Asia Pacific Dairy Market Size, Share, Trends and Forecast by Category, and Distribution Channel, and Region, 2026-2034

Asia Pacific Dairy Market Size, Share, Trends & Forecast (2026-2034)

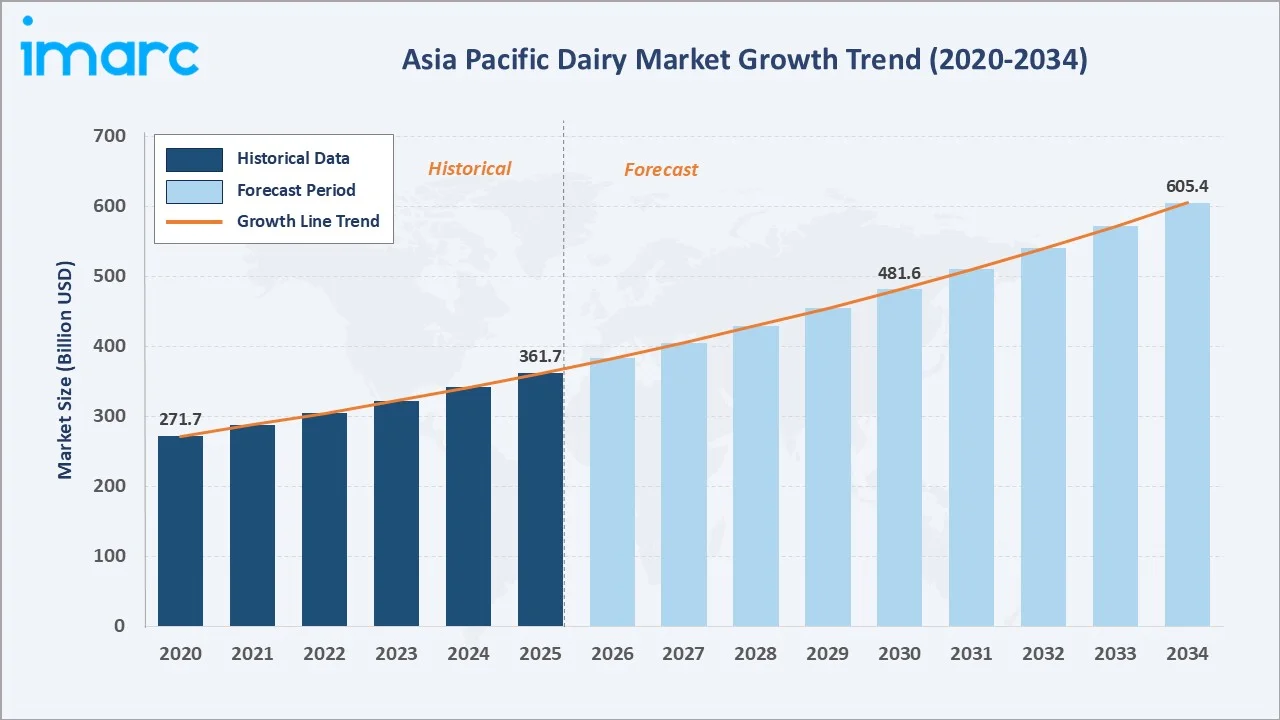

The Asia Pacific dairy market reached USD 361.7 Billion in 2025 and is projected to reach USD 605.4 Billion by 2034, growing at a CAGR of 5.89% during 2026-2034. The market is driven by rising population, increasing disposable incomes, and growing consumption of milk and dairy-based products across emerging economies. The Asia Pacific region accounts for around 60% of the global population, with nearly 4.3 billion people, including major population centers such as China and India. This large consumer base is driving the Asia Pacific dairy market by increasing demand for milk, yogurt, cheese, butter, and other dairy products. Urbanization, changing dietary habits, and expanding demand for protein-rich and functional dairy products are further supporting market growth. Milk leads at 34.8%. Off trade leads distribution at 78.6%. China commands 31.2% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 361.7 Billion |

|

Forecast Market Size (2034) |

USD 605.4 Billion |

|

CAGR (2026-2034) |

5.89% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Category |

Milk (34.8%, 2025) |

|

Dominant Distribution Channel |

Off Trade (78.6%, 2025) |

|

Leading Region |

China (31.2%, 2025) |

Asia Pacific's dairy market expanded from USD 271.7 Billion in 2020 to USD 361.7 Billion in 2025, anchored at USD 481.6 Billion in 2030, and forecast to reach USD 605.4 Billion by 2034. Asia Pacific is the largest and fastest-growing dairy market by absolute revenue. COVID-19 accelerated Asia Pacific's structural shift toward packaged dairy as lockdown-period at-home consumption surged, supply chain disruptions elevated milk preference above fresh dairy, and immunity-nutrition awareness created above-background demand for fortified dairy products across the region.

