Electronic Security Market Size, Share, Trends and Forecast by Product Type, Service Type, End-Use Sector, and Region, 2026-2034

Global Electronic Security Market Size, Share, Trends & Forecast (2026-2034)

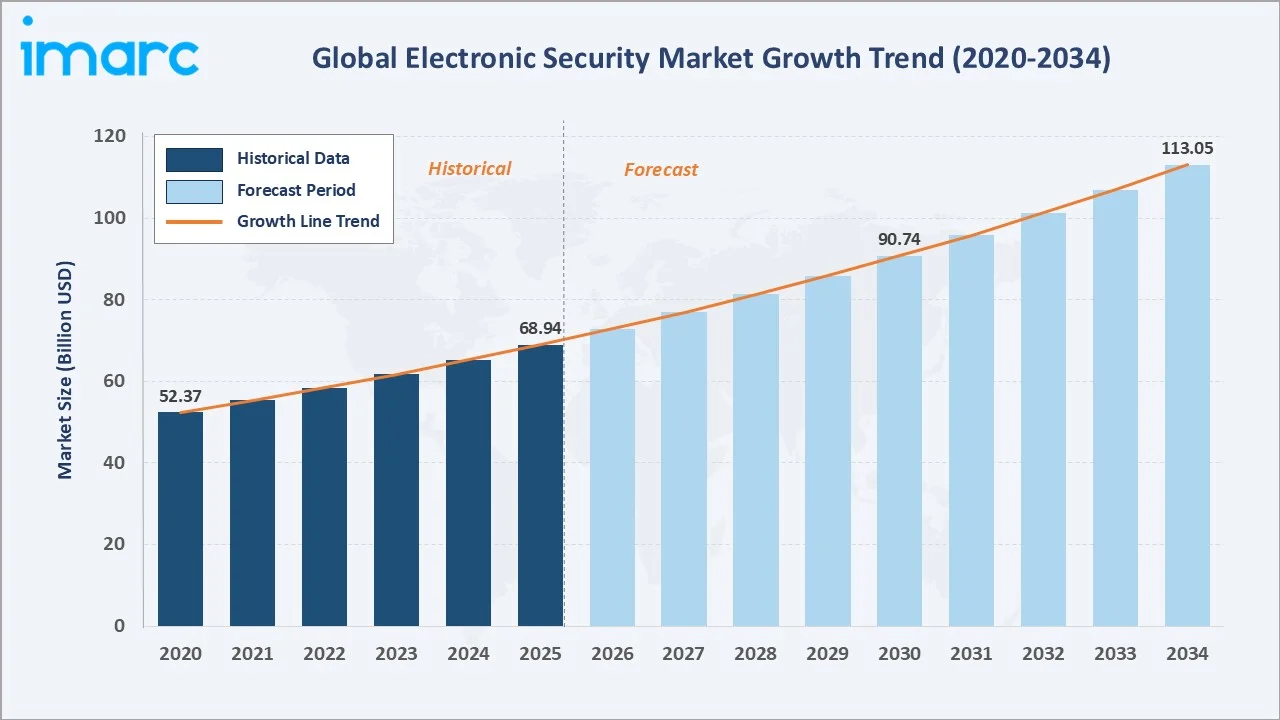

The global electronic security market size reached USD 68.94 Billion in 2025 and is projected to reach USD 113.05 Billion by 2034, exhibiting a CAGR of 5.65% during 2026-2034. Rising security threats, expanding IoT ecosystems, and growing regulatory compliance mandates are the primary forces driving electronic security market growth.

