India Medical Tourism Market Size, Share, Trends and Forecast by Treatment Type and Region, 2026-2034

India Medical Tourism Market Size, Share, Trends & Forecast (2026-2034)

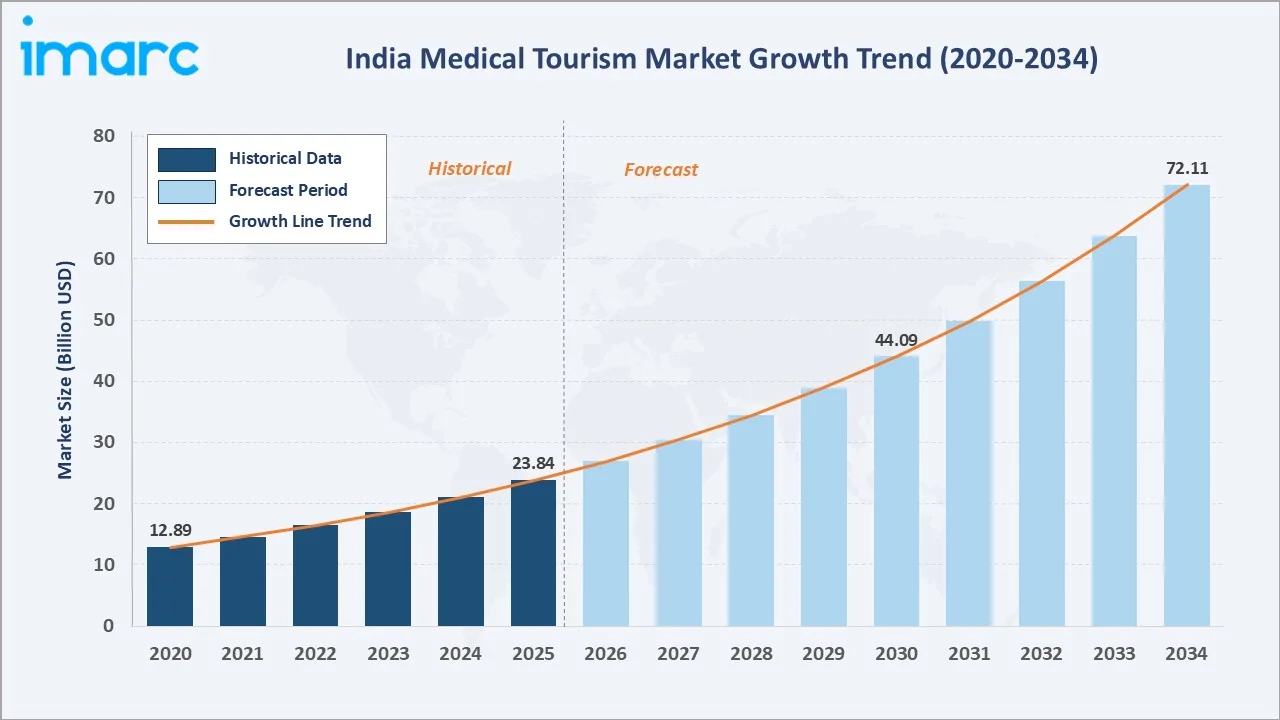

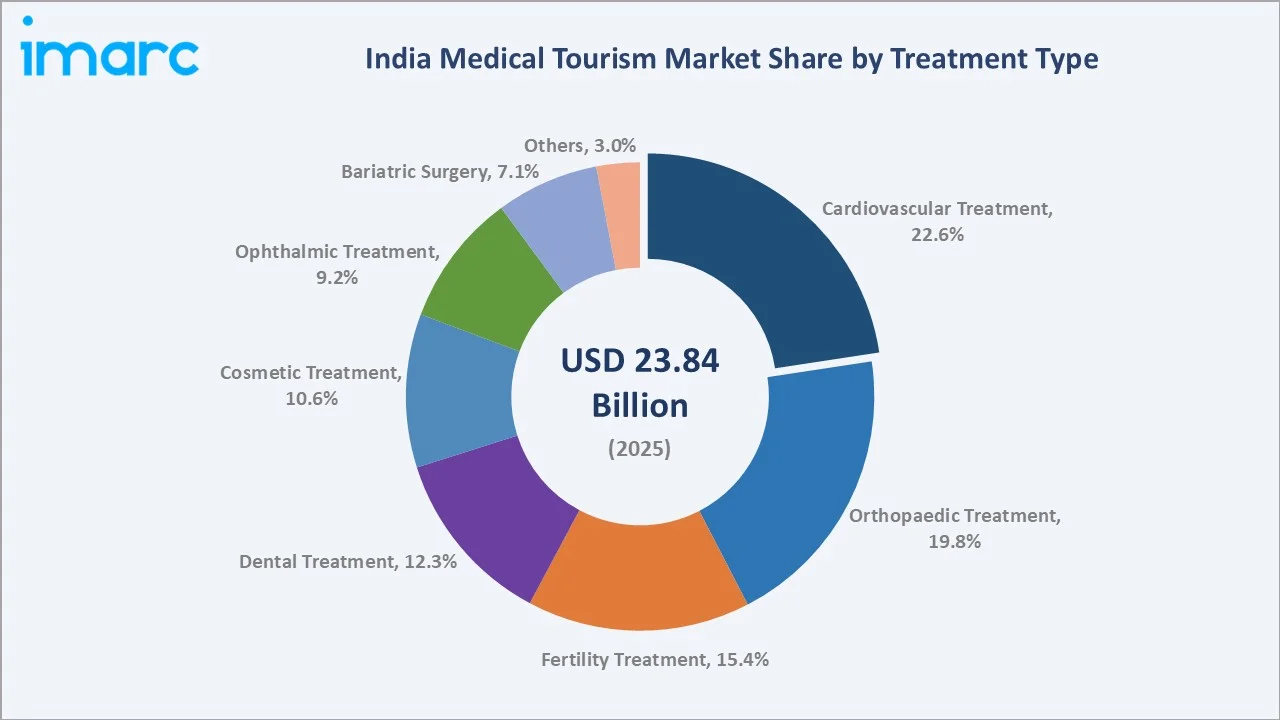

The India medical tourism market reached USD 23.84 Billion in 2025 and is projected to reach USD 72.11 Billion by 2034, growing at a CAGR of 13.09% during 2026-2034. The market is driven by cost-effective medical treatments, JCI-accredited hospital infrastructure, and the government's Heal in India initiative.

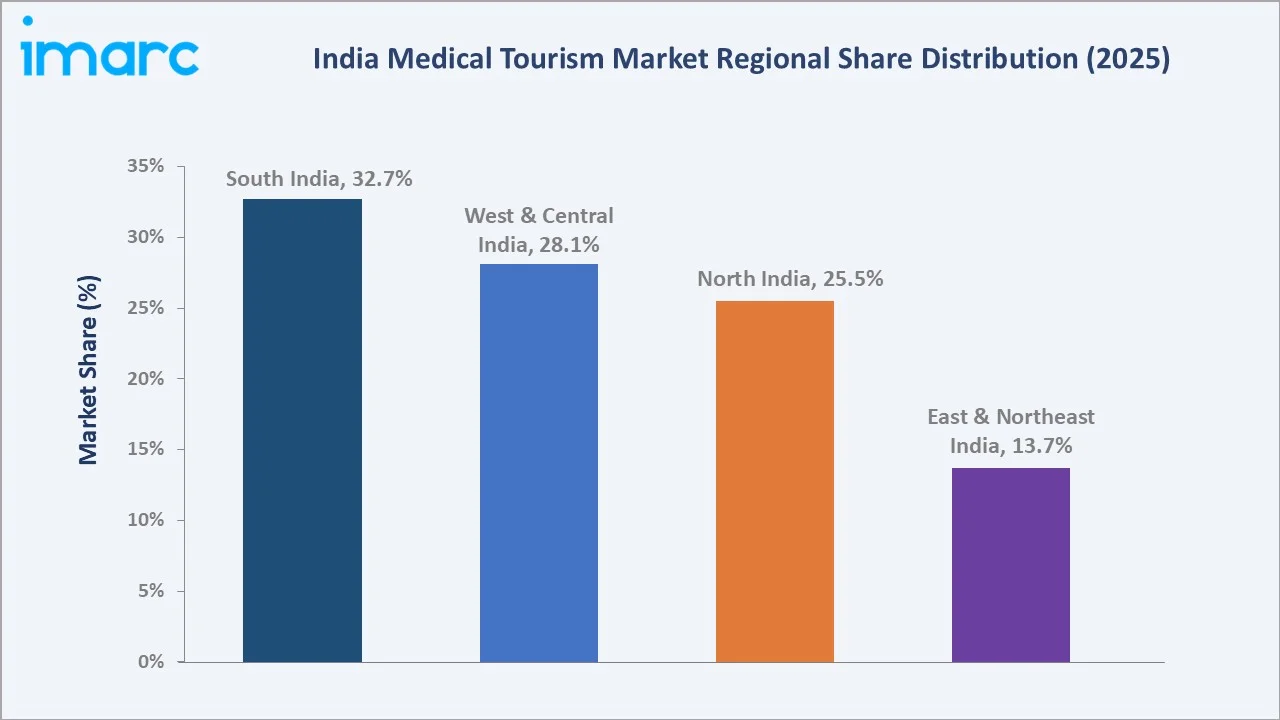

Cardiovascular treatment leads at 22.6%. South India commands 32.7% of the regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 23.84 Billion |

|

Forecast Market Size (2034) |

USD 72.11 Billion |

|

CAGR (2026-2034) |

13.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Treatment Type |

Cardiovascular Treatment (22.6%, 2025) |

|

Second Largest Treatment Type |

Orthopaedic Treatment (19.8%, 2025) |

|

Leading Region |

South India (32.7%, 2025) |

The market expanded from USD 12.89 Billion in 2020 to USD 23.84 Billion in 2025, anchored at USD 44.09 Billion in 2030, and forecast to reach USD 72.11 Billion by 2034. India's 60–90% cost advantage over Western benchmarks, expanding accredited hospital network, and government medical visa facilitation drive structural market growth.

