Industrial Gearbox Market Size, Share, Trends and Forecast by Type, Design, Application, and Region, 2026-2034

Industrial Gearbox Market Size, Share, Trends & Forecast (2026-2034)

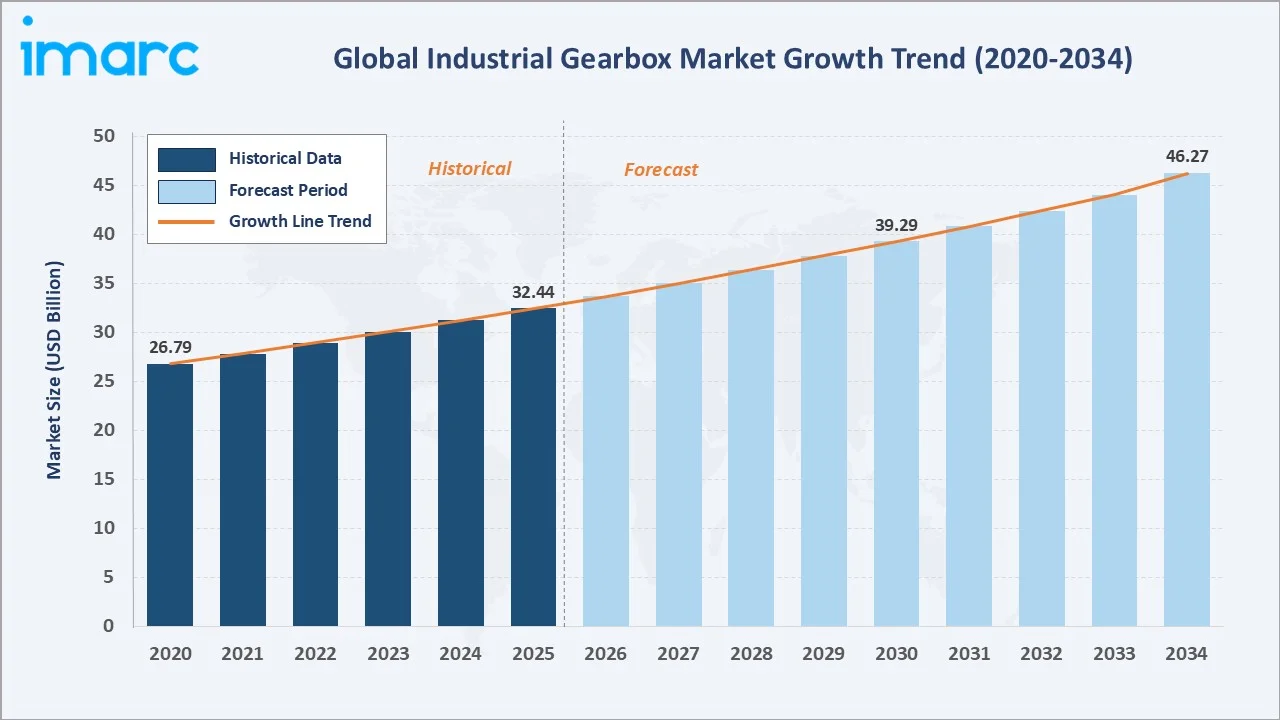

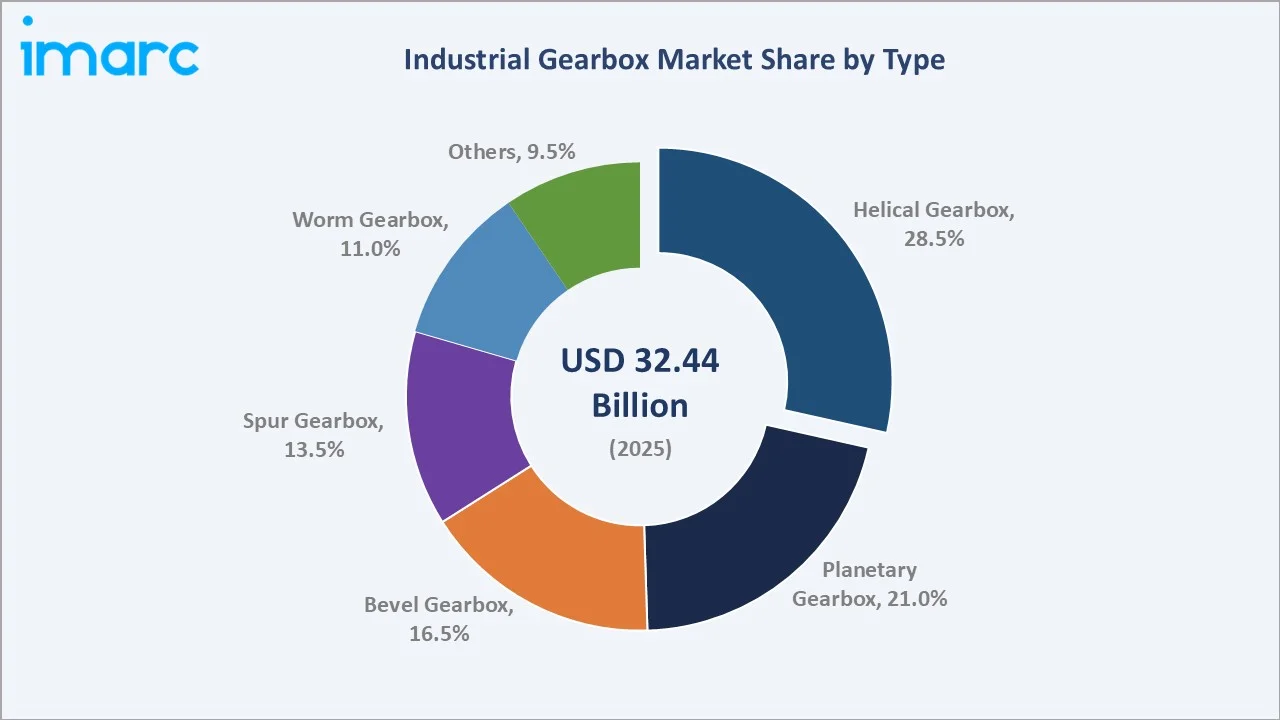

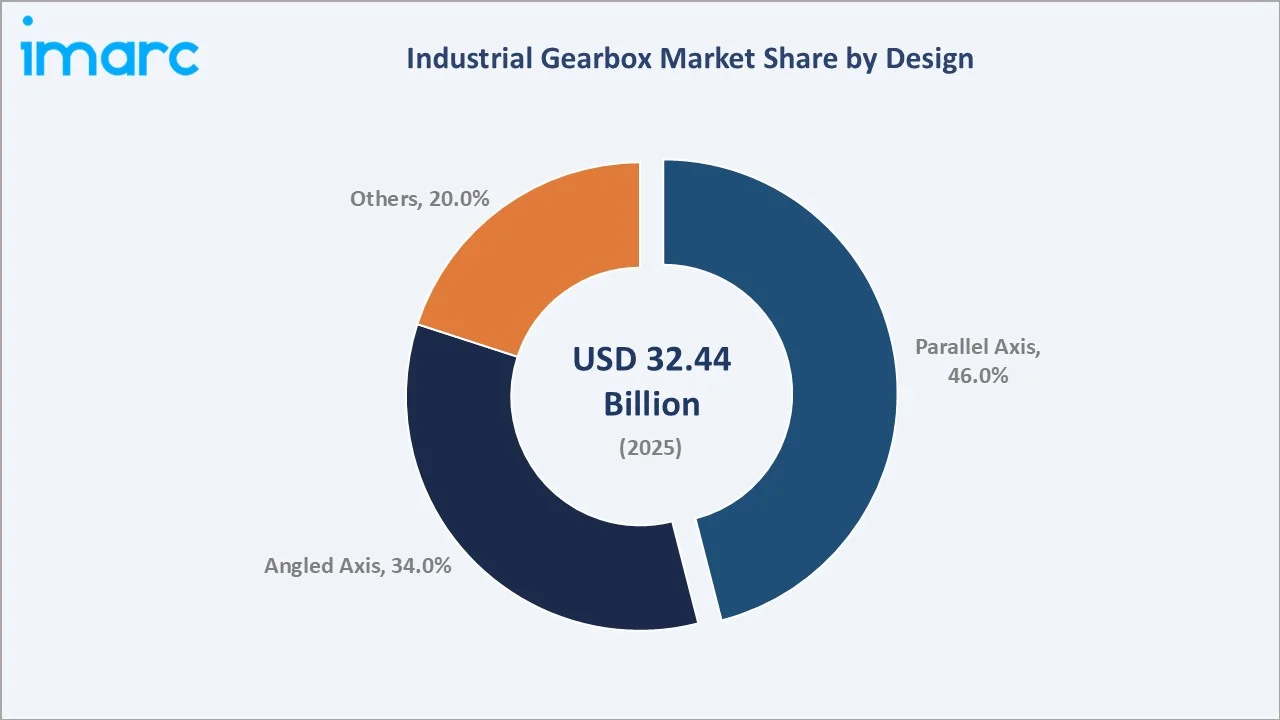

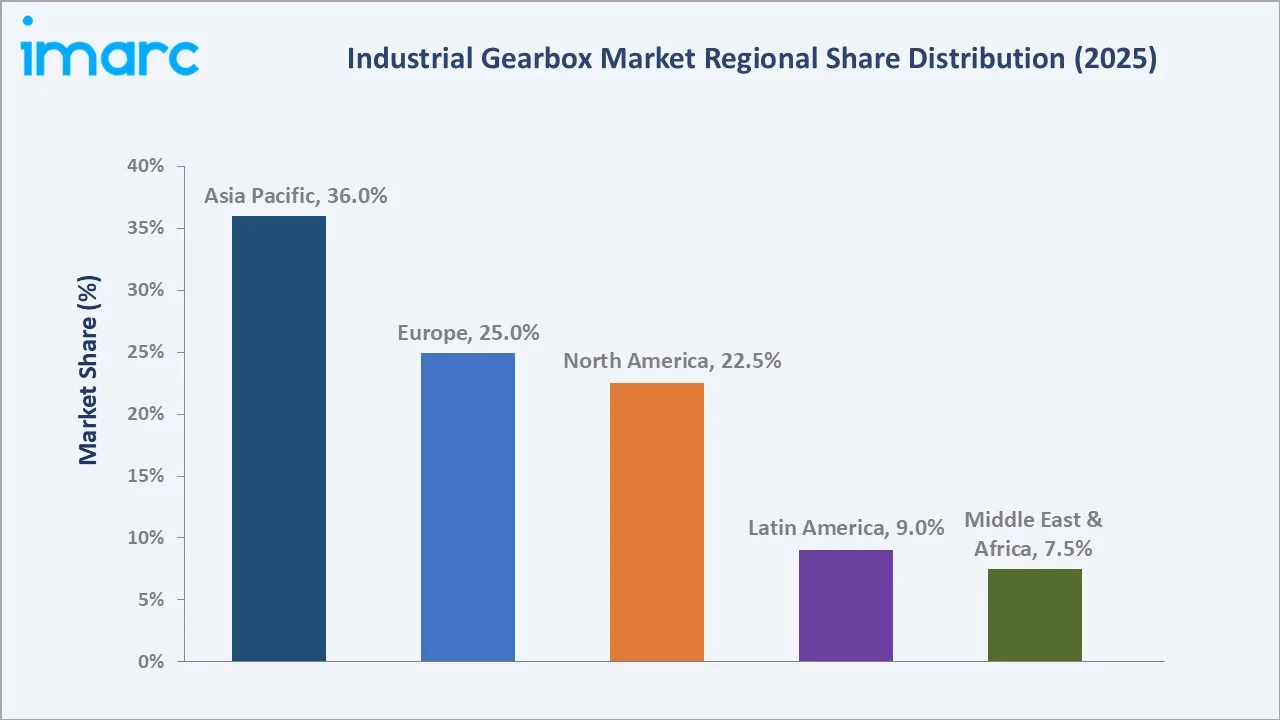

The global industrial gearbox market reached USD 32.44 Billion in 2025 and is projected to reach USD 46.27 Billion by 2034, growing at a CAGR of 3.90% during 2026-2034. The market is driven by rising automation, expanding manufacturing activities, and increasing demand for efficient power transmission systems across industries. The latest World Robotics 2025 statistics reported that 542,000 industrial robots were installed globally in 2024, more than twice the number recorded a decade ago. Annual robot installations have now exceeded 500,000 units for four consecutive years, highlighting the continued expansion of industrial automation. This trend is driving the industrial gearbox market as robots rely on precision gearboxes for accurate motion control, torque transmission, and operational efficiency. Helical gearbox leads type at 28.5%. Parallel axis design dominates at 46.0%. Asia Pacific commands 36.0% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 32.44 Billion |

|

Forecast Market Size (2034) |

USD 46.27 Billion |

|

CAGR (2026-2034) |

3.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Helical Gearbox (28.5%, 2025) |

|

Dominant Design |

Parallel Axis (46.0%, 2025) |

|

Leading Region |

Asia Pacific (36.0%, 2025) |

The global industrial gearbox market expanded from USD 26.79 Billion in 2020 to USD 32.44 Billion in 2025, anchored at USD 39.29 Billion in 2030, and forecast to reach USD 46.27 Billion by 2034. The COVID-19 pandemic disrupted gearbox supply chains and industrial capital expenditure, but the subsequent industrial recovery created above-trend gearbox demand through 2022-2024 as deferred maintenance and capacity expansion projects proceeded simultaneously above the steady-state replacement cycle.