To get more information on this market, Request Sample

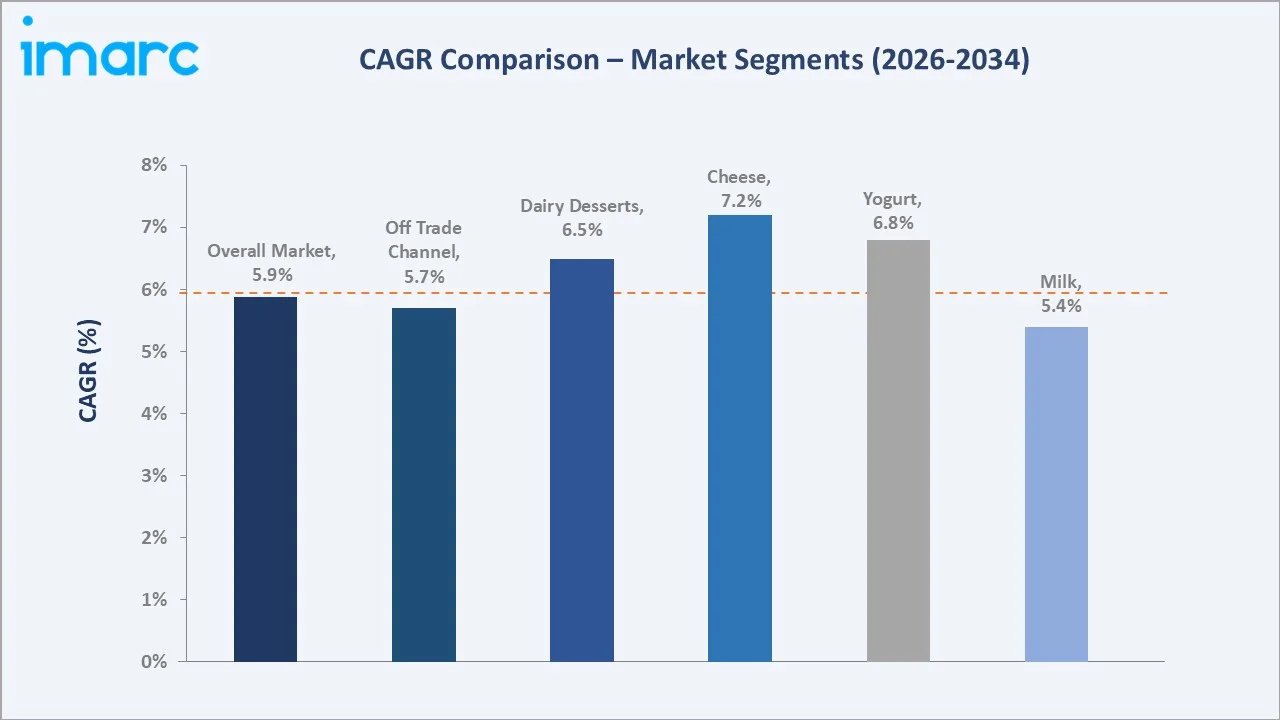

Cheese grows fastest at ~7.2% CAGR through Western food culture adoption. Yogurt at ~6.8% CAGR reflects Asia Pacific's probiotic and functional dairy adoption wave across China, Japan, South Korea, and India's health-conscious urban professional demographic.

Executive Summary

The Asia Pacific dairy market at USD 361.7 Billion in 2025 represents one of the most commercially significant dairy markets by revenue. The region's dairy market is commercially diverse, ranging from Japan's per-capita highly premium fresh dairy market to Indonesia's per-capita import-dependent reconstituted dairy market, creating market conditions where global dairy strategies require country-by-country commercial adaptation above regional standardization. The market is projected to reach USD 605.4 Billion by 2034.

Milk at 34.8% leads through Asia Pacific's dominant liquid dairy tradition. Off trade at 78.6% reflects the retail grocery dominance of Asia Pacific dairy distribution. China leads at 31.2% as the region's single largest national dairy market, followed by India (19.8%), Japan (12.6%), Indonesia (10.4%), Australia (9.1%), and South Korea (7.8%).

Key Market Insights

|

Insight |

Data |

|

Dominant Category |

Milk - 34.8% share (2025) |

|

Dominant Distribution Channel |

Off Trade - 78.6% market share (2025) |

|

Leading Region |

China - 31.2% Share (2025) |

|

Market Opportunity |

Premium organic and A2 milk; functional and fortified dairy for aging populations; cheese and yogurt premiumization; infant formula regulatory navigation in China; cold chain infrastructure investment across Southeast Asia |

Key Analytical Observations Supporting the Above Data:

- Milk at 34.8%: The milk segment dominates due to its daily consumption across households and its role as a staple source of protein, calcium, and nutrition. Strong demand from India, China, and Southeast Asian countries further supports its leading share.

- Off Trade at 78.6%: The off trade dominates as consumers mainly purchase milk, yogurt, cheese, butter, and other dairy products through supermarkets, convenience stores, local shops, and online grocery platforms for home consumption. Strong household demand and expanding modern retail networks further support segment growth.

- China at 31.2%: China dominates due to its large population, rising disposable incomes, and growing demand for milk, yogurt, cheese, and functional dairy products. Expanding urbanization, modern retail channels, and premium dairy consumption further support its leading position.

Asia Pacific Dairy Market Overview

Asia Pacific dairy market occupies a commercially unique position in the global dairy industry, simultaneously containing the most mature per-capita dairy markets, the most rapidly growing absolute dairy markets, and the most commercially underserved dairy markets by penetration. The market's commercial diversity creates the most complex single-region dairy investment thesis. Investors must simultaneously evaluate China's high-growth premium market, India's cooperative-dominated mass market, Japan's premium-functional market, and Southeast Asia's emerging import-dependent markets with fundamentally different commercial dynamics, regulatory environments, and competitive structures.

The Asia Pacific dairy ecosystem integrates dairy raw material exporters, domestic farm-to-factory supply chains, processing and manufacturing, cold chain logistics infrastructure, and regulatory frameworks. Macroeconomic factors include rising disposable incomes, population growth, urbanization, and expanding middle-class consumption.

Market Dynamics

To evaluate market opportunities, Request Sample

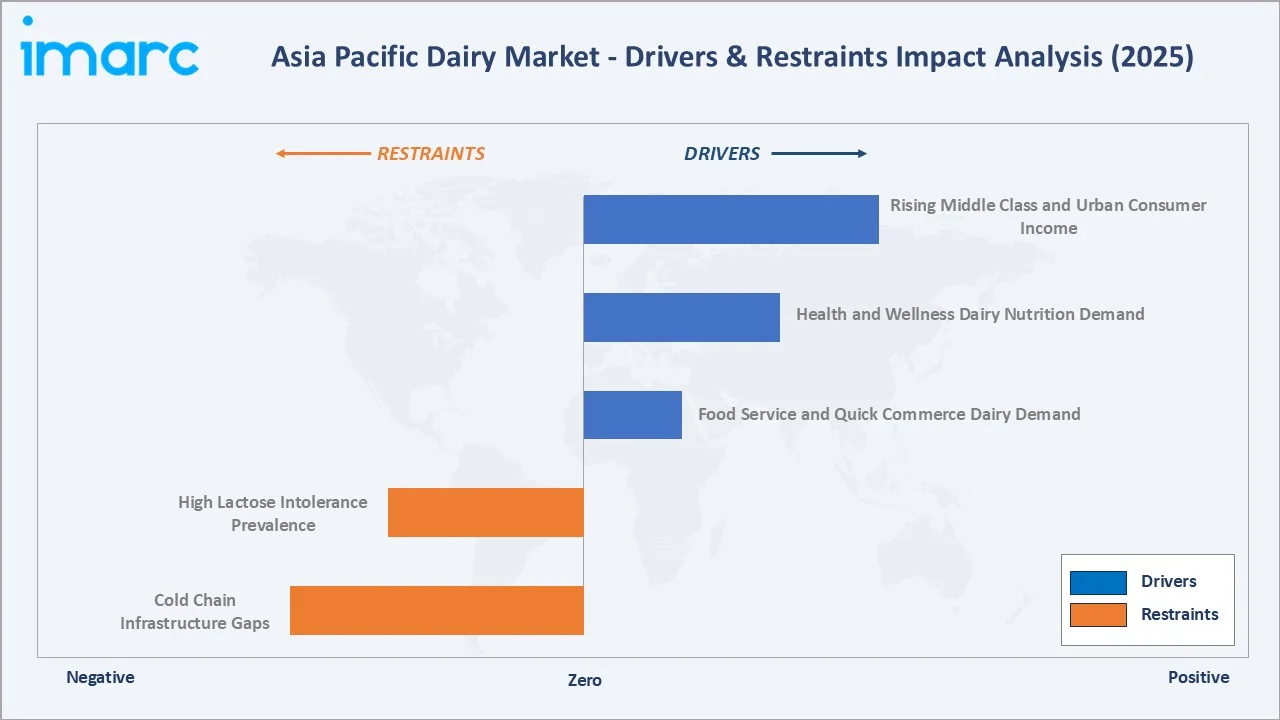

Market Drivers

- Rising Middle Class and Urban Consumer Income: The total number of middle-class households across Asia Pacific countries is projected to surpass one billion by 2034. This rising middle-class population and increasing urban consumer incomes are boosting spending on nutritious and value-added food products. Consumers are increasingly purchasing packaged milk, yogurt, cheese, flavored dairy beverages, and premium dairy products as their purchasing power improves. Urban lifestyles are also encouraging demand for convenient and fortified dairy offerings. This trend is particularly strong in rapidly developing economies such as China, India, Indonesia, and Vietnam.

- Health and Wellness Dairy Nutrition Demand: Health and wellness dairy nutrition demand is driving the market as consumers increasingly seek protein, calcium, vitamins, and probiotic-rich foods. Dairy products such as fortified milk, yogurt, probiotic drinks, and functional dairy beverages are gaining popularity among health-conscious consumers. Rising awareness of bone health, immunity, digestion, and child nutrition further supports demand. This is encouraging brands to expand value-added and functional dairy portfolios across the region.

- Food Service and Quick Commerce Dairy Demand: Food service and quick commerce dairy demand are increasing the use of milk, cheese, butter, cream, yogurt, and dairy beverages across cafés, restaurants, bakeries, and cloud kitchens. Rapid delivery platforms are also making packaged dairy products more accessible for daily household consumption. Rising demand for ready-to-eat meals, desserts, beverages, and convenience foods further supports dairy usage. In February 2026, Parle Agro expanded its dairy range with the launch of Smoodh Kesar Badam under its Smoodh brand. The flavored milk combines saffron and almonds in a creamy milk base and is positioned as an affordable indulgent drink for everyday consumption across age groups, available through retail stores, digital platforms, and quick commerce channels. This is encouraging brands to expand both foodservice and online grocery distribution channels.

Market Restraints

- High Lactose Intolerance Prevalence: A significant portion of consumers, particularly in East and Southeast Asia, experience difficulty digesting lactose. This can limit consumption of conventional milk and certain dairy products due to concerns about digestive discomfort. As a result, some consumers shift toward plant-based alternatives such as soy, oat, and almond beverages. Dairy manufacturers must therefore invest in lactose-free and digestive-friendly products to maintain market growth.

- Cold Chain Infrastructure Gaps: Cold chain infrastructure gaps hamper the market as milk, yogurt, cheese, and other dairy products require temperature-controlled storage and transport to maintain freshness. Limited refrigeration facilities, inconsistent logistics, and power supply issues can lead to spoilage and quality loss. This increases distribution costs and reduces product availability in rural and remote areas. As a result, dairy companies face challenges in expanding packaged and value-added dairy products across the region.

Market Opportunities

- A2 Milk Premium Market: The A2 milk premium market is creating opportunities as consumers increasingly associate A2 milk with easier digestion, purity, and better nutrition. Rising health awareness and demand for specialized dairy products are encouraging brands to launch A2 milk, ghee, yogurt, and infant nutrition products. Premium pricing also supports higher margins for dairy companies. This trend is especially strong among urban, health-conscious, and affluent consumers.

- Organic and Grass-Fed Premium Dairy: Organic and grass-fed premium dairy is creating opportunities as consumers seek cleaner, more natural, and higher-quality dairy products. Rising health awareness and concerns over additives, hormones, and animal welfare are boosting demand for organic milk, yogurt, cheese, and butter. These products allow brands to target affluent urban consumers with premium pricing. Growing modern retail and e-commerce channels further support their availability and adoption.

Market Challenges

- Competition from Plant-Based Dairy Alternatives: Competition from plant-based dairy alternatives is challenging as consumers increasingly choose soy, oat, almond, and coconut-based products due to lactose intolerance, vegan diets, and sustainability concerns. These alternatives are gaining visibility in supermarkets, cafés, and online channels. Their health and ethical positioning can reduce demand for conventional milk and dairy products. As a result, dairy companies face pressure to innovate with lactose-free, functional, and premium dairy offerings.

- Volatile Milk Procurement Prices: Volatile milk procurement prices are a major challenge as fluctuations in raw milk costs directly affect manufacturers' production expenses and profit margins. Prices can vary due to changes in feed costs, weather conditions, livestock productivity, and supply-demand imbalances. This makes pricing strategies difficult and can lead to higher retail prices for consumers. As a result, dairy companies face challenges in maintaining profitability while remaining competitive in the market.

Emerging Market Trends

1. Functional and Fortified Dairy Creating Clinical Nutrition Premium Markets

Functional and fortified dairy is emerging as consumers increasingly seek products that offer health benefits beyond basic nutrition. Dairy manufacturers are introducing milk, yogurt, and dairy beverages enriched with protein, probiotics, vitamins, minerals, omega-3, and immunity-supporting ingredients. These products are gaining popularity among health-conscious consumers, children, athletes, and aging populations. In November 2025, Akshayakalpa Organic launched High Protein Milk, expanding its functional nutrition portfolio that already includes High Protein Paneer and Peanut & Ragi-based snacks. The new product reflects the company’s focus on making clean, functional nutrition accessible to Indian consumers.

2. Premium Imported Dairy Brand Premiumization in China

Premium imported dairy brands are emerging as affluent consumers associate international dairy products with higher quality, safety, and nutrition. Demand is growing for imported milk, cheese, infant nutrition, yogurt, and specialty dairy products from trusted global origins. These brands often command premium pricing through strong quality assurance, packaging, and health positioning. This is encouraging dairy companies to expand premium portfolios and strengthen distribution through modern retail and e-commerce channels.