To get more information on this market, Request Sample

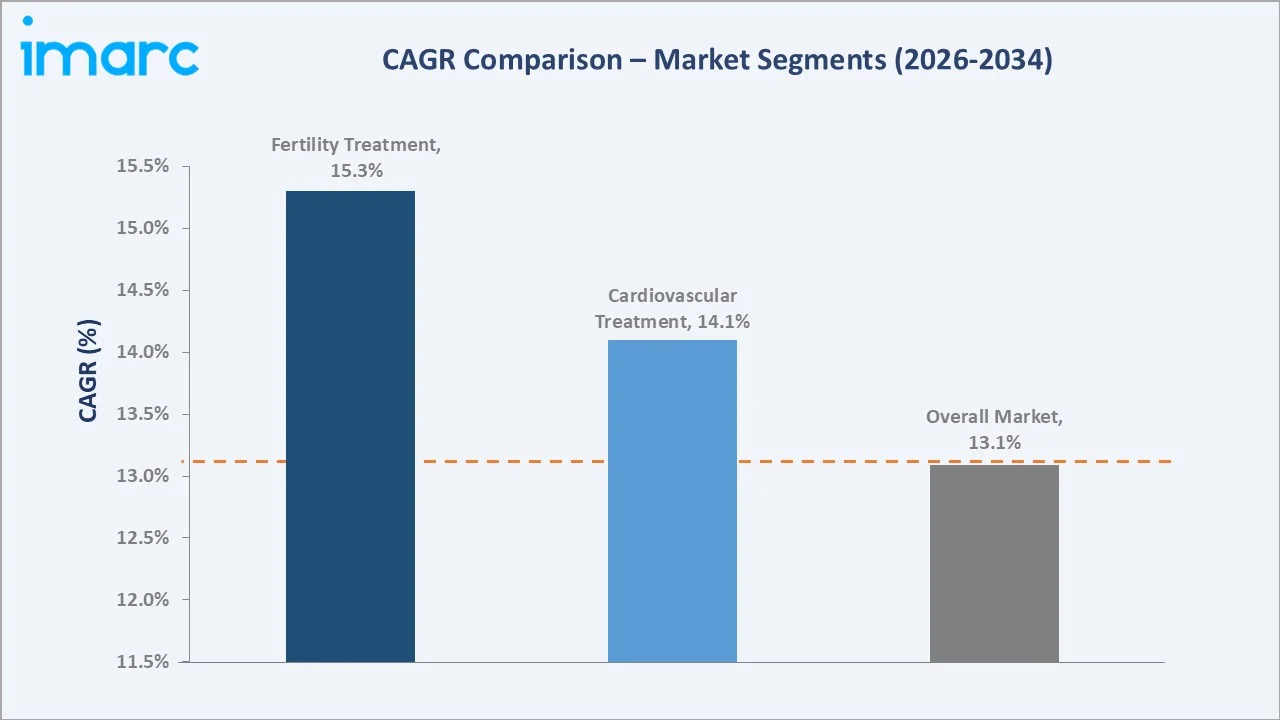

Fertility treatment grows fastest at ~15.3% CAGR as India's IVF cost competitiveness (USD 2,500–4,000 per cycle versus USD 12,000–15,000 in the US) attracts patients from Southeast Asia, Africa, and the Middle East. Cardiovascular treatment at ~14.1% CAGR reflects India's sustained cardiac surgery cost and quality advantage.

Executive Summary

The India medical tourism market reached USD 23.84 Billion in 2025, representing one of the world's fastest-growing medical tourism markets. India offers cost-effective treatment options while maintaining internationally recognized standards of care. The market is projected to reach USD 72.11 Billion by 2034, growing at a CAGR of 13.09%.

Cardiovascular treatment at 22.6% dominates in India's cardiac surgery cost advantage. Orthopaedic treatment at 19.8% captures joint replacement and spine surgery demand. South India at 32.7% leads through Chennai, Bengaluru, and Hyderabad's concentration of internationally accredited tertiary-care facilities.

Key Market Insights

|

Insight |

Data |

|

Dominant Treatment Type |

Cardiovascular Treatment – 22.6% share (2025) |

|

Second Largest Segment |

Orthopaedic Treatment – 19.8% market share (2025) |

|

Leading Region |

South India – 32.7% market share (2025) |

|

Market Opportunity |

IVF/fertility tourism; Ayurveda wellness integration; telemedicine pre/post care; digital patient facilitation platforms |

Key Analytical Observations Supporting The Above Data:

- Cardiovascular Treatment at 22.6%: India's cardiac surgery costs are 80–90% lower than those in the United States and Europe. Chennai, Bengaluru, and New Delhi's cardiac centres consistently achieve international clinical outcome benchmarks, sustaining cardiovascular treatment's market leadership.

- Orthopaedic Treatment at 19.8%: India's orthopaedic segment captures joint replacement, spinal surgery, and sports medicine demand from Middle Eastern, African, and Southeast Asian patients, where orthopaedic wait times and cost barriers are significant.

- South India at 32.7%: South India leads through various leading hospitals, which collectively form India's highest concentration of internationally accredited tertiary-care facilities, attracting medical tourists.

India Medical Tourism Market Overview

The India medical tourism market encompasses all medical treatment and healthcare services consumed by international patients traveling to India for clinical procedures, diagnostics, inpatient and outpatient services, and treatment-linked travel arrangements. The market spans cardiovascular, orthopaedic, fertility, dental, cosmetic, ophthalmic, and bariatric treatment categories.

The ecosystem integrates government regulatory bodies, hospital and healthcare providers, medical tourism facilitators, travel and hospitality service providers, insurance and third-party administrators, and digital patient coordination platforms. Macroeconomic factors include rising healthcare costs in developed nations, India's clinical cost advantage, expanding accreditation, and the government medical visa policy.

Market Dynamics

To evaluate market opportunities, Request Sample

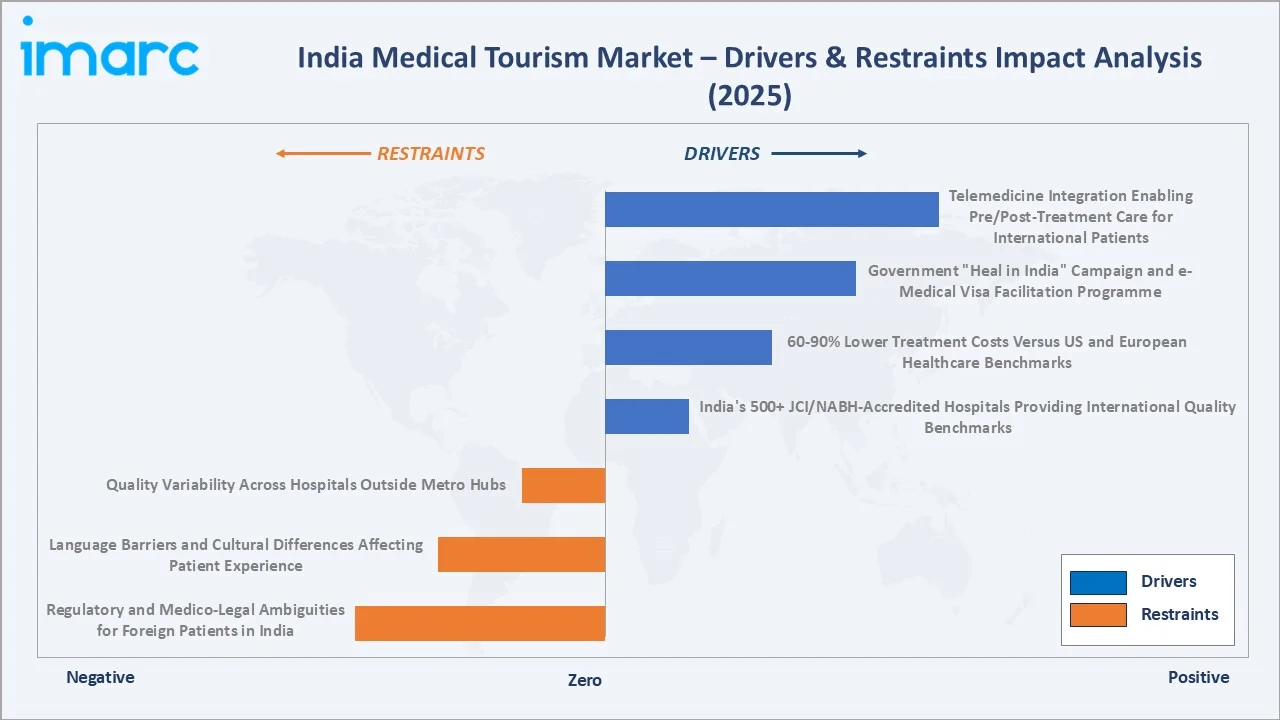

Market Drivers

- India's 500+ JCI/NABH-Accredited Hospitals Providing International Quality Benchmarks: India's rapidly expanding network of JCI and NABH-accredited hospitals provides international patients with verified clinical quality confidence. Over 50 Indian hospitals hold JCI accreditation, and more than 700 are NABH-accredited, providing quality assurance infrastructure comparable to leading global medical tourism destinations.

- 60-90% Lower Treatment Costs Versus US and European Healthcare Benchmarks: Healthcare services in India are generally available at significantly lower costs compared to many developed healthcare markets, while maintaining recognized standards of medical care. This cost advantage, combined with expanding healthcare infrastructure, skilled medical professionals, and increasing availability of advanced treatments, continues to attract both domestic and international patients across a wide range of medical specialties.

- Government "Heal in India" Campaign and e-Medical Visa Facilitation Programme: The Indian government's Heal in India initiative, simplified e-medical visa process, and single-window medical visa facilitation are reducing patient journey friction and attracting higher international patient volumes.

- Telemedicine Integration Enabling Pre/Post-Treatment Care for International Patients: India's leading hospitals have integrated telemedicine platforms enabling remote pre-surgical consultation, digital diagnostic review, and post-treatment follow-up care for international patients across time zones, reducing pre-travel barriers and improving the overall medical tourism value proposition.

Market Restraints

- Regulatory and Medico-Legal Ambiguities for Foreign Patients in India: Inconsistent regulatory frameworks governing medical tourism and ambiguous medico-legal recourse for foreign patients experiencing adverse outcomes create institutional risk for international patient confidence, limiting India's systematic attraction of risk-averse patient source markets.

- Language Barriers and Cultural Differences Affecting Patient Experience: Language barriers and cultural differences create patient experience challenges for non-English-speaking medical tourists from Southeast Asian, African, and Middle Eastern populations. Limited multilingual patient coordination infrastructure outside premium hospitals restricts India's addressable market in high-potential source regions.

- Quality Variability Across Hospitals Outside Metro Hubs: Significant quality variability between accredited tertiary hospitals and secondary-tier facilities creates reputational risk for India's medical tourism brand. Adverse outcomes at non-accredited facilities can disproportionately impact India's overall medical tourism perception in key international source markets.

Market Opportunities

- Fertility and IVF Medical Tourism Expansion: India's IVF success rates and cost structure create a high-growth fertility medical tourism opportunity. Demand from Southeast Asia, Africa, and the Middle East is expanding as awareness of India's fertility treatment capability grows.

- Ayurveda and Wellness Tourism Integration: India's unique Ayurveda, yoga, and wellness treatment heritage creates a differentiated medical tourism value proposition unavailable elsewhere globally. Integrating traditional wellness treatments with clinical medical tourism programmes creates a holistic care proposition attracting higher-value international patients.

Market Challenges

- Competition from Emerging Medical Tourism Destinations in Southeast Asia and the Middle East: Thailand, Malaysia, Turkey, and the UAE are expanding internationally accredited hospital capacity and aggressively marketing medical tourism programmes, directly competing with India for international patient flows in cardiovascular, orthopaedic, and cosmetic treatment categories.

- Infrastructure and Connectivity Gaps Outside Metropolitan Healthcare Hubs: Medical tourism demand is concentrated in six to eight metropolitan hospital clusters, with limited international patient infrastructure in tier-2 destinations. This geographic concentration limits India's capacity utilisation expansion and creates access barriers for patients in regions with limited direct air connectivity.

Emerging Market Trends

1. AI-Powered Diagnostics and Robotic Surgery Adoption in Leading Hospitals

India's leading hospitals are deploying AI-powered diagnostic systems and robotic surgical platforms that enable remote pre-surgical consultation, computer-aided diagnostics, and minimally invasive precision surgery.

2. Medical Tourism Facilitator Platform Digitalization

Digital medical tourism facilitation platforms aggregating hospital accreditation data, treatment pricing benchmarks, specialist availability, and patient reviews are transforming the international patient journey. These platforms reduce facilitator costs, improve price transparency, and enable direct hospital-to-patient engagement across multiple source markets simultaneously.

3. Wellness and Ayurveda Tourism Integration with Clinical Medical Tourism

India's medical tourism providers are integrating Ayurveda, yoga, naturopathy, and preventive health programmes alongside conventional clinical treatments, creating holistic health tourism packages. This wellness integration creates a differentiated value proposition attracting health-conscious international visitors seeking combined medical treatment and restorative wellness experiences.

4. Africa and CIS Market Expansion as New Medical Tourism Source Regions

Indian hospitals are actively expanding into African, Central Asian, and CIS patient markets as Western Asian patient flows normalise. Targeted patient coordination programmes in Kenya, Tanzania, Ethiopia, Uzbekistan, and Kazakhstan are creating new medical tourism source market diversification, reducing India's historical dependence on Bangladesh and Gulf patient inflows.

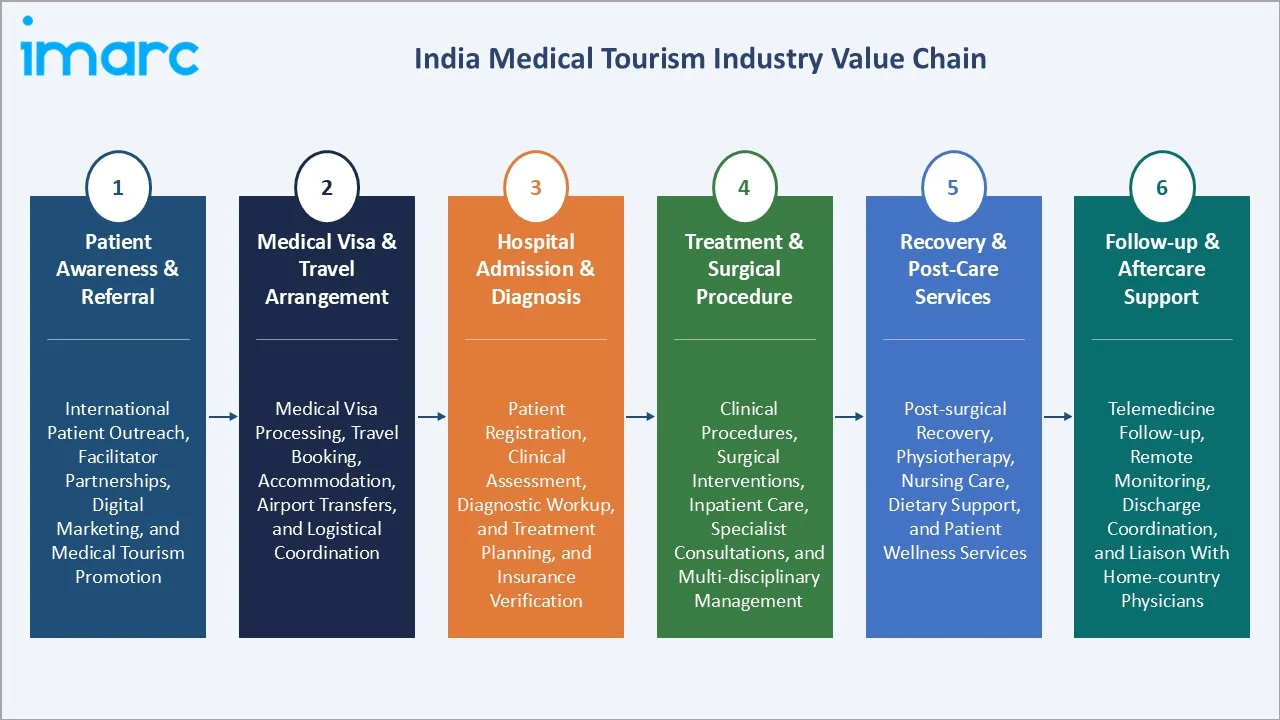

Industry Value Chain Analysis

The India medical tourism value chain integrates patient awareness and international referral, medical visa and travel arrangement, hospital admission and diagnosis, treatment and surgical procedure delivery, recovery and post-care services, and follow-up aftercare support. The commercial architecture integrates hospital providers, facilitators, and ancillary hospitality service providers.

|

Stage |

Key Activities |

|

Patient Awareness & Referral |

International patient outreach, facilitator partnerships, digital marketing, and medical tourism promotion |

|

Medical Visa & Travel Arrangement |

Medical visa processing, travel booking, accommodation, airport transfers, and logistical coordination |

|

Hospital Admission & Diagnosis |

Patient registration, clinical assessment, diagnostic workup, treatment planning, and insurance verification |

|

Treatment & Surgical Procedure |

Clinical procedures, surgical interventions, inpatient care, specialist consultations, and multi-disciplinary management |

|

Recovery & Post-Care Services |

Post-surgical recovery, physiotherapy, nursing care, dietary support, and patient wellness services |

|

Follow-up & Aftercare Support |

Telemedicine follow-up, remote monitoring, discharge coordination, and liaison with home-country physicians |

The hospital admission and treatment delivery tier is the value chain's highest-value stage. The follow-up and aftercare tier is experiencing rapid digitalization through telemedicine, creating a post-discharge care continuum that differentiates India's medical tourism proposition.

Technology Landscape in the India Medical Tourism Industry

Robotic Surgery Technology

Robotic-assisted surgery using da Vinci and other platforms is widely deployed in India's leading medical tourism hospitals across cardiac, orthopaedic, and urological procedures. Over 170 da Vinci systems serve Indian hospitals with 850+ trained surgeons, enabling minimally invasive precision surgery that reduces recovery times and improves clinical outcomes for international patients.

Telemedicine and Digital Health Platforms

Telemedicine platforms enabling video consultations, remote diagnostic review, and digital health record exchange between Indian specialists and international patients are reducing pre-travel barriers and enabling post-discharge care continuity. Digital health platforms with multilingual patient communication and hospital booking are improving the end-to-end international patient experience.

AI-Powered Diagnostic and Imaging Systems

Apollo Hospitals deployed advanced AI imaging analytics across the nation, enabling remote second-opinion services for international patients and accelerating pre-surgical diagnostic timelines. AI-powered diagnostic systems for cardiac imaging and orthopaedic analysis improve clinical accuracy and strengthen India's credibility among international patient communities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Treatment Type |

Cardiovascular Treatment |

22.6% |

2025 |

|

Region |

South India |

32.7% |

2025 |

By Treatment Type

The cardiovascular treatment segment leads at 22.6% in 2025, encompassing cardiac bypass surgery, heart valve replacement, angioplasty, and related cardiac interventions at a fraction of Western healthcare costs. India's cardiac surgery outcomes are comparable to leading international benchmarks, driving sustained international patient inflows for high-complexity cardiac procedures.

To access detailed market analysis, Request Sample

Orthopaedic treatment at 19.8% captures joint replacement, spinal surgery, and sports injury demand. Fertility treatment at 15.4% is the fastest growing at ~15.3% CAGR. Dental at 12.3%, cosmetic at 10.6%, ophthalmic at 9.2%, and bariatric surgery at 7.1% complete the landscape. Others account for 3.0%.

Regional Market Insights

|

Region |

Share (2025) |

Key Medical Tourism Market Drivers & Characteristics |

|

South India |

32.7% |

Driven by internationally accredited hospital concentration in Chennai, Bengaluru, and Hyderabad with strong cardiac, orthopaedic, and oncology capabilities attracting international patients from Southeast Asia and West Asia |

|

West & Central India |

28.1% |

Led by Mumbai and Pune's premium specialty hospitals with strong international connectivity and cosmetic, fertility, and cardiac treatment demand from international patients |

|

North India |

25.5% |

Anchored by Delhi NCR's Medanta, Max Healthcare, Apollo, and Fortis hospitals with strong cardiovascular and orthopaedic capabilities drawing Central Asian and West Asian patients |

|

East & Northeast India |

13.7% |

Emerging market anchored by Kolkata's hospital base, serving neighbouring countries with growing cardiac and oncology capabilities as the market develops |

South India, at 32.7%, leads through Apollo, Fortis Malar, Narayana Health, Manipal, and KIMS hospitals. West & Central India, at 28.1%, reflects Mumbai's Kokilaben Dhirubhai Ambani, Wockhardt, and P.D. Hinduja hospital strength.

North India, at 25.5%, captures Delhi NCR's Medanta The Medicity, Max Healthcare, and Apollo's international patient programme strength. East & Northeast India, at 13.7%, represents the market's emerging growth frontier, with Kolkata's hospitals historically serving Bangladesh before geopolitical disruptions accelerated diversification.

Competitive Landscape

The India medical tourism market competitive landscape is moderately concentrated with large hospital chains, specialty hospital networks, and medical tourism facilitators competing across cardiovascular, orthopaedic, fertility, and other treatment categories. Large hospital chains dominate through scale, accreditation, and international patient programme infrastructure.

|

Company Name |

Key Services |

Market Position |

Core Strength |

|

Apollo Hospitals |

Cardiac surgery, oncology, transplants, orthopaedics, fertility, neurosciences |

Market Leader |

India's largest hospital chain with the highest JCI-accredited facility count and the broadest international patient programme |

|

IHH Healthcare Berhad |

Cardiac, orthopaedic, neurology, oncology, organ transplantation |

Market Leader |

Executing its ACE strategy (Accelerate, Capitalize, Enhance) in India by integrating Fortis and Gleneagles operations, consolidating high-yield clusters in Delhi-NCR and Mumbai |

|

Narayana Hrudayalaya Ltd |

Cardiac surgery, haematology, bone marrow transplantation, oncology |

Strong Challenger |

Globally recognised cardiac surgery at significantly lower cost, attracting international patients from Africa and developing economies |

|

Max Healthcare |

Cardiac, oncology, orthopaedic, neurology |

Strong Challenger |

Northern India's largest hospital network with rapidly expanding international patient programme across West Asia and Africa |

|

MEMG |

Orthopaedic, cardiac, transplants, oncology |

Strong Challenger |

South India's leading multi-specialty hospital chain with strong international patient capabilities across Bengaluru and Hyderabad |

Key players include Apollo Hospitals, IHH Healthcare Berhad, Narayana Hrudayalaya Ltd, Max Healthcare, MEMG, and others.

Key Company Profiles

Apollo Hospitals

Apollo Hospitals is India's largest and most internationally recognised private hospital chain, with a dominant position in India's medical tourism market through its multi-specialty hospital network, comprehensive international patient programme, and the highest concentration of JCI-accredited facilities in India.

- Key Products: Cardiac surgery, oncology, organ transplantation, orthopaedics, fertility treatment, and neurosciences.

- Strategic Focus: Expanding international patient programme across West Asia, Southeast Asia, Africa, and CIS markets through digital health platform deployment and targeted geographic patient acquisition.

Narayana Hrudayalaya Ltd

Narayana is a Bengaluru-based hospital chain globally recognised for high-quality cardiac surgery delivered at significantly lower cost than comparable global benchmarks, attracting international patients from Africa, Southeast Asia, and developing economies for complex cardiac procedures.

- Key Products: Cardiac surgery, haematology, bone marrow transplantation, oncology, and organ transplants.

- Strategic Focus: Expanding internationally accessible cardiac surgery capacity and broadening the specialist clinical programme into oncology and organ transplantation to capture a wider international patient treatment profile.

Market Concentration Analysis

The India medical tourism market is moderately concentrated. The top 3 players collectively account for approximately 35–45% of India's organised medical tourism revenue. Further, the next top 3-4 players account for an additional 20–25%. Smaller specialty hospitals, Ayurveda and wellness centres, and dental and cosmetic clinic networks account for the remaining market share.

Investment & Growth Opportunities

Highest Growth Segments

Fertility treatment at ~15.3% CAGR, bariatric surgery at ~14.6% CAGR, cardiovascular treatment at ~14.1% CAGR, and telemedicine-integrated pre/post care platforms represent the highest-growth investment vectors through 2034. Africa and CIS patient market development programmes represent the highest-potential geographic growth investment opportunity.

Emerging Investment Opportunities

Digital medical tourism facilitation platforms aggregating accreditation data, pricing transparency, and multilingual patient coordination represent a high-growth technology investment opportunity. Ayurveda and wellness tourism integration with clinical medical tourism programmes creates a differentiated value proposition investable across South India's established wellness tourism infrastructure.

Investment Themes

- Tertiary Hospital Capacity Expansion in Tier-2 Healthcare Destinations: India's medical tourism market is geographically concentrated in six metropolitan clusters. Investment in internationally accredited tertiary-care hospital capacity in tier-2 destinations with direct international air connectivity can expand India's medical tourism capacity and reduce metropolitan cluster congestion.

- Africa and CIS Medical Tourism Patient Acquisition Infrastructure: Africa and CIS represent India's highest-potential emerging patient source markets. Investment in local-language patient coordination offices, referral hospital partnerships, and digital health platforms targeting these communities creates a scalable, long-term patient acquisition infrastructure, diversifying India's geographic dependency.

Future Market Outlook (2026-2034)

The India medical tourism market is projected to grow from USD 23.84 Billion in 2025 to USD 72.11 Billion by 2034, delivering a 13.09% CAGR. India's sustained cost competitiveness, expanding internationally accredited hospital network, and government policy support through the Heal in India initiative create a structural growth foundation through 2034.

Three structural forces define India medical tourism market growth through 2034. Rising healthcare costs and wait times in developed nations create a persistent demand for cost-competitive Indian medical tourism. Expanding digital health infrastructure reduces pre-travel friction and post-discharge barriers. Africa and CIS market development creates an additive patient source market growth above historically dominant West Asian and South Asian inflow channels.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including hospital international patient programme directors, medical tourism facilitators, government healthcare policy officials, insurance and TPA executives, and international patient coordinators across India's major medical tourism hubs.

Secondary Research

Secondary research encompassed hospital annual reports and international patient programme disclosures; India Ministry of Health and Family Welfare healthcare data; India Tourism Statistics international patient data; NABH and JCI hospital accreditation databases; medical tourism industry association reports; and healthcare market intelligence publications. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using international patient flow bottom-up model: (i) annual international patient inflow to India by source country and treatment type; (ii) average revenue per international patient by treatment category; (iii) hospital network capacity expansion adjustments; (iv) government policy impact multipliers for medical visa facilitation and Heal in India programme.

India Medical Tourism Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Treatment Types Covered | Cosmetic Treatment, Dental Treatment, Cardiovascular Treatment, Orthopaedic Treatment, Bariatric Surgery, Fertility Treatment, Ophthalmic Treatment, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Apollo Hospitals, IHH Healthcare Berhad, Narayana Hrudayalaya Ltd, Max Healthcare, MEMG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India medical tourism market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India medical tourism market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India medical tourism industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Medical Tourism Market Report

The India medical tourism market reached USD 23.84 Billion in 2025, driven by cardiovascular treatment at 22.6%, orthopaedic treatment at 19.8%, South India commanding 32.7% regional share, and India's structural cost advantage delivering 60–90% lower treatment costs versus the United States and Europe.

The India medical tourism market grows at 13.09% CAGR during 2026-2034, reaching USD 72.11 Billion by 2034, supported by expanding international patient inflows, rising healthcare costs in developed nations, government Heal in India policy support, and the Africa and CIS market development.

Cardiovascular treatment leads at 22.6% in 2025, driven by India's cardiac surgery cost advantage and internationally comparable cardiac surgery success rates at leading JCI-accredited hospitals in Chennai, Bengaluru, and New Delhi.

South India leads at 32.7% through Chennai, Bengaluru, and Hyderabad's concentration of internationally accredited hospitals, including Apollo, Fortis Malar, Narayana Health, Manipal, and KIMS, which collectively generate India's highest international patient volume.

West & Central India is the second-largest region at 28.1%, driven by Mumbai and Pune's premium specialty hospitals, including Kokilaben Dhirubhai Ambani Hospital, Wockhardt Hospitals, and P.D. Hinduja Hospital, attracting international patients for cardiac, orthopaedic, and cosmetic procedures.

Leading companies include Apollo Hospitals, IHH Healthcare Berhad, Narayana Hrudayalaya Ltd, Max Healthcare, MEMG, and others.

The India medical tourism market is projected to reach approximately USD 44.09 Billion by 2030, driven by expanding fertility and bariatric treatment tourism, telemedicine integration, Africa and CIS patient source market development, and the continued expansion of India's JCI and NABH-accredited hospital network.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)