Canada Packaging Market Size, Share, Trends and Forecast by Packaging Type and Region, 2026-2034

Canada Packaging Market Size, Share, Trends & Forecast (2026-2034)

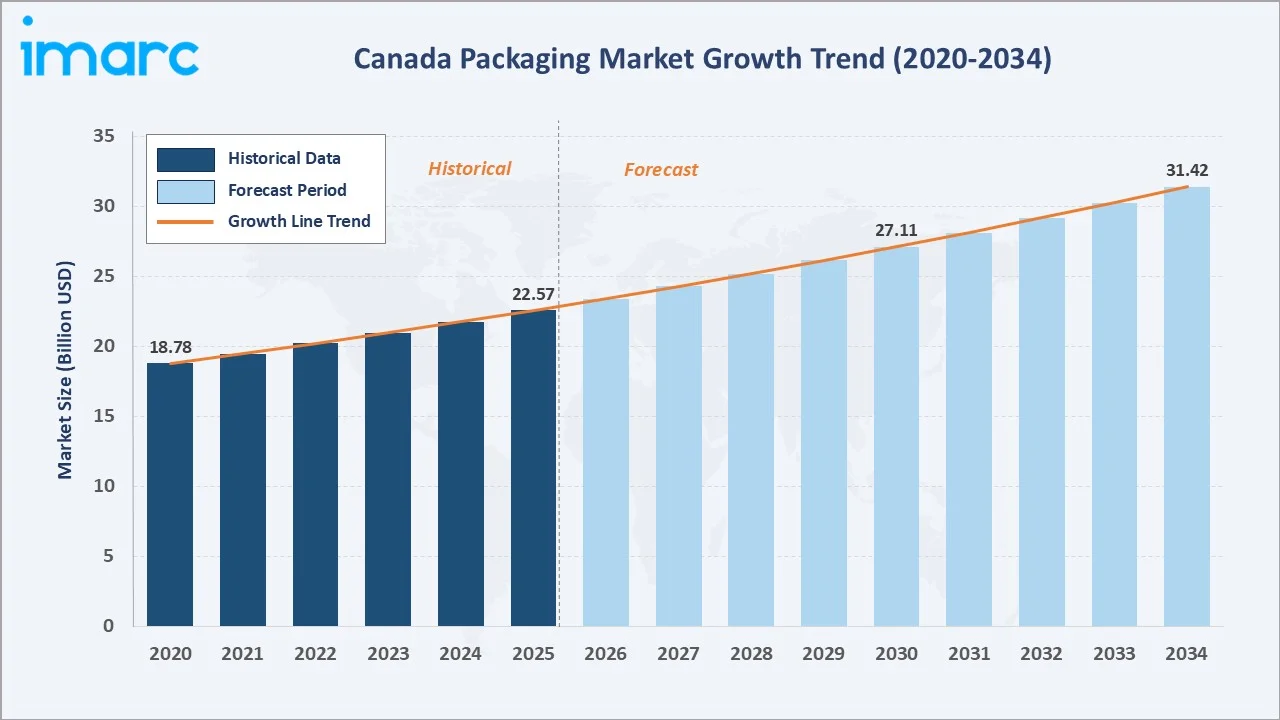

The Canada packaging market reached USD 22.57 Billion in 2025 and is projected to reach USD 31.42 Billion by 2034, growing at a CAGR of 3.74% during 2026 to 2034. Strong food and beverage industry demand, rapid e-commerce expansion driving protective and transit packaging requirements, increasing consumer and regulatory pressure toward sustainable and eco-friendly packaging materials, and smart packaging technology integration are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 22.57 Billion |

|

Forecast Market Size (2034) |

USD 31.42 Billion |

|

CAGR (2026-2034) |

3.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

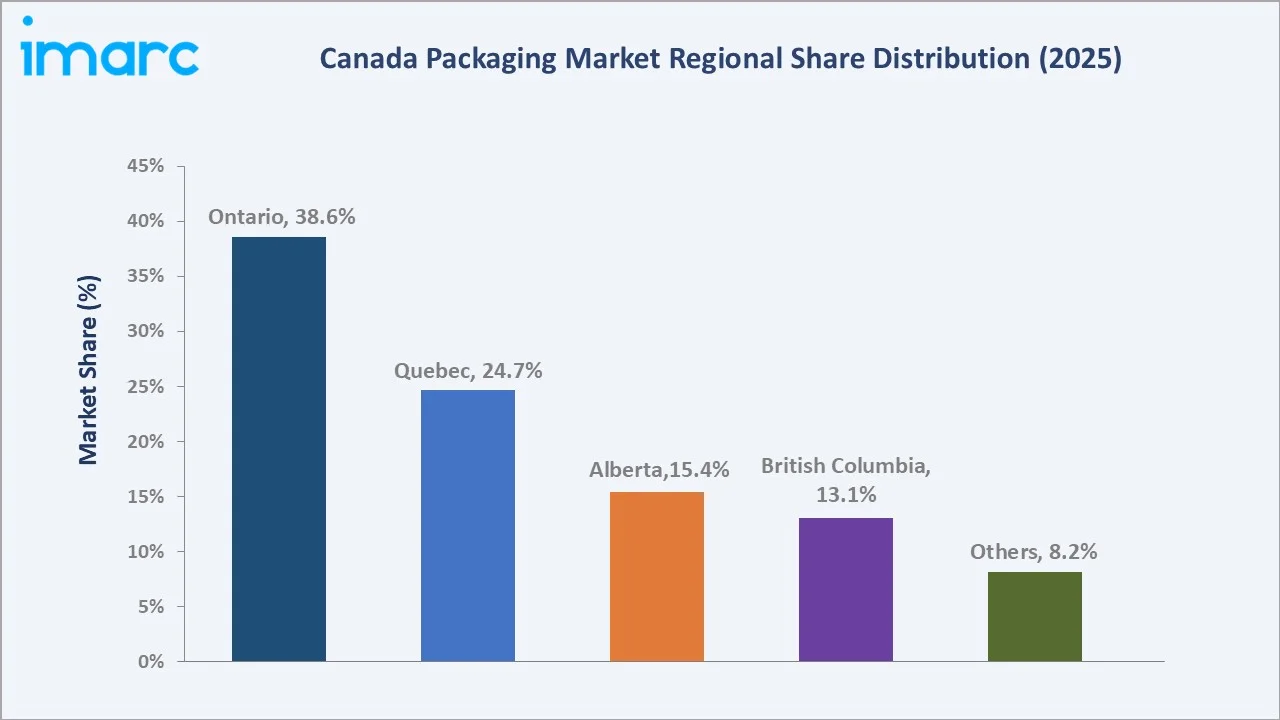

Ontario leads among Canadian provinces with a 38.6% market share in 2025, driven by its position as Canada’s largest provincial economy and manufacturing hub, the highest concentration of food and beverage and pharmaceutical industry clusters, and the largest consumer market by population. Plastic packaging commands the dominant 44.8% share, reflecting its irreplaceable combination of barrier properties, versatility, light weight, and cost-effectiveness across food and beverage, pharmaceutical, personal care, and retail packaging applications.

To get more information on this market, Request Sample

The Canada packaging market is driven by three structural demand forces: the food and beverage sector’s position as Canada’s largest packaging consumer, absorbing over 55% of total packaging output across fresh, processed, and chilled food categories; the e-commerce revolution that is structurally increasing corrugated board, flexible, and protective packaging demand as retail shifts from physical to online fulfilment; and the sustainability transition driving regulatory change that is redirecting material investment from conventional plastic toward recycled, bio-based, and compostable alternatives.

Executive Summary

The Canada packaging market is experiencing steady growth, driven by the enduring demand from the food and beverage sector, structural growth in e-commerce packaging, and a significant industry transformation toward sustainable materials driven by both consumer preference and regulatory mandate. The market was valued at USD 22.57 Billion in 2025 and is forecast to reach USD 31.42 Billion by 2034, growing at a CAGR of 3.74%.

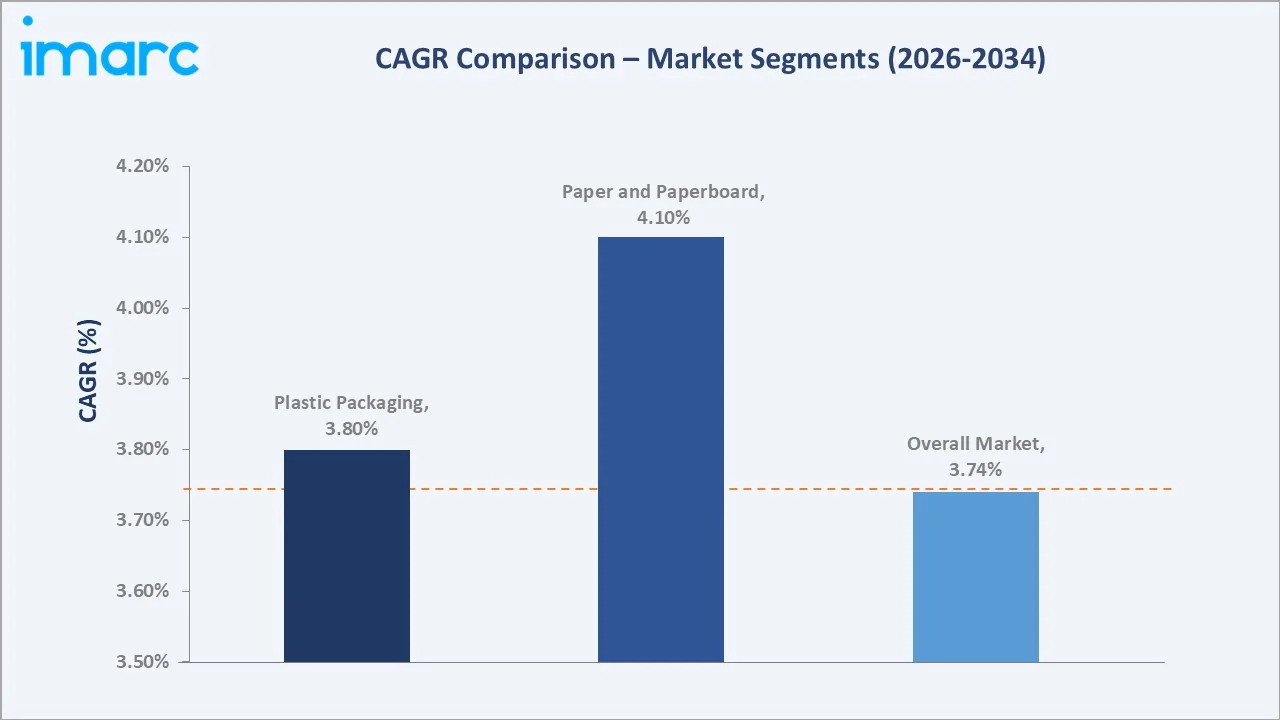

Plastic packaging leads at 44.8% of the packaging type segment in 2025, anchored by flexible plastic’s critical role in food safety, freshness preservation, and the light-weighting of packaging that reduces transport carbon footprint. Paper and paperboard at 31.6% is the fastest-growing packaging type by material substitution, driven by consumer preference for recyclable packaging and the structural growth of corrugated board e-commerce shipping cartons.

Ontario leads at 38.6% of provincial market share, reflecting Canada’s manufacturing concentration in the Greater Golden Horseshoe region. Key players in the market compete across material innovation, sustainability performance, and customer solution depth.

Key Market Insights

|

Insight |

Data |

|

Largest Packaging Type |

Plastic Packaging – 44.8% share (2025) |

|

Fastest Growing Packaging Type |

Paper and Paperboard – 4.1% CAGR (2026-2034) |

|

Leading Region |

Ontario – 38.6% share (2025) |

|

Top Companies |

Amcor plc, Sealed Air Corporation, Wihuri Group, and Silgan Holdings Inc.

|

Key Analytical Observations Supporting The Above Data:

- Plastic packaging at 44.8% (2025) leads despite regulatory pressure on single-use plastics because the federal ban targets specific single-use items rather than the broader plastic packaging market. Food-grade plastic packaging, including flexible films, rigid containers, closures, and PET bottles, retains its market position based on food safety, barrier, and cost performance that no alternative material currently matches at equivalent total cost of ownership in high-volume food processing applications.

- Paper and paperboard at 31.6% share (2025) is projected to grow at a CAGR of approximately 4.1%, driven by the sustainability substitution of plastic packaging for paper in consumer-facing categories including retail shelf packaging, takeaway food containers, and personal care secondary packaging; and the structural growth of e-commerce corrugated board demand as Canadian e-commerce accounted for 6.1% of total Canadian retail sales in December 2024.

- Metal packaging at 13.9% (2025) is sustained by the beverage can’s resurgence as a premium sustainable format, driving share gains versus glass in both alcohol and non-alcohol beverage categories, and the food can’s established position in the Canadian retail grocery market for processed fruit, vegetables, soup, and pet food products.

- Ontario’s 38.6% share (2025) reflects the province’s structural role as Canada’s packaging manufacturing heartland, with the Mississauga, Brampton, Hamilton, and Guelph industrial corridors hosting the highest concentration of packaging converter, printer, and manufacturer operations serving the Greater Toronto Area’s massive consumer market and the province’s food processing and pharmaceutical manufacturing clusters.

Canada Packaging Market Overview

Packaging encompasses all materials, containers, and systems used to contain, protect, transport, display, and identify products throughout the supply chain from manufacturer to end consumer. The Canadian packaging market spans rigid packaging, flexible packaging, corrugated and paperboard packaging, and specialty packaging. Canada’s packaging market is the second-largest in North America, serving a diverse industrial base encompassing food and beverage, pharmaceuticals, personal care, industrial, agricultural, and retail segments.

Macroeconomic drivers include Statistics Canada reporting food manufacturing as Canada’s largest manufacturing sector by value added, representing a structural anchor demand for packaging; online retail sales in Canada reaching approximately USD 3.14 billion (December 2024), creating sustained demand for corrugated, void fill, and protective packaging; and the Canadian government’s 2030 Zero Plastic Waste strategy aiming to extend product lifecycles and divert at least 75% of plastic waste from federal operations by 2030, creating a structural regulatory driver for packaging material transformation investment through the forecast period.

Market Dynamics

To evaluate market opportunities, Request Sample

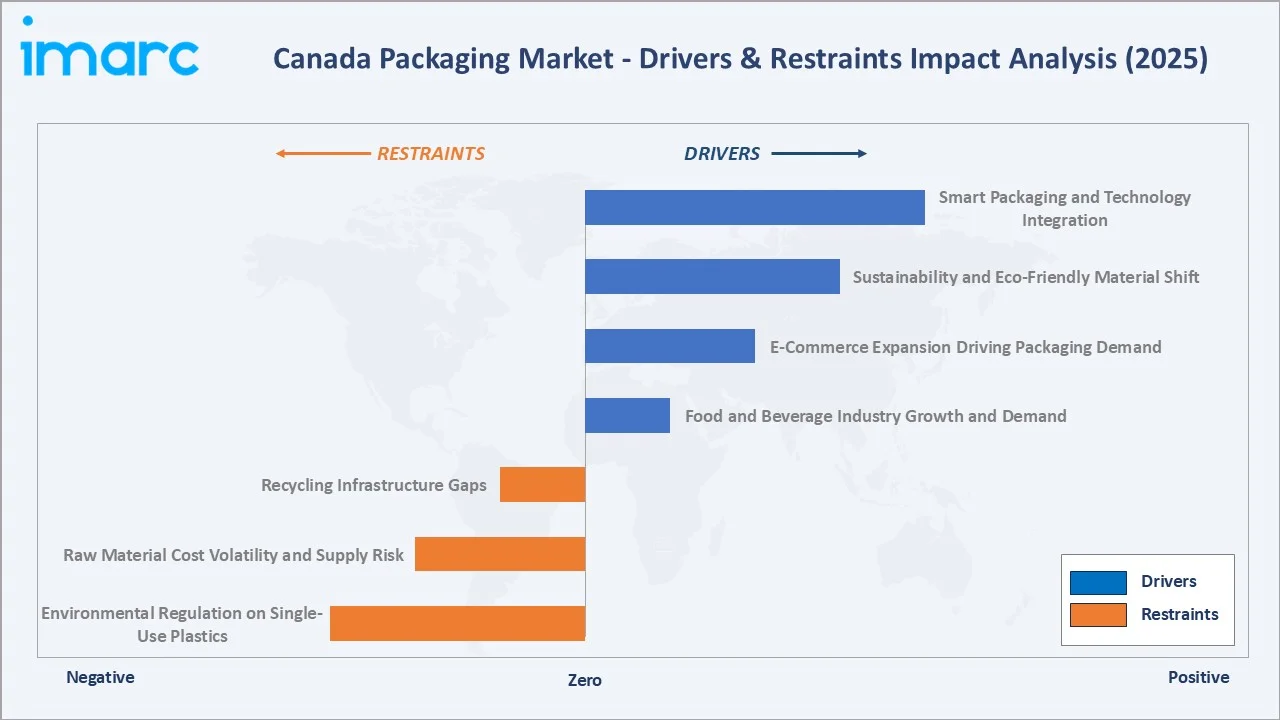

Market Drivers

- Food and Beverage Industry Growth and Demand: According to a new Farm Credit Canada report, Canada could add USD 40 billion to national GDP if its food and beverage sector achieves 3% annual growth, consuming an estimated 55–60% of total packaging output across fresh produce, processed food, dairy, meat and seafood, beverage, and confectionery categories.

- E-Commerce Expansion Driving Packaging Demand: In December 2024, e-commerce represented 6.1% of total retail sales in Canada, with online retail sales reaching approximately USD 3.14 billion, creating structural above-market demand for corrugated shipping cartons, mailers, void fill, and protective packaging.

- Sustainability and Eco-Friendly Material Shift: Canada’s Single-Use Plastics Prohibition Regulations, the Extended Producer Responsibility programs in Ontario, British Columbia, and Quebec, and retail chain sustainability sourcing policies are collectively requiring packaging manufacturers and brand owners to reformulate packaging portfolios toward compliant sustainable alternatives.

- Smart Packaging and Technology Integration: The adoption of active and intelligent packaging technologies is creating a premium packaging technology category growing at above-market rates. The pharmaceutical sector’s adoption of serialization and tamper-evident smart packaging for drug authentication, and the food sector’s adoption of modified atmosphere and active packaging for shelf-life extension, are each driving above-average packaging revenue per unit and creating high-value market segments.

Market Restraints

- Environmental Regulation on Single-Use Plastics: Canada’s federal Single-Use Plastics Prohibition Regulations, combined with provincial EPR programs requiring packaging producers to fund end-of-life collection and recycling infrastructure, are creating significant compliance costs and portfolio reformulation requirements for plastic packaging manufacturers.

- Raw Material Cost Volatility and Supply Risk: The COVID-19 supply chain disruption demonstrated the sector’s vulnerability to input cost escalation and material availability constraints, with packaging producers facing simultaneous resin shortages, pulp price spikes, and logistics cost inflation. Ongoing geopolitical factors affecting global commodity markets create persistent input cost uncertainty that limits packaging manufacturer margin management.

- Recycling Infrastructure Gaps: Canada’s packaging recycling infrastructure remains fragmented across provinces, with recycling rates for plastic packaging well below the government’s 100% by 2030 target. Limited availability of food-grade recycled resin supply, insufficient sorting infrastructure for multi-material flexible packaging, and inconsistent provincial recycling program standards collectively limit the pace at which packaging converters can incorporate recycled content at the volumes required by brand owner sustainability commitments.

Market Opportunities

- Bio-Based and Compostable Packaging Innovation: Canada’s agricultural sector provides abundant bio-based feedstock for bio-based plastics and compostable packaging material production. The convergence of federal policy support for circular economy innovation, brand owner commitment to compostable packaging targets, and growing foodservice compostable packaging demand is creating commercial opportunity for bio-based packaging manufacturers that can compete with conventional plastic on performance and total cost at commercial scale.

- Extended Producer Responsibility Program Packaging: Provincial EPR programs are creating new funding models that support collection, sorting, and reprocessing infrastructure investment. EPR frameworks that assign recycling cost to producers create a competitive advantage for packaging designs with proven recyclability, incentivizing packaging portfolio redesign and creating premium positioning for certified recyclable packaging solutions.

Market Challenges

- Transition to Circular Economy at Scale: The packaging industry’s transition from a linear model to a circular economy, where packaging materials are continuously recovered and reprocessed into new packaging, requires systemic change across design, material selection, collection infrastructure, and reprocessing investment that exceeds the capability of individual companies to implement independently. The pace of this systemic transition is constrained by fragmented provincial regulatory frameworks, insufficient investment in material recovery infrastructure, and consumer behavior change barriers that limit participation in collection programs.

- Lightweight and Material Reduction Pressure: Brand owner sustainability programs and regulatory pressure are driving continuous lightweighting of packaging that structurally constrains market revenue growth by reducing material volume per packaging unit. The industry’s technical innovation investment in thinner films, optimized container designs, and higher-strength materials that enable lightweighting can paradoxically limit revenue growth while improving the packaging’s environmental performance metrics.

Emerging Market Trends

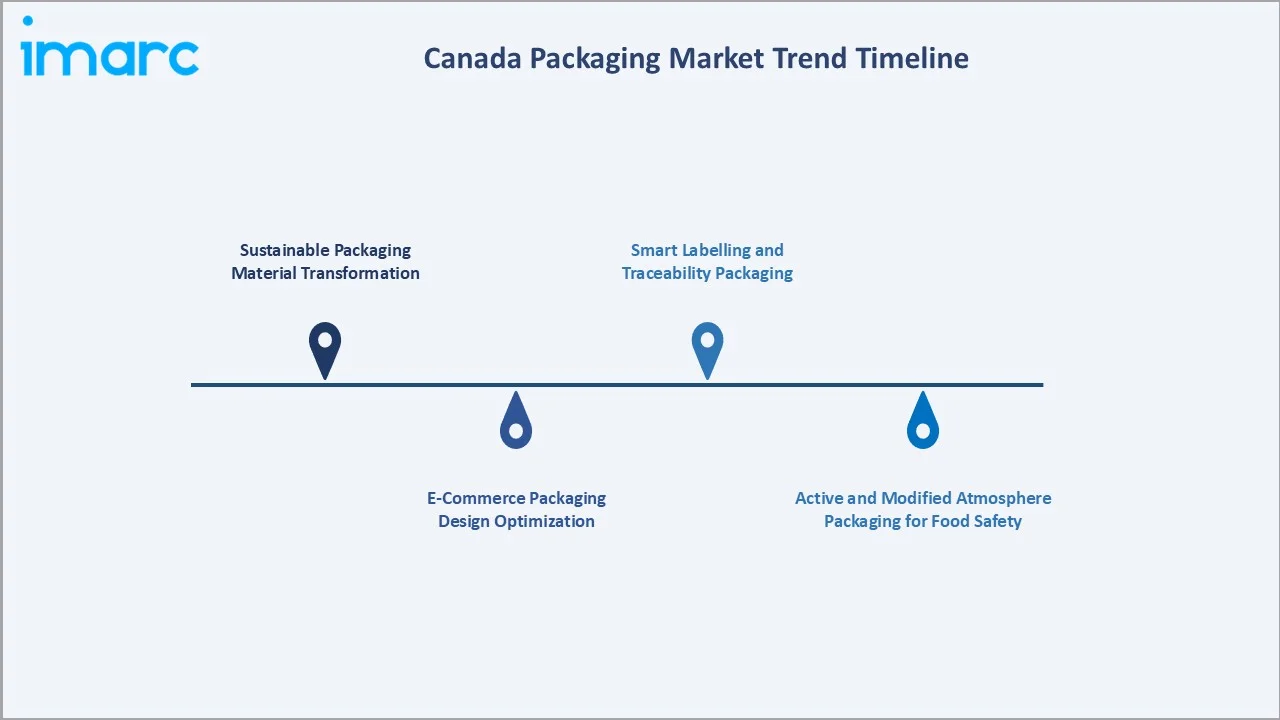

1. Sustainable Packaging Material Transformation

The transformation of Canada’s packaging material portfolio toward recycled, bio-based, and compostable alternatives is the dominant structural trend reshaping the industry through 2034. Federal Single-Use Plastics Prohibition Regulations, provincial EPR programs, and brand owner 2025–2030 packaging sustainability commitments are collectively mandating portfolio transformation at a pace and scale requiring significant R&D and capital investment from packaging manufacturers. Winpak’s partnership with PureCycle Technologies for ultra-pure recycled polypropylene and Amcor’s AmPrima sustainable flexible packaging range exemplify the commercial sustainable packaging innovation response to regulatory and market demand.

2. E-Commerce Packaging Design Optimization

The structural growth of Canadian e-commerce is driving dedicated packaging innovation for the direct-to-consumer supply chain, where packaging must protect products through multiple handling events, minimize dimensional weight for shipping cost management, and deliver a positive unboxing experience that reinforces brand perception. Right-sized packaging systems, paper-based mailers replacing polybag mailers, cushioning material shift from expanded polystyrene to paper-based alternatives, and re-sealable and returnable packaging for circular e-commerce models are the primary e-commerce packaging design trends attracting investment from Canadian packaging converters.

3. Active and Modified Atmosphere Packaging for Food Safety

Canadian food processors are adopting active packaging technologies, including oxygen scavengers, moisture regulators, and ethylene absorbers, and modified atmosphere packaging (MAP) systems that extend product shelf life by 50–200% versus standard air-filled packaging. These technologies enable food manufacturers to reduce food waste, extend distribution radius, and reduce preservative use, trends that are simultaneously commercially attractive and environmentally aligned.

4. Smart Labelling and Traceability Packaging

QR codes, NFC tags, and RFID integration in packaging are enabling full supply chain traceability from producer to consumer, supporting food safety recall management, brand anti-counterfeiting, and consumer engagement programs that provide usage guidance, recycling instructions, and brand loyalty incentives. Health Canada’s pharmaceutical serialization requirements and the Canadian Food Inspection Agency’s food traceability framework are mandating smart packaging adoption in regulated sectors, creating a compliance-driven adoption wave that is establishing the infrastructure for broader smart packaging deployment across consumer goods categories.

Industry Value Chain Analysis

The Canadian packaging value chain spans from raw material and feedstock supply through manufacturing, converting, distribution, end-use deployment, and end-of-life management.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Petrochemical resin producers, pulp and paper mills, aluminum and tinplate producers, and recycled material processors |

|

Packaging Manufacturers |

Plastic packaging converters, paper and paperboard carton producers, metal can manufacturers, and glass container producers |

|

Converters & Processors |

Printing and decoration specialists, laminating and coating processors, die-cutting and forming operations, and kitting providers |

|

Distributors & Logistics |

Packaging distributors, third-party logistics and warehousing providers, and import and export intermediaries |

|

End-Use Industries |

Food and beverage manufacturers, pharmaceutical and healthcare companies, personal care and household product brands, and e-commerce fulfilment operators |

|

After-Sales & Compliance Providers |

Extended Producer Responsibility (EPR) program operators, municipal recycling facilities, and waste management companies |

Technology Landscape in the Canada Packaging Industry

Flexible Packaging Technology

Flexible packaging is one of the highest-growth packaging technology categories in Canada, combining superior product protection per gram of material, efficient retail shelf space utilization, and consumer convenience features including reclosable zippers, pour spouts, and microwave-safe formats. The industry’s technical challenge is the recyclability of multi-material flexible packaging, where different polymer layers provide distinct barrier and mechanical properties but are difficult to separate for recycling. Development of mono-material flexible packaging retaining barrier performance using advanced coating and film technology is the primary sustainable flexible packaging R&D investment priority.

Corrugated and Paperboard Packaging Technology

Corrugated board innovation is addressing e-commerce packaging requirements through engineered high-performance fluting, water-based adhesive systems, and digital printing capability that enables on-demand customized shipping carton production. Canadian corrugated converters are investing in box-on-demand systems that produce exact-fit cartons for e-commerce orders, eliminating void fill material and reducing cubic shipping volume. The industry’s sustainability advantage positions paper-based packaging as the compliant default for e-commerce applications.

Extended Producer Responsibility Technology Platforms

EPR program administration in Ontario, British Columbia, and Quebec is driving investment in digital material reporting systems that track packaging placed on the market by each producer, enabling accurate fee calculation, compliance verification, and recycled content claim validation. These platforms are creating transparency infrastructure that enables circular economy material flow management and verifiable recycled content certification that supports brand owner sustainability reporting and regulatory compliance across Canada’s multi-provincial EPR framework.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Packaging Type |

Plastic Packaging |

44.8% |

2025 |

|

Region |

Ontario |

38.6% |

2025 |

By Packaging Type

Plastic packaging leads with a 44.8% share of the Canada packaging market in 2025, reflecting its technically irreplaceable performance in food packaging applications requiring high oxygen and moisture barrier, heat-seal capability for modified atmosphere packaging, and flexible form factors for retail consumer packaging. PET bottles for beverages, PE films for fresh produce and meat, PP containers for dairy and deli products, and multilayer flexible pouches for processed food collectively represent the core Canadian plastic packaging market segments.

To access detailed market analysis, Request Sample

Paper and paperboard at 31.6% share (2025) is projected to grow at the fastest rate at approximately 4.1% CAGR, driven by e-commerce corrugated demand, sustainable packaging substitution from plastic in retail shelf and secondary packaging, and the natural consumer preference for paper-based packaging that communicates sustainability credentials. Metal packaging at 13.9% serves the beverage can, food can, aerosol, and paint can markets, with the beverage can experiencing volume growth driven by its sustainability credentials and the craft beer and sparkling water market’s preference for cans.

Regional Market Insights

Ontario’s dominant position (38.6%, 2025) reflects the province’s structural role as Canada’s manufacturing heartland, with the largest concentration of food and beverage manufacturers, pharmaceutical producers, and retail and consumer goods companies that collectively generate the highest packaging demand volume of any Canadian province.

Quebec at 24.7% benefits from its large and integrated food processing sector, the province’s dairy, bakery, meat, and processed food industries each representing major packaging consumers, and its established paper and paperboard manufacturing infrastructure leveraging provincial forest resources. Alberta, at 15.4%, serves the energy sector’s industrial packaging requirements alongside a growing food processing sector.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Ontario |

38.6% |

One of Canada's largest provincial economies and manufacturing hubs with concentrated food and beverage and pharmaceutical industry clusters, and major packaging manufacturing and distribution infrastructure |

|

Quebec |

24.7% |

Strong food processing and dairy industry driving flexible and rigid packaging demand, established paper and paperboard manufacturing industry leveraging provincial forest resources, and significant pharmaceutical packaging activity |

|

Alberta |

15.4% |

Energy sector and industrial packaging demand, growing food processing sector in Calgary and Edmonton, and expanding retail and e-commerce fulfilment packaging requirements |

|

British Columbia |

13.1% |

Asia-Pacific trade gateway creating import and export packaging demand, strong beverage and seafood processing industries, growing sustainable packaging adoption, and expanding technology sector e-commerce activity |

|

Others |

8.2% |

Prairie agricultural provinces driving grain and food packaging, Atlantic Canada seafood processing & packaging, and northern territories’ remote supply chain packaging requirements for food and consumer goods |

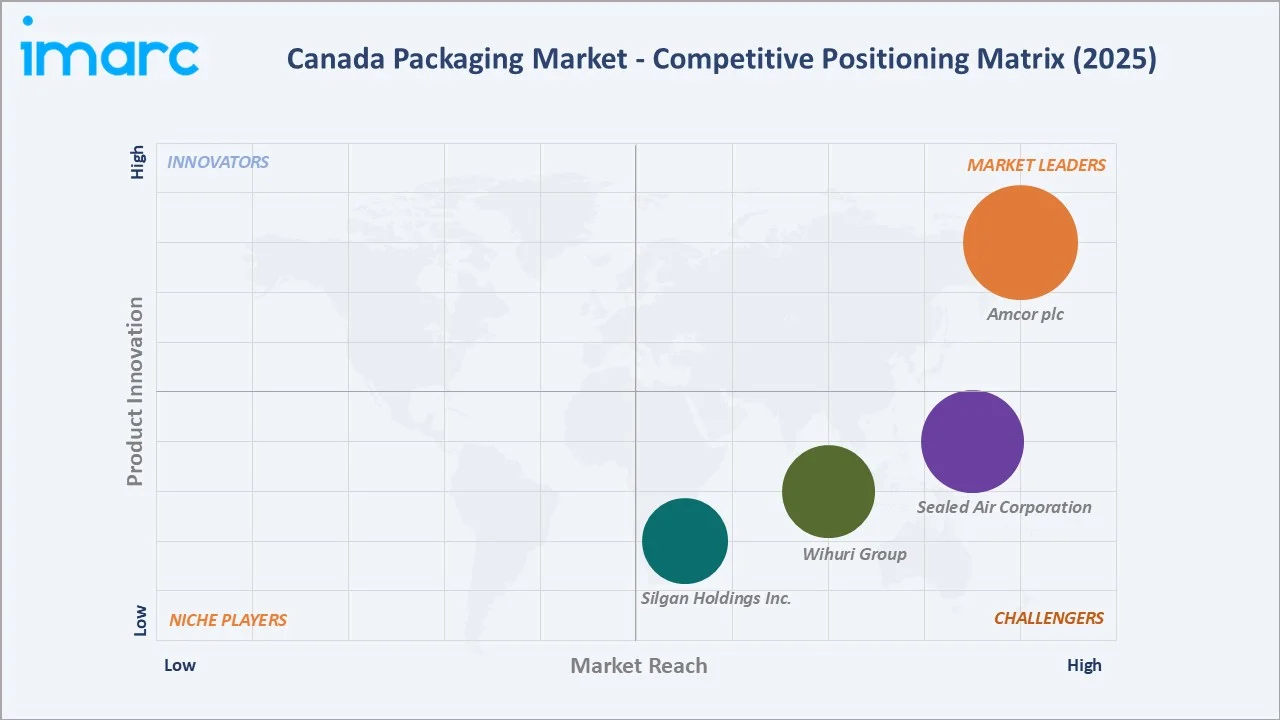

Competitive Landscape

The Canadian packaging market exhibits moderate concentration, with a mix of large multinational packaging corporations and strong Canadian-headquartered packaging companies competing across material segments, regional geographies, and end-use industry verticals.

|

Company Name |

Key Products/Brands |

Market Position |

Core Strength |

|

Amcor plc |

Flexible, rigid, specialty packaging |

Market Leader |

One of the global packaging leaders with significant Canadian operations, a broad portfolio spanning food, beverage, pharmaceutical, and personal care packaging segments |

|

Sealed Air Corporation |

Cryovac, Liquibox, Autobag, Bubble Wrap, SealedAir, Nexcel |

Strong Challenger |

Food protection packaging leadership; dominant in Canadian meat and dairy processing; protective e-commerce packaging growth in Bubble Wrap |

|

Wihuri Group |

Food Packaging, Pouches, Healthcare Packaging |

Strong Challenger |

Strong modified atmosphere packaging for food; growing sustainable flexible packaging portfolio |

|

Silgan Holdings Inc. |

Dispensing and Specialty Closures, Metal Containers, and Custom Containers |

Challenger |

North American metal packaging leader with Canadian operations; strong food can and closures position; growing healthcare packaging segment |

The competitive landscape is shaped by the packaging industry’s ongoing sustainability transition, which is creating new competitive differentiation opportunities around certified recycled content, verified compostability, EPR program compliance documentation, and Science-Based Targets-aligned carbon footprint reduction.

Key Company Profiles

Amcor plc

Amcor plc is one of the world’s largest packaging companies by revenue, with significant Canadian manufacturing and commercial operations. Its Canadian presence spans flexible packaging, rigid packaging, and specialty pharmaceutical packaging, serving the country’s largest food, beverage, and healthcare brand owner customers.

- Product Portfolio: Flexible packaging, plastic containers, sustainable packaging, Amcor Healthcare pharmaceutical packaging, flexible laminations for food and personal care, and specialty medical device packaging.

- Recent Developments: In January 2026, Amcor plc joined the City of Ottawa’s The Reuse City Canada Project, supporting efforts to reduce single-use packaging waste through scalable reuse systems for foodservice and consumer packaging. The collaboration aims to advance circular economy practices and increase the adoption of reusable packaging solutions across the city.

- Strategic Focus: 100% recyclable or reusable packaging commitment; recycled content integration across flexible and rigid portfolios; pharma packaging growth; sustainable innovation platform development.

Wihuri Group

Wihuri Group’s majority-controlled subsidiary Winpak Ltd. is one of Canada’s largest publicly traded packaging companies, specializing in modified atmosphere packaging films, flexible lidding, and rigid packaging for food, medical, and industrial applications.

- Product Portfolio: Mono and multilayer films, thermoform lidding, flexible pouches, modified atmosphere packaging systems, rigid trays and containers, medical packaging, and industrial packaging.

- Recent Developments: In July 2025, Winpak Ltd. announced that the company’s Winnipeg, Manitoba site became an authorized converter of DuPont Tyvek® healthcare packaging. The move expands medical device, pharmaceutical, and healthcare packaging coverage across North America, Europe, and Asia.

- Strategic Focus: Recycled content integration in polypropylene-based packaging; MAP film technology advancement for food shelf-life extension; medical packaging growth; sustainable innovation aligned with Canadian EPR requirements.

Market Concentration Analysis

The Canadian packaging market exhibits moderate concentration, with the top five packaging companies collectively accounting for approximately 35–40% of total Canadian packaging market revenue. The remaining 60–65% is distributed among hundreds of regional converters, specialty packaging manufacturers, and distributors serving specific material, geographic, or end-use industry niches. The market’s fragmented structure reflects the diversity of packaging formats, materials, and applications that preclude any single company from achieving dominant market share across all segments simultaneously.

Market consolidation is occurring at the large-format corrugated and flexible packaging tiers, where scale advantages in capital investment, material sourcing, and digital printing capability are driving acquisitions of smaller regional converters by national and multinational platforms. The sustainability transition is also creating consolidation pressure as smaller converters without the R&D investment capacity to develop compliant sustainable alternatives face competitive displacement by larger companies with dedicated sustainable packaging portfolios.

Investment & Growth Opportunities

Fastest Growing Segments

Paper and paperboard packaging (~4.1% CAGR), sustainable flexible packaging (~5–6% for compliant sustainable formats), e-commerce corrugated and mailer packaging (~7–9% annually), and pharmaceutical primary packaging represent the highest-growth investment vectors within the Canadian packaging market through 2034. Bio-based and compostable packaging for foodservice applications is the highest-growth emerging format, growing at above 10% annually from a modest base as federal single-use plastic bans mandate compliance.

Emerging Trends

Several transformative trends are reshaping the Canadian packaging market through 2034. The implementation of national EPR programs across all major provinces by 2026 will create a fully funded packaging collection and recycling ecosystem for the first time in Canada’s history, potentially unlocking the recycled material supply required for brand owners’ recycled content commitments. E-commerce packaging automation is attracting investment from Canadian fulfilment operators seeking to manage packaging labor costs while meeting sustainable packaging commitments.

Technology Investment Trends

- Recycled content integration is the highest-priority packaging technology investment, with Canadian converters investing in process equipment upgrades enabling the use of post-consumer recycled resin while maintaining food contact compliance and product quality standards required by major retailer and brand owner customers.

- Digital printing investment for short-run, personalized, and versioned packaging is growing across corrugated and flexible packaging converters, enabling faster time-to-market for new product launches, cost-effective seasonal and regional packaging variants, and reduced waste from minimum order quantity constraints of conventional print processes.

- Active and intelligent packaging sensor technology investment is concentrated in the food and pharmaceutical sectors, where shelf-life extension, tamper evidence, and supply chain traceability requirements are justifying premium packaging technology adoption at scale sufficient to drive commercial returns on development investment.

Future Market Outlook (2026-2034)

The Canadian packaging market is positioned for steady, sustained growth through 2034. From USD 22.57 Billion in 2025, the market is projected to reach USD 31.42 Billion by 2034, representing total incremental value creation of USD 8.85 Billion at a CAGR of 3.74%.

This growth is underpinned by the food and beverage sector’s continued packaging demand, e-commerce’s structural corrugated and protective packaging volume growth, pharmaceutical packaging expansion, and the sustainability transition that is redirecting investment toward higher-value compliant packaging formats commanding premium unit pricing.

The market’s material composition will continue evolving as paper and paperboard gain share from plastic packaging in consumer-facing sustainable packaging categories, while technical plastic packaging, retaining necessary food safety and barrier functionality, maintains its category position. The implementation of national EPR programs will create more circular material flows, with increasing recycled content mandates gradually reducing virgin material consumption while improving the environmental footprint of Canada’s packaging industry.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 65 industry participants in 2024–2025, including Canadian packaging manufacturer executives, brand owner packaging directors, provincial EPR program administrators, food and beverage industry packaging procurement managers, retail chain packaging compliance specialists, and recycling infrastructure operators. Expert input validated market sizing, segment growth rates, and provincial demand estimates.

Secondary Research

Secondary research encompassed packaging company annual reports and investor presentations, Statistics Canada Manufacturing Survey packaging sector data, Environment and Climate Change Canada Single-Use Plastics regulatory assessment data, Canadian Plastics Industry Association statistics, Packaging Association of Canada publications, provincial EPR program annual reports, and industry publications including Canadian Packaging Magazine, Packaging World, and Canopy's Pack4Good initiative reports.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating Canadian GDP and consumer expenditure growth projections, food and beverage manufacturing output data, e-commerce retail penetration modelling, packaging material cost and volume trend analysis, provincial industry concentration data, and regulatory impact assessment for plastic packaging prohibition effects.

Canada Packaging Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Packaging Types Covered |

|

| Regions Covered | Ontario, Quebec, Alberta, British Columbia, Others |

| Companies Covered | Amcor plc, Sealed Air Corporation, Wihuri Group, Silgan Holdings Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Canada packaging market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Canada packaging market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Canada packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Canada Packaging Market Report

The Canada packaging market reached USD 22.57 Billion in 2025 and is projected to reach USD 31.42 Billion by 2034.

The market is expected to grow at a CAGR of 3.74% during 2026-2034, driven by food and beverage industry demand, e-commerce packaging growth, sustainability material transitions, and pharmaceutical packaging expansion.

Ontario leads with a 38.6% share in 2025, driven by its position as Canada's largest provincial economy, the highest concentration of food and beverage and pharmaceutical industry clusters, and the largest consumer market by population in the Greater Toronto Area.

Plastic packaging leads with a 44.8% share in 2025, reflecting its technically irreplaceable food protection barrier performance, versatility across rigid, flexible, and semi-rigid formats.

Paper and paperboard, at 31.6% market share, is expected to grow fastest at approximately 4.1% CAGR, driven by e-commerce corrugated board structural demand growth and sustainability-driven substitution of plastic packaging in consumer-facing categories.

Some of the key players include Amcor plc, Sealed Air Corporation, Wihuri Group, and Silgan Holdings Inc.

Key drivers include food and beverage industry growth, sustained packaging demand, e-commerce expansion driving corrugated and protective packaging, sustainability and eco-friendly material regulation mandating portfolio transformation, and smart packaging technology integration in food and pharmaceutical applications.

Key opportunities include sustainable, flexible mono-material packaging development, e-commerce right-size corrugated packaging systems, pharmaceutical primary packaging growth, bio-based and compostable packaging for foodservice, and smart packaging traceability systems for food and pharmaceutical compliance applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)