Automotive Radar Market Size, Share, Trends and Forecast by Range, Vehicle Type, Application, and Region, 2026-2034

Automotive Radar Market Size, Share, Trends & Forecast (2026-2034)

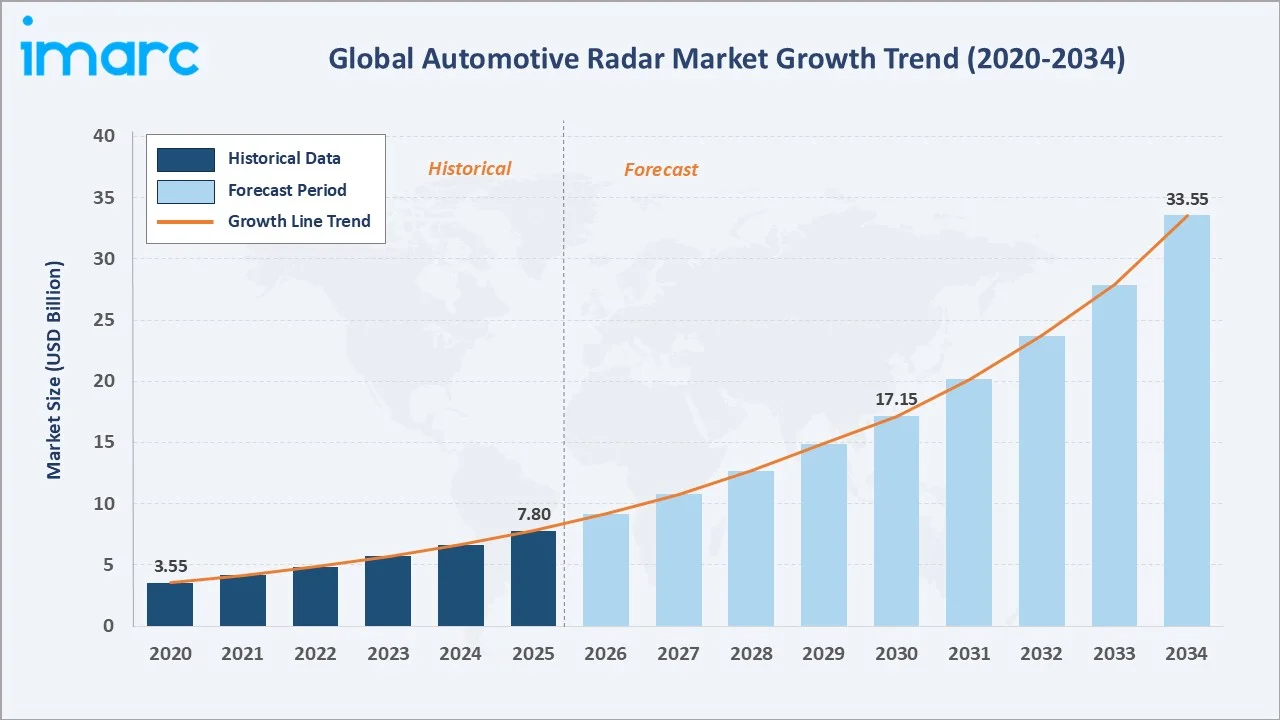

The global automotive radar market reached USD 7.80 Billion in 2025 and is projected to reach USD 33.55 Billion by 2034, growing at a CAGR of 17.07% during 2026-2034. Explosive growth is driven by mandatory ADAS safety regulations, accelerating autonomous vehicle development, and the rapid mainstream adoption of collision avoidance, adaptive cruise control, and blind-spot detection features across passenger and commercial vehicle segments.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 7.80 Billion |

