India HVAC Market Size, Share, Trends and Forecast by Product Type, End User, and Region, 2026-2034

India HVAC Market Size, Share, Trends & Forecast (2026-2034)

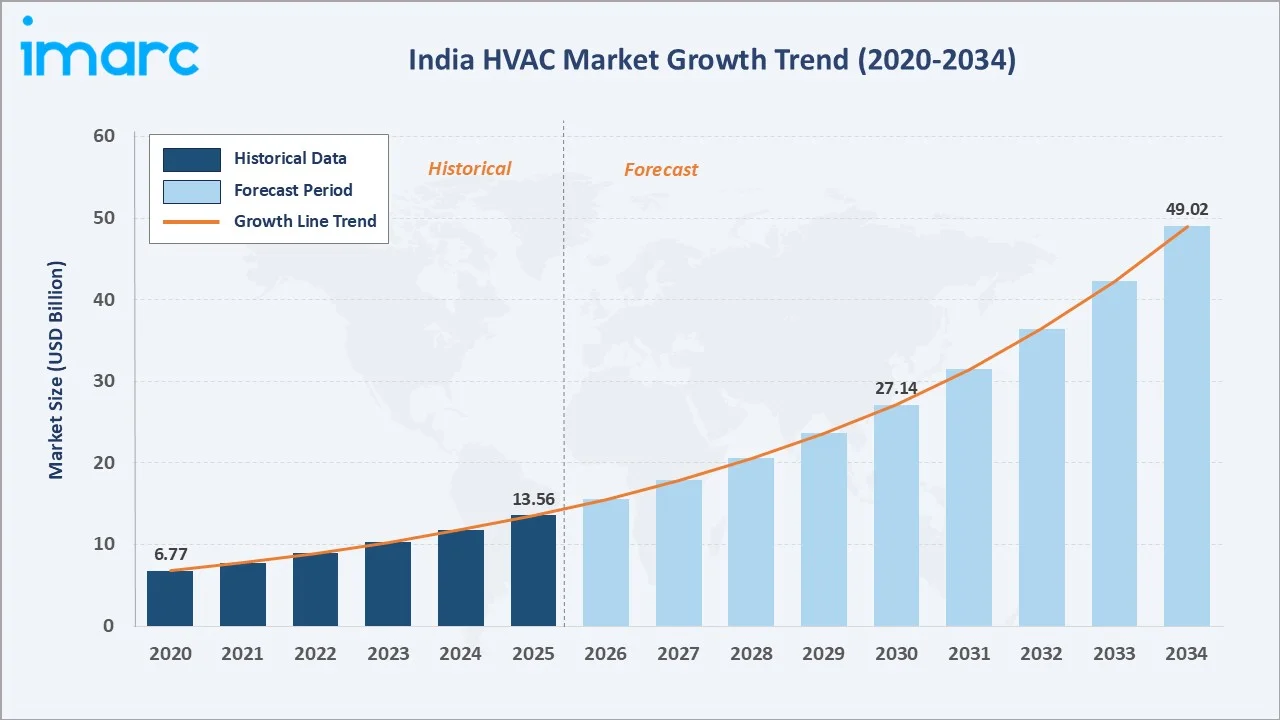

The India HVAC market was valued at USD 13.56 Billion in 2025 and is projected to reach USD 49.02 Billion by 2034, exhibiting a CAGR of 14.89% during 2026-2034. Rising heatwave intensity, with India recording around 536 heatwave days during summer 2024 according to the India Meteorological Department (IMD), rapid urbanization, growing disposable incomes, expanding commercial real estate, and supportive government efficiency programs are the primary drivers shaping the market growth.

