Distributed Antenna System Market Size, Share, Trends and Forecast by Offering, System Type, Coverage, Technology, End Use, and Region, 2026-2034

Global Distributed Antenna Systems Market Size, Share, Trends & Forecast (2026-2034)

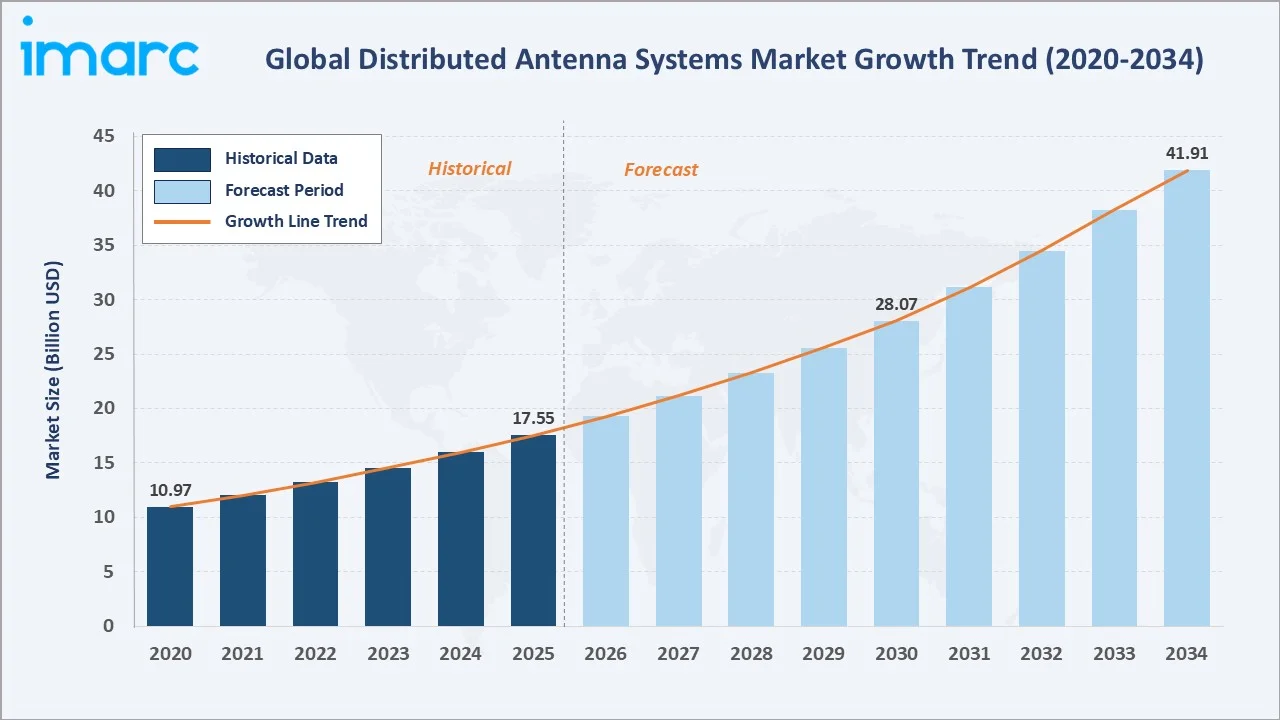

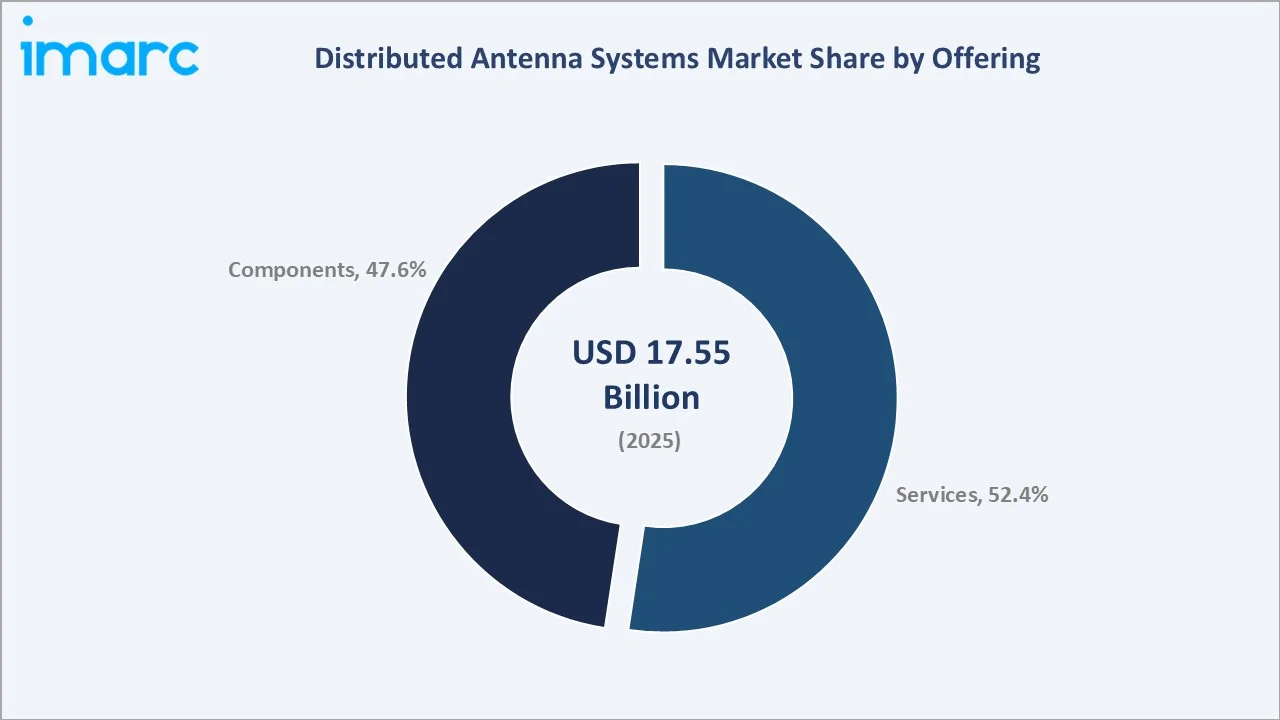

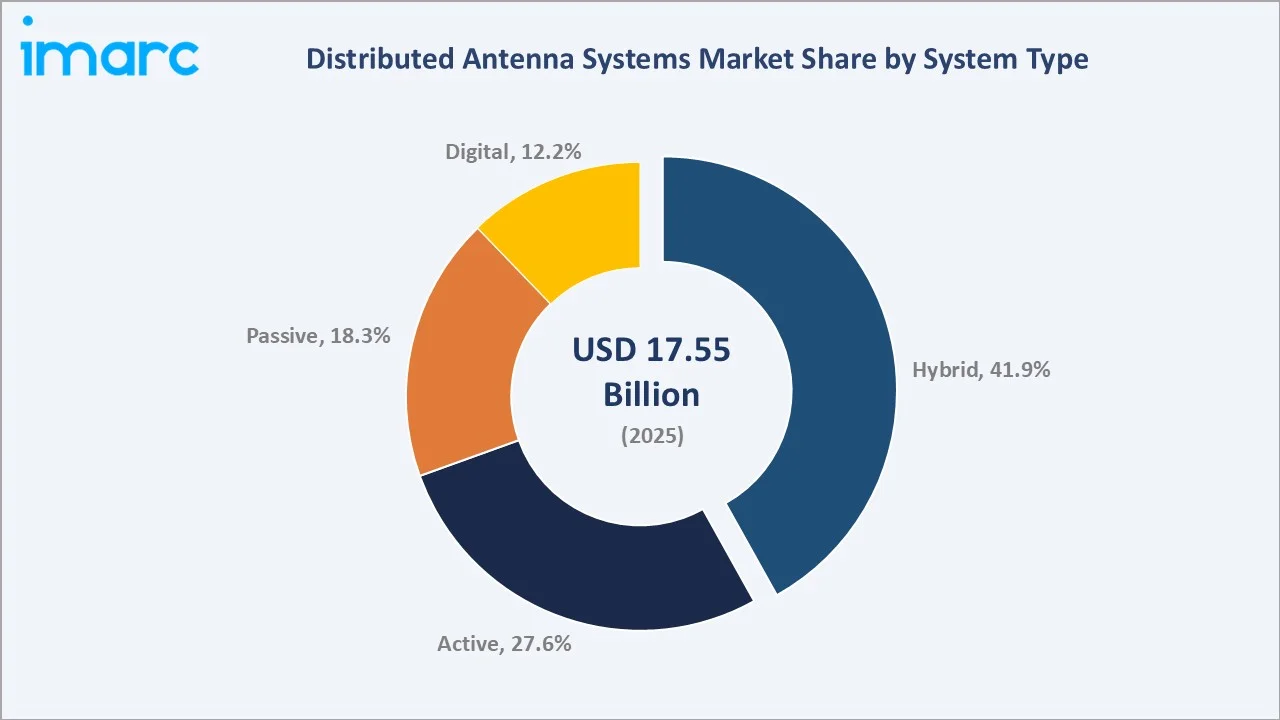

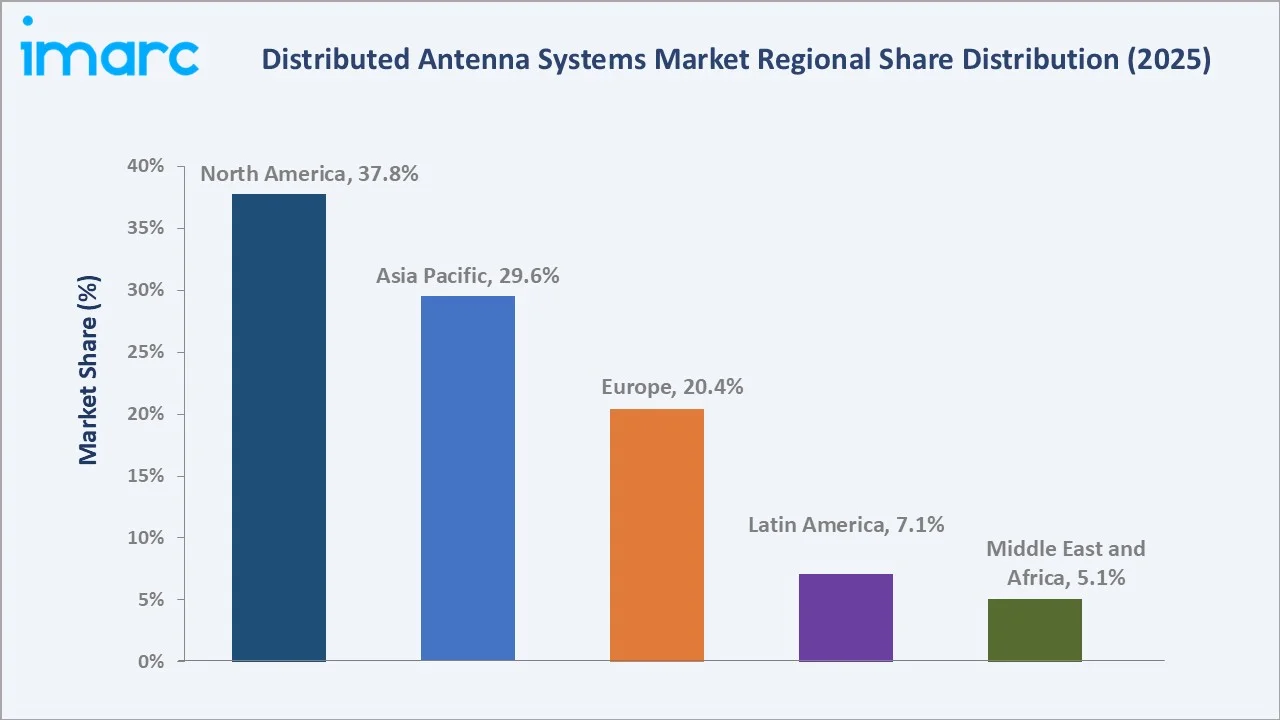

The global distributed antenna systems market size was valued at USD 17.55 Billion in 2025 and is projected to reach USD 41.91 Billion by 2034, exhibiting a CAGR of 9.85% during 2026-2034. Rapid 5G network densification, surging demand for seamless indoor wireless coverage across enterprises, healthcare facilities, and public venues, rising IoT device adoption, and mandatory public-safety in-building communication regulations are collectively driving the distributed antenna systems market growth. Services lead the offering segment at 52.4% in 2025, while Hybrid systems dominate the system-type segment at 41.9%. North America holds the largest regional share at 37.8% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 17.55 Billion |

|

Forecast Market Size (2034) |

USD 41.91 Billion |

|

CAGR (2026-2034) |

9.85% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (37.8% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~11.2%) |

|

Leading Offering |

Services (52.4% share, 2025) |

|

Leading System Type |

Hybrid (41.9% share, 2025) |

The chart below illustrates the global distributed antenna systems market size from 2020 through 2025. The market expanded from USD 10.97 Billion in 2020 to USD 17.55 Billion in 2025, representing a consistent historical CAGR of 9.85%, driven by enterprise connectivity upgrades, early 5G indoor infrastructure deployments, and growing public-safety broadband mandates.

To get more information on this market, Request Sample

The forecast chart captures accelerating market growth from USD 19.28 Billion in 2026 to USD 28.07 Billion in 2030 and USD 41.91 Billion by 2034, driven by 5G neutral-host expansion, private 5G enterprise adoption, and regulatory mandates for in-building emergency-responder coverage across North America, Europe, and the Asia Pacific.

Executive Summary

The global distributed antenna systems market is undergoing a structural transformation as telecommunications operators, enterprise IT teams, and public-safety agencies converge on shared indoor wireless infrastructure. Valued at USD 17.55 Billion in 2025, the market is forecast to reach USD 41.91 Billion by 2034 at a CAGR of 9.85%.

Services commands the dominant offering share at 52.4% in 2025, reflecting the shift from one-time hardware procurement toward long-term managed-service contracts that deliver recurring revenue streams for DAS vendors. Hybrid DAS leads system types at 41.9%, valued for simultaneously supporting multiple carrier frequencies, technologies, and spectrum bands on a single neutral-host platform - ideal for airports, stadiums, hospitals, and corporate campuses.

North America holds a 37.8% share in 2025, anchored by the US FirstNet public-safety broadband mandate and large-venue 5G upgrade programmes. Asia Pacific at 29.6% is the fastest-growing region, propelled by China's deployment of over 3.38 million 5G base stations by end-2024, India's PM Gati Shakti telecom programme, and South Korea's smart-city investments.

Key Market Insights

|

Insight |

Data |

|

Largest Offering Segment |

Services - 52.4% share (2025) |

|

Leading System Type |

Hybrid - 41.9% share (2025) |

|

Leading Region |

North America - 37.8% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~11.2%) |

|

Market Size (2030) |

USD 28.07 Billion |

|

Market Opportunity |

Private 5G + CBRS neutral-host convergence through 2034 |

|

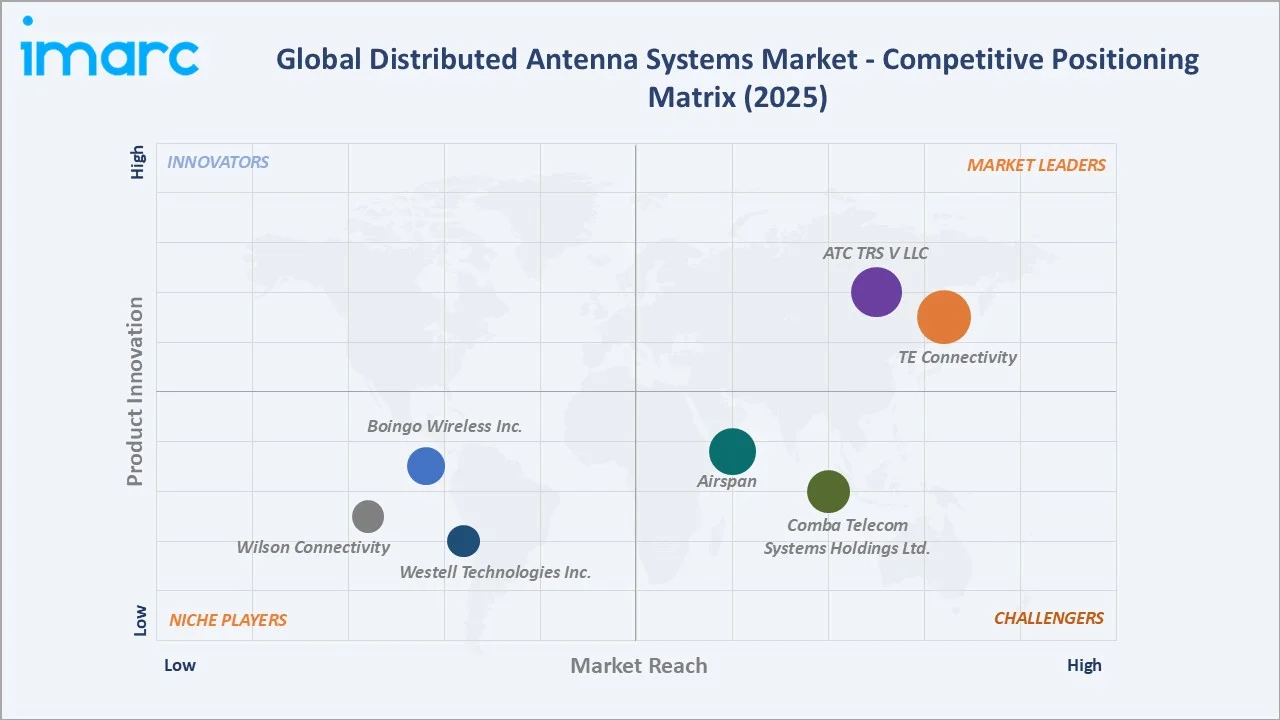

Top Companies |

Airspan, ATC TRS V LLC, TE Connectivity, Comba Telecom Systems Holdings Ltd. |

Key Analytical Observations Supporting the Above Data:

- Services Dominance (52.4%): The managed-service model - covering design, deployment, monitoring, and multi-year maintenance - accounts for the majority of DAS revenue in 2025. Building owners prefer predictable opex contracts over large upfront capex, driving long-term managed-service adoption across commercial real estate, hospitality, and healthcare verticals.

- Hybrid System Leadership (41.9%): Hybrid DAS is the preferred neutral-host architecture, supporting 4G LTE, 5G sub-6GHz, Wi-Fi 6, and public-safety Band 14 simultaneously on a single shared infrastructure - reducing per-operator costs and making DAS economically viable in a wider range of building typologies.

- North America Dominance (37.8%): The US market's layered demand drivers - FirstNet ERRCS mandates, sports-venue 5G upgrades, and high enterprise BYOD device density - create structural non-discretionary DAS investment independent of individual carrier capital cycles.

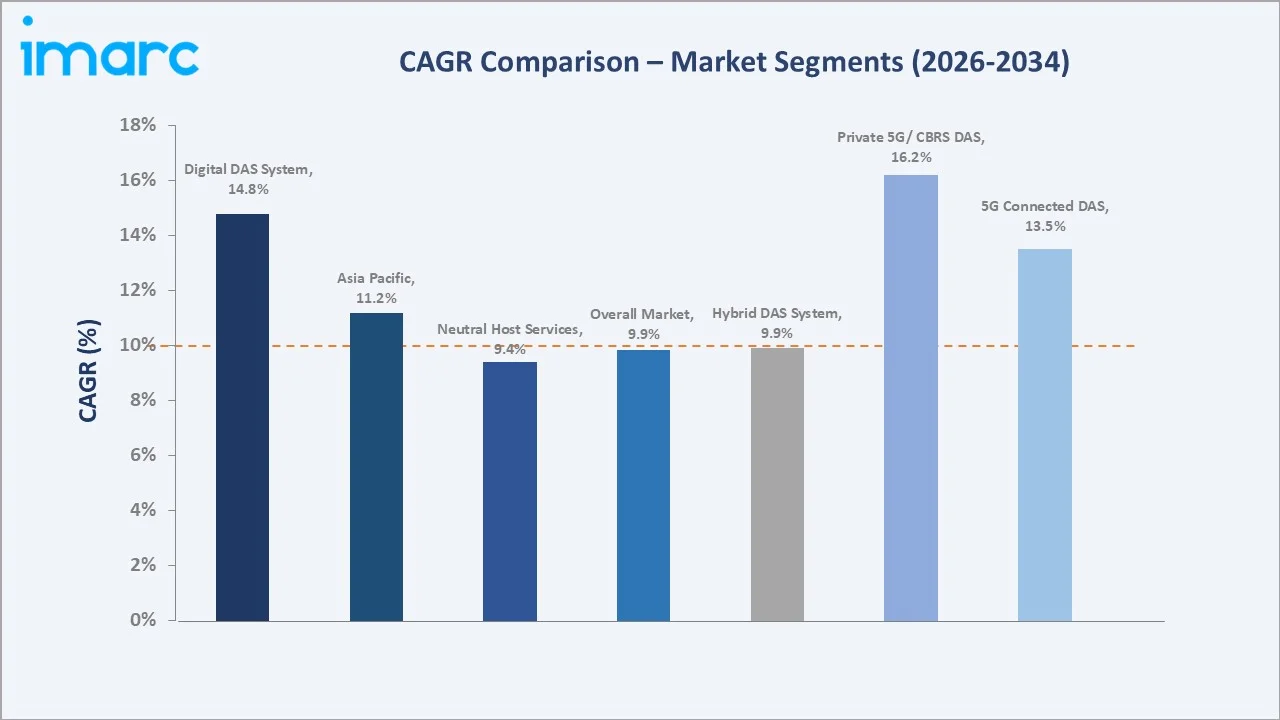

- Asia Pacific High Growth (~11.2% CAGR): China's 5G base station leadership, India's mandatory in-building coverage requirements post-5G spectrum auctions, and South Korea's smart-city programmes collectively position Asia Pacific as the world's fastest-growing Distributed Antenna Systems Market through 2034.

- 2030 Milestone (USD 28.07 Billion): The market is on track to nearly double from 2025 levels by 2030, driven by private 5G enterprise deployments, neutral-host portfolio consolidation by infrastructure fund-backed operators, and the global rollout of in-building 5G NR FR1 and mmWave infrastructure.

Global Distributed Antenna Systems Market Overview

Distributed Antenna Systems are wireless infrastructure architectures that distribute cellular, Wi-Fi, and public-safety radio signals across a large physical space through a network of spatially separated antenna nodes connected to one or more central signal sources - the head-end or base station hotel. By placing antenna nodes close to users, DAS eliminates coverage gaps, interference zones, and capacity bottlenecks that characterise single-antenna macro-cell designs in high-density indoor environments.

Applications span commercial real estate, healthcare, transportation hubs, sports venues, government facilities, and industrial campuses - each with distinct RF engineering, regulatory compliance, and business-model requirements. Global mobile data traffic is projected to reach 607 exabytes per month by 2029, per the Ericsson Mobility Report 2024, and the convergence of private 5G networks with enterprise DAS infrastructure is the most significant structural driver emerging for 2026-2034.

Market Dynamics

To evaluate market opportunities, Request Sample

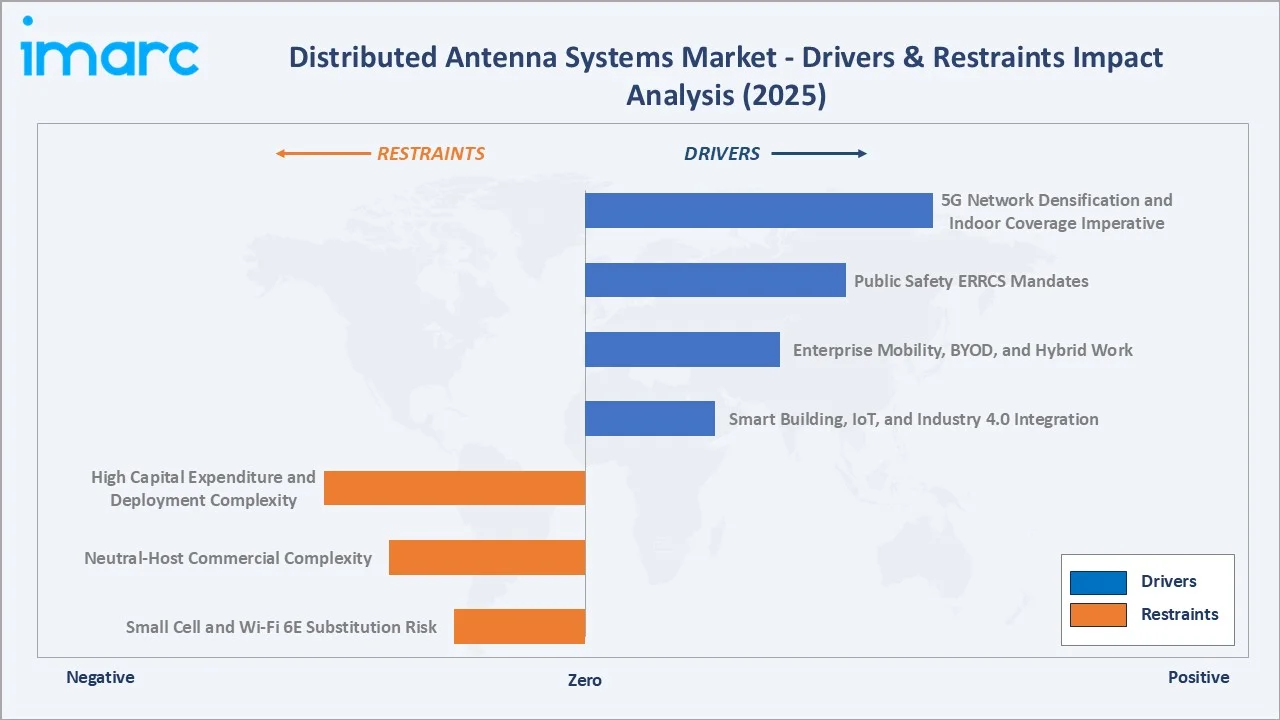

Market Drivers

- 5G Network Densification and Indoor Coverage Imperative: 5G mmWave frequencies at 28 GHz and 39 GHz deliver ultra-high bandwidth but suffer severe building penetration losses, making in-building DAS non-optional for carriers deploying 5G in dense urban markets. Approximately 80% of mobile data traffic originates indoors, requiring a dedicated DAS infrastructure that outdoor macro-cells cannot adequately serve.

- Public Safety ERRCS Mandates: NFPA 72, IFC, and local building codes across all US jurisdictions mandate in-building radio coverage for emergency responders in commercial buildings above defined size thresholds.

- Enterprise Mobility, BYOD, and Hybrid Work: Corporate mobility programmes and the structural shift to hybrid work have made indoor wireless quality a measurable productivity metric. Enterprises now specify minimum indoor wireless KPIs in real-estate procurement, driving DAS adoption across commercial office, hospitality, and healthcare verticals globally.

- Smart Building, IoT, and Industry 4.0 Integration: Building automation, IoT sensor networks, and industrial wireless communication requirements under Industry 4.0 frameworks are expanding DAS addressable market scope beyond cellular coverage to comprehensive in-building wireless platforms supporting sub-GHz IoT, Wi-Fi 6E, and private 5G simultaneously.

Market Restraints

- High Capital Expenditure and Deployment Complexity: Large-scale DAS deployments require upfront investment for major venues, plus multi-month installation timelines that disrupt building operations, creating procurement decision delays, particularly in cost-sensitive verticals.

- Neutral-Host Commercial Complexity: Negotiating revenue-sharing agreements with multiple MNOs simultaneously introduces contractual complexity that can extend DAS project sales cycles by 6-18 months, delaying deployment and revenue recognition for neutral-host operators.

- Small Cell and Wi-Fi 6E Substitution Risk: In lower-density applications and cost-sensitive verticals, small cells and Wi-Fi 6E can provide technically adequate and economically superior alternatives to full DAS, creating competitive displacement risk in certain building typologies and geographies.

Market Opportunities

- Private 5G and CBRS Spectrum Integration: The CBRS 3.5 GHz shared-spectrum framework in the US - and equivalent frameworks in Europe, Japan, and India - enables enterprises to deploy private 5G without carrier agreements. DAS infrastructure serves as the optimal physical antenna layer, opening a multi-billion-dollar enterprise wireless platform market beyond traditional carrier coverage applications.

- Smart Stadium and Large Venue 5G Upgrade Cycle: Professional sports leagues globally are investing in 5G-enabled fan engagement - AR replays, instant video, location services - requiring dense DAS infrastructure that existing Wi-Fi cannot support, representing a concentrated high-value project pipeline extending through 2030.

- Emerging Market Greenfield Opportunity: India's Bharat Net programme, South-East Asian smart-city initiatives, and GCC mega-project connectivity requirements represent substantial greenfield DAS deployment opportunities in geographies with limited legacy indoor wireless infrastructure.

Market Challenges

- Multi-Band Technology Fragmentation: Supporting concurrent 4G, 5G sub-6GHz, 5G mmWave, Wi-Fi 6E, CBRS, and FirstNet/Band 14 on a single DAS platform requires complex multi-band RF engineering, increasing per-project design costs and limiting scalability of standardised product architectures globally.

- Spectrum Regulatory Divergence: Varying spectrum allocations, building code requirements, and ERRCS standards across international markets increase engineering complexity and prevent fully standardised global DAS product families, elevating localisation costs for international deployment programmes.

Emerging Market Trends

1. Neutral-Host DAS as the Dominant Business Model

The market is shifting from operator-owned DAS toward neutral-host architectures, where a single system serves multiple carriers and tenants. Players like ATC, TRS, and VLL are expanding portfolios, improving asset utilization, and lowering cost-per-tenant. Adoption is strongest in large venues, with gradual expansion into mid-size buildings.

2. Open RAN Integration and Virtualised DAS Architectures

Open RAN principles are influencing DAS evolution toward virtualised, software-defined systems. Centralised baseband processing with distributed radios enables remote upgrades, multi-band support, and faster reconfiguration—reducing reliance on hardware-led upgrade cycles.

3. CBRS Spectrum and Private 5G Convergence

Frameworks like CBRS are enabling enterprise private 5G deployments. DAS is increasingly positioned as an indoor distribution layer in large or complex environments, though alternatives (e.g., small cells) remain relevant depending on use case and scale.

4. AI-Powered Network Management and Predictive Maintenance

The shift to cloud-managed DAS enables centralized monitoring and remote optimization. AI-driven automation is emerging, but its impact is currently incremental and deployment-specific, not uniformly quantified.

5. Multi-Technology Convergence on Unified DAS Platforms

Next-gen DAS increasingly supports cellular, Wi-Fi, public safety, and private 5G on shared infrastructure. While full convergence varies by deployment, the trend reduces duplication and positions DAS as a core in-building wireless layer rather than a carrier-specific add-on.

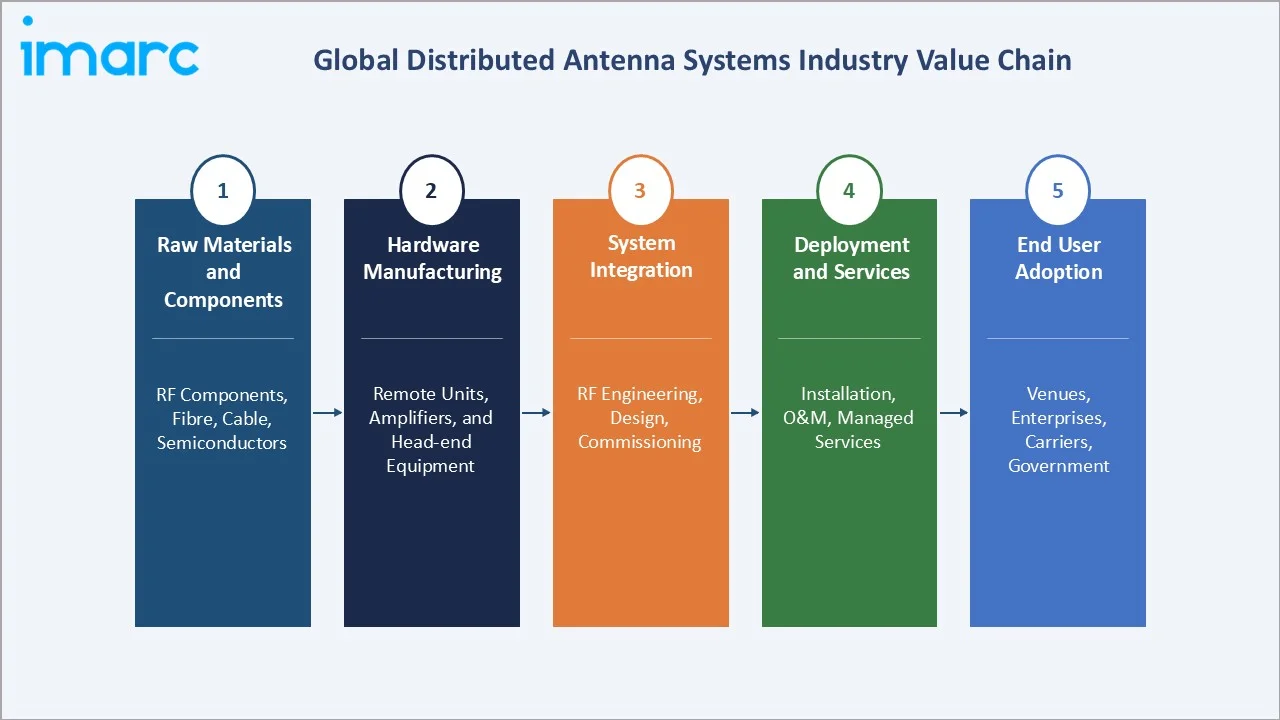

Industry Value Chain Analysis

|

Stage |

Activity |

|

Raw Materials and Components |

RF components, fibre, cable, semiconductors |

|

Hardware Manufacturing |

Remote units, amplifiers, and head-end equipment |

|

System Integration |

RF engineering, design, commissioning |

|

Deployment and Services |

Installation, O&M, managed services |

|

End User Adoption |

Venues, enterprises, carriers, government |

The distributed antenna systems value chain spans five integrated stages from raw materials and components through end-user adoption. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements. Tier-1 DAS hardware vendors and neutral-host operators occupy the highest strategic value positions, though mobile operators are increasingly exploring direct DAS ownership to capture infrastructure and service revenue simultaneously.

Technology Landscape in the Distributed Antenna Systems Industry

Active, Passive, and Digital DAS Architectures

Active DAS uses fibre-optic or Ethernet cabling between a central head-end and digitised remote antenna units (RAUs), offering superior signal quality and remote manageability for large complex deployments. Passive DAS uses coaxial cable with no active components beyond the head-end, suited for smaller cost-sensitive buildings. Digital DAS converts RF signals to digital data streams, enabling software-defined reconfigurability and precise power management - gaining traction in healthcare and government applications requiring strict interference isolation.

5G New Radio (NR) and mmWave Integration

5G NR support across sub-6GHz (FR1: 600 MHz to 7.125 GHz) and mmWave (FR2: 24.25 to 52.6 GHz) requires DAS hardware capable of handling both frequency ranges simultaneously. CommScope and Ericsson launched active DAS remote units with native 5G NR FR1 support in 2024-2025, with mmWave-capable indoor small-cell/DAS hybrid solutions entering deployment in major US venues and high-density commercial buildings.

Cloud Management and Open RAN Platforms

Cloud-native DAS management platforms enable remote configuration, real-time performance analytics, and OTA software updates across geographically dispersed deployments.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Offering | Services | 52.4% | 2025 |

| System Type | Hybrid | 41.9% | 2025 |

| Coverage | Indoor | 🔒 | 2025 |

| Technology | Self-Organizing Network | 🔒 | 2025 |

| End-Use | Public Venues | 🔒 | 2025 |

| Region | North America | 37.8% | 2025 |

By Offering

Services commands a 52.4% share in 2025, reflecting the fundamental shift from hardware-centric procurement to comprehensive managed-service contracts. Building owners now prefer predictable monthly opex over large upfront capital outlays. AI-powered remote monitoring platforms have enabled DAS vendors to scale managed-service portfolios across large geographically dispersed real-estate portfolios without proportional field technician headcount increases, improving service margins while enhancing system uptime metrics.

To access detailed market analysis, Request Sample

The Components segment at 47.6% in 2025 remains robust, driven by the global 5G infrastructure build-out requiring new antenna elements supporting 5G sub-6GHz and mmWave frequencies. Active DAS remote units incorporating software-defined radio capabilities - enabling remote reconfiguration without physical hardware replacement - are the fastest-growing component sub-category, with unit shipments growing at approximately 15% annually through 2025.

By System Type

Hybrid DAS leads at 41.9% in 2025, combining active and passive elements to optimise coverage, capacity, and cost across mixed-density building environments. The neutral-host model strongly favours Hybrid for its ability to serve multiple MNO tenants simultaneously. Hybrid DAS also offers the most cost-efficient 4G-to-5G migration path - preserving existing passive coaxial distribution infrastructure while adding 5G-capable active remote units at the antenna node level.

Digital DAS at 12.2% is the fastest-growing system type at approximately 14.8% CAGR through 2034. Active DAS at 27.6% dominates the high-capacity venue category, while Passive systems at 18.3% retain relevance in cost-sensitive installations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

37.8% |

5G rollout, FirstNet ERRCS mandates, large-venue upgrades, enterprise BYOD |

|

Asia Pacific |

29.6% |

China's 5G infrastructure, India's Bharat Net, South Korea's smart cities, and ASEAN growth |

|

Europe |

20.4% |

EU Digital Decade targets, building code mandates, transport DAS, smart buildings |

|

Latin America |

7.1% |

Brazil and Mexico 5G spectrum auctions, hospitality, and mining sector growth |

|

Middle East and Africa |

5.1% |

Saudi Vision 2030, UAE Centennial 2071, GCC mega-project connectivity requirements |

North America commands a 37.8% global revenue share in 2025, anchored by the US market's unique structural demand combination. Canada's smart-city wireless infrastructure programmes and mining-sector private wireless deployments add further regional depth.

Asia Pacific at 29.6% is the fastest-growing region. India's Distributed Antenna Systems Market is accelerating under 5G spectrum auction completions and mandatory in-building coverage requirements for new commercial construction. Europe, at 20.4%, is driven by EU Digital Decade mandates, transportation DAS requirements in metro rail networks, and smart-building energy efficiency regulations. Latin America at 7.1% and the Middle East and Africa at 5.1% represent emerging-market opportunities driven by infrastructure investment programmes, GCC mega-projects, and large-scale hospitality and venue development through 2030.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Airspan |

MobileAccess DAS |

Challenger |

Digital DAS, fibre optics |

|

ATC TRS V LLC |

Distributed Antenna System (DAS) |

Leader |

Neutral-host ownership and managed services |

|

TE Connectivity |

DAS Antennas - Ceiling Mount and Wall Mount Solutions |

Leader |

Components, RF connectivity, structured cabling |

|

Comba Telecom Systems Holdings Ltd. |

ComFlex DAS |

Challenger |

APAC DAS, 5G small cells, enterprise indoor |

|

Boingo Wireless Inc. |

5G DAS network |

Emerging |

Aviation, hospitality, neutral-host model |

|

Westell Technologies Inc. |

UltraWide Band DAS |

Emerging |

ERRCS compliance, passive DAS, in-building |

|

Wilson Connectivity |

Zinwave Active DAS Solutions |

Emerging |

Wideband active DAS, enterprise coverage |

The distributed antenna systems competitive landscape is characterised by a small number of global specialised vendors commanding substantial carrier and enterprise relationships, alongside neutral-host operators and emerging cloud-native DAS start-ups challenging the established hardware-centric hierarchy.

Key Company Profiles

Airspan

Airspan Networks is a global provider of 4G/5G radio access network (RAN) solutions with a growing presence in indoor wireless and distributed network architectures, including small cells and DAS-adjacent deployments for enterprise and private networks.

- Product and Platform Portfolio: 5G Open RAN solutions, indoor small cells, private 5G network platforms, cloud-native RAN software, and distributed radio units supporting enterprise, venue, and industrial connectivity use cases.

- Recent Developments: In February 2025, Airspan announced the expansion of its proven In-Motion 5G solution beyond commercial air-to-ground deployments into defense-grade 5G MANET, High-Altitude Pseudo-Satellite (HAPS) systems, and uncrewed aerial platforms.

- Strategic Focus: Airspan is positioning itself at the intersection of Open RAN, private 5G, and indoor coverage, targeting enterprise and mid-market segments. Rather than competing purely as a traditional DAS vendor, it is leveraging software-centric architectures and small cell–DAS hybrid models to address cost and deployment flexibility, aligning with the shift toward cloud-managed, programmable indoor wireless infrastructure through 2030.

ATC TRS V LLC

ATC TRS V LLC (American Tower) is a neutral-host DAS operator through its InSite DAS division, owning and operating in-building wireless infrastructure in airports, stadiums, healthcare facilities, and commercial real estate portfolios across North America and internationally.

- Product and Platform Portfolio: InSite DAS neutral-host platform, managed indoor wireless services, multi-carrier DAS infrastructure leasing across airports, stadiums, hospitals, and office towers.

- Recent Developments: In April 2026, American Tower completed a 5G Distributed Antenna System (DAS) deployment at Pittsburgh International Airport (PIT), delivering high-performance wireless connectivity across the new terminal and existing airport facilities.

- Strategic Focus: American Tower applies the macro-tower neutral-host model to indoor environments - owning critical infrastructure and leasing access to multiple tenants - while expanding into data-centre campus and logistics warehouse wireless infrastructure as growth adjacencies through 2030.

TE Connectivity

TE Connectivity is a key component and infrastructure supplier in the Distributed Antenna Systems (DAS) ecosystem, providing connectivity, passive RF, and fiber solutions that enable reliable in-building wireless networks across commercial, industrial, and telecom environments globally.

- Product and Platform Portfolio: RF connectors and coaxial cable assemblies, fiber optic connectivity solutions, antennas, passive components, and high-performance interconnect systems supporting DAS, small cells, and 5G indoor deployments.

- Recent Developments: In June 2024, TE Connectivity showcased its cutting-edge Internet of Things (IoT) technology at the 2024 CommunicAsia in Singapore.

- Strategic Focus: The company is positioned as an enabling technology provider rather than a DAS system operator, focusing on high-reliability components that support digital and hybrid DAS architectures. Its strategy emphasizes miniaturization, high-frequency performance (sub-6 GHz and mmWave), and fiber integration, aligning with the shift toward software-defined and high-capacity indoor networks.

Market Concentration Analysis

The global distributed antenna systems market exhibits moderate concentration, with Airspan, ATC TRS V LLC, TE Connectivity, and Comba Telecom Systems Holdings Ltd. collectively accounting for approximately 50-58% of global market revenue in 2025.

The market is structurally bifurcated. At the large-venue and carrier tier, consolidation is gradually increasing as 5G multi-band DAS deployments require high engineering complexity and sustained R&D, favoring large vendors and limiting mid-size participation in flagship projects. However, consolidation remains early-stage and market-dependent, unlike the rapid tower consolidation cycle of the 2000s. Conversely, the enterprise and mid-market segment remains highly fragmented, driven by regional system integrators and project-based deployments. Emerging vendors like Westell Technologies Inc. and Wilson Connectivity are gaining traction with software-defined architectures, improving cost and deployment flexibility. While disruptive potential exists, impact is likely to be gradual and segment-specific rather than broad-based in the near term.

Investment and Growth Opportunities

Fastest-Growing Segments

Digital DAS is the fastest-growing system type (~mid-teens CAGR), driven by healthcare, government, and smart buildings adopting software-defined platforms.

Private 5G–integrated DAS is the fastest-growing application, with large enterprise deployments increasingly requiring reliable indoor coverage layers, often via DAS or hybrid architectures.

Emerging Market Expansion

India is a high-growth market, supported by 5G rollout, in-building coverage requirements, and expanding commercial real estate, driving greenfield DAS demand across Tier-1 and Tier-2 cities.

In the GCC, mega-projects like NEOM, Red Sea Project, and Qiddiya are creating large, centralized deployment pipelines for advanced in-building wireless.

Venture and Private Investment Trends

Investors such as Macquarie Infrastructure, Brookfield Asset Management, and DigitalBridge Group are acquiring neutral-host DAS assets for stable, long-term returns. Meanwhile, players like Dali Wireless and JMA Wireless are driving cloud-native DAS innovation, improving scalability and deployment efficiency.

Future Market Outlook (2026-2034)

The global distributed antenna systems market is projected to expand from USD 17.55 Billion in 2025 to USD 28.07 Billion in 2030 and USD 41.91 Billion by 2034 at a CAGR of 9.85%, representing a near-tripling of market value over the forecast period. Three structural forces underpin this trajectory: the global 5G indoor coverage build-out, convergence of cellular and enterprise wireless networks on shared neutral-host DAS platforms, and expanding regulatory mandates for in-building public-safety communications coverage.

The 2026–2030 period will be driven by indoor 5G expansion, private 5G enterprise adoption, and neutral-host DAS consolidation. Venues with 4G LTE DAS deployed in 2015–2020 are entering upgrade cycles, creating a concentrated replacement capex wave. At the same time, private 5G and shared spectrum models are adding new enterprise demand across manufacturing, logistics, and healthcare—expanding DAS beyond traditional carrier coverage and supporting growth toward ~USD 28 Billion by 2030.

The industry is shifting from RF-based systems to software-defined, cloud-managed DAS, enabling OTA upgrades and multi-tenant scalability. By 2034, DAS will function as a digital indoor connectivity platform, with vendors lacking software capabilities facing structural displacement.

Research Methodology

Primary Research

Primary research encompassed structured interviews with over 50 DAS industry stakeholders in 2024-2025, including product and strategy directors at DAS hardware vendors, mobile network operator indoor coverage teams, neutral-host DAS operators, building owners and facility managers, systems integrators, and institutional investors in telecommunications infrastructure. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning across key geographies.

Secondary Research

Secondary sources include Ericsson Mobility Report (2024), GSMA Intelligence Connected Buildings report, FCC Universal Licensing System deployment data, NFPA 72 National Fire Alarm and Signalling Code, IFC International Fire Code, S& P Global Market Intelligence telecommunications datasets, company annual reports and investor presentations, and trade publications including Inside Towers, Wireless Week, RCR Wireless News, and Fierce Wireless.

Forecasting Models

Market size estimations were derived using combined top-down and bottom-up forecasting models incorporating 5G network deployment schedules, commercial real estate development pipelines, regulatory mandate implementation timelines, and historical market evolution patterns.

Distributed Antenna System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Offerings Covered | Components, Services |

| System Types Covered | Active, Passive, Digital, Hybrid |

| Coverages Covered | Indoor, Outdoor |

| Technologies Covered | Carrier Wi-Fi, Small Cells, Self-Organizing Network, Others |

| End-Uses Covered | Manufacturing, Healthcare, Government, Transportation, Hospitality, Public Venues, Education, Telecommunication, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Airspan, ATC TRS V LLC, TE Connectivity, Comba Telecom Systems Holdings Ltd., Boingo Wireless Inc., Westell Technologies Inc., Wilson Connectivity, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the distributed antenna system market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global distributed antenna system market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the distributed antenna system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Distributed Antenna System Market Report

The global distributed antenna systems market was valued at USD 17.55 Billion in 2025, growing from USD 10.97 Billion in 2020, driven by 5G indoor coverage demand, enterprise wireless upgrades, and public-safety broadband mandates.

The market is projected to reach USD 28.07 Billion by 2030 and USD 41.91 Billion by 2034, growing at a CAGR of 9.85% during 2026-2034, driven by neutral-host expansion, private 5G integration, and ERRCS regulatory mandates.

North America leads with a 37.8% share in 2025, anchored by US FirstNet public-safety mandates, large-venue 5G upgrade programmes, and high enterprise BYOD device density driving structural non-discretionary DAS investment.

Digital DAS is the fastest-growing system type at approximately 14.8% CAGR through 2034, driven by healthcare and government adoption of software-defined cloud-managed platforms supporting multiple wireless technologies simultaneously.

Services leads with 52.4% share in 2025, reflecting the market shift from hardware-only procurement to comprehensive managed-service contracts covering design, installation, monitoring, and long-term maintenance.

Hybrid DAS leads at 41.9% in 2025, preferred for neutral-host deployments that must simultaneously support multiple carrier frequencies - including 4G LTE, 5G sub-6GHz, Wi-Fi 6, and public-safety Band 14.

The market grew from USD 10.97 Billion in 2020 to USD 17.55 Billion in 2025 at 9.85% CAGR, driven by enterprise connectivity upgrades, early 5G indoor infrastructure deployments, and expanding public-safety broadband mandates across North America.

Leading companies include Airspan, ATC TRS V LLC, TE Connectivity, Comba Telecom Systems Holdings Ltd., Boingo Wireless Inc., Westell Technologies Inc., and Wilson Connectivity.

A neutral-host DAS is owned by a third-party infrastructure operator that leases shared antenna infrastructure access to multiple mobile operators simultaneously, distributing deployment costs across tenants and improving overall economics.

Private 5G deployments using CBRS spectrum are creating new DAS demand in manufacturing, healthcare, and logistics, where enterprises leverage existing DAS as the physical antenna layer for dedicated enterprise 5G networks alongside public carrier services.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)