Automotive Steering System Market Size, Share, Trends and Forecast by Type, Component, Vehicle Type, and Region, 2026-2034

Automotive Steering System Market Size, Share, Trends & Forecast (2026-2034)

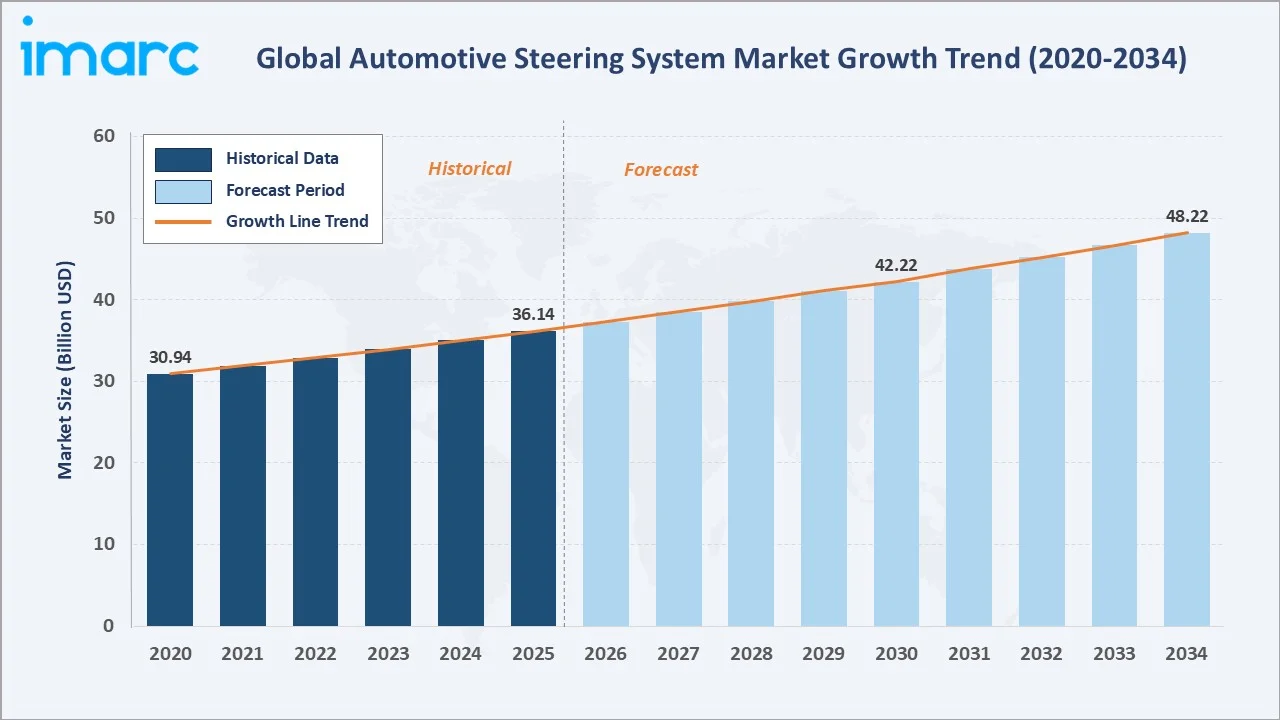

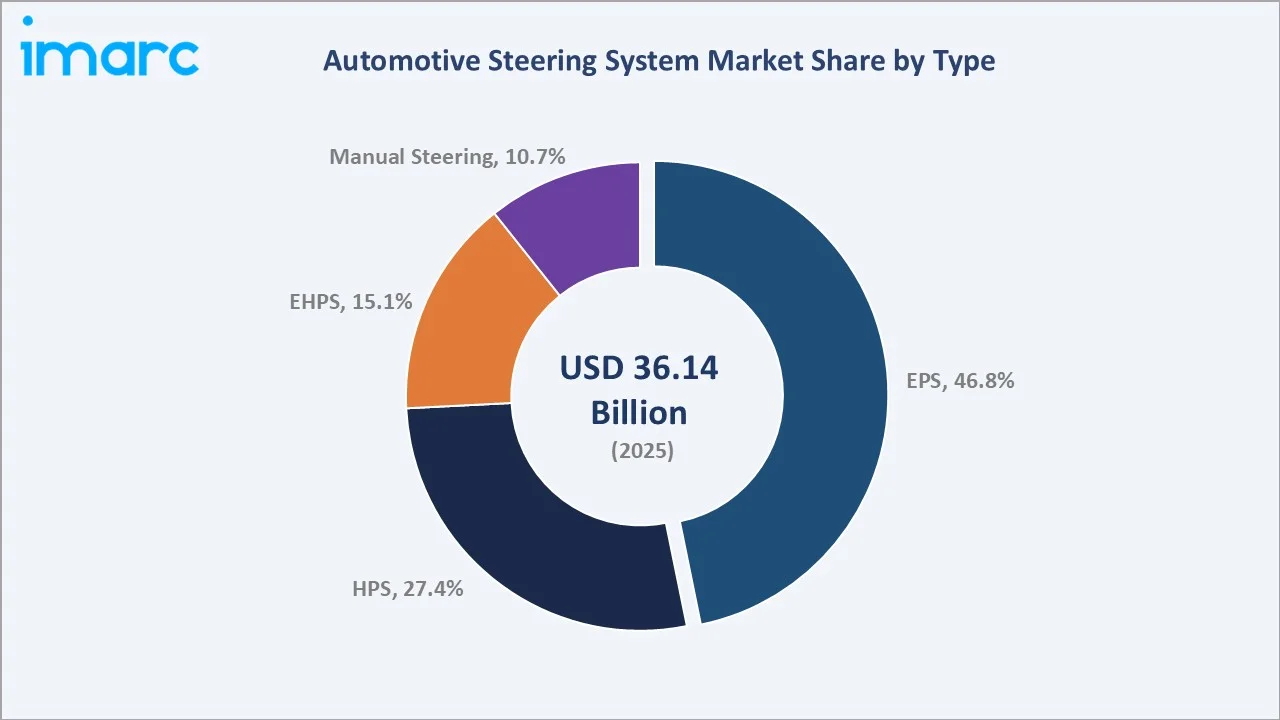

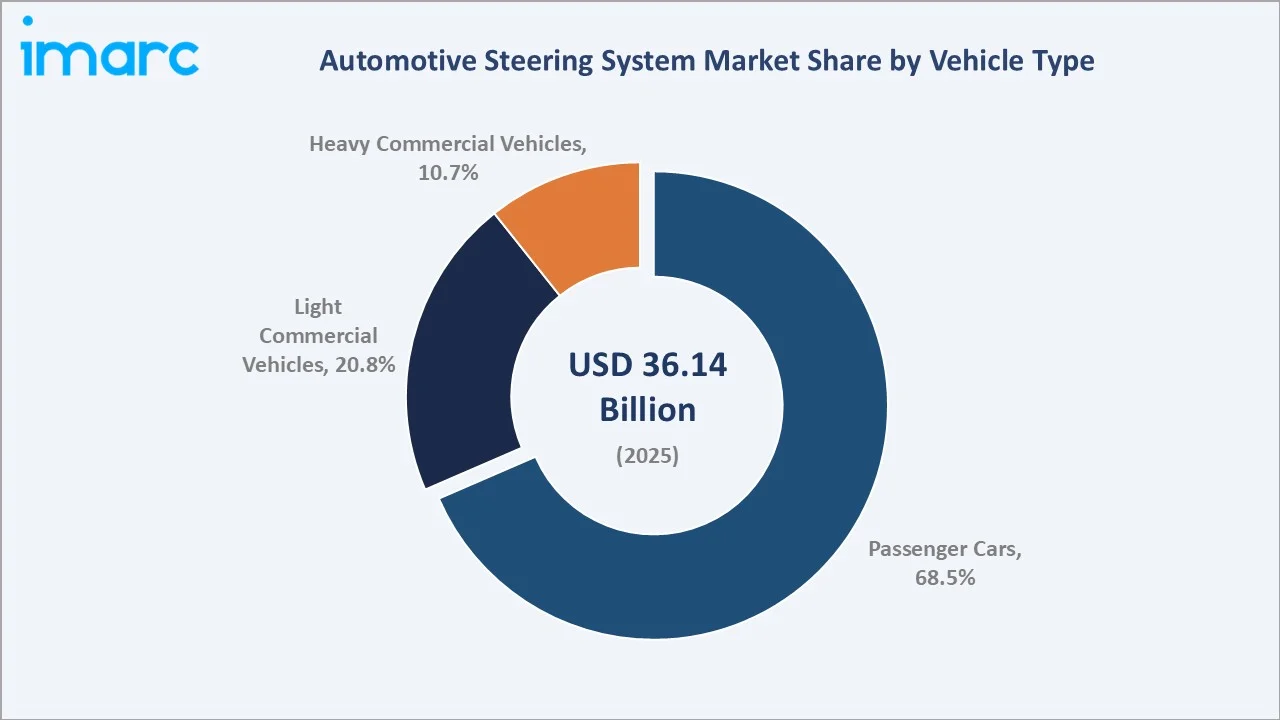

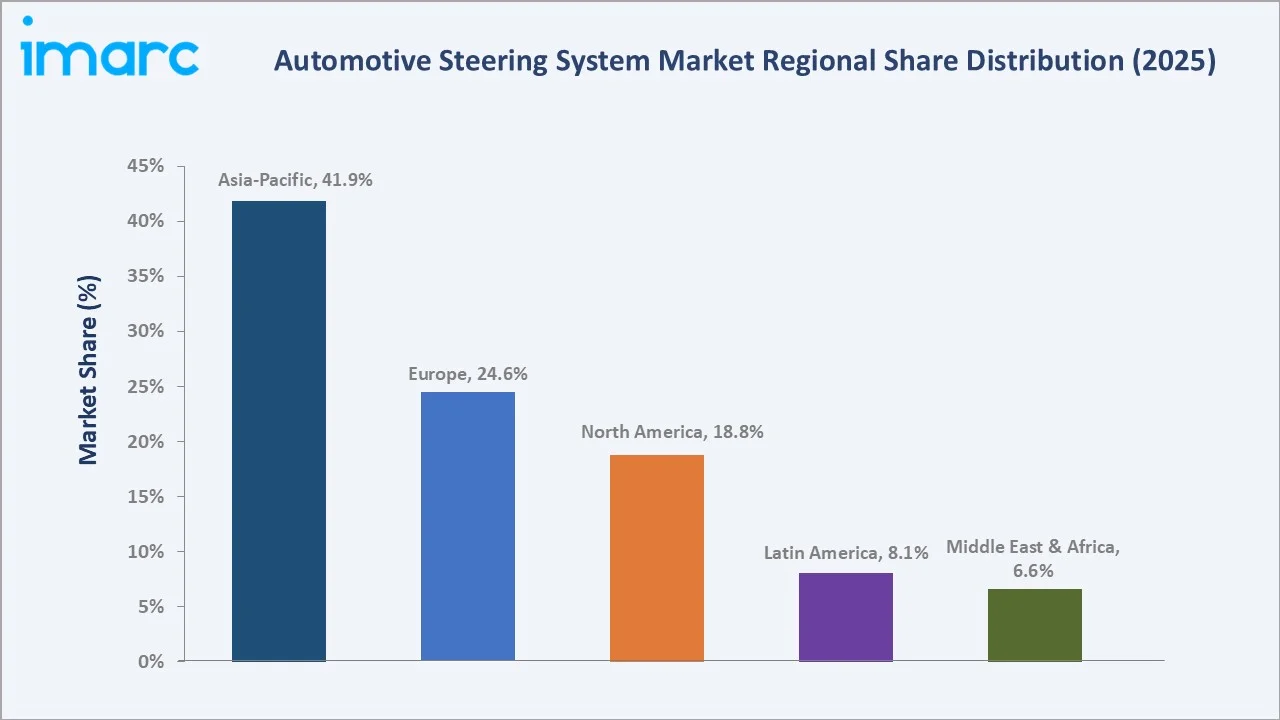

The global automotive steering system market reached USD 36.14 Billion in 2025 and is projected to reach USD 48.22 Billion by 2034, growing at a CAGR of 3.16% during 2026-2034. The market is driven by rising vehicle production, growing demand for advanced driver-assistance systems, and increasing adoption of electric power steering for better fuel efficiency. According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle sales reached nearly 99.8 million units in 2025, reflecting a 4.7% increase compared to 95.3 million units sold in 2024. This growth in vehicle sales is driving the automotive steering system market by increasing the demand for steering components and systems across passenger and commercial vehicles, while also supporting the adoption of advanced steering technologies in newly manufactured vehicles. Electric power steering (EPS) dominates at 46.8%. Passenger cars lead the vehicle type at 68.5%. Asia-Pacific commands 41.9% of the global market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 36.14 Billion |

| Forecast Market Size (2034) | USD 48.22 Billion |

| CAGR (2026-2034) | 3.16% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Type | Electric Power Steering - EPS (46.8%, 2025) |

| Dominant Vehicle Type | Passenger Cars (68.5%, 2025) |

| Leading Region | Asia-Pacific (41.9%, 2025) |

The market expanded from USD 30.94 Billion in 2020 to USD 36.14 Billion in 2025, anchored at USD 42.22 Billion in 2030, and forecast to reach USD 48.22 Billion by 2034. The COVID-19 pandemic's disruption of automotive production created a temporary market contraction. Still, the semiconductor shortage-driven production recovery of 2021-2024 and the acceleration of EV penetration have created a sustained structural shift from HPS to EPS that permanently elevates the market's average per-vehicle steering system content value above pre-pandemic levels.

To get more information on this market, Request Sample

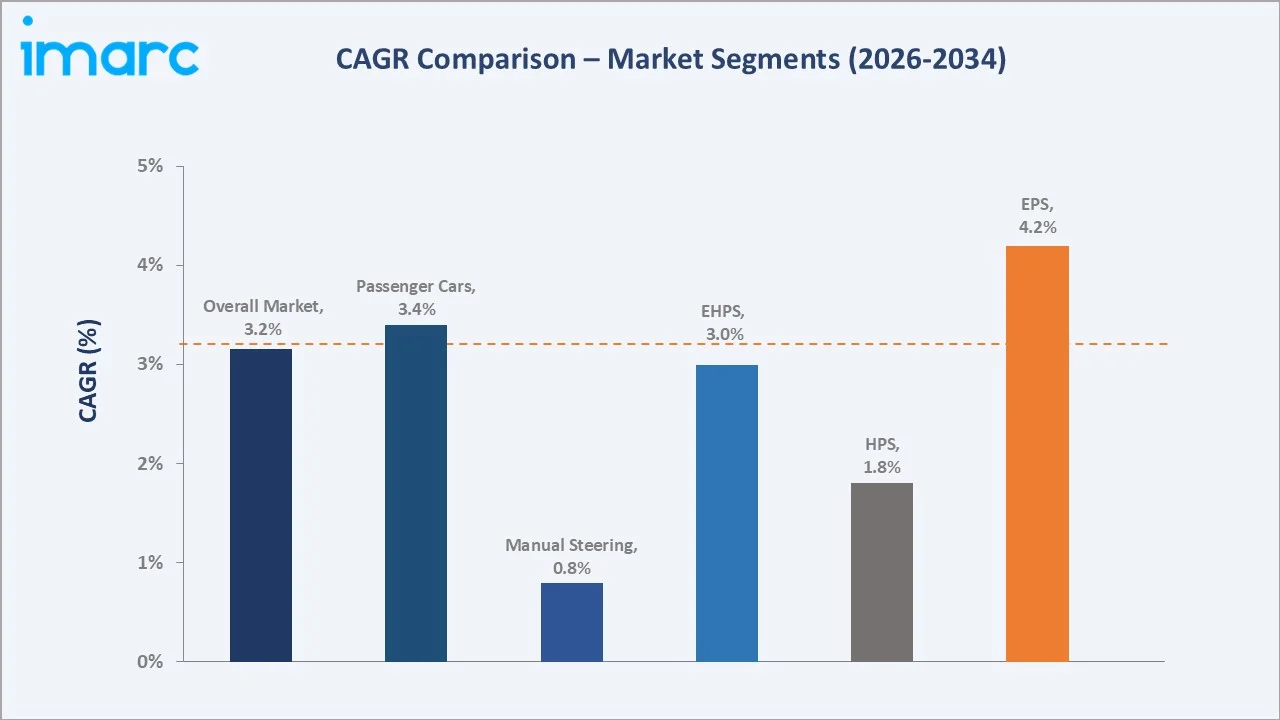

EPS grows fastest at ~4.2% CAGR as it is widely preferred in battery electric passenger vehicles because of its energy efficiency and electronic controllability, and as ADAS lane-keeping assist, automated parking, and highway driving assistance systems require electronically controllable steering torque overlay that EPS can provide.

Executive Summary

The global automotive steering system market reached USD 36.14 Billion in 2025, representing the most commercially significant steering technology transition period in the industry's history. The systematic replacement of hydraulic power steering (HPS) technology that dominated since the 1950s with electric power steering (EPS) that eliminates the engine-driven hydraulic pump, reduces fuel consumption, enables ADAS integration, and provides the foundational electronically controlled steering actuation required for steer-by-wire and autonomous driving architectures. The market is projected to reach USD 48.22 Billion by 2034.

Electric power steering at 46.8% leads by market value through its premium system content per vehicle and the highest CAGR driven by EV architecture requirements and ADAS integration. Passenger cars at 68.5% dominate vehicle type demand through the world's passenger car production volume, each requiring a steering system as a mandatory safety-critical component. Asia-Pacific at 41.9% leads globally through China, Japan, South Korea, and India's combined vehicle production volume, representing high global automotive output and housing the world's dominant EPS manufacturers.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Type | Electric Power Steering (EPS) - 46.8% share (2025) |

| Dominant Vehicle Type | Passenger Cars - 68.5% market share (2025) |

| Leading Region | Asia-Pacific - 41.9% market share (2025) |

| Market Opportunity | Steer-by-wire for autonomous vehicles; EPS for EV platforms; ADAS-integrated active steering; Asia-Pacific OEM volume growth; aftermarket EPS retrofit; commercial vehicle EPS adoption |

Key Analytical Observations Supporting the Above Data:

- Electric Power Steering (EPS) at 46.8%: The Electric Power Steering (EPS) segment dominates the market due to its fuel efficiency, lower weight, reduced maintenance, and compatibility with ADAS and electric vehicles. Its growing use in passenger cars and EVs continues to strengthen its market share.

- Passenger Cars at 68.5%: The passenger cars segment dominates the market due to high global passenger vehicle production and sales. Rising demand for comfort, safety, fuel efficiency, and advanced steering technologies in cars further supports segment growth.

- Asia Pacific at 41.9%: Asia Pacific dominates regionally due to large-scale vehicle production and sales in China, India, Japan, and South Korea. The region’s growing EV adoption, expanding automotive manufacturing base, and rising demand for passenger cars further support its lead.

Automotive Steering System Market Overview

The global automotive steering system market encompasses all steering mechanism technologies installed in new motor vehicles at the OEM level, from the steering input device through the steering column and intermediate shaft to the steering gear and steering linkage. The market includes the complete power steering assist system in EPS, HPS, and EHPS. The aftermarket for steering system replacement components, remanufactured steering racks, EPS ECU reprogramming, and steering system calibration services represents an additional market layer that complements the OEM new vehicle installation market.

The ecosystem integrates steering system manufacturers, component suppliers, OEM vehicle manufacturers, regulatory and safety bodies, and aftermarket channels. Macroeconomic factors include rising disposable incomes, urbanization, expanding vehicle ownership, and growth in automotive production.

Market Dynamics

To evaluate market opportunities, Request Sample

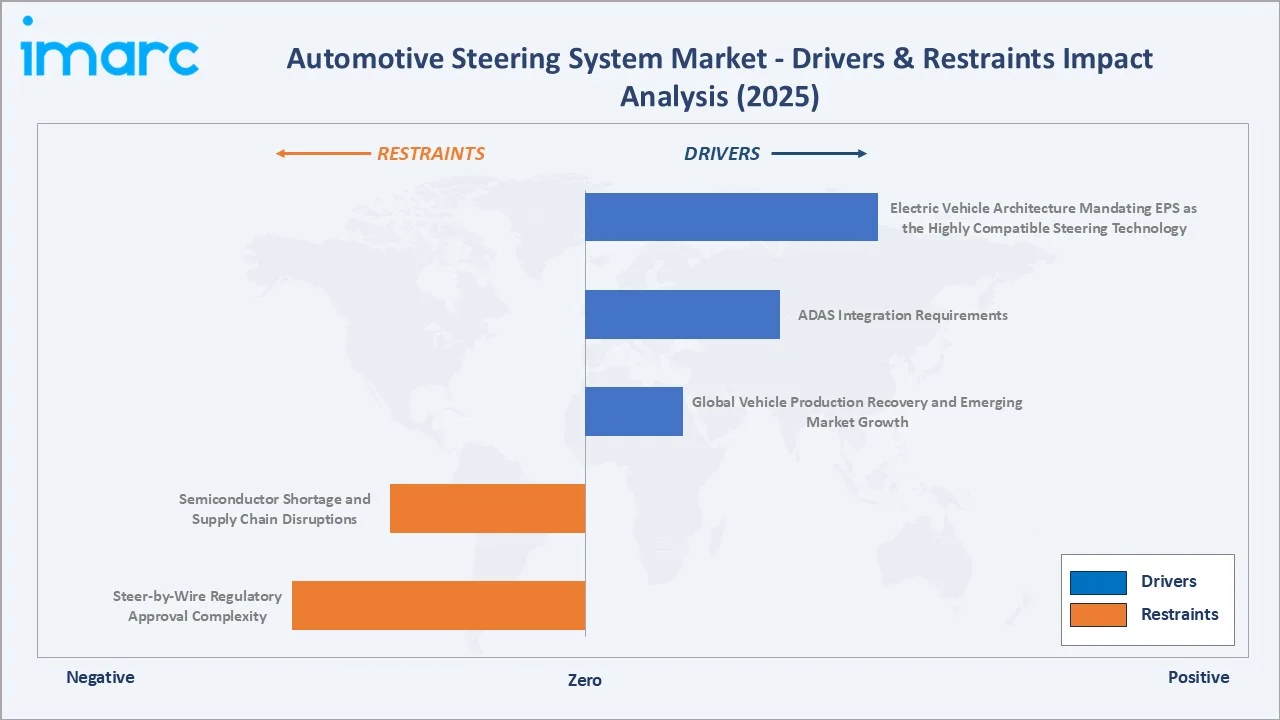

Market Drivers

- Electric Vehicle Architecture Mandating EPS as the Highly Compatible Steering Technology: Electric vehicle (EV) architecture is driving the market as Electric Power Steering (EPS) is the preferred and most compatible steering technology for EVs due to its lower energy consumption and absence of hydraulic components. EPS supports efficient battery utilization by operating only when steering assistance is required, improving overall vehicle efficiency. In addition, EV platforms increasingly integrate advanced features such as ADAS and autonomous driving systems, which rely on EPS for precise electronic control. The rapid expansion of EV production is therefore accelerating demand for EPS-based steering systems globally.

- ADAS Integration Requirements: ADAS integration requirements are driving the market demand as advanced features such as lane-keeping assist, automated parking, lane centering, and autonomous driving require electronically controlled steering systems for precise vehicle movement. Electric Power Steering (EPS) enables real-time steering adjustments and seamless communication with sensors and control units used in ADAS. Increasing consumer demand for vehicle safety and stricter government safety regulations are accelerating ADAS adoption. This, in turn, is boosting the demand for advanced steering technologies across modern vehicles.

- Global Vehicle Production Recovery and Emerging Market Growth: Global vehicle production recovery and growth in emerging markets are increasing overall vehicle manufacturing volumes and demand for steering components. According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle sales reached nearly 99.8 million units in 2025, higher than in 2024 (95.3 million units). The rebound in automotive production after supply chain disruptions, along with rising vehicle ownership in emerging economies such as China, India, Brazil, and Southeast Asian countries, is supporting market expansion. Rapid urbanization, improving income levels, and infrastructure development are further boosting passenger and commercial vehicle sales. This growth directly increases the adoption of steering systems across vehicle segments.

Market Restraints

- Semiconductor Shortage and Supply Chain Disruptions: Semiconductor shortages and supply chain disruptions are delaying the production of electronically controlled systems such as EPS and steer-by-wire. Limited chip availability affects sensors, control units, and ADAS-compatible steering modules. Rising raw material costs and logistics delays also increase manufacturing expenses. As a result, vehicle production slowdowns and longer delivery timelines restrict market growth.

- Steer-by-Wire Regulatory Approval Complexity: Steer-by-wire regulatory approval complexity hampers the market because the technology removes mechanical steering linkage, making safety validation more demanding. Manufacturers must prove fail-safe performance, redundancy, cybersecurity, and reliability under all driving conditions. Lengthy certification and varying regulations across countries delay commercialization. This slows wider adoption of steer-by-wire systems and limits near-term market growth.

Market Opportunities

- Steer-by-Wire Commercialization for Level 3-5 Autonomous Vehicles: Steer-by-wire commercialization offers a major opportunity as Level 3–5 autonomous vehicles require fully electronic, software-controlled steering. It enables faster response, flexible cabin design, weight reduction, and better integration with ADAS and autonomous driving systems. As automakers advance toward higher automation levels, demand for steer-by-wire technology is expected to increase. This creates growth opportunities for suppliers of sensors, actuators, control units, and redundant safety systems.

- Active Rear-Axle Steering Expansion from Premium to Mainstream Vehicle Segments: Active rear-axle steering offers an opportunity as it is moving beyond premium vehicles into mainstream models. It improves maneuverability at low speeds and stability at high speeds, enhancing comfort and safety. As consumers seek better driving performance, automakers are adding this feature to wider vehicle ranges. This creates new demand for advanced steering actuators, sensors, and control systems.

Market Challenges

- China EPS Market Domestic Supplier Development Creating Price Pressure on International Tier-1 Suppliers: China’s growing domestic EPS supplier base is creating price pressure on global Tier-1 suppliers by offering cost-competitive steering solutions. This challenges international players’ margins, reduces pricing power, and increases competition in one of the world’s largest automotive markets.

- HPS Installed Base Aftermarket Complexity During Technology Transition Creating Service Network Investment: The large installed base of Hydraulic Power Steering (HPS) systems creates aftermarket complexity as the industry shifts toward EPS and steer-by-wire technologies. Service networks must support both legacy hydraulic systems and newer electronic steering systems, requiring additional tools, training, and spare parts inventory. This increases operational costs for workshops and suppliers. The need for continued investment in service infrastructure can slow profitability and create challenges during the technology transition.

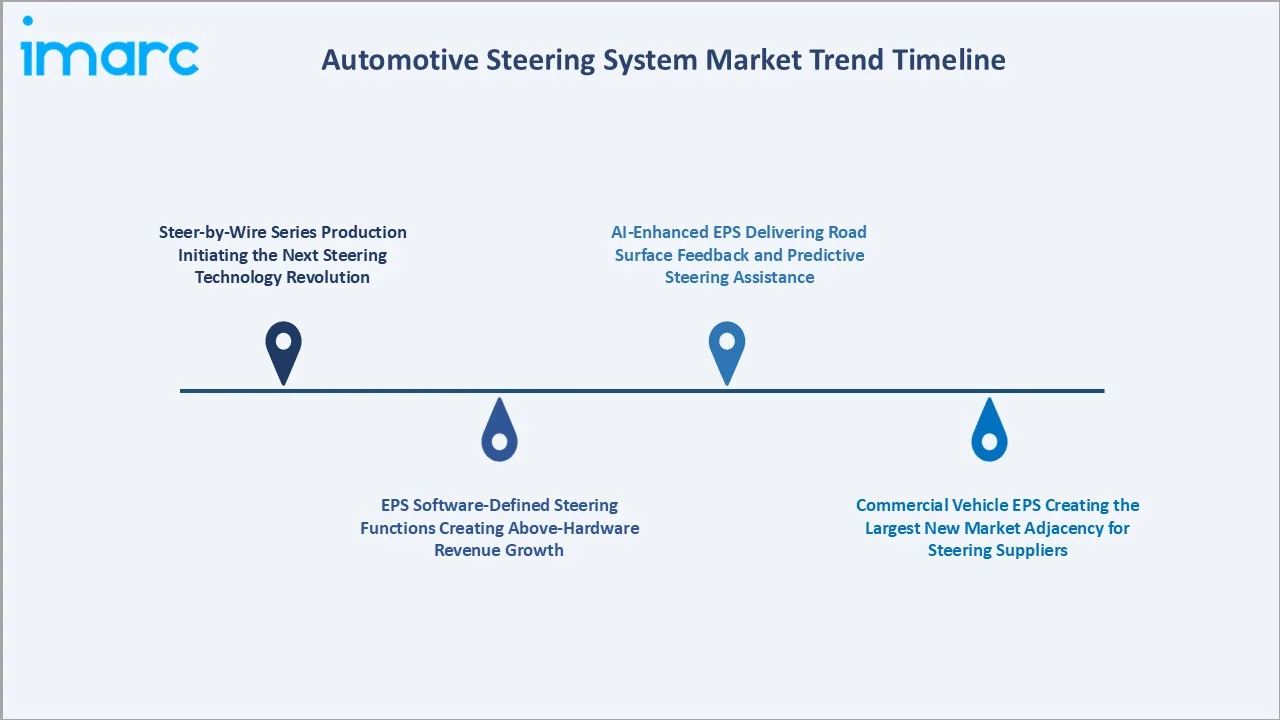

Emerging Market Trends

1. Steer-by-Wire Series Production Initiating the Next Steering Technology Revolution

Steer-by-wire series production replaces mechanical steering links with fully electronic control. This enables lighter vehicle design, better packaging flexibility, and seamless integration with ADAS and autonomous driving systems. Automakers are increasingly adopting it to improve steering precision, safety redundancy, and cabin design freedom. As production scales up, steer-by-wire is expected to shape the next phase of steering technology innovation. In April 2026, Nexteer Automotive supported a major Chinese new energy vehicle (NEV) manufacturer in launching the world’s first mass-produced passenger vehicle equipped with a fully drive-by-wire chassis. The vehicle integrates Nexteer’s steer-by-wire (SbW) system, which plays a crucial role in enabling the advanced platform architecture. It highlights the industry’s transition toward electronically controlled steering systems that support autonomous driving, improve vehicle design flexibility, and accelerate next-generation steering innovation in the automotive steering system market.

2. EPS Software-Defined Steering Functions Creating Above-Hardware Revenue Growth

EPS software-defined steering performance can now be enhanced through software, not just hardware upgrades. Automakers can offer features such as variable steering feel, lane-centering support, parking assist, and drive-mode-based steering customization. This creates new revenue opportunities through software updates, feature subscriptions, and premium steering functions. As vehicles become more connected and software-driven, EPS systems are evolving into value-generating electronic platforms.

3. Commercial Vehicle EPS Creating the Largest New Market Adjacency for Steering Suppliers

Commercial vehicle EPS is emerging as trucks, buses, and vans shift from hydraulic steering to electric power steering. EPS improves fuel efficiency, reduces maintenance, and supports driver-assistance features in heavy-duty applications. This creates a large new growth area for steering suppliers beyond passenger cars. As commercial fleets electrify and adopt ADAS, demand for advanced EPS systems is expected to rise.

4. AI-Enhanced EPS Delivering Road Surface Feedback and Predictive Steering Assistance

AI-enhanced EPS enables steering systems to analyze road conditions, driver behavior, and sensor data in real time. It can deliver improved road-surface feedback, smoother steering response, and predictive assistance during cornering, lane changes, or uneven terrain. This enhances safety, comfort, and driving precision. As vehicles become more intelligent, AI-based EPS is creating new value in advanced steering systems.

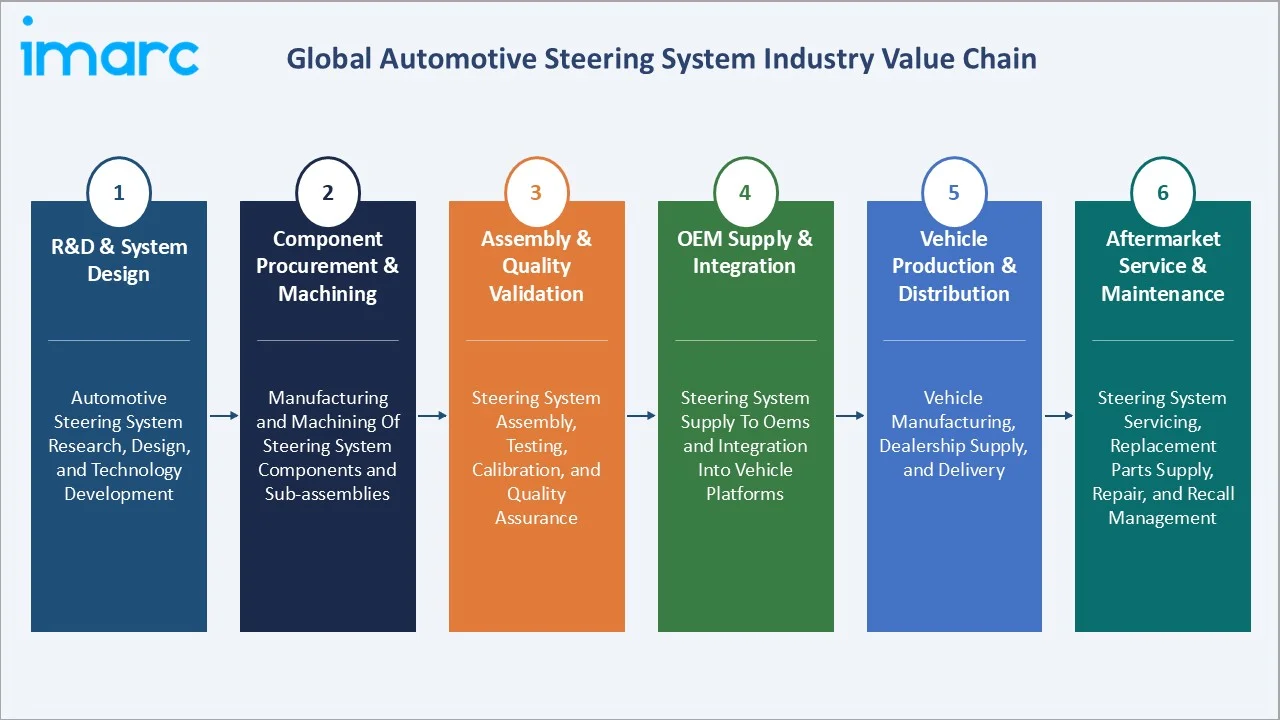

Industry Value Chain Analysis

The automotive steering system value chain integrates R&D and system design, component procurement and machining, assembly and quality validation, OEM supply and integration, vehicle sales and delivery, and aftermarket service and recall management. The value chain's commercial structure is dominated by a small number of large Tier-1 steering system manufacturers who perform most stages in-house or through captive supply relationships.

| Stage | Key Participants |

|---|---|

| R&D & System Design | Automotive steering system research, design, and technology development |

| Component Procurement & Machining | Manufacturing and machining of steering system components and sub-assemblies |

| Assembly & Quality Validation | Steering system assembly, testing, calibration, and quality assurance |

| OEM Supply & Integration | Steering system supply to OEMs and integration into vehicle platforms |

| Vehicle Production & Distribution | Vehicle manufacturing, dealership supply, and delivery |

| Aftermarket Service & Maintenance | Steering system servicing, replacement parts supply, repair, and recall management |

The OEM supply and integration tier represents the steering value chain's most commercially sensitive stage. EPS system specification, validation, and approval by OEM vehicle engineers creates a 2-5 year development cycle from initial supplier selection to production start, creating a high switching cost that makes OEM relationships inherently long-term.

Technology Landscape in the Automotive Steering System Industry

Electric Power Steering Technology

In March 2026, TERREPOWER expanded its North American Electric Power Steering (EPS) portfolio. The company introduced next-generation EPS technology aimed at simplifying repair processes for technicians, adding 60 new applications covering model years 2013–2025. This expansion increases its portfolio to more than 257 SKUs serving around 60 million vehicles in operation, with an additional 76 SKUs planned for launch covering another 21 million vehicles. This development supports electric power steering (EPS) technology growth by expanding aftermarket availability and service support for EPS-equipped vehicles. The broader product coverage improves replacement accessibility, strengthens maintenance infrastructure, and accelerates EPS adoption across a larger vehicle parc, reinforcing the transition from hydraulic steering systems to electric steering technologies.

Steer-by-Wire Technology

Steer-by-Wire (SbW) technology replaces mechanical steering connections with fully electronic control systems. It enables improved steering precision, reduced vehicle weight, and greater flexibility in vehicle design and cabin architecture. SbW also supports seamless integration with ADAS, autonomous driving, and software-defined vehicle platforms. Its commercialization is accelerating the shift toward intelligent, connected, and next-generation steering technologies.

Hydraulic and Electro-Hydraulic Systems

Hydraulic power steering (HPS) and electro-hydraulic power steering (EHPS) systems serve as transitional technologies between traditional mechanical steering and fully electric systems. HPS remains widely used in heavy-duty and commercial vehicles due to its high load-handling capability and durability. EHPS improves efficiency by combining hydraulic assistance with electronic control, offering better fuel economy and steering performance. These technologies continue to support legacy vehicle platforms and specific applications where full EPS adoption is still evolving.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Electric Power Steering (EPS) | 46.8% | 2025 |

| Component | 🔒 | 🔒 | 2025 |

| Vehicle Type | Passenger Cars | 68.5% | 2025 |

| Region | Asia-Pacific | 41.9% | 2025 |

By Type

Electric power steering (EPS) leads at 46.8% market share (2025). EPS encompasses column-type (low-to-mid-size passenger cars), rack-type (larger passenger cars and crossovers), dual-pinion (compact and mid-size vehicles), and emerging steer-by-wire production.

To access detailed market analysis, Request Sample

Hydraulic power steering (HPS) at 27.4% retains significant market value through commercial vehicle applications and remaining ICE passenger car platforms. Electro-hydraulic power steering (EHPS) at 15.1% serves the transition segment for higher-assist force requirements. Manual steering is at 10.7% confined to commercial vehicles, off-road, and budget economy applications.

By Vehicle Type

Passenger cars lead at 68.5% market share (2025). Passenger car steering encompasses the full technology spectrum from column EPS in economy hatchbacks to dual-motor SbW in luxury EVs, with the highest rate of EPS adoption and the highest average per-vehicle steering content value growth driven by ADAS integration and active steering function adoption.

Light commercial vehicles at 20.8% serve the pickup truck, van, and minibus segment, where EPS adoption is accelerating through electrification and ADAS. Heavy commercial vehicles at 10.7% represent the largest remaining HPS and EHPS application, with EPS transition beginning through emerging competitors in Class 8 trucks.

Regional Market Insights

| Region | Share (2025) | Key Automotive Steering System Market Drivers & Characteristics |

|---|---|---|

| Asia-Pacific | 41.9% | Driven by its large vehicle production base, growing EV adoption, and strong automotive manufacturing ecosystem across major economies. |

| Europe | 24.6% | Driven by high penetration of EPS, ADAS integration, vehicle electrification, and strong regulatory focus on safety and emissions. |

| North America | 18.8% | Supported by high vehicle ownership, increasing demand for advanced steering technologies, and growing adoption of autonomous and connected vehicles. |

| Latin America | 8.1% | Driven by improving vehicle production, rising passenger vehicle demand, and the gradual modernization of automotive manufacturing capabilities. |

| Middle East and Africa | 6.6% | Supported by growing automotive demand, infrastructure development, and increasing adoption of passenger and commercial vehicles across developing economies. |

Asia-Pacific, at 41.9%, leads the market by the world's largest vehicle production cluster and houses the dominant EPS Tier-1 suppliers. Europe, at 24.6%, reflects the highest EPS content per vehicle globally and the concentration of EPS technology innovators in Germany. North America, at 18.8%, is distinguished by full-size light truck EPS leadership and SbW production pioneers.

Latin America, at 8.1%, reflects Brazil and Mexico's OEM manufacturing integration with global platforms alongside Brazil's domestic entry-segment EPS adoption transition. MEA, at 6.6%, encompasses GCC premium SUV high-value EPS content, OEM manufacturing contribution, and South Africa's automotive industry.

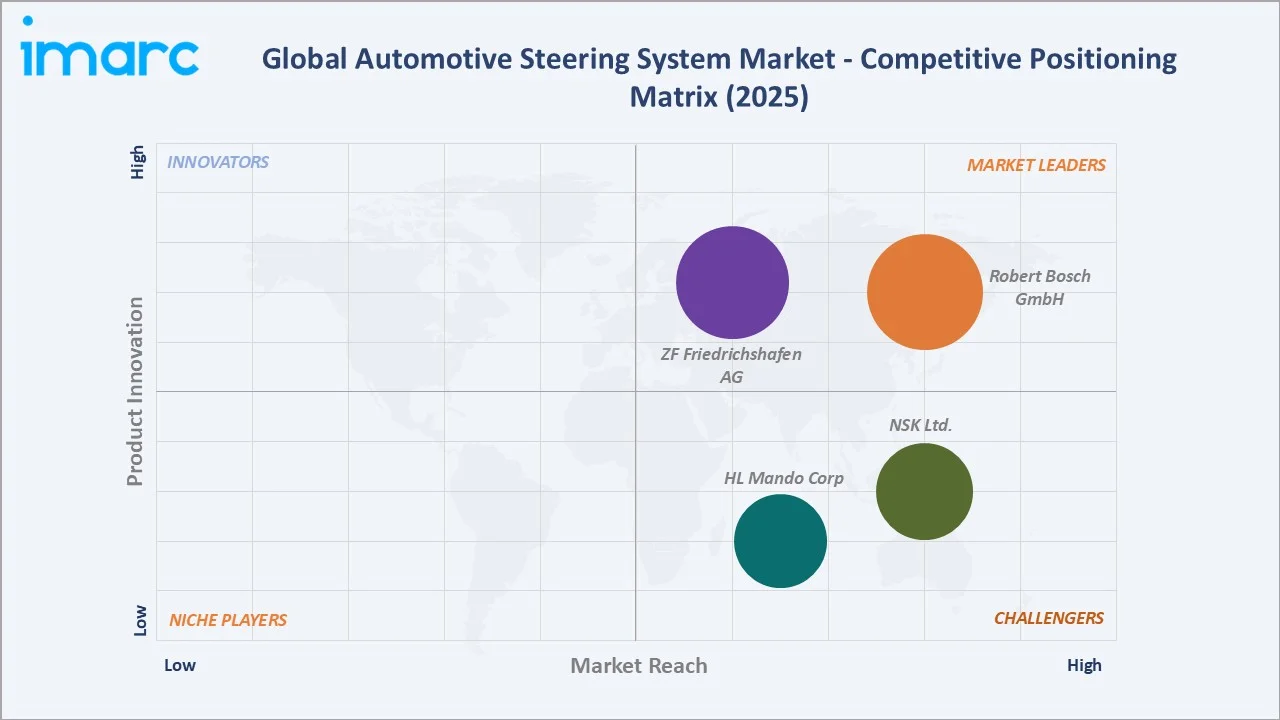

Competitive Landscape

The automotive steering system market's competitive landscape is highly concentrated at the Tier-1 full-system level, with Robert Bosch GmbH, ZF Friedrichshafen AG, NSK Ltd., and HL Mando Corp, together accounting for approximately 70-80% of global EPS and steering system revenue. This concentration reflects the multi-decade OEM qualification relationships, billion-dollar manufacturing footprints, and proprietary technology IP that define Tier-1 steering system supply.

| Company Name | Key Products | Market Position | Core Strength |

|---|---|---|---|

| Robert Bosch GmbH | Rear axle steering system, Servotwin electro-hydraulic steering system | Market Leader | Robert Bosch GmbH is a leading player in the automotive industry, specializing in advanced electric power steering (EPS) and steer-by-wire systems. |

| ZF Friedrichshafen AG | Belt Drive EPS systems, Steer-by-Wire Systems | Market Leader | ZF Friedrichshafen AG is a global leader in automotive steering systems, supplying advanced, modular solutions for passenger cars and commercial vehicles. |

| NSK Ltd. | Column Type Electric Power Steering, Pinion Type Electric Power Steering | Challenger | NSK Ltd. specializes in Electric Power Steering (EPS) systems, column-type EPS, pinion type, and advanced steer-by-wire technologies. |

| HL Mando Corp | R-EPS (Rack Type Electric Power Steering) | Challenger | HL Mando Corp specializes in advanced steering systems, including Electric Power Steering (EPS) and steer-by-wire technology. |

The competitive dynamic between Japan-headquartered suppliers and European suppliers is fundamentally shaped by their respective OEM anchor relationships.

Key Company Profiles

Robert Bosch GmbH

Robert Bosch GmbH is a leading global automotive technology supplier and a prominent player in the automotive steering system market. The company provides advanced steering solutions, including Electric Power Steering (EPS) systems, steering columns, sensors, control units, and software-enabled steering technologies for passenger and commercial vehicles. Bosch focuses on supporting vehicle electrification, ADAS integration, and autonomous driving applications through intelligent steering platforms.

- Key Products: Rear axle steering system, Servotwin electro-hydraulic steering system.

- Strategic Focus: Focuses on advanced EPS, steer-by-wire, ADAS-ready steering, and software-defined mobility solutions to support electrified and autonomous vehicles.

ZF Friedrichshafen AG

ZF Friedrichshafen AG is strongly focused on developing intelligent steering technologies that support vehicle electrification, ADAS integration, and autonomous driving. The company is advancing software-controlled steering systems and has been actively involved in commercializing steer-by-wire solutions to enable next-generation vehicle architectures.

- Key Products: Belt Drive EPS systems, Steer-by-Wire Systems.

- Recent Developments: In February 2026, ZF Friedrichshafen AG aims to at least double its revenue in India by the end of the decade, with the company positioning India as both a key growth market and an important global sourcing and export hub. In India, ZF supplies a broad portfolio of automotive components across multiple vehicle applications, including active and passive safety systems, steering systems, clutches, axles, suspension components, powertrains, chassis systems, transmissions, and related safety technologies.

- Strategic Focus: Focuses on advanced EPS, steer-by-wire, rear-axle steering, and autonomous driving-compatible steering technologies to support next-generation mobility solutions.

Market Concentration Analysis

The automotive steering system market is highly concentrated at the Tier-1 full-system level, with Robert Bosch GmbH, ZF Friedrichshafen AG, NSK Ltd., and HL Mando Corp together holding approximately 70-80% of global EPS market revenue. This concentration reflects the 5-10 year OEM qualification cycles that create relationship stickiness, the USD 200-500 Million manufacturing investments required for competitive EPS production capacity, and the proprietary software IP in EPS ECU control algorithms that new entrants must develop over 3-5 years to achieve OEM acceptance. Market concentration is declining at the margin as Chinese domestic EPS suppliers gain domestic OEM qualification and Korean suppliers expand beyond Korean OEM anchor relationships.

Investment & Growth Opportunities

Highest Growth Segments

EPS (~4.2% CAGR), steer-by-wire (~25-30% CAGR from near-zero 2025 base), active rear-axle electric steering (~12-15% CAGR), commercial vehicle EPS (~8-10% CAGR), India EPS market (~12-15% CAGR from HPS-to-EPS transition), and EPS aftermarket service and ECU programming (~8-10% CAGR as EPS vehicle fleet ages into service window) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

SbW production technology supply chain development represents the most commercially compelling emerging opportunity, each SbW system requiring a Hand Wheel Actuator (HWA) providing programmable feedback sensation, a Wheel Steering Actuator (WSA) with redundant dual-motor architecture, and a Steering Control Unit (SCU) with regulatory compliance, creating approximately USD 350-700 total SbW system value versus USD 200-450 for equivalent EPS.

Investment Themes

- India EPS market penetration for the world's fastest-growing major automotive market transitioning from HPS to EPS: India's passenger car market growth, combined with the transition from HPS-dominant to EPS-dominant steering across all price segments, creates a compounding investment opportunity.

- SbW ecosystem supplier development for hand wheel actuator, wheel steering actuator, and steering control unit supply: The SbW supply chain requires new components not present in conventional EPS systems such as the Hand Wheel Actuator (HWA) with programmable steering feel generation motor and road feel simulation algorithm, the Wheel Steering Actuator (WSA) with dual-redundant motor architecture and end-stop crash compliance, and the SbW-dedicated Steering Control Unit (SCU).

Future Market Outlook (2026-2034)

The global automotive steering system market is projected to grow from USD 36.14 Billion in 2025 to USD 48.22 Billion by 2034, delivering a 3.16% CAGR over the forecast period. The market's anchor value of USD 42.22 Billion in 2030 represents a steering system industry at its most consequential technology transition since HPS replaced manual steering in the 1960s. The moderate 3.16% market CAGR reflects a mature industry characteristic with global vehicle production growth.

Three structural forces define the automotive steering system market growth through 2034 with confidence. The EV transition's mandatory EPS requirement creates non-discretionary market growth. The ADAS regulatory cascade systematically mandates EPS-dependent safety features that create compulsory EPS adoption timelines independent of consumer preference or OEM product planning. The developing market volume growth engine creates compound volume and mix-shift revenue growth that more than offsets mature market vehicle production plateaus in Europe, Japan, and North America.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025) including Vice Presidents of Engineering; Chief Technology Officers; OEM Vehicle Integration Directors; NHTSA Office of Defects Investigation steering recall technical staff; Vehicle Active Safety technical committee members; automotive analysts, and Dynamics covering global vehicle production and steering system content forecasting.

Secondary Research

Secondary research encompassed International Organization of Motor Vehicle Manufacturers global vehicle production statistics 2020-2024; Global Mobility vehicle production and powertrain forecast 2025-2034; Automotive Steering System Content Forecast 2025; Assessment Protocols 2024 including ADAS steering requirements; Motor Vehicle Safety Standards; company annual reports; International technical paper database for EPS, SbW, and active steering system publications; automated vehicles regulations database; functional safety for road vehicles standard publications; individual patent database analysis for SbW, EPS, and active steering system patent activity by company. Over 70 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up product-level model: (i) global vehicle production forecast by region and vehicle segment from LMC Automotive and IHS Markit base cases; (ii) steering system content per vehicle by type with technology mix shift modelling based on EV penetration curve, ADAS mandate rollout, and cost reduction trajectory; (iii) average per-vehicle steering system value by technology type and vehicle segment calibrated against disclosed OEM supply prices and Tier-1 company financial disclosures.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Electric Power Steering (EPS), Hydraulic Power Steering (HPS), Electro-Hydraulic Power Steering (EHPS), Manual Steering |

| Components Covered | Steering Column, Steering Wheel Speed Sensors, Electric Motors, Hydraulic Pumps, Others |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Robert Bosch GmbH, ZF Friedrichshafen AG, NSK Ltd., HL Mando Corp, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Automotive Steering System Market Report

The global automotive steering system market reached USD 36.14 Billion in 2025, driven by electric power steering (EPS) leadership at 46.8% through EV architecture compatibility and ADAS integration requirements, global vehicle production recovery, Asia-Pacific vehicle production dominance, the accelerating transition from HPS and EHPS to EPS across emerging market vehicle models, and growing per-vehicle EPS system content value from ADAS feature integration.

The market grows at 3.16% CAGR during 2026-2034, reaching USD 48.22 Billion by 2034. Growth reflects EPS market share expansion driven by mandatory EV architecture EPS requirement and ADAS regulatory cascade, commercial vehicle EPS adoption, India and developing market EPS penetration growth, steer-by-wire commercial scale-up from initial GM electric truck production, and active rear-axle steering expansion from premium to mid-premium vehicle segments.

EPS leads at 46.8% through EV mandatory compatibility and ADAS integration enabling. EPS also grows fastest at ~4.2% CAGR.

Passenger cars lead at 68.5% through the world's highest volume segment, highest EPS content per vehicle, and fastest ADAS integration, creating premium EPS content value growth. Passenger Cars also grow at the fastest segment CAGR (~3.4%), reflecting EPS penetration depth improvement and per-vehicle value increase from ADAS integration, active rear-axle adoption, and eventual SbW introduction.

Asia-Pacific leads at 41.9% through China's annual vehicle sales, Japan's EPS global leadership, and India's rapidly growing passenger car market transitioning from HPS to EPS.

Leading companies include Robert Bosch GmbH, ZF Friedrichshafen AG, NSK Ltd., HL Mando Corp, among others.

The market is projected to reach approximately USD 42.22 Billion by 2030, with EPS achieving approximately 60-65% market share as HPS falls below 15%, and steer-by-wire scaling to high annual units.

HPS (hydraulic power steering) uses an engine-driven vane pump creating 8-15 MPa hydraulic pressure to assist steering rack movement, high assist force, proven reliability, but constant engine parasitic loss reduces fuel economy and is incompatible with EV. EPS (electric power steering) uses an electric motor to provide variable assist force calculated from torque sensor input and speed, eliminates parasitic power draw, enables ADAS integration, is compatible with EV, but is more electronics-intensive. EHPS (electro-hydraulic power steering) retains the hydraulic rack but replaces the engine-driven pump with an electric motor-driven pump, transitional technology for high-assist force applications not yet served by EPS. SbW (steer-by-wire) replaces the mechanical steering column with electronic signal transmission between steering input and wheel actuator, enabling autonomous interior space, software-defined steering feel, and redundant safety architecture for Level 3+ autonomous driving.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade