Baby Wipes Market Size, Share, Trends and Forecast by Technology, Product Type, Distribution Channel, and Region, 2026-2034

Global Baby Wipes Market Size, Share, Trends & Forecast (2026-2034)

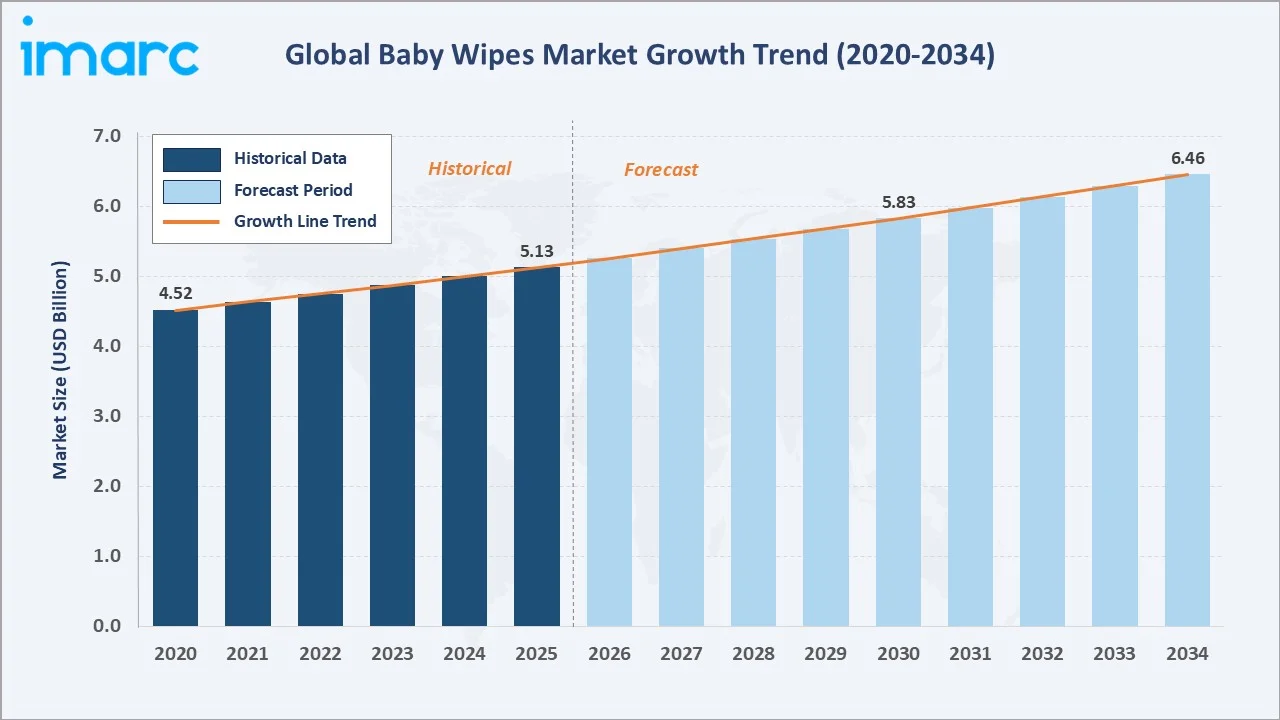

The global baby wipes market size was valued at USD 5.13 Billion in 2025 and is projected to reach USD 6.46 Billion by 2034, exhibiting a CAGR of 2.58% during the forecast period 2026-2034. Sustained growth is driven by rising parental awareness of infant hygiene, expanding birth rates across emerging economies, and a structural shift toward natural, biodegradable, and hypoallergenic formulations.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.13 Billion |

|

Forecast Market Size (2034) |

USD 6.46 Billion |

|

CAGR (2026-2034) |

2.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

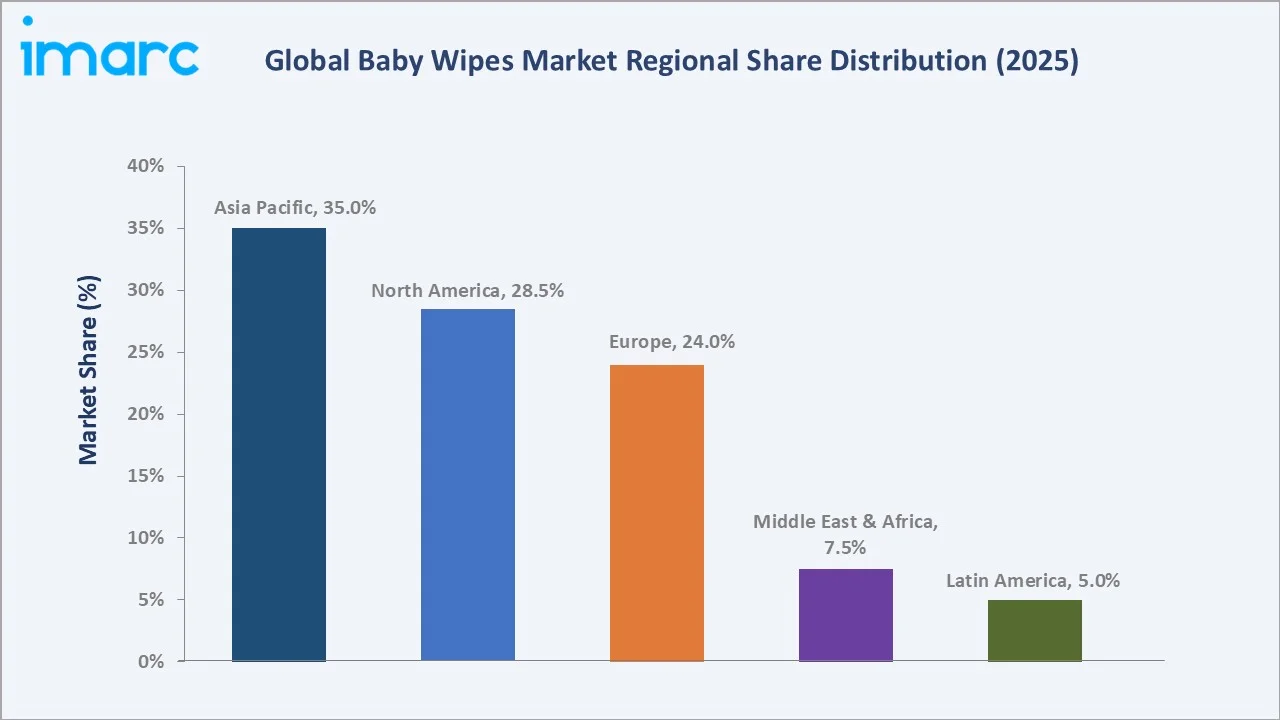

Largest Region |

Asia Pacific (35.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Product Type |

Wet Wipes (77.0%, 2025) |

|

Leading Technology |

Spunlace (35.0%, 2025) |

The market trajectory from 2020 through 2034 reflects consistent expansion, contrasting historical stability against a sustained forecast curve powered by infant care demand, urbanization-driven consumption, and eco-product innovation.

To get more information on this market, Request Sample

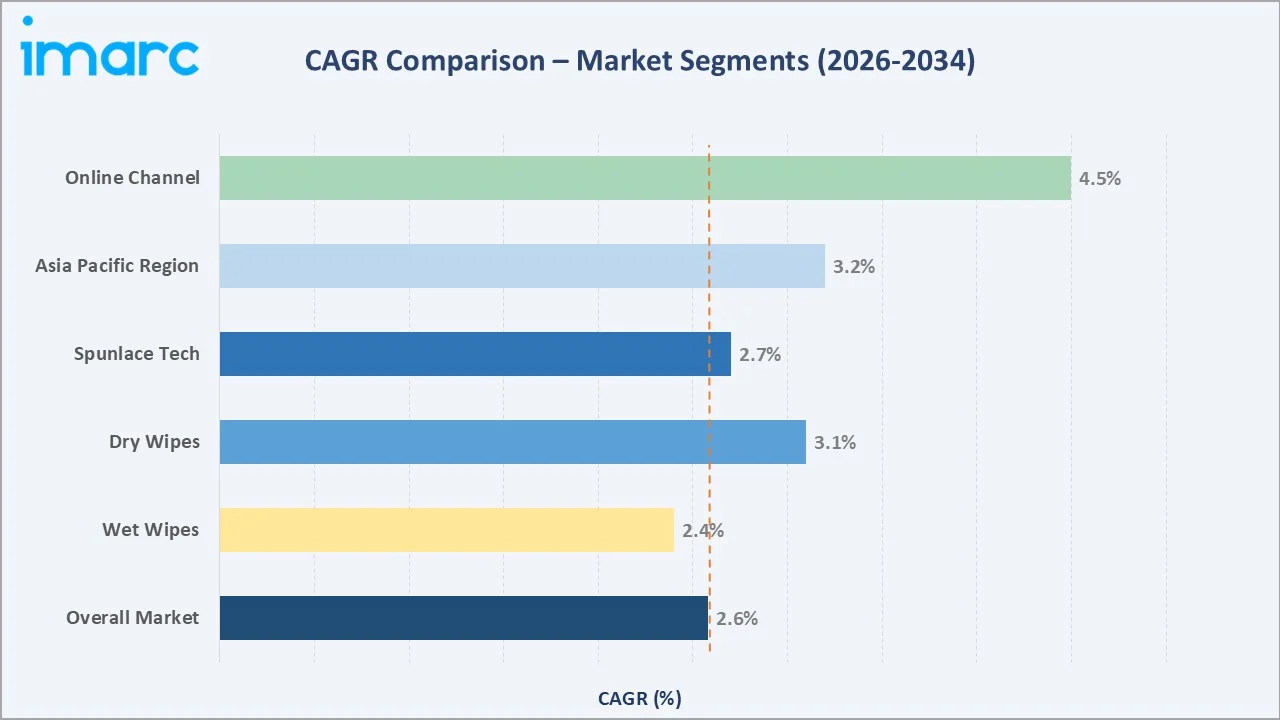

Segment-level CAGR comparisons highlight the online channel and dry wipes as the fastest-growing sub-categories within the global baby wipes market forecast through 2034, with the online channel advancing at an estimated CAGR of 4.50%.

Executive Summary

The global baby wipes market is witnessing a steady transformation driven by heightened infant hygiene awareness, the proliferation of working-parent households, and innovation in sustainable product formulations. Valued at USD 5.13 Billion in 2025, the market is forecast to reach USD 6.46 Billion by 2034 at a CAGR of 2.58%, supported by sustained demand across both developed and developing economies.

Wet wipes command a dominant 77.0% share in 2025, anchored by their pre-moistened convenience and hypoallergenic formulations enriched with aloe vera and vitamin E. Meanwhile, dry wipes are emerging as the fastest-growing product category, valued for their longer shelf life, customizability, and eco-friendly positioning. Spunlace technology holds a 35.0% share of the manufacturing base, favored for producing soft, cloth-like substrates ideal for sensitive infant skin.

Asia Pacific commands 35.0% of global revenue in 2025, powered by rising birth rates across Southeast Asia, government-backed maternal care programs, and rapid e-commerce penetration. North America holds 28.5% and Europe 24.0%. The baby wipes market outlook remains positive as ingredient transparency, biodegradable material adoption, and subscription-based retail models converge to redefine consumer expectations and brand strategies across all major geographies through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Wet Wipes – 77.0% share (2025) |

|

Fastest Growing Product |

Dry Wipes – growing at ~3.10% CAGR (2026-2034) |

|

Leading Technology |

Spunlace – 35.0% share (2025) |

|

Second Technology |

Airlaid – 22.5% share (2025) |

|

Leading Region |

Asia Pacific – 35.0% revenue share (2025) |

|

Second Region |

North America – 28.5% revenue share (2025) |

|

Top Companies |

Kenvue SA Proprietary Limited, Procter & Gamble, KCWW, Unicharm Corporation, Essity Aktiebolag |

|

Market Opportunity |

Biodegradable wipes; investments in eco materials up 35% (2022-2025) |

Key Analytical Observations Supporting The Insights Above:

- Wet Wipes' 77.0% dominance in 2025 reflects their pre-moistened convenience, superior skin-soothing efficacy, and dominant shelf presence across supermarkets and online platforms globally.

- Dry Wipes' fastest-growing status is underpinned by their longer shelf life, versatility with custom solutions, and alignment with eco-friendly consumer mandates, particularly in Europe and North America.

- Spunlace technology's 35.0% share reflects its manufacturing superiority in producing soft, high-strength nonwoven substrates through high-pressure water-jet entanglement — the gold standard for premium baby wipes.

- Asia Pacific's 35.0% dominance is driven by India's large birth cohort, Indonesia and Vietnam's expanding middle class, and government-supported maternal hygiene programs across the region.

- Eco-friendly investment momentum is accelerating — Investments in biodegradable materials have increased significantly in recent years, supported by the introduction of stricter single-use plastic regulations across multiple countries, accelerating the shift toward sustainable alternatives.

- E-commerce channel expansion is reshaping purchasing patterns — Online baby wipes subscriptions are witnessing strong growth, reflecting a shift toward convenience-driven purchasing and recurring delivery models.

Global Baby Wipes Market Overview

Baby wipes are disposable, pre-moistened, or dry nonwoven fabric sheets designed for gentle cleansing of infant skin during diaper changes, mealtime clean-ups, and daily care routines. The global baby wipes industry spans a comprehensive portfolio of products manufactured using spunlace, airlaid, coform, needlepunch, and composite nonwoven technologies, catering to sensitive-skin formulations, biodegradable substrates, and performance-optimized variants.

The industry operates at the convergence of infant care demand, retail channel evolution, regulatory compliance, and sustainability innovation. Growth is supported by macroeconomic drivers including expanding birth rates in Asia Pacific and Africa, rising disposable incomes enabling premiumization, and regulatory frameworks mandating the elimination of plastic-containing wipes in Europe and the UK. A structural shift toward natural, alcohol-free, and hypoallergenic product lines continues to redefine procurement priorities for both global brands and regional manufacturers through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

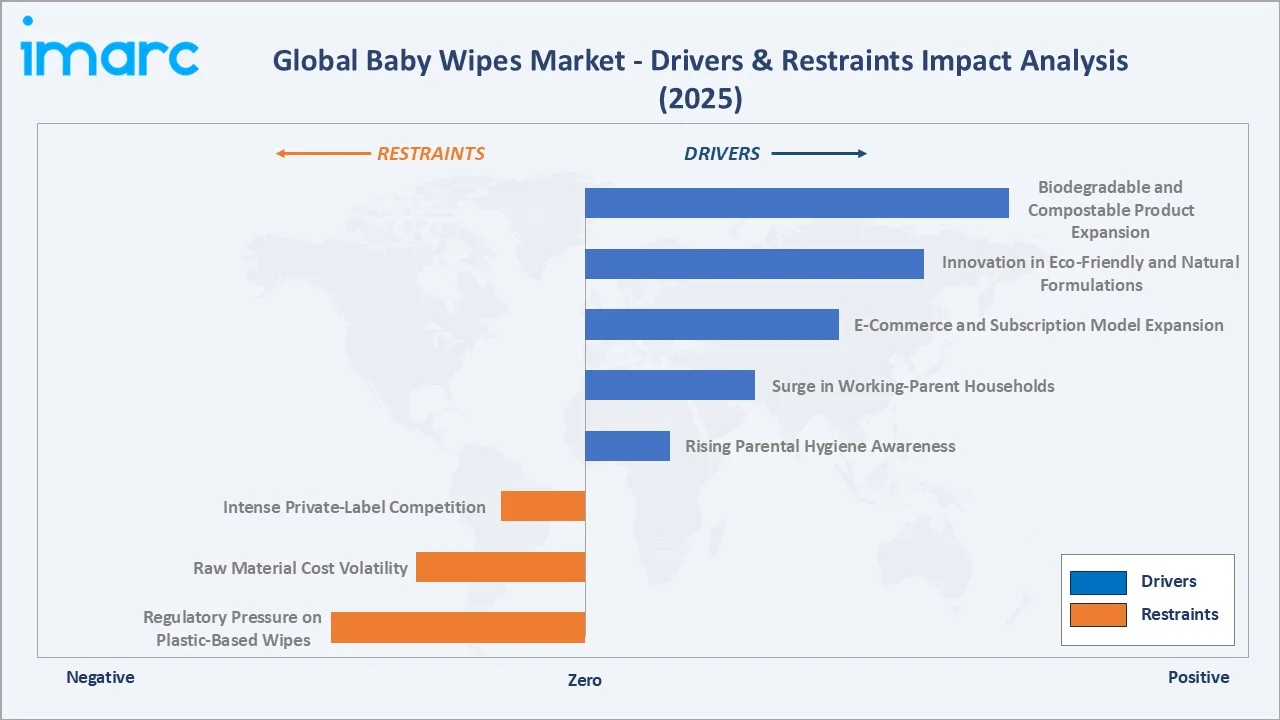

Market Drivers

- Rising Parental Hygiene Awareness: Modern digital-age parents are more informed than any previous generation. Social media, pediatric guidance, and parenting platforms consistently reinforce the importance of infant skin hygiene. Approximately 78% of households with infants aged 0-3 years use baby wipes daily, with average usage reaching 6-10 wipes per diaper change globally. This behavioral norm is structurally sustaining baseline demand.

- Surge in Working-Parent Households: The growing participation of women in the workforce — particularly across Asia Pacific and Latin America — is leading to the rise of dual-income households with limited time for traditional care routines. This demographic shift is significantly increasing the demand for convenient, ready-to-use solutions, establishing a stronger foundation for the adoption of convenience-oriented products.

- E-Commerce and Subscription Model Expansion: Online platforms are fundamentally reshaping how parents procure baby wipes. Subscription-based auto-replenishment models are witnessing rapid growth, and The Indian e-commerce market is projected to grow from US$ 125 billion in 2024 to US$ 345 billion in 2030, with baby care among its fastest-growing categories. This channel shift is both expanding market reach and increasing purchase frequency.

- Innovation in Eco-Friendly and Natural Formulations: Consumer demand for ingredient-transparent, chemical-free, and biodegradable products is accelerating R&D investment. Investments in eco-friendly materials are rising significantly, reflecting a strong shift toward sustainable innovation. Regulatory actions such as bans on plastic-containing wet wipes in key markets are compelling manufacturers globally to reformulate substrates — creating a structural demand catalyst for premium, sustainable variants.

Market Restraints

- Regulatory Pressure on Plastic-Based Wipes: Across Europe, North America, and Australia, tightening single-use plastics directives are creating compliance costs and reformulation requirements. Over 25 countries implemented stricter regulations on plastic-based wipes in 2024, increasing R&D expenditure and compressing margins for manufacturers reliant on traditional substrates.

- Raw Material Cost Volatility: Cotton, viscose, and polyester prices remain subject to commodity market fluctuations, creating input cost unpredictability. Biodegradable alternatives carry significantly higher costs compared to conventional wipe materials, limiting their accessibility in price-sensitive emerging markets.

- Intense Private-Label Competition: Retailer-owned private-label wipes account for a growing share of shelf space in major supermarkets, intensifying pricing pressure on branded players and limiting margin expansion opportunities in volume-driven market segments.

Market Opportunities

- Biodegradable and Compostable Product Expansion: The surge in eco-conscious consumer behavior and regulatory mandates is creating substantial white-space for brands that can offer certified biodegradable, plant-derived substrate wipes at scale. In June 2025, Coterie launched a flush wipe made from 100% plant-derived fibers certified by OEKO-TEX and EWG, capturing premium-segment demand.

- Emerging Market Penetration in Asia Pacific and Africa: With a significant share of future demand expected from Asia Pacific and Africa, brands with localized distribution, vernacular marketing, and value-tier pricing strategies are well positioned to capture first-mover advantages in high-birth-rate economies.

- Subscription-Based Digital Commerce: The AI-powered recommendation engines and auto-replenishment models being deployed by major e-commerce platforms are transforming baby wipes from impulse purchases to recurring subscriptions, increasing customer lifetime value and repeat purchase rates.

Market Challenges

- Greenwashing Scrutiny and Certification Complexity: As sustainability claims proliferate, consumers and regulators are demanding substantiation. Brands face reputational and legal risks from unverified 'biodegradable' or 'natural' claims, creating a compliance burden that disproportionately affects smaller manufacturers.

- Highly Fragmented Competitive Landscape: The presence of numerous manufacturing facilities globally dedicated to baby wipes production creates intense market fragmentation. A large number of regional manufacturers, particularly in Asia Pacific, compete aggressively on price, compressing margins and making it challenging for premium brands to maintain differentiated positioning.

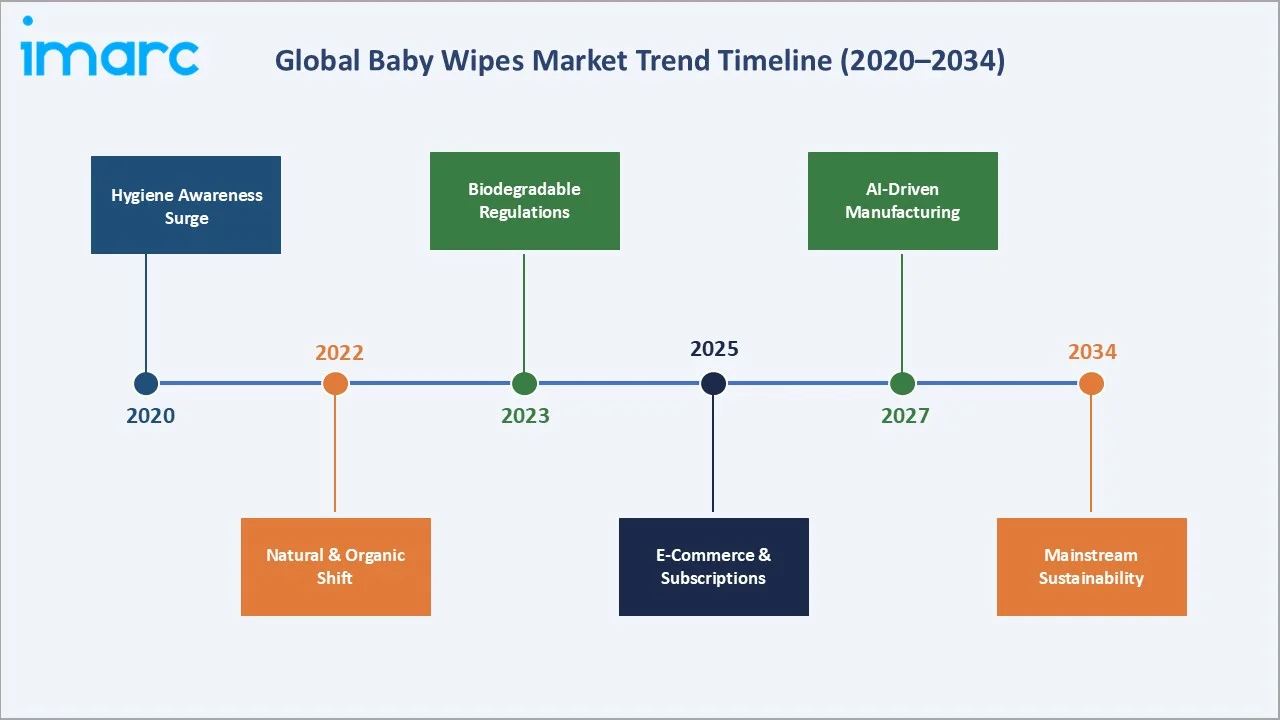

Emerging Market Trends

1. Natural and Hypoallergenic Formulation Shift

Consumer preference has decisively shifted toward natural, hypoallergenic baby wipes free from parabens, alcohol, and synthetic fragrances. A clear majority of parents now prioritize ingredient transparency and safety labeling when making purchasing decisions. In April 2025, RAAN launched its TruCotton wipes made from unbleached cotton with 99% purified water and organic aloe — exemplifying the industry's move toward ultra-clean formulations. Premium 'pure water' wipes containing 99-99.9% water are among the fastest-growing product variants globally.

2. Biodegradable and Sustainability-Led Innovation

Regulatory pressure from the EU's Single-Use Plastics Directive, the UK's 2025 plastic wipes ban, and sustainability activism is forcing the industry to reformulate. Baby wipes market trends show that brands are transitioning to FSC-certified plant fibers, compostable packaging, and OEKO-TEX-certified substrates. Coterie's Flush Wipe — launched in June 2025 — dissolves within 30 minutes and is certified by EWG and NEA, setting a new performance benchmark for sustainable alternatives.

3. E-Commerce and Subscription Commerce Growth

Digital platforms are restructuring the baby wipes purchase journey. Online subscription-based services are witnessing strong growth, as time-pressed parents increasingly favor auto-replenishment models for convenience and consistency. India's e-commerce market, valued at USD 125 Billion in FY24 and projected to reach USD 345 Billion by FY2030 per IBEF, is driving outsized growth in the Asia Pacific baby wipes digital channel. AI-powered recommendation engines are further optimizing product-to-consumer matching by skin type, infant age, and purchase history.

4. Premiumization and Ingredient Transparency

A clear bifurcation is emerging between premium, certified-natural wipes and high-volume value products. Premium wipes — particularly those positioned with organic aloe, vitamin E, chamomile, and dermatologist-tested claims — command significantly higher price points compared to standard alternatives. Major brands such as Pampers Pure Protection and Huggies Natural Care have reinforced this premium positioning, shaping consumer expectations around both ingredient quality and packaging sustainability across key markets.

5. AI-Driven Manufacturing and Demand Management

AI-driven demand forecasting is enabling brands to significantly reduce overstock, while machine learning-based ingredient screening tools help identify potentially irritating compounds during formulation. Automation investments are streamlining production processes, improving operational efficiency. These capabilities are not only enhancing supply chain performance but also enabling faster product development cycles — providing a competitive advantage for brands responding to evolving demand signals from emerging demographic segments.

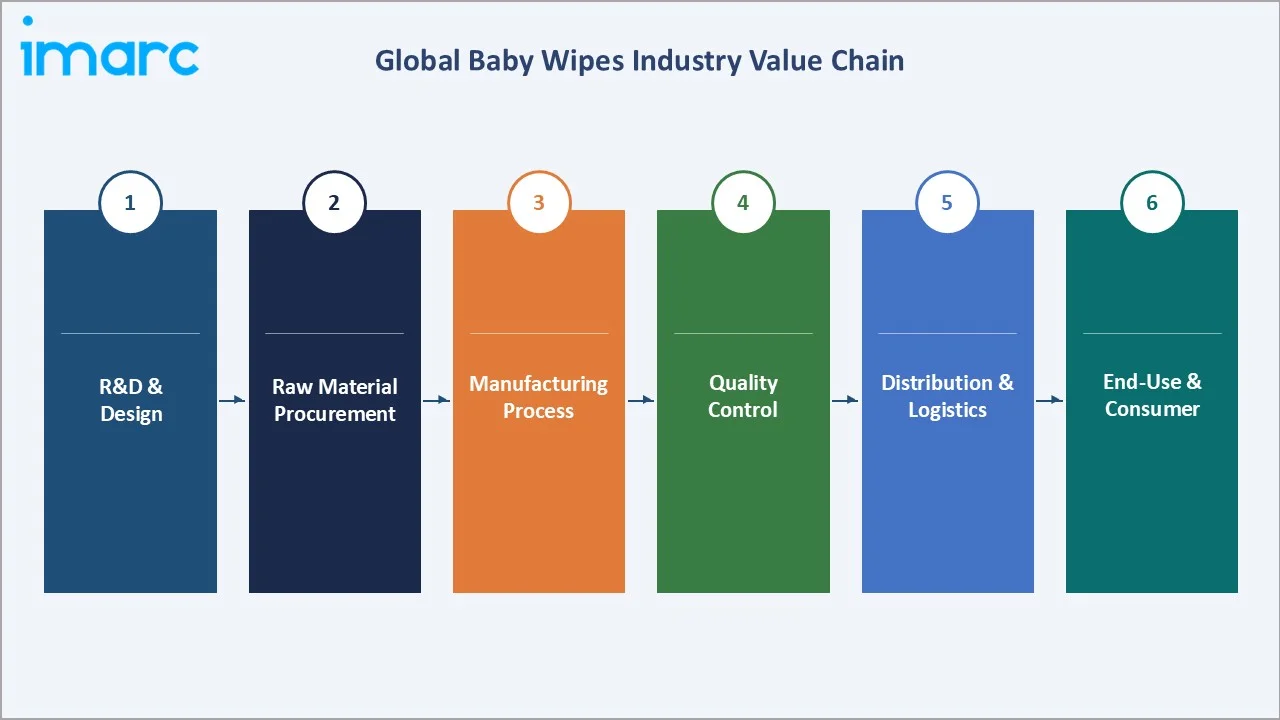

Industry Value Chain Analysis

|

Stage |

Key Activities |

Key Players / Inputs |

|

R&D & Design |

Formulation development, substrate testing, skin-safety validation |

Chemical companies, research labs, dermatology institutions |

|

Raw Material Procurement |

Nonwoven fibers (cotton, viscose, polyester), water purification agents, aloe vera, preservatives |

Fiber suppliers, chemical distributors |

|

Manufacturing Process |

Spunlace, airlaid, coform, needlepunch fabric production; moistening and folding |

OEM manufacturers, nonwoven fabric producers |

|

Quality Control |

Skin-compatibility testing, pH balance checks, contamination screening, certification (OEKO-TEX, EWG) |

Third-party testing labs, regulatory auditors |

|

Distribution & Logistics |

Warehousing, cold-chain (for sensitive wipes), retail supply, e-commerce fulfillment |

Supermarkets, pharmacies, Amazon, D2C platforms |

|

End-Use & Consumer |

Diaper changes, mealtime clean-up, on-the-go hygiene, healthcare settings |

Parents, caregivers, hospitals, childcare centers |

The global baby wipes industry value chain spans six integrated stages from raw material sourcing through end-consumer use. Each stage presents distinct competitive dynamics, margin profiles, and sustainability requirements relevant to the overall baby wipes market analysis.

Technology Landscape in the Baby Wipes Industry

Spunlace Technology (35.0% Share, 2025)

Spunlace — or hydroentanglement — involves bonding fibers through high-pressure water jets, producing soft, cloth-like fabrics with exceptional absorbency and tensile strength. Its gentle texture makes it the preferred substrate for sensitive infant skin applications. Spunlace remains the dominant manufacturing technology, supported by its ability to process natural fibers (cotton, viscose) compatible with biodegradable reformulation mandates.

Airlaid Technology (22.5% Share, 2025)

Airlaid technology blends pulp fibers with air and binders to form highly absorbent, soft substrates. Its superior liquid retention properties make it well-suited for thick, multi-layer wipe products targeting premium personal care segments. Airlaid wipes offer a higher bulk and softness profile than spunlace alternatives, driving preference among premium diaper-change and overnight-use segments.

Coform, Needlepunch, and Composite Technologies

Coform represents a significant share, combining meltblown and staple fibers to deliver enhanced barrier and absorbency properties. Needlepunch technology mechanically entangles fibers, creating durable substrates that are increasingly gaining traction in the eco-wipe segment. Composite technologies layer multiple substrate types to achieve targeted functional performance, particularly for specialized medical and sensitive-skin applications.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Technology | Spunlace | 35% | 2025 |

| Product Type | Wet Wipes | 77% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 30% | 2025 |

| Region | Asia Pacific | 35% | 2025 |

By Product Type

To access detailed market analysis, Request Sample

Wet Wipes represent the dominant product category at 77% of global market share in 2025. Their pre-moistened format delivers immediate cleansing efficacy with no preparation required — a decisive advantage during diaper changes and on-the-go care. Wet wipes formulated with aloe vera, vitamin E, chamomile, and purified water provide skin-soothing properties that dry alternatives cannot replicate.

By Technology

Spunlace technology commands the largest share at 35% of the global baby wipes market in 2025, driven by its capacity to produce soft, durable, and skin-compatible nonwoven substrates through high-pressure water-jet entanglement. The technology's compatibility with natural fibers — including cotton and viscose — aligns seamlessly with the industry's biodegradable reformulation imperative. Spunlace fabrics offer superior tactile properties, high tensile strength, and consistent thickness — attributes critical for premium baby wipe performance.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

35.0% |

Rising birth rates, India/Indonesia middle-class expansion, government maternal programs, e-commerce growth |

|

North America |

28.5% |

High parental hygiene awareness, premium product demand, strong retail/online infrastructure, regulatory-driven innovation |

|

Europe |

24.0% |

Plastic wipes ban (UK 2025), EU Single-Use Plastics Directive, biodegradable product adoption, premium brand market |

|

Middle East & Africa |

7.5% |

Young population, rising birth rates, urbanization, expanding modern retail penetration |

|

Latin America |

5.0% |

Brazil/Colombia residential urbanization, growing middle class, rising infant hygiene awareness |

Asia Pacific commands 35% of global revenue in 2025, establishing itself as the dominant region in the global baby wipes industry. India's significant birth cohort — with approximately 25 million births annually — creates a substantial baseline demand for infant hygiene products. Indonesia, Vietnam, and the Philippines are experiencing rapid urbanization and middle-class expansion, generating growing spending on premium baby care.

Competitive Landscape

The report provides a comprehensive analysis of the competitive landscape in the baby wipes market with detailed profiles of all major companies, including:

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Kenvue SA Proprietary Limited |

Johnson's Baby |

Leader |

Global brand trust, extensive retail distribution, dermatologist-tested portfolio |

|

Procter & Gamble |

Pampers |

Leader |

Market scale, Pampers Pure Protection, R&D investment in natural formulations |

|

KCWW |

Huggies, Pull-Ups, GoodNites |

Leader |

Huggies Natural Care line, North America dominance, sustainability commitments |

|

Unicharm Corporation |

MamyPoko, Moony |

Leader |

Asia Pacific leadership, Japan-origin premium quality, strong regional distribution |

|

Essity Aktiebolag |

Libero |

Challenger |

European strength, sustainability-led portfolio, biodegradable product innovation |

The global baby wipes market's competitive landscape is moderately fragmented, with global consumer goods powerhouses competing alongside regional specialists and high-volume Asian manufacturers. Leading players compete on brand trust, hypoallergenic formulations, sustainability credentials, and digital commerce capabilities. KCWW and Baby2Baby partnered in March 2024 to distribute millions of diapers and wipes, tripling their Maternal Health & Newborn Supply Kit Initiative — a strategic move reinforcing community-driven brand positioning.

Key Company Profiles

Kenvue SA Proprietary Limited

Kenvue SA Proprietary Limited is a global consumer health company headquartered in Summit, New Jersey. Formed in 2023 as a spin-off from Johnson & Johnson, it became the world’s largest pure-play consumer health business, overseeing a portfolio of iconic over-the-counter and personal-care brands.

- Product Portfolio: Johnson's Baby wipes range includes the Pure Protect, Cottontouch, and Extra Sensitive sub-lines, featuring fragrance-free, hypoallergenic formulations with aloe vera and vitamin E. The portfolio spans standard, thick-texture, and travel-pack configurations.

- Recent Developments: In 2025, Kenvue SA Proprietary Limited highlighted continued innovation and clinical research across its personal care portfolio, including baby care categories such as wipes. The company emphasized science-backed product development and consumer insights to enhance everyday care solutions, supporting premiumization and safety-focused innovation in baby wipes and related segments.

- Strategic Focus: Kenvue SA Proprietary Limited’s strategy centers on sustaining global brand trust through ingredient safety leadership, expanding premium sub-lines in Asia Pacific and the Middle East, and transitioning toward certified sustainable packaging and biodegradable substrate integration.

Procter & Gamble

Procter & Gamble is one of the world's largest fast-moving consumer goods companies, headquartered in Cincinnati, Ohio, USA. P&G's Pampers brand is the global market leader in baby diapers and among the largest baby wipes brands globally.

- Product Portfolio: P&G's baby wipes portfolio includes Pampers Sensitive, Pampers Pure Protection (formulated without harmful chemicals and certified by the Skin Health Alliance), and Pampers Aqua Pure (with 99% water). These products are positioned across value, mid, and premium tiers.

- Recent Developments: In 2026, Pampers through Procter & Gamble, launched its new premium diaper line, Pampers AMORE, marking its first major innovation in this segment in several years. The product emphasizes ultra-soft, cashmere-like materials, advanced absorbency, and hypoallergenic formulations free from fragrances and parabens. It also features a five-layer protection system and enhanced leak protection, positioning it as a high-performance, safety-focused solution for sensitive baby skin.

- Strategic Focus: P&G's strategy emphasizes portfolio premiumization through the Pampers Pure Protection platform, expanding e-commerce subscription models, and investing in sustainable substrate R&D to maintain regulatory compliance and brand relevance in European markets.

KCWW

KCWW is a leading global personal care company headquartered in Irving, Texas, USA. The company's Huggies brand is among the world's most recognized baby wipes and diapers platforms, serving markets across North America, Europe, Asia Pacific, and Latin America.

- Product Portfolio: KCWW 's baby wipes portfolio includes Huggies Natural Care, Huggies Simply Clean, and Huggies One & Done — spanning hypoallergenic, natural-ingredient, and value-tier formulations. The Natural Care range features plant-based ingredients and is free from parabens, alcohol, and fragrance.

- Recent Developments: In March 2024, Huggies, through the KCWW, partnered with Baby2Baby to support mothers and newborns in need by providing essential supplies such as diapers and baby wipes. The collaboration includes a multi-million-dollar contribution aimed at expanding maternal health programs and tripling the reach of newborn care kits across multiple U.S. states.

- Strategic Focus: KCWW's strategy focuses on reinforcing Huggies' North American market leadership through natural-ingredient positioning, expanding digital commerce capabilities, and accelerating the development of certified biodegradable wipe substrates to address European regulatory requirements.

Market Concentration Analysis

The global baby wipes market exhibits moderate fragmentation. The top five players — Kenvue SA Proprietary Limited, Procter & Gamble, KCWW, Unicharm Corporation, Essity Aktiebolag— collectively account for an estimated 40-50% of global market revenue in 2025. The remaining market share is distributed across hundreds of regional manufacturers concentrated in China, India, and Southeast Asia.

The market is experiencing a bifurcated dynamic. At the premium brand tier, consolidation is occurring around ingredient safety certifications, sustainable packaging, and digital commerce platform capabilities. Simultaneously, Asia Pacific regional manufacturers are generating cost-competitive, design-improved products increasingly targeting international export markets — intensifying competition across all price segments through 2034.

Private-label wipes from major supermarket chains are emerging as a strong competitive force, particularly in price-sensitive markets across Europe and North America. A large global manufacturing base further intensifies supply-side competition, making it increasingly challenging for leading brands to sustain premium positioning and maintain margin structures.

Investment & Growth Opportunities

Fastest-Growing Segments

Online channel sales represent the highest-growth distribution sub-segment at an estimated CAGR of 4.50% through 2034, significantly outpacing brick-and-mortar formats. The dry wipes segment is expanding at approximately 3.10% CAGR — the fastest among product types — driven by eco-conscious positioning and regulatory-compliant substrate mandates.

Emerging Market Expansion

India represents a high-potential emerging market, supported by a large birth cohort, expanding e-commerce infrastructure, and rising middle-class spending on infant care. Southeast Asia — including Indonesia, Vietnam, and the Philippines — offers strong volume growth opportunities for mid-tier formulations. The Middle East and Africa region, characterized by a large young population, presents a structural long-term demand pipeline for affordable and mid-range baby wipes manufacturers with strong local distribution capabilities.

Venture and Strategic Investment Trends

Venture capital investments in sustainable baby care products are rising strongly, with capital flowing into biodegradable substrate R&D, AI-powered demand forecasting platforms, and direct-to-consumer subscription e-commerce models. Distribution reach is expanding significantly through retail-manufacturer partnerships, strengthening market penetration. Companies investing in automation are achieving notable reductions in production time — creating meaningful cost advantages in a market where pricing discipline remains critical to volume growth.

Future Market Outlook (2026-2034)

The global baby wipes market forecast projects steady value expansion from USD 5.13 Billion in 2025 to USD 6.46 Billion by 2034 at a CAGR of 2.58%. Asia Pacific will retain regional leadership while accelerating structurally through urbanization and e-commerce penetration. North America and Europe will sustain premium value growth driven by sustainability-led reformulation and regulatory compliance cycles.

Three key structural shifts will reshape the baby wipes market through 2034. First, the mandatory transition to biodegradable and plastic-free substrates — accelerated by EU and UK regulatory frameworks — will fundamentally transform manufacturing input strategies and premium pricing structures. Second, subscription-based digital commerce will continue displacing traditional impulse-purchase retail models, with auto-replenishment platforms becoming the default acquisition channel for urban, dual-income households.

Third, AI-assisted formulation development is compressing R&D cycles and enabling faster hypoallergenic innovation — significantly reducing time-to-market for premium-certified products compared to traditional development methods.

Chinese and Indian manufacturers are expected to reach premium design and quality benchmarks by 2028-2030, intensifying global competition across mid-premium price tiers. Brands that establish early leadership in biodegradable certification, ingredient transparency, and subscription commerce ecosystems will be best positioned to capture disproportionate growth in the post-2026 market environment.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with baby wipes industry stakeholders, including product development directors at OEM manufacturers, procurement managers at pediatric healthcare institutions, retail buyers at major supermarket chains and pharmacy groups, and institutional investors in consumer health sectors. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include government demographic databases (UNFPA, national census bureaus), infant hygiene regulatory publications (EU Single-Use Plastics Directive, UK DEFRA guidelines), industry association reports, IBEF e-commerce data, company annual reports, and trade publications covering nonwoven manufacturing, personal care, and baby product sectors across major geographies.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating birth rate trends, urbanization indices, retail channel evolution data, and historical market performance patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty, regulatory shifts, and raw material cost volatility.

Baby Wipes Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Technologies Covered | Spunlace, Airlaid, Coform, Needlepunch, Composite, Others |

| Product types Covered | Dry wipes, wet wipes |

| Distribution channels covered | Supermarkets and hypermarkets, Pharmacies, Convenience stores, Online stores, Others |

| Regions Covered | North America, Europe, Asia Pacific, Middle East and Africa, Latin America |

| Companies Covered | Kenvue SA Proprietary Limited, Procter & Gamble, KCWW, Unicharm Corporation, Essity Aktiebolag, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the baby wipes market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global baby wipes market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the baby wipes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Baby Wipes Market Report

The global baby wipes market was valued at USD 5.13 Billion in 2025, driven by rising infant hygiene awareness, expanding birth rates in emerging economies, and growing parental preference for convenient, safe, and eco-friendly baby care products globally.

The market is projected to reach USD 6.46 Billion by 2034, growing at a CAGR of 2.58% during 2026-2034, supported by biodegradable product innovation, e-commerce subscription expansion, and sustained demand from Asia Pacific and North America.

Wet wipes lead with a 77.0% share in 2025. Their pre-moistened, hypoallergenic formulation ensures immediate cleansing convenience during diaper changes and daily care routines, driving dominant consumer preference globally.

Spunlace technology dominates with a 35.0% share in 2025. Its high-pressure water-jet fiber entanglement produces the soft, cloth-like substrates preferred for sensitive infant skin care applications across all major markets.

Asia Pacific dominates with a 35.0% share in 2025. India's large birth cohort, Southeast Asia's middle-class expansion, government maternal programs, and rapid e-commerce penetration collectively underpin the region's leadership.

Key drivers include rising parental hygiene awareness, growing working-parent households, e-commerce and subscription commerce expansion, natural and biodegradable product innovation, and regulatory mandates eliminating plastic-containing wipes in major markets.

Major players include Kenvue SA Proprietary Limited, Procter & Gamble, KCWW, Unicharm Corporation, Essity Aktiebolag, competing on brand trust, hypoallergenic formulations, and sustainability credentials.

Dry wipes are the fastest-growing segment, advancing at approximately 3.10% CAGR through 2034. Longer shelf life, customizability, and alignment with eco-friendly consumer mandates — particularly in Europe — are driving adoption.

E-commerce is the fastest-growing distribution channel at ~4.50% CAGR. Subscription auto-replenishment services grew 40% in 2023. India's digital commerce market expansion to USD 345 Billion by FY2030 is a key Asia Pacific growth driver.

Opportunities include biodegradable substrate development, subscription e-commerce platforms, emerging market penetration in India and Southeast Asia, natural ingredient certified product lines, and AI-powered demand forecasting and formulation tools.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)