India Nutritional Supplements Market Size, Share, Trends and Forecast by Product Type, Form, Consumer Group, Distribution Channel, and Region, 2026-2034

India Nutritional Supplements Market Size, Share, Trends & Forecast (2026-2034)

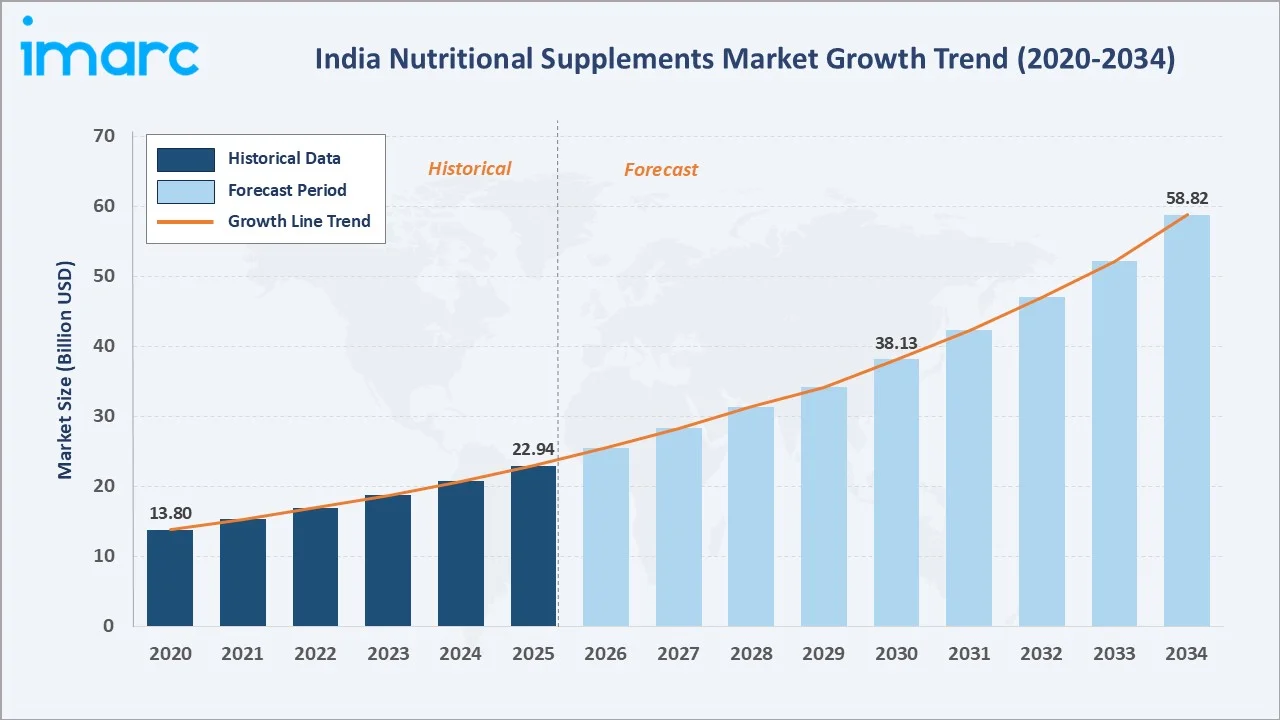

The India nutritional supplements market reached USD 22.94 Billion in 2025 and is projected to reach USD 58.82 Billion by 2034, growing at a CAGR of 10.70% during 2026-2034. India's nutritional supplements market is one of the fastest-growing globally, powered by a 1.4 billion population increasingly embracing preventive healthcare, the post-COVID immunity consciousness that permanently elevated supplement adoption, a booming fitness culture among India's youth, and the government's AYUSH policy framework legitimizing herbal and Ayurvedic supplement formulations.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 22.94 Billion |

|

Forecast Market Size (2034) |

USD 58.82 Billion |

|

CAGR (2026-2034) |

10.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

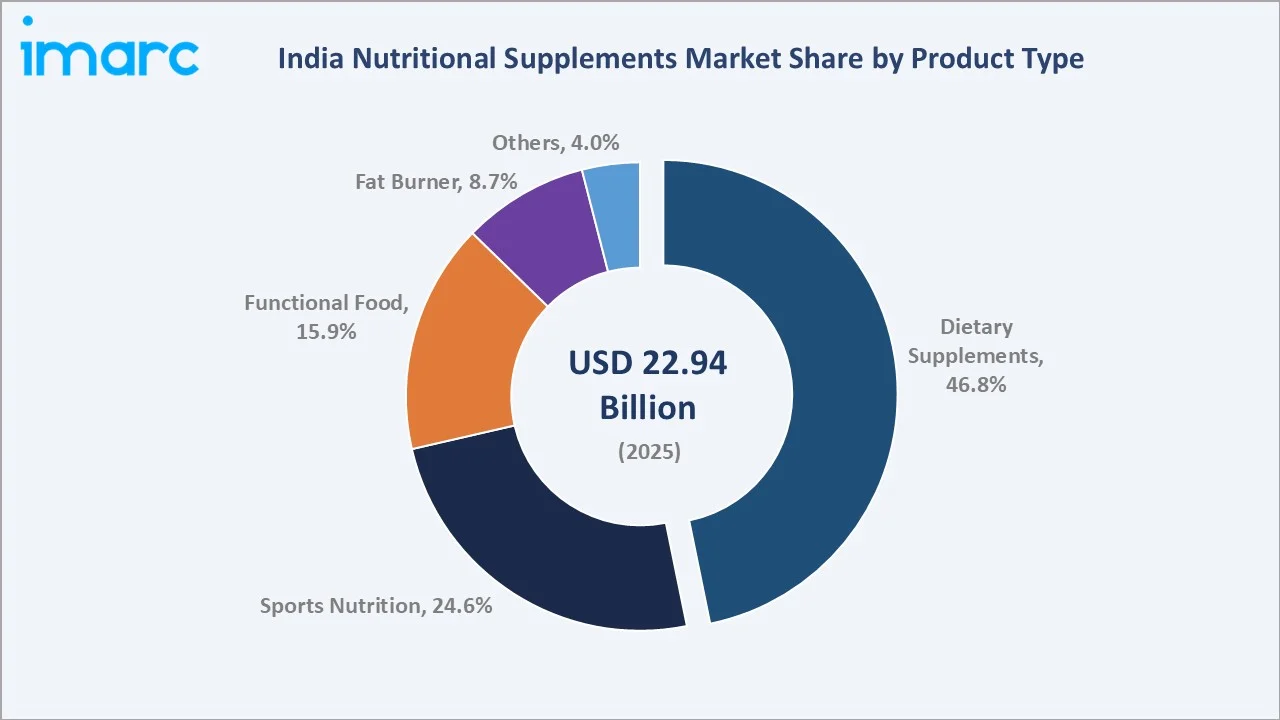

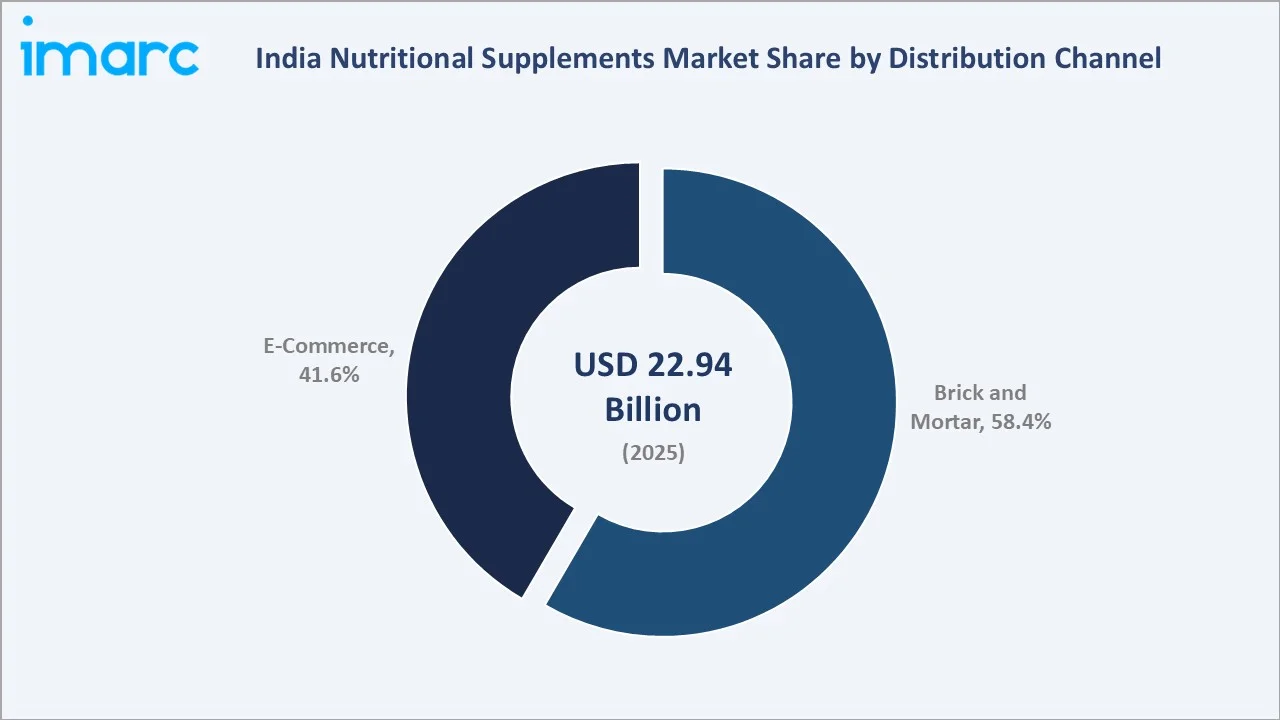

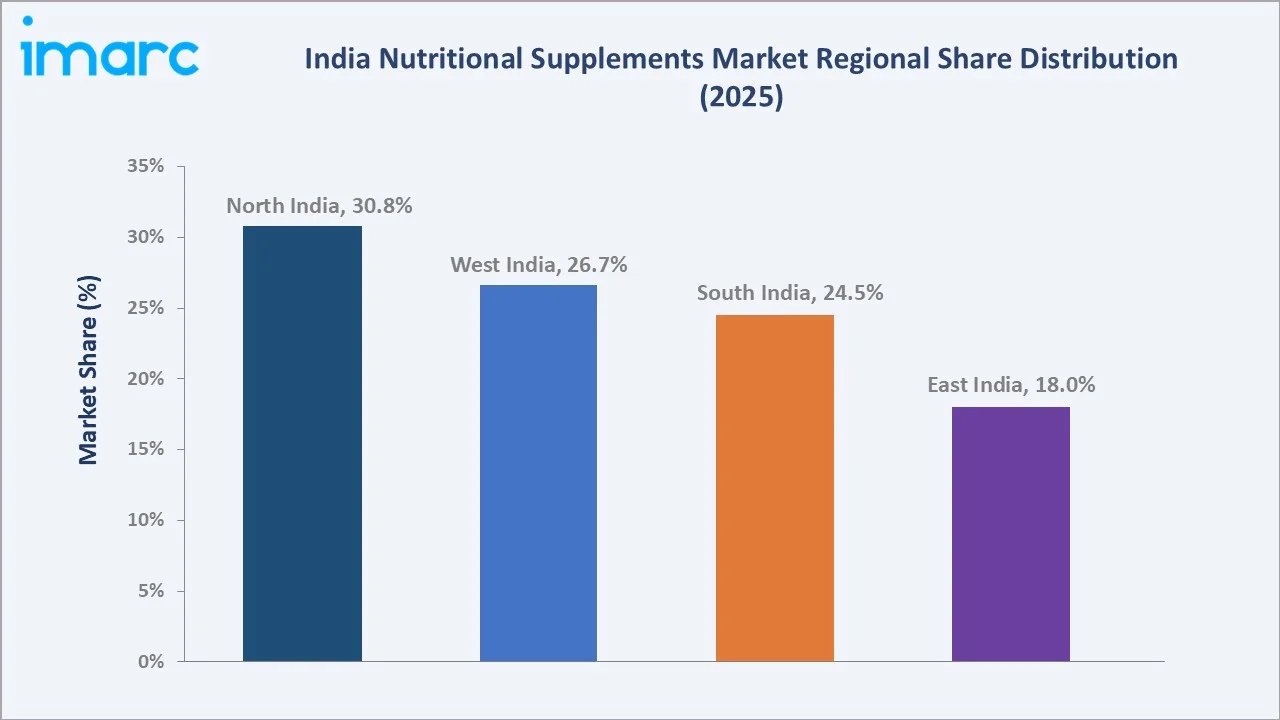

North India leads regionally with a 30.8% market share in 2025, driven by Delhi NCR's high health consciousness, fitness culture, and organized supplement retail density. Dietary supplements command a 46.8% product type share, while brick and mortar retains the largest distribution channel share at 58.4%.

To get more information on this market, Request Sample

The India nutritional supplements market is underpinned by three structural forces: post-COVID health consciousness that has made vitamins, immunity boosters, and preventive supplements part of mainstream Indian household consumption; the fitness revolution anchored by a network of over 46,500 fitness centers serving around 12.3 million members nationwide (2024), creating sustained sports nutrition demand; and the FSSAI regulatory framework's 2022 strengthening that legitimized organized supplement brands while creating barriers to entry that consolidate market revenue among compliant players with established manufacturing quality standards.

Executive Summary

India's nutritional supplements market reached USD 22.94 Billion in 2025 and is forecast to reach USD 58.82 Billion by 2034, growing at a CAGR of 10.70%. India's nutritional supplement market is characterized by the co-existence of global brands with strong domestic players and emerging direct-to-consumer supplement startups that are collectively expanding the market's addressable consumer base beyond the urban elite to India's aspirational Tier 2/3 city population.

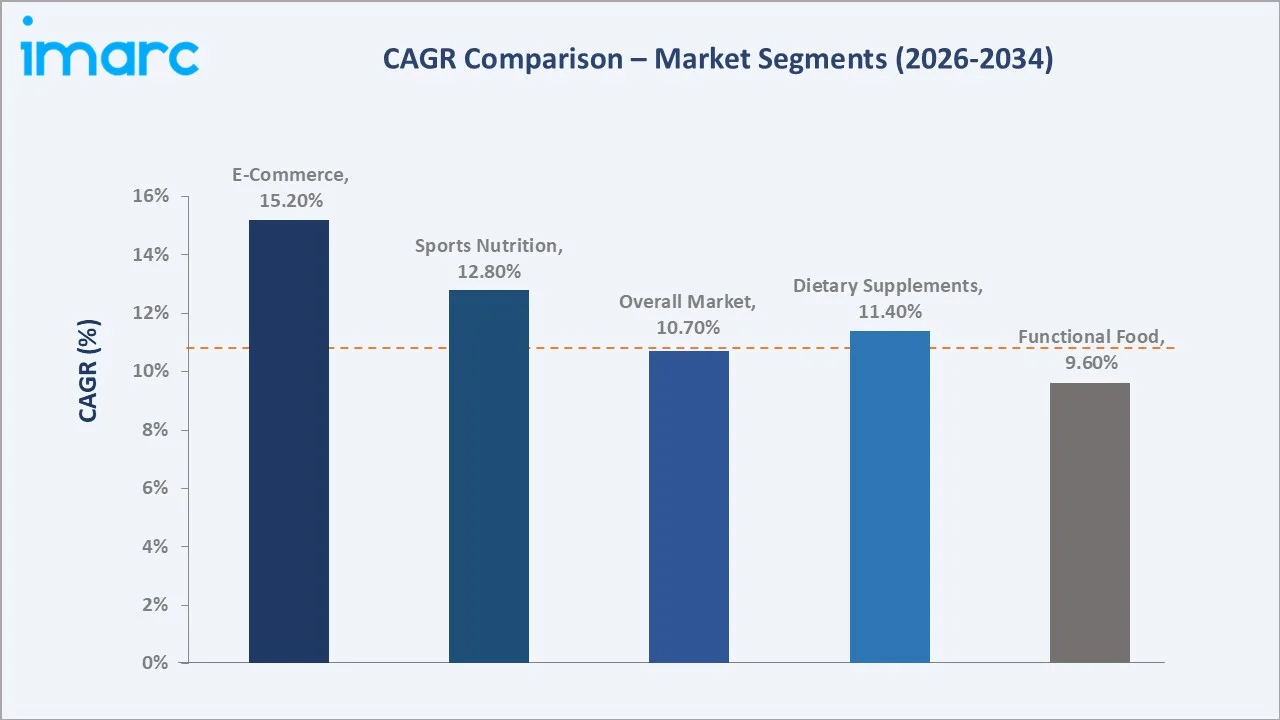

Dietary supplements dominate the product type segment at 46.8%, encompassing vitamins, minerals, omega-3, probiotics, and immunity supplements that constitute the largest and most broadly accessible supplement category. E-commerce is growing fastest at approximately 15.2% CAGR, transforming supplement distribution from a pharmacy and specialty retail model to a direct-to-consumer digital commerce model where brands build subscription customer bases through Amazon, Flipkart, and owned D2C storefronts.

North India at 30.8% leads regionally, owing to higher urbanization, rising fitness awareness, strong gym penetration, and increasing consumer spending on health and wellness products. Leading vendors collectively define India's nutritional supplements competitive landscape across the premium, mid-range, and value segments.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Dietary Supplements – 46.8% share (2025) |

|

Fastest Growing Product Type |

Sports Nutrition – ~12.8% CAGR (2026-2034) |

|

Largest Distribution Channel |

Brick and Mortar – 58.4% share (2025) |

|

Fastest Growing Channel |

E-Commerce – ~15.2% CAGR (2026-2034) |

|

Leading Region |

North India – 30.8% share (2025) |

|

Top Companies |

Amway Corporation, Herbalife Ltd., Abbott, Himalaya Wellness Company, Dabur India Limited |

Key Analytical Observations Supporting The Above Data:

- Dietary supplements at 46.8% (2025) dominate as vitamins, minerals, immunity supplements, omega-3 fatty acids, and probiotics constitute the broadest accessible supplement category, applicable to consumers of all ages, demographics, and health objectives, from children's multivitamins to senior joint support.

- Sports nutrition at 24.6% (2025) share is expected to grow fastest among product types (~12.8% CAGR) as India's gym culture has over 46,500 fitness centers, constituting approximately 12.3 million members nationwide, serving a digital fitness community that drives protein powder, creatine, BCAA, and pre-workout supplement consumption at a previously unseen scale for an emerging market.

- Brick and mortar at 58.4% (2025) leads distribution because India's pharmacy channel, comprising 850,000+ licensed pharmacies, constitutes the primary supplement purchase point for health-focused consumers who prefer pharmacist guidance and verified product authentication.

- E-commerce at 41.6% (2025) share is projected to grow fastest at ~15.2% CAGR, driven by D2C supplement brands building subscription customer bases through Amazon, Flipkart, and owned digital storefronts that deliver personalized supplement subscriptions to online consumers at pricing 20–35% below pharmacy retail due to eliminated distributor margins.

India Nutritional Supplements Market Overview

India's nutritional supplements market encompasses the full spectrum of products designed to supplement dietary intake: vitamins and minerals, protein supplements and meal replacements, sports nutrition, herbal and Ayurvedic supplements, omega-3 and essential fatty acids, probiotics and digestive health supplements, functional foods and nutraceuticals, fat burners and weight management products, and specialized clinical nutrition products for disease management.

India's supplement market macroeconomic foundation is supported by the government's National Ayush Mission (NAM) mandate, allocating INR 3,050 crore in the Union Budget 2024–25 for traditional medicine systems, including Ayurveda, directly supporting herbal and botanical supplement innovation. The FSSAI's Foods for Special Dietary Uses (FSDU) regulation framework provides a structured pathway for supplement product approvals, while the BIS mandatory certification requirements have progressively eliminated substandard imports, creating a compliance barrier that benefits organized manufacturers with established quality infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

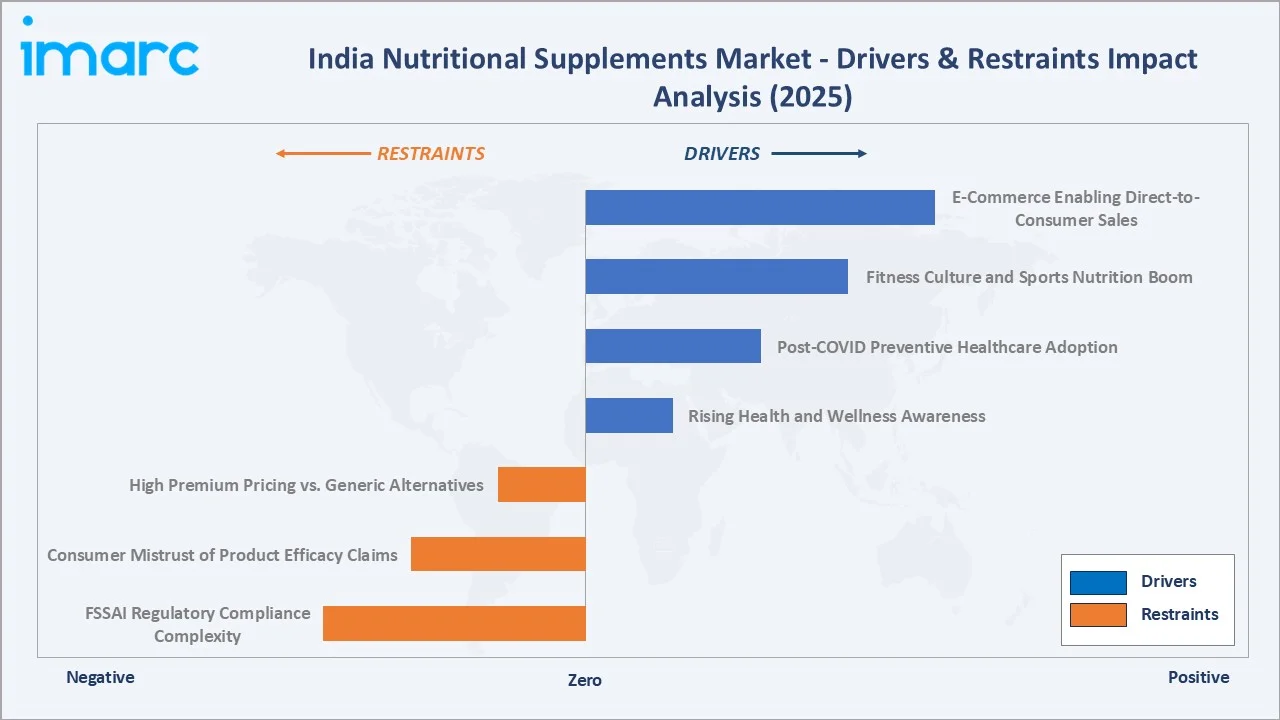

Market Drivers

- Rising Health and Wellness Awareness: The Union Health Ministry’s budget allocation increased from INR 74,602 crore in 2021-22 to INR 1.06 lakh crore in 2026-27, reflecting a structural shift from reactive disease treatment to proactive wellness investment. The latest National Family Health Survey (NFHS-6) found that 30.7% of women aged 15–49 were overweight or obese, compared with 24% in NFHS-5. Among men, the share increased from 22.9% to 27.3%, driving preventive supplement adoption across metabolic health, cardiovascular support, and weight management categories.

- Post-COVID Preventive Healthcare Adoption: COVID-19 permanently transformed India's supplement consumption habits. Vitamins C and D, zinc, and immunity supplement sales grew 300–400% during 2020–2021 and retained 60–70% of that incremental volume after the pandemic, establishing supplementation as a mainstream preventive healthcare behavior.

- Fitness Culture and Sports Nutrition Boom: India's fitness economy has expanded to over 46,500 fitness centers serving around 12.3 million members nationwide in 2024, collectively creating India's largest-ever sports nutrition addressable market. The Indian Premier League's glamour halo effect and social media fitness content creators with 100 million+ combined followers have made protein supplementation and sports nutrition culturally aspirational.

- E-Commerce Enabling Direct-to-Consumer Sales: Amazon India, Flipkart Health+, and Blinkit's 10-minute grocery delivery have transformed supplement distribution economics. These platforms have expanded product accessibility, enabled personalized product discovery, and accelerated the adoption of premium nutritional supplements across tier-II and tier-III cities.

Market Restraints

- FSSAI Regulatory Compliance Complexity: India's Food Safety and Standards Authority (FSSAI) requires supplement manufacturers to comply with the Foods for Special Dietary Uses (FSDU) regulations, obtain prior product approval for claims-bearing supplements, and maintain GMP (Good Manufacturing Practice) certification, which increases time-to-market for new supplement products by 6–18 months.

- Consumer Mistrust of Product Efficacy Claims: Multiple FSSAI enforcement actions against supplement brands making unsubstantiated health claims have created consumer skepticism about supplement efficacy that limits repeat purchase rates and constrains the conversion of casual supplement users to regular supplement consumers.

- High Premium Pricing vs. Generic Alternatives: Premium supplement brands command 3–8 times price premiums over unbranded or private-label alternatives that constitute 25–30% of supplement retail volume in India's price-sensitive markets. This premium-generic price gap limits the addressable premium supplement market.

Market Opportunities

- Personalized Nutrition and DNA-Based Supplement Programs: India's personalized nutrition market is emerging through companies such as Healthians, Redcliffe Labs, and Tata 1mg's MyMeds personalized health program. Personalized supplement subscriptions command 2–3 times premium pricing versus standard supplements and achieve subscription renewal rates of 70–80% versus 30–40% for standard supplements.

- Ayurvedic and Plant-Based Supplement Integration: India's AYUSH supplement market is projected to grow at approximately 18% CAGR as global consumer trends toward natural and plant-based supplements align with India's indigenous botanical heritage. Himalaya Wellness's Ayurvedic supplement line and Dabur's Chyawanprash franchise collectively demonstrate the commercial scale achievable through Ayurveda-credentialed supplementation.

Market Challenges

- Counterfeit Product Proliferation: India's supplement market faces significant counterfeit product infiltration, with counterfeit products estimated to represent 12–18% of online supplement volumes on marketplace platforms. Counterfeit supplements pose consumer safety risks through undisclosed ingredients, incorrect dosages, and microbiological contamination, while damaging brand trust and generating warranty returns that impose costs on genuine manufacturers.

- Consumer Education Gap in Tier 2/3 Markets: Tier 2/3 city consumers frequently lack the nutritional literacy to understand the difference between protein isolate and concentrate, pharmaceutical-grade versus food-grade vitamins, or clinical efficacy evidence grades. This creates a market development bottleneck that requires brand investment in consumer education before revenue conversion.

Emerging Market Trends

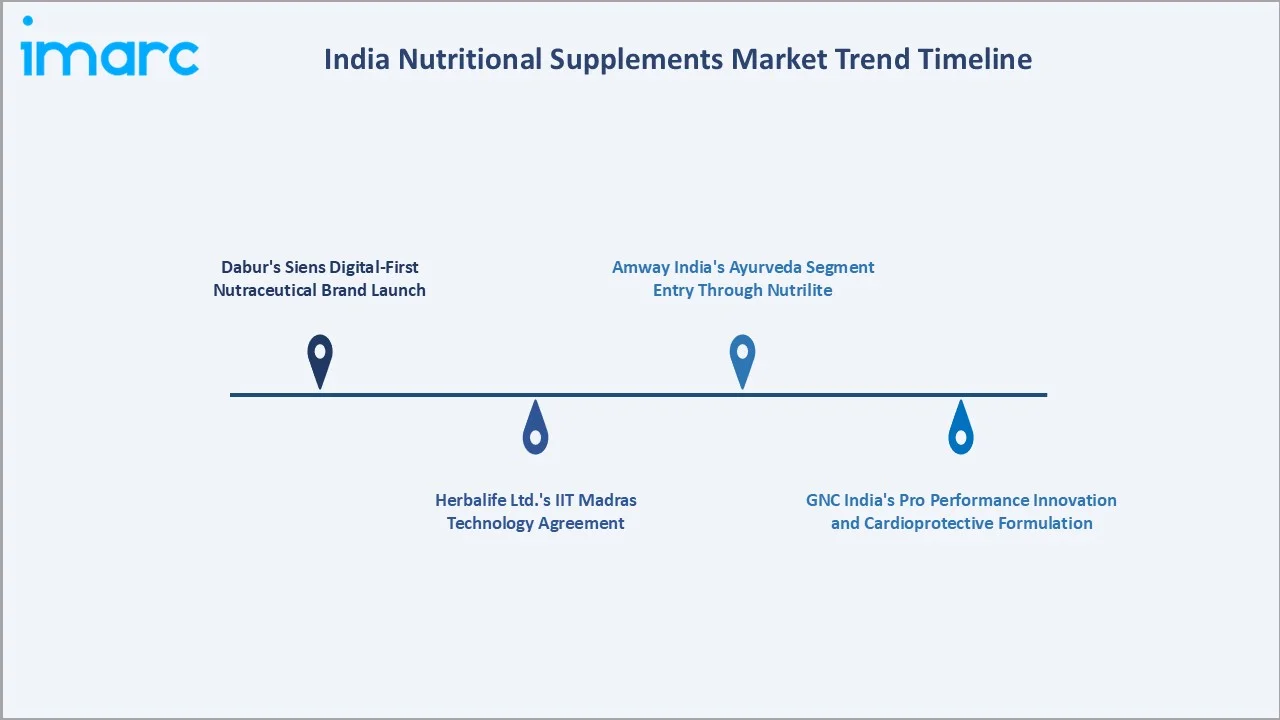

1. Dabur's Siens Digital-First Nutraceutical Brand Launch

In June 2025, Dabur India launched Siens, a digital-first premium nutraceutical brand offering beauty, gut health, and daily wellness supplements in modern formats including gummies, softgels, and effervescent tablets. Siens represents Dabur's strategic pivot from its traditional Ayurvedic formulation heritage toward science-backed, modern-format nutraceuticals. The digital-first launch strategy reflects Dabur's recognition that India's premium supplement consumer increasingly discovers and purchases supplements online rather than at pharmacy counters.

2. Herbalife Ltd.’s IIT Madras Technology Agreement

In February 2025, Herbalife Ltd. signed an agreement with IIT Madras to launch the Herbalife-IITM Plant Cell Fermentation Technology Lab, a research partnership designed to develop fermentation-derived bioactive ingredients for Herbalife's India supplement formulations. This academic-industry partnership signals Herbalife's strategic investment in India-specific supplement innovation beyond its global product portfolio, while IIT Madras's food technology research capabilities provide Herbalife access to India's premier food science and biotechnology expertise.

3. GNC India's Pro Performance Innovation and Cardioprotective Formulation

In March 2025, GNC India launched 'GNC Pro Performance 100% Whey + Nitro Surge', an indigenously developed whey protein incorporating a unique cardioprotective formulation with clinically proven cardiovascular health ingredients. The innovation demonstrates GNC India's commitment to India-specific product development beyond importing global GNC SKUs, addressing India's high cardiovascular disease prevalence through supplement formulation that combines sports nutrition performance with preventive cardiac health.

4. Amway India's Ayurveda Segment Entry Through Nutrilite

In March 2025, Amway India announced its active exploration of the Ayurveda supplement segment, with plans to launch products integrating traditional Indian botanical herbs within the Nutrilite brand's science-backed formulation framework within two to three years. This strategic initiative represents Amway's recognition that India's Ayurveda supplement market is too large to cede to domestic players and that Nutrilite's clinical science credentialing can differentiate Ayurvedic formulations from the competitive herbal supplement market.

Industry Value Chain Analysis

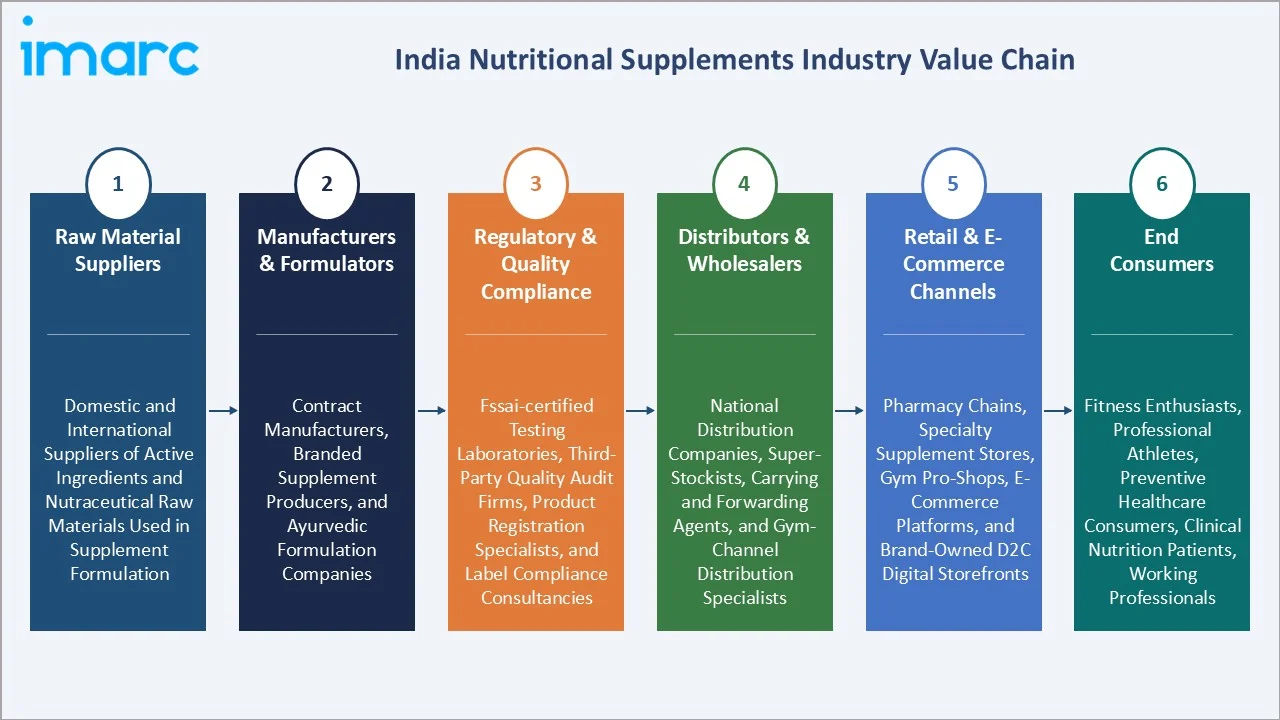

India's nutritional supplements value chain spans raw material sourcing through consumer delivery, with each stage occupied by specialized suppliers, formulators, manufacturers, distributors, and retail channels whose collective performance determines supplement quality, regulatory compliance, pricing, and consumer accessibility.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Domestic and international suppliers of active ingredients and nutraceutical raw materials used in supplement formulation |

|

Manufacturers & Formulators |

Contract manufacturers, branded supplement producers, and Ayurvedic formulation companies |

|

Regulatory & Quality Compliance |

FSSAI-certified testing laboratories, third-party quality audit firms, product registration specialists, and label compliance consultancies |

|

Distributors & Wholesalers |

National distribution companies, super-stockists, carrying and forwarding agents, and gym-channel distribution specialists |

|

Retail & E-Commerce Channels |

Pharmacy chains, specialty supplement stores, gym pro-shops, e-commerce platforms, and brand-owned D2C digital storefronts |

|

End Consumers |

Fitness enthusiasts, professional athletes, preventive healthcare consumers, clinical nutrition patients, working professionals |

Technology Landscape in the India Nutritional Supplements Industry

Sports Nutrition Technology

India's sports nutrition technology landscape has evolved from basic protein powders to sophisticated performance nutrition systems. Key technology trends include instantized protein solubility technology for clump-free mixing, ultra-filtration processing for protein isolate purity above 90%, microencapsulation for probiotic stability in protein formulations, and plant-protein blending for vegan athlete nutrition segments growing at 25%+ CAGR.

Herbal and Ayurvedic Supplement Technology

India's Ayurvedic supplement technology is advancing beyond traditional formulations toward standardized extract technologies that quantify bioactive compound concentrations. Himalaya Wellness's standardized ashwagandha extract with 2.5% withanolide content, Dabur Chyawanprash’s HPLC-verified amla C content, and the emerging field of adaptogen standardization are creating evidence-based Ayurvedic supplements that command clinical credibility previously limited to pharmaceutical-grade products.

Digital and Personalized Nutrition Platforms

India's personalized nutrition technology ecosystem is creating a data-driven supplement purchasing model where consumers receive customized supplement protocols rather than selecting from generic SKUs. Tata 1mg's MyMeds, Healthians' nutrition panel testing, and startups are building the technical infrastructure for personalized supplement recommendations at a commercial scale, targeting the 50 million+ health-conscious Indian consumers willing to pay premium prices for evidence-based personalized supplement guidance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Dietary Supplements |

46.8% |

2025 |

|

Distribution Channel |

Brick and Mortar |

58.4% |

2025 |

|

Consumer Group |

🔒 |

🔒 |

2025 |

|

Form |

🔒 |

🔒 |

2025 |

|

Region |

North India |

30.8% |

2025 |

By Product Type

Dietary supplements dominate with a 46.8% share in 2025, reflecting their broadest consumer applicability, creating addressable demand across every demographic, income segment, and health objective category. Post-COVID immunity supplement adoption has elevated the segment's mass-market penetration beyond the urban health-conscious consumer to include semi-urban and aspirational rural supplement consumers.

To access detailed market analysis, Request Sample

Sports nutrition at 24.6% share (2025) is expected to grow fastest among product types (~12.8% CAGR), encompassing protein powders, meal replacements, creatine, BCAAs, pre-workout supplements, and recovery formulations. Functional food at 15.9% includes fortified foods, health bars, protein snacks, and nutraceutical-enriched beverages.

By Distribution Channel

Brick and mortar commands a 58.4% share in 2025, reflecting Indian consumers' strong preference for pharmacist guidance when purchasing supplements for specific health conditions, the physical authentication advantage of established pharmacy brands over online marketplace counterfeits, and the cultural comfort of supplement purchase alongside medication in India's pharmacy shopping behavior.

E-commerce represents 41.6% of the market and is projected to grow fastest at approximately 15.2% CAGR. Brand-owned D2C platforms are capturing the highest-margin supplement revenue streams by eliminating marketplace commission fees while building direct consumer data relationships that enable personalized supplement subscription programs with 70–80% renewal rates.

Regional Market Insights

North India's market leadership (30.8%, 2025) reflects the region's combination of India's most health-conscious urban consumer base with the region's dense, organized retail infrastructure spanning pharmacy chains, fitness supplement specialty stores, and gym pro-shops. Delhi NCR's concentration of corporate professionals with higher disposable income and awareness of preventive nutrition benefits the specialized fitness supplement channels.

West India at 26.7% is India's second-largest supplement market, driven by Maharashtra and Gujarat's combination of high per-capita income, health-conscious consumer culture, and strong direct sales network penetration. Mumbai's premium supplement retail ecosystem further sustains West India's above-average per-unit supplement pricing and margin contribution.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

30.8% |

Delhi NCR's high health consciousness and fitness culture; corporate professional supplement adoption; dense organized pharmacy and specialty retail |

|

West India |

26.7% |

Mumbai's affluent urban consumer base; Gujarat's health-conscious consumer segments preferring plant-based supplements; Maharashtra's sports nutrition demand from Pune's fitness hub |

|

South India |

24.5% |

Bengaluru's IT professional health consciousness is driving premium supplement adoption; Tamil Nadu's strong pharmacy channel infrastructure for supplement distribution |

|

East India |

18.0% |

West Bengal's growing urban health awareness; expanding e-commerce supplement access in East India's Tier 2 cities; growing sports nutrition adoption among Kolkata's fitness community |

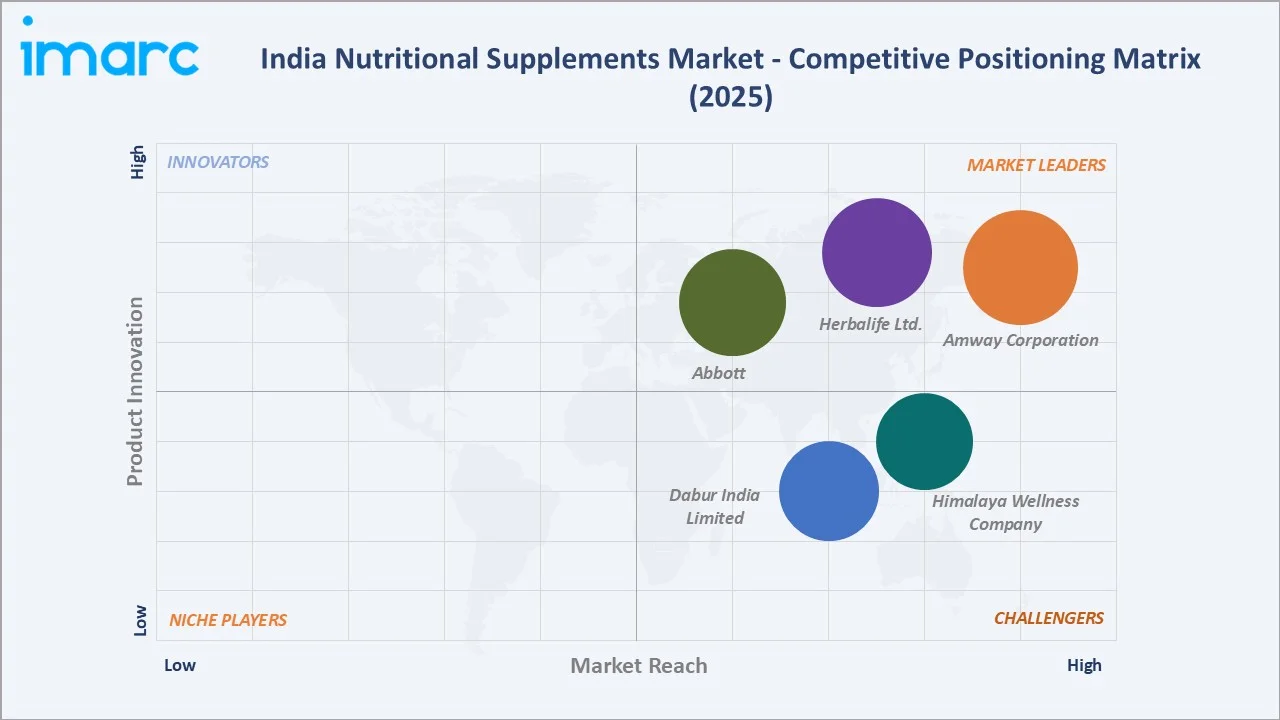

Competitive Landscape

India's nutritional supplements market exhibits moderate concentration, with the top five players collectively holding approximately 35–42% of market revenue in 2025.

|

Company Name |

Key Brands / Products |

Market Position |

Core Strength |

|

Amway Corporation |

Nutrilite, XS |

Market Leader |

One of the largest direct-selling networks; Nutrilite brand's phyto-nutrient credentialing; Ayurveda segment entry |

|

Herbalife Ltd. |

Formula 1, Herbalife24 |

Market Leader |

IIT Madras Plant Cell Fermentation Lab agreement; global nutrition science credentialing; independent distributor network |

|

Abbott |

Ensure, PediaSure, Similac, Glucerna |

Market Leader |

Clinical nutrition leadership across pediatric, adult, and diabetic segments; pharmaceutical-grade quality credentialing |

|

Himalaya Wellness Company |

Quista kidz, Quista DN, Quista PRO (Chocolate), Quista active |

Strong Challenger |

Extensive pharmacy distribution; D2C digital channel growth; herbal supplement portfolio breadth |

|

Dabur India Limited |

Dabur Chyawanprash, Dabur Honey, Siens, among others |

Strong Challenger |

Siens digital-first nutraceutical brand launch; Ayurvedic heritage with modern gummy and softgel formats; broad retail outlet distribution network |

The market's diversity across product types (dietary, sports, Ayurvedic, functional food), consumer segments, and price tiers sustains a competitive ecosystem of 200+ supplement brands competing alongside the dominant players.

Key Company Profiles

Amway Corporation

Amway Corporation’s subsidiary Amway India Enterprises Pvt. Ltd. is one of India's largest direct-selling companies and the leading nutritional supplement brand by distributor network scale. Amway India's Nutrilite brand commands India's largest premium supplement subscriber base through its independent business owner distribution network.

- Key Brands/Products: Nutrilite Daily, Nutrilite Protein Powder, Nutrilite All Plant Protein, Nutrilite Cal Mag D Plus, Nutrilite Double X, and XS Energy Drinks.

- Recent Developments: In November 2025, Amway India Enterprises Pvt. Ltd. launched Nutrilite Vitamin D Plus Boron, a science-backed supplement formulated with Vitamin D3, Boron, Vitamin K2, Quercetin, and Licorice. The product targets Vitamin D deficiency and supports bone health, calcium absorption, and preventive nutrition.

- Strategic Focus: Ayurveda segment entry through Nutrilite botanical herb formulations; digital transformation of direct-selling model; women's nutrition and children's health supplement expansion.

Dabur India Limited

Dabur India Limited is one of India's largest FMCG companies and one of the largest Ayurvedic healthcare companies globally. Dabur's nutritional supplement presence spans traditional Ayurvedic formulations to modern nutraceutical formats, positioning the company as India's broadest-spectrum supplement brand.

- Key Brands/Products: Dabur Chyawanprash, Dabur Honey, Dabur Glucose-D, Dabur Hepano, Dabur Active Blood Purifier, and Dabur Rheumatil Tablet, among others; Siens nutraceuticals.

- Recent Developments: In June 2025, Dabur India Limited launched Siens, a new digital-first nutraceutical brand targeting the premium wellness segment with beauty, gut health, and daily wellness supplements in modern formats. The range covers beauty, daily wellness, and gut health products, including collagen, gummies, multivitamins, Omega-3, and pre/probiotics.

- Strategic Focus: Siens D2C nutraceutical brand scaling; Chyawanprash immunity supplement franchise modernization for younger consumers; honey supplement product extension beyond food application.

Market Concentration Analysis

India's nutritional supplements market exhibits moderate fragmentation, with top players collectively holding approximately 35–42% of market revenue in 2025. The market's diversity across product categories, price tiers, consumer segments, and distribution channels inherently supports a large number of viable players—from multinational corporations with INR 1,000+ crore India supplement revenues to D2C supplement startups reaching INR 50–200 crore in their first three years of operation.

Investment & Growth Opportunities

Fastest Growing Segments

E-commerce distribution (~15.2% CAGR), sports nutrition (~12.8% CAGR), personalized nutrition platforms (~25% CAGR), and women's health supplements (~18% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address USD 20+ billion in incremental market opportunity within India's nutritional supplements ecosystem by 2030.

Emerging Market Expansion

India's Tier 2 and Tier 3 cities represent the next frontier of nutritional supplement market expansion. Current Tier 2/3 supplement penetration of 8–12% of households versus 30–40% in metro India implies 3–5x growth headroom in supplement adoption as e-commerce platforms extend same-day delivery, pharmacy chains expand to smaller cities, and supplement brand awareness grows through digital content consumption.

Venture and Institutional Investment Trends

- India's nutraceutical and health supplement startup ecosystem attracted USD 500+ million in venture investment between 2020 and 2025, demonstrating investor confidence in India's D2C supplement model, where direct consumer relationships, subscription revenue, and digital marketing efficiency create superior unit economics versus traditional distribution models.

- The AYUSH Ministry's INR 3,050 crore Budget 2024–25 allocation, the PLI (Production Linked Incentive) scheme for the food processing sector, and FSSAI's progressive Foods for Special Dietary Uses regulation framework collectively create a policy environment favorable to domestic supplement manufacturing investment.

Future Market Outlook (2026-2034)

The India nutritional supplements market is positioned for sustained, above-average expansion through 2034. From a base of USD 22.94 Billion in 2025, the market is projected to reach USD 58.82 Billion by 2034, representing total incremental value creation of USD 35.88 billion at a CAGR of 10.70%. This growth reflects India's fundamental healthcare transformation, where nutritional supplements are becoming a mainstream component of India's 1.4 billion consumers' daily health management routines.

By 2034, e-commerce will surpass brick and mortar as the dominant distribution channel as D2C supplement brands and marketplace platforms extend reach to India's Tier 2/3 cities. Sports nutrition will grow to approximately 30% product type share as gym culture matures. Ayurvedic and plant-based supplements will represent the fastest-growing category as global wellness trends align with India's traditional medicine heritage.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 95 industry participants in 2024–2025, including supplement brand executives, FSSAI regulatory consultants, gym chain nutrition program managers, pharmacy chain category buyers, e-commerce supplement category managers, and institutional investors across Delhi, Mumbai, Bengaluru, and Chennai.

Secondary Research

Secondary research encompassed company annual reports, FSSAI regulatory databases, ASSOCHAM supplement industry reports, AYUSH Ministry budget documents, and industry publications (Nutraceutical Business Review India, Supplement Insider India, Health & Nutrition India).

Forecasting Models

Market size estimations incorporated India healthcare expenditure growth projections, supplement category penetration modeling, e-commerce distribution growth forecasts, sports nutrition consumption trajectory data, and vendor revenue disclosures. A base-case CAGR of 10.70% reflects consensus estimates validated against brand revenue growth trajectories, pharmacy channel sell-through data, and e-commerce supplement category growth from FY2020 to FY2025.

India Nutritional Supplements Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Sports Nutrition, Dietary Supplements, Fat Burner, Functional Food, Others |

| Forms Covered | Powder, Tablets, Capsules, Liquid, Soft Gels, Others |

| Consumer Groups Covered | Infants, Children, Adults, Pregnant, Geriatric |

| Distribution Channels Covered | Brick and Mortar, E-Commerce |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Amway Corporation, Herbalife Ltd., Abbott, Himalaya Wellness Company, Dabur India Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India nutritional supplements market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India nutritional supplements market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India nutritional supplements industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Nutritional Supplements Market Report

The India nutritional supplements market reached USD 22.94 Billion in 2025 and is projected to reach USD 58.82 Billion by 2034.

The market is expected to grow at a CAGR of 10.70% during 2026-2034, driven by rising health awareness, fitness culture expansion, and e-commerce distribution democratizing supplement access.

North India leads with a 30.8% share in 2025, driven by Delhi NCR's high health consciousness, dense organized supplement retail, and corporate professional supplement adoption.

Dietary supplements dominate with a 46.8% share in 2025, encompassing vitamins, minerals, immunity supplements, omega-3 fatty acids, and probiotics, applicable across all consumer demographics and health objectives.

Brick and mortar holds the largest share at 58.4%, driven by India's 850,000+ licensed pharmacies serving as the primary supplement purchase point for health-focused consumers seeking pharmacist guidance and verified product authentication.

Some of the key players include Amway Corporation, Herbalife Ltd., Abbott, Himalaya Wellness Company, and Dabur India Limited.

E-commerce is growing at ~15.2% CAGR as D2C supplement brands can reach Indian online consumers at lower pricing versus pharmacy retail through eliminating distributor margins.

Some of the key challenges include FSSAI regulatory compliance complexity, consumer mistrust of supplement efficacy claims, premium pricing gaps limiting addressable market, raw material import dependency from China, and counterfeit product proliferation eroding brand trust in online channels.

E-commerce D2C supplement brands, personalized nutrition platforms, Ayurvedic and plant-based supplement innovation, Tier 2/3 city market expansion, and gym-channel sports nutrition distribution represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade