Gluten-Free Pasta Market Size, Share, Trends and Forecast by Product Type, Type, Ingredient, Distribution Channel, and Region, 2026-2034

Gluten-Free Pasta Market Size, Share, Trends & Forecast (2026-2034)

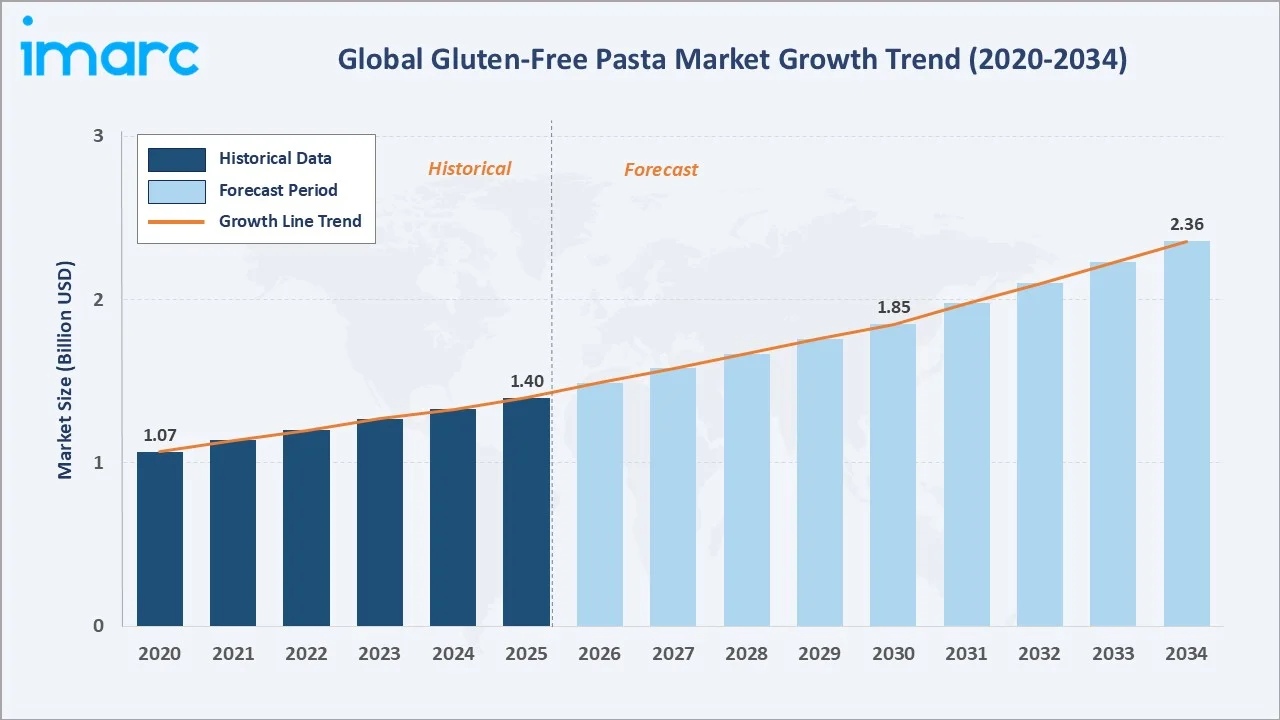

The global gluten-free pasta market reached USD 1.40 Billion in 2025 and is projected to reach USD 2.36 Billion by 2034, growing at a CAGR of 5.66% during 2026-2034. The market is driven by rising celiac disease prevalence, growing health consciousness, and expanding retail availability of gluten-free products globally.

