Automotive Memory Market Size, Share, Trends and Forecast by Product, Vehicle Type, Application, and Region, 2026-2034

Automotive Memory Market Size and Share:

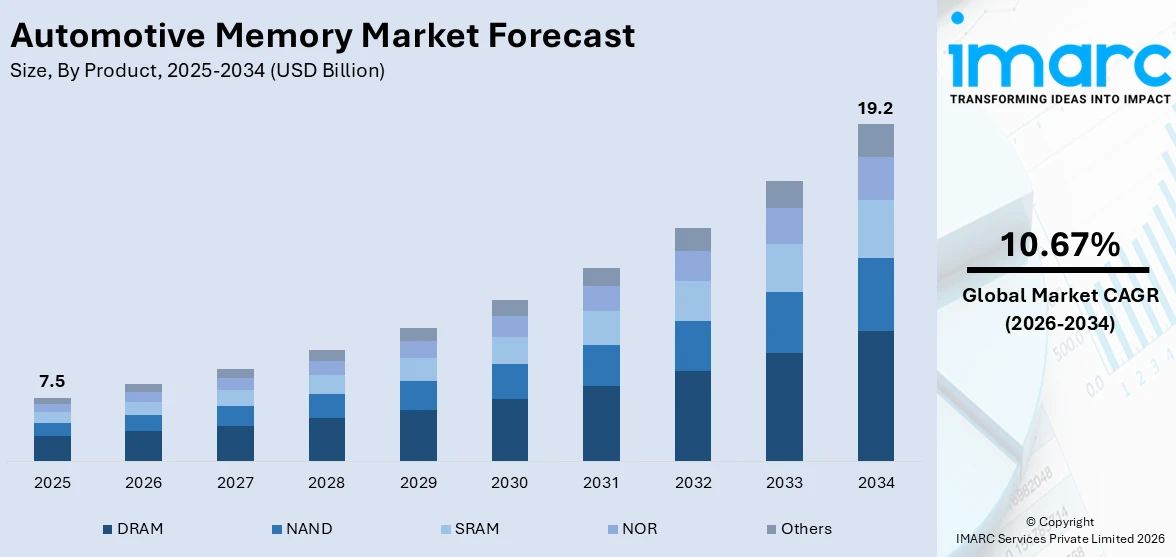

The global automotive memory market size was valued at USD 7.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 19.2 Billion by 2034, exhibiting a CAGR of 10.67% from 2026-2034. North America currently dominates the market, holding a market share of 36% in 2025. The region benefits from robust automotive manufacturing infrastructure, high adoption rates of advanced driver-assistance systems, and strong government initiatives supporting domestic semiconductor production, all of which are substantially contributing to the automotive memory market share.

The global automotive memory market is experiencing substantial growth, driven by the increasing integration of electronic components and software applications in modern vehicles. As automobiles become more connected and technologically advanced, the demand for high-capacity memory solutions continues to rise significantly. The growing role of artificial intelligence (AI) and machine learning (ML) in automotive systems for autonomous driving, predictive maintenance, and real-time decision-making is further fueling the automotive memory market growth. The implementation of favorable government policies and regulatory frameworks across major economies, aimed at promoting the development and adoption of EVs and smart automotive technologies, is also propelling the market growth. Furthermore, rapid advancements in manufacturing technologies, particularly three-dimensional (3D) NAND technology, are enabling the development of automotive memory with higher storage capacity, faster data transfer speeds, and greater reliability to meet the demands of next-generation vehicle applications.

The United States has emerged as a major region in the automotive memory market owing to many factors. The country benefits from a well-established automotive ecosystem that includes major vehicle manufacturers and technology companies actively integrating advanced driver-assistance systems (ADAS), infotainment platforms, and autonomous driving functionalities into their vehicles. Strong government initiatives, including legislation allocating more than USD 53 billion to boost domestic semiconductor production, are encouraging investment in memory chip manufacturing across the country. The rapid expansion of electric vehicles is also a significant growth enabler, with the country recording a 10% year-over-year increase in EV sales in January 2025. Additionally, the automotive memory market outlook remains highly positive, driven by increasing consumer preferences for technologically advanced vehicles, the growing deployment of connected car technologies, and the accelerating shift toward software-defined automotive platforms that require sophisticated, high-performance memory solutions to support their increasingly complex electronic architectures.

