India Reinsurance Market Size, Share, Trends and Forecast by Type, Mode, Distribution Channel, Application, and Region, 2026-2034

India Reinsurance Market Size, Share, Trends & Forecast (2026-2034)

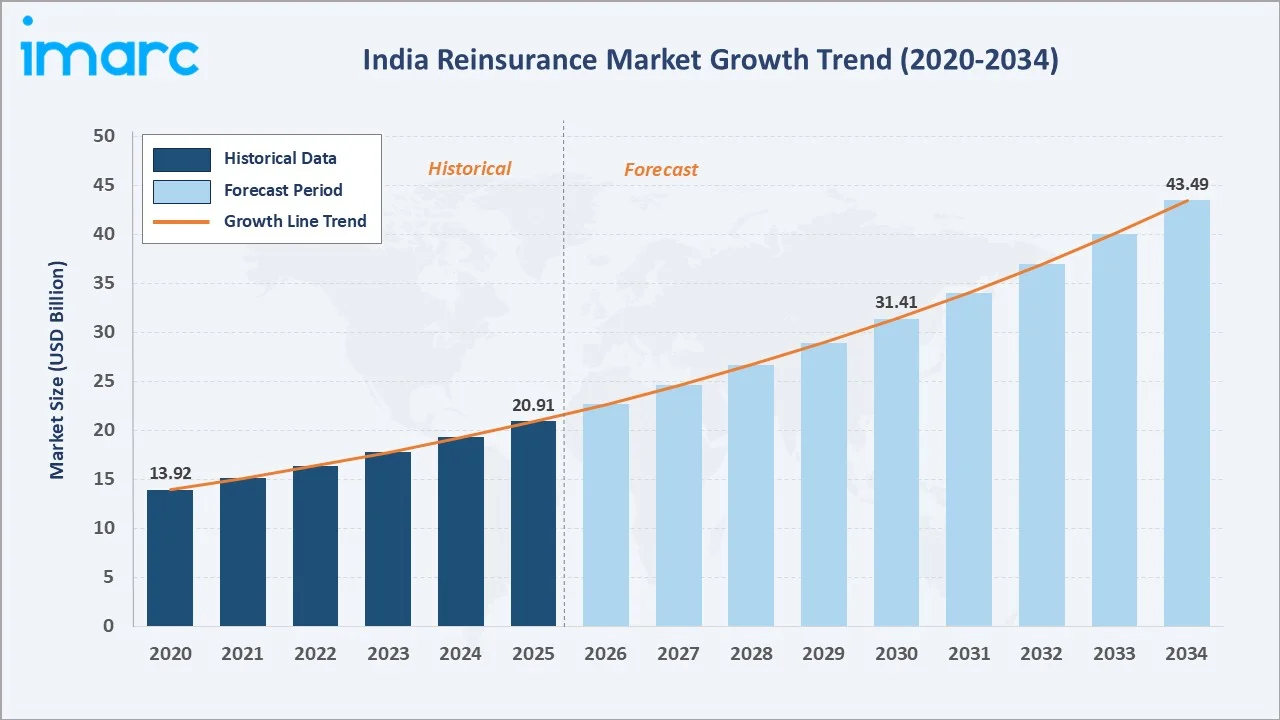

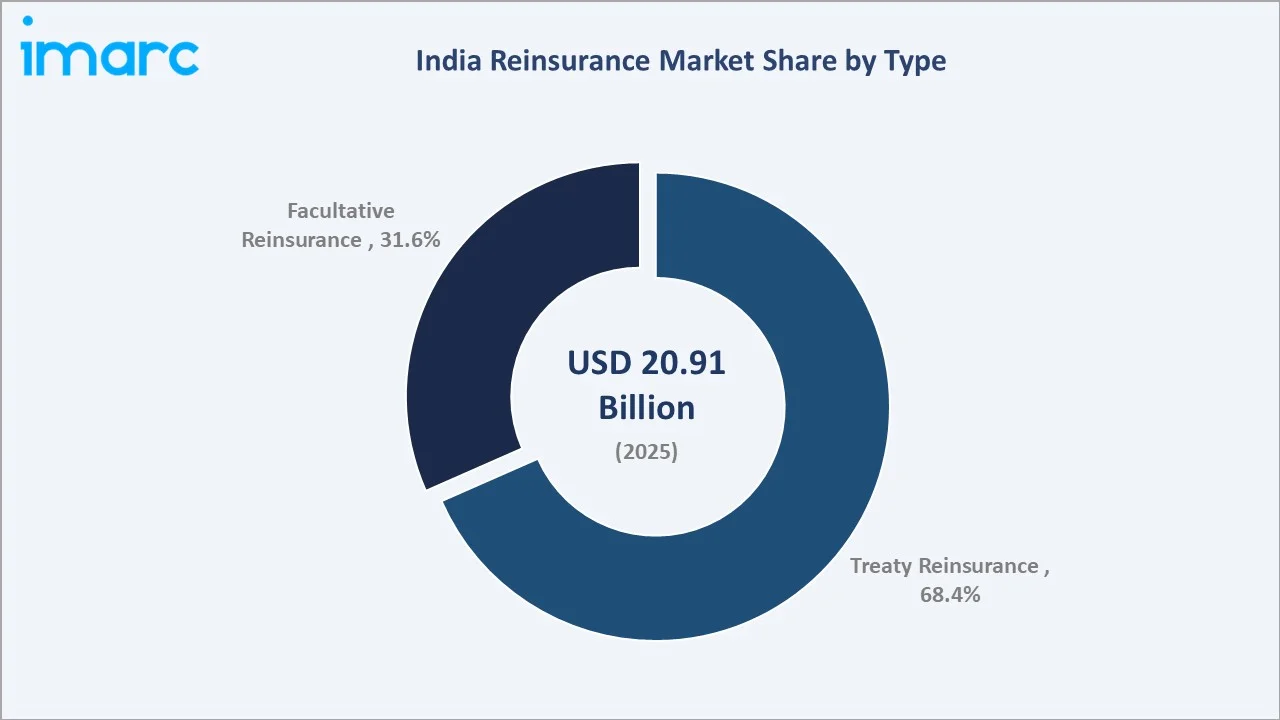

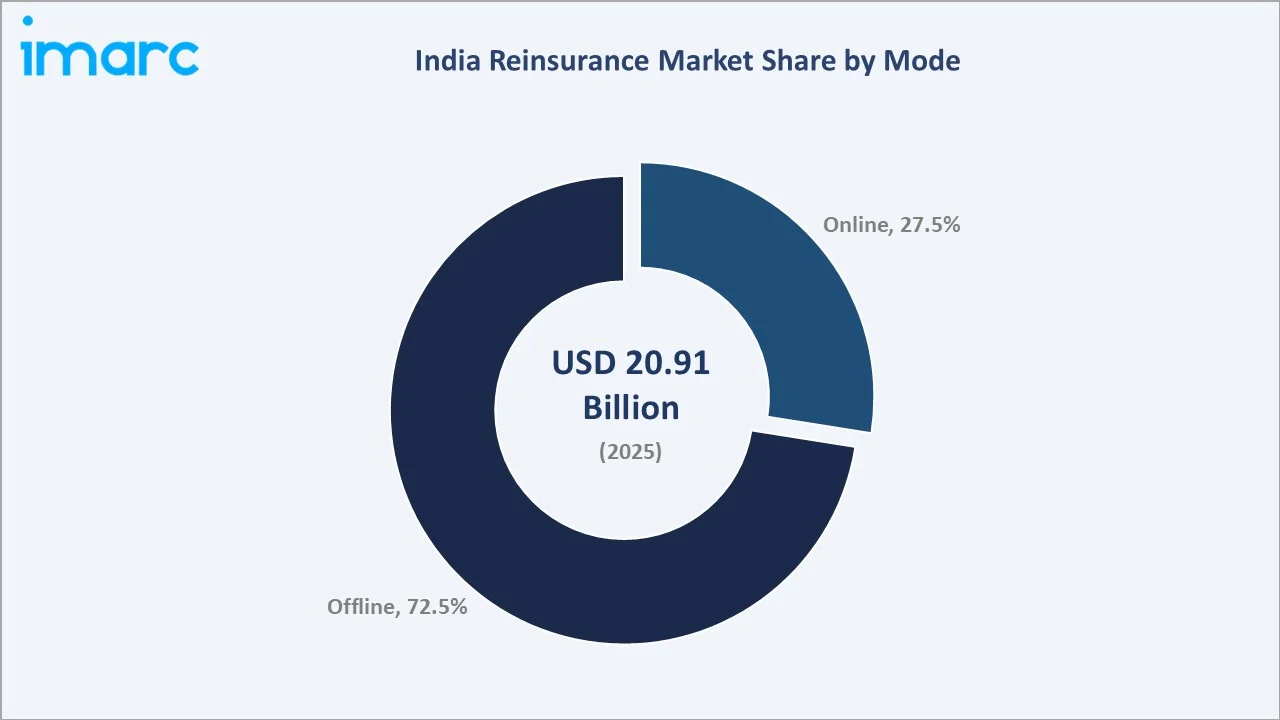

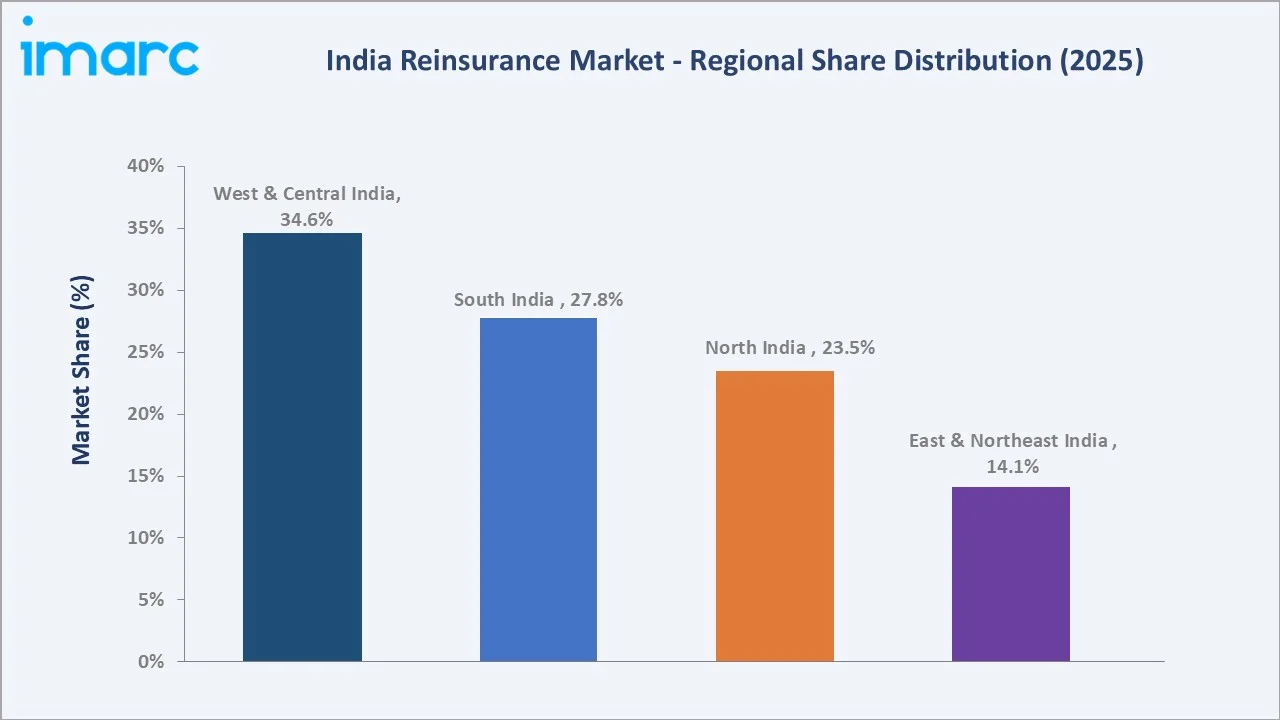

The India reinsurance market reached USD 20.91 Billion in 2025 and is projected to reach USD 43.49 Billion by 2034, growing at a CAGR of 8.47% during 2026-2034. The market is driven by rising insurance penetration with premiums of ₹11.93 lakh crore and AUM of ₹74.44 lakh crore in FY 2024–25, increasing demand for risk transfer solutions, and growing exposure to natural catastrophes, health risks, and large-scale infrastructure projects. Treaty reinsurance dominates at 68.4%. Offline mode leads at 72.5%. West and Central India commands 34.6% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 20.91 Billion |

|

Forecast Market Size (2034) |

USD 43.49 Billion |

|

CAGR (2026-2034) |

8.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Treaty Reinsurance (68.4%, 2025) |

|

Dominant Mode |

Offline (72.5%, 2025) |

|

Leading Region |

West & Central India (34.6%, 2025) |

The market expanded from USD 13.92 Billion in 2020 to USD 20.91 Billion in 2025, anchored at USD 31.41 Billion in 2030, and forecast to reach USD 43.49 Billion by 2034. The COVID-19 pandemic validated India's reinsurance market's structural importance and accelerated regulatory reforms, including reinsurance regulations amendments and the designation of GIFT City IFSC as a dedicated international reinsurance jurisdiction, collectively attracting new reinsurance capacity commitments from global reinsurers.