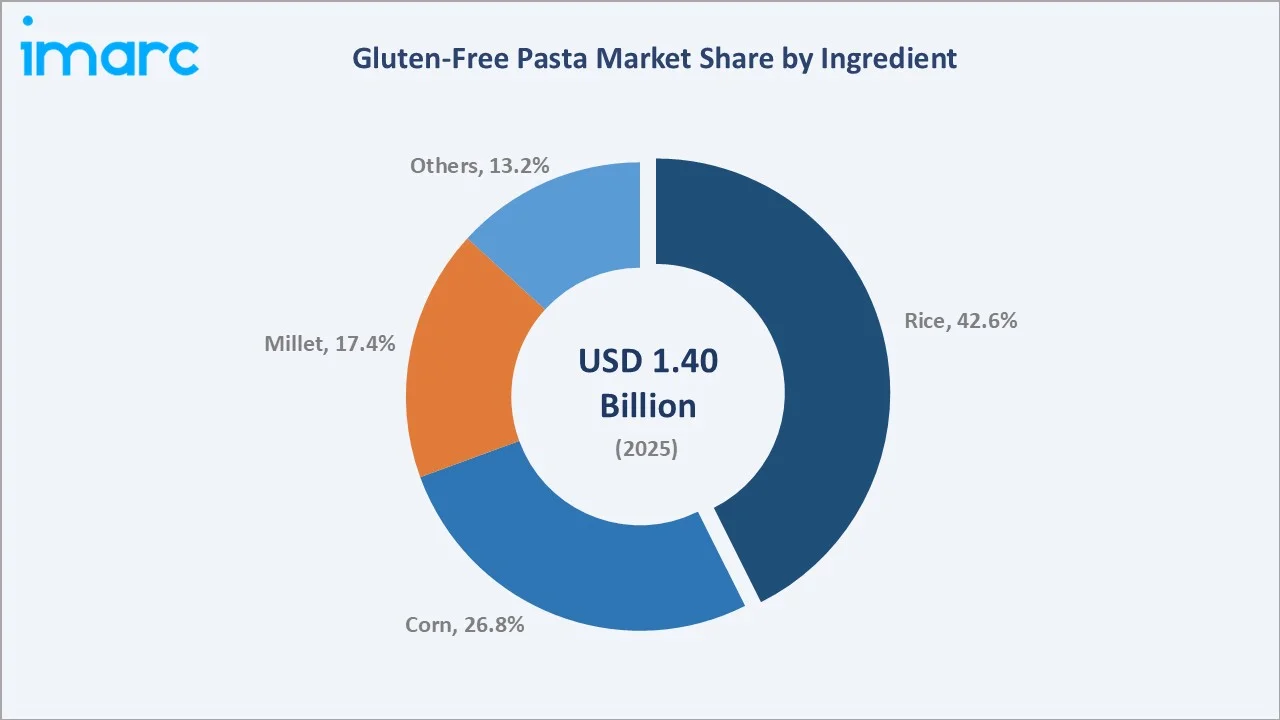

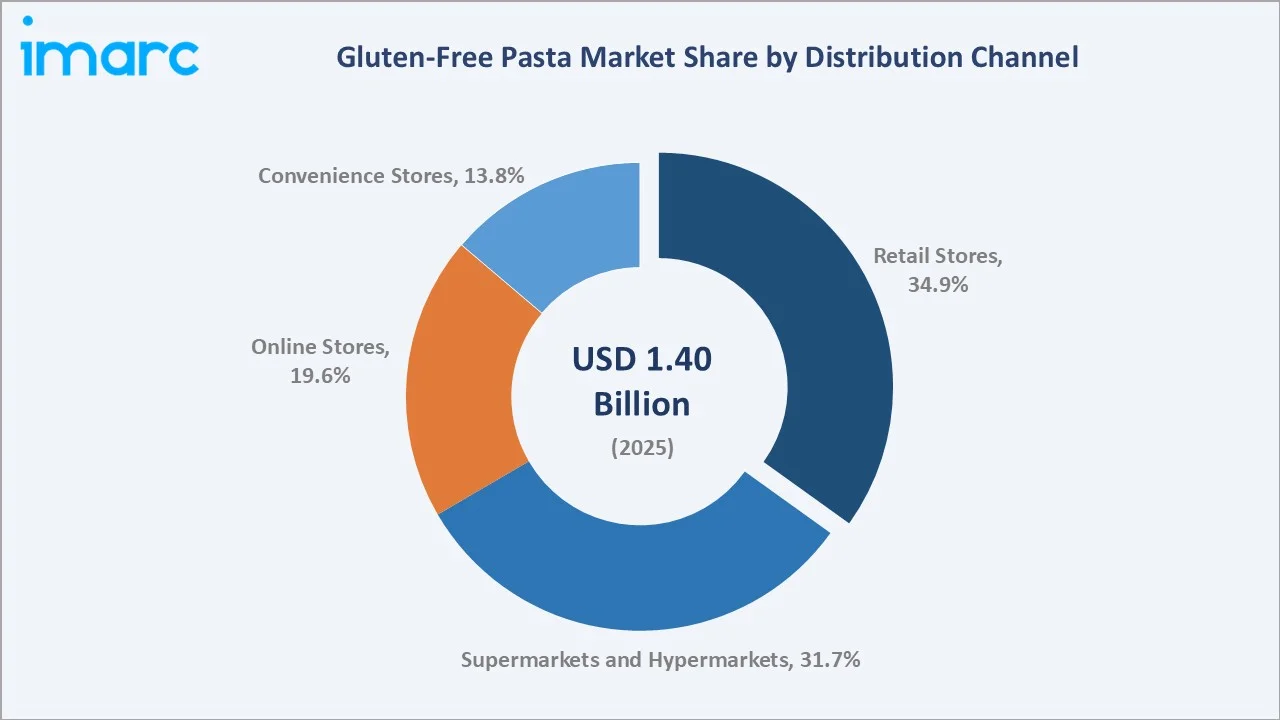

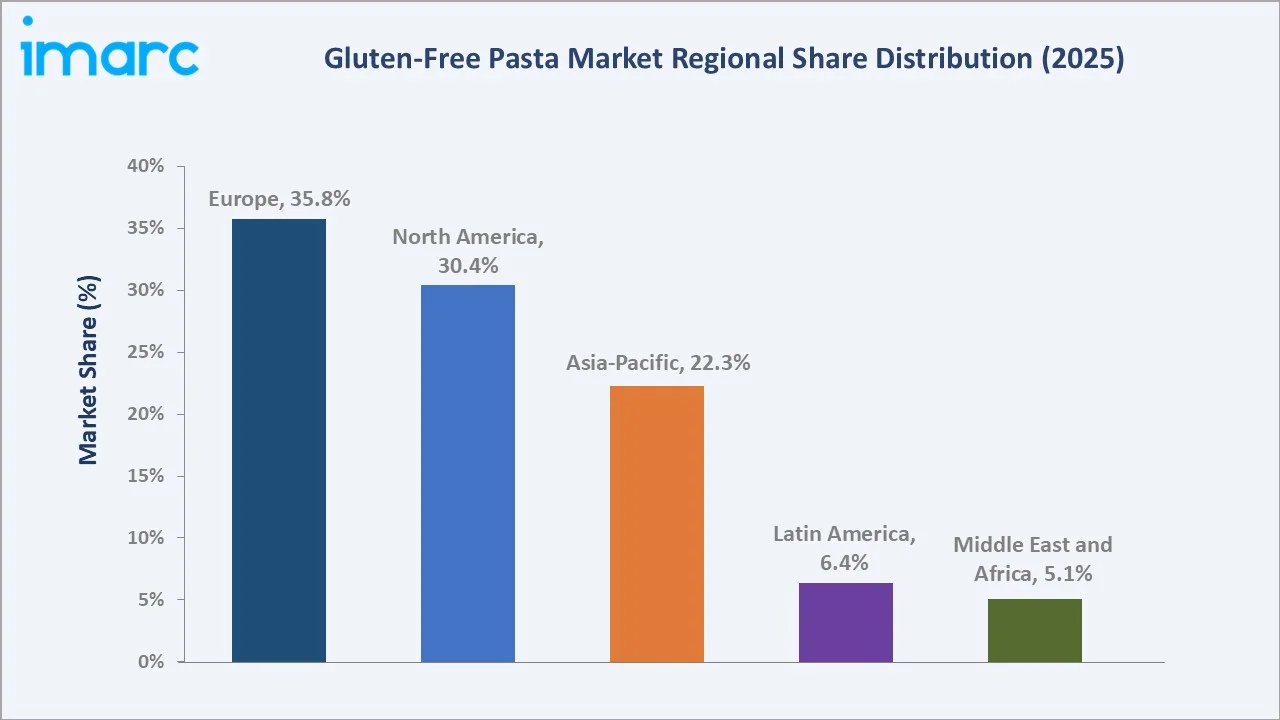

Rice leads the ingredient segment at 42.6%. Retail Stores dominate distribution at 34.9%. Europe commands 35.8% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.40 Billion |

|

Forecast Market Size (2034) |

USD 2.36 Billion |

|

CAGR (2026-2034) |

5.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Ingredient |

Rice (42.6%, 2025) |

|

Dominant Distribution Channel |

Retail Stores (34.9%, 2025) |

|

Leading Region |

Europe (35.8%, 2025) |

The market expanded from USD 1.07 Billion in 2020 to USD 1.40 Billion in 2025, anchored at USD 1.85 Billion in 2030 and forecast to reach USD 2.36 Billion by 2034. Increasing awareness of celiac disease and gluten intolerance, alongside the global wellness megatrend, sustained demand through market disruptions, recovering and accelerating through 2023-2025 as product quality improved and mainstream retail adoption widened.

To get more information on this market, Request Sample

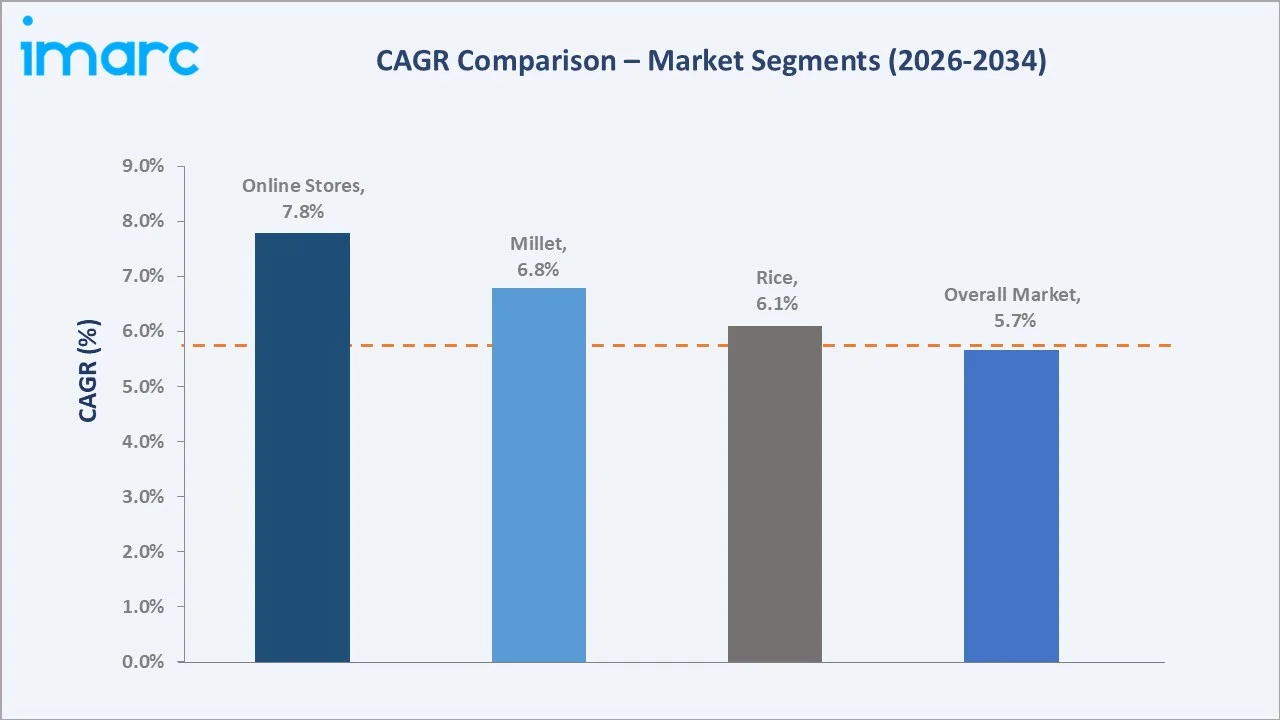

Rice-based pasta grows at ~6.1% CAGR, benefiting from mainstream consumer preference and established supply chains. Online Stores grow fastest at ~7.8% CAGR as e-commerce enables niche gluten-free brands to reach broader audiences across underserved geographies.

Executive Summary

The global gluten-free pasta market reached USD 1.40 Billion in 2025, representing one of the food industry's most dynamic specialty segments driven by health and wellness megatrends, rising celiac disease diagnosis rates, and expanding mainstream retail distribution. The market is projected to reach USD 2.36 Billion by 2034.

Rice-based ingredients at 42.6% dominate due to a superior taste profile and consumer familiarity. Retail Stores lead distribution at 34.9% through wide physical availability. Europe at 35.8% reflects strong celiac disease awareness and an established gluten-free food culture.

Key Market Insights

|

Insight |

Data |

|

Dominant Ingredient |

Rice – 42.6% share (2025) |

|

Dominant Distribution Channel |

Retail Stores – 34.9% market share (2025) |

|

Leading Region |

Europe – 35.8% market share (2025) |

|

Market Opportunity |

Millet/ancient grain innovation; online-first brands; Asia-Pacific expansion; foodservice penetration |

Key Analytical Observations Supporting The Above Data:

- Rice at 42.6%: Rice flour provides the closest texture to conventional wheat pasta, making it the top choice for health-conscious consumers and celiac patients seeking familiar eating experiences with minimal dietary compromise.

- Retail Stores at 34.9%: Physical health-food and grocery stores remain the dominant channel due to impulse purchasing and the tactile product assessment consumers prefer when selecting specialty dietary products.

- Europe at 35.8%: Europe's high celiac disease diagnosis rates, strong regulatory framework for gluten-free labelling, and established specialty food culture create the most mature and largest regional market globally.

Gluten-Free Pasta Market Overview

The global gluten-free pasta market encompasses the manufacture and distribution of pasta products made from non-wheat ingredients for consumers with celiac disease, wheat allergy, or gluten sensitivity. The market includes rice, corn, millet, quinoa, and legume-based pasta across dry, fresh, and frozen formats.

The ecosystem integrates grain and ingredient suppliers, specialty food manufacturers, packaging providers, retail distributors, certification bodies, and foodservice operators. Macroeconomic factors include rising healthcare awareness, growing celiac disease diagnoses, expanding vegan and clean-label food trends, and increasing modern retail infrastructure globally.

Market Dynamics

To evaluate market opportunities, Request Sample

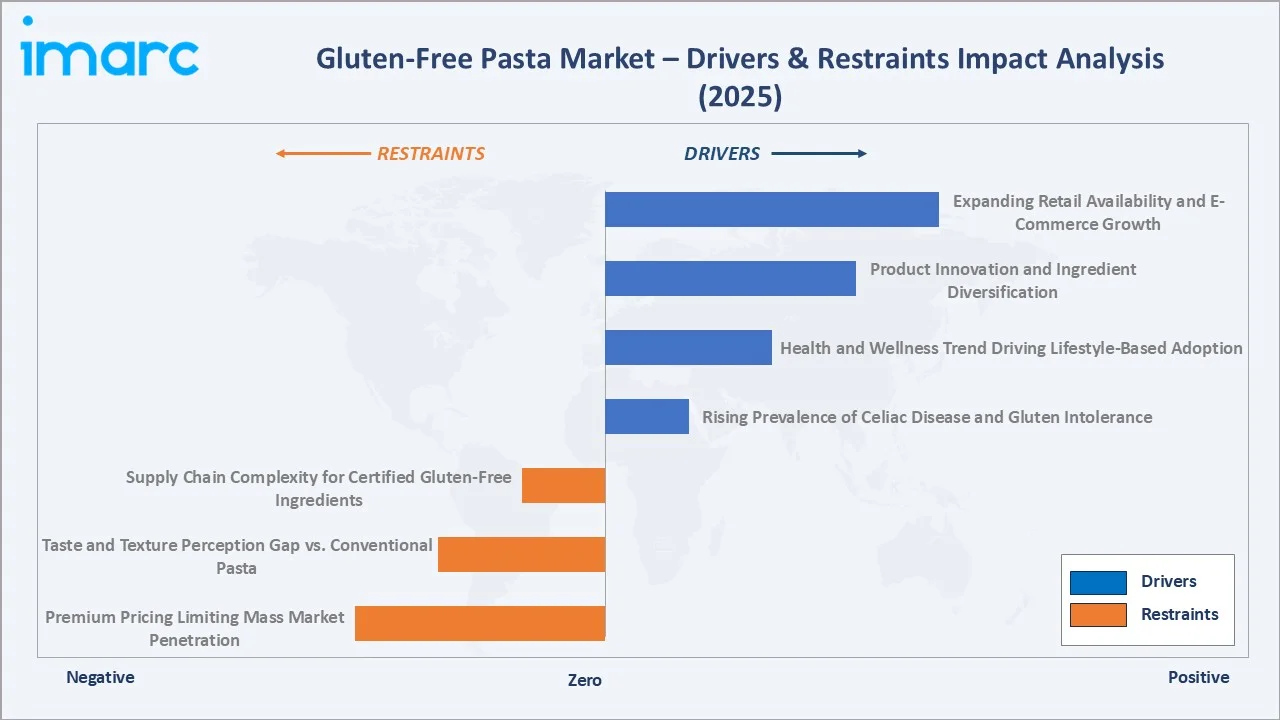

Market Drivers

- Rising Prevalence of Celiac Disease and Gluten Intolerance: Growing global awareness and diagnosis rates of celiac disease and non-celiac gluten sensitivity are directly expanding the addressable consumer base for gluten-free pasta. The Celiac Disease Foundation estimates 1 in 100 people worldwide are affected, creating sustained medically driven demand growth across all regions as clinical diagnosis infrastructure improves.

- Health and Wellness Trend Driving Lifestyle-Based Adoption: Beyond medical necessity, a growing segment of health-conscious consumers voluntarily adopts gluten-free diets, perceiving them as cleaner and healthier alternatives. This lifestyle-driven demand significantly expands the market beyond the core celiac patient population, creating incremental volume growth and premiumisation opportunities for manufacturers.

- Product Innovation and Ingredient Diversification: Manufacturers are expanding ingredient portfolios with millet, chickpea, lentil, and quinoa-based pasta variants, improving nutritional profiles and taste. Continuous innovation in extrusion and drying technologies has narrowed the texture gap between gluten-free and conventional pasta, removing a key adoption barrier and supporting penetration among non-celiac consumers.

- Expanding Retail Availability and E-Commerce Growth: Mainstream grocery chains globally have significantly expanded gluten-free product shelf space, while online specialty stores enable niche brands to reach consumers in markets with limited local availability. The rise of subscription meal kits and direct-to-consumer models has further accelerated distribution reach, particularly for premium and artisan gluten-free pasta brands.

Market Restraints

- Premium Pricing Limiting Mass Market Penetration: Gluten-free pasta typically commands a 2–3x price premium over conventional pasta due to higher ingredient costs, specialised manufacturing requirements, and smaller production volumes. This price differential restricts adoption among price-sensitive consumer segments in emerging markets, limiting the total addressable market and slowing volume growth in lower-income regions.

- Taste and Texture Perception Gap vs. Conventional Pasta: Despite improvement, a persistent consumer perception that gluten-free pasta offers inferior taste and texture compared to wheat-based alternatives limits trial and repeat purchase rates among non-celiac consumers. This sensory barrier particularly affects foodservice adoption, where consistency and palatability are critical to successful menu integration.

- Supply Chain Complexity for Certified Gluten-Free Ingredients: Maintaining certified gluten-free supply chains requires strict segregation protocols, dedicated processing facilities, and rigorous third-party testing, significantly increasing manufacturing costs. Sourcing certified gluten-free grains at scale remains challenging, particularly for millet and ancient grain varieties with fragmented supply bases.

Market Opportunities

- Millet and Ancient Grain Innovation for Premium Positioning: Millet, teff, amaranth, and sorghum-based pasta represent an underpenetrated premium segment with superior nutritional profiles and growing consumer interest in ancient grains. These variants command higher margins and align with clean-label and ancestral food trends, creating differentiation opportunities for manufacturers in increasingly competitive mainstream segments.

- Asia-Pacific Emerging Market Expansion: Rising celiac disease awareness in Japan, South Korea, and Australia, combined with expanding modern retail infrastructure in Southeast Asia and India, creates a substantial growth frontier. Localising product formats to suit Asian culinary traditions can accelerate penetration in this underpenetrated high-growth region.

Market Challenges

- Consumer Education Deficit in Emerging Markets: Limited awareness of celiac disease and gluten intolerance in many emerging markets suppresses diagnosis rates and restricts the addressable medical consumer base. Without robust clinical diagnosis infrastructure, primary demand remains lifestyle-driven, which is more price-sensitive and volatile than medically-driven purchasing behaviour.

- Private Label Competition Compressing Branded Margins: Major retailers including large supermarket chains have developed competitive private label gluten-free pasta lines at lower price points, intensifying pricing pressure on branded manufacturers. As the category matures, private label share expansion is compressing branded gross margins and increasing promotional intensity across key markets.

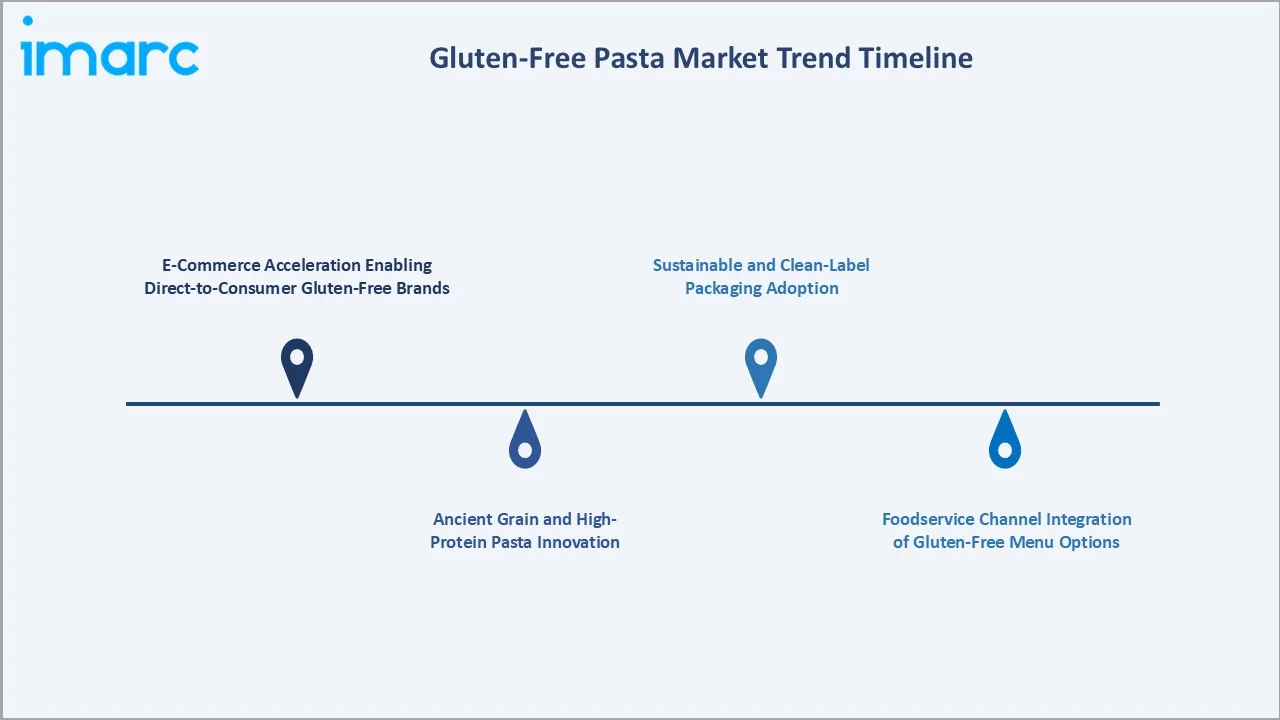

Emerging Market Trends

1. E-Commerce Acceleration Enabling Direct-to-Consumer Gluten-Free Brands

Online retail platforms and DTC subscription models are enabling specialist gluten-free pasta brands to build consumer relationships and achieve national distribution without traditional retail gatekeepers. In 2024, gluten-free food e-commerce grew approximately 18% year-on-year, driven by health-conscious millennial and Gen Z consumers preferring curated dietary products delivered to their homes.

2. Ancient Grain and High-Protein Pasta Innovation

Chickpea, lentil, and quinoa-based pasta variants are gaining consumer traction due to significantly higher protein content compared to traditional rice or corn gluten-free pasta. These products address the dual consumer demand for both gluten-free and high-protein nutrition, creating a fast-growing premium sub-segment within the broader gluten-free pasta category.

3. Foodservice Channel Integration of Gluten-Free Menu Options

Major restaurant chains and institutional foodservice operators are increasingly incorporating certified gluten-free pasta dishes into their menus, driven by growing consumer demand and liability concerns around allergen management. This structural shift is expanding the addressable market for gluten-free pasta beyond retail into the high-volume foodservice channel.

4. Sustainable and Clean-Label Packaging Adoption

Gluten-free pasta brands are adopting eco-friendly packaging and clean-label ingredient declarations as consumers increasingly align health-conscious food choices with environmental values. Brands combining certified gluten-free positioning with sustainable packaging and organic ingredient sourcing are achieving premium pricing and stronger retail positioning.

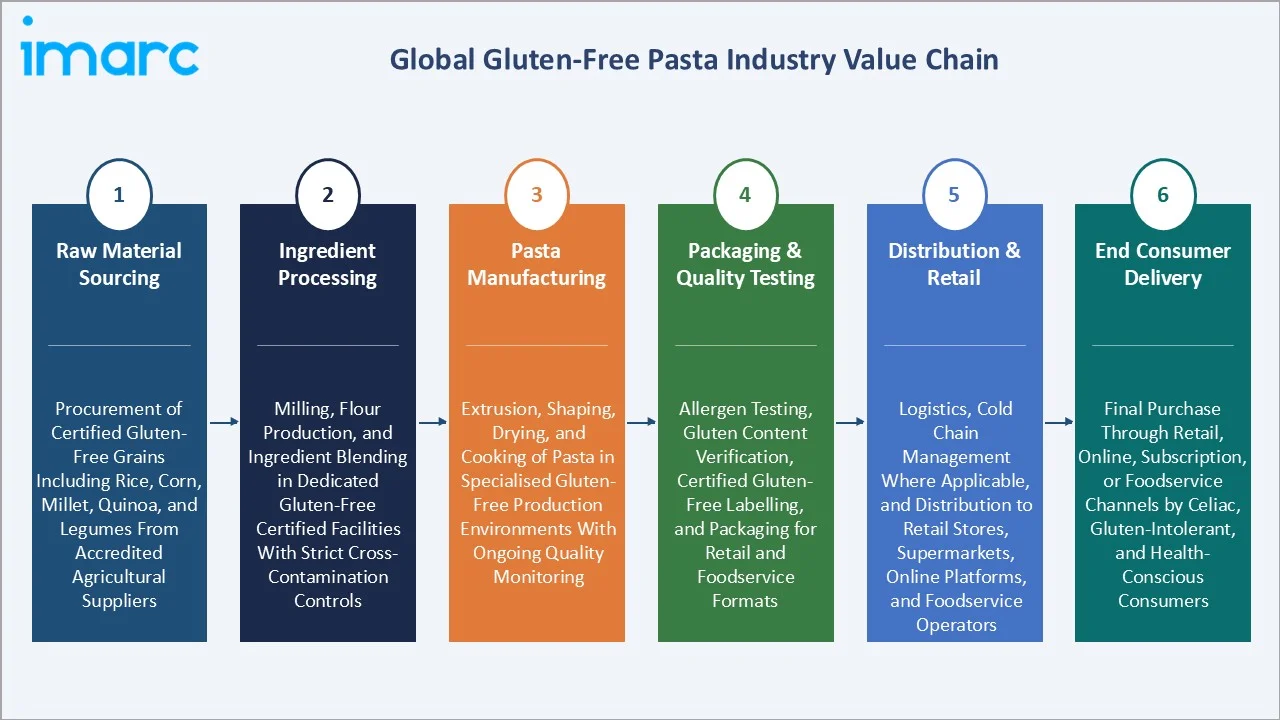

Industry Value Chain Analysis

The gluten-free pasta value chain integrates certified raw material sourcing, specialised ingredient processing, pasta manufacturing and quality testing, packaging and distribution, retail channel management, and consumer delivery. The value chain's key commercial differentiator is the certified gluten-free integrity maintained from farm to shelf.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Procurement of certified gluten-free grains including rice, corn, millet, quinoa, and legumes from accredited agricultural suppliers |

|

Ingredient Processing |

Milling, flour production, and ingredient blending in dedicated gluten-free certified facilities with strict cross-contamination controls |

|

Pasta Manufacturing |

Extrusion, shaping, drying, and cooking of pasta in specialised gluten-free production environments with ongoing quality monitoring |

|

Packaging & Quality Testing |

Allergen testing, gluten content verification, certified gluten-free labelling, and packaging for retail and foodservice formats |

|

Distribution & Retail |

Logistics, cold chain management where applicable, and distribution to retail stores, supermarkets, online platforms, and foodservice operators |

|

End Consumer Delivery |

Final purchase through retail, online, subscription, or foodservice channels by celiac, gluten-intolerant, and health-conscious consumers |

The raw material sourcing tier is the most commercially critical stage, as certified gluten-free grain supply chains require premium procurement relationships and strict quality standards. The ingredient processing stage is experiencing rapid technology investment as manufacturers seek to improve pasta texture and nutritional profiles to close the quality gap with conventional pasta.

Technology Landscape in the Gluten-Free Pasta Industry

High-Shear Extrusion Technology

Advanced high-shear extrusion technology enables consistent pasta shaping and texture development from alternative flour blends that lack the gluten network of conventional wheat pasta. Modern twin-screw extruders can process high-protein legume flours and ancient grain blends with precise temperature and pressure control, significantly improving the textural consistency of gluten-free pasta products.

Hydrocolloid Texture Enhancement Technology

Hydrocolloid ingredients, including xanthan gum, guar gum, and psyllium husk, are increasingly formulated into gluten-free pasta to replicate the binding and elasticity properties of gluten. Advanced hydrocolloid application technology enables manufacturers to achieve texture and cooking performance comparable to wheat pasta, addressing the primary barrier to non-celiac consumer adoption.

Continuous Drying and Moisture Control Technology

Precision drying technology with continuous moisture monitoring is critical for gluten-free pasta quality, as alternative flour blends exhibit different moisture absorption and drying behaviour compared to semolina wheat pasta. Advanced drying systems with automated humidity and temperature control reduce product breakage rates and improve shelf-life stability for gluten-free pasta manufacturers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Brown Rice Pasta |

🔒 |

2025 |

|

Type |

🔒 |

🔒 |

2025 |

|

Ingredient |

Rice |

42.6% |

2025 |

|

Distribution Channel |

Retail Stores |

34.9% |

2025 |

|

Region |

Europe |

35.8% |

2025 |

By Ingredient

The Rice segment leads at 42.6% in 2025, driven by superior taste, established supply chains, and strong consumer familiarity. Rice pasta is the most widely distributed and purchased gluten-free pasta format across all major retail channels globally.

To access detailed market analysis, Request Sample

Corn at 26.8% captures the North American mainstream consumer base through widely available branded products. Millet at 17.4% grows fastest at ~6.8% CAGR, fuelled by health trend migration toward ancient grains with superior micronutrient profiles. Others at 13.2% encompasses quinoa, chickpea, lentil, and blended flour variants at premium price points with strong DTC channel presence.

By Distribution Channel

Retail Stores lead at 34.9% in 2025, encompassing dedicated health-food retailers and natural grocery chains that serve as the primary channel for specialty dietary products. Supermarkets and Hypermarkets at 31.7% represent the channel with widest consumer reach through mass-market mainstream distribution.

Online Stores at 19.6% grow fastest at ~7.8% CAGR, driven by specialty e-commerce platforms and DTC brand models offering broader SKU variety than physical retail. Convenience Stores at 13.8% serve the impulse and on-the-go consumption occasion, primarily in urban markets where premium health-food positioning supports higher price points.

Regional Market Insights

|

Region |

Share (2025) |

Key Gluten-Free Pasta Market Drivers & Characteristics |

|

Europe |

35.8% |

Driven by high celiac disease diagnosis rates, strong regulatory gluten-free labelling framework, established specialty food retail, and major pasta manufacturers developing certified gluten-free product lines |

|

North America |

30.4% |

Driven by large health-conscious consumer base, high spending power, robust e-commerce infrastructure, and widespread mainstream grocery retailer adoption of gluten-free ranges |

|

Asia-Pacific |

22.3% |

Driven by rising celiac awareness in Japan and Australia, expanding modern retail in Southeast Asia, and growing health and wellness trend adoption among urban middle-class consumers |

|

Latin America |

6.4% |

Driven by growing awareness of gluten intolerance, increasing retail infrastructure, and rising disposable incomes in Brazil and Mexico supporting specialty food adoption |

|

Middle East and Africa |

5.1% |

Emerging with growing premium food retail, rising expatriate demand, and increasing lifestyle-driven dietary change among health-conscious consumers in GCC countries |

Europe at 35.8% leads through high clinical awareness, strong regulatory framework, and Italy's leadership in gluten-free pasta innovation. North America at 30.4% reflects the US market's health trend adoption and strong direct-to-consumer brand growth across speciality food categories.

Asia-Pacific at 22.3% represents the fastest-growing region, supported by rising celiac diagnosis infrastructure and modern retail expansion. Latin America at 6.4% and MEA at 5.1% are early-stage markets with long-term structural growth potential driven by urbanisation and rising health awareness.

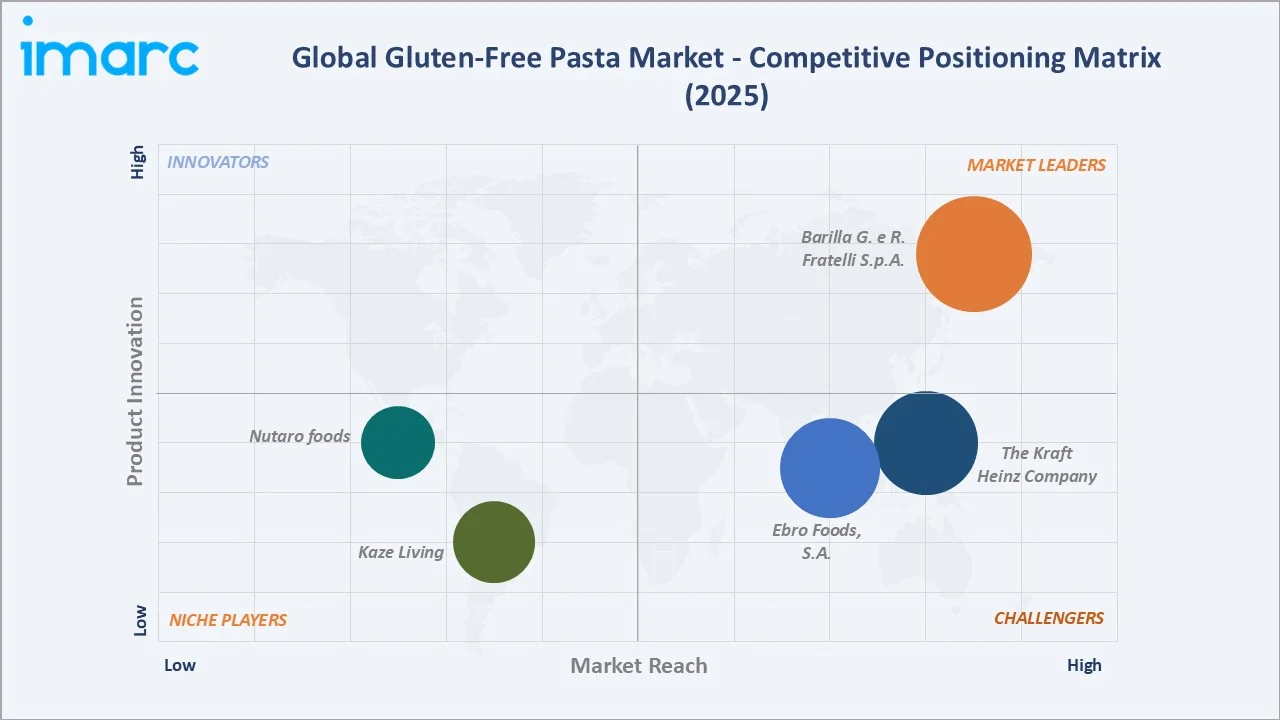

Competitive Landscape

The global gluten-free pasta market is fragmented, with established European pasta majors, dedicated gluten-free specialists, and health food brands competing across both premium and mass-market tiers. Product quality, certification credentials, distribution reach, and innovation capability shape the competitive landscape.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Barilla G. e R. Fratelli S.p.A. |

Gluten-Free Spaghetti, Penne, Fusilli |

Market Leader |

World's largest pasta brand with a mass-market gluten-free range distributed in numerous countries |

|

Ebro Foods, S.A. |

Garofalo Gluten-Free Pasta |

Strong Challenger |

Spanish food group with a premium Italian gluten-free pasta brand combining heritage and dietary innovation |

|

The Kraft Heinz Company |

Kraft Gluten Free Mac & Cheese |

Strong Challenger |

Large-scale distribution capability enabling mainstream retail penetration across multiple geographies |

|

Nutaro foods |

Gluten-Free Pasta |

Niche Player |

India-based dedicated gluten-free pasta manufacturer producing whole grain, high-protein pasta variants from a certified gluten-free facility |

|

Kaze Living |

Gluten-Free Pasta |

Niche Player |

India-based specialty food brand offering artisan gluten-free pasta alongside a broader health food portfolio |

Key players include Barilla G. e R. Fratelli S.p.A., Ebro Foods, S.A., The Kraft Heinz Company, Nutaro foods, Kaze Living, and others.

Key Company Profiles

Barilla G. e R. Fratelli S.p.A.

Barilla is an Italian multinational and the world's leading pasta manufacturer, with a significant gluten-free pasta portfolio distributed across more than 100 countries through mainstream grocery and online retail channels.

- Key Products: Gluten-Free Spaghetti, Penne, Fusilli

- Strategic Focus: Leveraging mainstream distribution scale to bring gluten-free pasta to mass-market price points while maintaining Italian quality heritage and achieving mainstream grocery shelf placement.

Ebro Foods, S.A.

Ebro Foods is a Spain-based global food group and one of the world's largest rice and pasta producers, with a significant gluten-free pasta presence through its Italian premium brand Garofalo (Pastificio Lucio Garofalo S.p.A.).

- Key Products: Garofalo Gluten-Free Pasta.

- Strategic Focus: Accelerating US market penetration through premium product innovation and retail expansion, leveraging Garofalo's Italian heritage and Gragnano provenance as key differentiators, while extending the brand into high-value adjacent segments, including high-protein and frozen premium pasta.

Market Concentration Analysis

The gluten-free pasta market is moderately fragmented, with the top 2-3 key players collectively accounting for an estimated 25-35% of global branded gluten-free pasta revenue. Dedicated gluten-free specialists hold strong positions in North America's premium natural food channel.

Private label gluten-free pasta accounts for an estimated 15-20% of global market volume and is growing as major retailers expand their own-brand specialty dietary ranges. Market concentration is declining over the forecast period as online-first brands and regional specialists gain distribution scale.

Investment & Growth Opportunities

Highest Growth Segments

Online Stores (~7.8% CAGR), Millet ingredient segment (~6.8% CAGR), Asia-Pacific regional market (~7.5% CAGR), premium ancient grain variants (~9-10% CAGR from a small base), and private label manufacturing for major retailers represent the highest-growth investment themes through 2034.

Emerging Investment Opportunities

Foodservice channel penetration represents an underpenetrated growth avenue, as gluten-free pasta adoption in restaurants and institutional catering remains significantly below retail levels. Quick-service restaurant chain partnerships and meal kit integration create scalable distribution expansion opportunities for volume gluten-free pasta manufacturers with consistent product performance.

Investment Themes

- Manufacturing scale-up for millet and ancient grain supply chains: Investment in certified gluten-free millet and quinoa ingredient supply chains creates a cost and quality advantage in the fastest-growing ingredient segment, enabling manufacturers to differentiate at premium price points.

- Asia-Pacific market entry through localised product development: Adapting gluten-free pasta formats to Asian cooking styles and regional retail distribution channels creates first-mover advantages in an underpenetrated high-growth market with structurally improving celiac diagnosis rates.

Future Market Outlook (2026-2034)

The global gluten-free pasta market is projected to grow from USD 1.40 Billion in 2025 to USD 2.36 Billion by 2034, delivering a 5.66% CAGR over the forecast period. The anchor value of USD 1.85 Billion in 2030 marks the market's transition from specialty niche to mainstream food category with broad retail availability and growing foodservice integration.

Three structural forces define gluten-free pasta market growth through 2034. Compounding celiac disease diagnosis growth creates a growing medically driven core demand base in all regions. Online retail expansion enables niche brands to reach underserved consumers globally. Product innovation reducing the taste and texture gap will convert lifestyle consumers into repeat purchasers, expanding the market well beyond medical necessity toward a broad healthy-eating category.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including food scientists, gluten-free brand managers, celiac disease clinical specialists, retail category managers, and foodservice distribution executives across major markets.

Secondary Research

Secondary research encompassed company annual reports, Celiac Disease Foundation global prevalence data, European Food Safety Authority gluten-free labelling standards, retail scanner data from major market research providers, and global gluten-free food industry reports. Over 50 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up model: (i) global celiac disease and gluten-sensitive population forecast by region; (ii) lifestyle adoption rate estimates by consumer segment; (iii) average consumer spend by channel and pasta format; (iv) technology and innovation premium adjustment for specialty ingredient variants and premium positioning.

Gluten-Free Pasta Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Brown Rice Pasta, Quinoa Pasta, Chickpea Pasta, Multigrain Pasta |

| Types Covered | Dried, Chilled/Fresh, Canned/Preserved |

| Ingredients Covered | Rice, Corn, Millet, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Retail Stores, Convenience Stores, Online Stores |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Barilla G. e R. Fratelli S.p.A., Ebro Foods S.A., The Kraft Heinz Company, Nutaro foods, Kaze Living, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the gluten-free pasta market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global gluten-free pasta market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the gluten-free pasta industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Gluten-Free Pasta Market Report

The global gluten-free pasta market reached USD 1.40 Billion in 2025, driven by rising celiac disease prevalence, health and wellness trends, and expanding mainstream retail distribution of gluten-free food products globally.

The gluten-free pasta market grows at 5.66% CAGR during 2026-2034, reaching USD 2.36 Billion by 2034. Growth reflects expanding medical demand, lifestyle adoption, product innovation, and e-commerce channel acceleration.

Rice leads at 42.6% in 2025, capturing mainstream consumer preference through superior taste profile and established production scale. Corn at 26.8% and Millet at 17.4% are the second and third largest ingredient segments respectively.

Retail Stores lead at 34.9% through dedicated health-food channels. Supermarkets and Hypermarkets at 31.7% offer the broadest consumer reach. Online Stores at 19.6% grow fastest at ~7.8% CAGR through expanding e-commerce penetration.

Europe leads at 35.8% through high celiac disease awareness, strong regulatory framework, and established gluten-free food culture. North America at 30.4% is the second largest market, driven by health-conscious consumers and strong specialty retail infrastructure.

Leading companies include Barilla G. e R. Fratelli S.p.A., Ebro Foods, S.A., The Kraft Heinz Company, Nutaro foods, Kaze Living, and others.

The gluten-free pasta market is projected to reach approximately USD 1.85 Billion by 2030, with online channel expansion, Asia-Pacific market growth, and millet-based product innovation driving above-market segment growth rates.

Online channel brand building, Asia-Pacific market entry, millet and ancient grain supply chain investment, foodservice channel penetration, and private label manufacturing for major retailers represent the leading investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)