Diesel Common Rail Injection System Market Size, Share, Trends and Forecast by Vehicle Type, Fuel Injector Type, Engine, Sales Channel, and Region, 2026-2034

Diesel Common Rail Injection System Market Size, Share, Trends & Forecast (2026-2034)

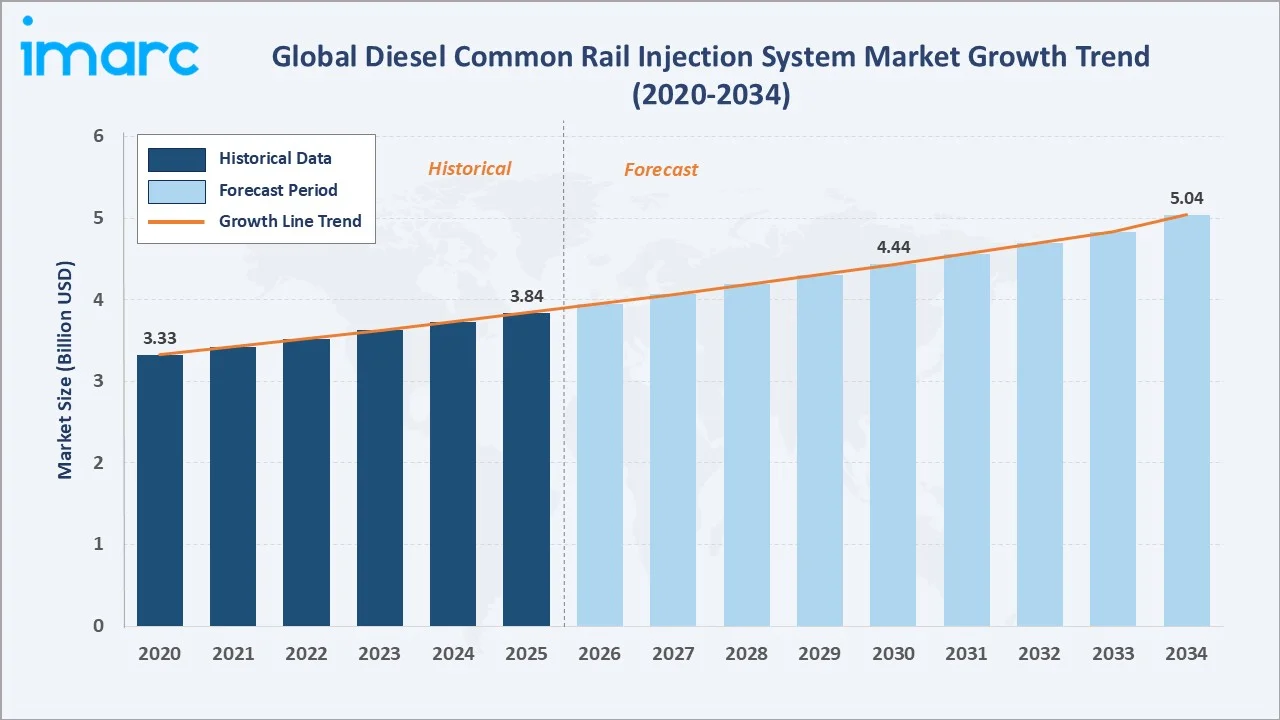

The global diesel common rail injection system market reached USD 3.84 Billion in 2025 and is projected to reach USD 5.04 Billion by 2034, growing at a CAGR of 2.92% during 2026-2034. Market expansion is anchored by tightening emission norms, robust commercial vehicle production across Asia-Pacific, and continuous technological upgrades in injection pressure and electronic control.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.84 Billion |

|

Forecast Market Size (2034) |

USD 5.04 Billion |

|

CAGR (2026-2034) |

2.92% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (39.8% share, 2025) |

|

Fastest Growing Segment |

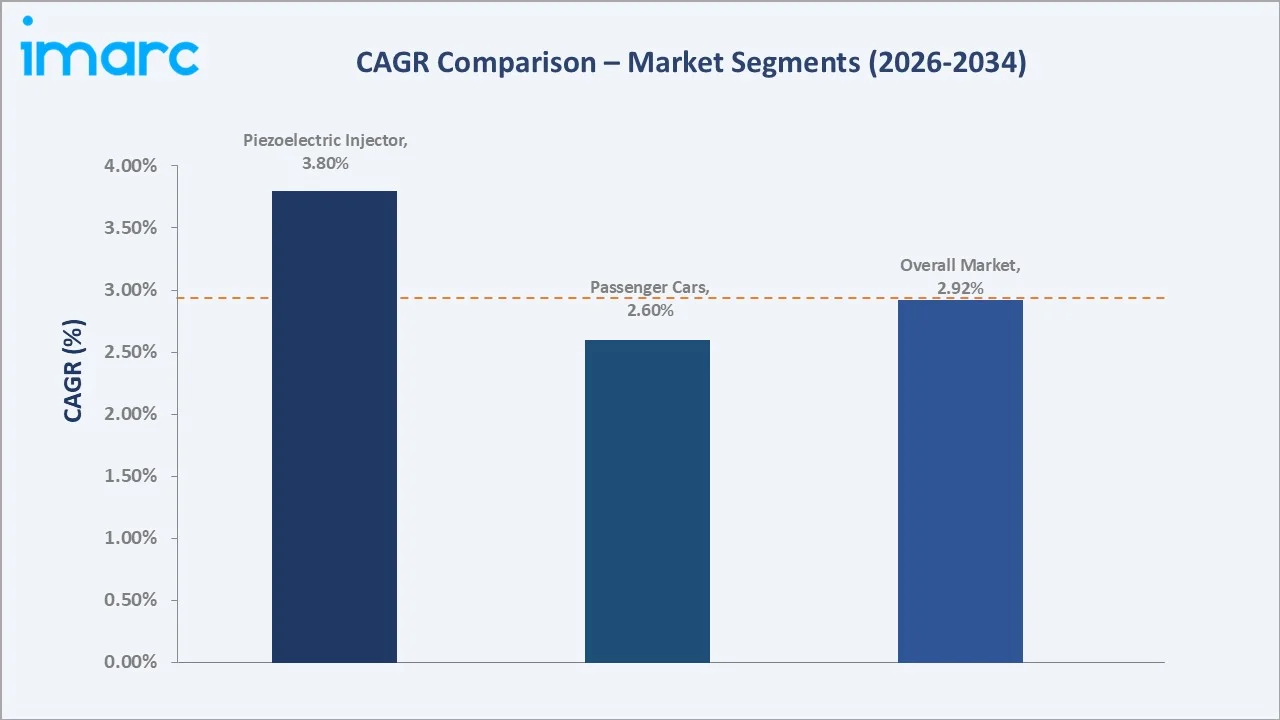

Piezoelectric Injector (~3.80% CAGR) |

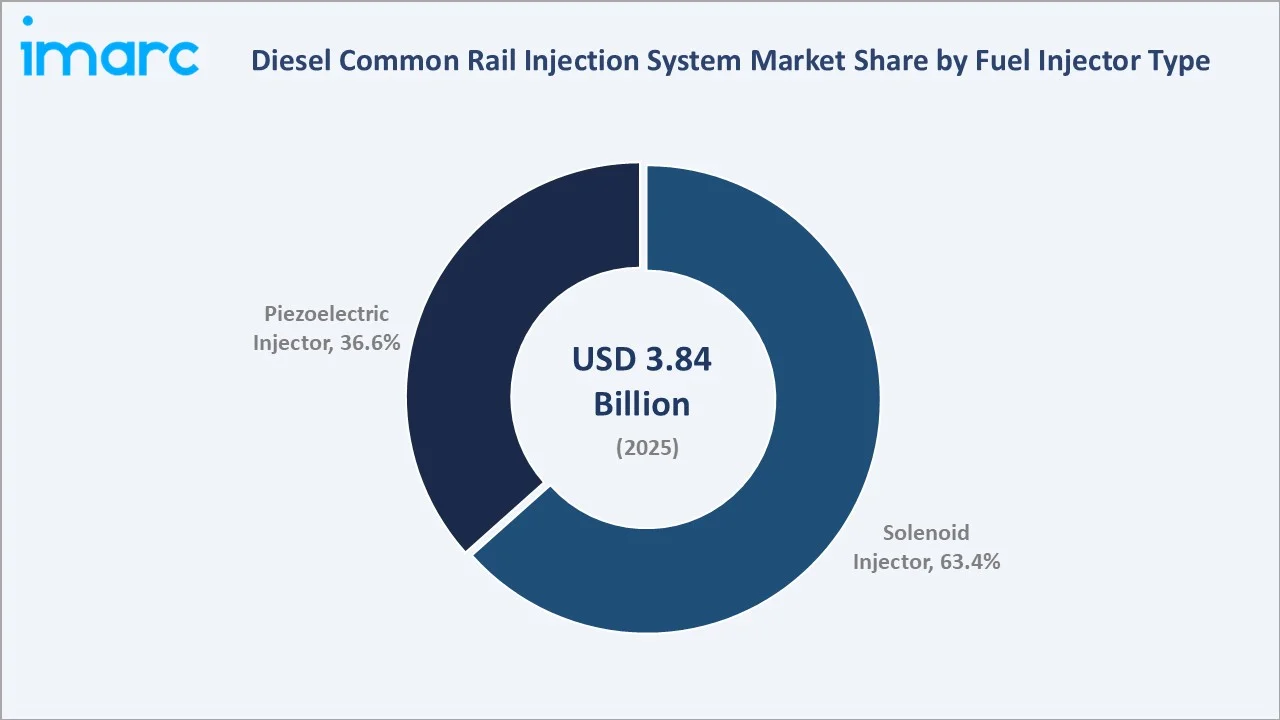

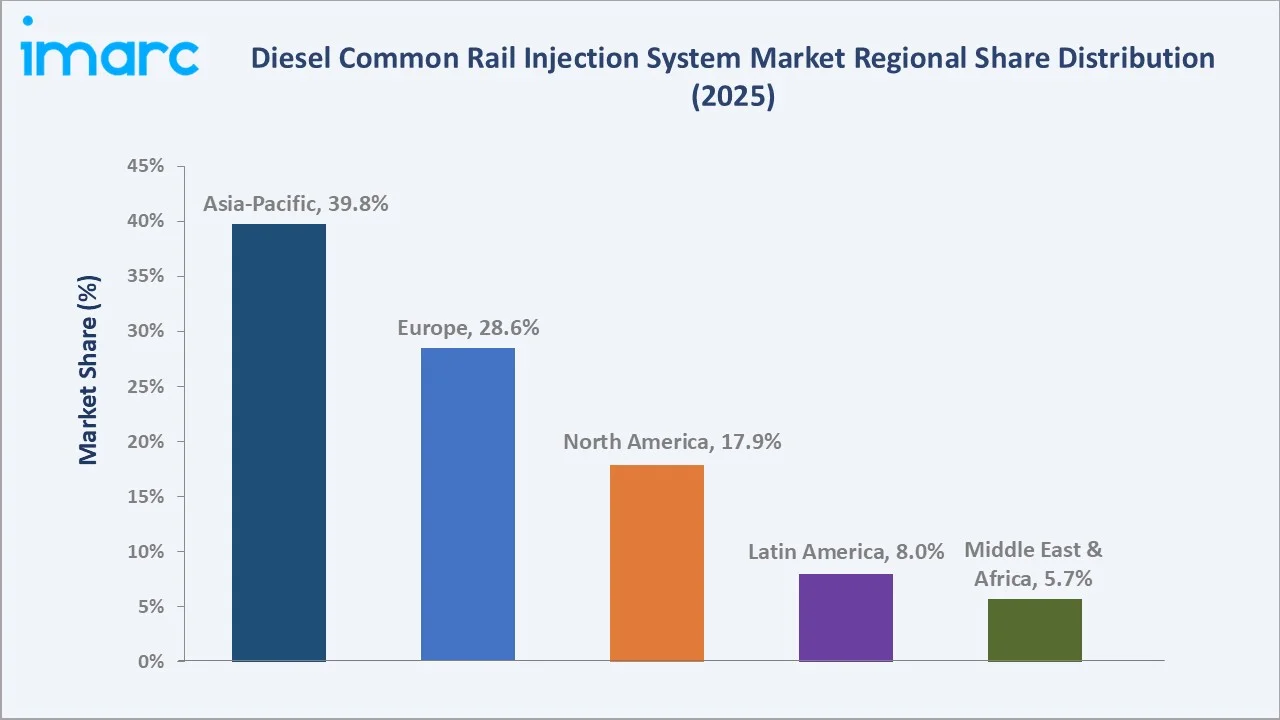

Asia-Pacific dominates with a 39.8% regional share in 2025, while solenoid injectors command 63.4% of the fuel injector type breakdown. Asia-Pacific's leadership is driven by China's massive commercial vehicle output, India's accelerating BS-VI compliance cycle, and Japan's precision manufacturing ecosystem for high-pressure injection components.

To get more information on this market, Request Sample

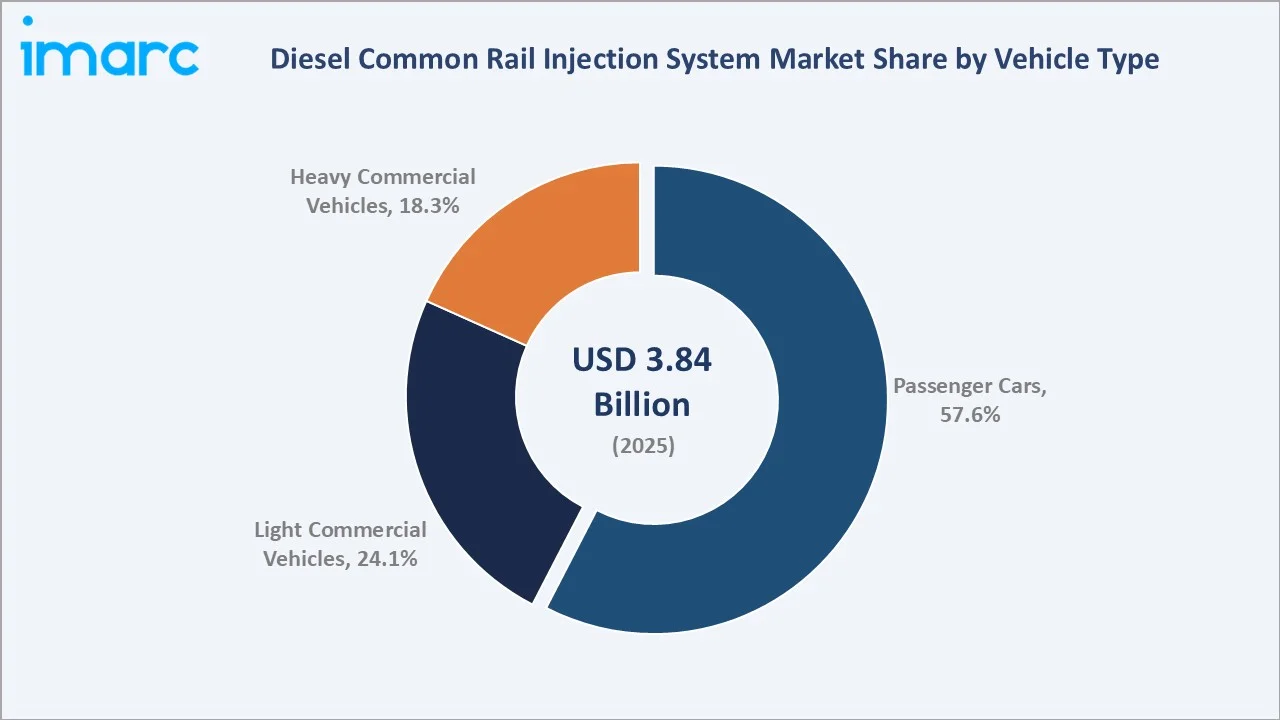

The passenger car segment's 57.6% dominance reflects the widespread use of common rail direct injection (CRDI) engines in diesel sedans and crossovers across Europe and Asia. The diesel CRDI market's steady growth trajectory is structurally supported by the continued global dependence on diesel powertrains in logistics, agriculture, and heavy industry, even as electrification accelerates in light passenger segments.

Executive Summary

The global diesel common rail injection system market is on a measured growth trajectory, driven by stringent emission legislation, sustained commercial vehicle demand, and precision technology upgrades. The market was valued at USD 3.84 Billion in 2025 and is forecast to reach USD 5.04 Billion by 2034, representing incremental value creation of USD 1.20 Billion at a 2.92% CAGR.

Passenger cars lead with a 57.6% vehicle-type share, driven by the widespread adoption of CRDI engines in mid-size and premium diesel cars, particularly across Europe and Asia-Pacific. Solenoid injectors hold a 63.4% share of the injector type segment in 2025, though piezoelectric variants are gaining traction in high-performance and ultra-low-emission engine configurations.

Key players, including Robert Bosch GmbH, DENSO Corporation, Cummins Inc., and Hyundai Motor Company, dominate through deep OEM partnerships, proprietary injection calibration software, and continuous pressure-rating and atomization improvements aligned to Euro 7 emission mandates.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Type |

Passenger Cars – 57.6% share (2025) |

|

Largest Fuel Injector Type |

Solenoid Injector – 63.4% share (2025) |

|

Fastest Growing Injector |

Piezoelectric Injector – ~3.80% CAGR (2026-2034) |

|

Leading Region |

Asia-Pacific – 39.8% share (2025) |

|

Top Companies |

Robert Bosch GmbH, DENSO Corporation, Cummins Inc., Hyundai Motor Company |

Key Analytical Observations:

- Passenger cars account for 57.6% of the diesel CRDI market in 2025. This dominance reflects the large installed base of diesel-powered vehicles in Europe and Asia, where CRDI engines remain the preferred powertrain for mid-range sedans, crossovers, and compact SUVs due to superior torque and fuel economy versus petrol equivalents.