3. India's Cooperative-to-Corporate Dairy Transition Creating New Commercial Competition

India’s cooperative-to-corporate dairy transition is emerging as private dairy companies increasingly compete with established cooperative networks for milk procurement, processing, and distribution. Corporate players are investing in branded products, value-added dairy offerings, digital supply chains, and premium segments to gain market share. This is intensifying competition across pricing, product innovation, and farmer engagement. As a result, the dairy sector is becoming more commercialized and consumer-focused, creating new growth opportunities across the value chain.

4. Sustainability and Origin Transparency Creating Dairy Purchase Decision Premium

Sustainability and origin transparency are emerging as consumers increasingly want to know where and how their dairy products are produced. Brands are highlighting farm-to-table traceability, animal welfare practices, sustainable sourcing, and environmentally responsible production methods. Transparent labeling and verified origin claims help build consumer trust and justify premium pricing. As a result, sustainability and provenance are becoming key factors influencing dairy purchasing decisions, particularly among urban and premium consumers.

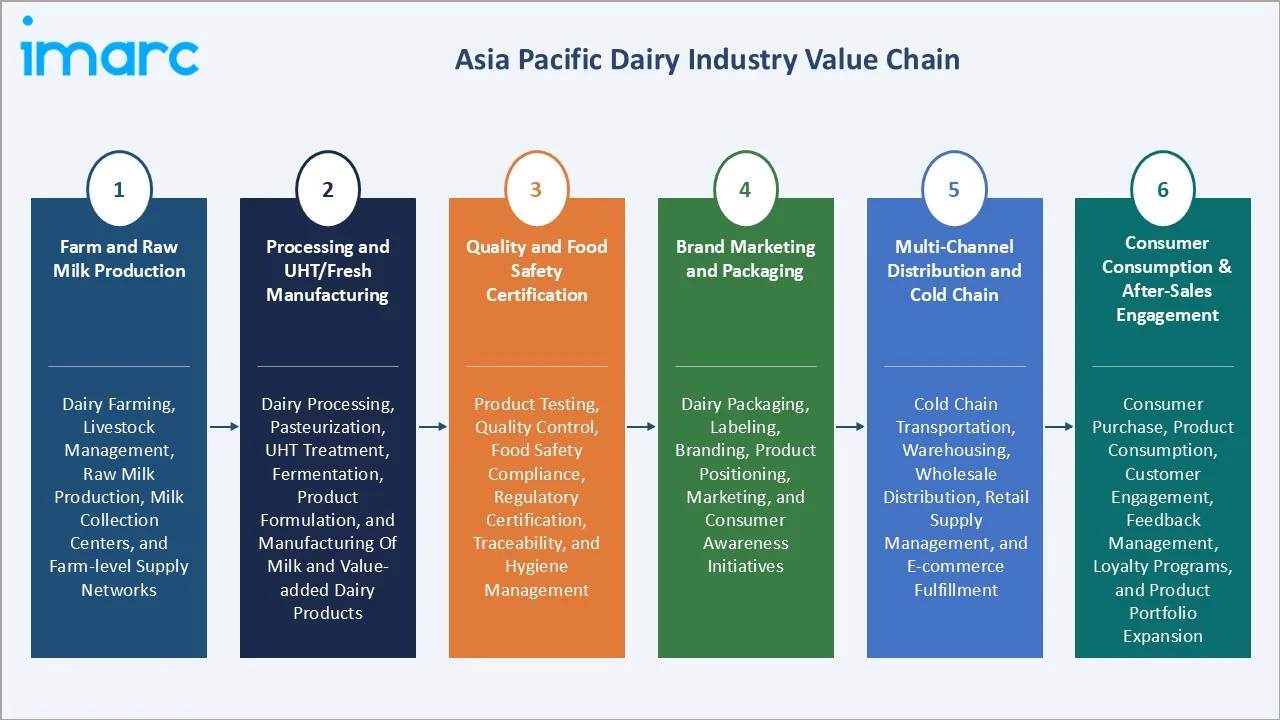

Industry Value Chain Analysis

Asia Pacific dairy value chain is the most geographically complex single-region dairy supply chain, integrating New Zealand and Australian dairy farm raw material at the upstream production end with consumers across national markets at the downstream consumption end through a mid-stream processing, distribution, and retail infrastructure that spans the most commercially diverse regulatory environments, cold chain capabilities, and consumer preferences.

|

Stage |

Key Participants |

|

Farm & Raw Milk Production |

Dairy farming, livestock management, raw milk production, milk collection centers, and farm-level supply networks |

|

Processing & UHT/Fresh Manufacturing |

Dairy processing, pasteurization, UHT treatment, fermentation, product formulation, and manufacturing of milk and value-added dairy products |

|

Quality & Food Safety Certification |

Product testing, quality control, food safety compliance, regulatory certification, traceability, and hygiene management |

|

Brand Marketing & Packaging |

Dairy packaging, labeling, branding, product positioning, marketing, and consumer awareness initiatives |

|

Multi-Channel Distribution & Cold Chain |

Cold chain transportation, warehousing, wholesale distribution, retail supply management, and e-commerce fulfillment |

|

Consumer Consumption & After-Sales Engagement |

Consumer purchase, product consumption, customer engagement, feedback management, loyalty programs, and product portfolio expansion |

The cold chain and distribution stage is the Asia Pacific dairy value chain's most commercially constraining physical infrastructure element. Cold chain investment by regional logistics providers is the value chain's most commercially consequential infrastructure development, creating the distribution capability for fresh dairy market expansion above ambient UHT dairy's current geographic dominance in Asia Pacific's commercially underdeveloped dairy markets.

Technology Landscape in the Asia Pacific Dairy Industry

UHT (Ultra-High Temperature) Processing Technology

UHT (ultra-high temperature) processing technology is transforming the Asia Pacific dairy industry by enabling milk and dairy products to remain safe and shelf-stable for extended periods without refrigeration before opening. In October 2025, Indian Prime Minister Narendra Modi inaugurated Rajasthan’s first Ultra-High Temperature (UHT) aseptic milk processing and packaging plant, marking a major milestone in the state’s dairy development. This technology helps reduce spoilage, supports long-distance distribution, and improves product availability in regions with limited cold chain infrastructure. It also enhances food safety by eliminating harmful microorganisms while preserving nutritional quality.

Pasteurization and Aseptic Processing Technology

Pasteurization and aseptic processing technologies are improving food safety, extending product shelf life, and maintaining product quality. Pasteurization eliminates harmful microorganisms while preserving essential nutrients, whereas aseptic processing enables dairy products to be packaged in sterile conditions to prevent contamination. These technologies support the production of safe, convenient, and ready-to-consume dairy products. They also facilitate wider distribution and reduce product losses across diverse regional markets.