To get more information on this market Request Sample

Automotive Memory Market Trends:

Exponential Increase in Electronic Components and Software Applications

The increasing utilization of electronic components and software applications in modern vehicles is stimulating automotive memory market growth. As vehicles become smarter and more sophisticated, the volume of electronic systems requiring robust memory infrastructure continues to expand significantly. From engine control units (ECUs) to advanced driver-assistance systems (ADAS) and infotainment platforms, each application demands high-capacity, high-speed memory solutions capable of processing vast amounts of data in real time. The advent of autonomous driving technology has intensified this requirement, as self-driving systems need to process sensor inputs, execute machine learning algorithms, and make split-second decisions, all of which are highly data-intensive operations. Furthermore, the rising popularity of connected cars, which integrate with smartphones and digital devices, is creating additional demand for memory chips that facilitate efficient data exchange and storage. The growing software complexity, including over-the-air update capabilities, in-vehicle entertainment systems, and real-time navigation, continues to push demand for advanced automotive memory solutions across all vehicle segments. In 2025, Dolby Laboratories highlighted its growing automotive influence at Auto Shanghai 2025, as several manufacturers revealed new vehicles featuring the company's Vision HDR imaging and Atmos immersive sound technologies. The company announced that more than 25 automakers currently endorse Dolby experiences in their vehicles, which is twice the figure from one year prior, as cars progressively evolve from mere transportation into entertainment venues.

Rising Adoption of Electric and Hybrid Vehicles

The escalating adoption of electric and hybrid vehicles is positively influencing the automotive memory market forecast, creating substantial growth opportunities for memory solution manufacturers. Electric vehicles rely on sophisticated electronic control units and battery management systems that require advanced memory for monitoring energy usage, performance, and safety functions in real time. Additionally, EVs are increasingly equipped with features such as regenerative braking, smart grid interaction, and advanced navigation, all requiring complex algorithms and real-time data processing. The implementation of government incentive programs and emission reduction mandates is accelerating EV production and purchase across major automotive markets, consequently boosting automotive memory demand. Furthermore, the growing consumer preference for electric vehicles with rich infotainment experiences is driving automakers to incorporate higher-density, faster memory solutions. In June 2025, Samsung Electronics partnered with Infineon Technologies AG and NXP Semiconductors to co-develop next-generation automotive semiconductor solutions using 5nm process technology, reflecting intensifying industry collaboration to meet the memory-intensive requirements of electric and autonomous vehicles. This partnership underscores the industry's commitment to delivering specialized memory architectures that can support the computational demands of advanced vehicle platforms.

Rapid Advancements in Manufacturing Technologies

Rapid advancements in manufacturing technologies are fundamentally reshaping automotive memory market trends, enabling development of next-generation memory components with superior performance characteristics. Semiconductor technologies such as three-dimensional (3D) NAND provide a way to stack memory cells vertically, offering substantially greater storage density without increasing chip footprint. These innovations enable automotive memory components to handle larger data volumes without compromising speed or reliability, critical for augmented reality dashboards, 360-degree camera systems, and advanced navigational applications. The transition toward next-generation memory technologies, including LPDDR5 and GDDR6, is enhancing bandwidth and energy efficiency in automotive applications, enabling real-time analytics and AI-assisted functions in connected and autonomous vehicles. Furthermore, emerging technologies such as magnetoresistive random-access memory (MRAM) and resistive RAM (ReRAM) are gaining traction as high-endurance alternatives to traditional flash memory for safety-critical automotive applications. In May 2025, Infineon Technologies AG's SEMPER NOR flash memory family achieved ASIL-D certification, establishing a new benchmark for functional safety in automotive memory solutions and supporting next-generation software-defined vehicle architectures that demand the highest reliability and performance standards.

Automotive Memory Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global automotive memory market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, vehicle type, and application.

Analysis by Product:

- DRAM

- NAND

- SRAM

- NOR

- Others

DRAM holds 38% of the market share. Dynamic random-access memory (DRAM) is critical for tasks requiring quick read and write access to storage in computing and data processing activities within vehicles. As a high-performance memory type, DRAM serves as the backbone of multiple automotive applications, ranging from basic control units to highly advanced data-intensive systems such as ADAS and infotainment platforms. The widespread utilization of DRAM in autonomous vehicles, owing to its capability to handle high-speed data processing required for sensor input, real-time decision-making, and machine learning algorithms, is a primary factor driving its dominance. Furthermore, the ability of DRAM to be rewritten numerous times with minimal wear and tear, essential given the continuous data processing in modern vehicles, supports its widespread adoption. The integration of next-generation DRAM technologies such as LPDDR5 and LPDDR5X in automotive applications is further strengthening market penetration.