- Solenoid injectors at 63.4% (2025) remain dominant owing to their proven reliability, lower unit cost, and compatibility with existing engine architectures. They are the standard choice for volume-segment passenger cars and LCVs produced by European and Korean OEMs.

- Piezoelectric injectors, with a 36.6% share (2025), are the fastest-growing injector type with an estimated 3.80% CAGR. Their faster actuation speed (up to 5× faster than solenoid), finer fuel metering, and ability to handle 2,500+ bar injection pressures make them the preferred technology for Euro 7 engine platforms.

- Asia-Pacific's 39.8% (2025) dominance is anchored by nearly 12 million diesel trucks that transport approximately 70% of India’s freight, accounting for 55% of national diesel consumption and an estimated annual fuel expenditure of USD 50 billion. Moreover, China's China-VI standard enforcement from 2021 onwards has compelled OEMs to upgrade to high-pressure CRDI systems across all heavy-duty vehicle categories.

Diesel Common Rail Injection System Market Overview

A diesel common rail injection system (DCRIS) is a fuel delivery architecture that maintains diesel fuel at high pressure in a shared rail and injects it directly into each cylinder via electronically controlled injectors. This enables multiple injections per combustion cycle, precise fuel metering, and operating pressures of 1,600–2,500 bar in modern systems. CRDI technology encompasses high-pressure pumps, common rail assemblies, solenoid or piezoelectric injectors, electronic control units (ECUs), and pressure sensors.

The market encompasses OEM supply to passenger car manufacturers, commercial vehicle producers, agricultural equipment OEMs, and construction machinery makers, as well as aftermarket replacement injectors and pump assemblies. Regulatory compliance with emission standards is the primary technical demand driver, compelling continuous pressure-rating and injector-geometry improvements from system suppliers.

Market Dynamics

To evaluate market opportunities, Request Sample

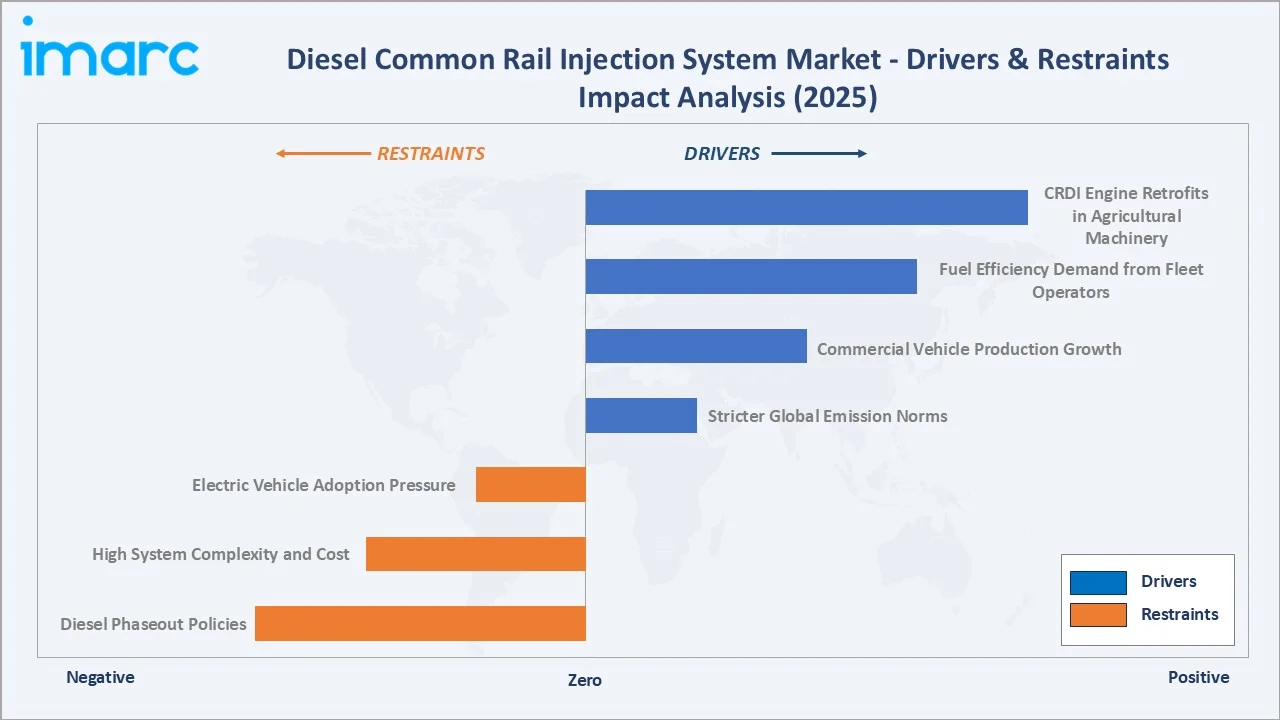

Market Drivers

- Stricter Global Emission Norms: Euro 7 (expected effective from November 2026), China-VI, and India's BS-VI Phase 2 mandate substantially lower NOx and particulate emissions from diesel engines. Compliance requires injection pressures above 2,000 bar and multi-injection strategies only achievable with advanced CRDI systems, directly driving technology upgrade demand across OEM supply chains.

- Commercial Vehicle Production Growth: As per ACEA, in 2025, diesel remained the preferred power source in the EU truck market with 93.2% of the total new registrations. Each heavy-duty truck requires a complete CRDI system valued at USD 1,200–2,500, creating substantial per-unit content value for system suppliers.

- Fuel Efficiency Demand from Fleet Operators: Long-haul logistics operators seek fuel savings of 5–12% that modern high-pressure CRDI systems deliver over older injection architectures, driving retrofit and upgrade demand across aging commercial vehicle fleets in Latin America, Southeast Asia, and the Middle East.

- CRDI Engine Retrofits in Agricultural Machinery: Mechanized farming expansion in India, Brazil, and Southeast Asia is driving tractor and combine harvester CRDI adoption, as Tier 4 Final and Stage V compliant engines replace mechanical injection systems.

Market Restraints

- Electric Vehicle Adoption Pressure: Accelerating EV penetration in passenger car segments is reducing future CRDI demand in the vehicle type that currently accounts for 57.6% of the market. In 2025, battery-electric cars captured 17.4% of the EU market, up from 13.6% in the previous year, constraining long-term diesel OEM procurement volumes.

- High System Complexity and Cost: A complete CRDI system for a passenger car costs USD 400–900 at OEM pricing. This cost differential constrains uptake in price-sensitive vehicle segments in emerging markets where mechanical injection alternatives remain viable.

- Diesel Phaseout Policies: In December 2025, the European Commission proposed requiring new car fleets sold from 2035 onward to reduce average tailpipe emissions by 90%. Along with that, the city-level diesel access restrictions are creating long-term demand uncertainty for passenger car CRDI systems, reducing OEM investment horizons for next-generation platforms.

Market Opportunities

- Piezoelectric Injector Uptiering: Transition to piezoelectric injectors for Euro 7 platforms creates a USD 400+ Million incremental market by 2030. Robert Bosch GmbH and DENSO Corporation, are investing in piezoelectric stack manufacturing capacity to meet anticipated specification upgrade timelines.

- HVO-Ready Injection Systems: Modification of CRDI hardware for hydrotreated vegetable oil (HVO) and synthetic diesel fuels creates an upgrade opportunity as fleet operators transition to renewable fuels without full electrification.

Market Challenges

- Precision Manufacturing Requirements: CRDI components require tolerances of 1–3 microns in injector nozzle geometries and sub-millisecond electronic actuation accuracy. Maintaining these specifications across high-volume production is a significant challenge for tier-2 and tier-3 suppliers.

- Supply Chain Fragility for Rare Earth and Precision Metals: Piezoelectric actuators require lead zirconate titanate (PZT) ceramics, while high-pressure pump plungers require ultra-hard carbide composites. Supply concentration in China for rare earth-derived materials creates sourcing vulnerability.

Emerging Market Trends

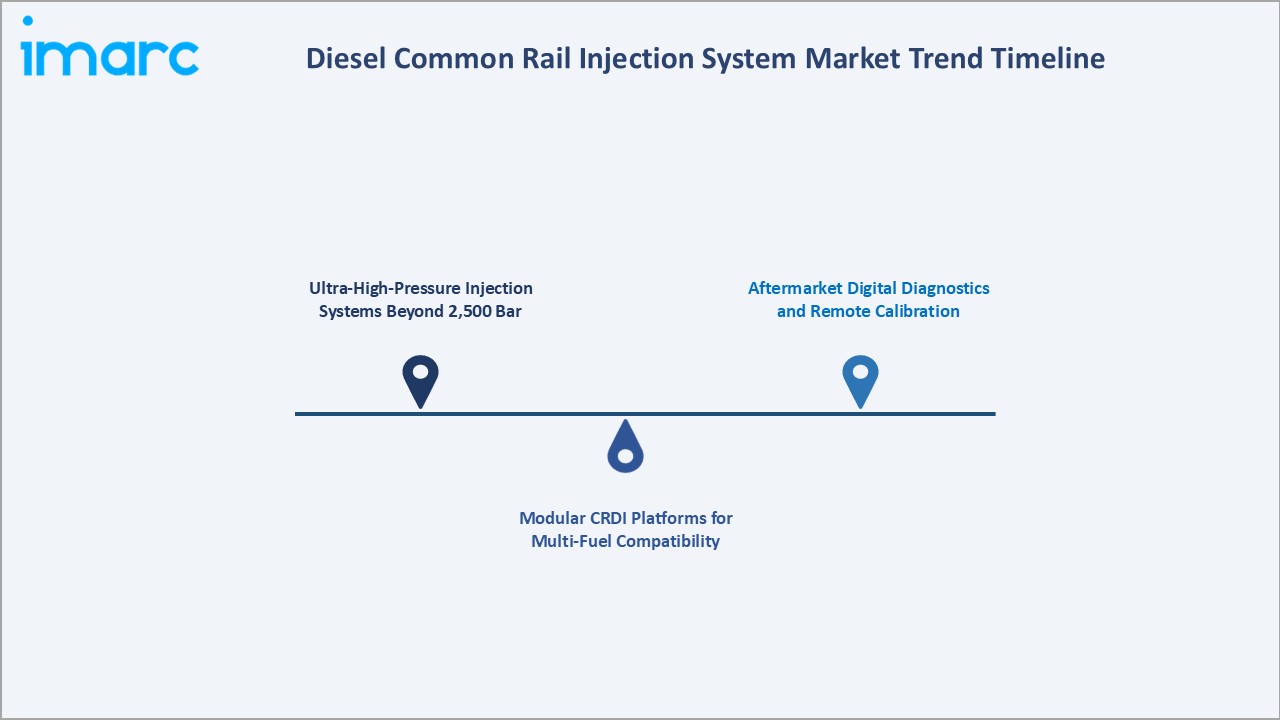

1. Ultra-High-Pressure Injection Systems Beyond 2,500 Bar

Robert Bosch GmbH’s second-generation CRDI systems for Euro 7 compliance operate at 2,700 bar injection pressure, reducing particulate formation by up to 40% compared to 1,800 bar. Injection pressures above 2,000 bar are becoming the OEM standard for heavy-duty engines, driving materials innovation in high-strength pump plungers, rail forgings, and injector nozzle coatings.

2. Modular CRDI Platforms for Multi-Fuel Compatibility

Multiple companies are developing modular CRDI architectures compatible with diesel, HVO, and synthetic fuels. These platforms allow OEMs to offer identical hardware certified for multiple fuel types, reducing development costs and future-proofing fleet investments as renewable fuel mandates expand across the EU and North America.

3. Aftermarket Digital Diagnostics and Remote Calibration

Connected vehicle platforms are enabling remote CRDI diagnostics and over-the-air ECU recalibration for fleet operators. PHINIA’s Delphi diagnostic tools reduce fuel injector maintenance costs by approximately 25% through predictive replacement scheduling.

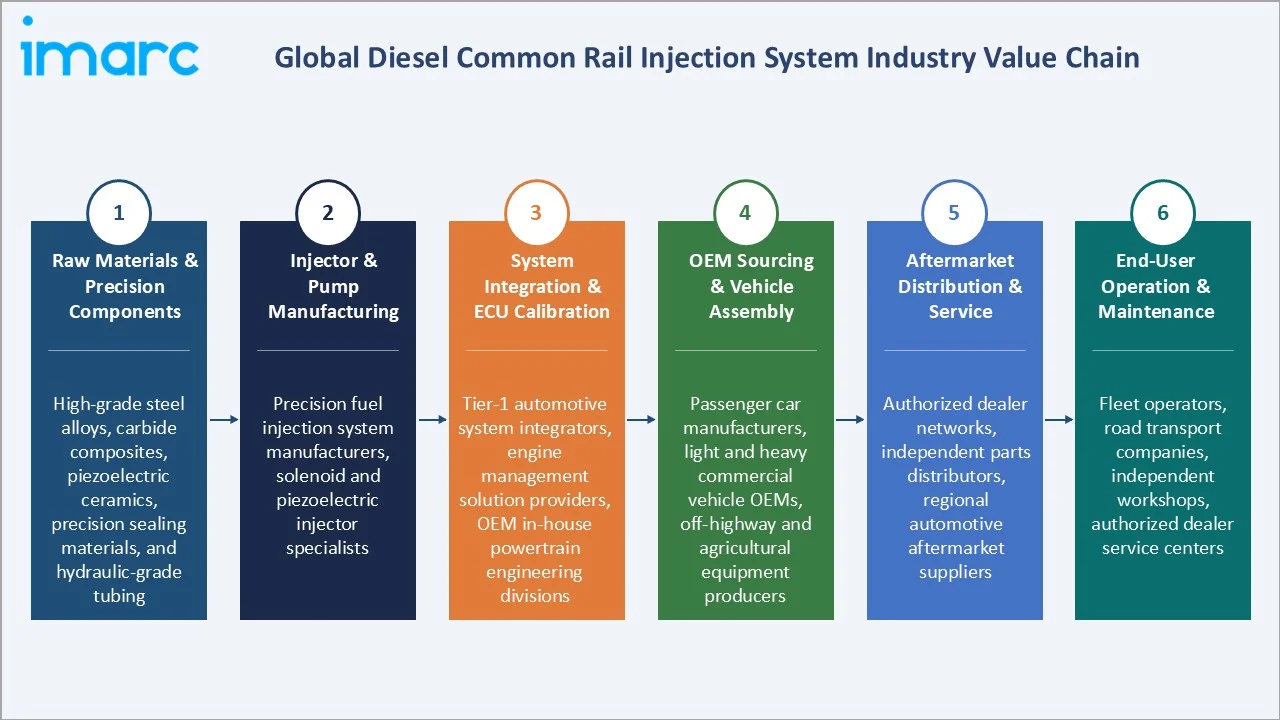

Industry Value Chain Analysis

The diesel CRDI value chain spans precision material inputs through end-user maintenance, with each stage requiring highly specialized capabilities in metallurgy, electronics, and calibration.

|

Stage |

Key Players / Examples |

|

Raw Materials & Precision Components |

High-grade steel alloys, carbide composites, piezoelectric ceramics, precision sealing materials, and hydraulic-grade tubing |

|

Injector & Pump Manufacturing |

Precision fuel injection system manufacturers, solenoid and piezoelectric injector specialists |

|

System Integration & ECU Calibration |

Tier-1 automotive system integrators, engine management solution providers, OEM in-house powertrain engineering divisions |

|

OEM Sourcing & Vehicle Assembly |

Passenger car manufacturers, light and heavy commercial vehicle OEMs, off-highway and agricultural equipment producers |

|

Aftermarket Distribution & Service |

Authorized dealer networks, independent parts distributors, regional automotive aftermarket suppliers |

|

End-User Operation & Maintenance |

Fleet operators, road transport companies, independent workshops, authorized dealer service centers |

Technology Landscape in the Diesel Common Rail Injection System Industry

Solenoid Injector Technology

Solenoid injectors use an electromagnetic solenoid to control a needle valve that opens and closes the injection orifice. They are the workhorse technology for volume-segment passenger cars and LCVs, compatible with injection pressures up to 2,200 bar in state-of-the-art configurations.

Piezoelectric Injector Technology

Piezoelectric injectors use a stack of lead zirconate titanate (PZT) crystals that expand when voltage is applied, providing actuation speeds 5× faster than solenoid equivalents. This enables up to 10 injection events per combustion cycle, dramatically reducing combustion noise and particulate formation.

High-Pressure Pump Systems

The high-pressure pump maintains rail pressure between 1,600 and 2,700 bar regardless of engine speed and load. Robert Bosch GmbH’s CP3/CP4 pump families are the dominant OEM choices globally. Diamond-like carbon (DLC) coatings on plunger surfaces have extended service life to 500,000 km equivalent in HD applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Passenger Cars |

57.6% |

2025 |

|

Fuel Injector Type |

Solenoid Injector |

63.4% |

2025 |

|

Engine |

🔒 |

🔒 |

2025 |

|

Sales Channel |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

39.8% |

2025 |

By Vehicle Type

Passenger cars lead the vehicle-type segment with a 57.6% share in 2025. This segment covers diesel-powered sedans, hatchbacks, crossovers, and SUVs equipped with CRDI engines delivering 1,600–2,200 bar injection pressure. European markets, where diesel passenger cars retain significant share in mid-size and large segments, and Asia-Pacific, where diesel SUVs and crossovers are popular in India and Southeast Asia, anchor this segment.

To access detailed market analysis, Request Sample

Light commercial vehicles (LCVs) hold a 24.1% share. Diesel LCVs, including vans, pickup trucks, and small buses, are the workhorses of urban last-mile logistics. Heavy commercial vehicles (HCVs) account for 18.3%, representing trucks, heavy buses, and off-highway equipment requiring the highest-specification CRDI systems operating at 2,000–2,700 bar.

By Fuel Injector Type

Solenoid injectors dominate with a 63.4% share in 2025. Their cost-effectiveness, proven durability in high-volume production, and compatibility with current-generation emission standards make them the default specification for mainstream passenger car and LCV CRDI systems. Robert Bosch GmbH and DENSO Corporation supply solenoid injectors to virtually all major global diesel vehicle platforms.

Piezoelectric injectors represent 36.6% of the market in 2025, concentrated in premium passenger cars, Euro 7-compliant engines, and high-performance HCV applications. Their superior injection precision justifies the 40–60% unit price premium over solenoid alternatives.

Regional Market Insights

Asia-Pacific leads global diesel CRDI demand with a 39.8% share in 2025. The region's position reflects China's status as the world's largest commercial vehicle market, India's growing BS-VI vehicle base, and Japan's role as a precision CRDI component manufacturing hub.

Europe's 28.6% share reflects the region's large diesel vehicle installed base and the advanced technology specification required for Euro 7 compliance. North America at 17.9% is anchored by heavy-duty trucking, where diesel retains near-total powertrain dominance, with EPA Phase 3 greenhouse gas standards further driving injection system upgrades from 2027.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

39.8% |

Rapid expansion of commercial vehicle production, growing enforcement of stringent emission standards, rising off-road equipment fleet size |

|

Europe |

28.6% |

Advanced emission compliance requirements driving high-pressure injection system upgrades, large installed base of diesel passenger cars and heavy commercial vehicles |

|

North America |

17.9% |

Sustained demand from heavy-duty trucking and agricultural machinery segments, regulatory pressure on vehicle emissions and fuel efficiency |

|

Latin America |

8.0% |

Expanding commercial vehicle and logistics fleet, growing regulatory focus on vehicular emissions, rising fuel efficiency requirements among long-haul transport operators |

|

Middle East & Africa |

5.7% |

Growing commercial vehicle and off-highway equipment deployments, high ambient temperature conditions increasing cooling and injection system demand |

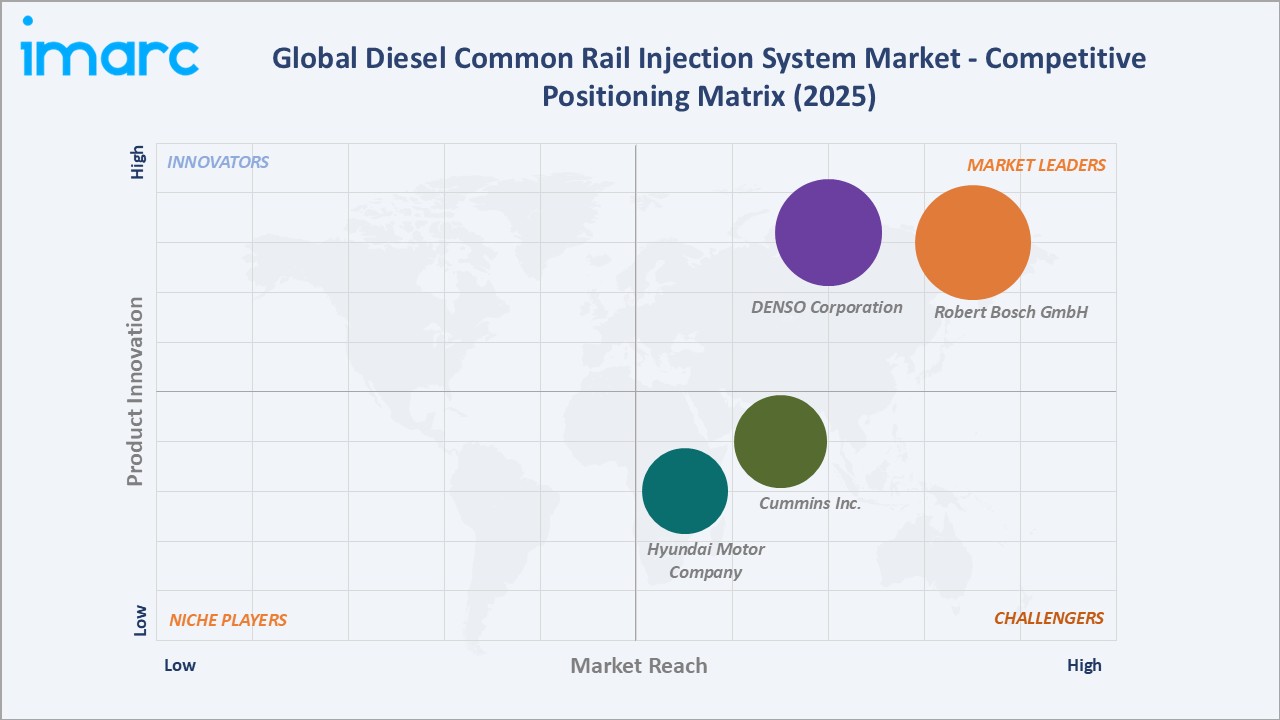

Competitive Landscape

The global diesel common rail injection system market is highly concentrated. Robert Bosch GmbH and DENSO Corporation together hold an estimated 55–60% of global OEM CRDI revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Robert Bosch GmbH |

Bosch |

Market Leader |

Broad OEM coverage across passenger car and commercial vehicle segments, advanced high-pressure injection technology, and proprietary engine control software platforms |

|

DENSO Corporation |

DENSO |

Market Leader |

Advanced piezoelectric injector technology, deep integration with Asian OEM platforms, and precision manufacturing capabilities across high-volume production facilities |

|

Cummins Inc. |

Cummins |

Challenger |

Specialization in heavy-duty and off-highway CRDI applications, integrated filtration and fuel system expertise, and an extensive global aftermarket distribution network |

|

Hyundai Motor Company |

KEFICO |

Challenger |

Captive OEM supply model serving domestic vehicle platforms, dual-technology injector manufacturing capability, and cost-competitive production infrastructure in South Korea |

Robert Bosch GmbH and Cummins Inc. represent the strong-challenger tier with complementary geographic and application strengths.

Key Company Profiles

Robert Bosch GmbH

Robert Bosch GmbH is one of the market leaders in diesel common rail injection technology. The company introduced one of the first commercial CRDI systems and has continuously advanced the technology to its current 2,700-bar specification.

- Product Portfolio: Solenoid injector families; piezoelectric injectors; high-pressure pumps; common rail assemblies; ECU platforms.

- Strategic Focus: Ultra-high-pressure solenoid and piezoelectric injector leadership; HVO and hydrogen co-injection compatibility; AI-driven ECU calibration platform development.

DENSO Corporation

DENSO Corporation is also one of the largest diesel common rail injection system suppliers globally and the primary supplier to Toyota's diesel engine programs.

- Product Portfolio: Piezoelectric injectors; HP3, high-pressure pumps; common rail assemblies; ECU platforms with AI-driven injection optimization.

- Strategic Focus: Piezoelectric injector scale-up, Toyota-ecosystem integration, India and Southeast Asia manufacturing expansion, and HVO-compatible injection platform development.

Market Concentration Analysis

The diesel CRDI market is highly concentrated, with DENSO Corporation and Robert Bosch GmbH alone representing an estimated 55–60% of global OEM revenues in 2025. The top vendors collectively account for approximately 80% of global CRDI system revenues, reflecting the capital intensity of precision manufacturing, the proprietary nature of ECU calibration IP, and the long-term OEM qualification cycles.

Consolidation in the second tier is accelerating. In July 2023, M&D acquired Seidel Diesel Group, strengthening M&D’s aftermarket diesel engine parts. The HCV and off-highway segments are relatively less concentrated, with Cummins Inc. and regional Chinese suppliers competing alongside the global tier-1 leaders.

Investment & Growth Opportunities

Fastest Growing Segments

Piezoelectric injectors (~3.80% CAGR), HVO-compatible CRDI systems, AI-enhanced ECU calibration platforms, and HCV aftermarket replacement injectors represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental addressable market of approximately USD 600 Million by 2034.

Emerging Market Expansion

India, Brazil, Indonesia, and Nigeria collectively represent a USD 300+ Million incremental CRDI opportunity by 2034, as emission standard upgrades compel OEMs and aftermarket suppliers to install high-pressure injection systems in previously lower-specification vehicle segments. India's commercial vehicle CRDI demand is projected to grow at 4.5% CAGR through 2034.

Venture and Institutional Investment Trends

- OEM investment in Euro 7 emission compliance creates a USD 800 Million+ injector upgrade procurement pipeline for tier-1 suppliers through 2028.

- Government PLI schemes in India for automotive components are enabling domestic CRDI pump and injector manufacturing capacity investment by tier-2 suppliers.

- Aftermarket digitization, including AI-driven predictive injector replacement services, is attracting technology investment with subscription-model aftermarket revenue streams.

Future Market Outlook (2026-2034)

The diesel common rail injection system market is positioned for moderate, steady growth through 2034. From USD 3.84 Billion in 2025, the market will reach USD 5.04 Billion by 2034, representing total incremental value creation of USD 1.20 Billion at a 2.92% CAGR. Growth will be anchored by commercial vehicle and agricultural equipment demand, even as light passenger car diesel volumes gradually decline under electrification pressure.

The technology composition will shift meaningfully toward piezoelectric injectors and 2,500+ bar pressure platforms by 2034 as Euro 7 compliance drives specification upgrades. The aftermarket segment will gain relative share as the large global diesel vehicle installed base ages and replacement injection demand intensifies.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including CRDI system engineers, automotive OEM procurement managers, fleet maintenance specialists, emission compliance consultants, and institutional investors across Europe, Asia-Pacific, and North America.

Secondary Research

Secondary research encompassed supplier annual reports, SAE and JSAE technical papers, Euro 7 regulatory documentation, OICA global vehicle production statistics, ACEA diesel market data, Indian SIAM commercial vehicle reports, and trade publications including Diesel Progress and Automotive Engineering International.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting, incorporating global diesel vehicle production volumes, CRDI system penetration rates by vehicle type, average system selling price trajectories, and aftermarket replacement cycle data. A base-case CAGR of 2.92% reflects consensus validated against OEM procurement commitments and emission standard implementation schedules.

Diesel Common Rail Injection System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles |

| Fuel Injector Types Covered | Solenoid Injector, Piezoelectric Injector |

| Engines Covered | Old Diesel Engine, CRDI Engine |

| Sales Channels Covered | OEMs, Aftermarket |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Robert Bosch GmbH, DENSO Corporation, Cummins Inc., Hyundai Motor Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the diesel common rail injection system market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global diesel common rail injection system market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the diesel common rail injection system industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Diesel Common Rail Injection System Market Report

The market reached USD 3.84 Billion in 2025 and is projected to grow to USD 5.04 Billion by 2034 at a 2.92% CAGR.

Asia-Pacific leads with a 39.8% share in 2025, driven by China and India commercial vehicle production and emission standard upgrades.

Passenger cars lead with a 57.6% share in 2025, driven by widespread diesel CRDI adoption in European and Asian vehicles.

Robert Bosch GmbH, DENSO Corporation, Cummins Inc., and Hyundai Motor Company, are some of the key players.

Solenoid injectors account for 63.4% of the fuel injector type segment, with piezoelectric injectors at 36.6% in 2025.

Euro 7 and China-VI emission compliance, commercial vehicle production growth, fuel efficiency demand, and CRDI retrofit activities are key drivers.

EV adoption pressure, diesel phaseout policies, high system complexity, and rare earth material supply concentration are key challenges.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)