IoT-Based Dairy Farm Monitoring Systems

IoT-based dairy farm monitoring systems enable real-time tracking of animal health, milk production, feeding patterns, and environmental conditions. Sensors and connected devices help farmers detect health issues early, improve herd management, and enhance productivity. These systems also support data-driven decision-making, reducing operational inefficiencies and production costs. As a result, IoT technology is improving dairy farm sustainability, milk quality, and overall supply chain efficiency across the region.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Category |

Milk |

34.8% |

2025 |

|

Distribution Channel |

Off Trade |

78.6% |

2025 |

|

Region |

China |

31.2% |

2025 |

By Category

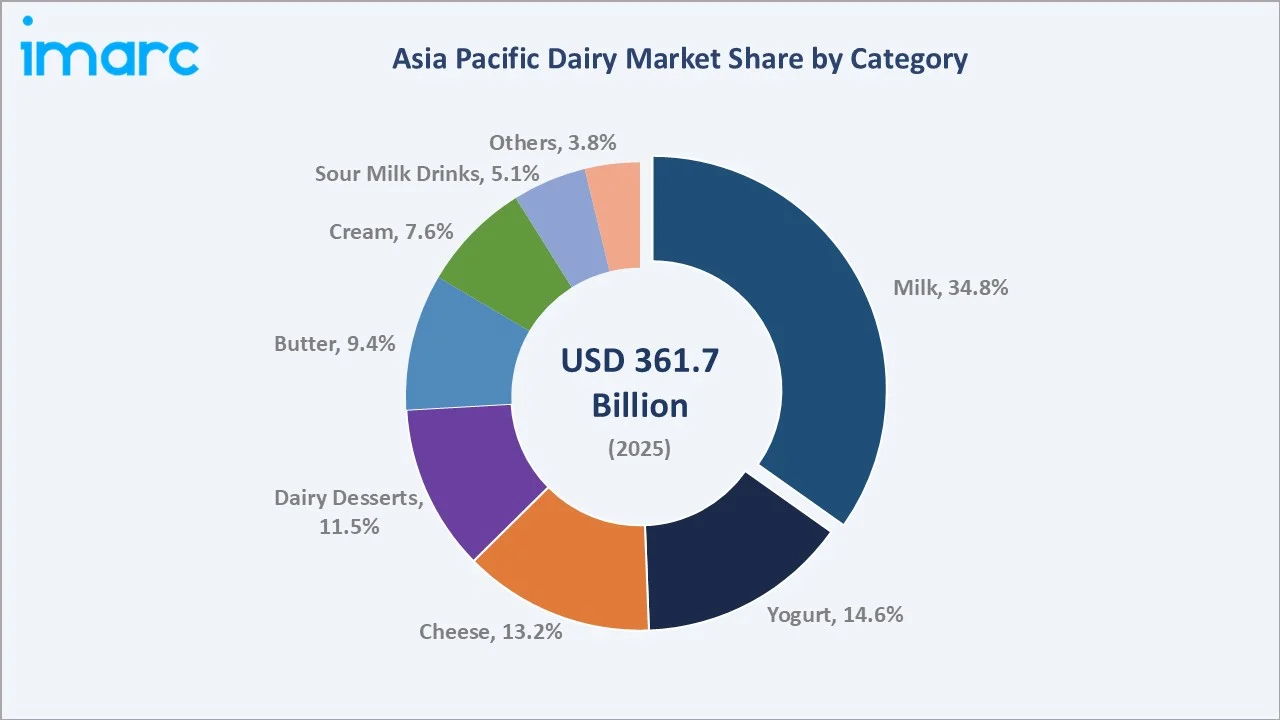

Milk leads at 34.8% (2025). The category encompasses fresh pasteurized, UHT ambient, flavored, organic, and A2 milk variants across Asia Pacific national markets, with above-average growth from China and Southeast Asia's dairy market development, creating above-commodity milk market expansion through premiumization and market penetration.

To access detailed market analysis, Request Sample

Yogurt at 14.6% and cheese at 13.2% are Asia Pacific's fastest-growing major categories at ~6.8% and ~7.2% CAGR, respectively. Dairy desserts at 11.5%, butter at 9.4%, and cream at 7.6% represent established categories growing steadily. Sour milk drinks at 5.1% reflect the Asia Pacific's traditional fermented dairy beverage markets. Others at 3.8% encompass milk-based beverages, dairy powder, and functional dairy.

By Distribution Channel

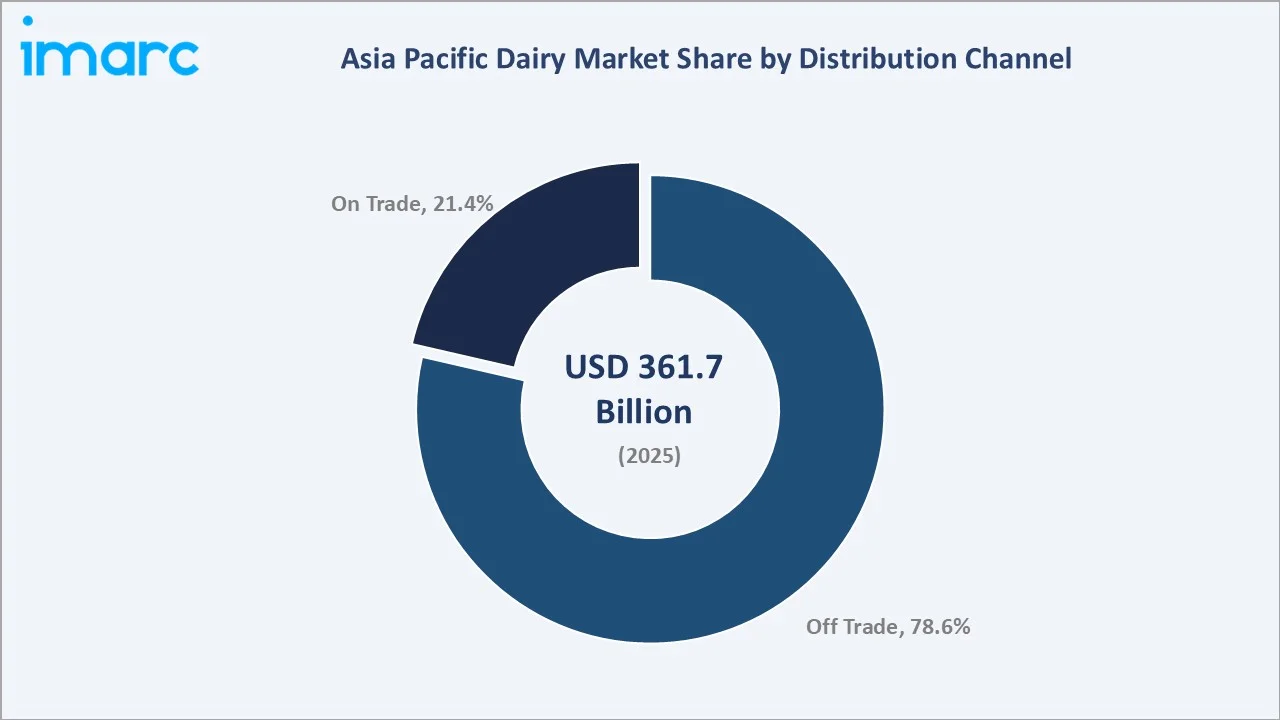

Off trade leads at 78.6% (2025). Supermarkets, hypermarkets, convenience stores, and specialty retail collectively create Asia Pacific's most commercially accessible dairy distribution infrastructure through organized modern trade expansion across the region's urban markets.

On trade at 21.4% grows at ~6.8% CAGR through food service dairy consumption led by Asia Pacific's coffee culture expansion, QSR dairy ingredient demand, and hotel and catering premium dairy procurement.

Regional Market Insights

|

Region |

Share (2025) |

Key Asia Pacific Dairy Market Drivers & Characteristics |

|

China |

31.2% |

Driven by its large consumer base, rising disposable incomes, growing demand for premium dairy products, and increasing consumption of milk, yogurt, and functional dairy beverages. |

|

India |

19.8% |

Driven by its large dairy production base, strong cultural preference for milk consumption, expanding middle-class population, and growing demand for packaged and value-added dairy products. |

|

Japan |

12.6% |

Supported by high consumer spending, strong demand for premium and functional dairy products, and advanced food processing and distribution infrastructure. |

|

Indonesia |

10.4% |

Driven by population growth, urbanization, rising household incomes, and increasing demand for milk, flavored dairy beverages, and dairy-based nutritional products. |

|

Australia |

9.1% |

Benefits from a well-developed dairy industry, high dairy consumption, strong export capabilities, and growing demand for premium, organic, and specialty dairy products across domestic and international markets. |

|

South Korea |

7.8% |

Characterized by strong demand for functional, fortified, and premium dairy products, supported by health-conscious consumers and a sophisticated retail ecosystem. |

|

Others |

9.1% |

Other Asia Pacific regions are driven by improving living standards, increasing dairy awareness, expanding retail infrastructure, and rising demand for nutritious and convenient dairy products. |

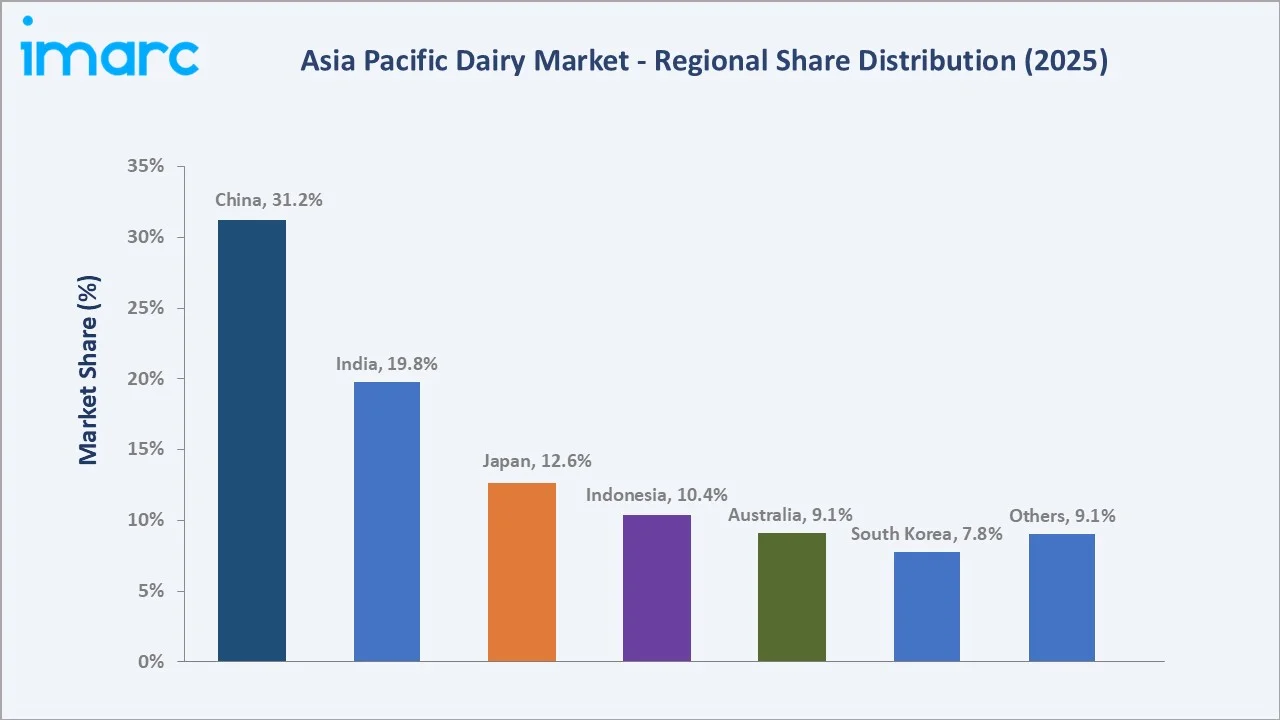

China's 31.2% market dominance reflects its status as the most commercially consequential single-country dairy market by absolute revenue growth, creating China the primary commercial investment destination for Asia Pacific dairy brands. India's 19.8% reflects the most commercially transformative dairy market development opportunity in the Asia Pacific through the cooperative-to-commercial transition, packaged dairy adoption, and premium yogurt and cheese category emergence. Japan's 12.6% represents the region's benchmark premium functional dairy market, where product innovation in probiotics, protein, and fortification sets the commercial standard that other Asia Pacific markets progressively adopt.

Indonesia's 10.4% reflects Southeast Asia's largest dairy market by absolute revenue, with the most commercially significant cold chain and import dependency challenge that limits fresh dairy market development above the ambient UHT and condensed milk market that ambient distribution supports. Australia's 9.1% represents the region's most commercially sophisticated premium export dairy economy, where organic, A2, and specialty dairy products command premium pricing. South Korea's 7.8% reflects the most Westernized East Asian dairy culture with the highest per-capita dairy consumption outside Japan and Australia. The others 9.1%, aggregating Vietnam, Thailand, Malaysia, Philippines, Singapore, and South Asia's emerging markets collectively, represents Asia Pacific's highest-growth regional aggregate by CAGR through the 2026-2034 forecast period.

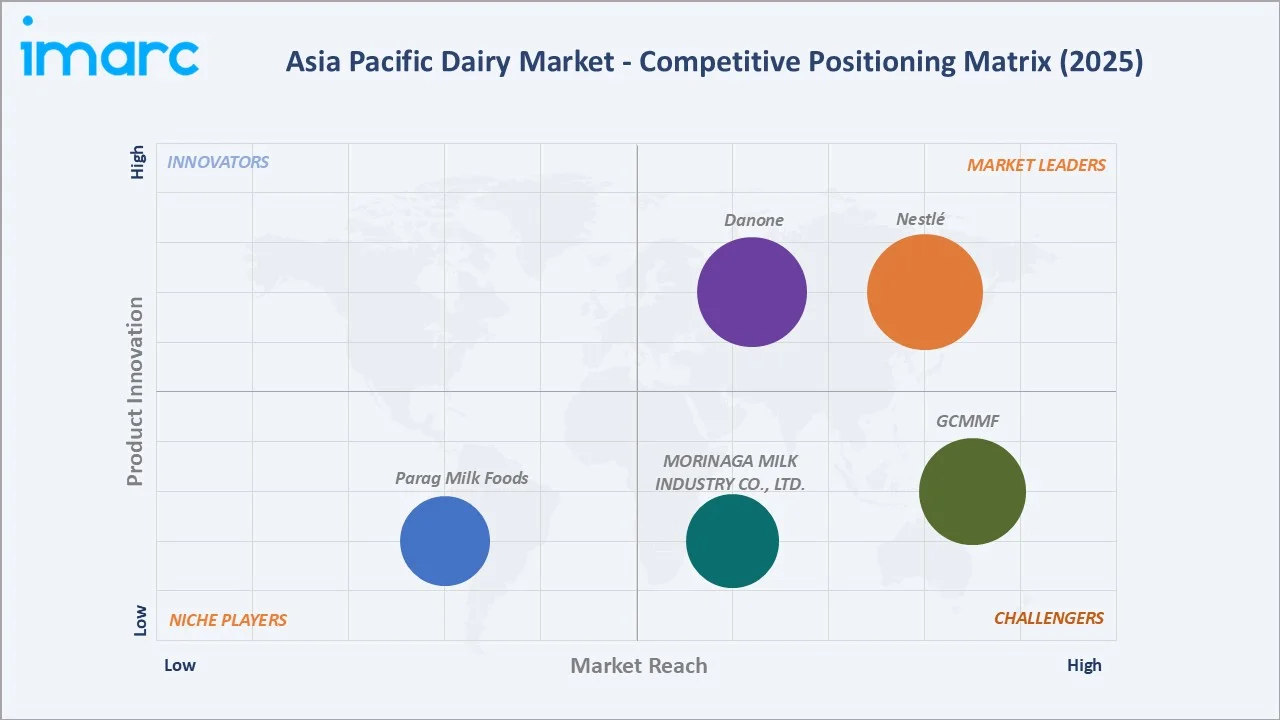

Competitive Landscape

Asia Pacific dairy market competitive landscape is the most commercially complex single-region dairy competitive environment, where multinational dairy companies, dairy cooperative exporters, Chinese domestic dairy giants, Japanese premium dairy innovators, Indian cooperative, Australian export-oriented producers, and many of the national dairy companies across Southeast Asia and South Asia compete simultaneously across the same geographic region with fundamentally different cost structures, brand equity, distribution capability, and regulatory access.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

Nestlé |

Nestlé |

Market Leader |

Nestlé plays a pivotal role in the Asia Pacific dairy sector, acting as a leading player in product innovation, dairy farming modernization, and sustainable sourcing, particularly in major markets like China, India, and Southeast Asia. |

|

Danone |

Activia, Aptamil |

Market Leader |

Danone is a major player in the Asia Pacific dairy and nutrition market, focusing on high-growth areas like specialized nutrition (infant formula), specialized dairy, and plant-based products. |

|

Parag Milk Foods |

GOWARDHAN, GO, PRIDE OF COWS, TOPP UP |

Niche Player |

Parag Milk Foods is a leading Indian private sector dairy company, with a focus on value-added products, premiumization via the "Pride of Cows" farm-to-home brand, and one of Asia's largest private cheese plants. |

|

GCMMF |

Amul |

Strong Challenger |

GCMMF, which owns the brand Amul, acts as a major force in the Asia Pacific dairy sector by combining immense scale with a community-driven cooperative model. As one of the strongest dairy brands, its role spans regional leadership in product manufacturing, market innovation, and acting as a template for rural development. |

|

MORINAGA MILK INDUSTRY CO., LTD. |

Bifidus yogurt, Bifiene |

Strong Challenger |

MORINAGA MILK INDUSTRY CO., LTD. plays a leading role in the Asia Pacific dairy sector as a major Japanese manufacturer and supplier of probiotics, functional ingredients, and premium dairy products. |

The competitive landscape's most commercially significant dynamics are China's domestic dairy consolidation and the Asia Pacific's most commercially disruptive new entrant.

Key Company Profiles

Nestlé

Nestlé is one of the leading dairy companies in the Asia Pacific dairy market, with a strong presence across key APAC countries. The company offers a broad portfolio of dairy products, including milk powders, dairy beverages, milkmaid, and fortified dairy products under well-known brands.

- Key Brands: Nestlé.

- Recent Developments: In April 2025, Nestlé launched BEAR BRAND MILK N’ SOY in the Philippines, a powdered drink combining milk and soy protein for school-age children. The company positioned the product as an affordable nutrition option and described it as a first-of-its-kind offering in the country’s kids’ nutrition category, available through supermarkets, grocery stores, and Sari-Sari neighborhood shops.

- Strategic Focus: Expanding its portfolio of fortified, functional, and affordable dairy products, while investing in nutrition innovation, hybrid dairy-plant offerings, premium dairy segments, and broad distribution networks to meet evolving consumer health and wellness needs across Asia Pacific.

Danone

Danone is a leading food and beverage company with a strong presence in the Asia Pacific dairy market through its portfolio of fresh dairy products, yogurt, probiotic beverages, infant nutrition, and specialized nutrition offerings.

- Key Brands: Activia, Aptamil.

- Recent Developments: In March 2024, Danone India launched a digital campaign to promote its AptaGrow product, designed to address the nutritional needs of children aged 3-6 years.

- Strategic Focus: Expanding its portfolio of probiotic, functional, and specialized nutrition dairy products, while strengthening its presence in premium health and wellness segments through innovation, gut-health solutions, sustainable sourcing, and consumer-centric nutrition offerings across Asia Pacific.

Market Concentration Analysis

The Asia Pacific dairy market is moderately concentrated at the regional level but highly concentrated within individual national markets. The regional market's concentration is increasing through three mechanisms: Chinese domestic dairy consolidation, multinational dairy acquisition, and cooperative-to-commercial transition. Competition is driven by product innovation, functional nutrition offerings, brand strength, distribution reach, and increasing investments in premium and value-added dairy segments.

Investment & Growth Opportunities

Highest Growth Segments

Cheese (~7.2% CAGR through Western food culture adoption), yogurt (~6.8% CAGR through probiotic adoption), on trade food service dairy (~6.8% CAGR through cafe and QSR expansion), India's packaged dairy transition from loose milk (~12-15% CAGR for branded dairy), Southeast Asia's premium fresh dairy market development (~10-12% CAGR for fresh dairy as cold chain infrastructure improves), and China's cheese market development (~15%+ CAGR from small base) represent Asia Pacific's highest-growth dairy investment segments through 2034.

Emerging Investment Opportunities

The most commercially significant underexploited Asia Pacific dairy investment opportunities are: Southeast Asia's cold chain infrastructure gap; India's cheese and yogurt premiumization; and A2 milk international expansion.

Investment Themes

- China premium dairy brand investment through A2 protein and organic origin differentiation: China's dairy market's premium import segment represents Asia Pacific's highest per-unit-revenue dairy investment opportunity.

- India's premium dairy brand development through organic and A2 positioning above Amul cooperative mass market: India's dairy market's premium commercial tier is growing as India's urban middle class income growth creates willingness to pay above cooperative pricing for perceived superior quality, organic certification, and A2 protein dairy. International dairy brands and India-born premium dairy companies are competing for India's most rapidly expanding dairy segment, which Amul's cooperative economics cannot serve at premium pricing above cooperative member pricing constraints.

Future Market Outlook (2026-2034)

The Asia Pacific dairy market is projected to grow from USD 361.7 Billion in 2025 to USD 605.4 Billion by 2034, delivering a 5.89% CAGR over the forecast period. The market's anchor value of USD 481.6 Billion in 2030 represents Asia Pacific dairy industry at a structural maturation inflection, from an emerging market-dominated dairy growth story toward a more balanced premium and volume growth narrative where Southeast Asia's emerging markets accelerate above China's moderating growth rate, India's premium dairy tier reaches commercial scale, and Australia and New Zealand's premium export dairy model creates value above the volume-growth era's commodity export economics.

Three structural forces define Asia Pacific's dairy market growth through 2034: Asia Pacific's demographic dividend, China's continued dairy market development, driven by per-capita consumption approaching Japan-level from current below-half-of-Japan levels, premium category expansion, and China's government dairy nutrition policy sustaining institutional demand-side support through public nutrition education, and India's packaged dairy transition is accelerating from a branded dairy market share.

Research Methodology

Primary Research

Primary research comprised structured interviews with Asia Pacific dairy industry stakeholders (2025) including Supply Chain Directors; Category Managers; Country Managers; Retail Dairy Category Heads; Cold Chain industry representatives; and dairy regulatory specialists. Consumer survey data from Asia Pacific dairy consumers across China, India, Japan, Indonesia, Australia, South Korea, and Southeast Asian markets.

Secondary Research

Secondary research encompassed dairy production statistics; China's mandatory dairy product registration data; India's dairy market regulatory compliance data; Dairy Australia Situation and Outlook Reports; New Zealand Ministry for Primary Industries dairy export statistics; China's National Dairy Industry market data; company annual reports; Asia Pacific dairy retail scanner data; International Asia Pacific Dairy Market Report. Over 80 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a country-by-country bottom-up dairy consumption model: each country's dairy market modelled through per-capita dairy consumption growth, national population projections, average dairy retail price inflation, and food service dairy demand growth.

Asia Pacific Dairy Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Categories Covered |

|

| Distribution Channels Covered |

|

| Regions Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Companies Covered | Nestlé, Danone, Parag Milk Foods, GCMMF, MORINAGA MILK INDUSTRY CO., LTD., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Asia Pacific dairy market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Asia Pacific dairy market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Asia Pacific dairy industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Asia Pacific Dairy Market Report

The Asia Pacific dairy market reached USD 361.7 Billion in 2025, driven by rising population, urbanization, increasing disposable incomes, and growing demand for protein- and calcium-rich foods. Expanding consumption of packaged milk, yogurt, cheese, fortified dairy, and functional dairy beverages further supports market growth.

Asia Pacific's dairy market grows at 5.89% CAGR during 2026-2034, reaching USD 605.4 Billion by 2034. The overall growth is sustained by Asia Pacific's middle-class income expansion, India's packaged dairy transition, China's premium category development, and Southeast Asia's cold chain infrastructure investment, enabling fresh dairy market expansion.

Milk leads at 34.8% through Asia Pacific's foundational liquid dairy consumption tradition, China, India, and Southeast Asia's dairy market development, anchored in UHT and fresh milk as the primary dairy consumption category.

Off trade leads at 78.6% through supermarkets, hypermarkets, and convenience stores, creating Asia Pacific's primary dairy retail distribution infrastructure.

China leads at 31.2% as the most commercially dynamic single-country dairy market by absolute revenue growth.

Leading companies include Nestlé, Danone, Parag Milk Foods, GCMMF, and MORINAGA MILK INDUSTRY CO., LTD., among others.

Asia Pacific's dairy market is projected to reach approximately USD 481.6 Billion by 2030, with China's dairy market growth as high per-capita consumption, India's branded packaged dairy reaching 25%+ of India's total dairy market value as commercial dairy investment accelerates, Southeast Asia's fresh dairy market expanding through cold chain infrastructure investment, and premium dairy categories collectively reaching above-25% of total Asia Pacific dairy market revenue from current below-20% as premiumization accelerates through the 2030 milestone.

East Asian adult lactose intolerance prevalence is the dairy industry's most commercially significant biological market constraint in the region's largest markets, moderated commercially by fermented dairy product adoption, lactose-free dairy product market development, and A2 protein dairy's market claim that A2 beta-casein protein reduces dairy digestive discomfort in lactose-sensitive consumers, creating commercial resonance in Asia Pacific's high-lactose-intolerance-prevalence markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)