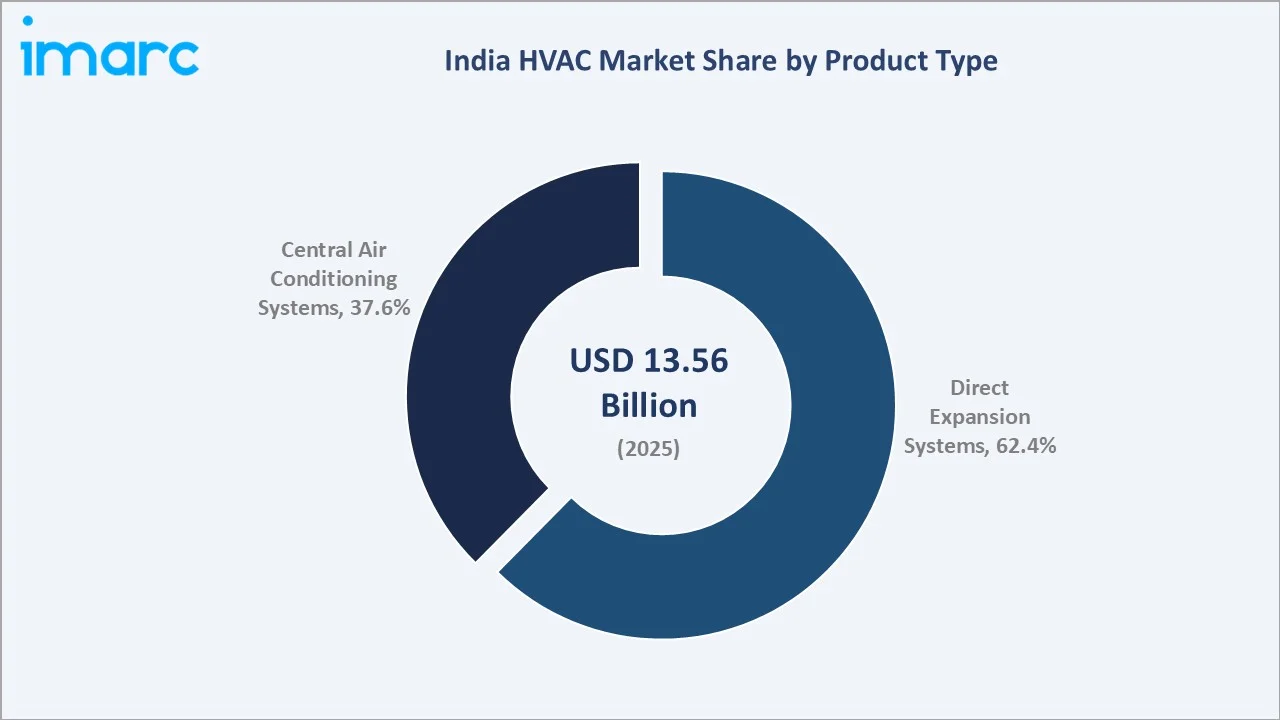

Direct expansion systems lead the product type segment at 62.4%, residential dominates the end user segment at 55.8%, and North India commands a 32.6% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 13.56 Billion |

|

Forecast Market Size (2034) |

USD 49.02 Billion |

|

CAGR (2026-2034) |

14.89% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

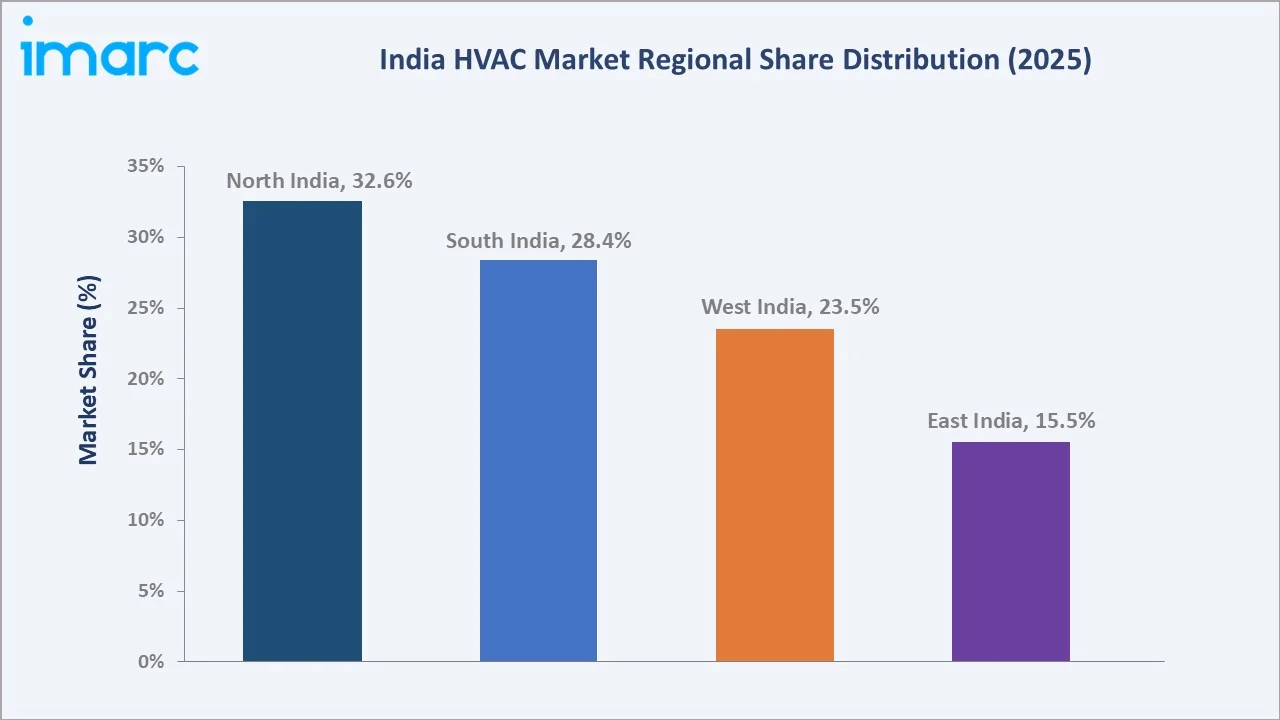

North India (32.6%, 2025) |

|

Fastest Growing Region |

South India (28.4%, 2025) |

|

Leading Product Type |

Direct Expansion Systems (62.4%, 2025) |

|

Leading End User |

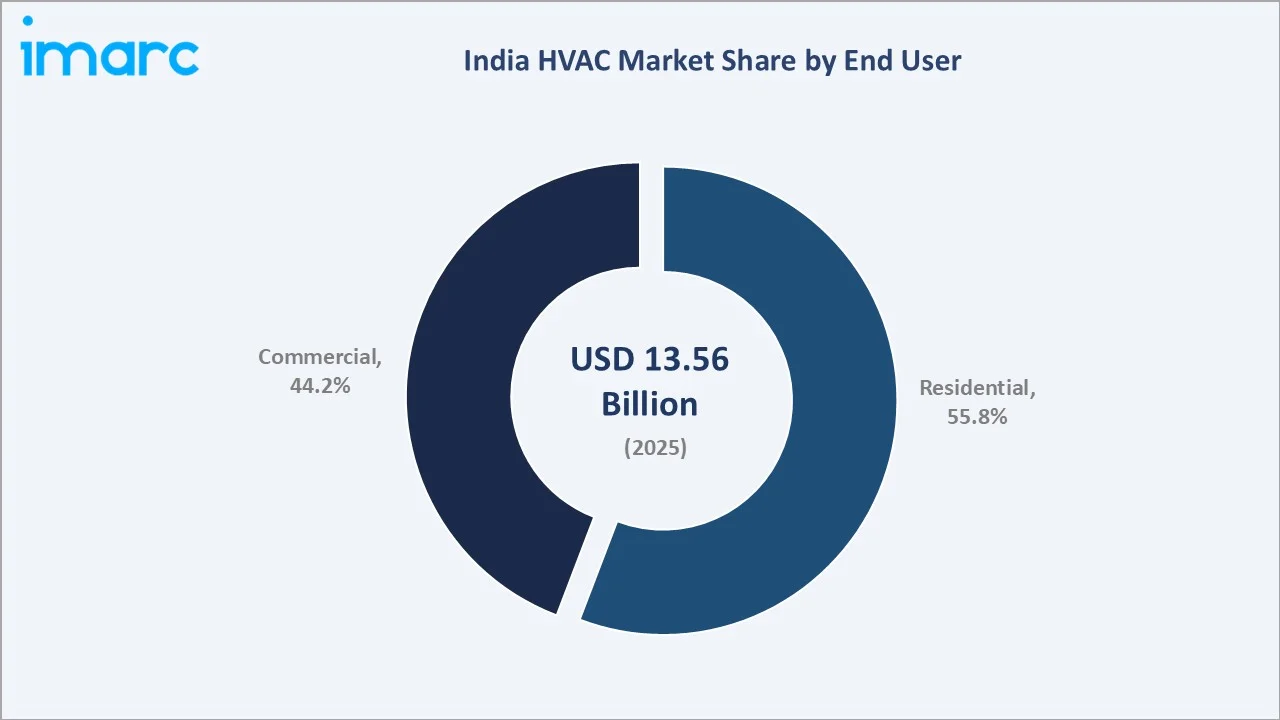

Residential (55.8%, 2025) |

The India HVAC market expanded from USD 6.77 Billion in 2020 to USD 13.56 Billion in 2025, supported by intensifying summer temperatures, faster urban housing rollouts, and growing penetration of inverter air conditioners. Anchored at USD 27.14 Billion in 2030, the forecast to USD 49.02 Billion by 2034 is supported by widening commercial cooling demand and steady residential uptake across tier-2 and tier-3 cities.

To get more information on this market, Request Sample

CAGR trajectories across the product type and end user sub-segments show that direct expansion systems and residential expand faster than the overall 14.89% market CAGR, supported by retail demand for split air conditioners, easy financing, and longer cooling seasons.

Executive Summary

The India HVAC market is on a strong growth path from USD 6.77 Billion in 2020 to USD 49.02 Billion by 2034. Air conditioning has shifted from a discretionary luxury to a near-essential household and workplace appliance, particularly in metro and tier-2 cities. Falling unit prices, easy EMI financing, and rising power efficiency standards are encouraging consumers to upgrade or buy first-time cooling systems.

Direct expansion systems dominate product type at 62.4% in 2025, supported by mass-market split and window air conditioner adoption across homes and small commercial premises. Residential leads the end user segment at 55.8%, fueled by rising household incomes, longer summers, and growing aspirations for indoor comfort. North India commands 32.6%, led by Delhi-NCR, Punjab, and Uttar Pradesh, where prolonged heat exposure and dense urban housing keep cooling demand high. In March 2026, Delhi recorded its warmest day of the year, with the temperature hitting 40.1 degrees Celsius in the Ridge area.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Direct Expansion Systems - 62.4% share (2025) |

|

Second Product Type |

Central Air Conditioning Systems - 37.6% share (2025) |

|

Leading End User |

Residential - 55.8% share (2025) |

|

Second End User |

Commercial - 44.2% share (2025) |

|

Leading Region |

North India - 32.6% share (2025) |

|

Fastest Growing Region |

South India - 28.4% share (2025) |

|

Top Companies |

Voltas, Daikin Industries, Ltd., Blue Star Limited, LG Electronics, Robert Bosch GmbH |

Key Analytical Observations Supporting the Above Data:

- Direct expansion systems dominance at 62.4% is supported by widespread household demand for split and window air conditioners, easy installation, and the affordability of inverter variants compared with centralized systems.

- Central air conditioning systems share at 37.6% is sustained by commercial real estate, hospitals, malls, hotels, and large institutional buildings that require centralized cooling for sustained loads and uniform indoor comfort.

- Residential leadership at 55.8% reflects rising disposable incomes, denser urban housing, and the increasing perception of cooling as a basic comfort rather than a luxury, especially in North India and West India. Voltas alone sold over 2 Million air conditioner units in FY 2024, the highest annual volume recorded by a single brand in India.

- Commercial share at 44.2% is supported by office space additions, retail expansion, hospitality investments, and growing healthcare infrastructure, with a strong shift toward variable refrigerant flow and energy-efficient chillers.

- North India at 32.6% leads owing to extreme summer temperatures, dense urban populations, and high HVAC penetration across both residential and commercial buildings, particularly in Delhi-NCR and major Punjab and Haryana cities.

India HVAC Market Overview

HVAC systems control indoor temperature, humidity, and air quality across residential, commercial, and industrial spaces in India. The category covers split and window air conditioners, variable refrigerant flow units, chillers, packaged units, air handling units, and smaller heating and ventilation products.

The Indian ecosystem links domestic component manufacturers, multinational OEMs, dealer and distributor networks, real-estate developers, EPC and MEP contractors, energy-efficiency regulators, and after-sales service partners. Macro-economic factors, including urbanization, rising household incomes, longer summer seasons, and government investment in smart cities and infrastructure, are shaping demand patterns across both household and commercial cooling.

Market Dynamics

To evaluate market opportunities, Request Sample

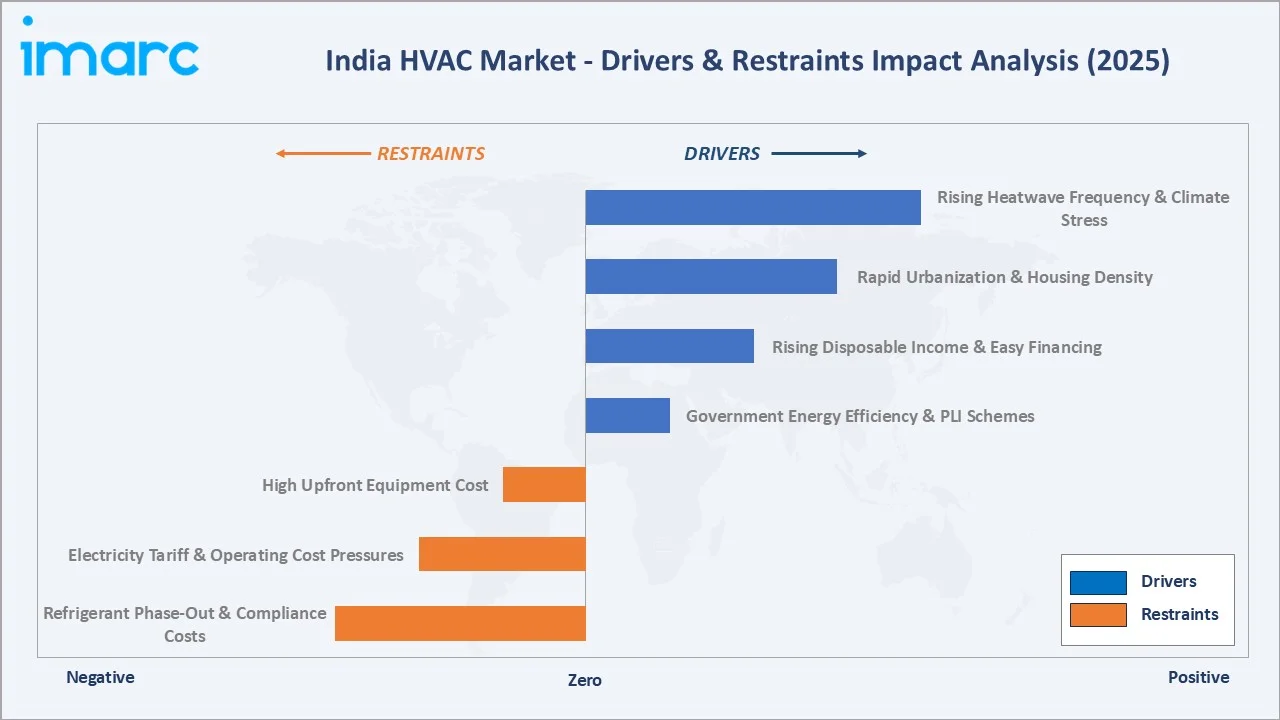

Market Drivers

- Rising Heatwave Frequency and Climate Stress: Increasing summer temperatures and longer heat seasons across India are turning HVAC ownership into a near-essential purchase, with cooling demand peaking from March to June each year. In 2025, India recorded its eighth hottest year ever, with the national average temperature being 0.28 degrees Celsius (°C) higher than the 1991-2020 Long Period Average (LPA), as per the Annual Climate Statement 2025 from IMD.

- Rapid Urbanization and Housing Density: City migration and tier-2 and tier-3 housing growth are driving steady demand for split air conditioners, packaged units, and centralized HVAC across new residential and mixed-use developments.

- Rising Disposable Income and Easy Financing: Higher household incomes and the spread of zero-cost EMI schemes are bringing first-time air conditioner ownership within reach for middle-income households across small cities.

- Government Energy Efficiency and PLI Schemes: BEE star labelling and the Production Linked Incentive (PLI) scheme for AC components are encouraging local manufacturing, supporting energy-efficient products, and reducing import dependency.

Market Restraints

- High Upfront Equipment Cost: Centralized chillers, variable refrigerant flow systems, and premium inverter air conditioners still represent a meaningful capital outlay for households and small businesses, slowing adoption in rural and lower-income segments.

- Electricity Tariff and Operating Cost Pressures: Air conditioning accounts for a significant share of summer power demand, and rising slab tariffs in metropolitan areas can discourage longer running hours and slow upgrade cycles in smaller homes.

- Refrigerant Phase-Out and Compliance Costs: The shift from legacy refrigerants to lower-GWP alternatives in line with environmental regulations is increasing product certification requirements and adding complexity to component sourcing for manufacturers and importers.

Market Opportunities

- Smart and Internet of Things (IoT)-Enabled HVAC: Wi-Fi-controlled units, voice-assistant integration, and AI-based climate optimization create premium-segment opportunities for OEMs targeting urban tech-savvy households and modern commercial buildings.

- Tier-2 and Tier-3 City Penetration: Smaller cities offer the largest untapped HVAC opportunity, supported by improving incomes, organized retail expansion, dealer-financed EMIs, and rising air conditioning awareness driven by hotter summers.

Market Challenges

- Skilled Installer and Service Workforce Shortage: Demand for trained technicians for installation, refrigerant handling, and maintenance is outpacing local availability in several states, slowing new project rollouts and after-sales service quality.

- Component Import Dependency: A meaningful share of compressors, controllers, and electronics is still imported, leaving manufacturers exposed to currency volatility, logistics disruptions, and tariff changes despite ongoing PLI-led localization.

Emerging Market Trends

1. Shift Toward Inverter and Energy-Efficient Air Conditioners

Inverter air conditioners have become the default purchase across urban India, replacing fixed-speed units owing to lower running costs, smoother temperature control, and better star ratings. Most leading brands offer inverter-only line-ups in the 1 Ton and 1.5 Ton categories. In Q1 2025, Samsung India doubled its room air conditioner sales by aggressively expanding its AI-enabled, inverter-driven AC portfolio, capturing 10% market share.

2. Rise of Smart, IoT, and AI-Enabled HVAC

Connected air conditioners with Wi-Fi control, voice-assistant integration, and AI-based climate sensing are gaining ground in metro cities. Brands are integrating smart home platforms, predictive maintenance alerts, and remote diagnostics to differentiate premium models and improve service economics.

3. Eco-Friendly Refrigerant Adoption

Manufacturers are accelerating the move from legacy refrigerants to lower-GWP alternatives in line with India's HFC phase-down obligations. Lower global warming potential, improved cooling efficiency, and emerging compliance norms are pushing OEMs to redesign compressors and heat exchangers for new refrigerants.

4. Centralized HVAC for Commercial Real Estate and Smart Cities

Large office complexes, hospitals, hotels, and metro rail projects are increasingly specifying variable refrigerant flow systems, water-cooled chillers, and integrated building management systems. Smart city projects are bundling centralized HVAC with energy management and indoor air quality monitoring as standard.

5. Local Manufacturing and PLI-Driven Component Localization

The PLI scheme is encouraging investment in compressors, motors, controllers, and copper tube facilities. This is strengthening domestic supply chains, reducing import dependence, and improving cost competitiveness for manufacturers.

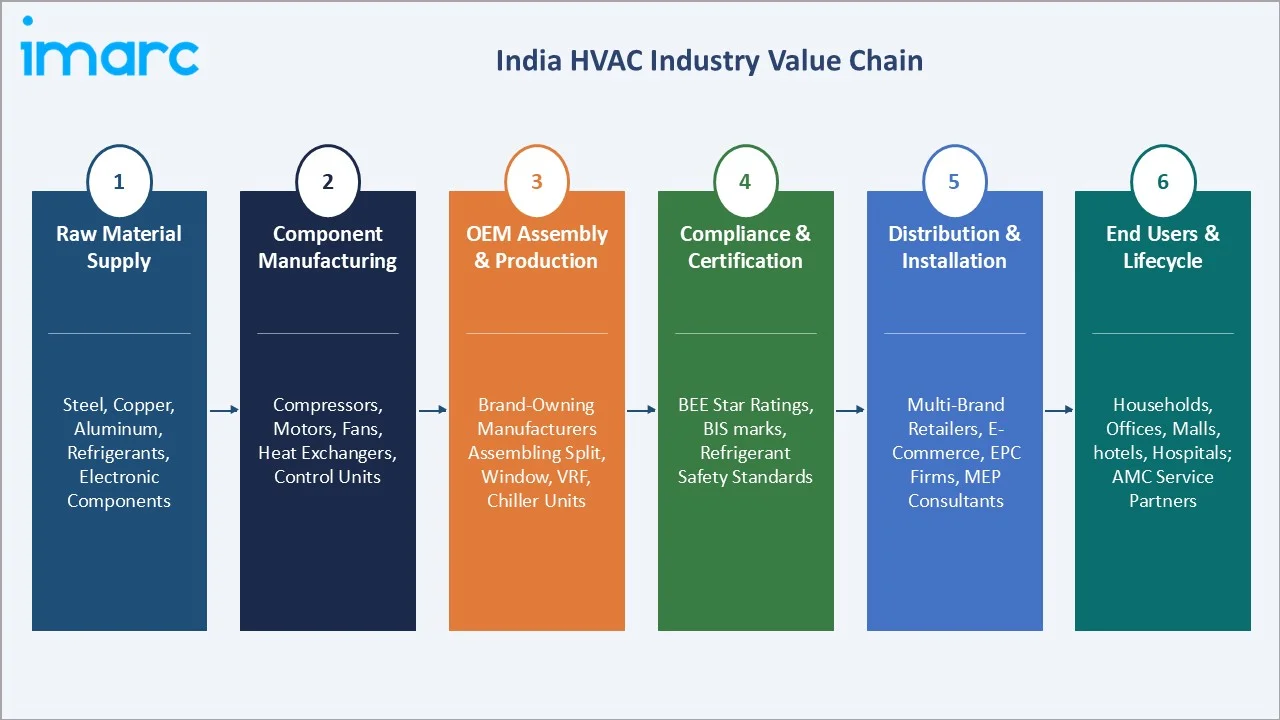

Industry Value Chain Analysis

The India HVAC value chain spans six stages from raw material sourcing through end-of-life service, with the highest value-add concentrated in component manufacturing, OEM assembly, and integrated system installation. Distributor networks and after-sales service capabilities create durable downstream advantages in this dealer-led category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of steel, copper, aluminum, refrigerants, and electronic components used in coils, cabinets, and circuit assemblies |

|

Component Manufacturing |

Compressor, motor, fan, heat-exchanger, and electronic control unit producers supplying both domestic OEMs and import-substituting PLI scheme participants |

|

OEM Assembly and Production |

Brand-owning manufacturers assembling split, window, packaged, VRF, and chiller units across plants in Tamil Nadu, Maharashtra, Andhra Pradesh, and Haryana |

|

Compliance and Certification |

BEE star ratings, Bureau of Indian Standards (ISI) marks, and refrigerant safety standards |

|

Distribution and Installation |

Multi-brand retailers, exclusive brand outlets, e-commerce platforms, electrical contractors, EPC firms, and MEP consultants for commercial and industrial projects |

|

End Users and Lifecycle |

Households, offices, malls, hotels, hospitals, transportation hubs, and industrial users; service partners handle installation, AMC, refrigerant top-up, and end-of-life recycling |

Vertically integrated players combine in-house compressor or assembly capabilities with extensive dealer and service networks to manage cost, quality, and delivery timelines, while specialist component makers and EPC firms support large commercial deployments.

Technology Landscape in the India HVAC Industry

Inverter and Variable Speed Compressor Technology

Inverter compressors that vary speed based on cooling load have become the mainstream technology for residential air conditioners, delivering quieter operation, smoother temperature control, and significant power savings versus fixed-speed units. Most premium models combine dual-rotor compressors with smart sensors to optimize part-load efficiency.

Eco-Friendly Refrigerants and Heat Exchangers

Manufacturers are transitioning from legacy refrigerants to lower global warming potential alternatives, alongside redesigned copper or aluminum heat exchangers. These changes are enhancing energy efficiency while aligning Indian products with international compliance norms.

Smart Connectivity and AI-Driven Climate Control

Wi-Fi-enabled air conditioners with mobile-app control, voice integration, and AI-based occupancy and weather sensing are gaining ground in urban homes. Manufacturers are layering predictive maintenance, energy-tracking dashboards, and remote diagnostics on top of cloud platforms for premium positioning.

Building Automation and Centralized HVAC

Variable refrigerant flow systems, smart chillers, and integrated building management systems are increasingly specified for new commercial projects. These platforms coordinate cooling, ventilation, and indoor air quality across zones, supporting energy savings and compliance with Energy Conservation Building Code requirements.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Direct Expansion Systems | 62.4% | 2025 |

| End User | Residential | 55.8% | 2025 |

| Region | North India | 32.6% | 2025 |

By Product Type

Direct expansion systems command a 62.4% majority share in 2025, driven by mass-market split, window, and packaged air conditioners across residential and small commercial premises. These systems offer lower upfront costs, easier installation, and broad availability through dealer and online channels.

To access detailed market analysis, Request Sample

Central air conditioning systems at 37.6% in 2025 serve commercial real estate, hospitals, hotels, malls, and industrial facilities that require uniform cooling across large floorplates. Variable refrigerant flow units, water-cooled chillers, and packaged rooftop systems anchor demand in this segment.

By End User

Residential dominates with a 55.8% share in 2025, reflecting rising household incomes, denser urban housing, and the perception of air conditioning as a comfort necessity rather than a luxury. Tier-1 metros lead absolute volumes, while tier-2 and tier-3 cities are accelerating fastest in incremental adoption.

Commercial accounts for 44.2% in 2025, supported by expanding office space, retail malls, hospitality investments, and healthcare infrastructure. Variable refrigerant flow units, chillers, and packaged HVAC platforms anchor demand across IT parks, large institutional buildings, and metro rail and airport projects.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

32.6% |

Extreme summer heat, dense urban housing, large institutional and commercial cooling load |

|

South India |

28.4% |

Strong IT and commercial real estate growth, rising residential demand in coastal and tier-2 cities |

|

West India |

23.5% |

Industrial growth, premium residential demand, large hospitality and retail HVAC requirements |

|

East India |

15.5% |

Expanding tier-2 city housing, growing healthcare and education infrastructure, rising humidity-driven demand |

North India at 32.6% in 2025 leads the country, supported by extreme summer temperatures across Delhi-NCR, Punjab, and Uttar Pradesh, dense urban populations, and high HVAC penetration in both residential and commercial buildings. Strong real-estate activity and large-scale infrastructure projects further reinforce regional demand.

South India at 28.4% is the fastest-growing region through 2034, driven by Bengaluru, Hyderabad, and Chennai's IT and commercial real estate expansion, alongside rising household cooling demand in tier-2 cities, such as Coimbatore, Kochi, and Visakhapatnam.

Competitive Landscape

The India HVAC market is moderately fragmented, with a few homegrown leaders and global majors holding the largest share of brand awareness, dealer reach, and after-sales coverage. Channel depth, energy efficiency credentials, and price-tier coverage form the core competitive moats, while service network density distinguishes commercial-segment leaders.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

| Voltas | Ultra-slim One-Way Cassette AC, 4 Way Cassette AC |

Leader |

Dealer-led residential strategy, value-pricing, and Tata-group brand trust |

| Daikin Industries, Ltd. | Daikin VRV Alpha, Daikin FTKL UV Series |

Leader |

Premium inverter and VRF technology, in-house compressor manufacturing |

| Blue Star Limited | Blue Star, Iconia S Series |

Leader |

Strong commercial HVAC focus, deep service network, growing residential portfolio |

|

LG Electronics |

LG AI+ DUAL inverter split air conditioners, |

Leader |

Premium inverter line-up, smart connectivity, broad consumer durables presence |

|

Robert Bosch GmbH |

Hitachi | Challenger | Engineering-driven mid-premium positioning, integrated commercial HVAC solutions |

Key players include Voltas, Daikin Industries, Ltd., Blue Star Limited, LG Electronics, and Robert Bosch GmbH, among others.

Key Company Profiles

Voltas

Voltas is one of the largest air conditioner firms in India, with an extensive dealer footprint across both metro and tier-2 cities and a strong presence in cooling products, engineering projects, and commercial refrigeration.

- Product Portfolio: Ultra-slim One-Way Cassette AC, 4 Way Cassette AC, inverter and adjustable inverter range, commercial cooling products, and water and air purifiers across the Voltas brand.

- Recent Developments: In December 2024, Voltas reintroduced its famous All-Weather winter campaign across North India, mainly through Digital platforms and Radio, aiming to generate interest in its All-Weather Hot & Cold AC offering, while highlighting its effectiveness in various weather conditions.

- Strategic Focus: Value-led residential pricing, deep multi-brand dealer relationships, expansion of inverter and energy-efficient ranges, and continued investments in domestic manufacturing capacity.

Daikin Industries, Ltd.

Daikin Industries, Ltd. is recognized as a technology leader in inverter air conditioning, variable refrigerant flow systems, and commercial chillers, supported by multiple production plants in the country. The company continues to strengthen its market presence through localized manufacturing and a wide distribution network.

- Product Portfolio: Split inverter air conditioners, ducted systems, VRV and VRF systems, large chillers, air handling units, and ventilation products across the Daikin brand for residential and commercial use.

- Recent Developments: Daikin Industries, Ltd. is expanding its footprint in India through capacity additions, localization of key components, and a stronger focus on energy-efficient and smart HVAC solutions tailored to evolving market demand.

- Strategic Focus: Premium technology positioning, in-house compressor and component manufacturing, expansion of VRV and chiller installations across commercial real estate, and growing exports from India.

Blue Star Limited

Blue Star Limited is a leading Indian HVAC and commercial refrigeration company with a strong presence in central air conditioning, room air conditioners, and engineering projects, supported by an extensive service network across the country.

- Product Portfolio: Split and window inverter air conditioners including the premium Iconia series (S Series), ducted systems, VRF systems, chillers, packaged air conditioners, and commercial refrigeration solutions under the Blue Star brand.

- Recent Developments: For Summer 2026, Blue Star Limited launched a comprehensive range of 125 new room air conditioner models, including the premium Iconia series, with manufacturing capacity scaled to 1.8 million units across facilities in Andhra Pradesh and Himachal Pradesh and distribution through over 10,000 outlets nationwide.

- Strategic Focus: Leadership in commercial central air conditioning, deep service network, growing residential portfolio, and continued investments in energy-efficient and inverter products.

Market Concentration Analysis

The India HVAC market is moderately concentrated, with the top five companies (Voltas, Daikin Industries, Ltd., Blue Star Limited, LG Electronics, and Robert Bosch GmbH) estimated to account for a meaningful majority of installed-capacity share in 2025, particularly in the room air conditioner segment.

Barriers to entry include energy-efficiency certifications, multi-year dealer-channel building, multiyear warranty and service network requirements, and the capital intensity needed to localize compressors, motors, and electronic controls. These dynamics favor well-capitalized incumbents and global majors with deep manufacturing footprints.

Consolidation is accelerating through joint ventures, parent-level acquisitions, and component-localization investments. Scale advantages in manufacturing, distribution, and after-sales service are reinforcing the competitive position of established players, while smaller regional brands compete primarily on price-to-feature ratio in entry-level segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Direct expansion systems at 62.4% and the residential end user segment at 55.8% expand faster than the overall 14.89% market CAGR through 2034, supported by mass-market split air conditioner adoption and rising disposable incomes. Variable refrigerant flow systems within central air conditioning are expected to outpace traditional chillers in commercial buildings.

Emerging Markets

South India at 28.4% is the highest-growth region, with Bengaluru, Hyderabad, and Chennai leading commercial demand. North and west India offer the largest untapped premium opportunities as rising affordability, longer summers, and easy financing unlock first-time air conditioner ownership across tier-2 and tier-3 cities.

Venture & Investment Trends

Capital is concentrated in compressor and component manufacturing under the PLI scheme, energy-efficient inverter platforms, IoT and AI-enabled connected HVAC, and centralized building management systems. Investment is also flowing into refrigerant transition, after-sales service technology, and electric mobility-linked HVAC for buses and metro projects.

Future Market Outlook (2026-2034)

The India HVAC market is forecast to expand from USD 13.56 Billion in 2025 to USD 49.02 Billion by 2034 at a CAGR of 14.89%, adding roughly USD 35.5 Billion in incremental annual market value over the forecast period. Anchored at USD 27.14 Billion in 2030, the market is expected to shift further toward inverter and energy-efficient models.

Four forces will shape the market through 2034: continued inverter and IoT adoption; the transition to lower global warming potential refrigerants; deeper localization of compressors and components under the PLI scheme; and rising centralized HVAC demand from commercial real estate, hospitality, and smart-city projects.

By 2034, air conditioners are expected to be installed in a substantially higher share of urban and emerging-city households, while VRF systems and smart chillers become the default specification for new commercial buildings. Tier-2 and tier-3 cities are likely to emerge as the largest incremental volume contributors.

Research Methodology

Primary Research

Primary research included interviews with senior product managers at leading HVAC manufacturers, dealer-channel partners, EPC and MEP contractors, real-estate developers, and household and commercial buyers, validating market sizing, regional demand, product-type mix, and end user adoption patterns.

Secondary Research

Secondary sources included industry association data, regulatory filings, Bureau of Energy Efficiency publications, India Cooling Action Plan documents, government PLI scheme disclosures, listed-company annual reports, investor presentations, and trade press.

Forecasting Models

Market forecasts used top-down and bottom-up models combining household penetration rates, commercial floor-space additions, average installed price per ton, replacement cycles, and regulatory transition timelines. Scenario analysis addressed power tariff variation, refrigerant compliance costs, and tier-wise income growth assumptions.

India HVAC Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Direct Expansion Systems, Central Air Conditioning Systems |

| End Users Covered | Residential, Commercial |

| Regions Covered | North India, South India, East India, West India |

| Comapnies Covered | Voltas, Daikin Industries, Ltd., Blue Star Limited, LG Electronics, Robert Bosch GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India HVAC market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India HVAC market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India HVAC industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India HVAC Market Report

The India HVAC market was valued at USD 13.56 Billion in 2025, supported by rising heatwaves, urbanization, growing disposable incomes, and expanding commercial real estate.

The market is projected to grow at 14.89% CAGR from 2026 to 2034, reaching USD 49.02 Billion, supported by inverter adoption, smart cooling, and commercial HVAC demand.

Direct expansion systems lead at 62.4% in 2025, driven by mass-market split and window air conditioner adoption. Central air conditioning systems hold the remaining 37.6% share.

Residential dominates at 55.8% in 2025, supported by rising household incomes and longer summers. Commercial accounts for 44.2%, driven by offices, malls, hospitals, and hospitality.

North India commands 32.6% in 2025, driven by high urban density, extreme seasonal temperature variations, and strong demand from residential and commercial segments across key states. South India at 28.4% is the fastest-growing region through 2034.

Leading players include Voltas, Daikin Industries, Ltd., Blue Star Limited, LG Electronics, and Robert Bosch GmbH.

Inverter adoption is driven by lower running costs, smoother temperature control, BEE star labelling reforms, and consumer focus on energy savings during long summer seasons.

Smart air conditioners with Wi-Fi, voice control, and AI-based climate sensing are gaining ground in metros, supporting premium-segment growth and new service-revenue models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)