| Forecast Market Size (2034) | USD 33.55 Billion |

| CAGR (2026-2034) | 17.07% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

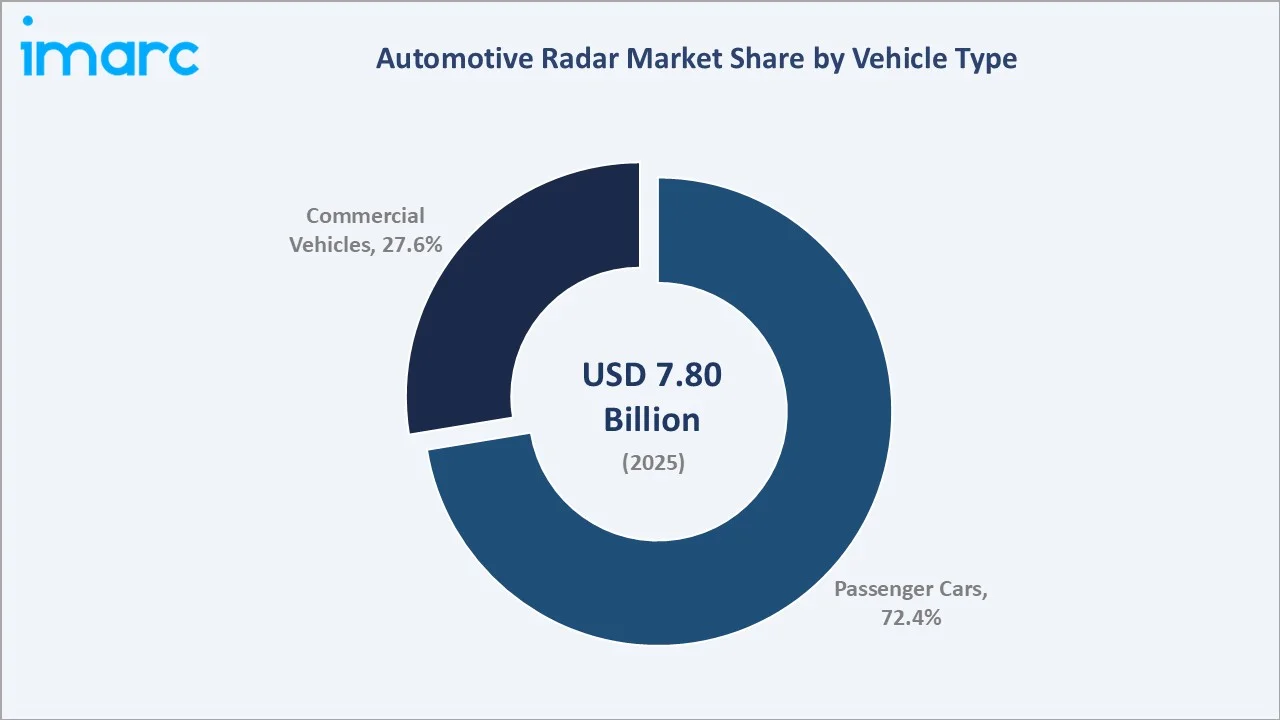

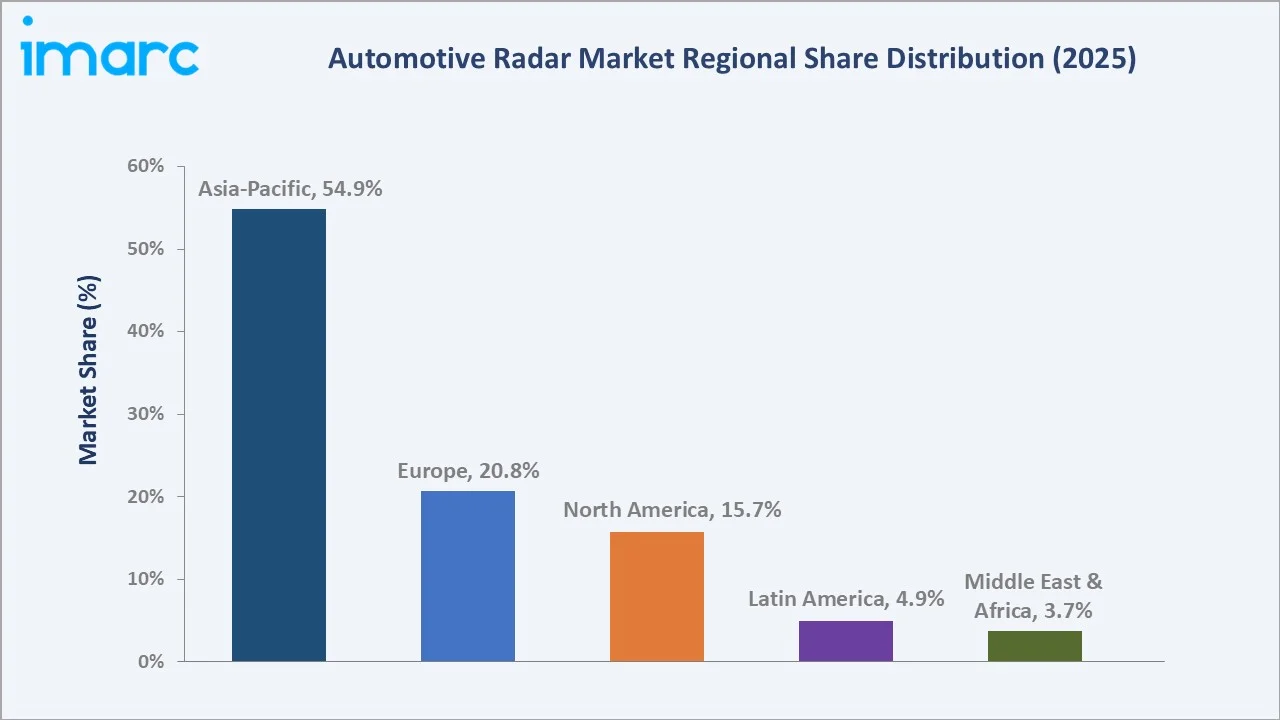

Asia-Pacific's commanding 54.9% share is underpinned by China's status as the world's largest automotive production market, Japan's precision sensor manufacturing ecosystem, and South Korea's rapid ADAS adoption in domestic brands. Passenger cars' 72.4% dominance reflects the proliferation of radar-enabled safety features, from lane-keep assist to automated emergency braking, which are transitioning from premium-only to mass-market standard fitment globally.

To get more information on this market, Request Sample

The market's exceptional 17.07% CAGR reflects a structural, regulation-driven demand acceleration. Global safety mandates requiring Automatic Emergency Braking (AEB), Euro NCAP five-star requirements, and US NHTSA AEB rulings are compelling OEMs to fit radar sensors across vehicle lines, from entry-level hatchbacks to heavy-duty commercial trucks.

Executive Summary

The global automotive radar market is one of the fastest-growing segments within the automotive electronics industry, driven by converging regulatory, technological, and consumer forces. From USD 7.80 Billion in 2025, the market is forecast to reach USD 33.55 Billion by 2034, creating incremental value of USD 25.75 Billion at a 17.07% CAGR, one of the highest growth trajectories among major automotive component categories.

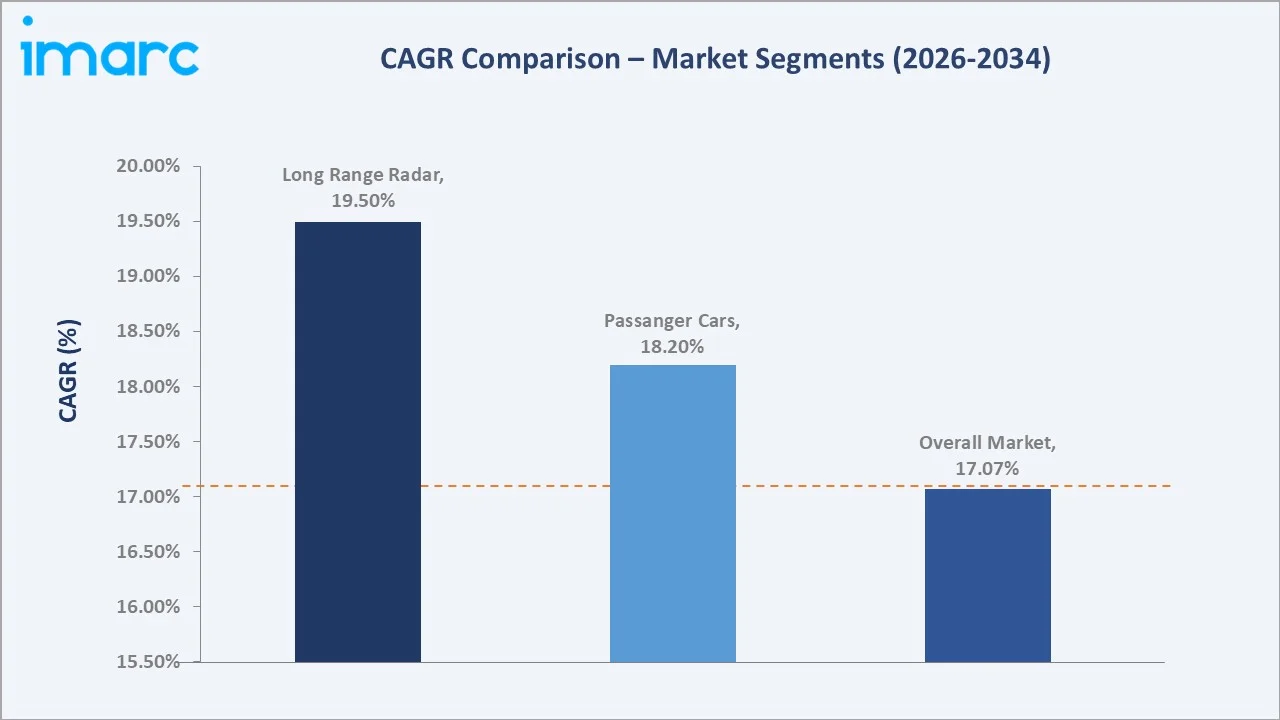

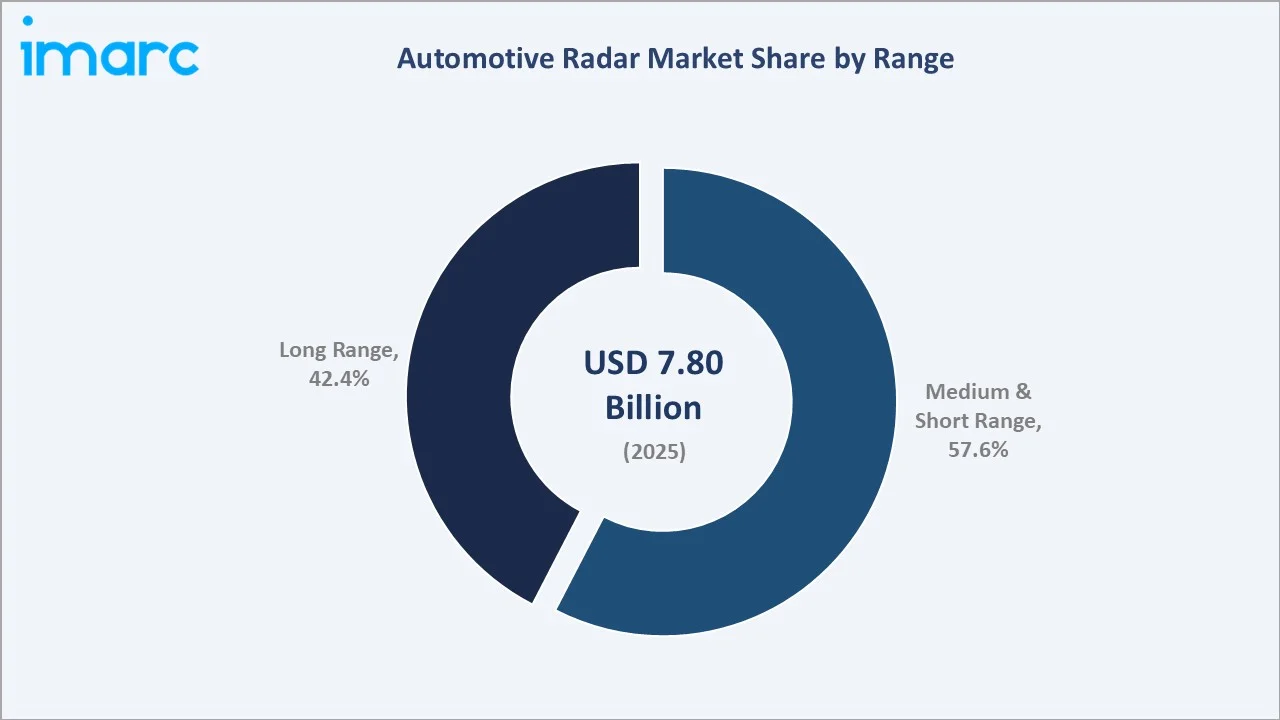

Medium and short range radar leads with a 57.6% share in 2025, driven by its critical role in blind-spot detection, parking assistance, lane-change assist, and rear cross-traffic alert applications. Passenger cars dominate with a 72.4% vehicle-type share, reflecting the mass-market rollout of ADAS features that were previously exclusive to premium segments. Long range radar, at 42.4%, is growing fastest, driven by adaptive cruise control and autonomous highway driving.

Key players, including Robert Bosch GmbH, VALEO, Aptiv, DENSO Corporation, and NXP Semiconductors, compete through proprietary 77 GHz radar chip designs, AI-enhanced signal processing, and deep OEM integration programs across passenger car and commercial vehicle platforms globally.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Range Segment | Medium & Short Range – 57.6% share (2025) |

| Fastest Growing Range | Long Range – ~19.50% CAGR (2026-2034) |

| Largest Vehicle Type | Passenger Cars – 72.4% share (2025) |

| Fastest Growing Vehicle Type | Commercial Vehicles – driven by AEB mandates for HCVs |

| Leading Region | Asia-Pacific – 54.9% share (2025) |

| Top Companies | Robert Bosch GmbH, VALEO, Aptiv, DENSO Corporation, NXP Semiconductors |

Key Analytical Observations:

- Medium and short range radar commands a 57.6% share in 2025. These systems are extensively used across the widest variety of ADAS applications, blind-spot monitoring, parking assist, cross-traffic alert, and lane-change assist, in vehicles across all price segments. Their lower per-unit cost, compact form factor, and compatibility with 24 GHz and 77 GHz architectures make them the default specification for mass-market vehicle platforms.

- Long range radar at 42.4% (2025) is growing fastest at an estimated 19.50% CAGR. As vehicles progress toward Level 2+ and Level 3 autonomy, long range radar (150–250 m detection range at 77 GHz) becomes architecturally required for adaptive cruise control, highway pilot functions, and automated emergency braking at motorway speeds.

- Passenger cars dominate at 72.4% (2025) due to the sheer volume of new car registrations in the EU, which rose by 1.8% year-on-year in 2025, combined with rapidly increasing ADAS penetration rates as safety standards mandate radar fitment across all vehicle classes from 2024 onwards in the EU, US, and China.

- Asia-Pacific's 54.9% (2025) dominance reflects the concentration of global automotive production in China, Japan, South Korea, and India. In 2025, China’s vehicle production reached 34.531 million units, marking year-on-year increases of 10.4% according to the China Association of Automobile Manufacturers (CAAM).

Automotive Radar Market Overview

Automotive radar systems use microwave radio frequencies, primarily 24 GHz (short range) and 77–81 GHz (medium and long range), to detect objects, measure distances, and calculate relative velocities around a vehicle.

Modern radar systems form the foundational sensing layer of ADAS platforms, enabling automated emergency braking (AEB), adaptive cruise control (ACC), lane-keep assist (LKA), blind-spot detection (BSD), and parking assistance. The market encompasses radar transceiver chips, complete radar modules, and fully integrated ADAS radar system-on-chip (SoC) solutions.

The market is structured around two primary deployment architectures: stand-alone radar sensors (dominant in current-generation ADAS) and sensor-fusion platforms that combine radar with cameras and lidar for higher-level autonomy.

The transition from 24 GHz to 77 GHz and the emergence of 4D imaging radar, which adds elevation measurement to conventional range, velocity, and azimuth detection, is the defining technology inflection point of the 2024–2030 period.

Market Dynamics

To evaluate market opportunities, Request Sample

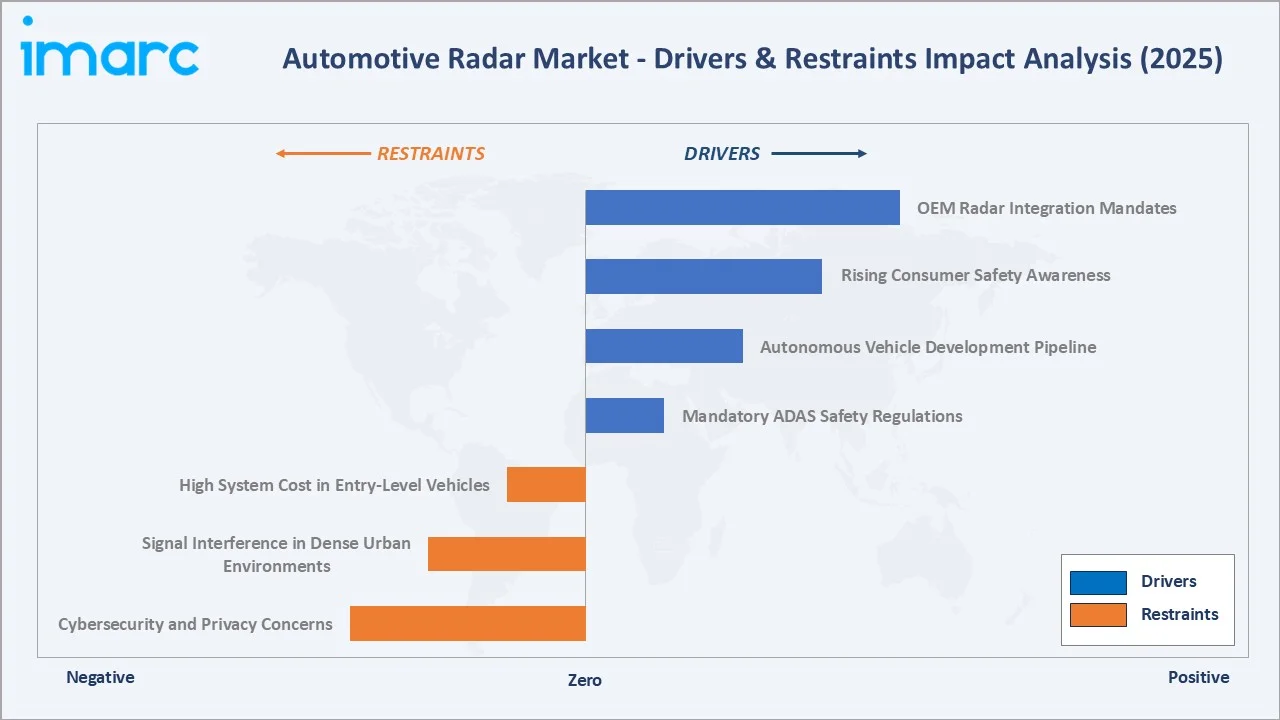

Market Drivers

- Mandatory ADAS Safety Regulations: Euro NCAP's five-star safety requirements effectively mandate AEB, lane-keeping assist, and blind-spot detection in all new passenger car models sold in Europe from 2024. The US NHTSA's AEB final rule (effective 2029, announced 2024) requires AEB in all new light vehicles, while China's GB/T 38186 and CNCAP standards create parallel demand in the world's largest auto market.

- Autonomous Vehicle Development Pipeline: Over 40 automakers and technology companies are actively developing Level 2+ to Level 4 autonomous vehicle platforms as of 2025. Each autonomy level requires increasing radar sensor counts per vehicle, from 1–2 units in Level 1 to 6–12 units in Level 3+ systems, creating a powerful content-per-vehicle value multiplier as autonomy levels advance across the industry.

- Rising Consumer Safety Awareness: Consumer demand for five-star safety ratings, insurance premium discounts tied to ADAS fitment, and the "safety halo" marketing value of radar-enabled features are compelling OEMs to include radar as standard equipment in mid-range vehicles where it was previously optional or unavailable, expanding the addressable market beyond premium segments.

- OEM Radar Integration Mandates: Global OEMs including Toyota, Volkswagen Group, Stellantis, and Hyundai-Kia have committed to standard radar fitment across their full model ranges by 2027–2029, creating secured volume demand for tier-1 radar suppliers that is reflected in 3–5 year supply contracts already announced by Robert Bosch GmbH and Aptiv.

Market Restraints

- High System Cost in Entry-Level Vehicles: A 77 GHz radar module costs USD 10-32 per unit at OEM pricing. For entry-level vehicles in price-sensitive markets (India, Southeast Asia, Latin America), where vehicles sell for USD 8,000–15,000, the cost of a full-suite ADAS radar package represents 3–5% of vehicle cost, constraining adoption timelines in the fastest-growing emerging automotive markets.

- Signal Interference in Dense Urban Environments: As vehicle radar density increases on urban roads, inter-vehicle radar interference becomes a material performance challenge. Dense sensor environments can cause ghost detections, reduced range accuracy, and false-positive ADAS interventions, requiring sophisticated interference-mitigation algorithms that add system complexity and cost.

- Cybersecurity and Privacy Concerns: Vehicle radar systems, particularly those integrated with cloud-connected ADAS platforms, represent potential cybersecurity attack surfaces. Regulatory scrutiny around connected vehicle data and the requirement for end-to-end encryption of radar-derived data adds compliance costs and development complexity for OEMs and tier-1 suppliers.

Market Opportunities

- 4D Imaging Radar Commercialization: 4D imaging radar, which adds elevation angle measurement and ultra-high angular resolution to conventional radar capabilities, is entering production at OEMs including BMW, GM, and Volkswagen.

- Commercial Vehicle ADAS Mandates: EU General Safety Regulation II requires advanced emergency braking and driver monitoring in all new heavy commercial vehicles from 2024. The commercial vehicle segment at 27.6% of the market is growing faster than passenger cars as HCV fleets globally begin mandatory radar fitment.

Market Challenges

- Sensor Fusion Integration Complexity: As vehicles incorporate radar alongside cameras, lidar, and ultrasonic sensors in multi-sensor fusion platforms, the software complexity of fusing heterogeneous sensor data in real time creates significant engineering challenges.

- Semiconductor Supply Chain Dependency: Automotive radar chips are manufactured on specialized RFCMOS and SiGe semiconductor processes with limited global production capacity. Supply concentration at foundries in Taiwan and South Korea creates geopolitical supply chain risk for the radar supply ecosystem, as demonstrated during the 2021–2022 semiconductor shortage.

Emerging Market Trends

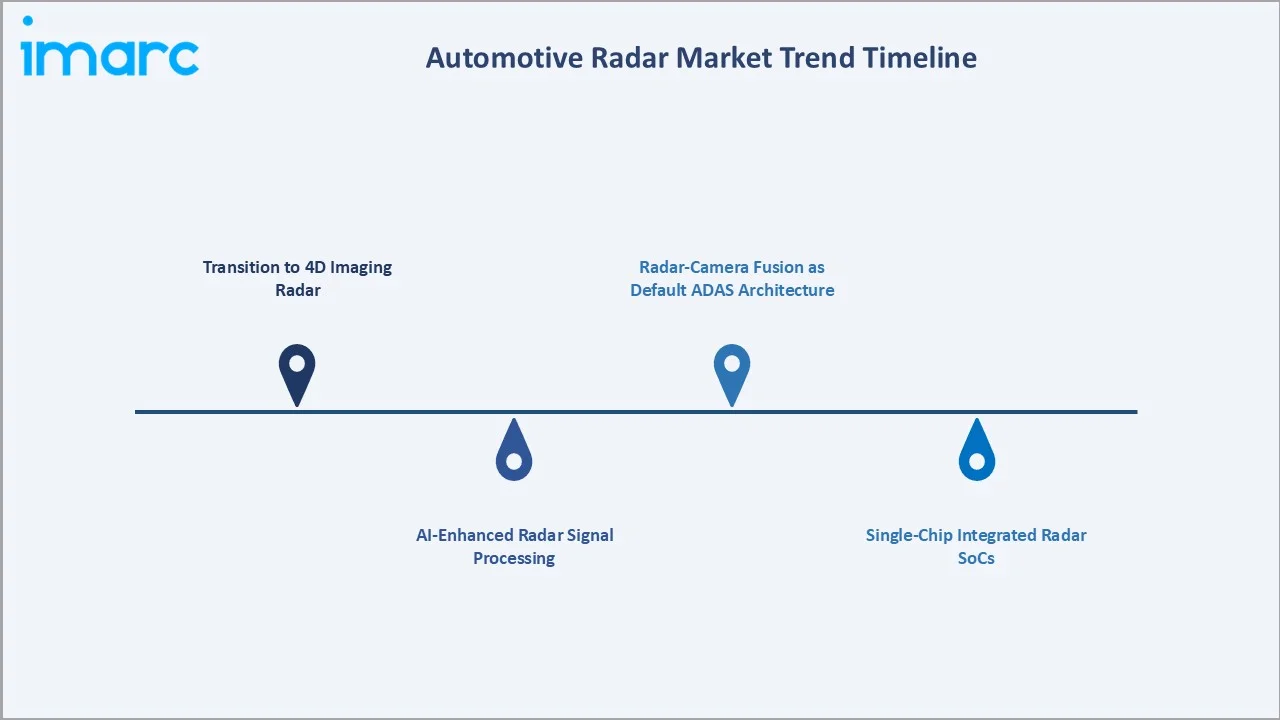

1. Transition to 4D Imaging Radar

The shift from conventional 3D radar to 4D imaging radar, which adds precise elevation measurement and dramatically increased angular resolution, is the defining technology trend of the 2024–2030 period. Aptiv’s FLR4+ imaging radar detects targets up to 300 meters and uses machine learning and sensor fusion to support advanced driver-assistance systems and automated driving.

2. AI-Enhanced Radar Signal Processing

Machine learning algorithms are being integrated into radar signal processing pipelines to improve object classification accuracy, reduce false positives, and enable pedestrian and cyclist differentiation that conventional Doppler radar cannot reliably achieve. NXP Semiconductors' S32R radar processor family integrates on-chip neural network accelerators, enabling AI-enhanced radar classification without external processing hardware.

3. Single-Chip Integrated Radar SoCs

The integration of radar transceiver, baseband processor, and safety microcontroller into a single automotive-grade SoC is reducing radar module cost and size by 40–60% compared to discrete component designs. Infineon Technologies' RASIC family and Texas Instruments' AWR platform exemplify this trend, enabling radar to reach entry-level vehicle price points that were previously economically inaccessible.

4. Radar-Camera Fusion as Default ADAS Architecture

OEMs are transitioning from single-sensor ADAS architectures to radar-camera fusion as the minimum sensor suite for Level 2 compliance. Raytron’s automotive thermal cameras deliver detection ranges of over 300 meters in darkness and low-visibility conditions. The company promotes sensor fusion of thermal imaging with 4D mmWave radar, cameras, and LiDAR to enhance ADAS and autonomous driving, with its technology deployed across 20+ vehicle models and partnerships with 15+ OEMs.

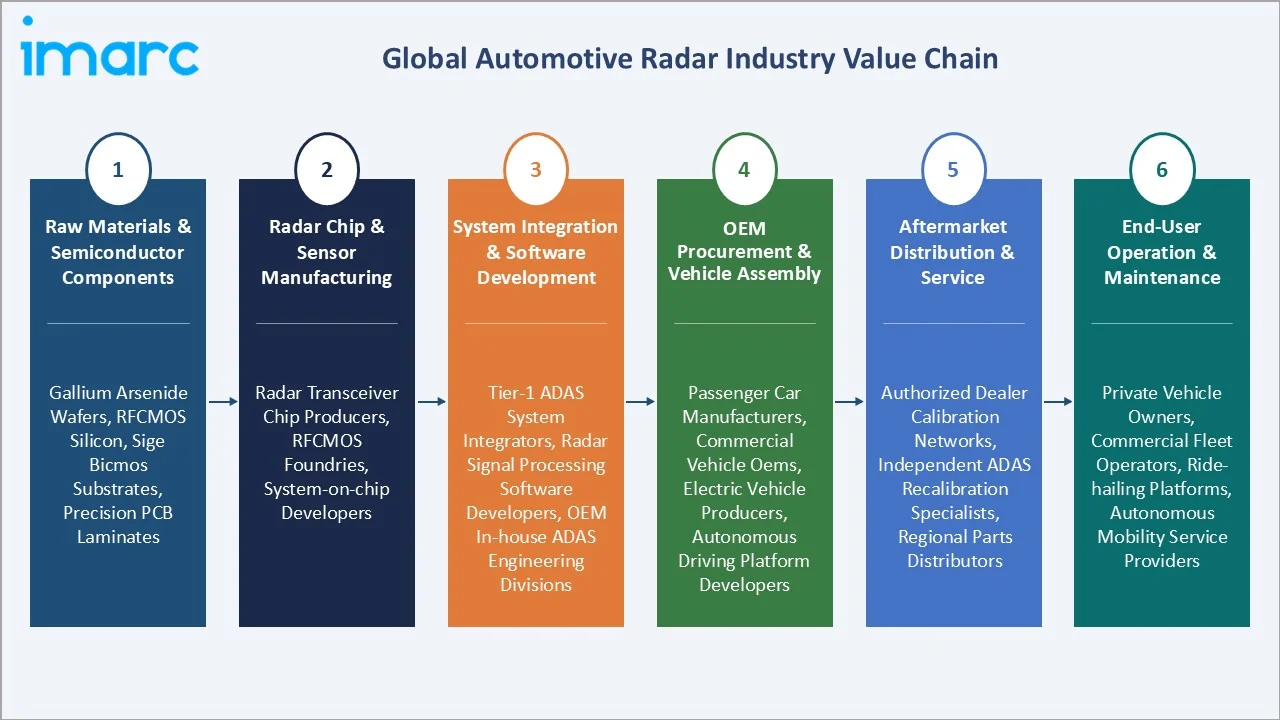

Industry Value Chain Analysis

The automotive radar value chain spans precision semiconductor fabrication through vehicle-level ADAS integration, with each stage requiring highly specialized capabilities in RF engineering, automotive software, and safety system validation.

| Stage | Key Players / Examples |

|---|---|

| Raw Materials & Semiconductor Components | Gallium arsenide wafers, RFCMOS silicon, SiGe BiCMOS substrates, precision PCB laminates |

| Radar Chip & Sensor Manufacturing | Radar transceiver chip producers, RFCMOS foundries, system-on-chip developers |

| System Integration & Software Development | Tier-1 ADAS system integrators, radar signal processing software developers, OEM in-house ADAS engineering divisions |

| OEM Procurement & Vehicle Assembly | Passenger car manufacturers, commercial vehicle OEMs, electric vehicle producers, autonomous driving platform developers |

| Aftermarket Distribution & Service | Authorized dealer calibration networks, independent ADAS recalibration specialists, regional parts distributors |

| End-User Operation & Maintenance | Private vehicle owners, commercial fleet operators, ride-hailing platforms, autonomous mobility service providers |

Technology Landscape in the Automotive Radar Industry

77 GHz Long Range Radar Technology

77 GHz long range radar operates at detection ranges of 150–250 meters with an angular resolution of 1–3°, enabling adaptive cruise control, highway pilot, and automated emergency braking at motorway speeds. The transition from 24 GHz to 77 GHz is complete for all new vehicle program launches in 2025, with 24 GHz systems confined to legacy aftermarket replacements.

Medium and Short Range Radar Technology

Medium range radar (30–80 m) and short range radar (0.2–30 m) operate at 77–81 GHz in modern systems, replacing legacy 24 GHz architectures. These sensors enable blind-spot detection, cross-traffic alert, parking assistance, and lane-change support. Their wider coverage angle, compact form factor, and sub-USD 50 unit cost trajectory make them the mass-market ADAS sensor of choice for volume passenger car programs.

4D Imaging Radar Technology

4D imaging radar adds elevation angle (z-axis) measurement and dramatically increases the number of virtual antenna apertures through MIMO (Multiple Input, Multiple Output) radar architectures, producing point-cloud-density object maps previously only achievable with lidar. Arbe Robotics' Phoenix chip is one of the leading 4D imaging radar architectures entering series production in 2025–2027 model year vehicles.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Range | Medium & Short Range | 57.6% | 2025 |

| Vehicle Type | Passenger Cars | 72.4% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | Asia-Pacific | 54.9% | 2025 |

By Range

Medium and short range radar leads with a 57.6% market share in 2025. These systems are deployed across the widest variety of ADAS applications, blind-spot monitoring, parking assistance, rear cross-traffic alert, and lane-change support, in vehicles across all price segments.

To access detailed market analysis, Request Sample

Long range radar represents 42.4% of the market in 2025 and is growing at the fastest CAGR (~19.50%) of all radar segments. Each incremental advance in vehicle autonomy level requires additional long range radar units per vehicle, creating a powerful content value multiplier. The adoption of Level 2+ and Level 3 highway pilot features by OEMs including Mercedes-Benz, BMW, and Stellantis directly drives long range radar volume growth through 2034.

By Vehicle Type

Passenger cars dominate with a 72.4% share in 2025. The rising global passenger car market and rapid ADAS penetration, driven by mandatory regulation in the EU, US, and China, is translating into guaranteed radar demand growth across all price segments.

Commercial vehicles represent 27.6% of the market in 2025. EU GSR II requirements for advanced AEB, driver monitoring, and lane-keeping systems in heavy commercial vehicles are mandating radar fitment in new trucks and buses.

Regional Market Insights

Asia-Pacific leads global automotive radar demand with a commanding 54.9% market share in 2025. The region's position reflects China's status as the world's largest automotive production market, Japan's globally dominant tier-1 radar sensor supply base, and South Korea's accelerating ADAS adoption driven by Hyundai and Kia's safety-focused product strategy.

Europe's 20.8% share is driven by the region's strictest global vehicle safety regulations. North America at 15.7% is anchored by the US's large passenger car and commercial vehicle market, where NHTSA's AEB mandate and the IIHS's safety ratings program are the primary regulatory demand engines.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| Asia-Pacific | 54.9% | Rapid expansion of the automotive manufacturing sector, rising vehicle production and sales, increasing consumer demand for premium and electric vehicles |

| Europe | 20.8% | Stringent vehicle safety regulations and Euro NCAP rating requirements, strong focus on autonomous and electric vehicle development, increasing penetration of ADAS technologies in mid-range vehicles |

| North America | 15.7% | Strong presence of leading automotive OEMs and Tier-1 suppliers, early adoption of ADAS, supportive regulatory mandates for vehicle safety features |

| Latin America | 4.9% | Gradual expansion of the automotive industry, rising awareness regarding vehicle safety standards, growing middle-class population with increasing vehicle ownership |

| Middle East & Africa | 3.7% | Increasing demand for luxury and premium vehicles, rising infrastructure investments and smart city initiatives, growing focus on road safety regulations |

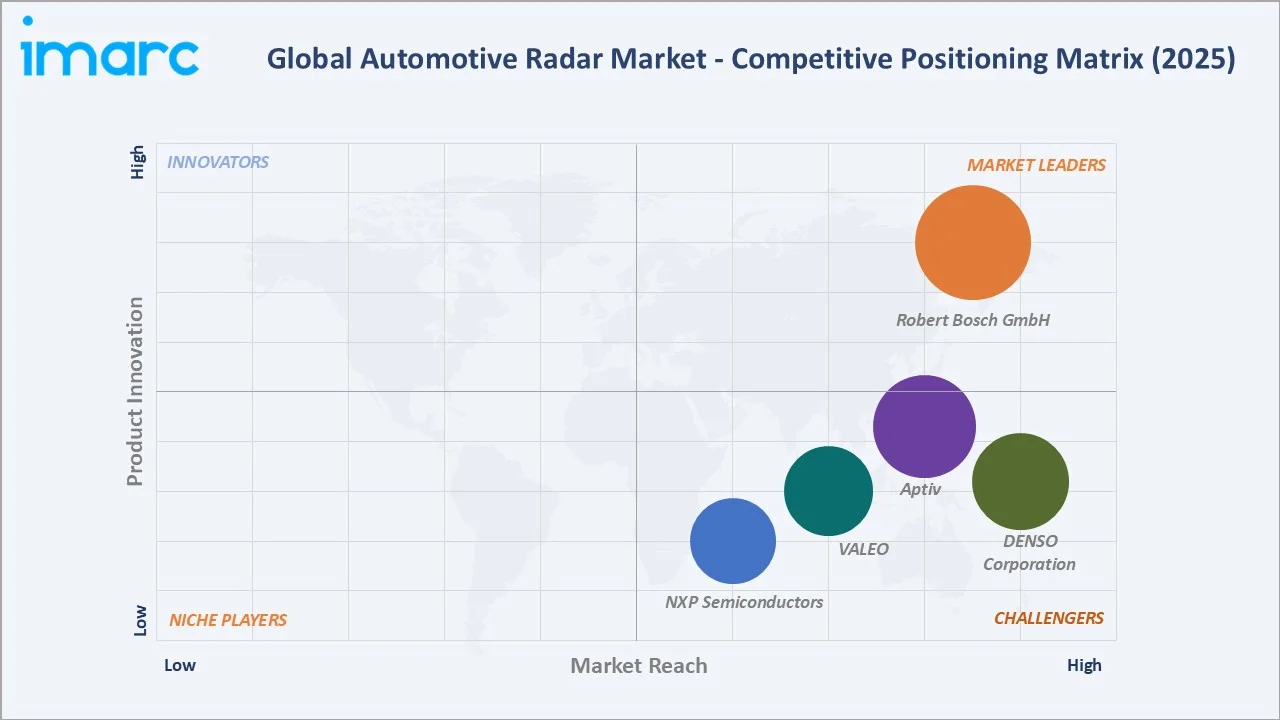

Competitive Landscape

The global automotive radar market is moderately concentrated at the system integration level but highly concentrated at the radar chip level. Robert Bosch GmbH and Aptiv together hold an estimated 45–50% of global OEM automotive radar module revenues in 2025.

| Company Name | Brand Name | Market Position | Core Strength |

|---|---|---|---|

| Robert Bosch GmbH | Bosch | Market Leader | Comprehensive radar product portfolio with broad OEM coverage and advanced platform technology |

| VALEO | Valeo | Challenger | European OEM partnerships, in-cabin radar for occupant sensing |

| Aptiv | Aptiv | Strong Challenger | Advanced radar-camera fusion architecture with broad North American and European OEM coverage |

| DENSO Corporation | DENSO | Strong Challenger | Deep integration within the Toyota ecosystem with strong Asian OEM presence and large-scale manufacturing |

| NXP Semiconductors | NXP | Challenger | Leading radar semiconductor solutions with on-chip AI capabilities, widely adopted by Tier-1 manufacturers |

At the semiconductor layer, NXP Semiconductors, Infineon Technologies, and Texas Instruments collectively supply the radar transceiver chips in approximately 70–75% of automotive radar modules worldwide.

Key Company Profiles

Robert Bosch GmbH

Robert Bosch GmbH is one of the global market leaders in automotive radar systems. The company supplies short, medium, and long range radar modules as well as 4D imaging radar platforms to virtually all major global OEMs.

- Product Portfolio: SRR2 short range radar, MRR Gen5 mid-range radar, LRR4 long range radar, 4D imaging radar for Level 2+ ADAS; integrated radar-ECU solutions for OEM ADAS platforms.

- Recent Developments: In April 2026, Bosch Mobility began Level 3 automated driving testing in China, enabling “hands-off, eyes-off” driving on motorways and urban expressways at speeds of up to 120 km/h.

- Strategic Focus: 4D imaging radar scale-up for Level 3 autonomy, single-chip radar SoC development, AI-enhanced signal processing integration, and OEM co-engineering programs for autonomous vehicle platforms.

Aptiv

Aptiv is a leading global provider of ADAS technologies including radar sensors, sensor fusion platforms, and autonomous driving software. Aptiv's Gen6 radar-camera fusion system represents a key competitive differentiator in the Level 2+ ADAS market.

- Product Portfolio: ESR2.5 long range radar, MRR front-facing mid-range radar, and the SVS (Surround View System) multi-radar integration platform for Level 2+ ADAS applications.

- Recent Developments: In May 2026, Aptiv’s Gen 8 high-resolution radar platform was selected by Volvo Cars for future vehicles beginning in 2028, supporting advanced safety, ADAS, and automated driving functions.

- Strategic Focus: Radar-camera fusion commercialization, autonomous driving software stack integration, North America and European market OEM penetration, and ADAS-as-a-Service software subscription model development.

Market Concentration Analysis

The automotive radar market is moderately concentrated at the module integration level, with Robert Bosch GmbH and Aptiv holding approximately 45–50% of OEM radar module revenues. At the semiconductor level, concentration is much higher, with NXP Semiconductors, Infineon Technologies, and Texas Instruments supplying radar chips used in approximately 70–75% of global radar module production.

Market consolidation is accelerating. FORVIA’s (formerly Faurecia) acquisition of Hella in January 2022 created a combined radar and lighting ADAS player. Aptiv's strategic focus on radar-camera fusion systems is vertically integrating chip, sensor, and software capabilities. New entrants, including Arbe Robotics and Uhnder, are challenging established players specifically in the 4D imaging radar segment, creating competitive disruption at the technology frontier.

Investment & Growth Opportunities

Fastest Growing Segments

Long range radar (~19.50% CAGR), 4D imaging radar (~30%+ CAGR), in-cabin occupant sensing radar, and commercial vehicle radar systems represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental addressable market of approximately USD 18 Billion by 2034 within the global automotive radar ecosystem.

Emerging Market Expansion

India, Brazil, Thailand, and Indonesia collectively represent a USD 3+ Billion incremental automotive radar opportunity by 2034. India's Bharat NCAP program and emerging AEB mandate discussions, Brazil's growing import of Euro-NCAP-rated vehicles, and Southeast Asia's rapid ADAS adoption in Japanese brand models are creating first-generation radar demand across markets that were previously price-constrained.

Venture and Institutional Investment Trends

- 4D imaging radar start-ups have collectively raised USD 500+ Million in venture capital, reflecting institutional conviction in next-generation radar's displacement of lidar in cost-sensitive autonomous vehicle platforms.

- Government safety regulation investment in road safety infrastructure provides regulatory demand certainty that institutional investors view as de-risking the automotive radar market's exceptional 17.07% CAGR trajectory through 2034.

Future Market Outlook (2026-2034)

The automotive radar market is positioned for exceptional, regulation-driven growth through 2034. From USD 7.80 Billion in 2025, the market will reach USD 33.55 Billion by 2034, representing total incremental value creation of USD 25.75 Billion at a 17.07% CAGR. This trajectory is secured by mandatory AEB and ADAS regulations across the world's three largest automotive markets, EU, US, and China, which together represent over 65% of global vehicle production.

The technology landscape will shift decisively toward 4D imaging radar, radar-camera fusion as the standard Level 2 ADAS architecture, and AI-enhanced signal processing by 2034. The transition from 3D to 4D radar represents a 2–3× increase in per-unit content value, creating a powerful ASP tailwind alongside volume growth. In-cabin radar for occupant monitoring will emerge as a significant incremental revenue stream through the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 95 industry participants in 2024–2025, including radar system engineers, ADAS platform architects, automotive OEM procurement managers, fleet safety managers, and institutional investors across Asia-Pacific, Europe, and North America. Expert input validated market sizing, technology adoption timelines, and regulatory demand triggers.

Secondary Research

Secondary research encompassed supplier annual reports, SAE and IEEE automotive radar technical papers, Euro NCAP regulatory documentation, US NHTSA rulemaking records, China GB/T automotive safety standards, OICA vehicle production statistics, and trade publications including Automotive World, SAE Mobilus, and IEEE Spectrum.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting incorporating global vehicle production volumes, radar penetration rates by vehicle type and segment, average radar system selling price trajectories, regulatory mandate timelines, and OEM ADAS platform investment disclosures. A base-case CAGR of 17.07% reflects consensus validated against OEM supply contracts and regulatory implementation schedules.

Automotive Radar Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Ranges Covered | Long Range, Medium and Short Range |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles |

| Applications Covered | Adaptive Cruise Control (ACC), Autonomous Emergency Braking (AEB), Blind Spot Detection (BSD), Forward Collision Warning (FCW), Intelligent Park Assist, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Robert Bosch GmbH, VALEO, Aptiv, DENSO Corporation, NXP Semiconductors, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive radar market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive radar market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive radar industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Radar Market Report

The market reached USD 7.80 Billion in 2025 and is projected to grow to USD 33.55 Billion by 2034 at a 17.07% CAGR.

Asia-Pacific leads with a 54.9% share in 2025, driven by China's large vehicle production base and rising safety mandates.

Medium and short range radar leads with a 57.6% share in 2025, widely deployed in blind-spot detection, parking, and lane-change assist applications.

Passenger cars dominate with a 72.4% share in 2025, driven by mandatory ADAS regulation and rapid radar fitment across all price segments.

Robert Bosch GmbH, VALEO, Aptiv, DENSO Corporation, and NXP Semiconductors, are some of the key players.

Mandatory ADAS safety regulations, autonomous vehicle development, rising consumer safety awareness, and OEM ADAS platform integration mandates are the primary drivers.

High system cost in entry-level vehicles, signal interference in urban environments, and cybersecurity concerns are key challenges.

4D imaging radar, growing at an estimated 30%+ CAGR, is the fastest evolving technology segment, enabling lidar-quality object classification at radar cost levels.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)