Controlled Release Fertilizer Market Size, Share, Trends and Forecast by Type, Form, Application, and Region, 2026-2034

Controlled Release Fertilizer Market Size, Share, Trends & Forecast (2026-2034)

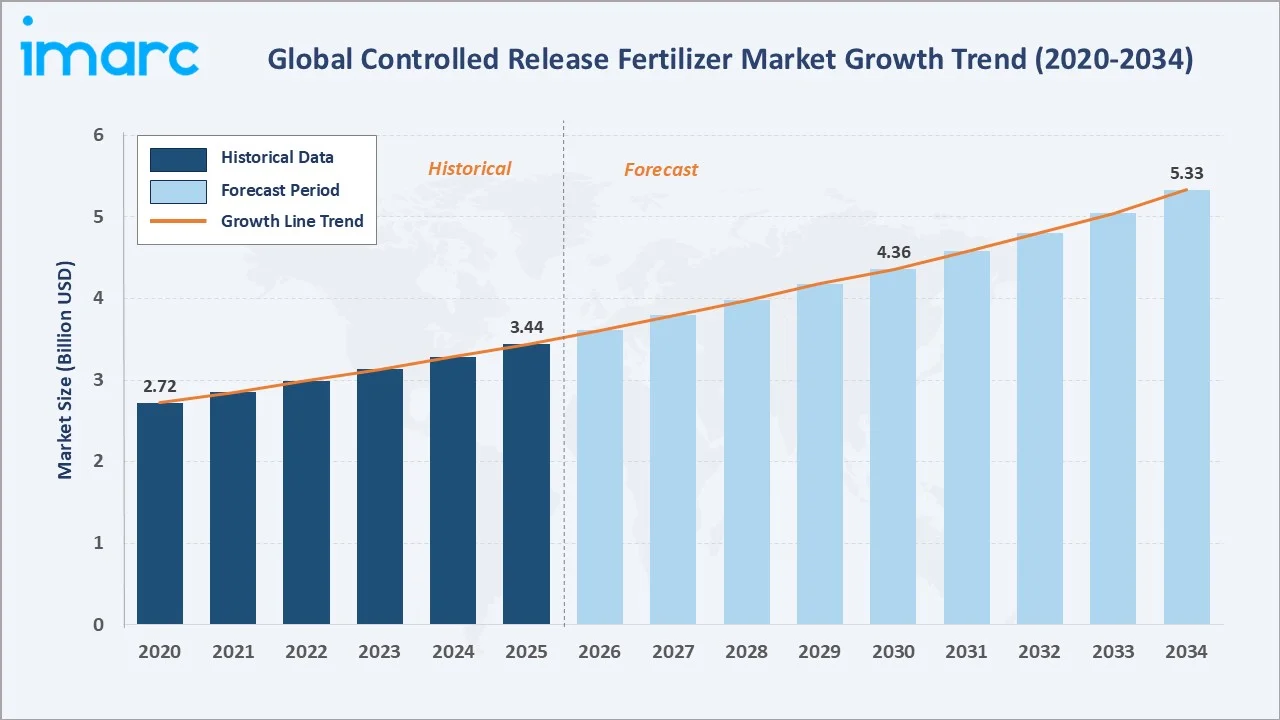

The global controlled release fertilizer market reached USD 3.44 Billion in 2025 and is projected to reach USD 5.33 Billion by 2034, growing at a CAGR of 4.82% during 2026-2034. The market is driven by rising global food demand, precision agriculture adoption, stringent environmental regulations on nutrient runoff, and government support for sustainable agronomic practices.

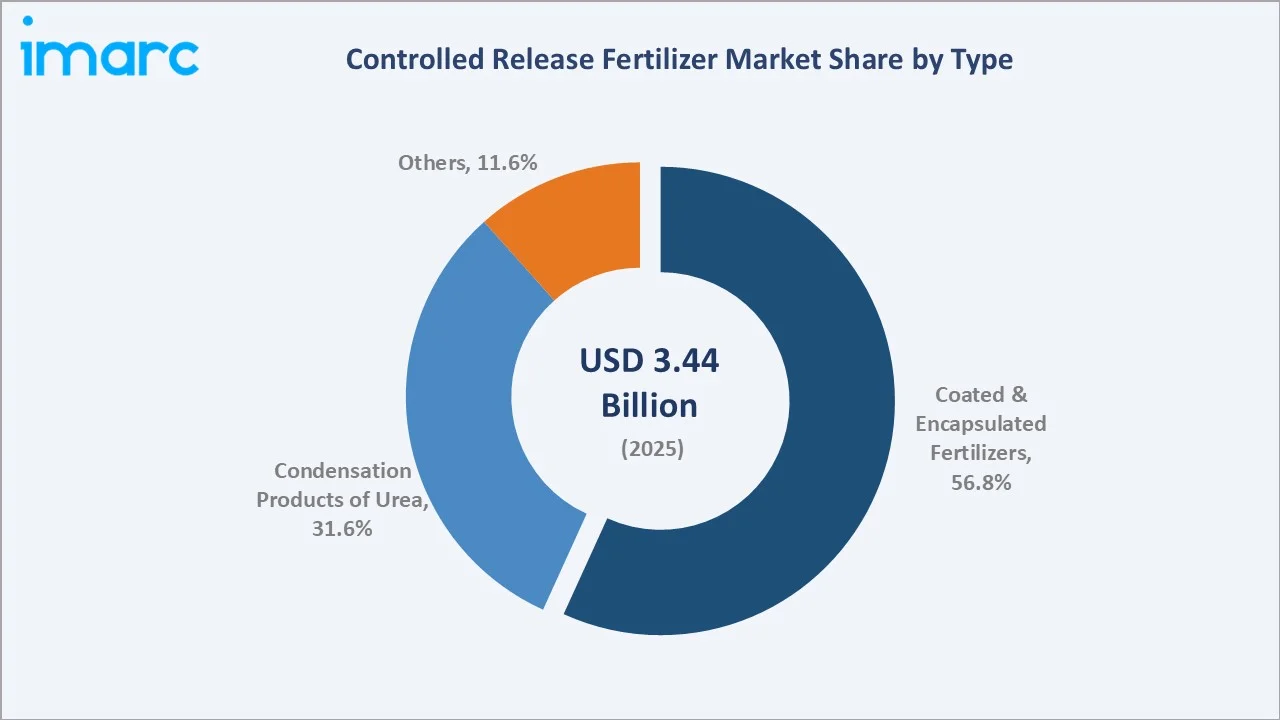

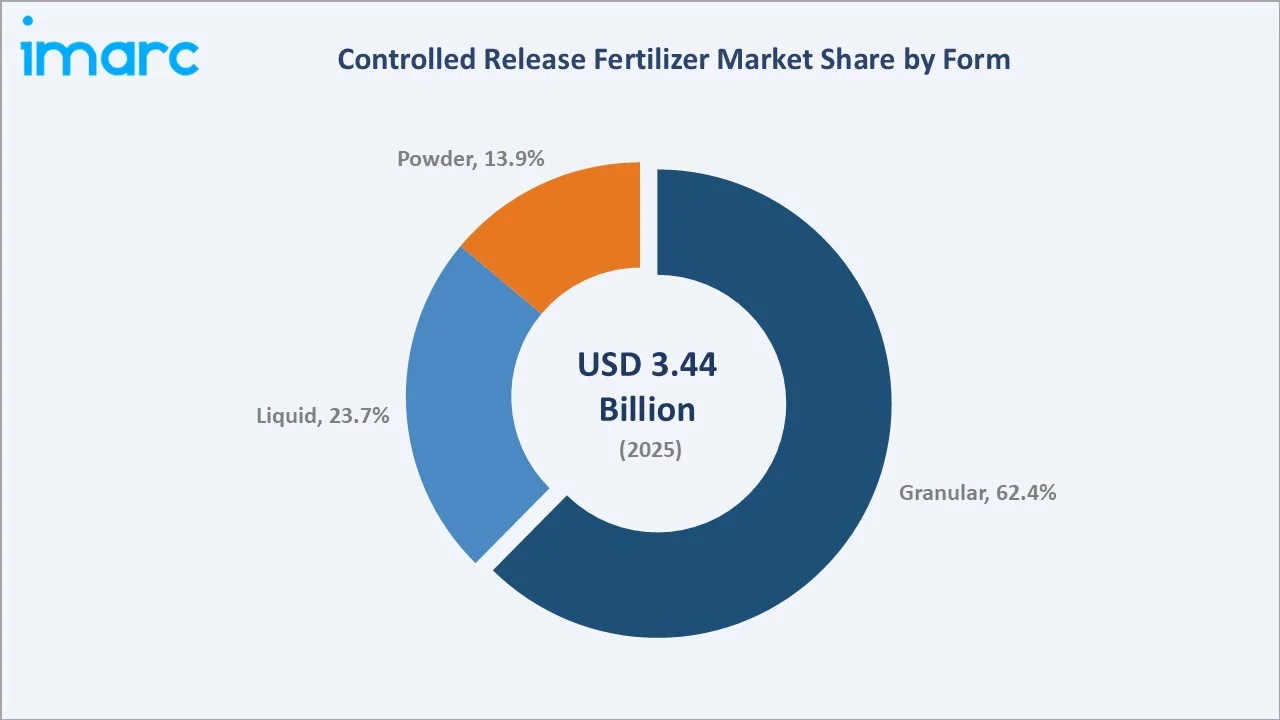

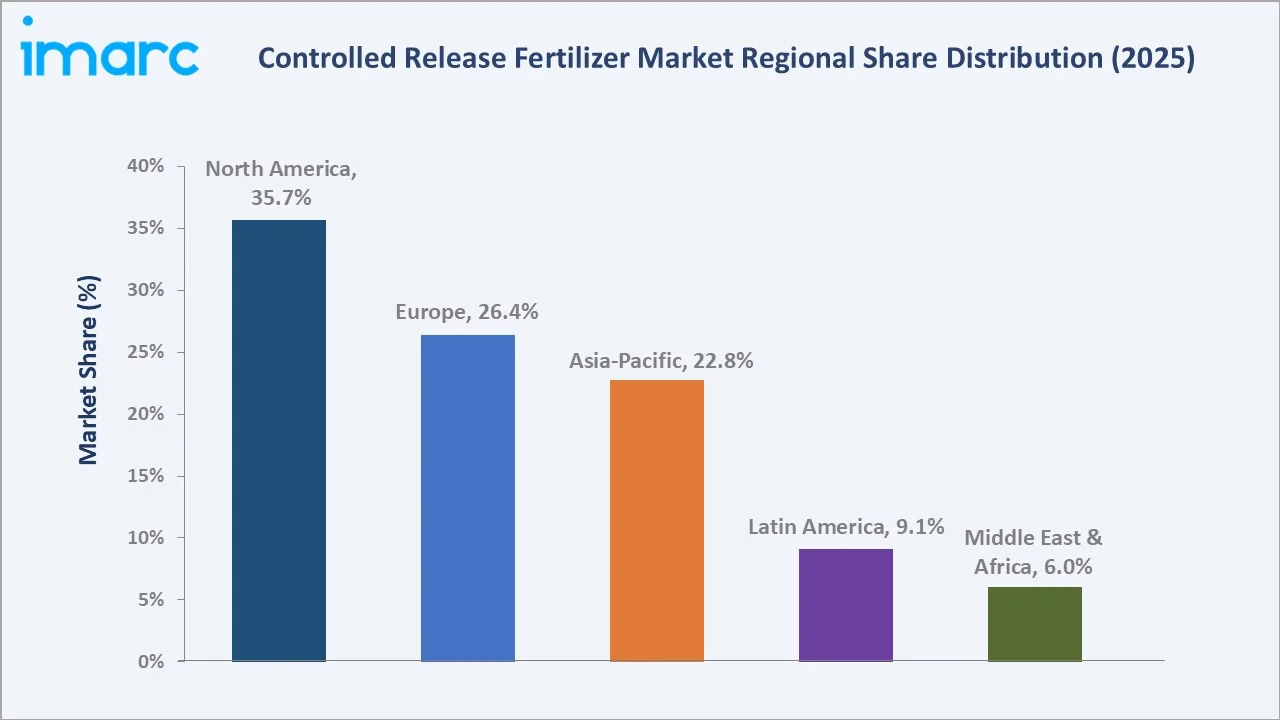

Coated and Encapsulated Fertilizers dominate at 56.8% by type. Granular form leads at 62.4%. North America commands 35.7% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.44 Billion |

|

Forecast Market Size (2034) |

USD 5.33 Billion |

|

CAGR (2026-2034) |

4.82% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Coated and Encapsulated Fertilizers (56.8%, 2025) |

|

Dominant Form |

Granular (62.4%, 2025) |

|

Leading Region |

North America (35.7%, 2025) |

The market expanded from USD 2.72 Billion in 2020 to USD 3.44 Billion in 2025, anchored at USD 4.36 Billion in 2030, and forecast to reach USD 5.33 Billion by 2034. Growing environmental pressures on nutrient leaching and runoff have accelerated regulatory mandates favoring controlled release nutrient delivery, supporting sustained market expansion across key agricultural economies.

To get more information on this market, Request Sample

North America at 35.7% leads through large-scale row crop production, strong precision agriculture infrastructure, and regulatory frameworks incentivizing nutrient management.

Coated and Encapsulated Fertilizers at 56.8% dominate as polymer and sulfur-coated technologies deliver superior nutrient synchronization with crop uptake cycles.

Executive Summary

The global controlled release fertilizer market reached USD 3.44 Billion in 2025, representing one of agriculture's highest-priority specialty input categories driven by the global transition toward sustainable and precision nutrient management. CRFs deliver nutrients in synchrony with crop demand, reducing leaching losses and improving fertilizer use efficiency. The market is projected to reach USD 5.33 Billion by 2034.

Coated and Encapsulated Fertilizers at 56.8% dominate by capturing the premium crop nutrition segment with polymer and sulfur-coated products delivering controlled nutrient timing. Granular form at 62.4% leads through ease of application and compatibility with standard spreader equipment. North America at 35.7% leads globally through high-value specialty crop acreage, precision agriculture adoption, and regulatory nutrient management compliance requirements.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Coated and Encapsulated Fertilizers – 56.8% share (2025) |

|

Dominant Form |

Granular – 62.4% market share (2025) |

|

Leading Region |

North America – 35.7% market share (2025) |

|

Market Opportunity |

Biodegradable coatings; smart CRF formulations; developing-market expansion; 4R nutrient stewardship programs |

Key Analytical Observations Supporting The Above Data:

- Coated and Encapsulated Fertilizers at 56.8%: This segment dominates as polymer-coated and sulfur-coated technologies provide precise nutrient release timing matched to crop growth stages. Adoption is accelerating in high-value crops including fruits, vegetables, and turf applications where fertilizer efficiency directly impacts input cost economics and regulatory compliance requirements.

- Granular form at 62.4%: Granular CRFs lead through direct compatibility with conventional and precision application equipment, uniform distribution characteristics, and availability across all crop systems. Granular formulations provide the best logistics, handling, and storage performance, sustaining dominant market position across all geographies.

- North America at 35.7%: North America leads through the United States' extensive row crop and high-value horticultural production, supported by nutrient management regulations, USDA precision agriculture incentive programs, and strong agronomic advisory infrastructure. The region's mature specialty crop sector generates premium CRF demand volumes.

Controlled Release Fertilizer Market Overview

The global controlled release fertilizer market encompasses the development, manufacture, and supply of fertilizers designed to release nutrients at a controlled rate over an extended period, aligned with crop nutrient uptake requirements. Product categories include polymer-coated fertilizers, sulfur-coated urea, urea-formaldehyde condensation products, and hybrid sulfur-polymer coated formulations.

The ecosystem integrates raw material suppliers, coating technology developers, fertilizer manufacturers, specialty distribution networks, agronomic advisory services, and end-user farming operations across row crops, horticultural, turf, and ornamental applications. Macroeconomic factors include rising food security concerns, global population growth, tightening environmental regulations on nutrient runoff, and investment in precision agriculture technologies.

Market Dynamics

To evaluate market opportunities, Request Sample

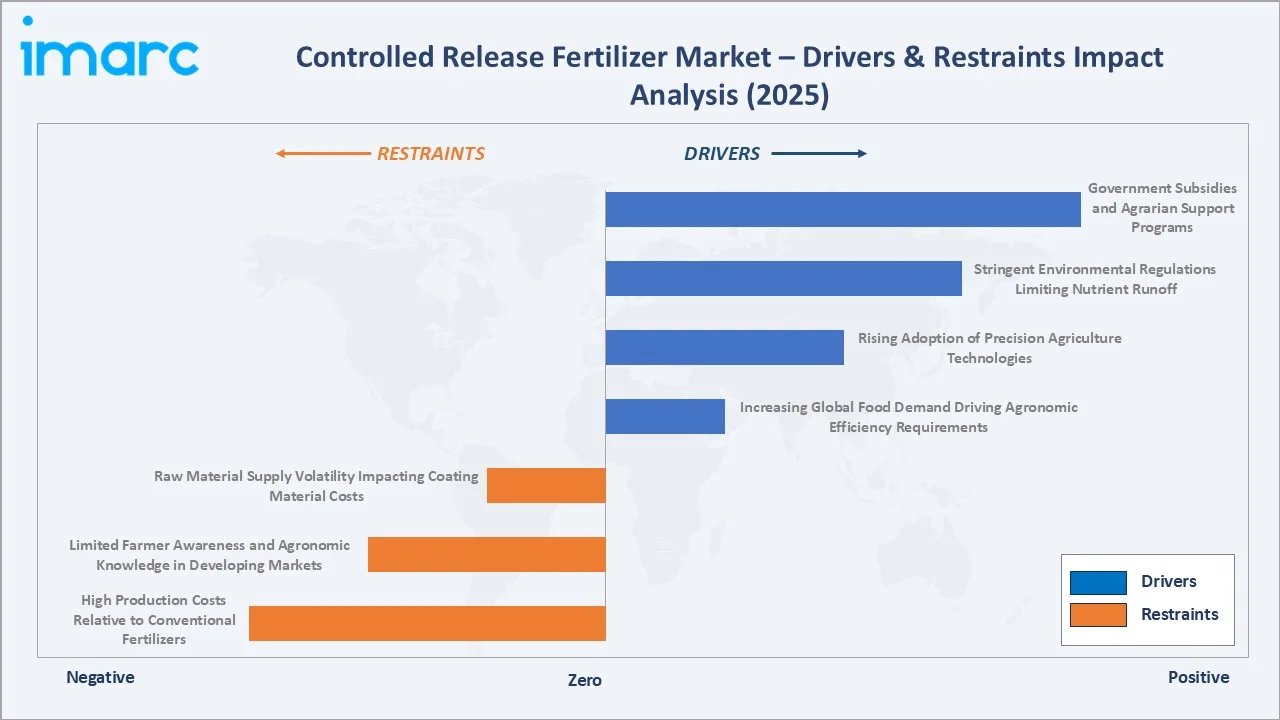

Market Drivers

- Increasing Global Food Demand Driving Agronomic Efficiency Requirements: Rising global food demand, driven by population growth projecting 9.7 billion people by 2050, is accelerating pressure on agricultural productivity per unit area. CRFs enable higher nutrient use efficiency by releasing nutrients precisely when crops need them, reducing leaching losses by up to 50% versus conventional fertilizers. As arable land availability constraints intensify, CRFs provide a critical technology for maximizing yield per hectare, directly supporting demand across major grain and commercial crop markets worldwide.

- Rising Adoption of Precision Agriculture Technologies: Precision agriculture adoption, including variable-rate application equipment, GPS-guided spreading, and soil sensor networks, is creating agronomic infrastructure compatible with and complementary to CRF deployment. The integration of CRF products within precision agronomy programs is accelerating adoption among commercial and large-scale farming operations, particularly across North America and Europe, where precision agriculture infrastructure is most developed and economically justified.

- Stringent Environmental Regulations Limiting Nutrient Runoff: Regulatory frameworks including the EU Nitrates Directive, US EPA Nutrient Management Regulations, and equivalent national frameworks in Asia-Pacific are mandating reductions in agricultural nutrient losses to water bodies. CRFs reduce nitrate leaching and phosphorus runoff through controlled nutrient delivery, enabling farmers to achieve regulatory compliance while maintaining crop productivity. Regulatory tightening across major agricultural economies is a structural long-term driver for CRF substitution of conventional fertilizers.

- Government Subsidies and Agrarian Support Programs: Multiple major agricultural economies including the United States, China, India, and EU member states operate farm subsidy and sustainability support programs providing financial incentives for adoption of environmentally beneficial input technologies including CRFs.

Market Restraints

- High Production Costs Relative to Conventional Fertilizers: CRFs carry a significant price premium of 2-5x over conventional fertilizers per unit of nutrient, reflecting coating material, manufacturing complexity, and quality control costs. These premium limits adoption to high-value crop systems, precision agriculture operations, and markets with strong regulatory incentives. In price-sensitive developing markets serving subsistence and smallholder agriculture, cost barriers constrain addressable market penetration and sustain the dominance of conventional fertilizers.

- Limited Farmer Awareness and Agronomic Knowledge in Developing Markets: In developing agricultural economies including parts of South Asia, Sub-Saharan Africa, and Southeast Asia, limited farmer awareness of CRF technology benefits and agronomic application protocols constrains adoption. Agronomic advisory infrastructure in these markets is insufficient to support widespread technology transition, and the lack of localized field efficacy demonstration data reduces farmer confidence in CRF investment, limiting market penetration despite favorable crop economic fundamentals.

- Raw Material Supply Volatility Impacting Coating Material Costs: CRF manufacturing relies on petrochemical-derived polymer coatings including polyurethane, polyolefin, and alkyd resins, alongside sulfur from oil refinery by-products. Volatility in crude oil prices and petrochemical feedstock markets creates cost unpredictability in CRF manufacturing. Periods of elevated polymer prices compress manufacturer margins and reduce competitiveness versus conventional fertilizers, creating demand cycle volatility aligned with energy commodity price movements.

Market Opportunities

- Biodegradable and Bio-based Coating Technology Development: Development of biodegradable polymer coatings derived from bio-based feedstocks including starch, lignin, and plant oils addresses growing environmental concerns about microplastic contamination from conventional polymer-coated CRFs. Regulatory momentum in Europe and similar initiatives in other markets is creating structural demand for biodegradable CRF coatings, opening a premium technology segment for manufacturers investing in bio-coating research and development programs.

- Smart and Sensor-Responsive CRF Formulations for Precision Agriculture Integration: Emerging smart CRF technologies incorporating sensor-responsive coatings that release nutrients in response to soil moisture, temperature, or pH represent a high-value next-generation product category. Integration with IoT agricultural sensor networks creates potential for autonomous nutrient delivery systems aligned with real-time crop demand data, with early commercial deployment in premium horticultural and turf markets validating the technology.

Market Challenges

- Microplastic Contamination Concerns from Conventional Polymer Coatings: Conventional polymer-coated CRFs shed microplastic particles during nutrient release as coatings fragment and accumulate in soil profiles. Growing scientific and regulatory attention to agricultural microplastic contamination is creating reputational risk for polymer-coated CRF products and driving regulatory scrutiny. The transition creates near-term market uncertainty for established polymer-coated CRF manufacturers pending regulatory clarification on permissible coating materials.

- Complexity of CRF Product Selection and Agronomy Protocol Customization: Matching CRF product type, coating release profile, and application rate to specific crop systems, soil types, and climate zones requires sophisticated agronomic expertise. The diversity of CRF product specifications creates decision complexity for distributors and farmers without strong agronomic advisory support, limiting broad-based adoption outside markets with mature agronomic advisory infrastructure.

Emerging Market Trends

1. Biodegradable Polymer Coating Technology Replacing Conventional Plastics

Regulatory pressure on microplastic contamination and sustainability mandates are accelerating development of biodegradable CRF coatings derived from natural polymers, bio-polyesters, and cellulose derivatives. Leading manufacturers are investing in bio-coating R&D programs with commercial biodegradable CRF launches expected to capture regulatory-compliance premium pricing in EU and North American markets through the forecast period.

2. Integration of CRF Products with Digital Precision Agriculture Platforms

CRF manufacturers are partnering with precision agriculture platform providers to integrate product nutrient release profiles with digital farm management systems. Real-time crop modeling tools are being developed that optimize CRF product selection and application timing based on satellite imagery, soil sensor data, and weather forecasts, creating value-added agronomic decision support services that differentiate CRF product lines in competitive markets.

3. Expansion into Turf, Ornamental, and Professional Horticulture Markets

High-value turf management including golf courses, sports facilities, and professional landscaping represents a structurally growing premium CRF application segment where precise nutrient delivery directly translates into appearance quality and maintenance cost reduction. CRF adoption in professional ornamental and nursery production is accelerating through regulatory requirements on nutrient runoff management and premium willingness to pay in these high-value market segments.

4. Emerging Market Penetration Through Smallholder Farmer Agronomic Programs

Leading CRF manufacturers are developing smallholder-targeted program models in high-growth emerging markets including India and Southeast Asia, combining subsidized CRF access with mobile agronomic advisory services and field demonstration programs. These programs address the primary adoption barriers of cost and agronomic knowledge in developing markets, creating long-term demand development infrastructure in markets with 3-6x potential unit volume growth trajectory through 2034.

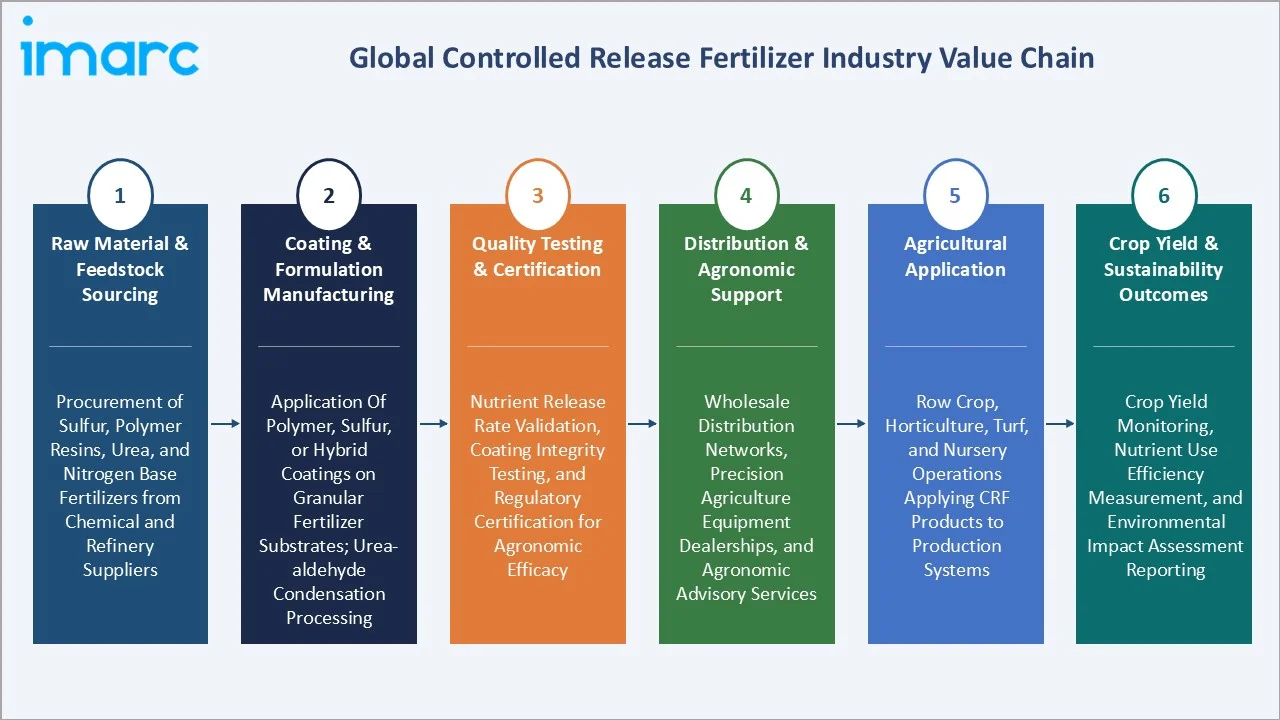

Industry Value Chain Analysis

The CRF value chain integrates raw material and feedstock procurement, coating and formulation manufacturing, quality testing, distribution and agronomic advisory services, and end-user agricultural application with crop performance monitoring. The commercial architecture of CRF supply chains is consolidating toward integrated manufacturer-agronomist-farmer relationships as technical complexity requires embedded agronomic support throughout the value chain.

|

Stage |

Key Activities |

|

Raw Material & Feedstock Sourcing |

Procurement of sulfur, polymer resins, urea, and nitrogen base fertilizers from chemical and refinery suppliers |

|

Coating & Formulation Manufacturing |

Application of polymer, sulfur, or hybrid coatings on granular fertilizer substrates; urea-aldehyde condensation processing |

|

Quality Testing & Certification |

Nutrient release rate validation, coating integrity testing, and regulatory certification for agronomic efficacy |

|

Distribution & Agronomic Support |

Wholesale distribution networks, precision agriculture equipment dealerships, and agronomic advisory services |

|

Agricultural Application |

Row crop, horticulture, turf, and nursery operations applying CRF products to production systems |

|

Crop Yield & Sustainability Outcomes |

Crop yield monitoring, nutrient use efficiency measurement, and environmental impact assessment reporting |

The coating manufacturing tier represents the highest value-add and technology differentiation stage, with proprietary coating formulations and release profile control constituting the primary competitive moat for CRF manufacturers. The distribution and agronomic support tier are experiencing rapid commercial transformation as digital platforms enable manufacturer-direct agronomic engagement with farmers at scale.

Technology Landscape in the Controlled Release Fertilizer Industry

Polymer-Coated Fertilizer Technology

Polymer-coated CRF technology applies thin thermoplastic or thermoset polymer membranes to granular fertilizer substrates, creating a semi-permeable barrier that controls nutrient diffusion rate based on temperature, soil moisture, and coating thickness. Advanced polyolefin and polyurethane coating systems provide tunable release profiles from 30 to 360 days, enabling precise matching of nutrient delivery to crop growth stage requirements. Polymer-coated CRFs represent the highest-performance and highest-margin CRF product category globally.

Sulfur-Coated Urea Technology

Sulfur-coated urea applies molten sulfur as a coating material around urea granules, providing a cost-effective controlled release mechanism through gradual sulfur oxidation enabling nitrogen diffusion. SCU products provide slower and less precisely controllable release profiles than polymer coatings but at significantly lower manufacturing cost, positioning them for price-sensitive commodity crop applications. Sulfur-polymer coated fertilizers combining SCU and polymer technologies provide intermediate performance and cost positioning.

Urea-Formaldehyde Condensation Technology

Urea-formaldehyde and related urea-aldehyde condensation products deliver nitrogen through slow microbial decomposition of the condensation polymer, providing season-long nitrogen availability through biological release mechanisms. The products offer low cost, absence of polymer coating environmental concerns, and compatibility with organic certification in some markets. Their release mechanism dependence on soil microbial activity creates release rate variability with temperature and soil biological conditions, requiring careful agronomy protocol selection.

Biodegradable and Bio-based Coating Technology

Biodegradable CRF coating technology utilizes natural polymer-derived materials including starch, lignin, cellulose acetate, and bio-polyesters to create coating membranes that decompose fully in soil environments without leaving microplastic residues. Bio-based coatings address the primary environmental concern associated with conventional polymer-coated CRFs while maintaining comparable nutrient release profile control.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Coated and Encapsulated Fertilizers |

56.8% |

2025 |

|

Form |

Granular |

62.4% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

North America |

35.7% |

2025 |

By Type

Coated and Encapsulated Fertilizers lead at 56.8% in 2025, capturing the premium precision nutrition segment with superior release profile controllability and compatibility with high-value crop systems. The segment's leadership reflects the agronomic performance advantages and premium pricing power of polymer-coated, and sulfur-polymer coated products across key markets.

To access detailed market analysis, Request Sample

Condensation Products of Urea and Aldehydes at 31.6% represent the cost-effective slow-release segment, widely adopted in commodity row crop applications where price sensitivity constrains adoption of premium polymer-coated products.

By Form

Granular form leads at 62.4% through universal compatibility with standard and precision application equipment, ease of handling, storage stability, and availability across all major crop systems and geographies. Granular CRFs dominate row crop and large-scale commercial agricultural applications globally.

Liquid CRFs at 23.7% are growing in fertigation and drip irrigation system applications, particularly in horticultural, greenhouse, and high-value vegetable production where liquid delivery enables more precise nutrient placement. Powder form at 13.9% serves professional nursery, greenhouse substrate production, and controlled environment agriculture applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

North America |

35.7% |

Precision agriculture adoption, EPA nutrient management compliance, and extensive row crop and specialty crop production base |

|

Europe |

26.4% |

EU Nitrates Directive compliance, Common Agricultural Policy sustainability provisions, and strong environmental regulations on nutrient runoff |

|

Asia-Pacific |

22.8% |

China's agricultural sustainability programs, Japan's premium crop production sector, and India's soil health program expansion |

|

Latin America |

9.1% |

Brazil's soy and sugarcane precision agriculture adoption and rising commercial crop premium nutrition requirements |

|

Middle East & Africa |

6.0% |

Arid climate water-efficiency farming programs and emerging adoption of nutrient-efficient technologies |

North America, at 35.7%, leads through the United States' extensive row crop production base, strong precision agriculture infrastructure, and regulatory frameworks including EPA nutrient management requirements mandating fertilizer use efficiency. The US specialty crop sector represents the highest-value per-acre CRF application segment globally.

Europe, at 26.4%, reflects EU Nitrates Directive-driven adoption and Common Agricultural Policy sustainability provisions. Asia-Pacific, at 22.8%, grows through China's agricultural sustainability programs, Japan's premium crop nutrition market, and India's developing precision agriculture adoption. Latin America at 9.1% and Middle East & Africa at 6.0% represent earlier-stage but structurally growing CRF markets.

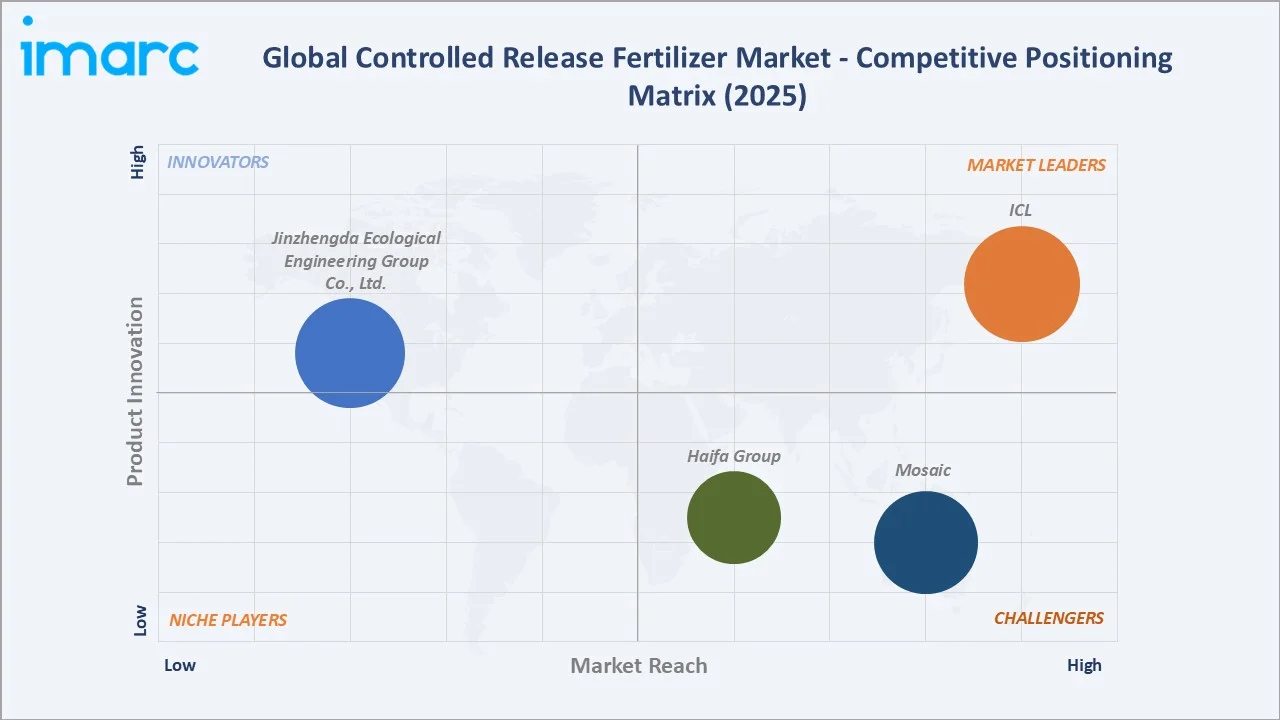

Competitive Landscape

The global controlled release fertilizer market competitive landscape is moderately fragmented with a defined tier of global specialty fertilizer majors, regional CRF specialists, and emerging domestic manufacturers competing across geographic markets and crop application segments.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

ICL |

Agroblen, Agromaster, Agriform, Agrocote |

Market Leader |

Specialty fertilizer manufacturer with proprietary polymer coating technology and global distribution |

|

Mosaic |

MicroEssentials Range |

Strong Challenger |

Integrated phosphate and potash producer with CRF product development capabilities |

|

Haifa Group |

Multicote, Multicote Agri, CoteN, Multigreen |

Strong Challenger |

Specialty CRF producer focused on drip irrigation and fertigation market applications |

|

Jinzhengda Ecological Engineering Group Co., Ltd. |

Controlled-release compound fertilizer, Controlled Release Potassium Nitrate & Controlled Release Phosphoric Acid, Controlled release fertilizer polymer coated urea |

Established |

China-based CRF manufacturer with large domestic scale and cost-competitive production |

Key players include ICL, Mosaic, Haifa Group, Jinzhengda Ecological Engineering Group Co., Ltd., and others.

Key Company Profiles

ICL

ICL is an Israel-based specialty minerals and specialty fertilizer company with a significant position in the controlled release fertilizer market through its polymer-coated fertilizer product lines serving professional horticulture, turf management, and row crop markets globally.

- Key Products: Agroblen, Agromaster, Agriform, Agrocote

- Strategic Focus: Biodegradable coating technology commercialization, expansion of CRF product applications into emerging Asian agricultural markets, and precision agriculture platform integration for digital agronomic service differentiation.

Mosaic

Mosaic is a United States-based producer and marketer of phosphate and potash crop nutrients with CRF product development capabilities and specialty fertilizer blend products for the North American and global agricultural markets.

- Key Products: MicroEssentials Range

- Strategic Focus: Strengthening integrated specialty fertilizer positioning in North American corn and soybean belt markets, expanding CRF technology adoption in Latin American premium crop systems, and developing next-generation enhanced efficiency fertilizer products aligned with sustainability and regulatory requirements.

Market Concentration Analysis

The CRF market is moderately fragmented at the global level, with top 3-4 players collectively accounting for approximately 35-45% of global CRF revenue. Regional specialists hold significant positions in specific geographic and application segment markets.

Market concentration is stable in premium polymer-coated CRF segments but declining in commodity slow-release segments as Chinese and Asian domestic manufacturers expand production capacity and improve product quality. Regulatory-driven technology transitions toward biodegradable coatings are creating potential disruption to established competitive positions, with early-movers in biodegradable coating technology likely to gain structural market share advantages in regulated markets through 2030.

Investment & Growth Opportunities

Highest Growth Segments

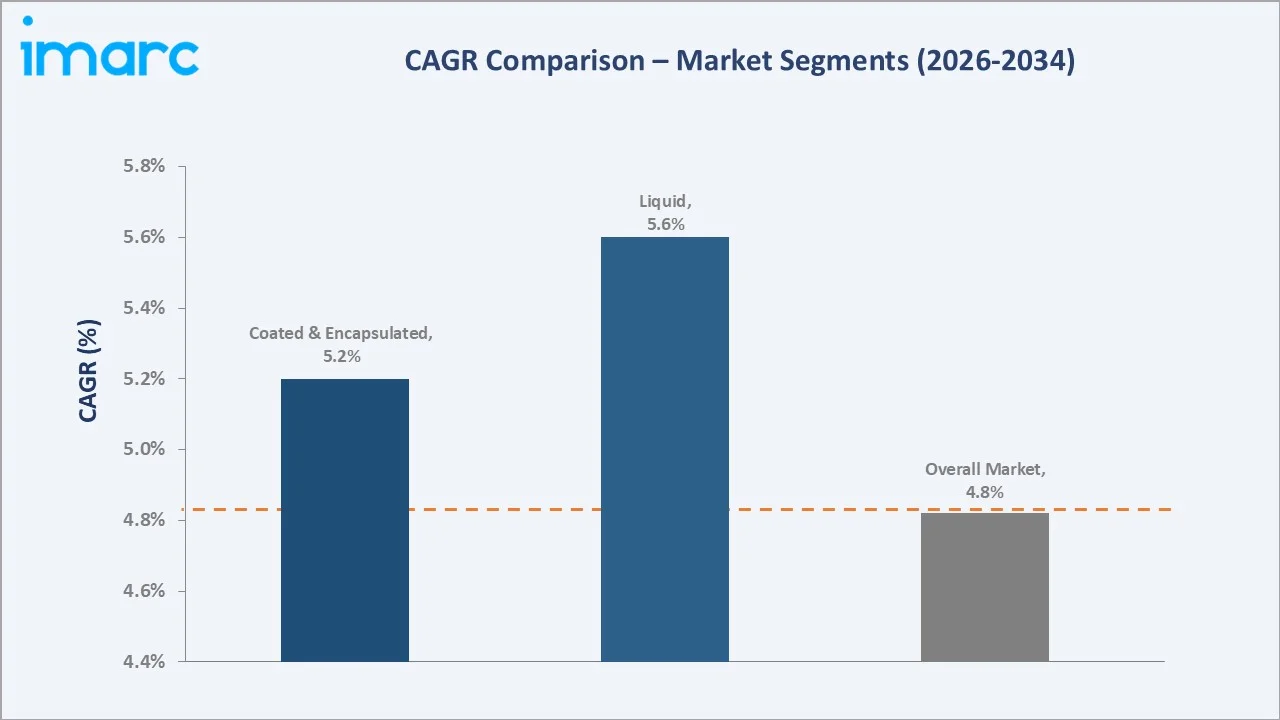

Liquid CRF for fertigation (~5.6% CAGR), biodegradable polymer-coated CRF premium segment (~12-15% CAGR from smaller base), Asia-Pacific row crop CRF penetration (~6.0% CAGR), smart sensor-responsive CRF formulations (~18-22% CAGR from near-zero base), and Latin American precision agriculture CRF adoption (~5.5% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Biodegradable CRF coating technology commercialization represents the CRF market's highest-value emerging investment opportunity, with first-mover regulatory compliance positioning in EU markets creating a durable competitive advantage. Smart CRF formulations integrated with IoT precision agriculture systems represent a USD 200-400 Million addressable market by 2030, with premium per-ton pricing potential 3-5x above conventional polymer-coated CRF products.

Investment Themes

- Biodegradable coating R&D investment for EU and North American regulatory compliance advantage: Manufacturers investing in certified biodegradable polymer coating technologies will access premium regulatory-compliance market segments with structural pricing advantages over conventional polymer-coated products as EU microplastic restrictions on agricultural coatings take effect through the forecast period.

- Asia-Pacific smallholder CRF adoption program development: Structured agronomic program development in India's kharif and rabi crop cycles and Southeast Asia rice production systems creates long-term addressable market development in regions with 3-5x potential CRF demand growth from near-zero current penetration rates, representing the largest volume growth opportunity in the global CRF market.

Future Market Outlook (2026-2034)

The global controlled release fertilizer market is projected to grow from USD 3.44 Billion in 2025 to USD 5.33 Billion by 2034, delivering a 4.82% CAGR over the forecast period. The market's anchor value of USD 4.36 Billion in 2030 represents a CRF industry at its critical commercial inflection from early adoption to mainstream agricultural practice in key crop systems globally.

Three structural forces define CRF market growth through 2034. Global food security pressures and arable land constraints are creating irreversible incentives for fertilizer use efficiency improvement at the farm level. Regulatory tightening on nutrient runoff across major agricultural markets creates structural demand for CRF products meeting environmental compliance requirements. Digital precision agriculture platform adoption creates agronomic decision-support infrastructure necessary for optimized CRF deployment, removing the primary knowledge barrier to farmer adoption in both developed and emerging agricultural markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including CRF product development scientists, precision agriculture agronomists, specialty fertilizer distributors, crop nutrition regulatory specialists, and commercial farming operation managers across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary research encompassed company annual reports; IFA global crop nutrition demand data; FAO food security production projections; EU Nitrates Directive compliance reporting; EPA Nutrient Management Regulation documentation; and over 55 secondary sources reviewed for market sizing and trend validation.

Forecasting Models

Market revenue forecasts were developed using a crop application bottom-up model integrating global arable land by crop system, CRF adoption penetration rate projections by crop and geography, average CRF application rate per hectare, and average CRF product pricing by technology tier, with technology premium adjustments applied for biodegradable and smart CRF product segments.

Controlled Release Fertilizer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Forms Covered | Granular, Liquid, Powder |

| Applications Covered | Grains and Cereals, Pulses and Oilseeds, Commercial Crops, Fruits and Vegetables, Turf and Ornamentals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ICL, Mosaic, Haifa Group, Jinzhengda Ecological Engineering Group Co., Ltd.,etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the controlled release fertilizer industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Controlled Release Fertilizer Market Report

The global CRF market reached USD 3.44 Billion in 2025, driven by Coated and Encapsulated Fertilizers dominant at 56.8%, Granular form leading at 62.4%, and North America commanding 35.7% market share through precision agriculture adoption and regulatory nutrient management compliance requirements.

The CRF market grows at 4.82% CAGR during 2026-2034, reaching USD 5.33 Billion by 2034. Growth reflects regulatory-driven fertilizer use efficiency mandates, precision agriculture adoption, and emerging biodegradable coating technology premium segment development.

Coated and Encapsulated Fertilizers lead at 56.8%, capturing the premium precision nutrition segment. Polymer-coated products deliver superior release profile controllability for high-value crop, turf, and horticultural applications, sustaining segment dominance through the 2034 forecast period.

Granular form leads at 62.4% through universal compatibility with conventional and precision application equipment, ease of handling, and applicability across all major crop systems from large-scale row crop to specialty horticulture operations globally.

North America leads at 35.7% through the United States' extensive row crop and specialty crop production, EPA nutrient management compliance requirements, and strong precision agriculture infrastructure enabling optimized CRF agronomic deployment at commercial scale.

Leading companies include ICL, Mosaic, Haifa Group, Jinzhengda Ecological Engineering Group Co., Ltd., and others.

The CRF market is projected to reach approximately USD 4.36 Billion by 2030, with biodegradable polymer coatings achieving first commercial scale, Asia-Pacific penetration accelerating, and liquid CRF fertigation systems becoming standard in premium horticultural production globally.

Three priority investment opportunities: biodegradable CRF coating technology commercialization for EU regulatory compliance market leadership; Asia-Pacific smallholder agronomic program development; and smart sensor-responsive CRF formulation development for premium precision agriculture integration and value-added product positioning.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)