To get more information on this market, Request Sample

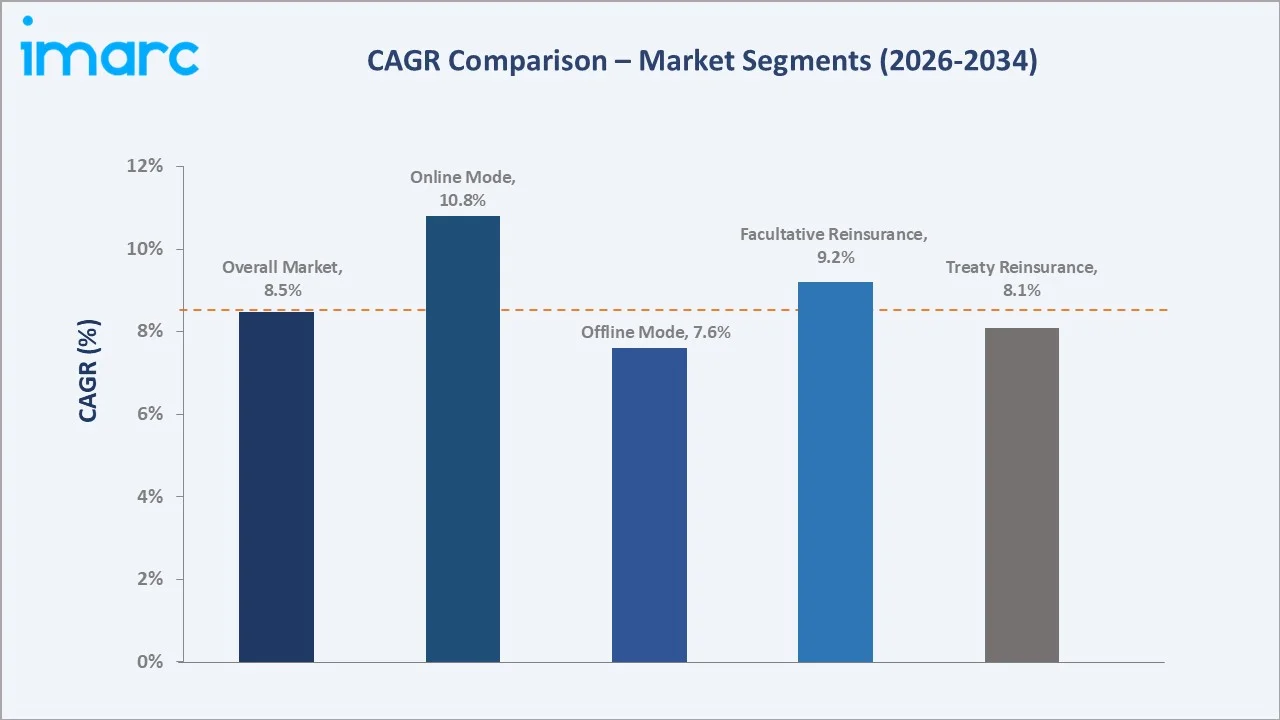

Facultative reinsurance grows fastest at ~9.2% CAGR (2026-2034), driven by India's infrastructure investment boom creating large complex project insurance risks that exceed primary insurer retention capacity; specialty lines development; and premium industrial risks in India's expanding petrochemical, power, and pharmaceutical sectors requiring bespoke facultative underwriting. Online mode grows fastest at ~10.8% CAGR as GIFT City's digital placement platforms and insurtech-enabled treaty platforms digitize reinsurance placement workflows.

Executive Summary

The India reinsurance market reached USD 20.91 Billion in 2025, positioning India as one of Asia's largest reinsurance markets and one of the world's most structurally dynamic reinsurance growth stories. India's reinsurance market is unique in the global context, simultaneously serving a vast government-mandated agricultural reinsurance program, the world's fastest-growing health insurance reinsurance market, a rapidly professionalizing corporate insurance market generating complex treaty and facultative demand, and India's emerging specialty lines segment. The market is projected to reach USD 43.49 Billion by 2034 at 8.47% CAGR.

Treaty reinsurance at 68.4% dominates as the natural structure for India's volume of non-life and life insurance portfolios. Offline mode at 72.5% reflects reinsurance's inherently relationship-driven negotiation process, annual treaty renewals conducted through face-to-face meetings, cedant visits, and broker-intermediated physical placement processes that digitization is progressively transforming but not yet displacing. West and Central India, at 34.6%, leads through Mumbai's insurance hub concentration and GIFT City's reinsurance prominence.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Treaty Reinsurance - 68.4% share (2025) |

|

Dominant Mode |

Offline - 72.5% market share (2025) |

|

Leading Region |

West & Central India - 34.6% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Treaty reinsurance at 68.4%: The treaty reinsurance provides insurers with continuous and cost-effective risk coverage across large portfolios under pre-agreed terms. Its ability to improve capital management, underwriting capacity, and long-term risk sharing makes treaty reinsurance widely preferred by life and non-life insurers.

- Offline at 72.5%: Global reinsurance treaty placement remains one of the world's least digitized financial services transactions. Annual treaty renewals in India require extensive pre-renewal actuarial data exchanges, cedant visits by reinsurer underwriters, broker-facilitated negotiations, and a final treaty wording agreement that cannot yet be automated.

- West and Central India at 34.6%: All major reinsurance brokers and PSU insurer head offices make it India's undisputed reinsurance epicenter for treaty placement, actuarial analytics, and claims management.

India Reinsurance Market Overview

India's reinsurance market encompasses all risk transfer arrangements whereby primary insurance companies transfer portions of their insurance risk portfolios to professional reinsurers in exchange for proportional premium sharing. The market covers all non-life reinsurance classes and life reinsurance. Reinsurance in India operates through two structural types: treaty and facultative.

The ecosystem integrates primary insurance cedants, reinsurance brokers, professional reinsurers, retrocessionnaires (entities providing reinsurance to reinsurers), actuarial and catastrophe modeling firms, and regulatory bodies. Macroeconomic factors include strong economic growth, rising insurance penetration, expanding financial inclusion, increasing infrastructure investments, and rapid urbanization.

Market Dynamics

To evaluate market opportunities, Request Sample

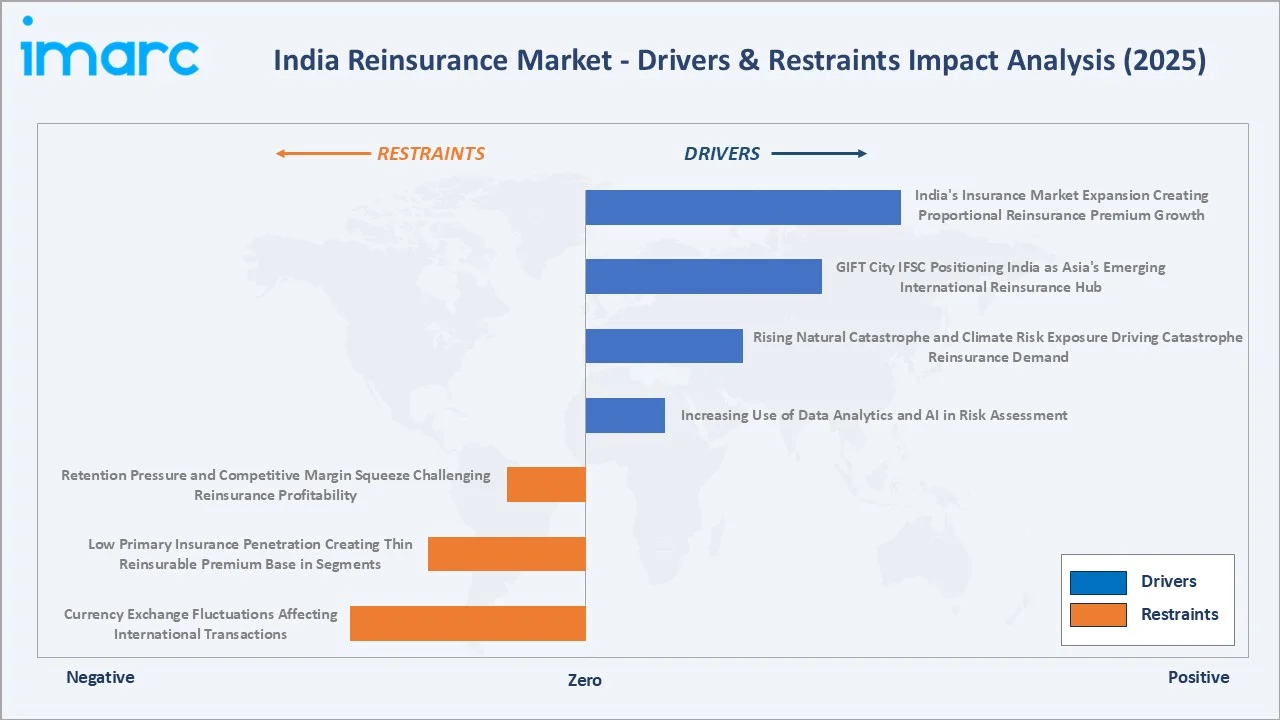

Market Drivers

- India's Insurance Market Expansion Creating Proportional Reinsurance Premium Growth: India's insurance industry growth, representing a doubling of the reinsurable premium base within the forecast period. Each 1% growth in India's primary insurance premium automatically generates proportional reinsurance premium growth through mandatory statutory cession and voluntary treaty arrangements.

- GIFT City IFSC Positioning India as Asia's Emerging International Reinsurance Hub: India's International Financial Services Centre at GIFT City was designated by the Government of India as a dedicated reinsurance jurisdiction, enabling foreign reinsurers to establish branches and write India and international reinsurance business from a USD-denominated, low-tax regulatory environment.

- Rising Natural Catastrophe and Climate Risk Exposure Driving Catastrophe Reinsurance Demand: Rising exposure to floods, cyclones, heatwaves, earthquakes, and other climate-related disasters is increasing demand for catastrophe reinsurance in India as insurers seek stronger risk-sharing and capital protection mechanisms. Events such as Cyclone Amphan, recurring urban flooding in cities like Mumbai and Chennai, and large-scale weather-related crop and property losses have encouraged insurers to expand catastrophe coverage and strengthen reinsurance arrangements to manage rising claim volatility.

Market Restraints

- Retention Pressure and Competitive Margin Squeeze Challenging Reinsurance Profitability: India's primary insurers are subject to regulatory guidelines on minimum retention, and insurers are required to retain prescribed proportions of each risk class rather than ceding excessive portions to reinsurers. This retention requirement creates tension between cedants seeking maximum risk transfer and the objective of building Indian insurance industry capacity.

- Low Primary Insurance Penetration Creating Thin Reinsurable Premium Base in Segments: Low primary insurance penetration limits the overall volume of insurable risks and reduces the available premium base for reinsurers. Large sections of the population, particularly in rural and informal sectors, remain underinsured across health, property, crop, and liability insurance segments, restricting policy issuance and risk diversification opportunities for insurers and reinsurance providers.

Market Opportunities

- India's Health Reinsurance Market as Asia's Fastest-Growing Reinsurance Segment: India's health insurance is growing, driven by Ayushman Bharat PM-JAY, corporate health insurance mandates, and individual health insurance awareness.

- Parametric and Innovative Reinsurance Products for India's Agricultural and Catastrophe Risk: Parametric and innovative reinsurance products enable faster and more transparent claim settlements for agricultural losses, floods, cyclones, droughts, and other catastrophe-related risks. In October 2025, Gallagher designed and placed a customized risk solution for the Indian market, with The Phoenix Mills Ltd. becoming the first company in India to receive coverage for business interruption losses arising from pandemic or epidemic outbreaks through a parametric trigger-based insurance structure.

Market Challenges

- India's Actuarial Data Quality and Catastrophe Modeling Accuracy Constraining Precision Pricing: International reinsurers underwriting India business face persistent challenges with primary insurance data quality, loss run data from Indian cedants often lacks granularity that international catastrophe models require for precise PML estimation.

- Regulatory Complexity Around India's Reinsurance Order of Preference Creating Market Friction: Regulatory complexity surrounding India’s reinsurance order of preference creates market friction by limiting flexibility in reinsurer selection and increasing compliance and placement procedures for insurers. Frequent regulatory changes, approval requirements, and preference rules for domestic reinsurers can delay transactions, affect pricing efficiency, and reduce operational ease for global reinsurance participants.

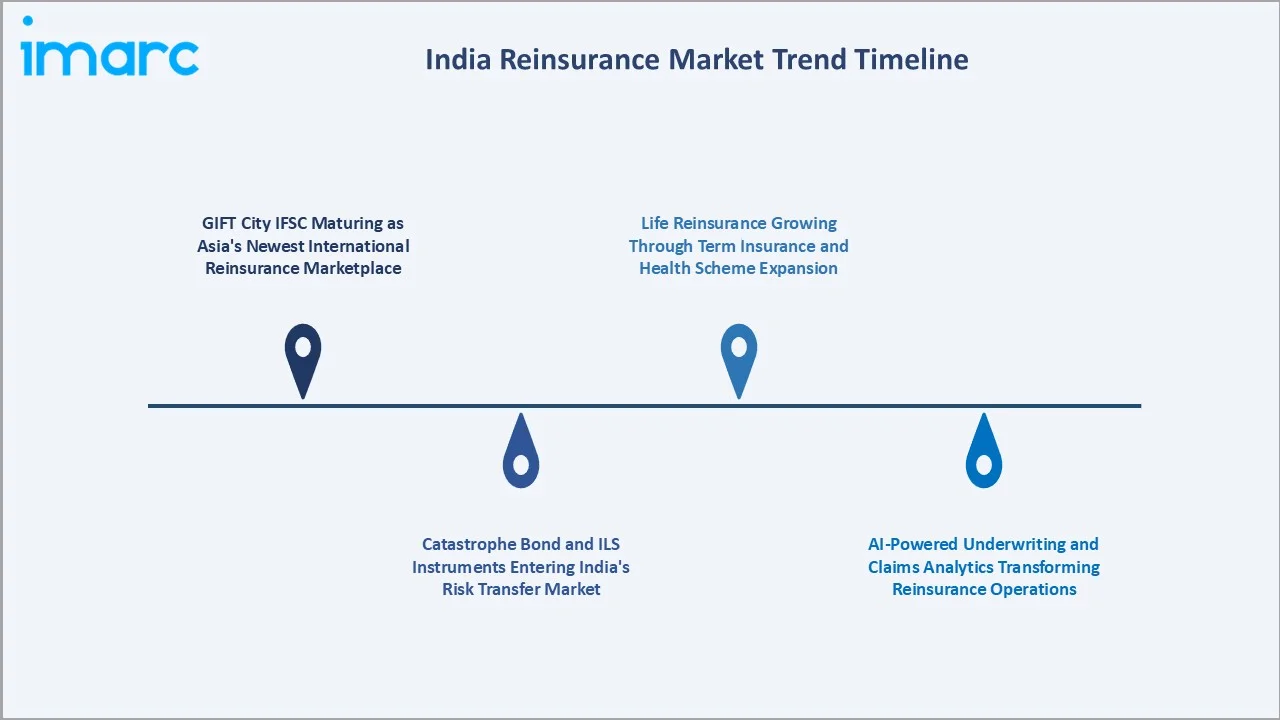

Emerging Market Trends

1. GIFT City IFSC Maturing as Asia's Newest International Reinsurance Marketplace

GIFT City IFSC is positioning itself as an international hub for cross-border reinsurance, specialty insurance, and global risk management activities. The platform offers regulatory flexibility, tax incentives, and simplified operating frameworks, attracting global reinsurers, brokers, and insurance companies to establish regional operations and serve Asian and Middle Eastern markets from India.

2. Catastrophe Bond and ILS Instruments Entering India's Risk Transfer Market

Catastrophe bonds and insurance-linked securities (ILS) provide alternative risk transfer mechanisms for managing large-scale disaster and climate-related exposures. These instruments help insurers and reinsurers access global capital market funding for risks related to cyclones, floods, earthquakes, and agricultural losses, while improving capital efficiency and diversification of risk coverage.

3. AI-Powered Underwriting and Claims Analytics Transforming Reinsurance Operations

AI-powered underwriting and claims analytics are improving risk assessment, pricing accuracy, fraud detection, and claims management efficiency. Reinsurers are increasingly using predictive analytics, machine learning, and real-time data modeling to evaluate catastrophe exposure, automate underwriting decisions, and enhance portfolio risk management across life and non-life segments.

4. Life Reinsurance Growing Through Term Insurance and Health Scheme Expansion

Life reinsurance is emerging as a key trend due to the expansion of term insurance products, rising health insurance penetration, and growing government-backed healthcare schemes. Increasing awareness of financial protection, higher mortality and health risk coverage demand, and rapid growth in digital insurance distribution are encouraging insurers to strengthen life and health reinsurance partnerships for capital and risk management support.

Industry Value Chain Analysis

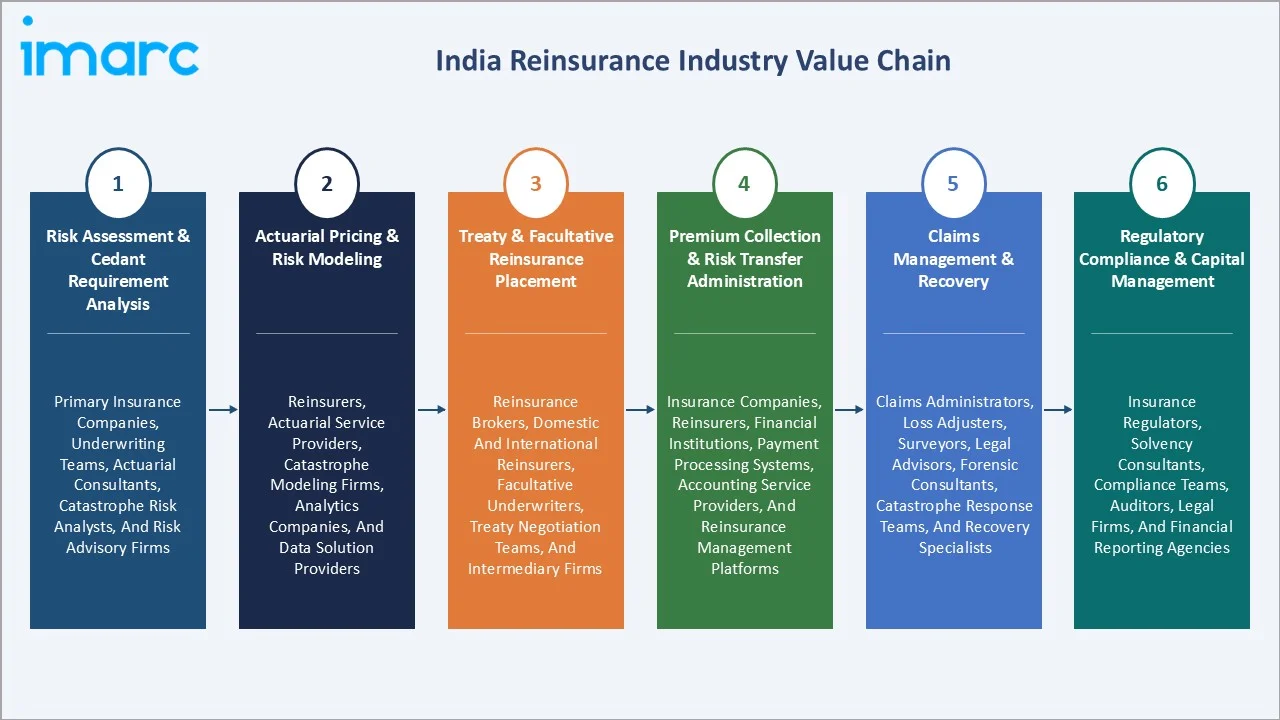

India's reinsurance value chain integrates primary insurer risk identification, actuarial pricing and risk modeling, treaty/facultative placement and negotiation, premium remittance and ceding accounting, claims administration and recoveries, and regulatory reporting. Reinsurance brokers earn 5-12% brokerage on treaty premiums and 10-15% on facultative premiums; professional reinsurers earn combined ratios of 85-105% for profitable segments.

|

Stage |

Key Participants |

|

Risk Assessment & Cedant Requirement Analysis |

Primary insurance companies, underwriting teams, actuarial consultants, catastrophe risk analysts, and risk advisory firms. |

|

Actuarial Pricing & Risk Modeling |

Reinsurers, actuarial service providers, catastrophe modeling firms, analytics companies, and data solution providers. |

|

Treaty & Facultative Reinsurance Placement |

Reinsurance brokers, domestic and international reinsurers, facultative underwriters, treaty negotiation teams, and intermediary firms. |

|

Premium Collection & Risk Transfer Administration |

Insurance companies, reinsurers, financial institutions, payment processing systems, accounting service providers, and reinsurance management platforms. |

|

Claims Management & Recovery |

Claims administrators, loss adjusters, surveyors, legal advisors, forensic consultants, catastrophe response teams, and recovery specialists. |

|

Regulatory Compliance & Capital Management |

Insurance regulators, solvency consultants, compliance teams, auditors, legal firms, and financial reporting agencies. |

The treaty placement and negotiation tier is India's reinsurance value chain's most relationship-intensive and commercially contested stage, where Mumbai-based reinsurance brokers and direct reinsurer business development teams compete for treaty placement mandates from large cedants. India's annual treaty renewal season represents a 3-4 month intensive period of cedant data exchanges, underwriter visits, and commercial negotiations where pricing, capacity, and terms are collectively determined for the subsequent 12-month treaty period.

Technology Landscape in the India Reinsurance Industry

Catastrophe Modeling and Risk Analytics Platforms

Catastrophe modeling and risk analytics platforms enabling reinsurers to assess climate, flood, cyclone, earthquake, and agricultural risk exposures with greater accuracy. Advanced analytics, geospatial mapping, predictive modeling, and AI-driven simulation tools help insurers and reinsurers estimate probable losses, optimize pricing, and strengthen portfolio risk management. In September 2025, JBA Risk Management launched an updated version of its probabilistic India crop catastrophe model for insurers and reinsurers, incorporating enhanced market data, crops, seasons, and districts to provide better risk management insights.

Digital Placement Platforms and InsurTech Reinsurance

Digital placement platforms and InsurTech-led reinsurance solutions streamlining treaty placement, risk assessment, pricing, and policy administration processes. Cloud-based platforms, AI-driven underwriting tools, and digital broking systems are helping insurers and reinsurers improve transaction speed, transparency, and data-sharing efficiency across cross-border reinsurance operations. The growth of digital insurance ecosystems, API-based integrations, and the expansion of GIFT City IFSC as an international reinsurance hub are further accelerating the adoption of technology-enabled reinsurance platforms in India.

Satellite and Remote Sensing for Agricultural Reinsurance

Satellite and remote sensing technologies enable accurate monitoring of crop conditions, weather patterns, flood impact, drought stress, and agricultural risk exposure. Reinsurers and insurers are increasingly using geospatial analytics, satellite imagery, and weather-data platforms to improve crop insurance underwriting, parametric insurance design, and faster claim assessment in rural regions. The adoption of these technologies has gained importance under large-scale agricultural insurance programs and climate-risk management initiatives, particularly in states vulnerable to monsoon variability, floods, and drought-related crop losses.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Treaty Reinsurance |

68.4% |

2025 |

|

Mode |

Offline |

72.5% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

34.6% |

2025 |

By Type

Treaty reinsurance leads at 68.4% market share (2025). India's treaty market is dominated by proportional treaties for motor, health, and life classes, and non-proportional excess-of-loss treaties for fire, marine, engineering, and crop classes. Health reinsurance proportional treaties for Ayushman Bharat-implementing insurance companies and corporate group health books generate growing proportional treaty premiums from India's fastest-expanding insurance class.

To access detailed market analysis, Request Sample

Facultative reinsurance at 31.6% grows fastest at ~9.2% CAGR, serving individual large risk placements in fire (petrochemical, power, refinery), marine (large cargo shipments, hull risks), engineering (major infrastructure projects), aviation (aircraft fleet, airport infrastructure), liability (product liability), and specialty (cyber, political risk) classes.

By Mode

Offline mode leads at 72.5% market share (2025). The offline reinsurance market encompasses all treaty and facultative business negotiated through traditional face-to-face channels. The offline mode is highly relationship-driven nature of reinsurance transactions, complex treaty negotiations, and the need for personalized underwriting and risk assessment discussions. Large-value contracts, regulatory compliance requirements, broker-led placements, and direct engagement between insurers and reinsurers continue to support the dominance of traditional offline operations.

Online mode at 27.5% grows fastest at ~10.8% CAGR. Digital reinsurance covers treaty data exchanges through online portals, digital placement platforms, and emerging reinsurance InsurTech platforms. Routine treaty documentation exchange, premium accounting, and claims data reporting are progressively migrating to digital platforms, but commercial negotiations and complex facultative risk placement remain predominantly offline.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

West & Central India |

34.6% |

The concentration of insurance companies, financial institutions, corporate headquarters, and large commercial risks. The region also benefits from strong demand for property, marine, infrastructure, health, and corporate reinsurance solutions supported by expanding industrial and financial activity. |

|

South India |

27.8% |

Driven by the growth of IT, technology services, healthcare, manufacturing, and digital businesses, requiring specialized risk coverage. Rising demand for cyber insurance, health insurance, engineering risk protection, and commercial liability reinsurance is supporting regional market expansion. |

|

North India |

23.5% |

Supported by strong government-linked insurance activity, infrastructure development, group health insurance programs, and increasing corporate risk management adoption. The region is witnessing growing demand for life, health, motor, property, and infrastructure-related reinsurance coverage. |

|

East & Northeast India |

14.1% |

Driven by marine trade, agriculture, infrastructure projects, and rising climate-related risk exposure. Increasing focus on crop insurance, catastrophe coverage, logistics, and regional industrial development is gradually supporting market growth. |

West and Central India's 34.6% market leadership is structurally anchored by three non-substitutable advantages: Mumbai's role as India's insurance and reinsurance capital, GIFT City's emergence as India's international reinsurance hub, and Maharashtra-Gujarat's concentration of India's largest insurable industrial and commercial risks, generating the highest-value individual facultative placements.

South India's 27.8% reflects the region's PMFBY exposure concentration, Bengaluru's specialty lines reinsurance demand, and Kerala's life reinsurance intensity from the state's high insurance penetration. North India's 23.5% is dominated by Delhi's PSU insurance headquarters, UP's PMFBY premium concentration, and North India's industrial corridor reinsurance demand. East and Northeast India's 14.1% represents the market's highest growth potential region.

