Sensor Fusion Market Size, Share, Trends and Forecast by Type, Technology, Industry Vertical, and Region, 2026-2034

Sensor Fusion Market Size, Share, Trends & Forecast (2026-2034)

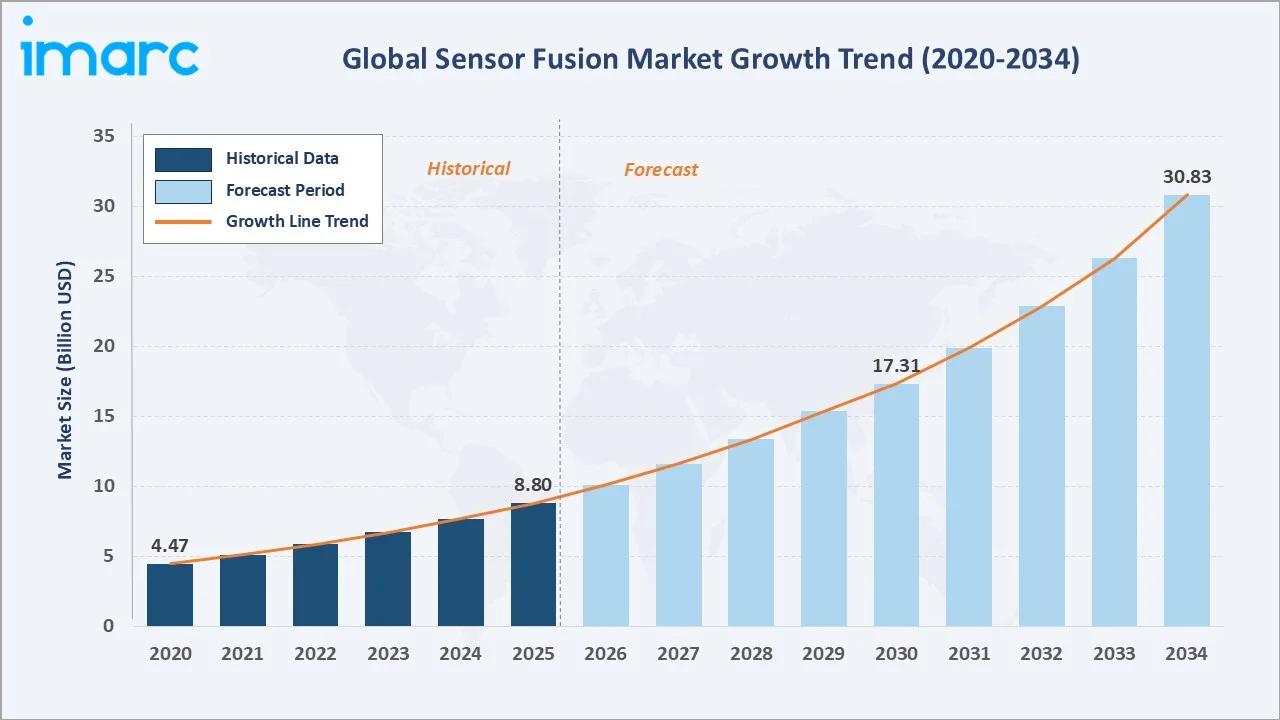

The global sensor fusion market reached USD 8.80 Billion in 2025 and is projected to reach USD 30.83 Billion by 2034, growing at a CAGR of 14.50% during 2026-2034. Accelerating adoption of autonomous vehicles and ADAS, the proliferation of IoT-connected consumer electronics, growing demand for healthcare wearables, and rapid advances in MEMS and AI-based fusion algorithms are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.80 Billion |

|

Forecast Market Size (2034) |

USD 30.83 Billion |

|

CAGR (2026-2034) |

14.50% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

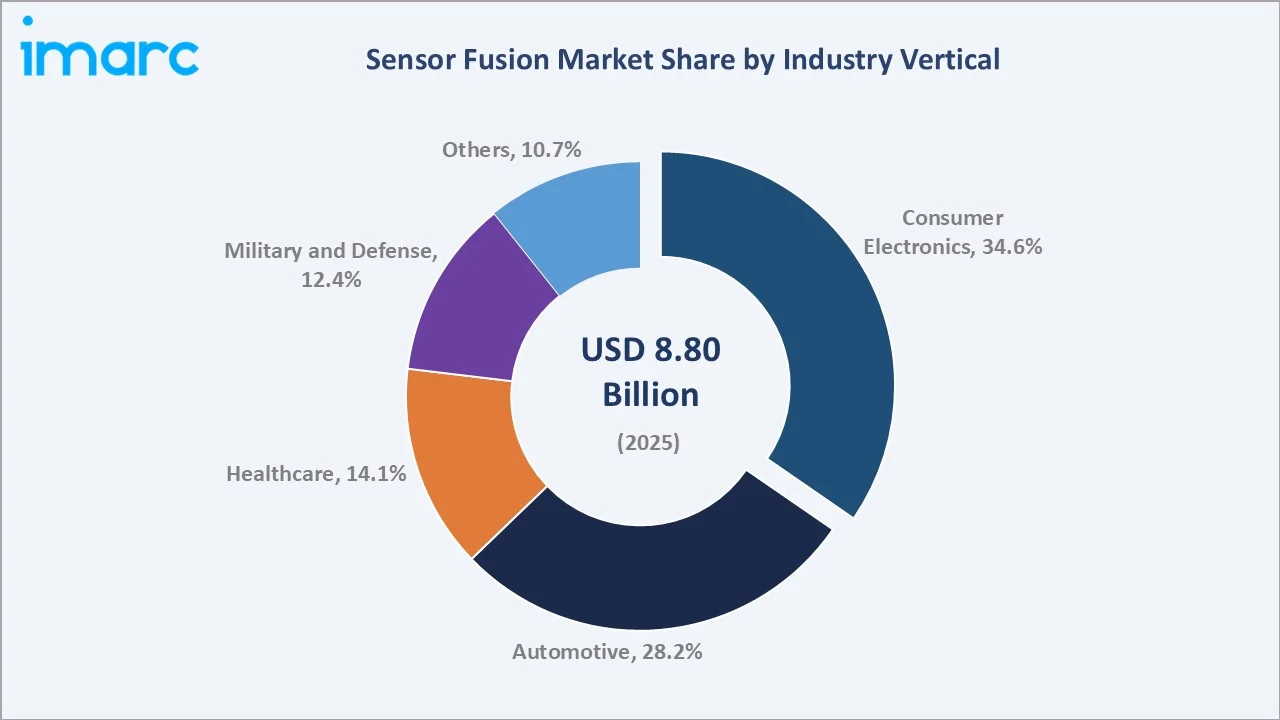

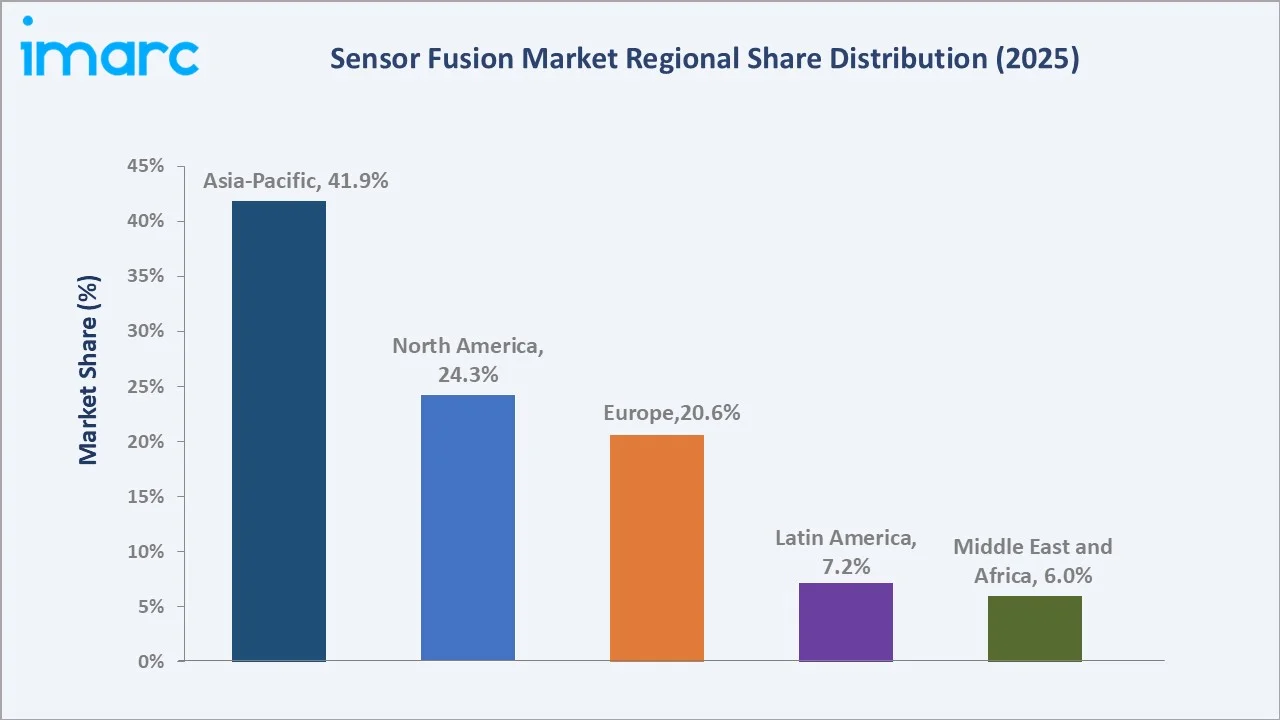

Asia-Pacific leads regionally with a 41.9% market share in 2025, driven by its world-leading consumer electronics manufacturing base, large automotive production sector, and strong government investment in AI, robotics, and smart infrastructure. Consumer electronics commands the dominant 34.6% industry vertical share, reflecting the pervasive integration of multi-axis MEMS sensor fusion into smartphones, tablets, smartwatches, AR/VR headsets, and connected home devices.

To get more information on this market, Request Sample

The sensor fusion market is driven by three converging structural forces: the indispensable requirement for multi-sensor data integration in autonomous and semi-autonomous systems; the miniaturization and cost reduction of MEMS sensors enabling fusion deployment in billions of consumer devices; and the AI-powered algorithm revolution that is transforming fusion from static linear filtering to adaptive, context-aware real-time inference.

Executive Summary

The global sensor fusion market is experiencing high-growth expansion, driven by the simultaneous acceleration of autonomous vehicle technology development, the proliferation of AI-powered IoT devices, and the growing integration of multi-sensor systems across healthcare, defense, and industrial automation applications. The market was valued at USD 8.80 Billion in 2025 and is forecast to reach USD 30.83 Billion by 2034, growing at a CAGR of 14.50%.

Consumer electronics lead the industry vertical at 34.6% in 2025, underpinned by the mass deployment of 6-axis and 9-axis MEMS inertial measurement units (IMUs) in smartphones for screen orientation, motion gaming, fitness tracking, and AR/VR positioning. The automotive segment at 28.2% reflects the accelerating adoption of multi-sensor ADAS systems, including radar, LiDAR, camera, and ultrasonic sensor fusion for automatic emergency braking, lane keeping, and adaptive cruise control.

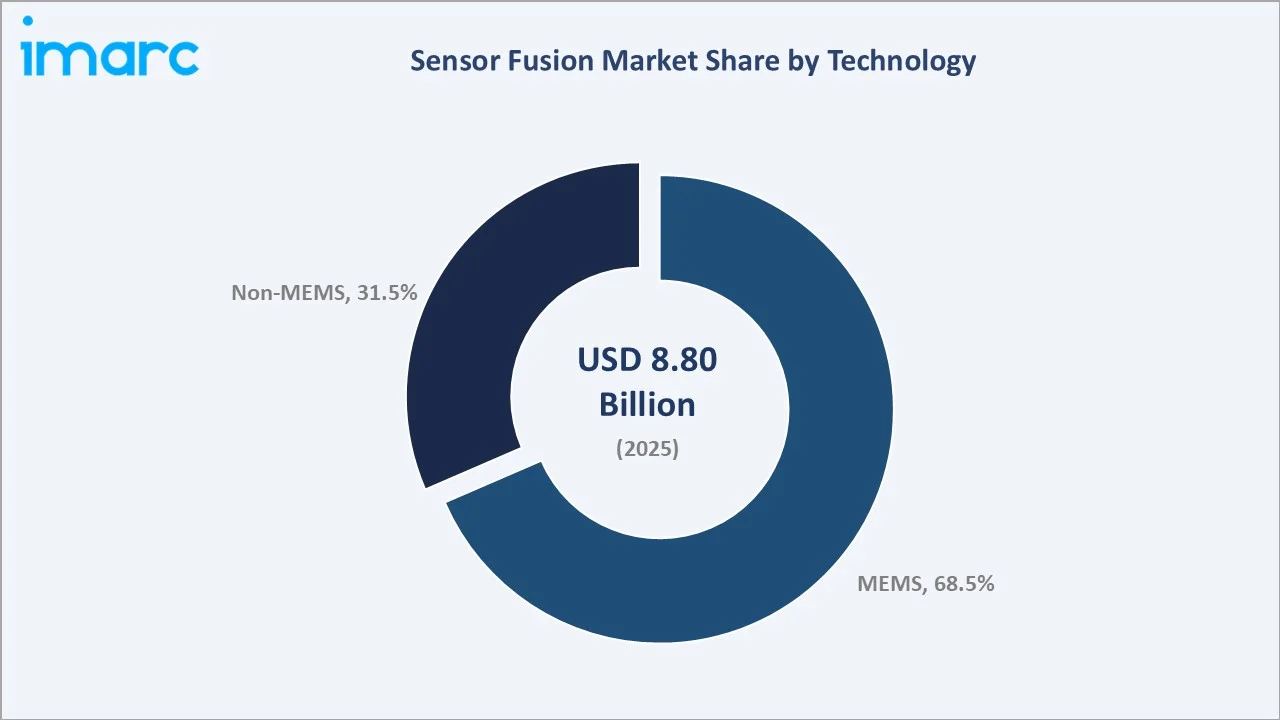

MEMS dominates 68.5% of the technology segment, reflecting its cost-effectiveness, miniaturization, and mass production scalability across consumer, automotive, and industrial applications. Key players collectively dominate the competitive landscape through semiconductor integration, MEMS technology leadership, and AI algorithm capability.

Key Market Insights

|

Insight |

Data |

|

Largest Industry Vertical |

Consumer Electronics – 34.6% share (2025) |

|

Second Largest Vertical |

Automotive – 28.2% share (2025) |

|

Largest Technology |

MEMS – 68.5% share (2025) |

|

Second Largest Technology |

Non-MEMS – 31.5% share (2025) |

|

Leading Region |

Asia-Pacific – 41.9% share (2025) |

|

Top Companies |

Qualcomm Incorporated, STMicroelectronics, Robert Bosch GmbH, Analog Devices, Inc., TDK Corporation |

Key Analytical Observations Supporting the Above Data:

- Consumer electronics at 34.6% (2025) lead the market as sensor fusion is now a foundational capability in every smartphone, smartwatch, and AR/VR headset. The 9-axis IMU fusion of accelerometer, gyroscope, and magnetometer data underpins screen rotation, step counting, navigation, gaming, and AR overlay positioning across billions of shipped devices annually.

- Automotive at 28.2% (2025) reflects the mandatory adoption of multi-sensor fusion in ADAS systems across new vehicle models. ISO 26262 defines Automotive Safety Integrity Levels (ASILs). It establishes requirements for system design, development, validation, production, operation, and decommissioning to ensure vehicle safety, creating regulatory-driven structural demand independent of market cycles.

- MEMS at 68.5% (2025) dominates as MEMS fabrication processes enable accelerometers, gyroscopes, and pressure sensors to be produced at semiconductor-grade scale and cost, with modern MEMS IMUs integrating onboard sensor fusion processing that delivers sub-degree heading accuracy while consuming milliwatts of power.

- Asia-Pacific’s 41.9% share (2025) reflects China’s simultaneous dominance as the world’s largest smartphone manufacturer, largest electric vehicle producer, and the leading investor in industrial AI and robotics, all of which create proportional demand for MEMS sensor fusion across consumer, automotive, and industrial application categories.

Sensor Fusion Market Overview

Sensor fusion is the process of combining data from multiple sensor sources, including inertial, magnetic, optical, acoustic, and radio-frequency sensors, to produce an integrated estimate of physical state that is more accurate, reliable, and comprehensive than any individual sensor could achieve independently. The global market encompasses sensor fusion hardware (MEMS chips, SoCs, and fusion processors), software (fusion algorithms, middleware, and AI inference frameworks), and integrated sensor fusion modules across automotive, consumer electronics, healthcare, defense, and industrial applications.

Macroeconomic drivers include around USD 40 billion in investments announced by the end of 2024 for EV manufacturing in India through 2030, the global smartphone shipments increased by 2% in 2025, reaching 1.25 billion units with increasing sensor complexity, and the number of connected IoT devices is projected to reach 39 billion by 2030, registering a CAGR of 13.2% from 2025 (according to IoT Analytics). Moreover, regulatory mandates for ADAS safety features in new vehicles across the EU, USA, Japan, and China are creating structural non-discretionary sensor fusion demand embedded in vehicle manufacturing cost structures for the entire forecast period.

Market Dynamics

To evaluate market opportunities, Request Sample

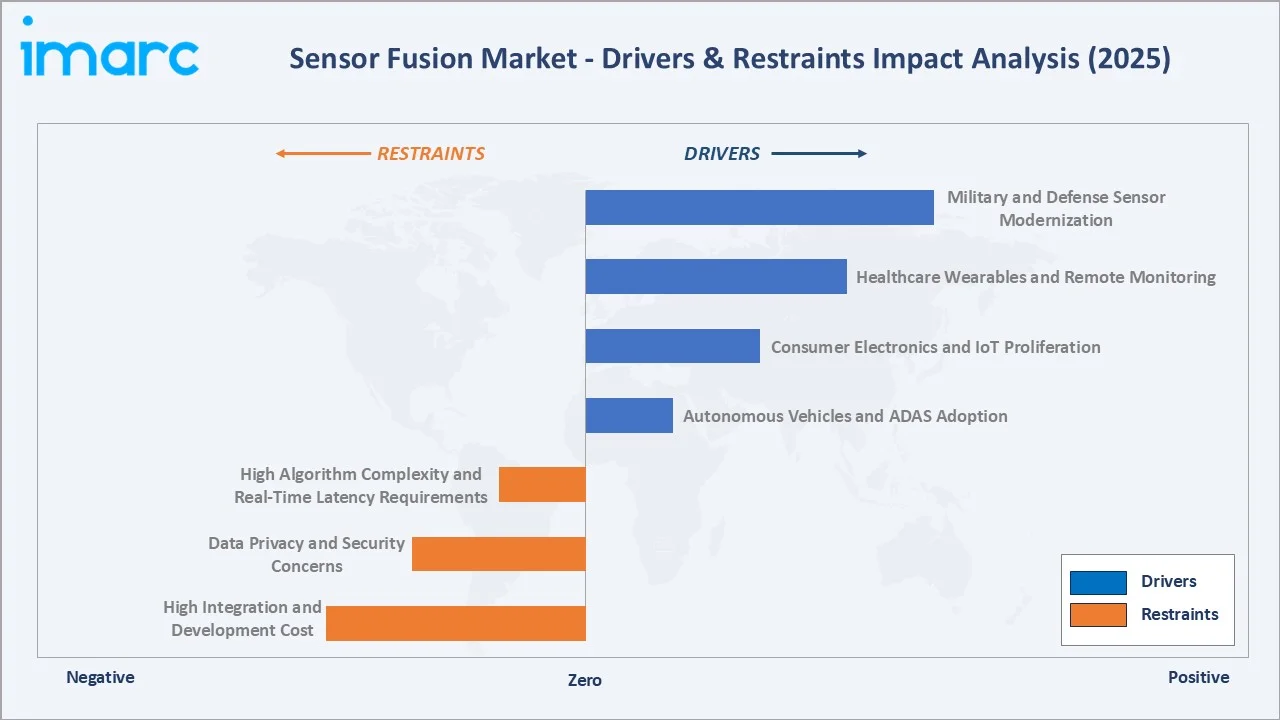

Market Drivers

- Autonomous Vehicles and ADAS Adoption: The global automotive industry’s mandatory transition to ADAS features is the most powerful structural driver of sensor fusion demand. Euro NCAP 5-star safety ratings now require automatic emergency braking, lane departure warning, and driver monitoring, all requiring multi-sensor fusion.

- Consumer Electronics and IoT Proliferation: Smartphones, smartwatches, fitness trackers, AR/VR headsets, and smart home devices are deploying increasingly sophisticated MEMS sensor arrays with onboard fusion processing. With global smartphone shipments reaching 1.25 Billion in 2025 and the wearables market growing at 15%+ CAGR, the cumulative installed base of consumer sensor fusion systems represents the single largest volume application category in the market.

- Healthcare Wearables and Remote Monitoring: Clinical-grade wearable devices for continuous heart rate, blood oxygen, fall detection, gait analysis, and neurological monitoring require multi-modal sensor fusion integrating inertial, optical, electrochemical, and RF sensing. The ageing global population, post-pandemic telehealth expansion, and regulatory approval of AI-powered clinical wearables are driving above-market growth in the healthcare sensor fusion segment.

- Military and Defense Sensor Modernization: Modern defense platforms, including soldier wearables, unmanned aerial vehicles, naval vessels, and missile guidance systems, require robust sensor fusion for navigation, target tracking, and situational awareness in GPS-denied and electronically contested environments. US DoD, NATO, and Asian defense procurement programs are driving sustained high-value sensor fusion R&D and procurement activity.

Market Restraints

- High Algorithm Complexity and Real-Time Latency Requirements: Robust sensor fusion in safety-critical applications requires computationally intensive algorithms that must execute within strict latency budgets (typically below 10 milliseconds for automotive ADAS). Meeting these requirements while minimizing power consumption and silicon area represents a persistent technical challenge that limits rapid adoption in power-constrained applications.

- Data Privacy and Security Concerns: Sensor fusion systems that continuously collect motion, location, biometric, and environmental data create significant privacy and cybersecurity exposure. Regulations, including GDPR in Europe, CCPA in California, and emerging AI liability frameworks, impose compliance costs and liability risks on sensor fusion deployments in consumer and healthcare applications, creating adoption friction particularly for cloud-connected fusion architectures.

- High Integration and Development Cost: Developing validated, production-ready sensor fusion solutions for safety-critical applications requires substantial investment in algorithm development, calibration infrastructure, test and validation equipment, and regulatory certification. These costs create barriers for smaller OEMs and system integrators, concentrating sensor fusion capability among large, well-resourced semiconductor companies and Tier-1 automotive suppliers.

Market Opportunities

- Edge AI Sensor Fusion for Wearables and IoT: The deployment of dedicated AI inference engines within MEMS sensor modules, enabling on-device fusion without offloading to a host processor, is dramatically reducing power consumption and latency for wearable and IoT sensor fusion applications. This capability is enabling always-on context awareness, gesture recognition, and health monitoring in battery-powered devices with multi-day battery life, opening large new consumer and healthcare application categories.

- Industrial Robotics and Autonomous Mobile Robots: The global logistics automation and industrial robotics markets are deploying autonomous mobile robots (AMRs) requiring robust real-time sensor fusion for obstacle detection, navigation, and manipulation. With 542,000 industrial robots installed in 2024 (World Robotics 2025 statistics) and AMR adoption accelerating in warehousing and manufacturing, industrial sensor fusion represents a rapidly growing high-value application segment.

Market Challenges

- Sensor Calibration and Environmental Robustness: Maintaining sensor fusion accuracy across varying temperatures, vibration levels, electromagnetic interference, and sensor ageing remains a significant engineering challenge. MEMS gyroscopes and accelerometers exhibit temperature-dependent drift, camera-based fusion degrades in poor lighting, and radar performance varies with target material properties.

- Fragmented Standards and Interoperability: The absence of universal sensor fusion algorithm standards means that sensor fusion implementations are typically proprietary and non-interoperable. This fragmentation increases OEM integration complexity and cost, limits the ability to mix sensors from multiple vendors, and creates ecosystem lock-in that may not serve the best technical outcome for end users.

Emerging Market Trends

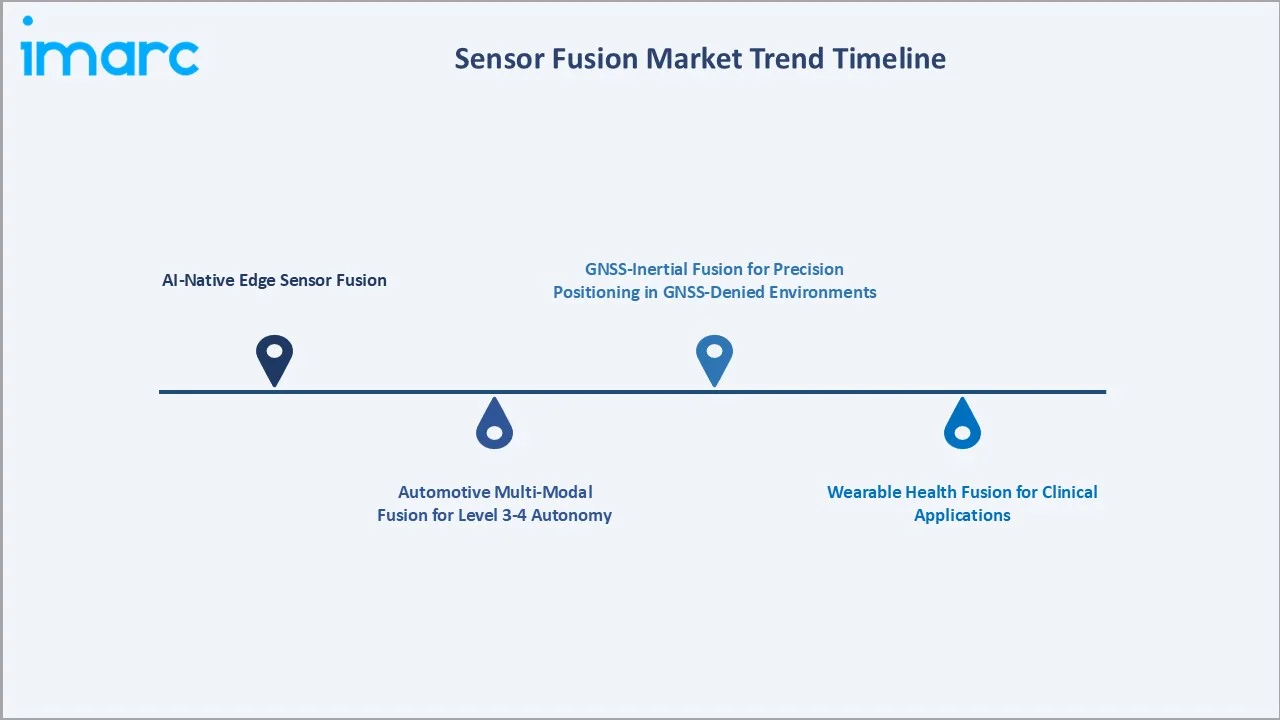

1. AI-Native Edge Sensor Fusion

The embedding of dedicated neural processing units (NPUs) within MEMS sensor modules and automotive SoCs is enabling AI-native sensor fusion that dynamically selects and weights sensor inputs based on environmental context. Robert Bosch GmbH’s BHI360 and STMicroelectronics’ ISM330IS intelligent sensor module exemplify this trend. AI-native fusion systems learn from deployment data to progressively improve accuracy, making them self-optimizing across diverse real-world conditions.

2. Automotive Multi-Modal Fusion for Level 3-4 Autonomy

Level 3 and Level 4 autonomous vehicles require the fusion of LiDAR, 4D imaging radar, surround-view camera, ultrasonic, and V2X communication data into a unified environmental model with sub-100ms latency and ISO 26262 ASIL-D safety integrity. NVIDIA DRIVE AGX Thor and Qualcomm Snapdragon Ride Flex are the leading computing platforms for this application, both offering dedicated sensor fusion hardware accelerators alongside AI inference units for perception and prediction tasks.

3. Wearable Health Fusion for Clinical Applications

Clinical-grade wearable devices combining photoplethysmography, electrocardiography, accelerometry, and skin temperature into fused physiological state models are earning FDA clearance for atrial fibrillation detection, continuous blood pressure monitoring, and stress assessment. The clinical wearables market is growing at above 20% CAGR, driven by post-pandemic telehealth expansion and insurer reimbursement models that incentivize continuous remote patient monitoring over episodic clinical visits.

4. GNSS-Inertial Fusion for Precision Positioning in GNSS-Denied Environments

Agricultural robots, underground mining vehicles, underground construction machinery, and GPS-jammed military platforms require precision positioning through inertial-visual-LiDAR sensor fusion when GNSS signals are unavailable or unreliable. Advances in visual-inertial odometry (VIO) algorithms and low-cost high-accuracy IMUs are enabling decimetric positioning accuracy in complex indoor and underground environments without infrastructure dependency, creating new addressable markets for sensor fusion in previously challenging applications.

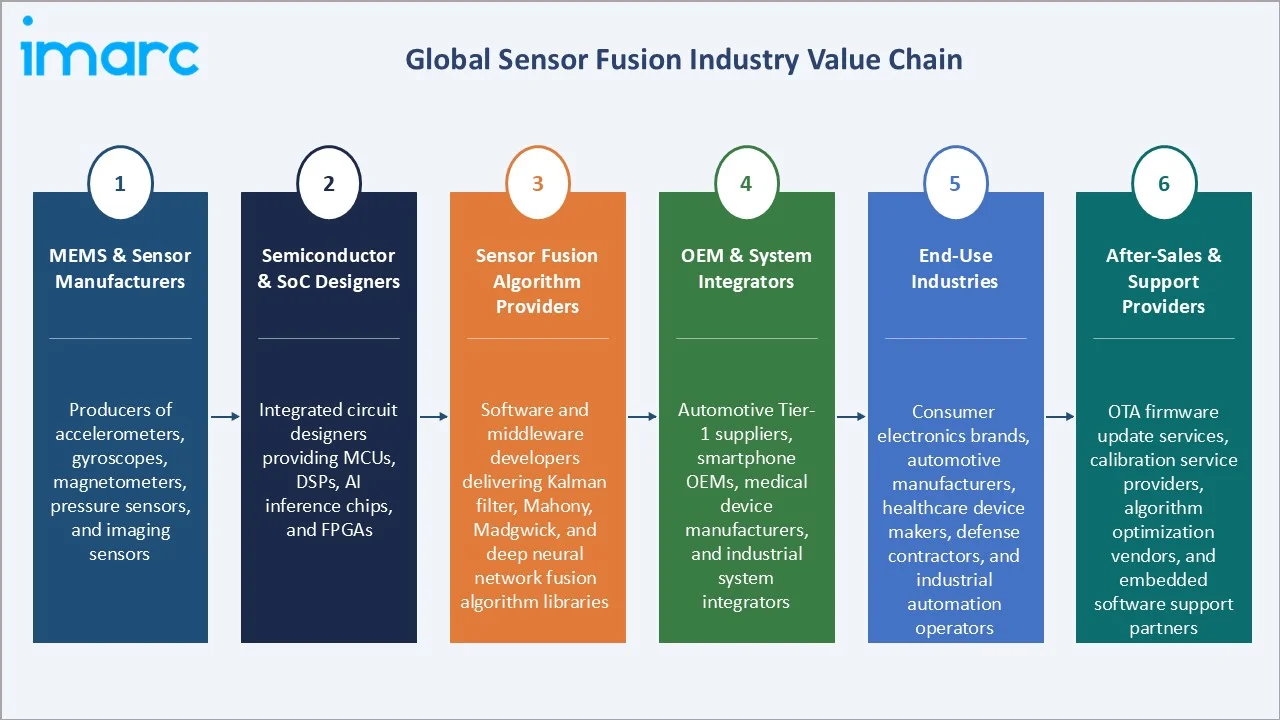

Industry Value Chain Analysis

The sensor fusion value chain spans from MEMS and optical sensor manufacturing through semiconductor SoC design, algorithm development, OEM integration, and end-use deployment across consumer, automotive, healthcare, and defense applications. The semiconductor and SoC design tier represents the highest value-add stage, with companies integrating MEMS sensing, signal conditioning, AI inference, and fusion algorithm execution into single-chip solutions.

|

Stage |

Key Players / Examples |

|

MEMS & Sensor Manufacturers |

Producers of accelerometers, gyroscopes, magnetometers, pressure sensors, and imaging sensors |

|

Semiconductor & SoC Designers |

Integrated circuit designers providing MCUs, DSPs, AI inference chips, and FPGAs |

|

Sensor Fusion Algorithm Providers |

Software and middleware developers delivering Kalman filter, Mahony, Madgwick, and deep neural network fusion algorithm libraries |

|

OEM & System Integrators |

Automotive Tier-1 suppliers, smartphone OEMs, medical device manufacturers, and industrial system integrators |

|

End-Use Industries |

Consumer electronics brands, automotive manufacturers, healthcare device makers, defense contractors, and industrial automation operators |

|

After-Sales & Support Providers |

OTA firmware update services, calibration service providers, algorithm optimization vendors, and embedded software support partners |

Technology Landscape in the Sensor Fusion Industry

MEMS Sensor Technology

MEMS inertial sensors are the foundational hardware enabling consumer and automotive sensor fusion at scale. Modern 6-axis MEMS IMUs integrate accelerometer and gyroscope functionality in a single 2.5×2.5mm package at below-USD-1 unit cost, making multi-axis motion fusion economically viable in every consumer electronic device. MEMS fabrication process advances continue to improve noise performance, temperature stability, and power consumption, progressively expanding the performance envelope of cost-effective sensor fusion applications.

AI and Machine Learning Fusion Algorithms

The transition from classical Kalman filter-based sensor fusion to deep learning-based approaches is transforming the accuracy, adaptability, and application scope of sensor fusion systems. Deep neural networks trained on large labelled sensor datasets outperform classical filters in complex non-linear environments, including indoor positioning, human activity recognition, and multi-object tracking. Federated learning approaches are enabling fusion models to be trained across distributed edge devices without centralizing private sensor data, addressing privacy concerns in wearable and healthcare applications.

High-Performance Computing Platforms for Automotive Fusion

The processing requirements for Level 3+ autonomous vehicle sensor fusion, integrating real-time data from 30+ sensors at 100Hz+ update rates with sub-50ms system latency, demand custom AI accelerator SoCs with 100–500+ TOPS of neural network inference capability. Qualcomm’s Snapdragon Ride Flex (700+ TOPS) represents one of the leading automotive-grade platforms, each providing dedicated fusion processing alongside functional safety certification that meets ISO 26262 ASIL-B to ASIL-D requirements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Industry Vertical |

Consumer Electronics |

34.6% |

2025 |

|

Technology |

MEMS |

68.5% |

2025 |

|

Type |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

41.9% |

2025 |

By Industry Vertical

Consumer electronics lead with a 34.6% share of the global sensor fusion market in 2025, reflecting the mass-market deployment of MEMS IMU sensor fusion in every smartphone, smartwatch, fitness tracker, and AR/VR headset shipped globally. Google’s Tensor chips all incorporate dedicated sensor fusion processing that continuously integrates accelerometer, gyroscope, and magnetometer data for fitness tracking, navigation, screen rotation, and AR experiences.

To access detailed market analysis, Request Sample

Automotive at 28.2% share (2025) is one of the fastest-growing major verticals, driven by the mandatory integration of multi-sensor ADAS systems across new vehicle models. Healthcare at 14.1% benefits from clinical wearable approvals and remote patient monitoring adoption. Military and defense at 12.4% represents the highest-value per-unit application, with defense-grade inertial navigation systems and multi-domain sensor fusion platforms commanding significant price premiums.

By Technology

MEMS dominates with a 68.5% share in 2025, driven by its unmatched combination of miniaturization, mass production cost efficiency, integration capability, and breadth of sensor types encompassing inertial, pressure, microphone, and optical proximity sensing. The MEMS sensor fusion market is further supported by the growing integration of onboard AI fusion processing within MEMS sensor packages, transforming standalone sensing elements into autonomous intelligent sensing nodes.

Non-MEMS at 31.5% encompasses radar, LiDAR, vision-based systems, GPS/GNSS receivers, and radio-frequency sensing technologies that are increasingly integrated with MEMS inertial data in automotive, defense, and precision positioning applications. The non-MEMS segment’s growth is driven by the automotive sector’s rapid adoption of 4D imaging radar and solid-state LiDAR as primary perception sensors requiring MEMS-inertial fusion for ego-motion compensation and robust environmental modelling.

Regional Market Insights

Asia-Pacific’s dominant position (41.9%, 2025) reflects the region’s simultaneous dominance across every major sensor fusion application category, including consumer electronics, automotive, and industrial. China’s position as the world’s largest smartphone manufacturer, largest EV producer, and the fastest-growing market for industrial robotics creates proportional sensor fusion demand that structurally anchors the region’s global market leadership.

North America, at 24.3%, is driven by the concentration of autonomous vehicle technology development, the largest global defense procurement budget, and leadership in AI-powered consumer electronics through Apple, Google, and Qualcomm.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

41.9% |

World-leading consumer electronics and smartphone manufacturing base, large automotive production sector, and strong government investment in AI, robotics, and smart infrastructure |

|

North America |

24.3% |

High autonomous vehicle development activity, strong defense and aerospace sensor modernization programs, advanced IoT and wearables market, and significant AI and semiconductor R&D investment |

|

Europe |

20.6% |

Mature automotive industry driving ADAS and autonomous vehicle sensor fusion adoption, stringent safety regulations accelerating multi-sensor integration, and a strong industrial automation and robotics sector |

|

Latin America |

7.2% |

Growing consumer electronics adoption, expanding connected vehicle market, increasing smartphone penetration, and rising industrial automation investment |

|

Middle East and Africa |

6.0% |

Defense and security sector modernization, smart city infrastructure investment, growing consumer electronics market, and increasing industrial automation adoption across manufacturing sectors |

Europe’s 20.6% share (2025) benefits from the automotive industry’s ADAS intensity, GDPR-compliant privacy-preserving fusion architectures, and strong industrial automation demand. Latin America at 7.2% and the Middle East and Africa at 6.0% represent smaller but growing markets driven by smartphone adoption and defense modernization, respectively.

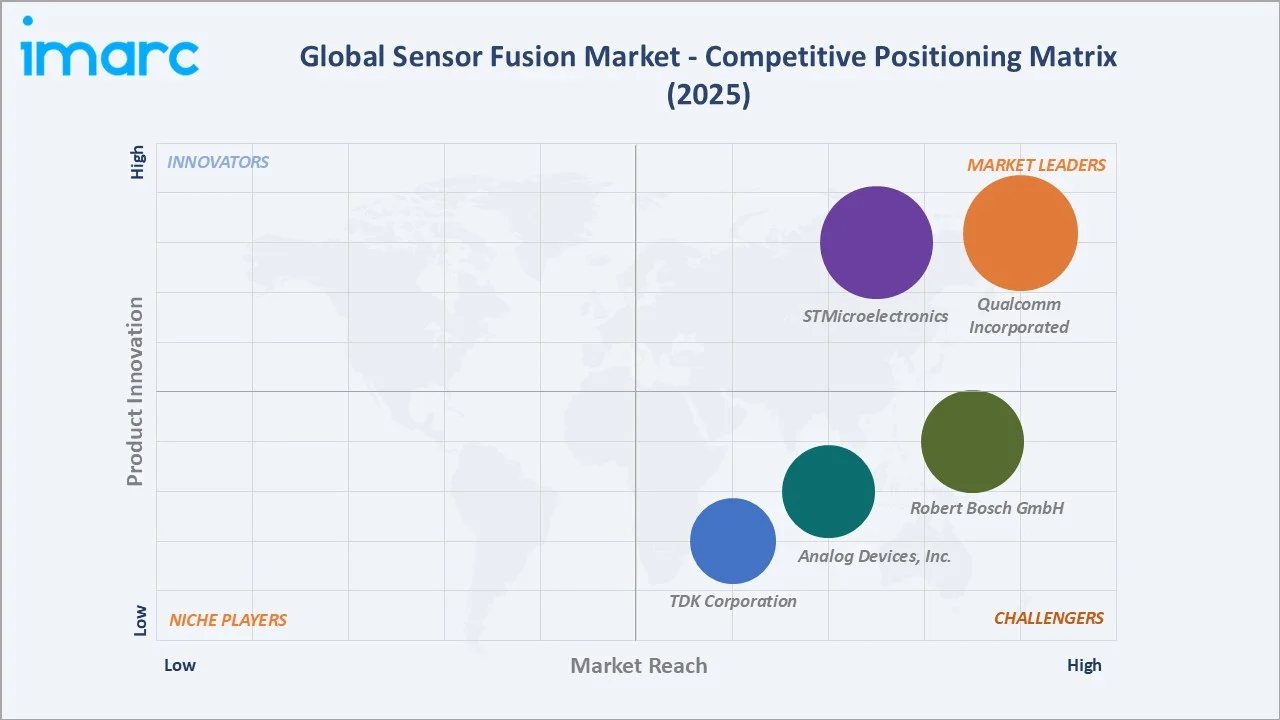

Competitive Landscape

The global sensor fusion market exhibits moderate-to-high concentration at the silicon and algorithm platform tier, with leading semiconductor companies collectively accounting for approximately 55–60% of market revenues in 2025.

|

Company Name |

Products |

Market Position |

Core Strength |

|

Qualcomm Incorporated |

Snapdragon Ride, Qualcomm Hexagon NPU, Qualcomm Snapdragon 8 Series |

Market Leader |

Leading automotive and mobile AI fusion platform with high-performance dedicated sensor fusion processing |

|

STMicroelectronics |

ISM330IS, LSM6DSV, LIS2MDL, LPS22HH |

Market Leader |

Broad MEMS sensor and fusion middleware portfolio with deep consumer electronics and IoT OEM penetration |

|

Robert Bosch GmbH |

BHI360, BMI323, BHI260AP |

Strong Challenger |

Leading MEMS IMU innovation for wearables, smartphones, and industrial IoT with onboard AI fusion capability |

|

Analog Devices, Inc. |

ADIS16577, ADIS16576, ADIS16575, ADIS16501, ADIS16545, ADIS16547, ADIS16550, ADIS16446, ADIS16486, ADIS16500 |

Challenger |

High-precision inertial sensing for industrial, defense, and medical applications with advanced signal processing capability |

|

TDK Corporation |

IMU (Inertial Measurement Unit), Acceleration Sensors, Gyroscopes, Positioning Software, MEMS Microphones (Sensor) |

Challenger |

High-accuracy 6-axis and 9-axis MEMS solutions with low-power fusion for consumer wearables and IoT devices |

The competitive landscape is bifurcating between general-purpose consumer MEMS sensor fusion leaders and high-performance automotive and defense fusion platform providers. AI algorithm capability is emerging as the primary differentiator in both tiers, with companies investing heavily in neural network-based fusion models that outperform classical filter approaches in complex real-world environments.

Key Company Profiles

Qualcomm Incorporated

Qualcomm Incorporated is one of the global leaders in mobile and automotive AI processing platforms and one of the most significant sensor fusion enablers through its Snapdragon SoC family.

- Product Portfolio: Snapdragon 8 Gen series, Snapdragon Ride Flex and Ride Vision, and Hexagon NPU for on-device AI fusion inference.

- Recent Developments: In January 2026, Qualcomm Technologies Inc. (a subsidiary of Qualcomm Incorporated) and Hyundai Mobis signed a strategic collaboration agreement to jointly develop next-generation automotive technologies, including software-defined vehicles (SDVs), digital cockpits, advanced driver-assistance systems (ADAS), and connected mobility solutions.

- Strategic Focus: Automotive sensor fusion platform leadership for Level 3–4 autonomy; mobile AI-native sensor fusion for next-generation AR/VR; Snapdragon ecosystem expansion into industrial IoT.

STMicroelectronics

STMicroelectronics is one of the world’s leading MEMS sensor manufacturers and one of the most prolific sensor fusion innovators. Its MEMS sensor portfolio spans accelerometers, gyroscopes, magnetometers, and environmental sensors, with its latest ISM330IS and LSM6DSV intelligent sensor modules embedding AI-based fusion directly within the sensor package.

- Product Portfolio: LSM6DSV 6-axis IMU with onboard machine learning, ISM330IS intelligent sensor module with embedded AI, LIS2MDL magnetometer, LPS22HH pressure sensor.

- Recent Developments: In February 2026, STMicroelectronics completed the acquisition of NXP Semiconductors’ MEMS sensors business after regulatory approvals. The deal expands ST’s sensors portfolio for automotive safety, non-safety, and industrial applications.

- Strategic Focus: Intelligent MEMS sensor platform with embedded AI fusion; automotive-grade inertial sensing for ADAS and body dynamics; industrial IoT predictive maintenance sensor node deployment.

Market Concentration Analysis

The global sensor fusion market exhibits moderate-to-high concentration at the semiconductor and platform tier, with the top companies holding approximately 55–60% of market revenue in 2025. The concentration is higher in the automotive segment compared to the consumer MEMS segment, where multiple qualified MEMS manufacturers compete on cost, power consumption, and form factor.

The competitive intensity at the algorithm and AI middleware tier is higher than at the hardware tier, with both established semiconductor companies and specialist AI software firms competing for OEM design wins. CEVA, Inc.’s acquisition of Hillcrest Laboratories, Inc. (Hillcrest Labs) business from InterDigital, Inc., consolidated a leading position in embedded sensor fusion middleware, while automotive software pure-plays are challenging hardware-bundled fusion software from traditional semiconductor suppliers through open, hardware-agnostic fusion software platforms.

Investment & Growth Opportunities

Fastest Growing Segments

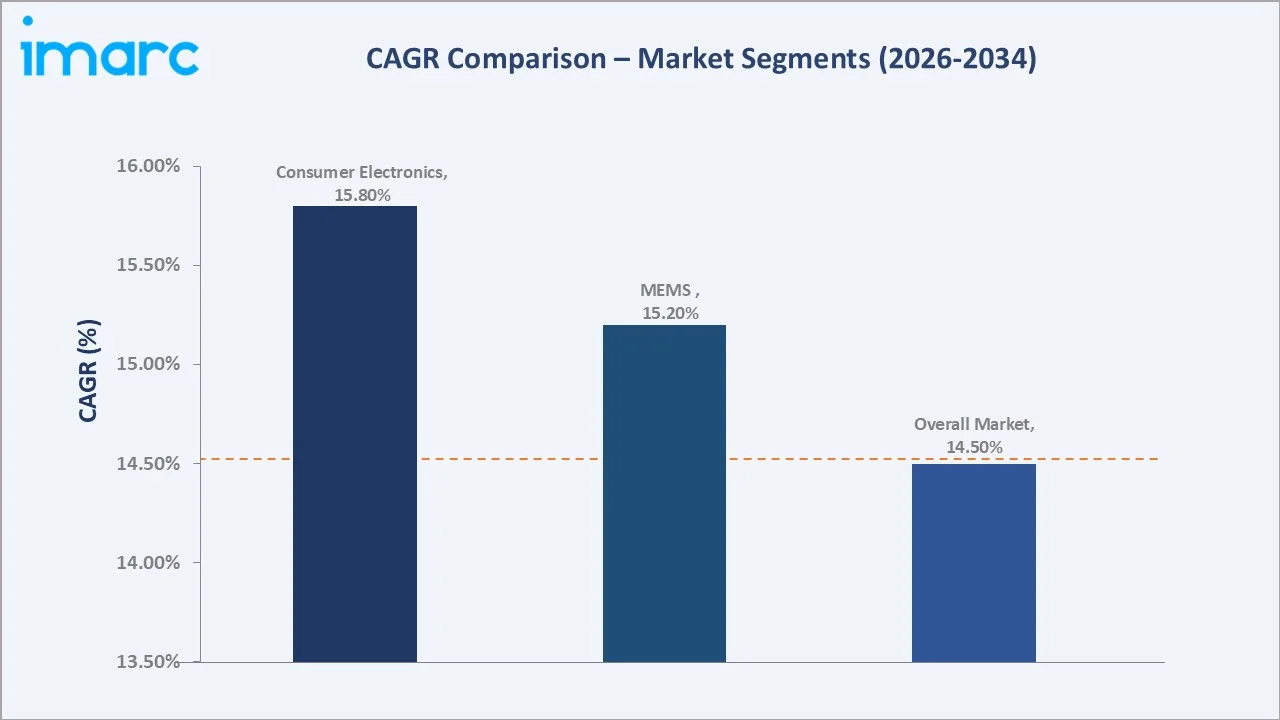

Automotive sensor fusion for Level 3–4 autonomy (~20% CAGR), healthcare clinical wearables sensor fusion (~18% CAGR), and industrial robotics multi-sensor fusion (~16% CAGR) represent the highest-growth investment vectors within the sensor fusion market through 2034. Edge AI fusion chip investments are growing at above-market rates as OEMs demand on-device processing to address latency, privacy, and connectivity constraints.

Emerging Application Opportunities

Extended Reality (XR) devices, including AR glasses and mixed reality headsets, represent one of the most significant emerging sensor fusion application categories, requiring 9-axis IMU fusion combined with inside-out visual tracking at sub-millisecond latency for comfortable, low-latency spatial computing experiences. With Apple Vision Pro, Meta Quest, and Android XR ecosystem devices launching globally, XR sensor fusion is projected to become a USD 1–2 Billion market segment by 2028.

Technology Investment Trends

- Edge AI fusion chip investment is accelerating, with STMicroelectronics, Robert Bosch GmbH, and Analog Devices, Inc. each committing significant R&D resources to embedding NPU inference within MEMS sensor packages, enabling context-aware always-on fusion at sub-milliwatt power consumption for wearable and IoT applications.

- Automotive sensor fusion software platform investment is attracting venture and strategic funding, with open-platform fusion middleware providers challenging proprietary bundled software from semiconductor incumbents. This software unbundling trend is enabling automotive OEMs to mix sensor hardware from multiple vendors, reducing cost and strategic supplier dependency.

- Defense investment in multi-domain sensor fusion for GPS-denied navigation, electronic warfare resilience, and collaborative autonomous systems is creating specialized high-value market segments with significant unit economics advantages over commercial applications.

Future Market Outlook (2026-2034)

The global sensor fusion market is positioned for sustained high-growth expansion through 2034. From USD 8.80 Billion in 2025, the market is projected to reach USD 30.83 Billion by 2034, representing total incremental value creation of USD 22.03 Billion at a CAGR of 14.50%.

This growth trajectory is underpinned by three concurrent megatrends: the global automotive industry’s mandatory transition to AI-enhanced ADAS and autonomous capability; the continued proliferation of intelligent IoT and wearable devices embedding ever-more-sophisticated multi-sensor fusion; and the defense and industrial sectors’ systematic upgrading of sensor architectures for AI-enhanced situational awareness.

The technology composition of the market will continue to evolve as AI-native fusion architectures replace classical algorithm approaches across all application categories. MEMS technology will retain its dominant position through 2034 as the foundational sensing layer, while Non-MEMS sensing modalities grow their share in automotive and defense applications requiring long-range, high-resolution environmental perception beyond MEMS’ measurement capabilities.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants in 2024–2025, including sensor fusion chip manufacturers, automotive Tier-1 engineers, consumer electronics OEM product managers, healthcare device developers, defense electronics procurement officers, and industrial IoT platform architects. Expert input validated market sizing, segment growth rates, and regional penetration estimates.

Secondary Research

Secondary research encompassed semiconductor company annual reports and earnings disclosures, MEMS Industry Group technical publications, IEEE Sensors Journal research, Society of Automotive Engineers (SAE) ADAS technical papers, FDA digital health device clearance databases, DoD procurement announcements, and industry publications including EE Times, IEEE Spectrum, and Automotive World.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating global MEMS sensor shipment volume data, sensor fusion chip ASP trajectories by application segment, automotive ADAS penetration rate modelling, consumer electronics sensor integration trend analysis, and healthcare wearable regulatory approval pipeline projections.

Sensor Fusion Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Radar Sensors, Image Sensors, IMU, Temperature Sensor, Others |

| Technologies Covered | MEMS, Non-MEMS |

| Industry Verticals Covered | Automotive, Healthcare, Consumer Electronics, Military and Defense, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Qualcomm Incorporated, STMicroelectronics, Robert Bosch GmbH, Analog Devices, Inc., TDK Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the sensor fusion market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global sensor fusion market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the sensor fusion industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Sensor Fusion Market Report

The global sensor fusion market reached USD 8.80 Billion in 2025 and is projected to reach USD 30.83 Billion by 2034.

The market is expected to grow at a CAGR of 14.50% during 2026-2034, driven by autonomous vehicle ADAS adoption, consumer electronics IoT proliferation, healthcare wearables, and AI-powered fusion algorithm advances.

Asia-Pacific leads with a 41.9% share in 2025, driven by the region’s dominance in consumer electronics manufacturing, automotive production, and government investment in AI, robotics, and smart infrastructure.

Consumer electronics lead with a 34.6% share in 2025, reflecting the mass deployment of MEMS IMU sensor fusion across smartphones, smartwatches, fitness trackers, and AR/VR headsets globally.

MEMS dominates with a 68.5% share in 2025, reflecting its miniaturization, mass production cost efficiency, and broad sensor type range that makes it the foundational hardware platform for sensor fusion across consumer, automotive, and industrial applications.

Some of the key players include Qualcomm Incorporated, STMicroelectronics, Robert Bosch GmbH, Analog Devices, Inc., and TDK Corporation.

Key drivers include mandatory ADAS and autonomous vehicle multi-sensor integration, consumer electronics IoT proliferation, healthcare wearable clinical approval expansion, and AI-powered fusion algorithm advances enabling new application capabilities.

Fastest-growing opportunities include automotive Level 3-4 multi-sensor fusion platforms, edge AI fusion chips for wearables, clinical wearable health monitoring, XR spatial computing fusion, and open-platform automotive fusion software that challenges proprietary semiconductor-bundled middleware.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)