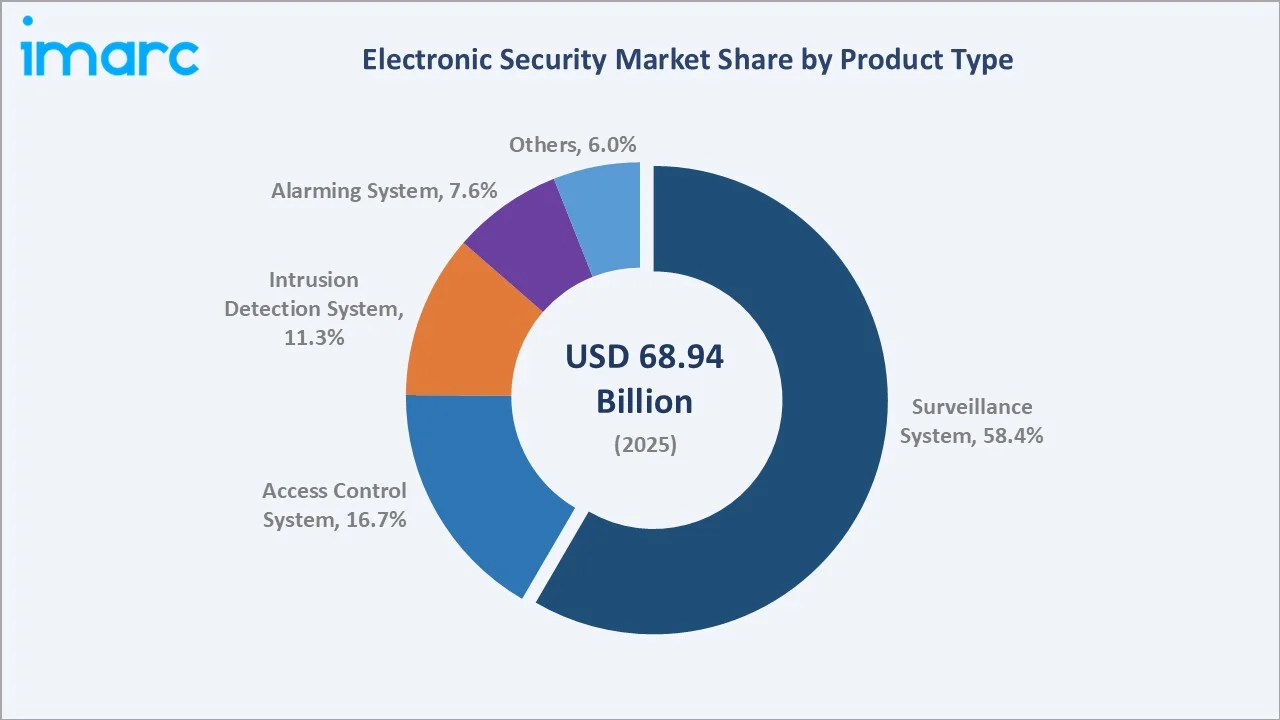

Surveillance systems dominate product type at 58.4% in 2025, while managed services lead the service segment at 43.5%. North America commands 29.5% of the global market in 2025, reflecting its mature security infrastructure and high awareness levels.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 68.94 Billion |

|

Forecast Market Size (2034) |

USD 113.05 Billion |

|

CAGR (2026-2034) |

5.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (29.5% share, 2025) |

| Second Largest Region |

Asia-Pacific (27.6% share, 2025) |

| Leading Product Type |

Surveillance System (58.4%, 2025) |

| Leading Sevice Tyoe |

Managed Services (43.5%, 2025) |

The global electronic security market growth trajectory from 2020 through 2034, with the historical expansion to USD 68.94 Billion in 2025, reflects consistent demand for advanced security solutions, while the forecast to USD 113.05 Billion captures accelerating adoption of AI-powered analytics, cloud integration, and smart city investment programmes.

To get more information on this market, Request Sample

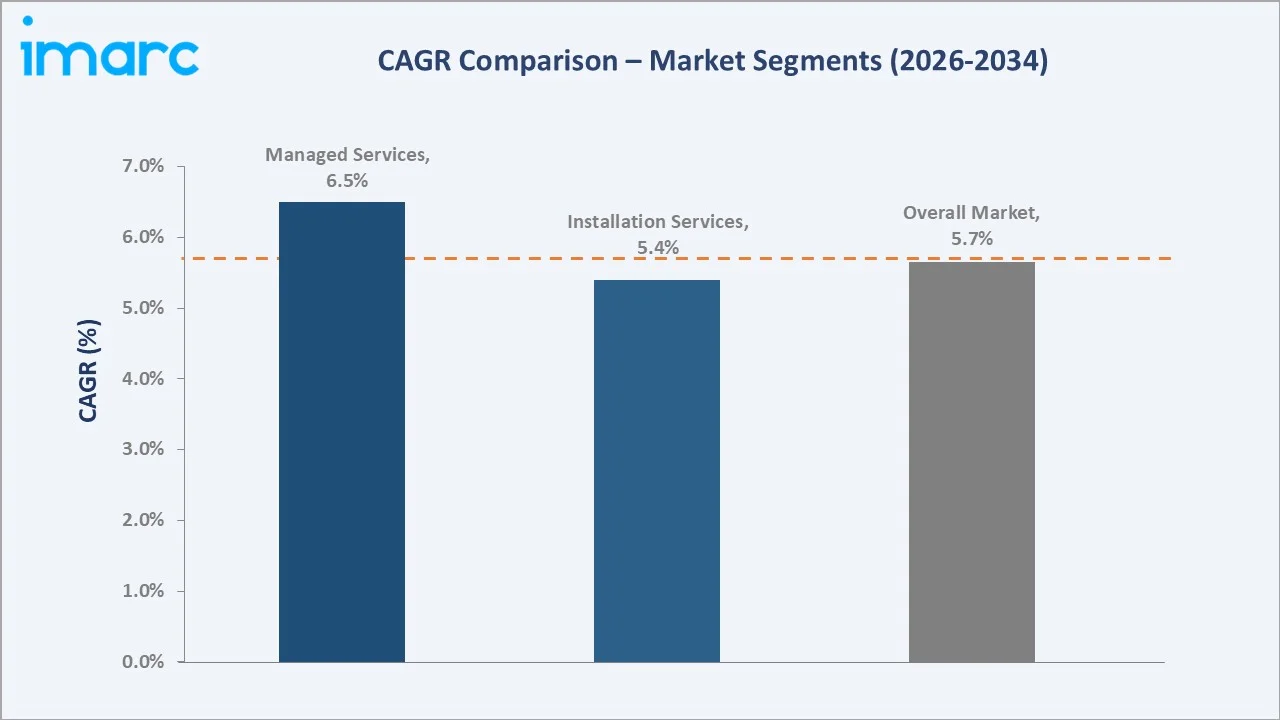

The CAGR trajectories across key product, service, and regional sub-segments, with managed services at ~6.5% CAGR and surveillance systems at ~6.2% CAGR, are the fastest-growing categories within the global electronic security industry analysis through 2034.

Executive Summary

The global electronic security market is on a sustained growth trajectory from USD 68.94 Billion in 2025 to USD 113.05 Billion by 2034. Electronic security systems, including surveillance, access control, intrusion detection, and alarm solutions, provide critical protection for commercial, residential, government, and industrial environments.

Surveillance systems dominate product type at 58.4% in 2025, owing to widespread CCTV adoption across retail, transportation, banking, and government sectors. Access control systems (16.7%) command premium pricing in corporate and critical infrastructure applications, leveraging biometrics and smart card technologies. Intrusion detection systems (11.3%) serve residential and commercial markets with growing integration into smart home ecosystems.

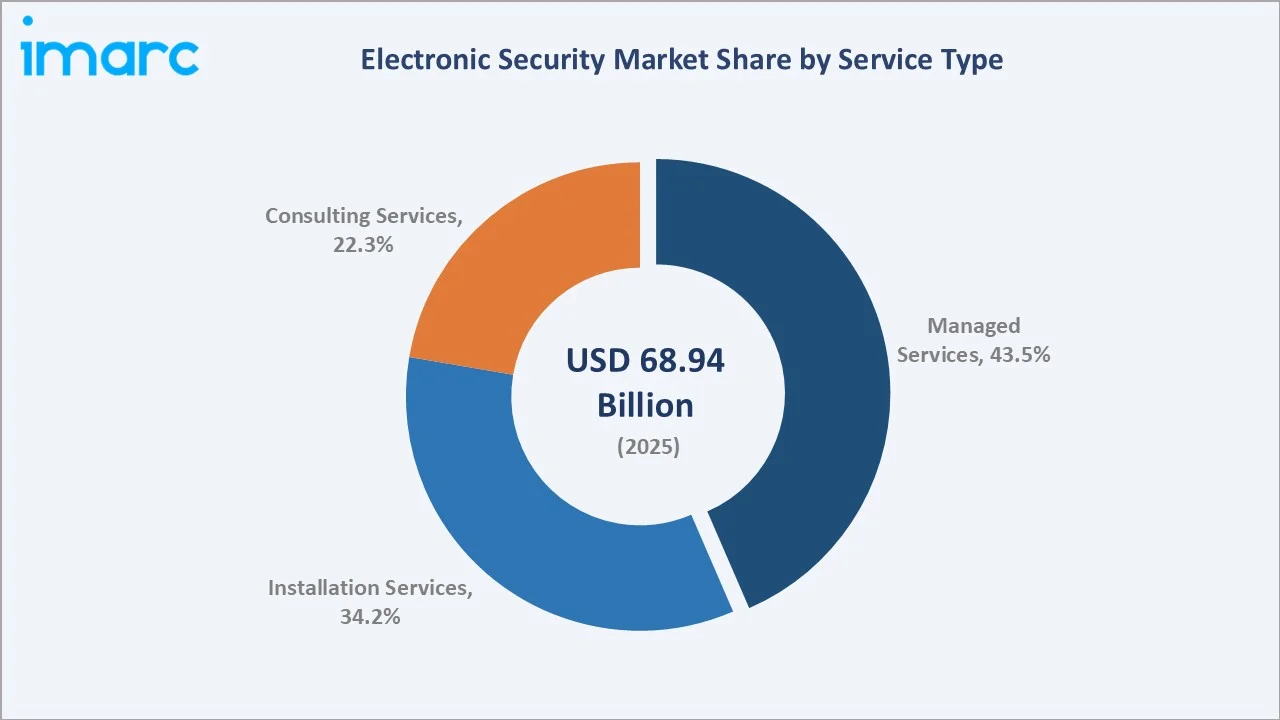

Managed services lead the service segment at 43.5% in 2025, reflecting enterprise preference for outsourced monitoring, maintenance, and proactive support. Installation services (34.2%) capture significant revenue from new infrastructure deployments.

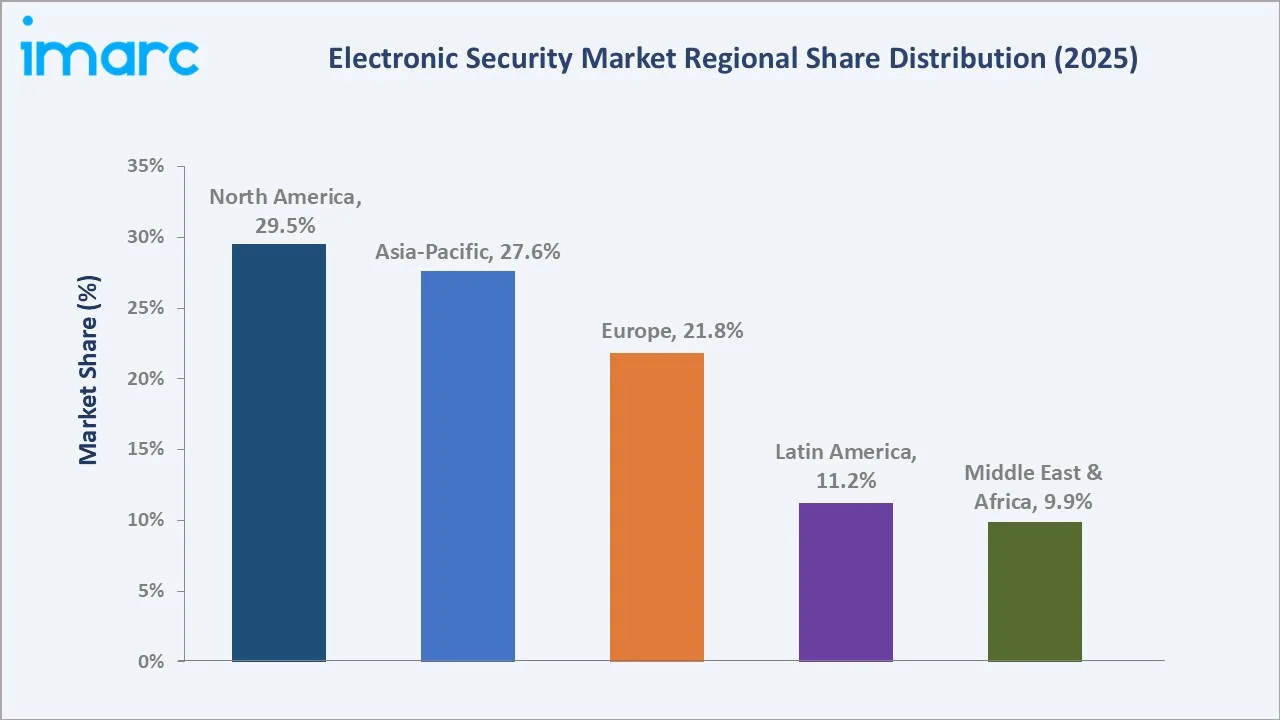

North America (29.5%) and Asia-Pacific (27.6%), driven by cybersecurity investments, smart city initiatives, and rising safety awareness.

Key Market Insights

|

Insight |

Data |

| Largest Product Type |

Surveillance System – 58.4% share (2025) |

| Leading Service Type |

Managed Services – 43.5% share (2025) |

| Leading Region |

North America - 29.5% (2025) |

| Second Largest Region |

Asia-Pacific - 27.6% (2025) |

|

Top Companies |

Honeywell International Inc., Securitas Technology, Siemens, Vivint LLC, OSI Systems, Inc. |

Key Analytical Observations Supporting the Above Data:

- Surveillance systems, with 58.4% in 2025, dominate because of their universal applicability across public safety, retail loss prevention, transportation monitoring, and enterprise security. IP-based cameras and AI-powered video analytics have transformed surveillance from passive recording to proactive threat intelligence.

- Managed services, with 43.5% in 2025, lead because enterprises increasingly prefer outsourced security operations that provide 24/7 monitoring, predictive maintenance, and rapid incident response without the burden of maintaining in-house security operations centers (SOCs).

- North America's 29.5% dominance in 2025 reflects robust public and private sector security spending. The US government's critical infrastructure protection mandates, financial sector compliance requirements, and enterprise risk management programs generate consistent procurement of advanced electronic security solutions.

- Asia-Pacific, with 27.6% in 2025, benefits from rapid urbanization, smart city investments across China, India, and Southeast Asia, and growing awareness of workplace and residential security. China's national surveillance programs alone have deployed hundreds of millions of IP cameras across public infrastructure.

Global Electronic Security Market Overview

Electronic security is a comprehensive system that employs embedded technology and electronic devices to enhance safety measures and protect human life and physical assets. Core functions include surveillance, access control, intrusion detection, and alarm management, deployed across commercial, residential, government, industrial, and transportation environments.

The global ecosystem integrates component manufacturers (cameras, sensors, controllers), system integrators, software developers, installation service providers, managed service operators, and diverse end-use industries spanning government, banking, healthcare, retail, and hospitality.

Market Dynamics

To evaluate market opportunities, Request Sample

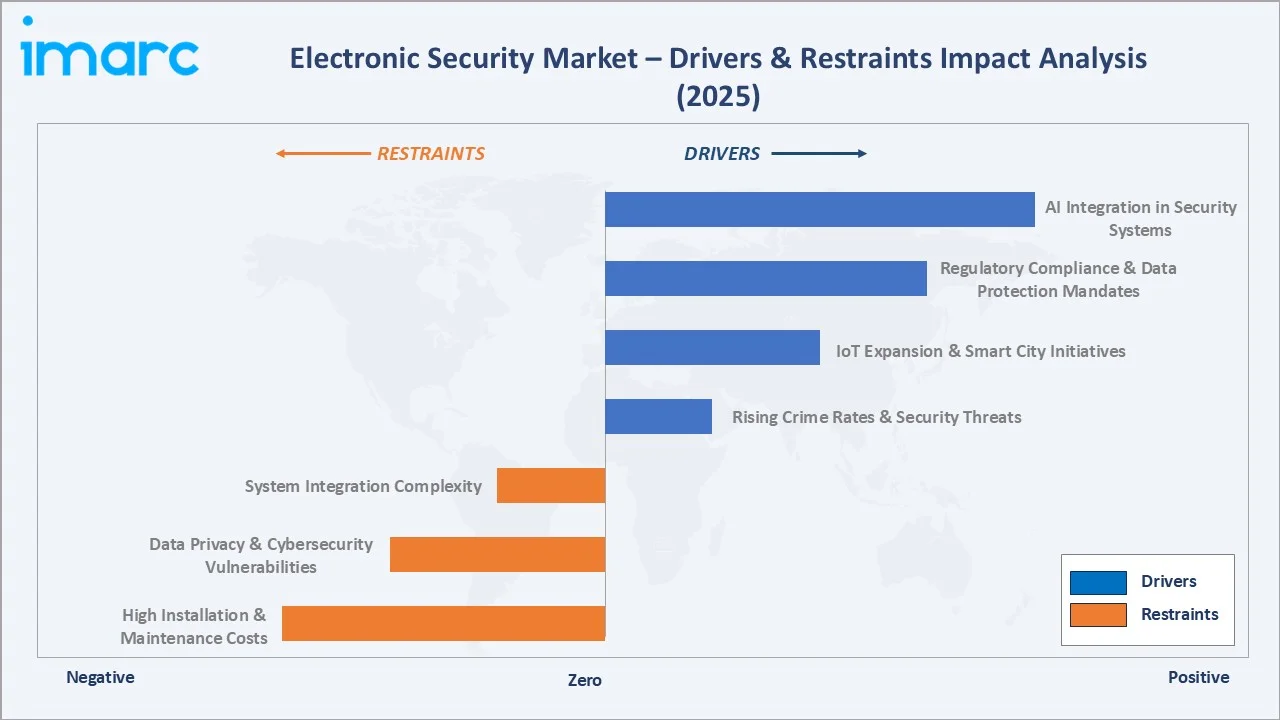

Market Drivers

- Rising Crime Rates and Security Threats: Globally increasing incidents of theft, vandalism, terrorism, and unauthorized access are compelling organizations to invest in advanced electronic security. The FBI reports that property crimes in the US alone resulted in losses exceeding USD 16 Billion annually, reinforcing the business case for surveillance and access control deployments.

- IoT Expansion and Smart City Initiatives: The proliferation of IoT devices, projected to surpass 30 Billion globally by 2026, is creating an interconnected security ecosystem. Government-led smart city programs across China, India, UAE, and Europe are integrating AI-powered surveillance, facial recognition, and smart access control into urban infrastructure at scale.

- Regulatory Compliance and Data Protection Mandates: GDPR, HIPAA, PCI DSS, and sector-specific regulations require organizations to implement robust security measures. Financial institutions, healthcare providers, and government agencies face stringent audit requirements, driving systematic investments in electronic security infrastructure to ensure compliance and avoid significant penalties.

Market Restraints

- High Installation and Maintenance Costs: Enterprise-grade electronic security systems require substantial upfront investment in hardware, software, and integration, along with ongoing costs for maintenance, upgrades, and system management, leading to a high total cost of ownership. For large-scale deployments, these expenses can become significant, making it challenging for small and medium-sized enterprises and budget-constrained organizations to adopt and implement such comprehensive security solutions.

- Data Privacy and Cybersecurity Vulnerabilities: Connected security systems present attack surfaces for cybercriminals. High-profile breaches of IP cameras and access control systems have highlighted the risks of inadequate cybersecurity hygiene in electronic security deployments, raising concerns among privacy advocates and regulators worldwide.

Market Opportunities

- AI-Powered Analytics and Predictive Security: Machine learning algorithms enabling behavior analysis, facial recognition, anomaly detection, and predictive threat assessment are transforming electronic security from reactive to proactive. AI-driven analytics can reduce false alarms by up to 90%, significantly improving operational efficiency for security operators and reducing incident response costs.

- Cloud-Based Security-as-a-Service (SECaaS): The transition from on-premises to cloud-managed security platforms enables scalable, remotely accessible security operations with reduced infrastructure investment. VSaaS (Video Surveillance as a Service) and ACaaS (Access Control as a Service) markets are growing at double-digit rates, opening new recurring revenue models for providers.

Market Challenges

- Skilled Workforce Shortage: The global security industry faces a critical shortage of trained professionals in cybersecurity, system integration, and AI-driven security analytics. The (ISC)² Cybersecurity Workforce Study estimates a global cybersecurity workforce gap of over 3 million professionals, constraining service delivery capacity and increasing labour costs for providers.

- System Integration Complexity: Large enterprises operate heterogeneous security environments with legacy systems from multiple vendors. Integrating new electronic security platforms with existing IT infrastructure, building management systems, and operational technology presents significant technical and project management challenges that extend deployment timelines and increase costs.

Emerging Market Trends

1. AI-Driven Surveillance and Intelligent Video Analytics

AI-powered surveillance systems are replacing traditional passive monitoring with proactive threat detection. Computer vision algorithms enable real-time identification of suspicious behavior, unauthorized access attempts, and unattended objects. Deep learning models trained on billions of video frames provide detection accuracy exceeding 95%, enabling security teams to respond instantly to genuine threats while eliminating false alarms from environmental factors.

2. Cloud-Based Security Platforms and Remote Monitoring

Cloud migration is fundamentally reshaping electronic security architecture. Cloud-hosted video management systems (VMS) eliminate server room infrastructure, enabling pay-per-use consumption models, automatic software updates, and seamless scalability. Remote monitoring via mobile applications allows facility managers to access live feeds, configure alerts, and manage access permissions from any location globally.

3. Biometric Authentication and Multi-Factor Access Control

Traditional PIN and card-based access control is rapidly being supplemented by biometric authentication, fingerprint, iris, facial recognition, and behavioral biometrics. Multi-factor authentication combining biometric, mobile credential, and PIN verification is becoming standard in high-security environments including data centers, financial institutions, and government facilities.

4. Cybersecurity Convergence in Physical Security

The boundary between physical and cyber security is dissolving as connected devices become standard. Forward-thinking organizations are adopting unified security platforms that integrate physical access control, video surveillance, cybersecurity monitoring, and IT security event management into single panes of glass, enabling comprehensive threat visibility across both domains.

Industry Value Chain Analysis

The electronic security value chain spans seven stages from raw component supply through end-use deployment. System integration and managed services capture the highest value-add margins, while installation and consulting services generate significant recurring revenue streams that favor well-capitalized, geographically diversified service providers.

| Stage |

Key Players / Examples |

| Component Supply |

Semiconductors, image sensors, microcontrollers, optical lenses, housing materials, and electronic sub-assemblies sourced from component manufacturers and distributors. |

| Hardware Manufacturing |

Assembly and production of cameras, access readers, control panels, alarm sensors, and ancillary security hardware at OEM and ODM manufacturing facilities. |

| Software Development |

Development of video management systems (VMS), access control software, analytics engines, mobile applications, and cloud security management platforms. |

| System Integration |

Design, configuration, testing, and commissioning of integrated security solutions combining hardware, software, and communication infrastructure for end-user environments. |

| Distribution & Sales |

Multi-channel distribution through value-added resellers (VARs), specialty security distributors, direct enterprise sales, and e-commerce platforms reaching diverse customer segments. |

| Installation & Service |

On-site installation, commissioning, preventive maintenance, remote monitoring, and break-fix services delivered by certified security contractors and managed service providers. |

| End-Use Deployment |

Operational use of electronic security systems across government, commercial, industrial, residential, transportation, healthcare, banking, and critical infrastructure environments. |

Technology Landscape in the Electronic Security Industry

Video Surveillance: IP Cameras and AI Analytics

IP-based network cameras have displaced analog CCTV as the dominant surveillance technology, enabling higher resolution, digital zoom, remote access, and direct integration with AI analytics engines. 4K Ultra HD cameras, multisensor panoramic devices, and thermal imaging cameras are expanding deployment in perimeter security, traffic monitoring, and crowd management applications globally.

Access Control: Cloud-Native and Mobile Credentials

Cloud-native access control platforms are replacing on-premises servers with subscription-based models offering automatic firmware updates, centralized multi-site management, and seamless integration with HR directories. Mobile credentials using NFC and Bluetooth Low Energy (BLE) are replacing physical key cards, enabling touchless entry and remote credential management from smartphones.

Intrusion Detection: Sensor Fusion and Edge Intelligence

Modern intrusion detection systems employ sensor fusion, combining passive infrared (PIR), microwave, acoustic, and vibration sensing, to improve detection accuracy and reduce false alarms. Edge computing devices embedded in detectors perform preliminary AI analysis locally, transmitting only verified alerts to central monitoring stations, reducing bandwidth requirements and response latency considerably.

Alarm and Communication: Cellular and Cloud Connectivity

Dual-path communication combining cellular and broadband connectivity ensures alarm signal transmission even during network outages. Cloud-hosted alarm receiving centers (ARCs) with automated verification workflows using video analytics and two-way audio are replacing traditional monitoring centers, reducing alarm response times from minutes to seconds in enterprise deployments.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Surveillance System |

58.4% |

2025 |

|

Service Type |

Managed Services |

43.5% |

2025 |

|

End-Use Sector |

Government |

18.7% |

2025 |

|

Region |

North America |

29.5% |

2025 |

By Product Type

Surveillance systems command a 58.4% majority share in 2025 owing to their universal deployment across public safety, retail loss prevention, banking security, and corporate environments. The widespread adoption of IP cameras, AI-powered video management systems, and video analytics software has made surveillance the cornerstone of modern electronic security architecture worldwide.

To access detailed market analysis, Request Sample

Access control systems at 16.7% in 2025 are growing rapidly, driven by biometric authentication adoption, mobile credentialing, and zero-trust security architectures. Intrusion detection systems (11.3%) serve both residential and commercial markets, increasingly integrated into smart home and building automation ecosystems.

Alarming systems (7.6%) provide critical life-safety and perimeter protection functions, while Others (6.0%) encompass cybersecurity-physical convergence and integrated command center solutions.

By Service Type

Managed services lead the segment at 43.5% in 2025, reflecting enterprise preference for outsourced continuous monitoring, proactive threat response, and compliance reporting. Managed security service providers (MSSPs) offer 24/7 SOC operations, SLA-backed response times, and scalable coverage without capital investment in staffing and infrastructure, driving strong adoption across large enterprises and mid-market organizations alike.

Installation services at 34.2% capture significant activity from new construction projects, system upgrades, and technology refresh cycles driven by the convergence of IP networking and physical security. Consulting services (22.3%) provide high-margin advisory, risk assessment, compliance audit, and system design engagements, growing with enterprise security governance investments and increasing regulatory complexity globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

| North America |

29.5% |

Cybersecurity compliance; critical infrastructure protection; AI surveillance adoption; enterprise risk management programs |

| Asia-Pacific |

27.6% |

Smart city programs; urbanization; large-scale national surveillance; ASEAN commercial expansion |

| Europe |

21.8% |

GDPR compliance investment; public safety mandates; smart building integration; data center security growth |

| Latin America |

11.2% |

Rising urban crime rates; banking sector security investments; retail loss prevention; government surveillance programs |

| Middle East & Africa |

9.9% |

GCC Vision 2030 smart infrastructure; NEOM mega-city project; oil & gas facility security; African urbanization and commercial real estate expansion |

North America's 29.5% market dominance in 2025 is sustained by the most mature regulatory and compliance framework globally. The US Department of Homeland Security's critical infrastructure protection programs, financial sector FFIEC guidelines, and healthcare HIPAA mandates drive systematic electronic security procurement across government and enterprise sectors, ensuring sustained baseline demand regardless of macroeconomic cycles.

Asia-Pacific, with 27.6% in 2025, is the fastest-growing region for electronic security, driven by China's large-scale public surveillance infrastructure, India's Safe City Mission covering more than 100 cities, and Southeast Asia's booming commercial real estate and retail sectors. The region's established manufacturing base for security hardware further accelerates domestic adoption by enabling cost-competitive deployments.