Analysis by Vehicle Type:

- Passenger Vehicles

- Commercial Vehicles

Passenger vehicles lead the market with a share of 75%. The dominance of passenger vehicles in the automotive memory market stems from the sheer volume of these vehicles on the road globally compared to commercial vehicles. Modern passenger cars are increasingly equipped with a range of advanced technologies, from infotainment systems to ADAS, requiring substantial memory capabilities to support complex functionalities. The rise in consumer expectations around in-vehicle experiences, encompassing enhanced entertainment, navigation, connectivity, and safety features, has led to the adoption of increasingly sophisticated electronic systems. The growing adoption of electric and hybrid passenger vehicles, which require specialized memory solutions for battery management and energy distribution, is contributing meaningfully to segment dominance. The integration of AI-powered features, including predictive maintenance, driver-monitoring systems, and personalized infotainment preferences, further elevates memory requirements.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Infotainment and Connectivity

- ADAS

- Others

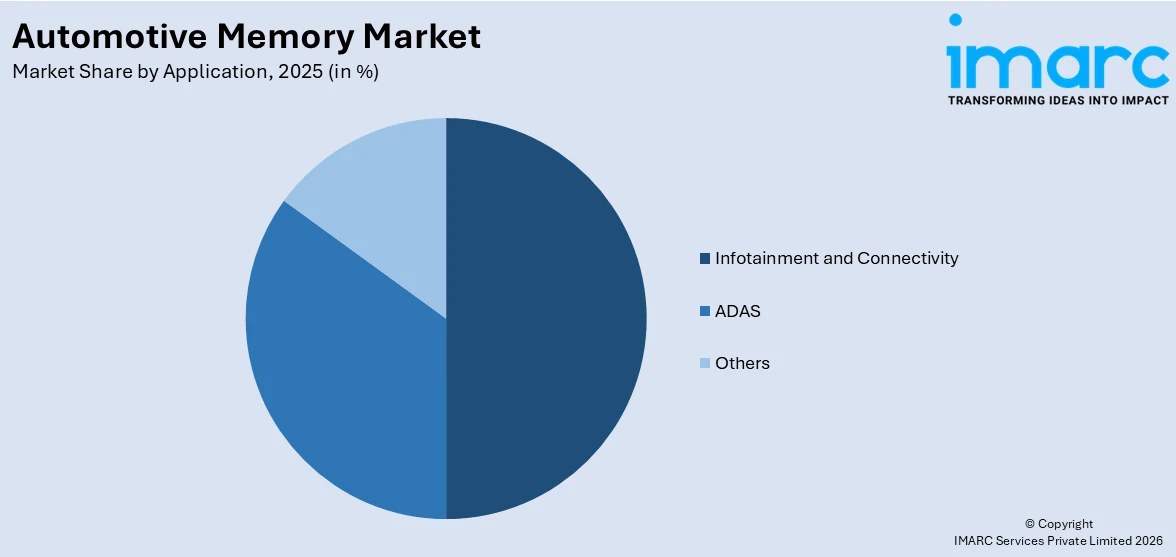

Infotainment and connectivity dominate the market, with a share of 43%. These modules serve as centralized systems for entertainment, navigation, voice assistance, and communications within modern vehicles, relying heavily on efficient and robust automotive memory solutions to manage a multitude of simultaneous tasks. The surge in consumer demand for seamless in-vehicle digital experiences, including touchscreen interfaces, smartphone integration, high-resolution display systems, and real-time streaming capabilities, has substantially elevated memory requirements of infotainment platforms. Furthermore, the growing adoption of 5G-enabled connectivity in vehicles is accelerating automotive memory market growth within this application segment, as 5G-connected systems require faster data processing and larger memory capacities. The integration of AI-powered voice assistants, over-the-air software update functionality, and cloud-based navigation services further increases memory demands.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 36% of the share, enjoys the leading position in the market. The region's strong presence in the automotive memory market is supported by its advanced automotive manufacturing ecosystem, which includes major vehicle manufacturers and technology companies driving the adoption of sophisticated electronic systems. The United States has implemented the CHIPS and Science Act, which allocated more than USD 50 billion to boost domestic semiconductor production, creating substantial investment opportunities for automotive memory manufacturers and suppliers. The high adoption rates of advanced driver-assistance systems and infotainment technologies in North American vehicles, supported by stringent safety regulations and strong consumer preferences for technologically advanced cars, continue to underpin robust demand for high-performance automotive memory. Furthermore, the region's growing electric vehicle market and expanding connected car infrastructure are creating additional avenues for automotive memory deployment. North America's well-established research and development ecosystem, combined with the presence of leading memory chip suppliers, is further reinforcing its leading market position globally.

Key Regional Takeaways:

United States Automotive Memory Market Analysis

The United States has established a strong position in the global automotive memory market, driven by a combination of technological innovation, regulatory support, and growing consumer demand for advanced automotive technologies. The country's automotive sector is undergoing rapid digital transformation, with major manufacturers increasingly integrating ADAS, intelligent infotainment systems, and autonomous driving features into their vehicle lineups. These advanced functionalities require sophisticated, high-capacity memory solutions, positioning the US as a key demand center for automotive memory globally. The implementation of the CHIPS and Science Act, which allocated approximately USD 53 billion for domestic semiconductor manufacturing, is directly benefiting the automotive memory supply chain by encouraging domestic production and reducing reliance on imports. The country's strong emphasis on vehicle safety regulations and cybersecurity compliance is also driving demand for memory solutions meeting the highest functional safety standards, including AEC-Q100 and ISO 26262 certifications. The presence of major technology companies and semiconductor suppliers further strengthens the US market position. In 2025, Intel unveiled a new processor named Panther Lake, which belongs to the company's Intel Core Ultra processor series. This will be the initial one constructed using the company’s 18A semiconductor process and will be solely produced at Intel’s Arizona fabrication plant.

Europe Automotive Memory Market Analysis

Europe holds a significant position in the global automotive memory market, supported by a strong automotive manufacturing base that includes premium vehicle brands driving adoption of advanced electronic systems. The region has been at the forefront of regulatory frameworks governing vehicle safety and emissions, accelerating the integration of ADAS, electrified powertrains, and sophisticated infotainment systems in European-manufactured vehicles. The European Union's stringent emission standards are driving substantial investments in EV development, consequently increasing demand for automotive memory solutions across passenger and commercial vehicle segments. Furthermore, European automakers are increasingly adopting zonal electrical/electronic architectures in next-generation vehicles, which require high-performance code-storage memory with fast secure-boot capabilities. Germany, France, and the United Kingdom remain the largest automotive markets in the region, with strong demand for premium vehicles equipped with advanced technology features. In December 2024, Black Semiconductor secured EUR 255 million in funding to launch advanced semiconductor technology in Europe, strengthening regional manufacturing capabilities for automotive-grade components and supporting the long-term resilience of the European automotive memory supply chain.

Asia-Pacific Automotive Memory Market Analysis

Asia-Pacific accounts for a substantial share of the global automotive memory market, driven by the region's dominant position as the world's largest automotive manufacturing hub. Countries such as China, Japan, South Korea, and India are among the leading producers of automobiles globally, generating high volumes of demand for automotive memory solutions across all vehicle types. The rapid expansion of electric vehicles in China, supported by strong government subsidies and a robust EV supply chain, is driving particularly significant demand for advanced memory solutions. The region also benefits from the concentration of leading semiconductor and memory solution manufacturers, including major players with extensive research and development facilities that advance automotive-grade memory technologies. In August 2025, Hyundai Mobis acquired semiconductor development process certification for ISO 26262 ASIL-D, demonstrating the region's commitment to advancing automotive-grade semiconductor standards and supporting the adoption of safety-compliant memory solutions across next-generation vehicle platforms throughout Asia-Pacific.

Latin America Automotive Memory Market Analysis

Latin America is gradually emerging as a growing market for automotive memory solutions, supported by expanding vehicle production in Brazil and Mexico and rising consumer demand for vehicles equipped with modern technology features. The region's increasing integration into global automotive supply chains, combined with improving economic conditions in major markets, is encouraging greater adoption of ADAS, infotainment, and connectivity technologies in locally manufactured vehicles. Government initiatives promoting the electrification of transportation and investments in smart mobility infrastructure are creating additional opportunities for automotive memory deployment.

Middle East and Africa Automotive Memory Market Analysis

The Middle East and Africa presents an emerging growth opportunity in the global automotive memory market, supported by rising vehicle sales, increasing urbanization, and growing demand for technologically sophisticated automotive products. Gulf Cooperation Council (GCC) countries are leading the region's adoption of connected and electric vehicles, driven by government diversification initiatives and smart city programs. The development of advanced transportation infrastructure across the UAE, Saudi Arabia, and other GCC nations is creating demand for vehicles with sophisticated ADAS, navigation, and connectivity systems requiring high-performance memory.

Competitive Landscape:

The global automotive memory market features a moderately concentrated competitive landscape, with several leading semiconductor manufacturers competing to develop high-performance, durable, and reliable memory solutions for evolving automotive applications. Key market players are actively differentiating their offerings by developing specialized memory solutions for distinct automotive use cases, including high-speed DRAM optimized for real-time ADAS processing and low-power, high-capacity storage solutions for infotainment systems. Companies are forming strategic alliances and partnerships with original equipment manufacturers and Tier-1 automotive suppliers, creating opportunities for co-development projects and exclusive supply contracts. Additionally, major players are pursuing geographic expansion strategies, focusing on high-growth regions by establishing local manufacturing units or pursuing mergers and acquisitions. Investments in advanced packaging technologies, next-generation process nodes, and automotive-grade safety certifications are becoming key competitive differentiators. Supply chain resilience has also emerged as a strategic priority, with leading companies maintaining strategic inventories and implementing just-in-time delivery models to ensure uninterrupted supply to automotive customers.

The report provides a comprehensive analysis of the competitive landscape in the automotive memory market with detailed profiles of all major companies, including:

- Infineon Technologies AG

- Integrated Silicon Solution Inc.

- Macronix International Co. Ltd.

- Micron Technology Inc.

- Nanya Technology Corporation

- Renesas Electronics Corporation

- Samsung Electronics Co. Ltd.

- SK hynix Inc.

- Texas Instruments Incorporated

- Western Digital Corporation

- Winbond Electronics Corporation

Latest News and Developments:

- February 2026: Renesas Electronics Corporation (TSE:6723), a leading provider of advanced semiconductor technologies, revealed a customizable ternary content-addressable memory (TCAM) based on a 3nm FinFET process. The updated TCAM provides increased density, reduced power consumption, and enhanced functional safety, making it ideal for automotive uses. Renesas showcased the findings at the International Solid-State Circuits Conference 2026 (ISSCC 2026), which took place from February 15 to 19 in San Francisco, USA.

- July 2025: KIOXIA America, Inc. has announced that it has started sampling1 the new Universal Flash Storage2 (UFS) Ver. 4.1 memory devices integrated for use in automotive applications. Designed to satisfy the stringent requirements of advanced in-vehicle systems, these innovative devices provide substantial performance, adaptability, and diagnostic improvements, driven by KIOXIA’s 8th generation BiCS FLASHTM 3D flash memory technology and proprietary controller technology.

Automotive Memory Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | DRAM, NAND, SRAM, NOR, Others |

| Vehicle Types Covered | Passenger Vehicles, Commercial Vehicles |

| Applications Covered | Infotainment and Connectivity, ADAS, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Infineon Technologies AG, Integrated Silicon Solution Inc., Macronix International Co. Ltd., Micron Technology Inc., Nanya Technology Corporation, Renesas Electronics Corporation, Samsung Electronics Co. Ltd., SK hynix Inc., Texas Instruments Incorporated, Western Digital Corporation, Winbond Electronics Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive memory market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive memory market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive memory industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Memory Market Report

The automotive memory market was valued at USD 7.5 Billion in 2025.

The automotive memory market is projected to exhibit a CAGR of 10.67% during 2026-2034, reaching a value of USD 19.2 Billion by 2034.

The automotive memory market is driven by the increasing integration of electronic components in modern vehicles, rising adoption of electric and hybrid vehicles, growing demand for advanced driver-assistance systems, and rapid advancements in semiconductor manufacturing technologies such as 3D NAND and LPDDR5 that enable higher storage capacities and faster data processing for next-generation automotive applications.

North America currently dominates the automotive memory market, accounting for a share of 36% in 2025. The region benefits from strong semiconductor manufacturing initiatives, high adoption rates of advanced driver-assistance systems, and a rapidly growing electric vehicle fleet requiring sophisticated automotive memory solutions across multiple vehicle applications.

Some of the major players in the automotive memory market include Infineon Technologies AG, Integrated Silicon Solution Inc., Macronix International Co. Ltd., Micron Technology Inc., Nanya Technology Corporation, Renesas Electronics Corporation, Samsung Electronics Co. Ltd., SK hynix Inc., Texas Instruments Incorporated, Western Digital Corporation, Winbond Electronics Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade