Commercial Printing Market Size, Share, Trends and Forecast by Technology, Print Type, Application, and Region, 2026-2034

Global Commercial Printing Market Size, Share, Trends & Forecast (2026-2034)

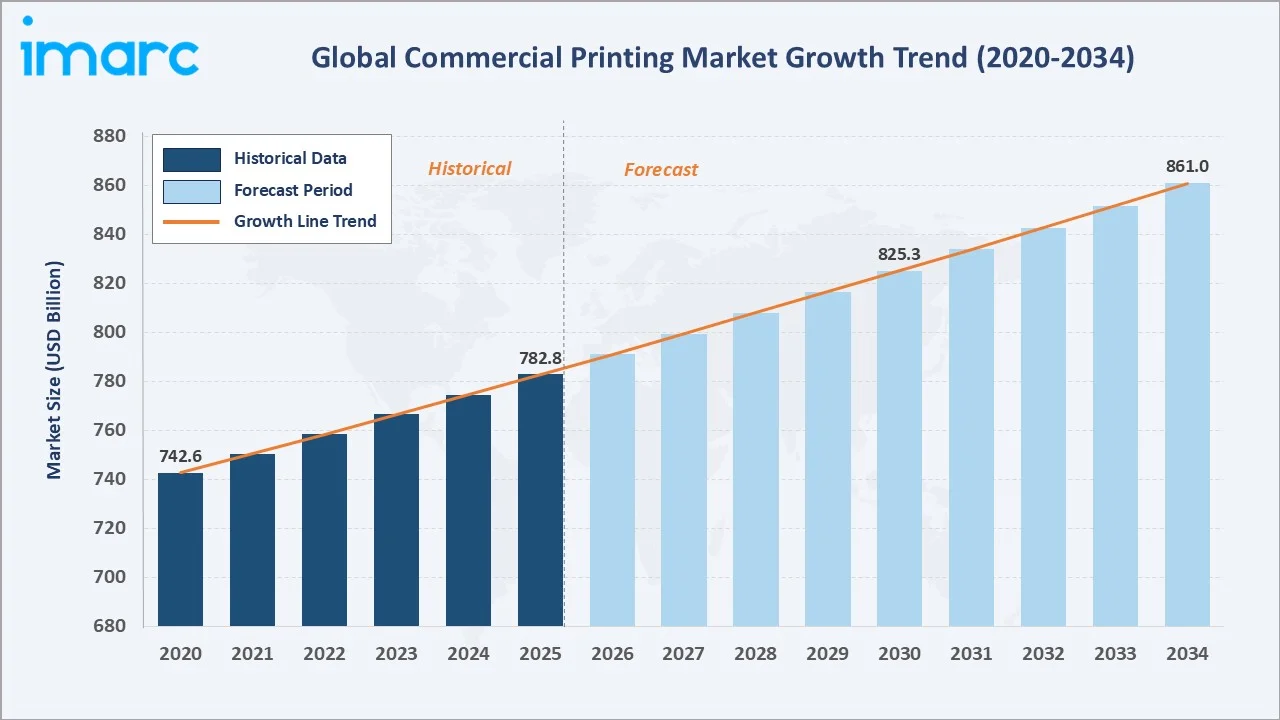

The global commercial printing market size reached USD 782.8 Billion in 2025 and is projected to reach USD 861.0 Billion by 2034, exhibiting a CAGR of 1.06% during 2026-2034. The growing demand for packaged consumer products, integration of digital printing technologies, rising brand marketing expenditure, and expanding e-commerce packaging requirements are the primary forces driving commercial printing market growth.

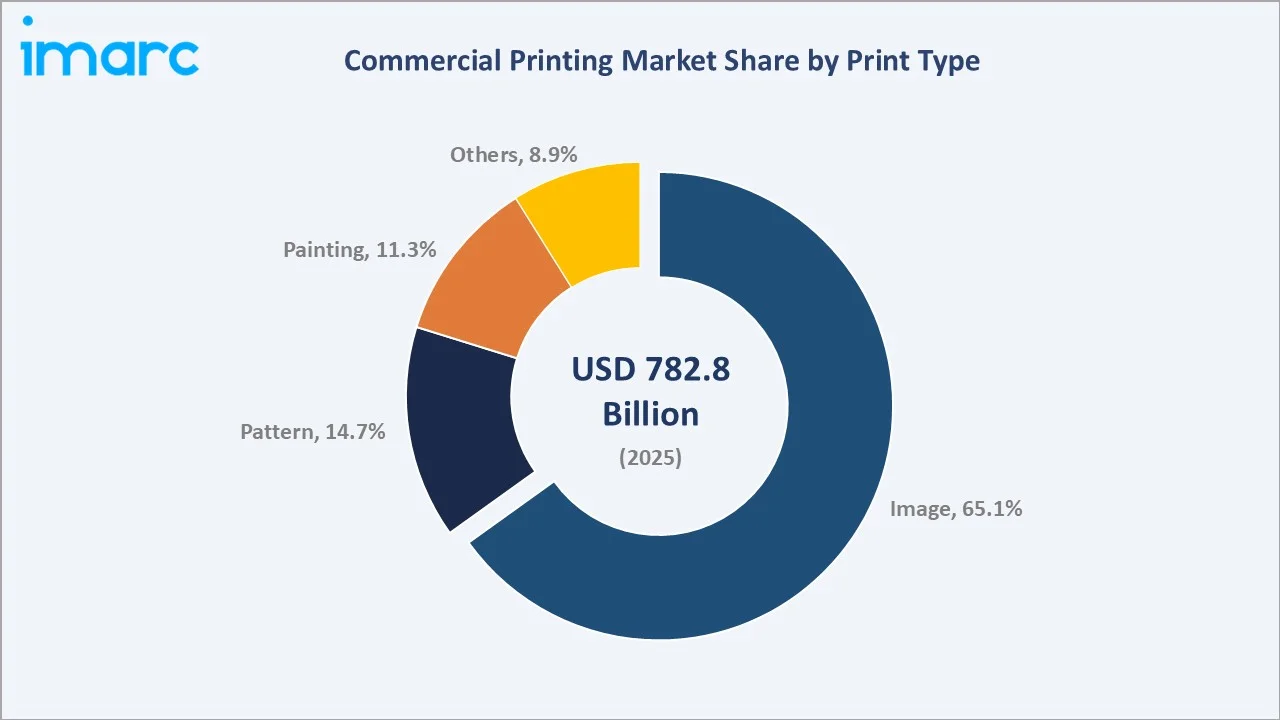

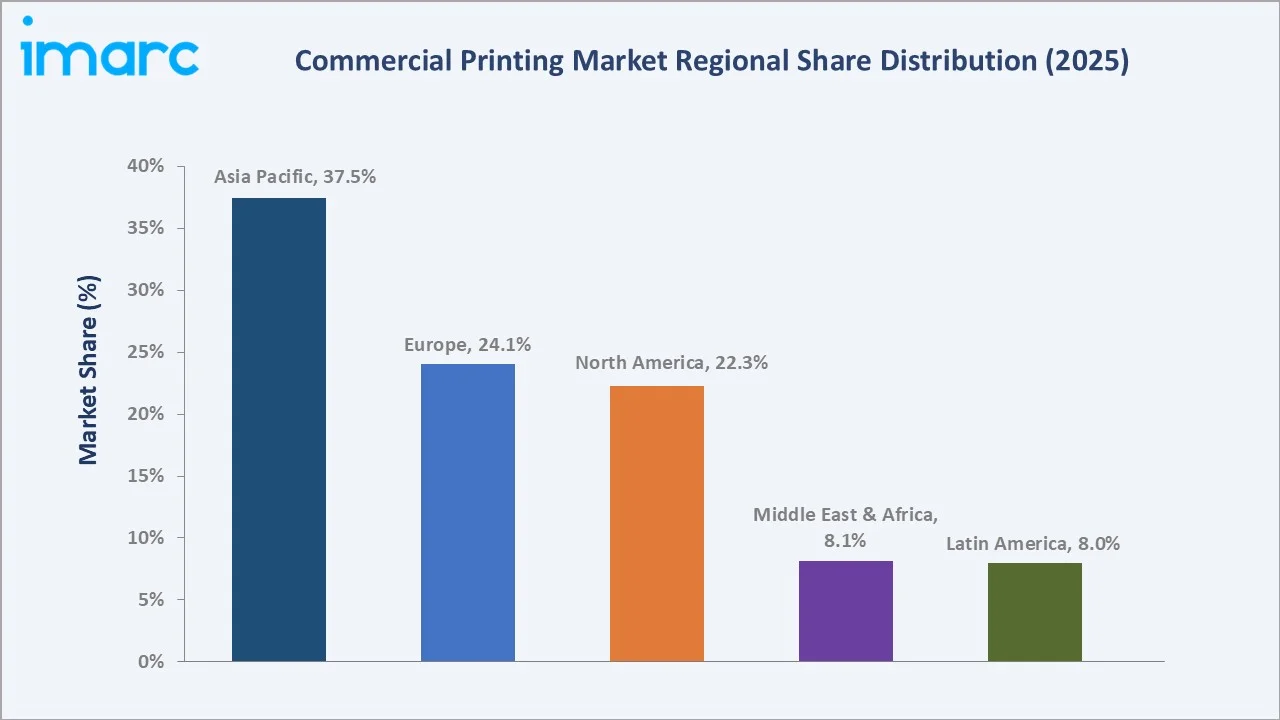

Packaging dominates the application mix at 36.4% in 2025, while Image leads print type at 65.1%. Asia Pacific commands a dominant 37.5% regional share in 2025, underpinned by its strong manufacturing base, rapid urbanisation, and high consumption of printed materials across retail, education, and e-commerce sectors.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 782.8 Billion |

|

Forecast Market Size (2034) |

USD 861.0 Billion |

|

CAGR (2026-2034) |

1.06% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (37.5% share, 2025) |

|

Second Largest Region |

Europe (24.1% share, 2025) |

|

Leading Application |

Packaging (36.4%, 2025) |

|

Leading Print Type |

Image (65.1%, 2025) |

The global commercial printing market growth trajectory from 2020 through 2034, with historical expansion to USD 782.8 Billion in 2025, reflects consistent demand from packaging and advertising sectors, while the forecast to USD 861.0 Billion captures digital print adoption, e-commerce-driven packaging growth, and Asia Pacific urbanisation-led demand.

To get more information on this market, Request Sample

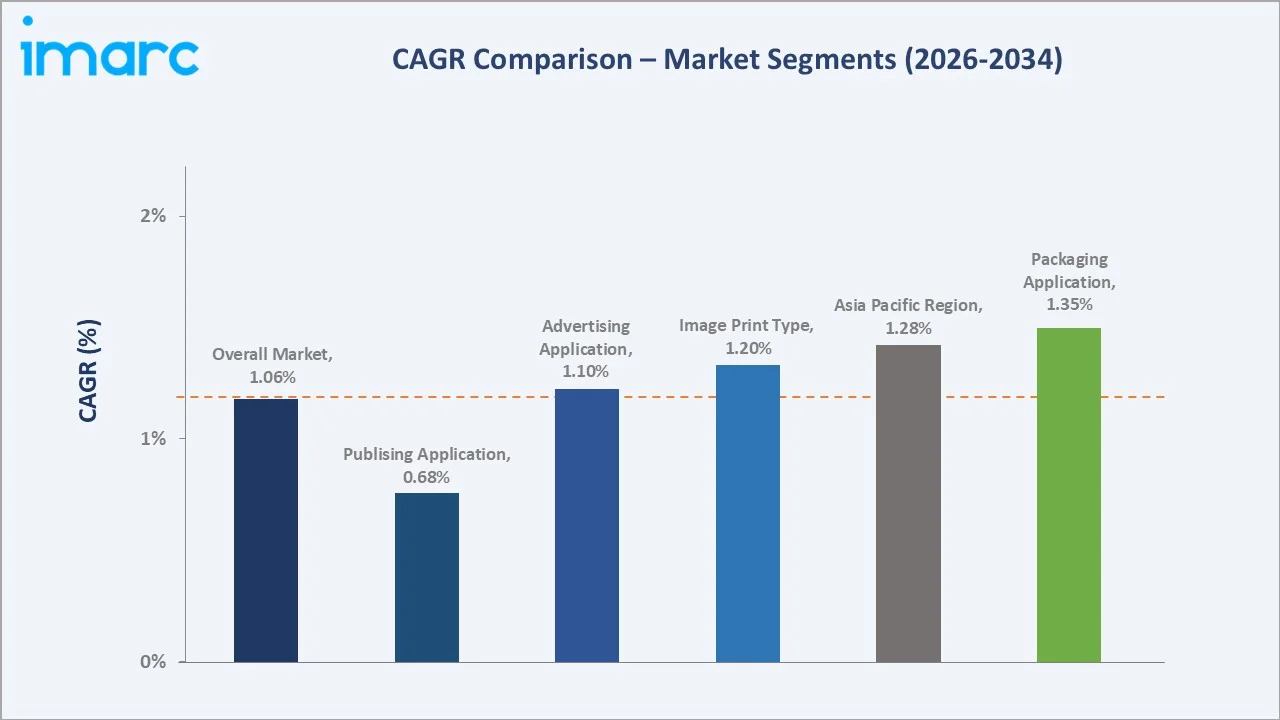

The CAGR trajectories across key application, print type, and regional sub-segments, with Packaging application at ~1.35% CAGR and Asia Pacific at ~1.28% CAGR, are the fastest-growing categories within the global commercial printing industry through 2034.

Executive Summary

The global commercial printing market is on a sustained growth trajectory from USD 782.8 Billion in 2025 to USD 861.0 Billion by 2034. Commercial printing, essential communications and branding medium deployed across packaging, advertising materials, publishing, and transactional documents, benefits from the non-discretionary nature of branded product packaging and regulatory compliance printing requirements globally.

Packaging dominates application at 36.4% in 2025, driven by FMCG, pharmaceutical, and e-commerce demand for branded cartons, flexible packaging, and labels. Advertising at 33.2% captures direct mail, point-of-purchase displays, and promotional printing expenditure. Publishing at 30.4% reflects education, catalogue, and periodical printing demand, sustaining volumes alongside emerging market literacy growth and government communications requirements.

Image print type leads at 65.1% in 2025, reflecting photographic and graphic-rich printing dominance across packaging and advertising applications. Pattern (14.7%) and Painting (11.3%) serve speciality and textile printing segments. Asia Pacific commands 37.5% in 2025, supported by China, India, Japan, and Southeast Asia as both low-cost production hubs and high-growth consumption markets for commercial print.

Key Market Insights

|

Insight |

Data |

|

Leading Application |

Packaging – 36.4% share (2025) |

|

Second Application |

Advertising – 33.2% share (2025) |

|

Leading Print Type |

Image – 65.1% share (2025) |

|

Leading Region |

Asia Pacific – 37.5% share (2025) |

|

Second Region |

Europe – 24.1% share (2025) |

|

Key Companies |

Eastman Kodak Company, R.R. Donnelley & Sons Company, Dai Nippon Printing Co., Ltd., Transcontinental Inc., Cimpress |

Key Analytical Observations Expanding on the Above Data:

- Packaging at 36.4% in 2025 dominates because growth in organised retail, e-commerce, and FMCG requires high-quality printed packaging for product differentiation, shelf presence, and regulatory compliance across food, beverage, pharmaceutical, and cosmetics categories globally, creating durable structural demand that grows with consumption.

- Image print type at 65.1% leads because photographic and graphic-rich content is the dominant output of packaging and advertising printing, requiring high-resolution colour reproduction technologies such as offset lithography and digital inkjet across all major commercial print categories and end-use applications.

- Asia Pacific at 37.5% in 2025 reflects the region's structural advantages: large-scale low-cost manufacturing, rapid urbanisation expanding retail and FMCG consumption, growing e-commerce packaging requirements, and China's position as the world's largest printing production base by volume and output value.

- North America at 22.3% benefits from advanced digital print adoption, sophisticated direct-mail and personalised marketing, healthcare compliance printing demand, and strong corporate branding investment driving premium commercial print volumes from a concentrated base of large enterprise clients.

Global Commercial Printing Market Overview

Commercial printing is the professional production of printed materials for business, marketing, packaging, and publishing purposes. Output types of span offset-printed packaging cartons, digitally printed direct mail, screen-printed promotional items, flexographic food packaging, gravure-printed magazines, and web-to-print customised products across an extremely diverse range of substrates and formats.

The global ecosystem integrates raw material suppliers, pre-press technology providers, commercial printing companies, post-press finishers, and diverse end-use industries spanning retail, FMCG, healthcare, finance, publishing, and government. Digital channels and physical print increasingly co-exist as complementary touchpoints within integrated brand communication strategies.

Market Dynamics

To evaluate market opportunities, Request Sample

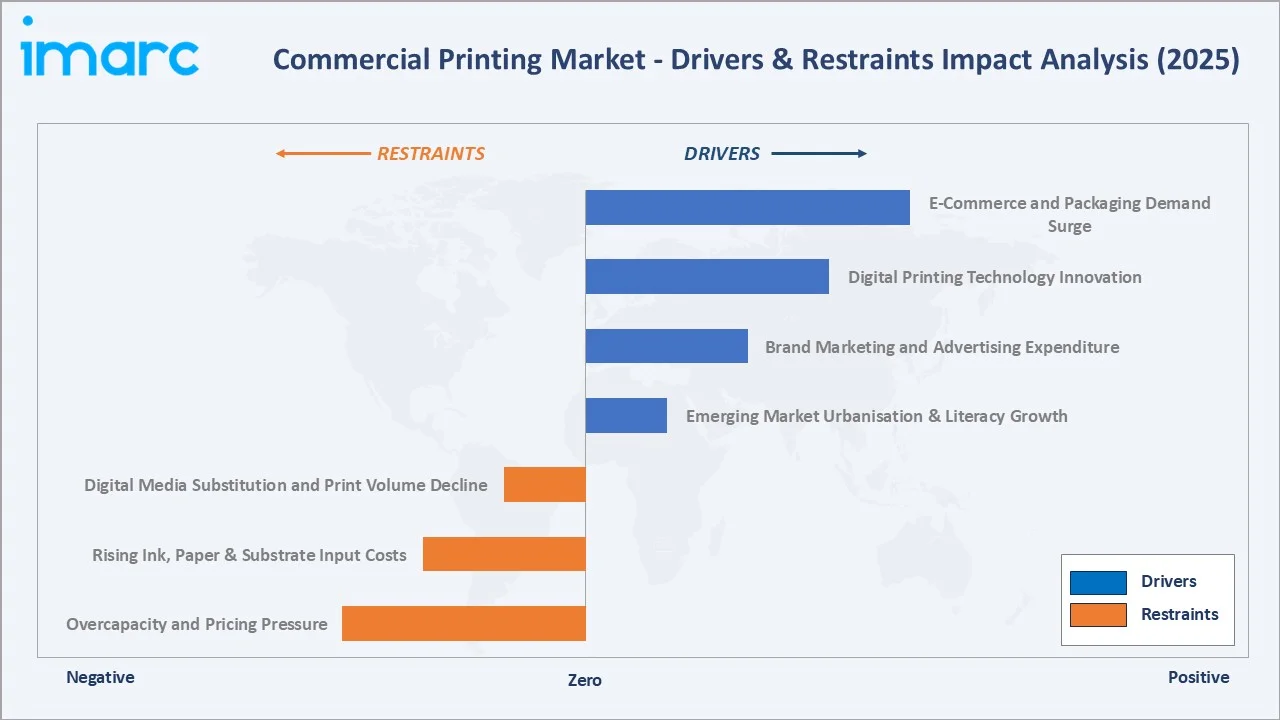

Market Drivers

- E-Commerce and Packaging Demand Surge: The exponential growth of global e-commerce market is creating structural demand for printed corrugated boxes, retail-ready packaging, branded mailer bags, and product labels. Every package shipped requires printed communication, creating a durable link between e-commerce transaction volume and commercial packaging print demand across fulfilment-focused markets.

- Digital Printing Technology Innovation: High-speed inkjet and laser printing technologies are enabling cost-effective short-run production, variable data personalisation, and rapid turnaround that offset cannot match at equivalent economics. The US Government Publishing Office awarded USD 469.2 Million in contracts with private-sector commercial printers in fiscal year 2024, reflecting sustained institutional demand for advanced printing capabilities alongside private sector growth.

- Brand Marketing and Advertising Expenditure: Global advertising spend reached USD 963.5 Billion in 2024, with direct mail, catalogues, point-of-purchase displays, and out-of-home print materials representing a significant share. Brand owners consistently invest in premium printed marketing collateral as a tangible, high-impact medium that delivers measurably superior engagement compared to many digital alternatives.

- Emerging Market Urbanisation and Literacy Growth: Rapid urbanisation in Asia Pacific, Africa, and Latin America is expanding retail infrastructure, educational publishing, and government communications, creating new commercial print demand pools. Growing literacy and rising disposable incomes in developing economies drive consumption of textbooks, newspapers, and branded packaged goods, each generating incremental commercial print volumes.

Market Restraints

- Digital Media Substitution and Print Volume Decline: Accelerating migration of advertising budgets toward digital media platforms, including social media, streaming video, and programmatic advertising, is structurally reducing demand for certain print categories including newspaper inserts, magazine advertising, and some direct mail segments. This secular shift constrains overall market growth, particularly affecting publication printers in mature markets.

- Rising Ink, Paper, and Substrate Input Costs: Paper prices experienced significant volatility in 2021–2023, with coated free-sheet prices increasing materially during peak inflationary periods. Petroleum-derived ink components tracked crude oil price fluctuations, compressing commercial printer margins in competitive contract printing environments where price adjustment mechanisms lag input cost increases and clients resist price escalation.

- Overcapacity and Pricing Pressure: The global commercial printing industry has faced structural overcapacity since the 2008 financial crisis, intensified by consolidation-driven capacity rationalisation falling below the pace of demand contraction in mature print categories. Excess capacity drives sustained price competition that erodes margins, particularly in commodity segments such as web offset publication printing where product differentiation is inherently limited.

Market Opportunities

- Sustainable and Eco-Friendly Printing: Corporate ESG commitments are driving demand for FSC-certified paper, soy and water-based inks, UV-LED curing systems, and carbon-neutral printing certifications. Major brand owners are mandating sustainable packaging printing across supply chains, creating premium pricing opportunities for certified printers with documented environmental credentials and independently audited lifecycle impact assessments.

- Personalisation and Variable Data Printing: Advanced variable data printing technology enables one-to-one personalised direct mail, individualised packaging, and customised promotional materials at near-offset economics. Personalised direct mail achieves response rates 3–5x higher than generic equivalents, generating measurable ROI that drives sustained investment in personalised print programmes from financial services, insurance, retail, and healthcare marketers globally.

Market Challenges

- Skilled Workforce Shortage and Technology Transition: The commercial printing industry faces a dual challenge of retiring experienced press operators and an insufficient new entrant pipeline. Graphic arts education programmes are not producing graduates at a rate that replaces natural workforce attrition, constraining production capacity expansion plans and increasing per-unit labour costs at a time when technology investment requirements are simultaneously accelerating.

- Regulatory Compliance and Food Safety Requirements: Expanding food-contact packaging regulations require commercial printers serving food and pharmaceutical packaging markets to demonstrate ink and coating compliance, maintain traceability documentation, and invest in certified materials. Compliance infrastructure represents significant capital and operational overhead that disadvantages smaller printers relative to large integrated print service providers with dedicated regulatory affairs capabilities.

Emerging Market Trends

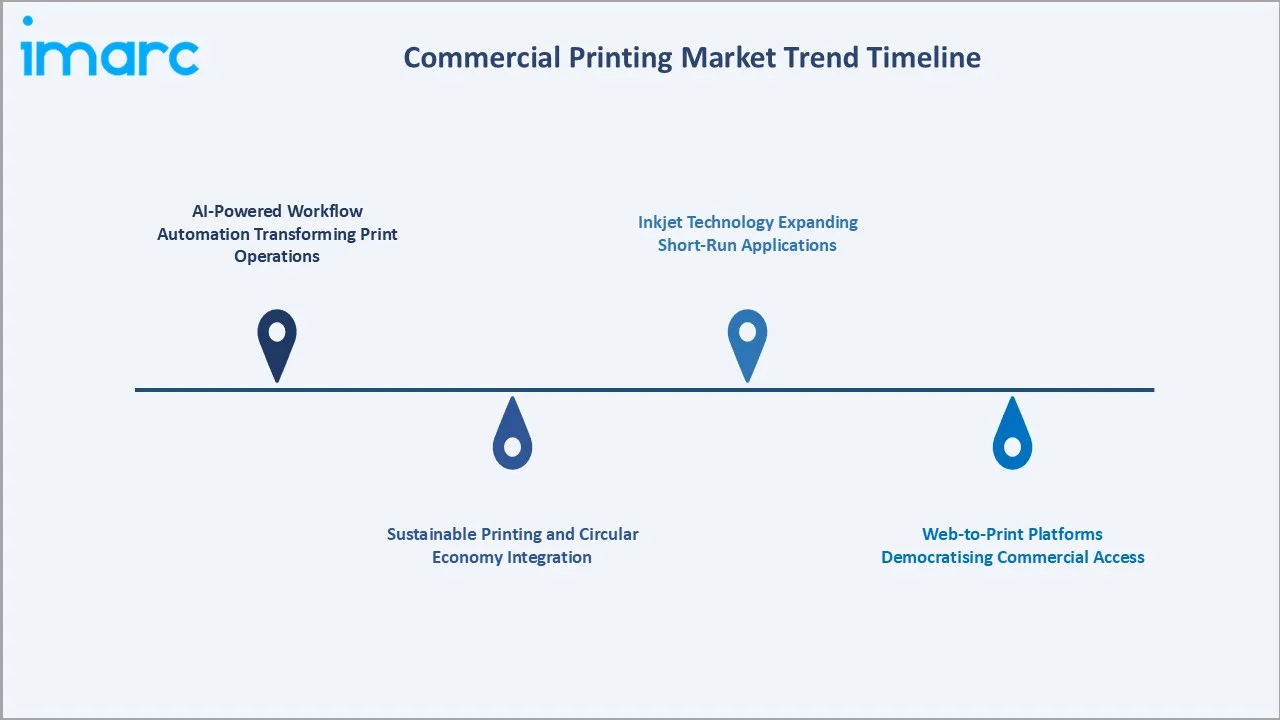

1. AI-Powered Workflow Automation Transforming Print Operations

Artificial intelligence integration across pre-press, colour management, and production scheduling is improving print quality, reducing waste, and accelerating delivery times. In September 2024, HP introduced HP Print AI, an intelligent printing experience with Perfect Output technology for professional-grade print quality, signalling the industry transition toward AI-augmented commercial print production.

2. Sustainable Printing and Circular Economy Integration

Environmental pressures and corporate sustainability commitments are driving adoption of FSC-certified substrates, UV-LED curing systems eliminating VOC emissions, waterless offset technologies, and closed-loop ink recovery programmes. SGP and FSC certifications are increasingly specified by major brand owners as mandatory supplier requirements in packaging and promotional print category sourcing decisions.

3. Web-to-Print Platforms Democratising Commercial Access

Online print platforms are enabling SMEs and consumers to access professional-grade commercial printing at scale through automated digital workflow, aggregating micro-order volumes into economically viable production runs. These platforms eliminate traditional sales and pre-press cost structures, progressively expanding the addressable market for commercial printing services at the long-tail end of the customer spectrum.

4. Inkjet Technology Expanding Short-Run Applications

High-speed production inkjet platforms are displacing conventional offset in mid-volume commercial printing, transactional, direct mail, and book-on-demand applications. Inkjet's cost advantage in short-run and variable-content work is expanding the addressable market volume for digital-first commercial printers while enabling economic one-to-one personalisation across packaging, direct mail, and retail promotional print categories.

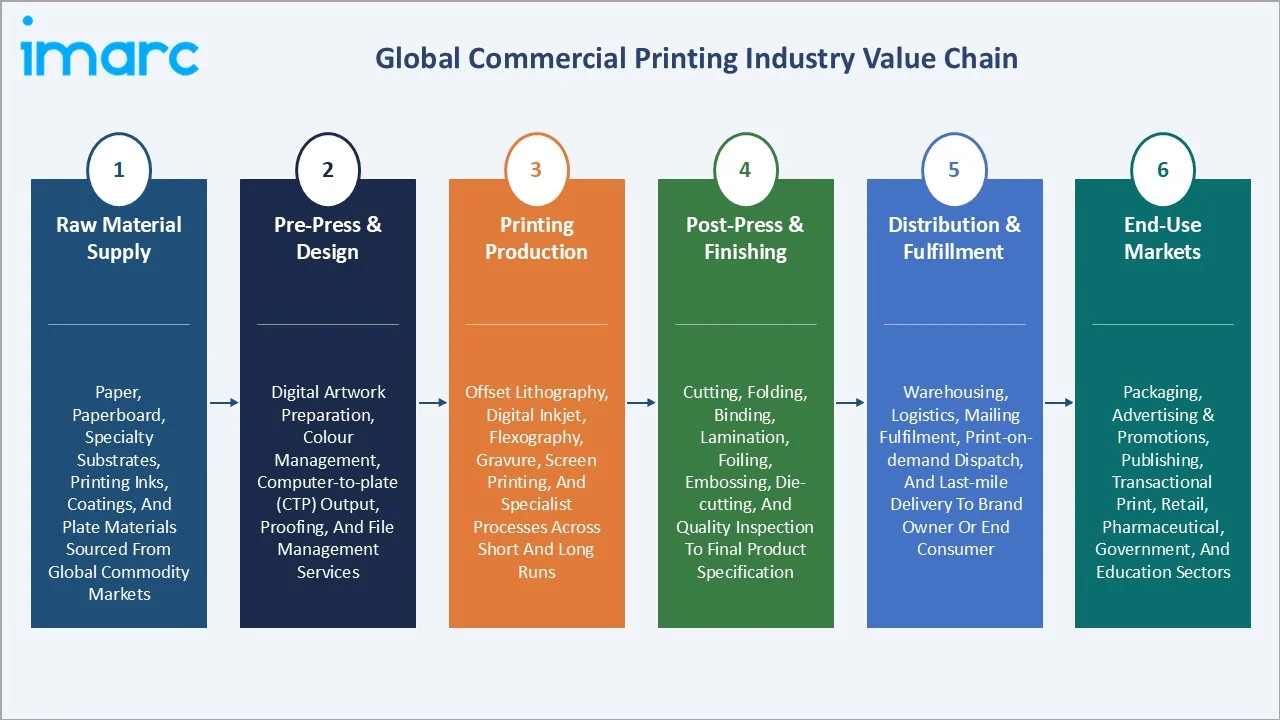

Industry Value Chain Analysis

The commercial printing value chain spans six stages from raw material input through end-use delivery. Pre-press design and printing production capture the highest value-add margins, while post-press finishing, distribution logistics, and content personalisation generate differentiation opportunities that favour technology-integrated commercial printers with end-to-end service capabilities.

|

Stage |

Description |

|

Raw Material Supply |

Paper, paperboard, specialty substrates, printing inks, coatings, and plate materials sourced from global commodity markets |

|

Pre-Press & Design |

Digital artwork preparation, colour management, computer-to-plate (CTP) output, proofing, and file management services |

|

Printing Production |

Offset lithography, digital inkjet, flexography, gravure, screen printing, and specialist processes across short and long runs |

|

Post-Press & Finishing |

Cutting, folding, binding, lamination, foiling, embossing, die-cutting, and quality inspection to final product specification |

|

Distribution & Fulfillment |

Warehousing, logistics, mailing fulfilment, print-on-demand despatch, and last-mile delivery to brand owner or end consumer |

|

End-Use Markets |

Packaging, advertising & promotions, publishing, transactional print, retail, pharmaceutical, government, and education sectors |

Integrated commercial printers combining digital storefront ordering, automated pre-press, multi-technology print production, and fulfilment logistics achieve superior margin profiles and client retention versus pure-play production printers dependent on broker distribution. Vertical integration across the value chain is a meaningful competitive advantage in commodity market segments where price competition is intense and switching costs are otherwise low.

Technology Landscape in the Commercial Printing Industry

Offset Lithography: Dominant Technology for High-Volume Production

Sheet-fed and web offset lithography remain the dominant commercial printing technologies for high-volume, colour-critical applications including catalogues, magazines, packaging cartons, and premium marketing collateral. Modern computer-to-plate systems achieve rapid makeready times, enabling increasingly economic short runs that compete with digital alternatives across a broadening range of commercial print applications and run lengths.

Digital Printing: Enabling Personalisation and Short-Run Economics

HP Indigo, Xerox iGen, Canon Océ, and Konica Minolta digital presses enable economically viable runs from single copies to tens of thousands, supporting personalisation, versioning, and on-demand inventory elimination strategies. Digital presses now deliver near-offset colour quality at commercial production speeds, fundamentally changing the economics of short-run colour printing and enabling mass personalisation across packaging, direct mail, and promotional print categories.

Flexographic Printing: Packaging and Label Market Dominance

Flexographic printing dominates flexible packaging, labels, corrugated, and folding carton printing due to its compatibility with non-porous substrates and water-based inks. Extended colour gamut flexography using seven-colour ink sets enables brand-owner standardisation on fixed palette printing, eliminating spot colour premixed inks, reducing inventory costs, and improving consistency across large-scale packaging production runs globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

🔒 |

🔒 |

2025 |

|

Print Type |

Image |

65.1% |

2025 |

|

Application |

Packaging |

36.4% |

2025 |

|

Region |

Asia Pacific |

37.5% |

2025 |

By Application

Packaging commands a 36.4% majority share in 2025 owing to structural demand from the global FMCG, e-commerce, pharmaceutical, and food and beverage industries where printed packaging is non-discretionary for product protection, regulatory compliance, and consumer communication. The packaging printing segment benefits from the compound growth of organised retail expansion, e-commerce fulfilment volume, and increasing regulatory labelling requirements across multiple product categories.

To access detailed market analysis, Request Sample

Advertising at 33.2% in 2025 captures direct mail, point-of-purchase, promotional, and out-of-home printed marketing materials, sustaining high revenue value despite digital media competition due to the measurable response rate premiums of personalised print.

By Print Type

Image print type dominates at 65.1% in 2025, reflecting the photographic and graphic-rich content requirements across packaging artwork, advertising creative, and publishing illustration that demand high-fidelity colour reproduction. Image printing encompasses four-colour process and extended colour gamut reproduction across offset, digital, and flexographic platforms serving the full spectrum of commercial print applications globally.

Pattern print type at 14.7% in 2025 serves textile printing, decorative surface applications, gift wrap, and speciality packaging where repeating geometric or artistic patterns are the primary output objective. Painting at 11.3% captures fine art reproduction, gallery-quality giclée printing, and artistic canvas output on wide-format inkjet platforms.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

37.5% |

Large-scale low-cost manufacturing base; rapid urbanisation and retail expansion; strong e-commerce packaging demand; growing literacy and education publishing |

|

Europe |

24.1% |

Premium quality specifications; sustainability and FSC mandates; sophisticated publishing sector; luxury packaging and direct mail requirements |

|

North America |

22.3% |

Advanced digital print adoption; personalised direct mail marketing; healthcare compliance labelling; strong corporate branding investment |

|

Middle East & Africa |

8.1% |

Growing retail and FMCG sectors; rising government publication volumes; urban infrastructure expansion driving commercial print demand |

|

Latin America |

8.0% |

Brazil and Mexico packaging sector growth; expanding retail infrastructure; increasing literacy and education print volumes |

Asia Pacific's 37.5% market dominance in 2025 is driven by the region's structural combination of large-scale low-cost manufacturing, rapid retail and e-commerce expansion, and strong domestic consumption of packaged goods and educational materials. The region benefits from vertically integrated printing supply chains, competitive labour costs, and government investment in manufacturing infrastructure across China, India, and Southeast Asian emerging markets.

Europe, with 24.1% in 2025, is characterised by premium quality specifications, strong sustainability mandates including EU packaging regulations, and a sophisticated publishing sector driving demand for high-quality commercial print. North America at 22.3% benefits from advanced digital printing adoption, sophisticated direct mail and marketing personalisation, and robust pharmaceutical labelling demand from regulated healthcare sectors sustaining premium commercial print volumes.

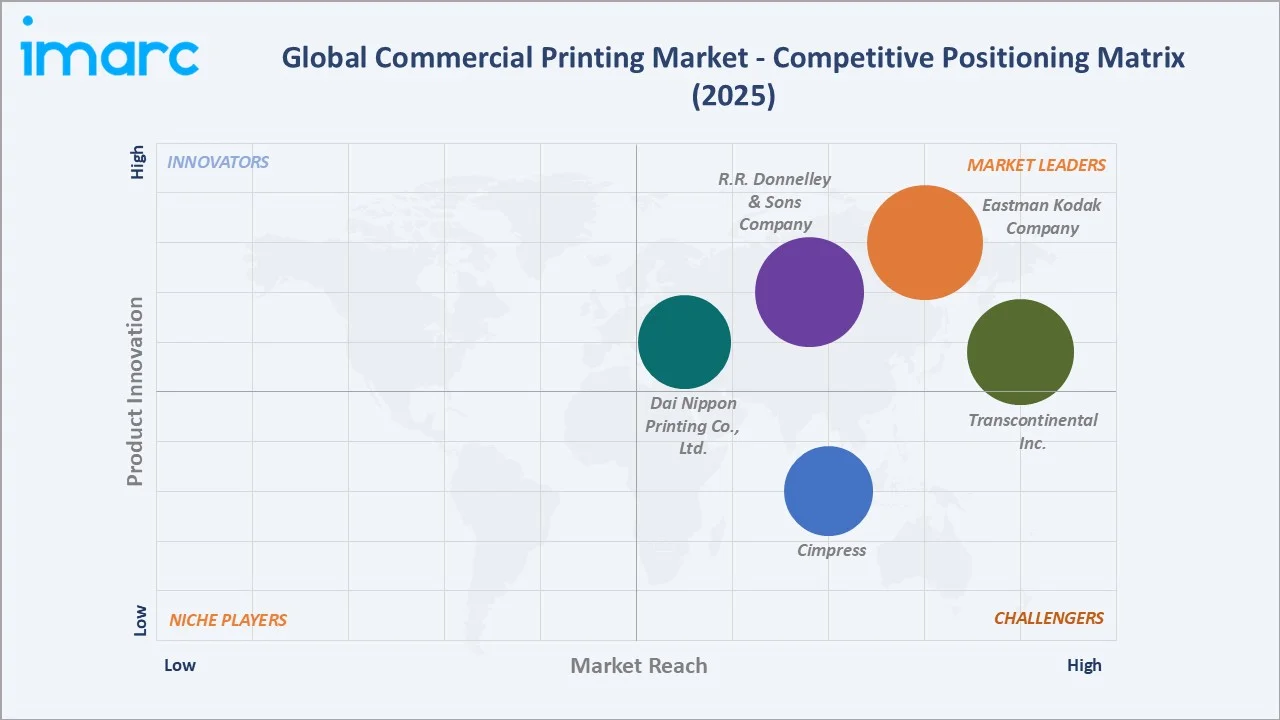

Competitive Landscape

The global commercial printing market is moderately fragmented, with large integrated print service providers holding strong positions in their home regions while competing across multiple end-use verticals. North American and European markets are served by well-established commercial printing conglomerates, while Asia Pacific's market is increasingly served by technology-capable regional champions and vertically integrated domestic producers.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Eastman Kodak Company |

Digital Printing Solutions, Inkjet Printing Presses, Imprinting Systems |

Leader |

Global; digital inkjet technology leadership; commercial print, packaging, and publishing digitalisation across North America, Europe, and Asia Pacific |

|

R.R. Donnelley & Sons Company |

Commercial Printing, Direct Mail, Financial Printing, Labels, Packaging, Supply Chain Solutions, Digital Marketing Services |

Leader |

Global; financial, healthcare & enterprise communications |

|

Dai Nippon Printing Co., Ltd. |

High-design printing, Multifunctional/multiform printing products, UV inkjet (digital) printing |

Leader |

Asia Pacific & global; security printing, packaging & smart labels |

|

Transcontinental Inc. |

Retail Flyers, Books, Magazines, Newspapers, Direct Mail, Catalogues, Educational Publishing, In-Store Marketing |

Leader |

Canada/North America, retail & educational publishing |

|

Cimpress |

Tradeprint, Printi, Exaprint, Pixartprinting, VistaPrint |

Challenger |

Global e-commerce print; SME and consumer personalised print segments |

Key players include Eastman Kodak Company, R.R. Donnelley & Sons Company, Dai Nippon Printing Co., Ltd., Transcontinental Inc., Cimpress, and others.

Key Company Profiles

R.R. Donnelley & Sons Company

R.R. Donnelley & Sons Company (RRD) is a global leader in multichannel business communications and marketing solutions, headquartered in Chicago, Illinois, with roots tracing to 1864. RRD serves thousands of clients across financial services, healthcare, retail, and publishing sectors through a comprehensive portfolio of print, digital, and fulfilment communication capabilities across global markets.

- Product Portfolio: Commercial printing, direct mail, financial printing, labels, packaging, supply chain solutions, digital marketing services

- Recent Developments: In September 2023, R.R. Donnelley & Sons Company (RRD), expanded its digital printing capabilities with the installation of the EFI Nozomi C18000 Plus single-pass digital inkjet printer. The Nozomi C18000 Plus press will drive high-volume production at speeds three to five times faster than scanning superwide-format printers.

- Strategic Focus: RRD's strategy focuses on expanding digital transformation services and integrating AI-powered workflow automation with multi-channel campaign management tools into its core print fulfilment infrastructure, positioning the company as an enterprise communications partner rather than a pure commercial printer for major corporate clients globally.

Dai Nippon Printing Co., Ltd.

Dai Nippon Printing Co., Ltd. (DNP) is one of the world's largest printing companies, headquartered in Tokyo, Japan, with operations spanning commercial printing, packaging, electronic components, and lifestyle solutions. DNP's diversified business model extends beyond printing into high-tech materials and digital content, making it uniquely positioned within Asia Pacific's commercial printing market and globally.

- Product Portfolio: High-design printing, Multifunctional/multiform printing products, UV inkjet (digital) printing.

- Strategic Focus: DNP's commercial printing strategy leverages its P&I (printing and information) technology platform to integrate commercial printing with digital communication services, including IC-tag-enabled secure packaging, dye-sublimation imaging, XR content communication, and smart card solutions.

Market Concentration Analysis

The global commercial printing market is moderately fragmented at the global level, reflecting significant regional concentration among national leaders with no single company holding more than 4–6% of total global market revenue. Asia Pacific, representing 37.5% of the market, is served primarily by domestic Chinese and Japanese producers, while North American and European markets maintain distinct competitive ecosystems with their own specialist leaders.

Consolidation at the regional level is more advanced than global fragmentation suggests. Large print conglomerates hold disproportionate share in their respective home markets through integrated marketing services positions, long-term client contracts, and proprietary technology platforms. Global consolidation through M&A is occurring primarily through large print service providers acquiring regional commercial printers as strategic additions to geographic coverage and vertical end-use specialisation.

Investment & Growth Opportunities

Fastest-Growing Segments

Packaging application at ~1.35% CAGR through 2034 is the highest-growth application segment, driven by e-commerce fulfilment packaging, FMCG shelf differentiation, and pharmaceutical compliance labelling requirements that grow structurally with global consumption. Asia Pacific at ~1.28% CAGR is the fastest-growing geography, supported by urbanisation, retail expansion, and manufacturing base development across emerging markets.

Emerging Markets

Africa and Southeast Asia represent high-potential emerging commercial printing markets, with rapidly growing retail sectors, expanding middle-class consumer bases, and underdeveloped domestic commercial printing infrastructure being built to serve international brand owner requirements. India's packaging printing sector is growing at above-market rates supported by government-backed domestic manufacturing initiatives driving branded product development and packaging demand.

Venture & Investment Trends

Private equity interest in consolidating fragmented commercial printing markets is accelerating, where defensible regional market positions and recurring packaging contract revenue profiles make specialist commercial printers attractive platform investment targets. Sustainable printing certification and digital workflow technology investment are generating premium valuations for technology-forward operators versus analogue-only peers in competitive acquisition processes.

Future Market Outlook (2026-2034)

The global commercial printing market is forecast to expand from USD 782.8 Billion in 2025 to USD 861.0 Billion by 2034 at a CAGR of 1.06%, adding USD 78.2 Billion in incremental annual market value over the forecast period. This measured, sustained growth reflects the market's essential but digitally pressured demand characteristics across mature and emerging market geographies.

Three forces will most significantly shape the commercial printing industry through 2034. Sustainable printing mandates, with EU packaging regulations requiring recyclable and reduced-material packaging by 2030, will require capital investment in new ink, substrate, and process technologies that reward certified printers with preferential brand-owner supply chain positions and premium contract pricing.

Digital-physical integration through AR-enabled packaging, NFC smart labels, and QR-linked printed media will create new value dimensions for printed materials that digital-only media cannot replicate, supporting premium print product demand from brand owners seeking measurable consumer engagement metrics from physical touchpoints across an increasingly digital media environment.

Research Methodology

Primary Research

Primary research encompassed structured interviews with commercial printing industry stakeholders including senior print service provider executives, packaging procurement managers at major FMCG companies, printing technology suppliers, and industry association representatives from FESPA, Printing Industries of America, and the Packaging and Printing Association. Primary data validated market sizing, application segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Printing Industries of America Annual Reports, FESPA Global Print Census, AICC Independent Packaging Converter data, Smithers Pira commercial printing market reports, US Census Bureau printing industry statistics, Eurostat manufacturing data, government trade body publications, and trade media including Printing News, Print Week, and Package Printing serving commercial print industry professionals globally.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting models incorporating GDP growth rates, urbanisation indices, retail trade growth, e-commerce penetration, and historical market evolution patterns. Scenario analysis incorporating base, optimistic, and conservative cases accounts for macroeconomic uncertainty, digital substitution acceleration, and sustainable printing regulatory impact on the commercial printing market through 2034.

Commercial Printing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Lithographic Printing, Digital Printing, Flexographic Printing, Screen Printing, Gravure Printing, Others |

| Print Types Covered | Image, Painting, Pattern, Others |

| Applications Covered | Packaging, Advertising, Publishing |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Eastman Kodak Company, R.R. Donnelley & Sons Company, Dai Nippon Printing Co. Ltd., Transcontinental Inc., Cimpress, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the commercial printing market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global commercial printing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the commercial printing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Commercial Printing Market Report

The global commercial printing market reached USD 782.8 Billion in 2025, driven by sustained packaging demand, advertising print expenditure, and emerging market publishing growth across global commercial print categories.

The market is projected to reach USD 861.0 Billion by 2034, growing at a CAGR of 1.06% during 2026-2034, supported by packaging sector growth, digital print adoption, and Asia Pacific market expansion driven by urbanisation and retail development.

Packaging leads with a 36.4% application share in 2025, valued for its non-discretionary demand from e-commerce, FMCG, pharmaceutical, and food and beverage industries requiring branded and compliant packaging solutions globally.

Image print type leads at 65.1% in 2025, representing high-fidelity photographic and graphic-rich colour reproduction across packaging artwork, advertising creative, and publishing illustration applications produced by commercial printers.

Asia Pacific commands a dominant 37.5% market share in 2025, driven by large-scale manufacturing, India and China packaging sector growth, and Southeast Asia's rapidly expanding retail and FMCG consumption base.

Key drivers include the e-commerce packaging demand surge, digital printing technology innovation enabling cost-effective personalisation, brand marketing expenditure, and emerging market urbanisation expanding retail and publishing print volumes.

Leading companies include Eastman Kodak Company, R.R. Donnelley & Sons Company, Dai Nippon Printing Co., Ltd., Transcontinental Inc., Cimpress, and others.

Sustainability mandates are driving investment in FSC-certified substrates, water-based and UV-LED ink systems, and carbon-neutral printing certifications. Brand-owner ESG commitments are creating premium demand for certified commercial printers with documented environmental credentials and circular economy-compatible production processes globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)