construction workforce and material supply chain.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Market Share |

|

Sector |

Residential Construction |

33.8% |

2025 |

|

Region |

Buenos Aires Region |

36.4% |

2025 |

By Sector

Residential Construction leads at 33.8% (2025). The residential segment encompasses affordable housing developments, mid-market apartment buildings, premium residential towers, and social housing programs. Government subsidy schemes and mortgage financing programs sustain high residential construction volumes across Argentina's major urban centers including Buenos Aires, Córdoba, and Rosario.

To access detailed market analysis, Request Sample

Infrastructure (Transportation) Construction at 24.6% encompasses road and highway construction, bridge and tunnel projects, airport expansion, port infrastructure, and urban transit systems. Government capital expenditure on transport connectivity and multilateral financing sustain this segment's strong position. Commercial Construction at 17.5% includes office buildings, retail centers, hotels, and mixed-use developments concentrated in Buenos Aires and provincial capitals.

Regional Market Insights

|

Region |

Share (2025) |

Key Argentina Construction Market Drivers & Characteristics |

|

Buenos Aires Region |

36.4% |

Driven by concentration of economic activity, corporate investment, residential demand, and government infrastructure spending in the national capital and surrounding metropolitan area. |

|

Litoral Region |

18.7% |

Driven by agricultural processing infrastructure, residential construction in Rosario, Santa Fe, and Entre Ríos, and expanding industrial facilities along the Paraná River corridor. |

|

Cordoba Region |

15.2% |

Driven by Córdoba's status as Argentina's second largest city, strong automotive and manufacturing sector construction, and sustained residential and commercial development demand. |

|

Northern Region |

11.8% |

Driven by government social infrastructure investment, energy sector construction in Jujuy and Salta, and residential development in provincial capitals including Tucumán. |

|

Patagonia Region |

9.6% |

Driven by Vaca Muerta energy sector construction, oil and gas pipeline infrastructure, renewable energy projects, and tourism-related commercial and hospitality construction. |

|

Cuyo Region |

8.3% |

Driven by mining sector infrastructure, renewable energy construction in San Juan, agricultural processing facilities, and residential development in Mendoza. |

Buenos Aires Region's 36.4% market leadership reflects Argentina's economic concentration in its capital metropolitan area. Litoral Region's 18.7% captures the industrial and agricultural infrastructure of Argentina's productive heartland. Patagonia Region's 9.6% is expected to grow above average through 2034 driven by the Vaca Muerta energy construction wave.

Competitive Landscape

The Argentina construction market competitive landscape encompasses distinct tiers: large integrated construction groups, specialized civil engineering firms, building materials manufacturers, and international construction joint ventures active in major infrastructure and energy projects.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Techint Group |

EPC contracts, industrial plant construction, oil and gas |

Market Leader |

Techint plays a central role in Argentina's construction market through EPC contracts for energy, oil and gas, petrochemical, and industrial infrastructure projects locally and internationally. |

|

Holcim |

Cement, aggregates, ready-mix concrete |

Established Player |

Holcim plays a central role in the construction market by providing cement, concrete, and pre-cast systems, strengthening its position through the 2024 Tensolite acquisition. |

|

Loma Negra |

Cement, concrete, lime |

Established Player |

Loma Negra plays a central role in Argentina's construction supply chain as the leading cement manufacturer, serving all construction segments with a nationwide distribution network. |

Market concentration is moderate at the civil engineering and infrastructure tier, with three to four large integrated groups competing for major government-awarded contracts. Residential construction is highly fragmented. Materials manufacturing is concentrated, with Loma Negra and Holcim Argentina controlling the majority of cement supply.

Key Company Profiles

Techint Group (Techint Engineering & Construction)

Techint Engineering & Construction is the engineering, procurement, and construction arm of the Techint Group, one of Latin America's largest industrial conglomerates. The company specializes in EPC contracts for oil and gas, petrochemical, industrial, and infrastructure projects across Argentina and internationally.

- Key Services: EPC contracts, industrial plant construction, oil and gas infrastructure, pipeline construction, power generation facilities.

- Recent Developments: In October 2025, Techint Engineering & Construction strengthened its position in the Vaca Muerta shale region through Tecpetrol's Los Toldos II Este project, where it is executing the Central Processing Facility (CPF), crude oil and gas export pipelines, water management systems, and associated infrastructure. The project is expected to double production capacity to 70,000 barrels per day by 2027, reinforcing Argentina's energy export capabilities and industrial infrastructure expansion.

- Strategic Focus: Centered on energy sector construction, industrial EPC projects, and international expansion leveraging Argentina's growing oil and gas production and export capabilities through the forecast period.

Holcim

Holcim provides cement, aggregates, ready-mix concrete, and construction solutions across Argentina. The company strengthened its market position in April 2024 through the acquisition of Tensolite, a pre-cast concrete systems manufacturer.

- Key Services: Cement production, ready-mix concrete, aggregates, pre-cast concrete systems (via Tensolite), construction materials solutions.

- Recent Developments: In March 2025, Holcim Argentina acquired ready-mix concrete producer Horcrisa for approximately US$33 million, further expanding its construction materials and concrete operations in Argentina.

- Strategic Focus: Expanding from materials supply into construction solutions and systems, leveraging the Tensolite acquisition to provide integrated pre-cast concrete construction products across Argentina, Paraguay, and Uruguay.

Market Concentration Analysis

The Argentina construction market is highly fragmented at the residential and small commercial tier, with thousands of local developers and contractors. Large infrastructure and industrial construction is moderately concentrated among five to seven major integrated groups. Market concentration is expected to increase through M&A and PPP qualification requirements favoring large, financially robust construction firms.

Investment & Growth Opportunities

Highest Growth Segments

Energy and Utility Construction (~4.5% CAGR) driven by Vaca Muerta development, Infrastructure (Transportation) Construction (~3.60% CAGR) through PPP programs, affordable Residential Construction (~3.80% CAGR) through government subsidy schemes, and green Commercial Construction (~4.0% CAGR) from sustainable building adoption represent the highest-growth Argentina construction investment vectors through 2034.

Emerging Investment Opportunities

Vaca Muerta energy infrastructure construction represents the largest near-term opportunity for industrial and energy construction specialists. Contractors establishing preferred supplier relationships with Vaca Muerta oil and gas operators are positioned for above-market revenue growth through the energy construction wave projected to peak between 2026 and 2030.

Investment Themes

- PPP infrastructure construction capturing government-guaranteed revenue from transport concessions: Argentina's PPP framework creates construction opportunities where government revenue guarantees reduce commercial risk. Firms qualifying for concession participation and securing road, bridge, or airport concession contracts access stable, long-duration revenue streams with reduced payment risk.

- Affordable housing construction capturing government subsidy program demand across urban centers: Procrear and related programs create predictable residential construction demand backed by public subsidy. Firms building government-approved affordable housing access a demand segment insulated from commercial real estate market cycles, providing stable revenue diversification.

Future Market Outlook (2026-2034)

The Argentina construction market is projected to grow from USD 65.52 Billion in 2025 to USD 88.16 Billion by 2034, delivering a 3.35% CAGR over the forecast period. The market's anchor value of USD 77.26 Billion in 2030 represents an important structural inflection point as energy construction peaks and PPP infrastructure execution accelerates.

Three structural forces define Argentina construction market growth through 2034. Vaca Muerta energy sector construction creates a decade-long investment wave in Patagonia and connecting infrastructure. Government PPP infrastructure programs provide a structured pipeline of transport and social infrastructure demand independent of economic cycles. Urbanization and population growth create persistent residential construction demand sustaining the market's largest segment.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025) including construction company CEOs, Infrastructure Project Directors, Government Procurement Officers, Real Estate Development Directors, and regional construction market specialists across Argentina's major provinces.

Secondary Research

Secondary research encompassed Argentine Chamber of Construction (CAMARCO) data, INDEC construction activity statistics, World Bank and IDB project financing documentation, corporate annual reports, and government infrastructure investment plans. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a segment bottom-up model: (i) residential construction component; (ii) infrastructure construction component; (iii) commercial and industrial construction components. Macroeconomic scenario analysis applied for Argentina's economic volatility characteristics.

Argentina Construction Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Sectors Covered | Commercial Construction, Residential Construction, Industrial Construction, Infrastructure (Transportation) Construction, Energy and Utility Construction |

| Regions Covered | Buenos Aires Region, Litoral Region, Northern Region, Cordoba Region, Cuyo Region, Patagonia Region |

| Companies Covered | Techint Group, Holcim, Loma Negra, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Argentina construction market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Argentina construction market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Argentina construction industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Argentina Construction Market Report

The Argentina construction market reached USD 65.52 Billion in 2025. The market is driven by economic expansion, rising urbanization and housing demand, infrastructure development, and increasing foreign investment through PPP frameworks. Government housing programs and Vaca Muerta energy construction are additional key demand drivers.

The market grows at 3.35% CAGR during 2026-2034, reaching USD 88.16 Billion by 2034. Energy and Utility Construction grows fastest at ~4.5% CAGR through Vaca Muerta development. Residential Construction at ~3.80% CAGR reflects sustained government housing program support.

Residential Construction leads at 33.8% through sustained housing demand, government mortgage subsidy programs including Procrear, and rapid urbanization driving residential development in Buenos Aires, Córdoba, Rosario, and other major cities.

Buenos Aires Region leads at 36.4% through its position as Argentina's economic and population center. The region attracts the majority of real estate investment, commercial development, and infrastructure spending, reinforcing its structural market leadership throughout the forecast period.

Leading companies include Techint Group, Holcim, and Loma Negra, among others.

The market is projected to reach approximately USD 77.26 Billion by 2030, with Vaca Muerta energy construction at peak deployment velocity, PPP infrastructure programs in active construction execution, and affordable housing programs sustaining residential construction volume.

Key growth drivers include economic expansion and GDP growth, rising urbanization and housing demand, government PPP infrastructure programs, Vaca Muerta energy development creating industrial construction demand, renewable energy construction targets, and multilateral financing from IDB and World Bank supporting major infrastructure projects.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)