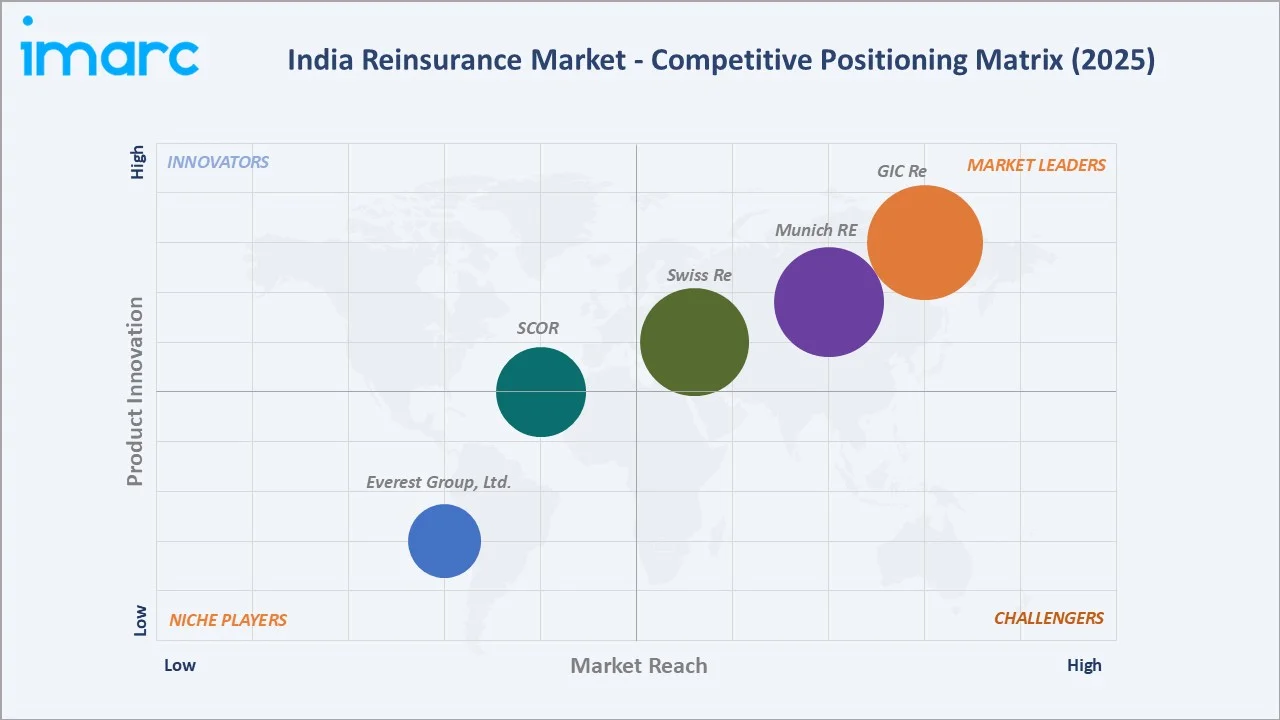

Competitive Landscape

India's reinsurance market exhibits a unique competitive structure defined by regulatory design rather than pure market competition. The mandatory statutory cedant position makes it structurally central to all reinsurance arrangements, commanding 40-45% of total reinsurance premium through mandatory cession and voluntary additional placements. The remaining 55-60% is competed for by GIFT City FRBs and offshore reinsurers. The reinsurance broker community plays a disproportionately influential role in shaping competitive dynamics by advising cedants on optimal reinsurance program structure and introducing competitive tension between participating reinsurers at treaty renewal.

|

Company Name |

Business Lines |

Market Position |

Core Strength |

|

GIC Re |

Property, Health U/W Claims, Marine, Aviation U/W & Claims, Motor U/W & Claims, Life Re U/W & Claims, Liability U/W & Claims, Financial Risk, Credit & Guarantee |

Market Leader |

As a sole reinsurer in the domestic reinsurance market, GIC Re provides reinsurance to the direct general insurance companies in the Indian market. |

|

Munich RE |

Property/Casualty, Life/Health, Munich Re Specialty, Industry Clients, Public Sector |

Market Leader |

Munich Re strong presence in the Indian market since 1951 for general insurance, and since 1957 for life insurance. |

|

Swiss Re |

Property & Casualty Reinsurance, Life & Health Reinsurance |

Market Leader |

The Swiss Re is one of the world's leading providers of reinsurance, insurance and other forms of insurance-based risk transfer, working to make the world more resilient. |

|

SCOR |

Life & Health reinsurance; P&C reinsurance |

Established Player |

As a leading global reinsurer, SCOR offers its clients a diversified and innovative range of reinsurance and insurance solutions and services to control and manage risk. |

|

Everest Group, Ltd. |

Property, Casualty, and Facultative |

Niche Player |

A global leader in risk management, rooted in a rich heritage, focused on long-term value, disciplined with capital, caring deeply about Everest's impact on communities and the wider world. |

The competitive landscape is evolving rapidly as GIFT City matures. Regulations create the foundation for a genuine regional reinsurance marketplace that could challenge Singapore's regional dominance in the South Asia reinsurance business.

Key Company Profiles

GIC Re

General Insurance Corporation of India (GIC Re) is India's sole domestic professional reinsurer and the statutory recipient of mandatory cedant cession from all Indian primary insurers.

- Business Lines: Property, Health U/W Claims, Marine, Aviation U/W & Claims, Motor U/W & Claims, Life Re U/W & Claims, Liability U/W & Claims, Financial Risk, Credit & Guarantee.

- Strategic Focus: Strengthening its leadership in domestic treaty reinsurance while expanding specialty, catastrophe, health, agriculture, and international reinsurance portfolios.

Munich RE

Munich Re has had a strong presence in the Indian market since 1951 for general insurance, and since 1957 for life insurance. Since then, Munich Re has continuously engaged with insurers and large corporate clients in India, providing technical expertise and risk management solutions.

- Business Lines: Property/Casualty, Life/Health, Munich Re Specialty, Industry Clients, Public Sector.

- Recent Developments: In October 2025, Gallagher created India’s First Pandemic Insurance using parametric triggers launched by New India Assurance, reinsured by Munich Re.

- Strategic Focus: Expanding specialty reinsurance solutions across health, life, cyber, agriculture, and catastrophe risk segments while strengthening partnerships with Indian insurers.

Market Concentration Analysis

India's reinsurance market exhibits high structural concentration at the top. GIC Re commands 40-45% of total reinsurance premium as the mandatory statutory cedant, creating a market structure without a global parallel where a single government-owned entity receives legally guaranteed premium flows. Among voluntary placement, Munich Re, Swiss Re, and others collectively capture 20-25% of the market premium, with the remaining 35-40% distributed among additional participating reinsurers.

Concentration dynamics are changing as GIFT City FRBs collectively increase their India voluntary treaty market share, a trajectory suggesting GIFT City may control 30-35% of voluntary reinsurance by 2030 if current growth rates continue. This GIFT City concentration growth is occurring at the expense of offshore market placements rather than GIC Re's mandatory cession, creating a geographic relocation of reinsurance activity from overseas centers to GIFT City without disrupting GIC Re's structural position. The reinsurance broker community effectively controls placement decision influence for 60-70% of voluntary reinsurance through their advisory relationships with large cedants, creating an information intermediary concentration that shapes competitive dynamics among participating reinsurers.

Investment & Growth Opportunities

Fastest Growing Segments

Facultative reinsurance (~9.2% CAGR), online mode (~10.8% CAGR), health reinsurance class (~15-18% CAGR), cyber reinsurance (~35-40% CAGR from a small base), life reinsurance (~12% CAGR), and GIFT City IFSC-based reinsurance (~25%+ CAGR from 2022 base) represent India's highest-growth reinsurance investment vectors.

Emerging Market Opportunities

India's infrastructure development represents an incremental annual facultative reinsurance premium by 2030. Each major metro project requires custom construction all risks and erection all risks reinsurance beyond treaty automatic acceptance limits, creating significant facultative placement opportunities for Lloyd's India and specialty reinsurers.

Investment Themes

- Agricultural parametric reinsurance scale-up for PMFBY modernization: India's government has expressed intent to modernize PMFBY from indemnity to a parametric structure, which would transform the crop reinsurance market from slow, dispute-prone traditional claims settlement to rapid automated payment on measurable triggers.

- Cyber reinsurance capacity development for India's digital economy accumulation risk: India's cybersecurity incident costs are rising, with major incidents at AIIMS Delhi, ICMR, and vaccination portals demonstrating systemic cyber vulnerability. India's primary cyber insurance market is dramatically under-reserving this economic risk, creating an opportunity for specialized cyber reinsurers to develop India-specific cyber loss models, create standardized cyber coverage language for Indian regulatory compliance, and build cyber reinsurance capacity for India's financial, healthcare, and technology sectors, where accumulation risk concentration is highest.

Future Market Outlook (2026-2034)

The India reinsurance market is projected to grow from USD 20.91 Billion in 2025 to USD 43.49 Billion by 2034, delivering an 8.47% CAGR over the forecast period. The market's anchor value of USD 31.41 Billion in 2030 represents a reinsurance ecosystem where GIFT City IFSC has matured into a recognized international reinsurance hub hosting 25-30 FRBs with combined annual premium, health reinsurance has become India's largest single reinsurance class surpassing traditional property and crop classes, and parametric and ILS instruments have begun transforming India's agricultural and catastrophe reinsurance architecture toward more efficient capital markets-based risk transfer.

Three structural forces define India's reinsurance market growth with high certainty through 2034: India's primary insurance premium doubling as penetration improves, each percentage point of primary premium growth generating proportional reinsurance demand through statutory cession and voluntary treaty arrangements; government-mandated schemes creating guaranteed reinsurance premium flows that sustain market growth independent of private insurance market cycles; and GIFT City IFSC's maturation as a genuine reinsurance hub attracting international capital and creating a self-reinforcing ecosystem of reinsurers, brokers, actuaries, and insurtech firms that progressively reduces India's reinsurance dependency on other markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with 60+ industry stakeholders (2025), including Chief Reinsurance Officers and treaty underwriting teams from GIC Re, Munich Re India, Swiss Re India, Hannover Re India, and SCOR India; reinsurance broker managing directors from Marsh India, Aon Re India, and Guy Carpenter India; Chief Risk Officers from Star Health Insurance, New India Assurance, and HDFC ERGO regarding reinsurance procurement strategy; IFSCA (International Financial Services Centres Authority) GIFT City reinsurance regulatory officials; IRDAI reinsurance department officials; and actuarial principals from major Indian insurance companies.

Secondary Research

Secondary research encompassed IRDAI Annual Report 2024-25 (reinsurance statistics by class and cedant), IFSCA Annual Report 2024-25 (GIFT City FRB licensing and premium data), GIC Re Annual Report FY2025, Swiss Re India Insurance Market Report 2025, Munich Re database India data, Reinsurance News India market analysis, CEIB (Council of Insurance and Economic Brokers) India market data, India Budget 2025-26 (PMFBY allocation), Ministry of Agriculture PMFBY premium and claim statistics 2024-25, and NIC (National Insurance Commission) comparative global reinsurance market data. Over 80 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up type x mode segmental models calibrated against IRDAI's annual reinsurance statistics (non-life class-wise cession data, life reinsurance statistics), GIC Re's annual premium trajectories, PMFBY government scheme premium projections (Ministry of Agriculture 5-year outlook), Ayushman Bharat scale-up targets (National Health Authority), and India primary insurance penetration improvement scenarios based on IRDAI's Insurance Vision 2047 document. Key inputs include IMF India GDP growth projections, India primary insurance CAGR projections by class, GIFT City FRB licensing pipeline and premium commitment data from IFSCA, and Swiss Re sigma India protection gap analysis, determining incremental reinsurance premium from improving insurance penetration.

India Reinsurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Modes Covered | Online, Offline |

| Distribution Channels Covered | Direct Writing, Broker |

| Applications Covered |

|

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | GIC Re, Munich RE, Swiss Re, SCOR, Everest Group, Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India reinsurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India reinsurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India reinsurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Reinsurance Market Report

The India reinsurance market reached USD 20.91 Billion in 2025, driven by India's primary insurance market expansion, PMFBY government crop reinsurance, Ayushman Bharat health insurance generating health reinsurance growth, GIFT City IFSC attracting Foreign Reinsurance Branches, and GIC Re's statutory position as mandatory cedant recipient for all Indian primary insurers.

The market grows at 8.47% CAGR during 2026-2034, reaching USD 43.49 Billion by 2034, driven by India's primary insurance market growth, health reinsurance becoming India's largest class, GIFT City IFSC maturing with more FRBs, PMFBY parametric transformation, and India's first catastrophe bond issuance demonstrating ILS market integration.

Treaty reinsurance leads at 68.4% through GIC Re's mandatory cession, PMFBY crop treaty, health proportional treaties, and motor programs.

Offline leads at 72.5% through relationship-intensive annual treaty renewal negotiations, physical cedant-underwriter meetings, and broker-mediated slip presentation for facultative placements.

West and Central India lead at 34.6%, anchored by Mumbai's reinsurance capital status, GIFT City IFSC’s FRBs, and Maharashtra-Gujarat's concentration of India's largest facultative risks requiring specialist reinsurance.

Leading companies include GIC Re, Munich RE, Swiss Re, SCOR, and Everest Group, Ltd., among others.

The market is projected to reach approximately USD 31.41 Billion by 2030, with GIFT City hosting more FRBs commanding market premium, health reinsurance overtaking crop as India's largest class, India's first catastrophe bond issuance, and facultative reinsurance accelerating as infrastructure investment generates unprecedented engineering risk complexity.

GIFT City serves as an international financial hub that enables global reinsurers, brokers, and insurers to operate under a more flexible regulatory and tax environment. It supports cross-border reinsurance business, specialty risk underwriting, and international capital inflows, helping position India as a regional reinsurance and risk management center.

Pradhan Mantri Fasal Bima Yojana (PMFBY) generates large-scale agricultural risk coverage that requires insurers to transfer weather- and crop-related exposures to reinsurers. The scheme increases demand for catastrophe, weather, and crop reinsurance solutions due to recurring risks from floods, droughts, cyclones, and monsoon variability.

Health reinsurance is growing at 15-18% annually, driven by Ayushman Bharat, corporate health mandates, and standalone health insurer growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade