Brazil Lubricants Market Size, Share, Trends and Forecast by Product Type, End User, and Region, 2026-2034

Brazil Lubricants Market Size, Share, Trends & Forecast (2026-2034)

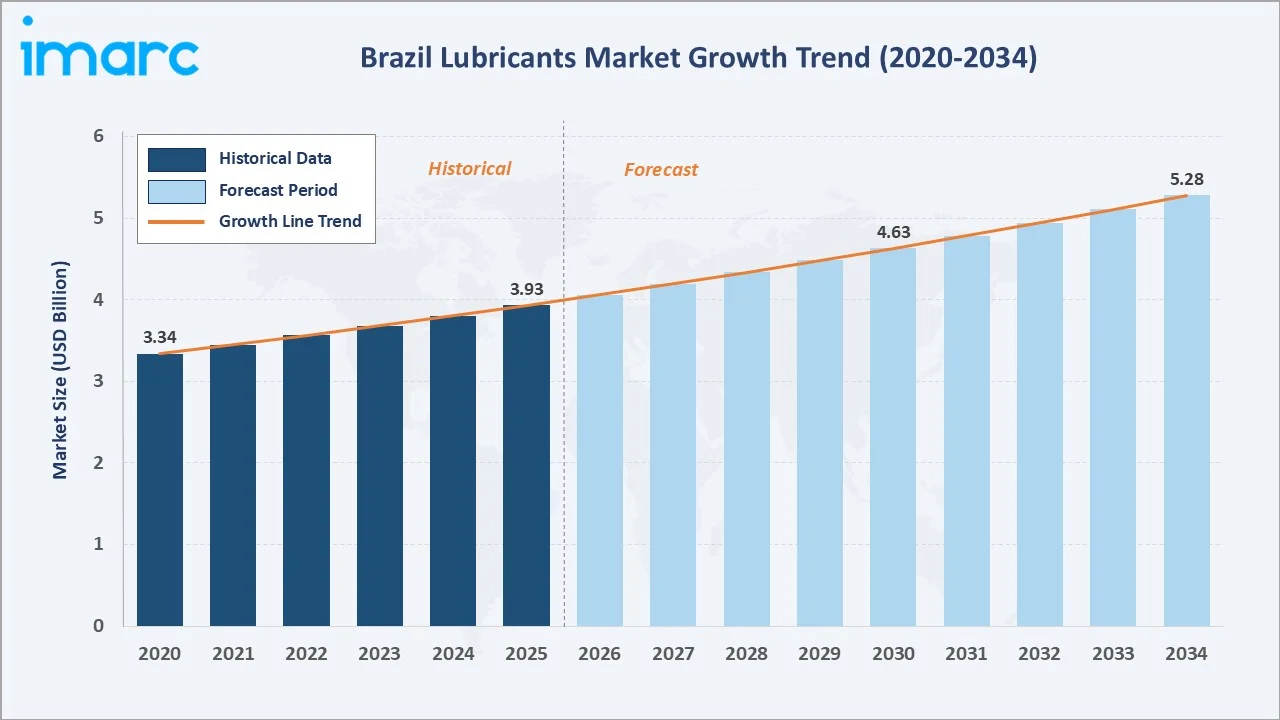

The Brazil lubricants market size reached USD 3.93 Billion in 2025 and is projected to reach USD 5.28 Billion by 2034, exhibiting a CAGR of 3.33% during 2026-2034. Rising vehicle ownership, robust industrial output, and growing adoption of synthetic and bio-based formulations are the primary forces driving Brazil lubricants market growth.

Engine oils dominate at 42.6% in 2025, the automotive segment leads end users at 55.3%, and the Southeast region commands 38.7% regional share, reflecting Brazil's densest concentration of industrial and transportation activity.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.93 Billion |

|

Forecast Market Size (2034) |

USD 5.28 Billion |

|

CAGR (2026-2034) |

3.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (38.7% share, 2025) |

|

Second Largest Region |

South (22.4% share, 2025) |

|

Leading Product Type |

Engine Oils (42.6%, 2025) |

|

Leading End User |

Automotive (55.3%, 2025) |

The Brazil lubricants market growth trajectory from 2020 through 2034, with historical expansion to USD 3.93 Billion in 2025, reflects consistent automotive and industrial demand, while the forecast to USD 5.28 Billion captures accelerating synthetic lubricant adoption, fleet growth, and agribusiness mechanization investment.

To get more information on this market, Request Sample

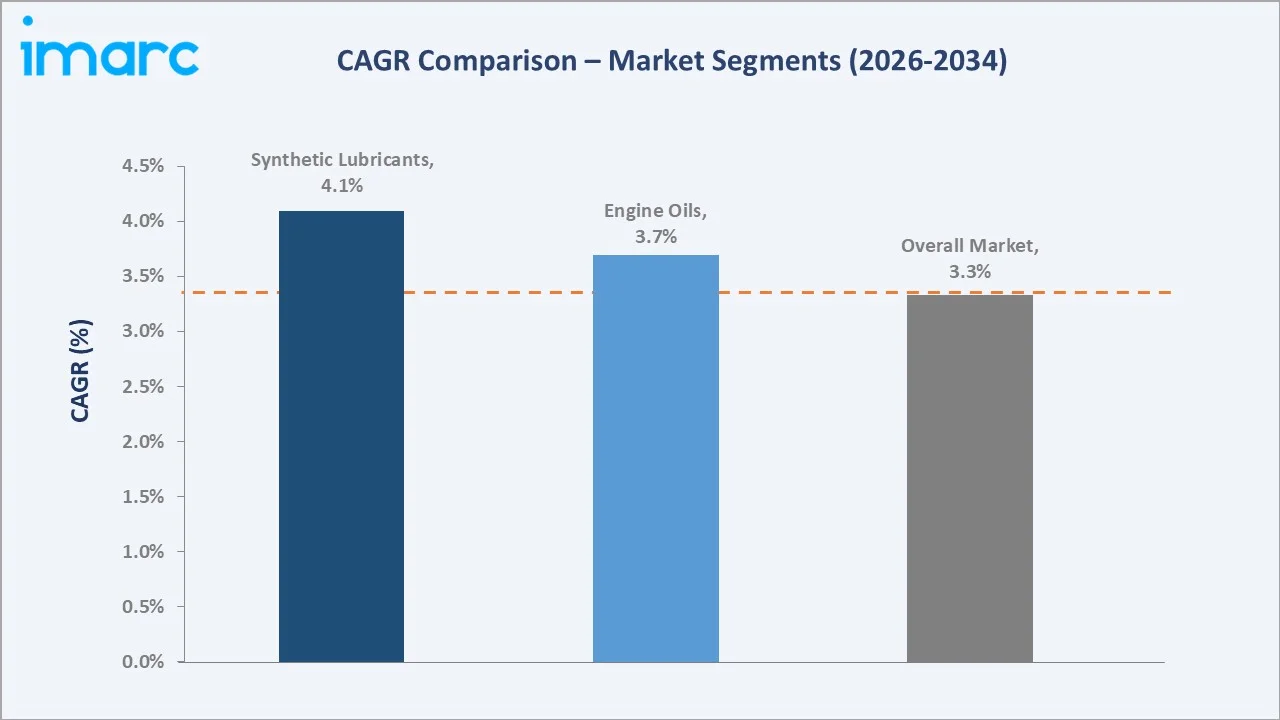

The CAGR trajectories across key product and end-user sub-segments, with synthetic lubricants at ~4.1% CAGR and engine oils at ~3.7% CAGR, are the fastest-growing categories within the Brazil lubricants market analysis through 2034.

Executive Summary

The Brazil lubricants market is on a sustained growth trajectory from USD 3.93 Billion in 2025 to USD 5.28 Billion by 2034. Lubricants serve as essential consumables across automotive, heavy equipment, metallurgy, and power generation sectors, ensuring friction reduction, wear prevention, and operational efficiency across Brazil's expanding industrial base.

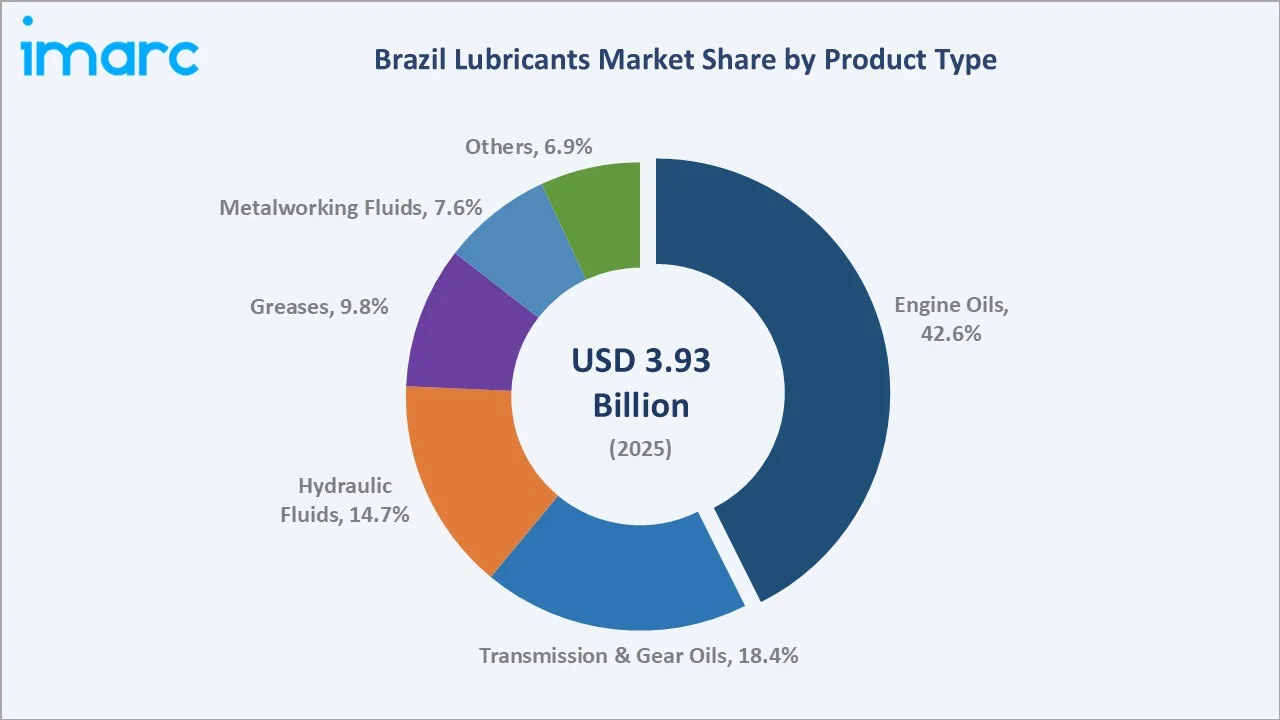

Engine oils lead product type at 42.6% in 2025, driven by Brazil's growing passenger and commercial vehicle fleet. Transmission and gear oils (18.4%) and hydraulic fluids (14.7%) serve industrial machinery and heavy equipment applications extensively across mining, agribusiness, and construction. Greases (9.8%) and metalworking fluids (7.6%) serve specialized industrial segments with precision lubrication requirements.

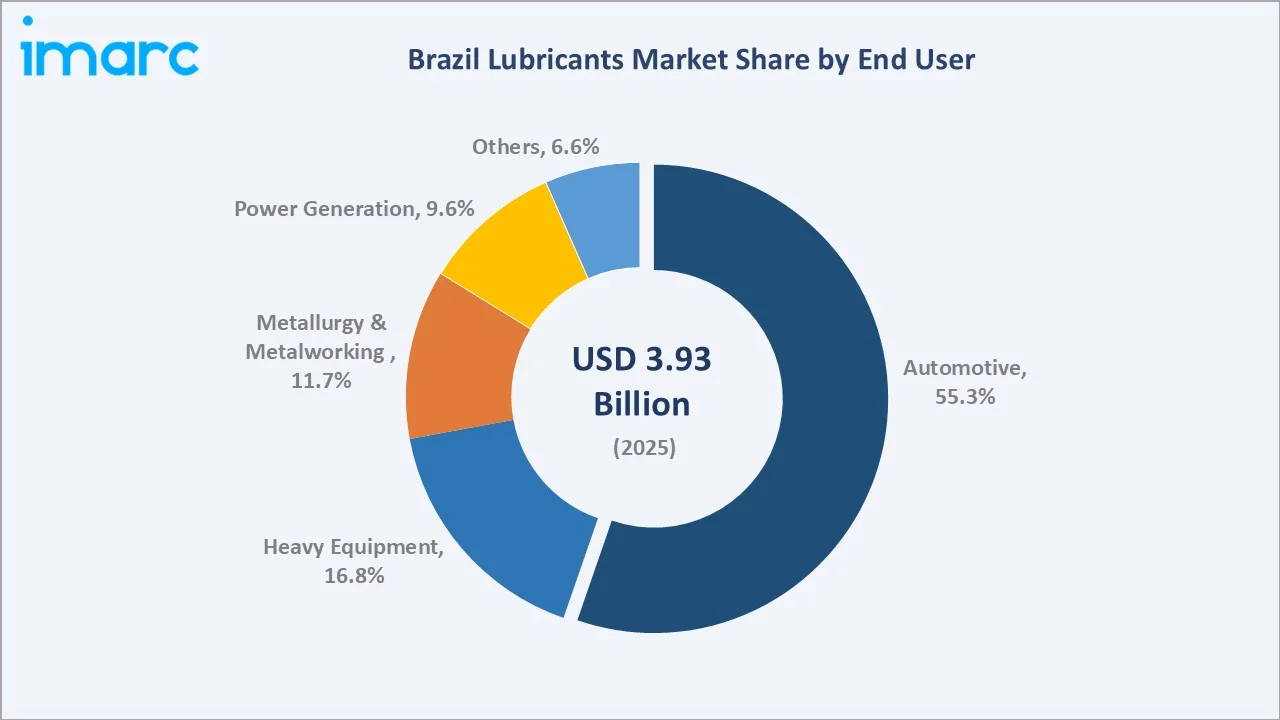

The automotive end-user segment commands 55.3% of market share in 2025, reflecting Brazil's position as Latin America's largest vehicle market. Heavy equipment (16.8%) and metallurgy and metalworking (11.7%) follow, supported by Brazil's industrial expansion.

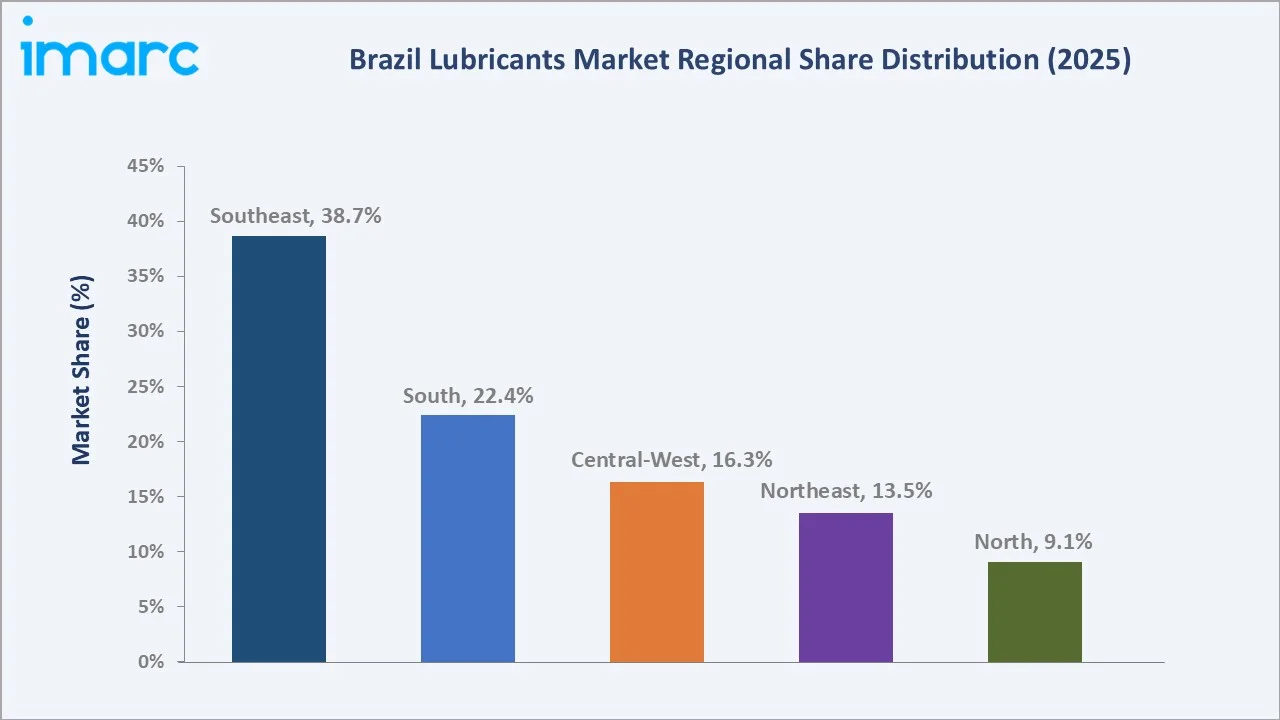

Southeast Brazil leads regionally at 38.7%, followed by the South at 22.4% and Central-West at 16.3%.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Engine Oils – 42.6% share (2025) |

|

Leading End User |

Automotive – 55.3% share (2025) |

|

Leading Region |

Southeast – 38.7% share (2025) |

|

Second Largest Region |

South – 22.4% share (2025) |

|

Top Companies |

Ultrax Lubrificantes, Petroliam Nasional Berhad (PETRONAS), TotalEnergies |

Key Analytical Observations Expanding on the Above Data:

- Engine Oils Dominance: Engine oils, with 42.6% in 2025, dominate because of their non-discretionary demand across all vehicle categories. Rising vehicle ownership, OEM-mandated replacement intervals, and growing preference for synthetics sustain engine oil demand as the core lubricant category in Brazil.

- Automotive Segment Leadership: The automotive segment commanding 55.3% in 2025 reflects Brazil registering approximately 2.3 million new motor vehicles in 2023, a trend accelerating through 2025. Passenger cars, commercial trucks, and fleet operators create consistent, recurring lubricant demand underpinning stable market growth.

- Southeast Regional Dominance: Southeast Brazil's 38.7% dominance reflects São Paulo's concentration of automotive manufacturing, industrial facilities, and transportation infrastructure. São Paulo state accounts for approximately one-third of Brazil's GDP, making it the primary lubricant consumption hub.

- South Region Position: South region's 22.4% share benefits from agribusiness mechanization in Rio Grande do Sul and Santa Catarina, where agricultural equipment and metalworking industries generate disproportionate lubricant demand relative to population and geographic area.

Brazil Lubricants Market Overview

Lubricants are refined petroleum or synthetic fluid formulations designed to reduce friction, control operating temperature, prevent corrosion, and remove contaminants across mechanical systems. Product categories span engine oils, transmission and gear oils, hydraulic fluids, greases, and metalworking fluids, each engineered for specific viscosity, thermal stability, and additive performance requirements.

Brazil's lubricant ecosystem integrates base oil refiners, additive manufacturers, lubricant blenders, wholesale distributors, retail service channels including automotive parts chains and fuel station networks, and diverse end industries spanning automotive, heavy equipment, mining, agribusiness, power generation, and metallurgy across all five Brazilian regions.

Market Dynamics

To evaluate market opportunities, Request Sample

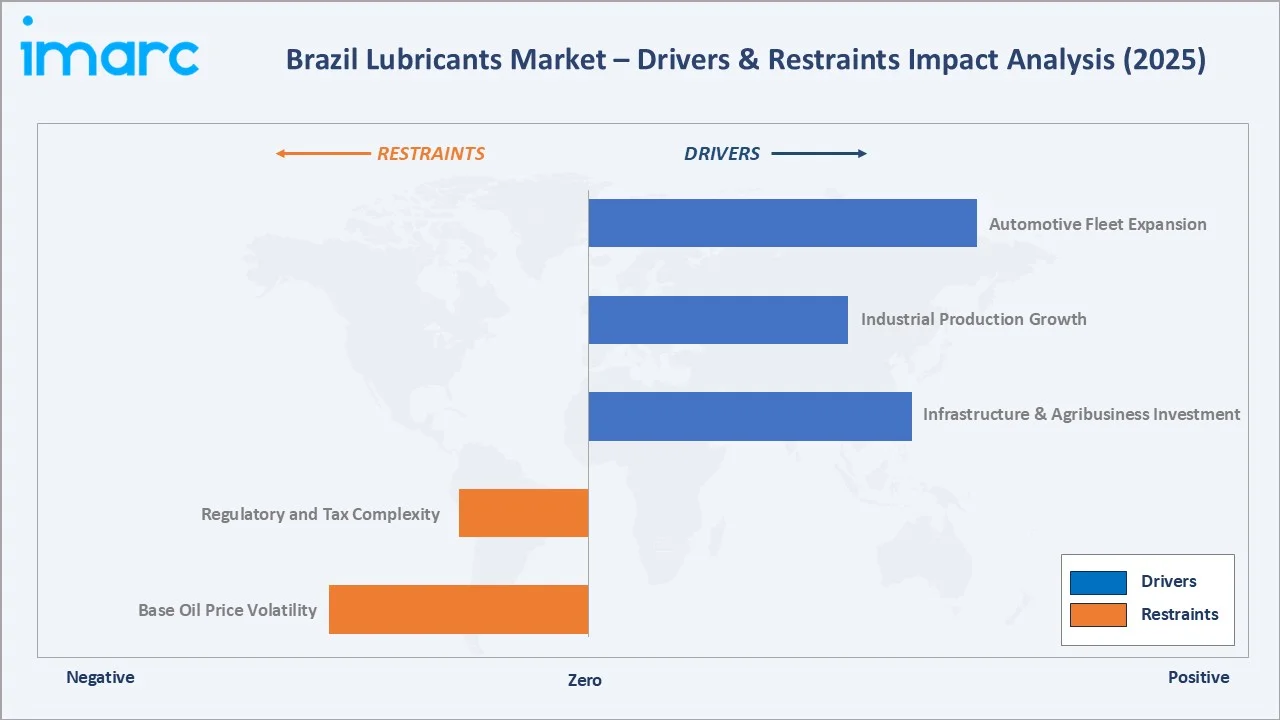

Market Drivers

- Automotive Fleet Expansion: More than 1.7 million new vehicles were sold across Brazil during the first four months of 2026, marking a 16 per cent increase compared with the same period last year and the strongest performance since 2013. Rising vehicle ownership across passenger cars, commercial trucks, and two-wheelers create sustained demand for engine oils, transmission fluids, and brake fluids.

- Industrial Production Growth: Brazil's industrial production recorded a 5.8% year-on-year increase in October 2024, with manufacturing, mining, and agribusiness sectors expanding machinery utilization. Industrial expansion directly increases hydraulic fluid, gear oil, and grease consumption across heavy-duty equipment operations nationwide.

- Infrastructure & Agribusiness Investment: Government infrastructure programs including the New Growth Acceleration Program (PAC) and agricultural credit expansion under the Safra Plan fuel demand for construction machinery and agricultural equipment lubricants, particularly hydraulic fluids and greases in high-stress applications.

Market Restraints

- Base Oil Price Volatility: Fluctuations in base oil prices, which are closely linked to crude oil market trends, continue to create revenue and margin volatility for lubricant blenders. Periodic swings in global crude oil prices during recent years have pressured blender profitability and prompted inventory destocking behaviors among distributors and end users across the supply chain.

- Regulatory and Tax Complexity: Brazil's complex tax structure, including ICMS state tax varying by product and region and PIS/COFINS levies, creates regulatory compliance burdens for lubricant distributors and affects product pricing competitiveness across different Brazilian states and distribution tiers.

Market Opportunities

- Electric Vehicle Lubricant Demand: Electric vehicle penetration in Brazil, while nascent at under 3% of new vehicle sales in 2024, is expanding under government EV incentive programs. EVs require specialized thermal management fluids and e-fluids for battery cooling and transmission systems, creating new premium lubricant product categories.

- Pre-Salt Oil Exploration Expansion: Brazil's pre-salt oil exploration expansion and deepwater drilling activity drive demand for specialized lubricants including compressor oils, drilling fluids, and offshore equipment lubricants with extreme-pressure and corrosion-resistance performance attributes in harsh marine environments.

Market Challenges

- Counterfeit Lubricant Market: The presence of counterfeit and substandard lubricants in the informal market continues to challenge branded manufacturers by eroding margins and intensifying price competition. These low-quality products also create operational and safety risks in vehicle and industrial machinery maintenance applications, impacting consumer trust and overall market standards.

- Extended Drain Interval Pressure: Extended oil drain intervals for modern synthetic lubricants and improving engine technology reduce lubricant volume consumption per vehicle over time, partially offsetting fleet growth-driven demand expansion and creating pressure on overall market volume growth rates.

Emerging Market Trends

1. Accelerating Shift to Synthetic and Semi-Synthetic Lubricants

Brazilian consumers and fleet operators are migrating from mineral to synthetic lubricants, driven by OEM requirements for modern turbocharged engines, longer drain interval economics, and growing awareness of fuel efficiency benefits from lower-viscosity synthetic formulations that reduce internal engine friction.

2. Bio-Based Lubricant Adoption Under Environmental Regulations

Brazil's regulatory environment, particularly CONAMA environmental resolutions and corporate sustainability mandates, is driving adoption of bio-based lubricants derived from soy, castor oil, and sugarcane derivatives, sectors where Brazil holds significant agricultural competitive advantage globally.

3. Digital Distribution and E-Commerce Channel Expansion

Online lubricant sales through major e-commerce platforms and manufacturer direct-to-consumer channels are expanding, particularly for passenger vehicle engine oils. Partnerships with digital retail marketplaces have established new commercial infrastructure that multiple lubricant brands are now actively replicating across Brazil.

4. IIoT-Enabled Condition-Based Lubrication Management

Industrial Internet of Things connected machinery sensors enabling real-time oil condition monitoring and predictive maintenance scheduling are increasingly adopted in Brazilian manufacturing plants, shifting lubricant procurement from fixed-interval replacement toward condition-based optimization favoring premium long-life products.

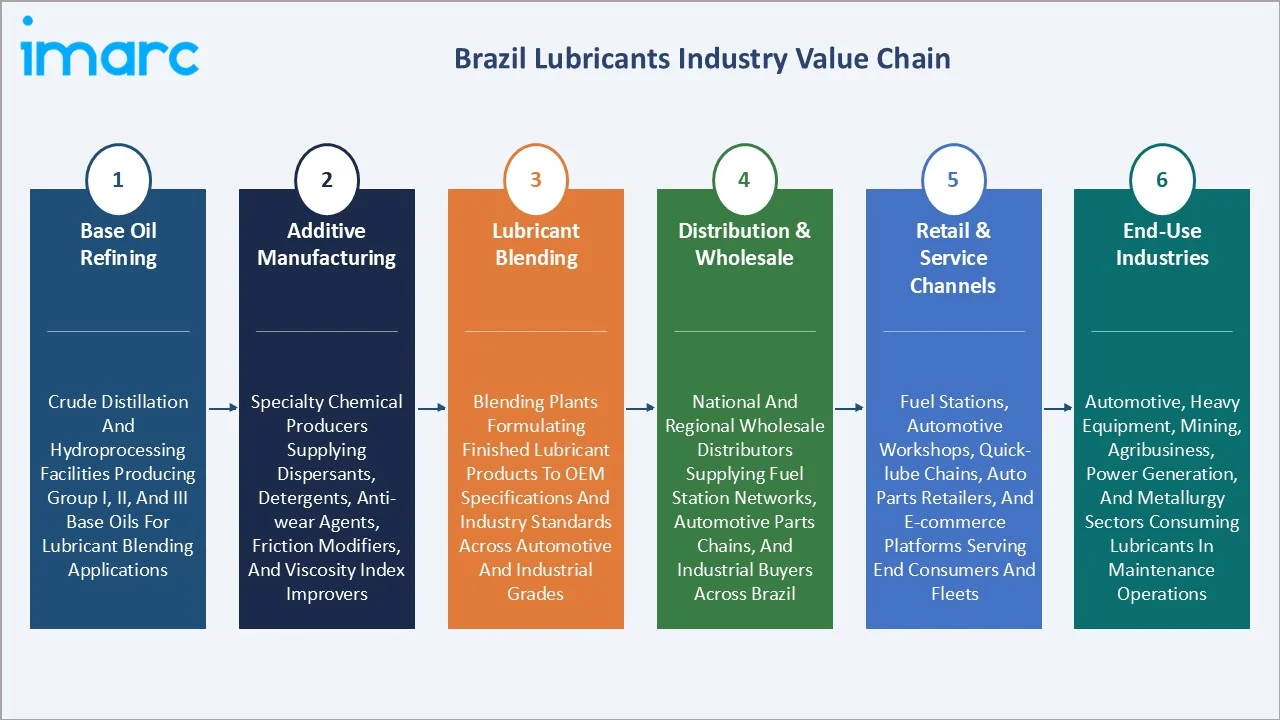

Industry Value Chain Analysis

The Brazil lubricants value chain spans six stages from crude oil refining through end-use maintenance. Blending and additive incorporation capture the highest value-add margins, while distribution logistics and retail channel management represent significant working capital requirements favoring well-capitalized national distributors and blenders.

|

Stage |

Description |

|

Base Oil Refining |

Crude distillation and hydroprocessing facilities producing Group I, II, and III base oils for lubricant blending applications |

|

Additive Manufacturing |

Specialty chemical producers supplying dispersants, detergents, anti-wear agents, friction modifiers, and viscosity index improvers |

|

Lubricant Blending |

Blending plants formulating finished lubricant products to OEM specifications and industry standards across automotive and industrial grades |

|

Distribution & Wholesale |

National and regional wholesale distributors supplying fuel station networks, automotive parts chains, and industrial buyers across Brazil |

|

Retail & Service Channels |

Fuel stations, automotive workshops, quick-lube chains, auto parts retailers, and e-commerce platforms serving end consumers and fleets |

|

End-Use Industries |

Automotive, heavy equipment, mining, agribusiness, power generation, and metallurgy sectors consuming lubricants in maintenance operations |

Integrated lubricant manufacturers with captive base oil refining arrangements and in-house blending capabilities achieve lower material cost bases than processors relying entirely on spot-market base oil procurement. This vertical integration represents a meaningful competitive advantage in commodity market segments where price competition is intense.

Technology Landscape in the Brazil Lubricants Industry

Base Oil Technology: Group II and III Transition

Brazil's lubricant industry is transitioning from Group I base oils toward Group II and III hydroprocessed base oils, improving oxidation stability, viscosity index, and compatibility with modern engine requirements. This base oil evolution underpins the broader shift toward synthetic and semi-synthetic lubricant formulations across automotive and industrial segments.

Additive Technology: Multifunctional Packages and Nano-Additives

Advanced additive packages combining dispersants, detergents, anti-wear agents, friction modifiers, and viscosity index improvers enable modern lubricant formulations to meet increasingly stringent API SN Plus, ILSAC GF-6, and ACEA specifications demanded by vehicle OEMs. Nano-particle additives incorporating molybdenum disulfide derivatives are entering premium product lines.

Synthetic Lubricant Technology: PAO and Ester-Based Formulations

Polyalphaolefin and synthetic ester-based fully synthetic lubricants deliver superior low-temperature fluidity, thermal stability, and extended drain capabilities. These advanced formulations cater to the increasing demand for specialized lubricants in automotive, industrial, and mining sectors, ensuring equipment performs optimally under Brazil's diverse and demanding operating conditions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Engine Oils |

42.6% |

2025 |

|

End User |

Automotive |

55.3% |

2025 |

|

Region |

Southeast |

38.7% |

2025 |

By Product Type

Engine oils command a 42.6% majority share in 2025, driven by Brazil's large and growing vehicle fleet. Engine oils are non-discretionary maintenance consumables with regulatory and OEM-mandated replacement intervals, creating predictable recurring demand across passenger cars, commercial trucks, motorcycles, and agricultural machinery powertrains throughout Brazil.

To access detailed market analysis, Request Sample

Transmission and gear oils (18.4% in 2025) serve manual and automatic transmissions, differentials, and axles in automotive and heavy equipment applications. Hydraulic fluids (14.7%) are critical for construction equipment, agricultural machinery, and industrial hydraulic systems, benefiting from Brazil's infrastructure investment cycle. Greases (9.8%) serve heavy-duty industrial and agricultural equipment requiring long-lasting lubrication under extreme pressure and temperature conditions. Metalworking fluids (7.6%) support Brazil's manufacturing and auto parts production sector.

By End User

The automotive segment dominates with 55.3% in 2025, reflecting the country’s large and expanding vehicle parc along with strong aftermarket maintenance activity, the automotive segment continues to dominate lubricant consumption. Demand is supported by both OEM factory-fill requirements and ongoing aftermarket servicing needs, contributing to the segment’s sustained market leadership and stable growth trajectory.

Heavy equipment (16.8% in 2025) serves Brazil's mining, construction, and agribusiness sectors, where high-value machinery requires premium lubricants with extended drain intervals and extreme-pressure performance. Metallurgy and metalworking (11.7%) demands specialized cutting fluids, quenching oils, and rust preventives supporting Brazil's steel and auto parts manufacturing sectors.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

38.7% |

Largest automotive manufacturing hub; highest vehicle and industrial concentration; major metropolitan demand centers |

|

South |

22.4% |

Agribusiness mechanization; metalworking and food processing industries; active port-driven logistics lubricant demand |

|

Central-West |

16.3% |

Rapid agricultural expansion; growing demand for agricultural equipment lubricants; agro-industrial processing development |

|

Northeast |

13.5% |

Infrastructure investment; growing manufacturing zones; petrochemical industrial complex driving industrial lubricant demand |

|

North |

9.1% |

Industrial district activities; oil and gas exploration; nascent manufacturing base generating increasing lubricant demand |

Southeast Brazil's 38.7% market dominance in 2025 is driven by the most structurally concentrated combination of automotive manufacturing, industrial activity, and vehicle density in Brazil. The Southeast hosts the country's largest automotive OEM production cluster and the highest concentration of industrial facilities requiring regular lubricant maintenance and replacement.

South region's 22.4% share is anchored by agribusiness-linked equipment lubricant demand, with expanding soybean, corn, and food processing sectors requiring extensive machinery lubrication. Central-West (16.3%) reflects Brazil's agricultural frontier expansion, with large-scale farming mechanization requiring hydraulic fluids and greases for agricultural equipment across the Cerrado biome.

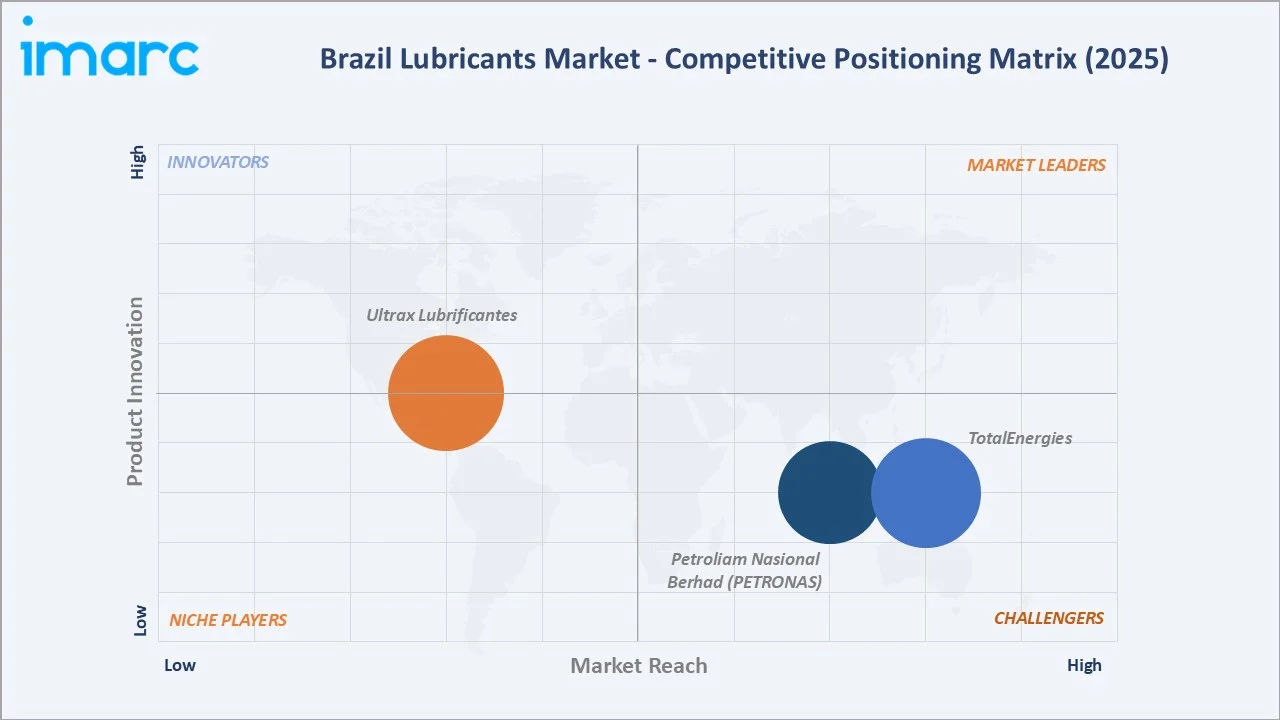

Competitive Landscape

The Brazil lubricants market is moderately concentrated, with multinational oil majors commanding significant shares alongside domestic players maintaining strong positions in specific product and regional segments.

|

Company Name |

Key Products |

Position |

Strategic Focus |

|

Ultrax Lubrificantes |

Top1, PDV, Extron Lubrificantes, Lubrioil |

Emerging |

Independent lubricant producers, brand licensor, multi-brand portfolio |

|

Petroliam Nasional Berhad (PETRONAS) |

Syntium, Urania, Tutela |

Challenger |

Growing Brazil presence; OEM partnerships; competitive pricing strategy |

|

TotalEnergies |

Total Quartz, Rubia, Azolla, CLASSIC 5 SF SAE 40, CLASSIC 9 LL 5W-30 |

Challenger |

Industrial lubricants strength; European OEM specifications; growing commercial fleet |

Key players include Ultrax Lubrificantes, Petroliam Nasional Berhad (PETRONAS), TotalEnergies, and others.

Key Company Profiles

Petroliam Nasional Berhad (PETRONAS)

Petroliam Nasional Berhad (PETRONAS) is an energy company operating across the full oil and gas value chain, with a significant and growing presence in Brazil spanning upstream exploration, downstream lubricants, and retail fuel distribution.

- Product Portfolio: Offers Syntium, Urania, Tutela, and others.

- Recent Developments: In November 2022, PETRONAS announced its first oil discovery in Brazil’s Sepia Field, marking a significant milestone in the company’s upstream expansion strategy and strengthening its presence in the country’s offshore energy sector. The discovery also highlights the growing investment potential of Brazil’s deepwater reserves and reinforces the region’s importance in global energy production.

- Strategic Focus: PETRONAS Lubricants International's Brazil strategy is built on four pillars: leveraging its Mercedes-AMG PETRONAS Formula One technical partnership to position the Syntium range as the premium automotive engine oil of choice; expanding retail channel access through its branded fuel station pilot with distributor SIM Distribuidora, targeting SIM's 540-station network across southern Brazil; and using Brazil as a regional supply hub serving over 20 countries across Latin America and the Caribbean.

Ultrax Lubrificantes

Ultrax Lubrificantes is one of Brazil's largest independent lubricant producers, founded in 2002 and headquartered in Pederneiras, São Paulo, one of the country's largest lubricant markets. Operating as both a producer and brand licensor, Ultrax serves the automotive, industrial, and agricultural segments through a multi-brand portfolio and an intermodal logistics network spanning road, rail, and navigable waterways connecting Brazil with Mercosur states and countries.

- Product Portfolio: Offers Top1, PDV, Extron Lubrificantes, Lubrioil, and others.

- Strategic Focus: Ultrax's strategy centers on consolidating its position as the leading independent domestic lubricant producer by leveraging its Southeast manufacturing base, intermodal logistics advantage, and multi-brand licensing model.

Market Concentration Analysis

The Brazil lubricants market is moderately concentrated, with the top five players accounting for approximately 60–65% of total sales volume, with a fragmented tail of over 3,000 registered lubricant brands including regional blenders, specialty formulators, and importers serving niche segments and geographic markets.

Consolidation is occurring through multinational joint ventures combining global brand and technology assets with domestic distribution networks. Integrated manufacturers with vertical base oil refining advantages maintain structural cost advantages that smaller domestic blenders dependent on imported base oils cannot easily replicate in price-competitive market segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Synthetic lubricants at ~4.1% CAGR through 2034 represent the highest-growth product category, driven by OEM mandates for modern engine formulations and consumer premiumization. Engine oils at ~3.7% CAGR and hydraulic fluids at ~3.5% CAGR benefit from fleet expansion and Brazil's infrastructure investment under government development programs.

Emerging Market Opportunities

Electric vehicle fluids represent the emerging premium growth category, with EV coolants, e-transmission fluids, and battery thermal management fluids anticipated to grow at double-digit rates from a small base as Brazil's EV adoption accelerates through government incentive programs and declining electric vehicle acquisition costs.

Venture & Investment Trends

Private equity interest in Brazilian lubricant distribution and blending is increasing, driven by the market's recession-resilient demand profile and attractive operating margins at the specialty blending level. Bio-lubricant companies leveraging Brazil's agricultural raw material base are attracting investment aligned with environmental, social, and governance mandates.

Future Market Outlook (2026-2034)

The Brazil lubricants market is forecast to expand from USD 3.93 Billion in 2025 to USD 5.28 Billion by 2034 at a CAGR of 3.33%, adding USD 1.35 Billion in incremental annual market value over the forecast period. This consistent growth reflects the market's transportation and industrial-linked, non-discretionary demand characteristics across all Brazilian regions.

Three structural forces will most significantly shape the Brazil lubricants industry through 2034: the transition from mineral to synthetic lubricants across automotive and industrial segments, electric vehicle proliferation creating demand for new specialized fluid categories, and Brazil's continuing agricultural mechanization driving hydraulic fluid and grease volumes in rapidly expanding farming regions.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Brazil lubricant industry stakeholders, including commercial managers at major blenders, automotive workshop chains, industrial distributors, fleet maintenance managers, and regulatory body data teams. Primary data validated market sizing, product type and end-user segment shares, and regional demand estimates.

Secondary Research

Key secondary sources include Brazil ANP Statistical Yearbook of Petroleum and Natural Gas, ANFAVEA automotive production and registration data, IBGE industrial production indices, industry association reports, and trade publications covering the Brazilian automotive, industrial, and lubricant market sectors.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating Brazil GDP growth rates, vehicle fleet expansion rates, industrial production indices, and historical lubricant volume consumption data. Scenario analysis covering base, optimistic, and conservative macroeconomic trajectories was performed.

Brazil Lubricants Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Engine Oils, Greases, Hydraulic Fluids, Metalworking Fluids, Transmission and Gear Oils, Others |

| End Users Covered | Automotive, Heavy Equipment, Metallurgy and Metalworking, Power Generation, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Ultrax Lubrificantes, Petroliam Nasional Berhad (PETRONAS), TotalEnergies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil lubricants market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Brazil lubricants market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil lubricants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Lubricants Market Report

The Brazil lubricants market reached USD 3.93 Billion in 2025, reflecting sustained demand from automotive fleet growth, industrial expansion, and agribusiness mechanization across Brazil's diverse regional markets.

The market is projected to reach USD 5.28 Billion by 2034, growing at a CAGR of 3.33% during 2026-2034, driven by vehicle fleet growth, industrial lubricant demand, and synthetic lubricant adoption across sectors.

Engine oils lead with 42.6% product type share in 2025, valued for their non-discretionary automotive maintenance demand and growing synthetic oil premiumization across Brazil's expanding vehicle fleet.

The automotive segment leads at 55.3% in 2025, driven by Brazil's fleet of over 115 million registered vehicles, high aftermarket maintenance activity, and rising consumer demand for premium synthetic engine oils.

Southeast Brazil commands 38.7% market share in 2025, driven by São Paulo's automotive manufacturing concentration, highest vehicle density, and largest industrial base in Latin America.

Synthetic lubricants at ~4.1% CAGR and engine oils at ~3.7% CAGR are the fastest-growing categories through 2034, driven by OEM mandates, fleet expansion, and consumer premiumization trends.

Leading companies include Ultrax Lubrificantes, Petroliam Nasional Berhad (PETRONAS), TotalEnergies, and others.

Key applications include automotive engine lubrication, transmission and gear systems, hydraulic machinery in construction and agriculture, industrial metalworking, heavy equipment maintenance, and power generation turbine and compressor systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)