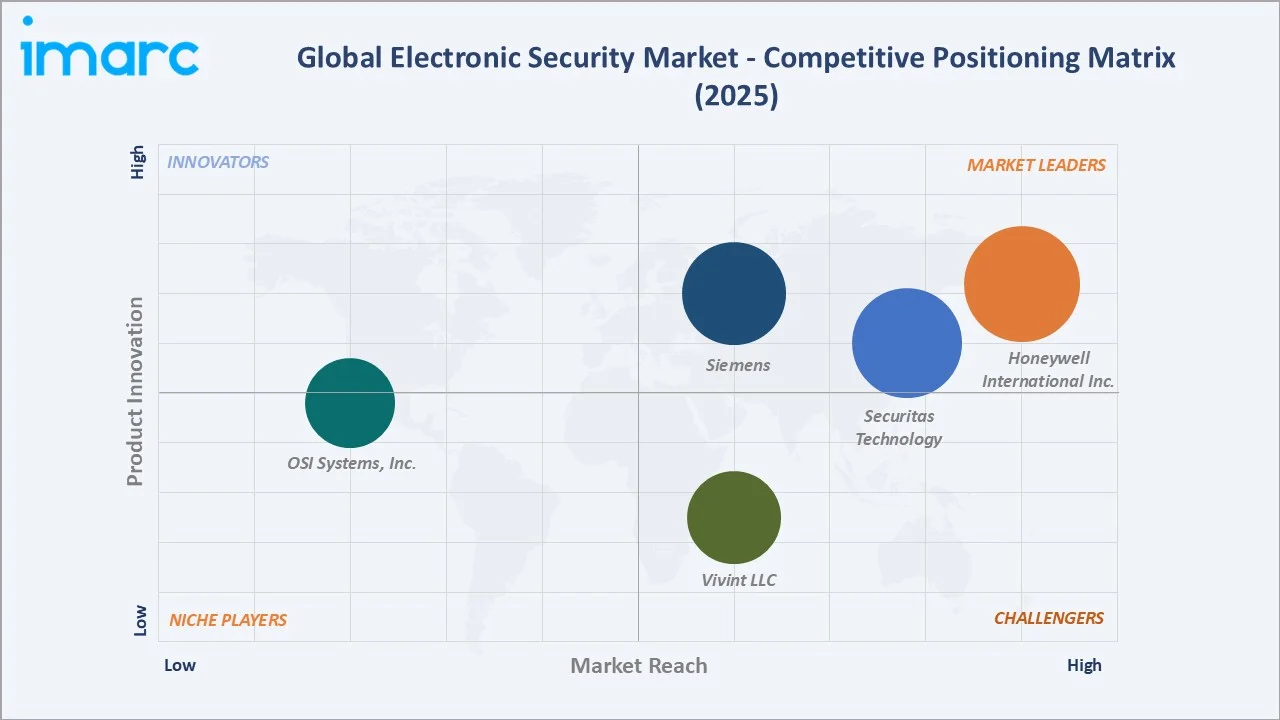

Competitive Landscape

The global electronic security market is moderately consolidated, with global technology conglomerates competing alongside specialized security companies and regional champions. North American and European markets are served by well-established integrated security companies, while Asia-Pacific features both global players and dominant domestic manufacturers.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

| Honeywell International Inc. | Maxpro VMS, 35 Series IP Cameras, 30 Series IP Cameras, NetBox |

Leader |

Global integrated security; building automation convergence; connected enterprise platform |

| Securitas Technology | Video Surveillance, Intrusion systems | Leader | Company is part of Securitas AB, GenAI-powered cloud security platforms; digital transformation of enterprise security operations |

| Siemens | SiPass, SIPORT, Siveillance Video | Leader |

Building technologies integration; European and global industrial focus |

| Vivint LLC | Outdoor Camera, Doorbell Camera, Indoor Camera Pro | Challenger |

Residential smart home security leadership in North America; AI-powered surveillance with Smart Deter and Smart Sentry detection; professionally installed and 24/7 monitored security ecosystems; integration of security with energy management under NRG Energy ownership |

| OSI Systems, Inc. | Rapiscan screening systems, perimeter security |

Emerging |

Aviation and port security screening; government checkpoint contracts; physical security inspection solutions |

Key players include Honeywell International Inc., Securitas Technology, Siemens, Vivint LLC, OSI Systems, Inc., and others.

Key Company Profiles

Honeywell International Inc.

Honeywell International Inc. is a global technology and manufacturing leader with a comprehensive electronic security portfolio spanning video surveillance, access control, intrusion detection, and cloud-based security management platforms serving enterprise and critical infrastructure clients worldwide.

- Product Portfolio: Maxpro VMS, 35 Series IP Cameras, 30 Series IP Cameras, 70 Series, NetBox

- Recent Developments: In June 2024, Honeywell International acquired Carrier's Global Access Solutions business, significantly strengthening its position as a provider of digital-age security solutions and substantially expanding its access control market presence.

- Strategic Focus: Honeywell's security strategy centers on connected enterprise platforms that integrate physical security, building automation, and cybersecurity into unified operational intelligence systems for enterprise and critical infrastructure customers across global markets.

Securitas Technology

Securitas Technology is the world's second-largest commercial electronic security provider, headquartered in Uniontown, Ohio, USA, and operating as the technology division of Securitas AB. The company delivers end-to-end integrated security solutions, serving millions of enterprise clients in commercial, industrial, healthcare, retail, and government environments.

- Product Portfolio: Video Surveillance, Intrusion systems, and others

- Recent Developments: In March 2026, Securitas Technology entered into a global reseller agreement with Ambient.ai to expand its portfolio of AI-driven security solutions, enabling the deployment of advanced threat detection and automation capabilities across its global client base. Through this partnership, the company enhanced its ability to transition organizations from traditional, reactive security models to proactive, intelligence-led operations, where AI continuously analyzes and responds to real-world events in real time alongside human operators.

- Strategic Focus: Securitas Technology's core strengths include access control, video, intrusion and fire systems, with the company designing, installing, integrating, servicing and monitoring these systems to deliver end-to-end protection tailored to clients' needs; its broader offerings encompass remote video monitoring, cloud-based security services, and professional and managed services that support every stage of the security journey.

Market Concentration Analysis

The global electronic security market is moderately consolidated at the global level, with regional leaders holding dominant positions in their home markets while several large global suppliers compete across geographies. No single company holds more than 8-10% of total global market value, reflecting the diversity of product categories, service models, and regional dynamics that characterize this industry.

Consolidation through strategic acquisitions is accelerating Honeywell's acquisition of Carrier's access control division, Johnson Controls' investments in intelligent building integration, and Motorola Solutions' acquisition of Avigilon reflect a clear trend of large conglomerates building comprehensive security ecosystems. Private equity activity is consolidating installation and managed services providers into regional platform companies with enhanced scale and service capabilities.

Investment & Growth Opportunities

Fastest-Growing Segments

Managed services at ~6.5% CAGR through 2034 is the highest-growth service segment, driven by enterprise preference for outsourced security operations and the transition from capital expenditure to operating expenditure security models. AI-powered video analytics growing at ~6.2% CAGR represents the broadest-based technological opportunity within the surveillance sub-segment of the global electronic security market.

Emerging Markets

Middle East & Africa at ~6.8% CAGR is the fastest-growing region for electronic security through 2034. Saudi Arabia's NEOM project and Vision 2030 smart infrastructure investments, UAE's advanced surveillance ecosystem, and African commercial real estate expansion are creating large-scale security procurement from regions with rapidly growing installed bases and increasing government focus on public safety.

Venture & Investment Trends

Venture capital investment in AI-native security startups, computer vision analytics, biometric authentication, and autonomous drone surveillance, exceeded USD 2 Billion in 2024. Private equity consolidation of regional managed security service providers is creating national platform companies with 24/7 monitoring scale. ESG-linked smart building investments are driving bundled security and energy management solution procurement across commercial real estate portfolios.

Future Market Outlook (2026-2034)

The global electronic security market is forecast to expand from USD 68.94 Billion in 2025 to USD 113.05 Billion by 2034 at a CAGR of 5.65%, adding USD 44.11 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's non-discretionary nature, security investment is driven by regulatory compliance, risk management, and insurance requirements that remain resilient through economic cycles.

Three technological forces will shape the electronic security landscape most significantly through 2034: autonomous AI surveillance systems capable of operating without human monitoring intervention; quantum-resistant encryption for next-generation access control credentials; and digital twin security platforms enabling virtual simulation of physical security system performance before full-scale deployment.

Research Methodology

Primary Research

Primary research encompassed structured interviews with electronic security industry stakeholders, including senior product managers, EPC procurement specialists, security systems integrators, chief security officers, and financial analysts covering the global security sector. Primary data validated market sizing, product and service segment shares, regional demand estimates, and technology adoption timelines across all major geographies.

Secondary Research

Key secondary sources include Security Industry Association (SIA) Annual Almanac, IHS Markit Physical Security Intelligence Service, ASIS International security spending surveys, IFSEC Global market reports, ISC West industry data, government procurement records, SEC filings of major electronic security companies, and trade publications including Security Business, SDM Magazine, and Security Management.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating end-use sector spending data, GDP growth correlations, regulatory compliance investment cycles, and installed base replacement rates. Scenario analysis — base, optimistic, and conservative cases — was applied to account for macroeconomic and geopolitical uncertainty affecting the global electronic security industry.

Electronic Security Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Surveillance System, Access Control System, Intrusion Detection System, Alarming System, Others |

| Service Types Covered | Installation Services, Managed Services, Consulting Services |

| End-Use Sectors Covered | Government, Residential, Transportation, Banking, Hospitality, Healthcare, Retail, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Honeywell International Inc., Securitas Technology, Siemens, Vivint LLC, OSI Systems, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electronic security market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global electronic security market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electronic security industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Electronic Security Market Report

The global electronic security market reached USD 68.94 Billion in 2025, reflecting consistent demand driven by rising security threats, expanding IoT infrastructure, smart city programs, and regulatory compliance requirements across commercial, government, and residential sectors worldwide.

The market is projected to reach USD 113.05 Billion by 2034, growing at a CAGR of 5.65% during 2026-2034, driven by AI-powered surveillance adoption, cloud-based security platforms, biometric access control expansion, and increasing security investments in emerging markets across Asia-Pacific, Middle East, and Africa.

Surveillance systems lead with a 58.4% product share in 2025, valued for their universal applicability across commercial, government, transportation, banking, and residential environments. IP-based cameras and AI-powered video analytics have transformed surveillance into the foundational layer of modern integrated security architectures.

Managed services dominate at 43.5% in 2025, representing the largest service segment as enterprises increasingly outsource 24/7 security monitoring, maintenance, and incident response to managed security service providers (MSSPs) to reduce capital costs and improve security posture without building in-house security operations centers.

North America commands a dominant 29.5% market share in 2025, driven by mature regulatory compliance frameworks, extensive critical infrastructure protection mandates, high enterprise security awareness, and robust government cybersecurity spending programs. Asia-Pacific closely follows at 27.6%, propelled by large-scale smart city and national surveillance programs.

Managed services are the fastest-growing service segment at approximately 6.5% CAGR through 2034, driven by the shift from capital expenditure to operating expenditure security models, growth of cloud-based monitoring platforms, and increasing enterprise adoption of Security-as-a-Service (SECaaS) delivery models that offer flexibility, scalability, and predictable cost structures.

Leading companies include Honeywell International Inc., Securitas Technology, Siemens, Vivint LLC, OSI Systems, Inc., among others.

Key applications include perimeter surveillance and intrusion detection, employee and visitor access control, retail loss prevention, banking and ATM security, critical infrastructure protection, transportation hub monitoring, residential smart security, healthcare facility safety, data center physical security, and government and defense facility protection across global markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)