To get more information on this market, Request Sample

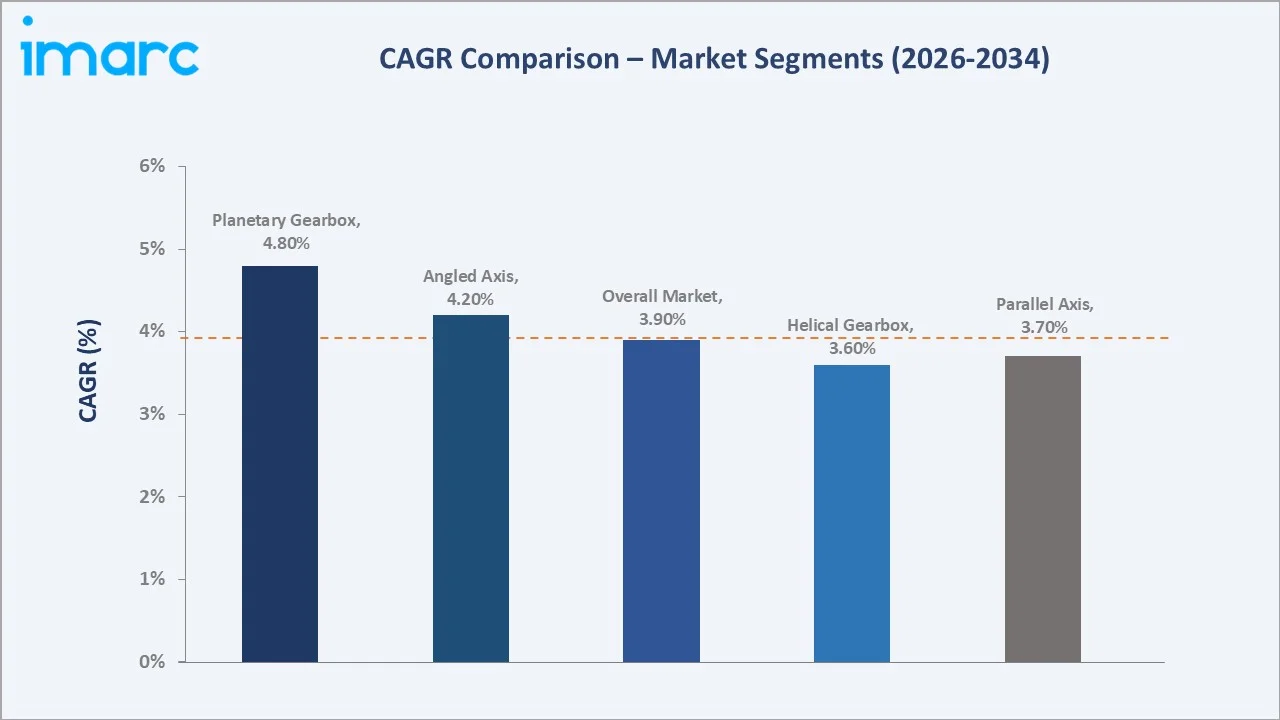

Planetary gearbox grows fastest at ~4.8% CAGR driven by wind turbine gearbox demand, collaborative robot joint gearbox adoption, and electric vehicle industrial machinery drive applications. Angled axis design grows at ~4.2% CAGR through bevel-helical right-angle drive adoption in conveyor, mixer, and food processing applications requiring compact directional change at reduced mounting footprint versus parallel shaft alternatives.

Executive Summary

The global industrial gearbox market at USD 32.44 Billion in 2025 represents one of the most commercially fundamental mechanical engineering product categories in the global industrial economy. The gearbox's role as the ubiquitous speed-torque interface creates structural demand across every industrial sector, such as cement, steel, mining, power generation, food processing, water treatment, oil and gas, and manufacturing automation, each creating distinct gearbox specification requirements and replacement cycle economics. The market is projected to reach USD 46.27 Billion by 2034.

Helical gearbox at 28.5% leads through commercial breadth, helical gears' smooth meshing, high efficiency, and broad torque range, creating the most commercially versatile gearbox type serving cement, mining, steel, water, food, and automotive manufacturing. Parallel axis design at 46.0% leads through cost-effective high-torque industrial drive economics. Asia Pacific leads at 36.0% through China's manufacturing and renewable energy infrastructure investment.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Helical Gearbox - 28.5% share (2025) |

|

Dominant Design |

Parallel Axis - 46.0% market share (2025) |

|

Leading Region |

Asia Pacific - 36.0% share (2025) |

|

Market Opportunity |

Wind energy planetary gearbox for multi-MW turbines; smart IoT-enabled condition monitoring gearboxes; mining and cement sector gearbox replacement; industrial automation servo gearbox for robotics |

Key Analytical Observations Supporting The Above Data:

- Helical Gearbox at 28.5%: Helical gearboxes dominate due to their high efficiency, smooth operation, low noise, and ability to handle heavy loads. Their wide use in manufacturing, conveyors, mining, material handling, and power transmission applications supports strong demand.

- Parallel Axis design at 46.0%: Parallel axis gearboxes dominate due to their compact design, high power transmission efficiency, and ability to handle high torque loads. Their widespread use in conveyors, material handling systems, manufacturing equipment, and heavy industrial machinery drives strong market demand.

- Asia Pacific at 36.0%: Asia Pacific dominates regionally due to rapid industrialization, expanding manufacturing output, and strong growth in automation across China, India, Japan, and Southeast Asia. Rising investments in energy, mining, construction, and material handling industries further support gearbox demand in the region.

Industrial Gearbox Market Overview

The global industrial gearbox market operates within the broader power transmission and industrial machinery components industry as the highest-torque-density single component in virtually every industrial drive system above a direct drive alternative. The gearbox market's commercial uniqueness is its installed base-driven aftermarket structure.

The industrial gearbox ecosystem integrates globally distributed steel and specialty alloy material supply, precision gear manufacturing, gearbox assembly and quality testing, distribution through industrial distributor networks, and aftermarket service through manufacturer service centres and independent gear repair specialists globally. Macroeconomic factors include industrialization, manufacturing expansion, rising infrastructure investment, and growing automation across production facilities.

Market Dynamics

To evaluate market opportunities, Request Sample

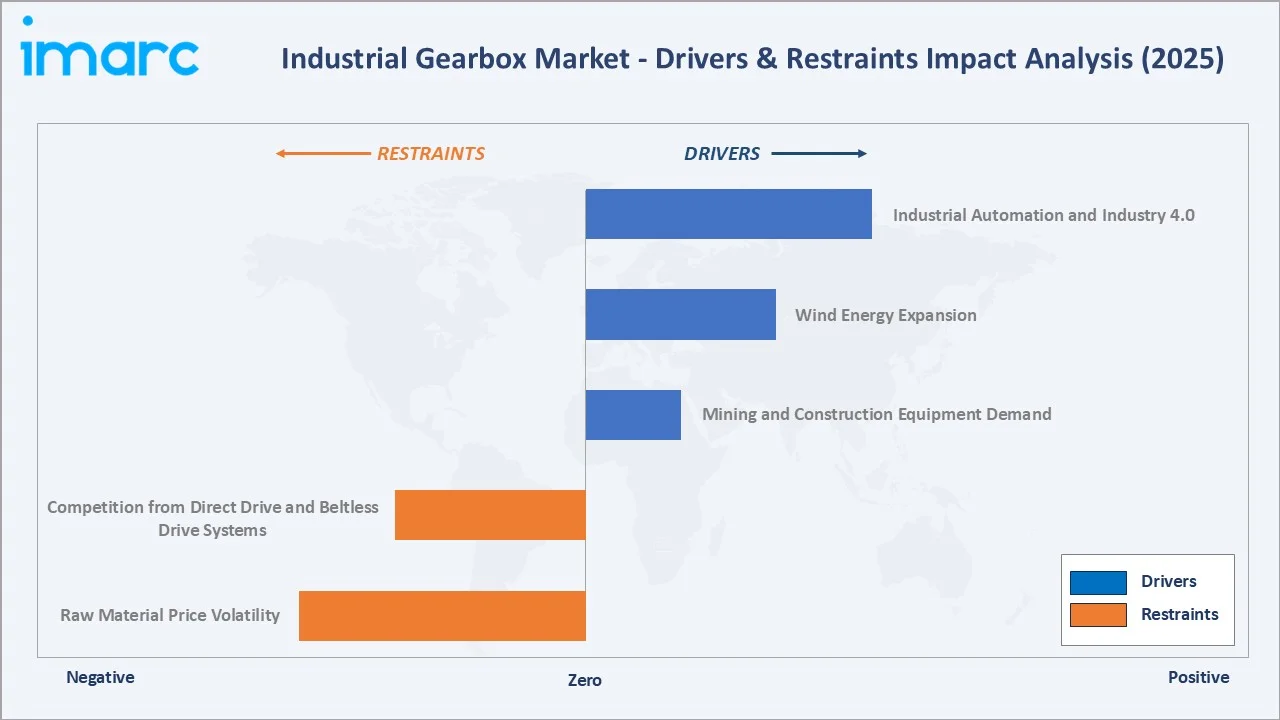

Market Drivers

- Industrial Automation and Industry 4.0: Industrial Automation and Industry 4.0 are increasing the adoption of automated machinery, robotics, and smart manufacturing systems that require reliable power transmission solutions. Industrial gearboxes play a critical role in controlling speed, torque, and motion in automated production lines. As manufacturers invest in Industry 4.0 technologies to improve productivity and operational efficiency, demand for high-performance and precision gearboxes continues to rise. The growing use of robotics, conveyor systems, and automated material handling equipment further supports market growth.

- Wind Energy Expansion: In 2025, wind energy played a record role in global electricity generation, with wind turbines producing enough power to meet over 11% of worldwide demand. This wind energy expansion is driving the market as wind turbines require gearboxes to convert low-speed rotor movement into high-speed generator rotation. Growing investments in onshore and offshore wind projects are increasing demand for durable, high-torque gearboxes. These systems must withstand variable loads, harsh weather, and continuous operation, encouraging innovation in reliability and efficiency. As renewable energy capacity expands, gearbox demand from wind turbine manufacturers and maintenance providers continues to rise.

- Mining and Construction Equipment Demand: Mining and construction equipment demand is driving market demand as heavy machinery, such as crushers, excavators, conveyors, loaders, and drilling systems, require robust gearboxes for torque transmission and speed control. Rising infrastructure development, urbanization, and mineral extraction activities are increasing the use of such equipment. Gearboxes help these machines operate efficiently under high-load and harsh working conditions. This supports demand for durable, high-performance industrial gearbox solutions.

Market Restraints

- Raw Material Price Volatility: Raw material price volatility increases the cost of key inputs such as steel, cast iron, aluminum, copper, and specialty alloys. Frequent price fluctuations make production costs unpredictable for gearbox manufacturers, affecting profit margins and pricing strategies. Higher material costs can also raise final gearbox prices, discouraging purchases from cost-sensitive industries. This creates challenges in long-term contracts, inventory planning, and competitive pricing.

- Competition from Direct Drive and Beltless Drive Systems: Competition from direct drive and beltless drive systems reduces or eliminates the need for traditional gearbox assemblies. Direct drive systems offer benefits such as lower maintenance, reduced mechanical losses, quieter operation, and higher energy efficiency. In applications where precision and compact design are critical, manufacturers may shift toward these solutions. This can limit gearbox demand, particularly in robotics, wind turbines, conveyors, and advanced automation systems.

Market Opportunities

- IoT-Connected Smart Gearbox: IoT-connected smart gearboxes enable real-time monitoring of temperature, vibration, load, lubrication, and performance. These insights help industries predict failures, reduce downtime, and shift from reactive to predictive maintenance. Smart gearboxes also improve operational efficiency by supporting remote diagnostics and data-driven asset management. As factories adopt Industry 4.0 and connected machinery, demand for intelligent gearbox solutions is expected to rise.

- Innovative Worm Gearbox: Innovative worm gearboxes offer high torque output, compact design, and smooth speed reduction in space-constrained applications. Their self-locking capability improves safety and positioning control in lifts, conveyors, solar trackers, packaging machines, and material handling systems. In March 2025, Stagnoli introduced Spinyx, an advanced worm gearbox designed to enhance power transmission performance. Made from technopolymer, a high-performance composite material, Spinyx offers strong operational efficiency while helping reduce maintenance costs. Advances in materials, lubrication, and efficiency are reducing traditional performance limitations. This supports adoption in automation, renewable energy, and precision industrial equipment.

Market Challenges

- High Maintenance and Lubrication Requirements: High maintenance and lubrication requirements pose a challenge as gearboxes require regular inspection, oil changes, and component servicing to ensure reliable performance. Inadequate lubrication can lead to increased friction, overheating, wear, and unexpected equipment failures. These maintenance needs increase operating costs and downtime, particularly in continuous-process industries. As a result, some end users may seek lower-maintenance alternatives such as direct drive systems.

- Noise and Heat Generation in Heavy-Duty Applications: Noise and heat generation in heavy-duty applications present a challenge as high-load operations can create excessive friction, vibration, and thermal stress. Prolonged exposure to these conditions can accelerate component wear, reduce efficiency, and increase the risk of equipment failure. Managing heat often requires additional cooling and lubrication systems, raising operational costs. These issues can also impact workplace conditions and encourage the adoption of quieter, more energy-efficient drive alternatives.

Emerging Market Trends

1. Predictive Maintenance and IoT Gearbox Condition Monitoring

Predictive maintenance and IoT gearbox condition monitoring are emerging as industries increasingly seek to reduce downtime and improve equipment reliability. Smart sensors continuously monitor parameters such as vibration, temperature, load, and lubrication levels, enabling early detection of potential failures. This allows operators to schedule maintenance proactively rather than reactively, reducing repair costs and production interruptions. As Industry 4.0 adoption grows, demand for connected and data-driven gearbox solutions is accelerating.

2. Planetary Gearbox Scale-Up for Multi-Megawatt Wind Turbines

Planetary gearbox scale-up for multi-megawatt wind turbines is emerging as larger turbines require higher torque capacity and improved power transmission efficiency. Advanced planetary gearboxes provide compact designs, high load distribution, and greater reliability for demanding onshore and offshore wind applications. Manufacturers are developing larger and more durable gearbox systems to support increasing turbine sizes and energy output. This trend is driving innovation in gearbox materials, design, and condition-monitoring technologies.

3. Gearbox Remanufacturing Creating Circular Economy Commercial Model

Gearbox remanufacturing extends the life of used gearboxes through repair, rebuilding, and component replacement. It helps reduce material waste, lowers replacement costs, and minimizes the environmental impact of manufacturing new units. Scania’s milestone gearbox remanufacturing project used around 50% less material and generated nearly 45% fewer carbon emissions compared to producing a new gearbox. Industries benefit from shorter lead times and cost-effective performance restoration. This model also creates recurring revenue opportunities for OEMs and service providers through refurbishment, maintenance, and lifecycle support.

4. Lightweight Composite and Additive-Manufactured Gearbox Components

Lightweight composite and additive-manufactured gearbox components are emerging as manufacturers seek stronger, lighter, and more customized power transmission solutions. 3D printing enables complex gear designs, rapid prototyping, and reduced material waste, while composites help lower equipment weight and improve energy efficiency. These technologies are especially useful in robotics, aerospace, wind energy, and compact industrial machinery. As industries prioritize performance, sustainability, and design flexibility, demand for advanced gearbox components is increasing.

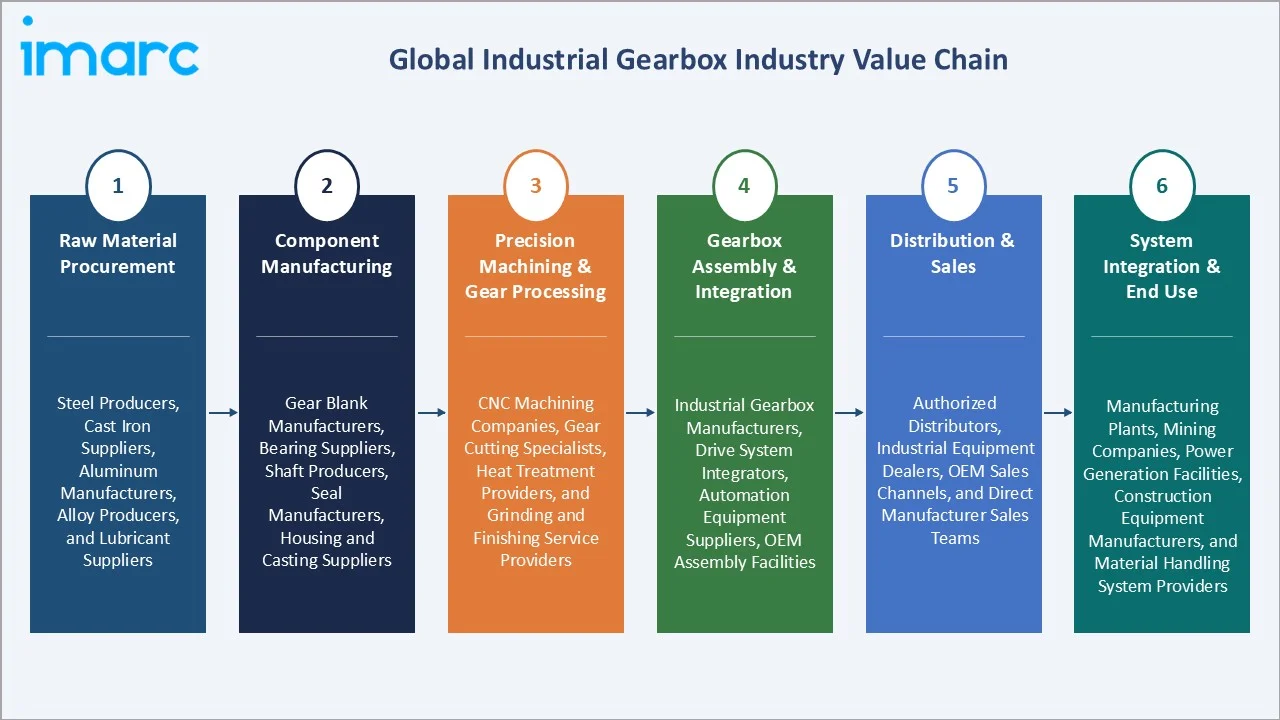

Industry Value Chain Analysis

The global industrial gearbox value chain encompasses raw material procurement, component manufacturing, precision machining & gear processing, gearbox assembly & integration, distribution & sales, and system integration & end use.

|

Stage |

Key Participants |

|

Raw Material Procurement |

Steel producers, cast iron suppliers, aluminum manufacturers, alloy producers, and lubricant suppliers |

|

Component Manufacturing |

Gear blank manufacturers, bearing suppliers, shaft producers, seal manufacturers, housing and casting suppliers |

|

Precision Machining & Gear Processing |

CNC machining companies, gear cutting specialists, heat treatment providers, and grinding and finishing service providers |

|

Gearbox Assembly & Integration |

Industrial gearbox manufacturers, drive system integrators, automation equipment suppliers, OEM assembly facilities |

|

Distribution & Sales |

Authorized distributors, industrial equipment dealers, OEM sales channels, and direct manufacturer sales teams |

|

System Integration & End Use |

Manufacturing plants, mining companies, power generation facilities, construction equipment manufacturers, and material handling system providers |

Precision machining and gear processing are the most commercially intensive quality-differentiation stage in the industrial gearbox value chain because it directly determines gearbox accuracy, efficiency, durability, and load-carrying performance. Advanced processes such as gear cutting, grinding, heat treatment, and finishing create tighter tolerances and smoother operation, enabling manufacturers to command premium pricing and differentiate their products in demanding industrial applications.

Technology Landscape in the Industrial Gearbox Industry

Gear Geometry and Material Science Advancement

Gear geometry and material science advancements are improving efficiency, load capacity, and operational lifespan. Optimized gear tooth designs reduce friction, vibration, and noise while enhancing torque transmission and power density. At the same time, the use of advanced alloys, surface coatings, and high-strength composite materials increases wear resistance and durability under demanding operating conditions. These innovations enable manufacturers to develop more compact, reliable, and energy-efficient gearbox solutions for modern industrial applications.

Digitalization and Intelligent Drive Systems

Digitalization and intelligent drive systems are integrating sensors, connectivity, and analytics into gearbox operations. Smart gearboxes can monitor parameters such as vibration, temperature, load, and lubrication in real time, enabling predictive maintenance and reducing unplanned downtime. These systems improve operational efficiency through data-driven performance optimization and remote diagnostics. As Industry 4.0 adoption accelerates, intelligent drive systems are becoming a key differentiator in modern industrial power transmission solutions.

Wind Turbine Gearbox Innovations

Wind turbine gearbox innovations enable higher torque transmission, greater reliability, and improved efficiency for increasingly larger turbines. Manufacturers are developing advanced planetary gearbox designs, stronger materials, and enhanced lubrication systems to withstand harsh operating conditions and variable loads. Integration of condition-monitoring sensors and predictive maintenance technologies is also helping reduce downtime and maintenance costs. In March 2026, Flender opened India’s largest wind turbine gearbox test rig at its Walajabad facility near Chennai, Tamil Nadu, with a 13.5 MW testing capacity. The advanced back-to-back electric test rig is built to assess next-generation wind turbine gearboxes under challenging operating conditions, handling torque of up to 18,000 kNm and tensile and compressive forces of up to 500 tonnes. This supports wind turbine gearbox innovation by strengthening testing capabilities for larger, high-capacity turbines.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Helical Gearbox |

28.5% |

2025 |

|

Design |

Parallel Axis |

46.0% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Asia Pacific |

36.0% |

2025 |

By Type

Helical gearbox leads at 28.5% (2025). The helical gearbox segment encompasses inline parallel shaft, offset shaft, and multi-stage helical configurations serving the broadest industrial application spectrum. Helical gearbox's ~3.6% CAGR reflects the type's mature market position with growth driven by replacement cycle and industrial capacity expansion above the above-market growth of planetary and precision gearbox types.

To access detailed market analysis, Request Sample

Planetary gearbox at 21.0% grows fastest at ~4.8% CAGR through wind energy and robotics. Bevel gearbox at 16.5% serves right-angle, and angle shaft drives for mixer, extruder, and marine applications. Spur gearbox at 13.5% serves low-speed simple drive applications. Worm gearbox at 11.0% serves self-locking high-ratio drives. Others at 9.5% include cycloidal, hypoid, and harmonic drive types serving specialty precision applications.

By Design

Parallel axis design leads at 46.0% (2025). The parallel axis configuration encompasses inline shaft and offset shaft helical gearboxes as well as spur gearboxes for direct-coupled motor-to-load drives, where the parallel shaft arrangement simplifies installation above angular shaft configurations. Parallel Axis's ~3.7% CAGR reflects the design's broad industrial base with steady growth from manufacturing capacity expansion.

Angled axis at 34.0% grows at ~4.2% CAGR through right-angle bevel-helical and solar tracker worm gearbox adoption. Others at 20.0% include epicyclic (planetary), cycloidal, and harmonic drive configurations serving specialty high-precision and high-torque-density applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Industrial Gearbox Market Drivers & Characteristics |

|

Asia Pacific |

36.0% |

Driven by rapid industrialization, expanding manufacturing output, and strong investments in automation across China, India, Japan, and Southeast Asia. |

|

Europe |

25.0% |

Driven by its advanced manufacturing sector, strong adoption of Industry 4.0 technologies, and leadership in renewable energy projects. |

|

North America |

22.5% |

Supported by increasing automation investments, modernization of industrial facilities, and growing demand from the energy, mining, and logistics sectors. |

|

Latin America |

9.0% |

Driven by expanding mining activities, agricultural processing industries, and infrastructure development projects. |

|

Middle East & Africa |

7.5% |

Supported by investments in oil and gas, mining, power generation, water treatment, and infrastructure projects. |

Asia Pacific's 36.0% market dominance reflects the region's combined manufacturing capacity, infrastructure investment, and renewable energy deployment, creating the world's most commercially active industrial gearbox procurement geography across new installation and replacement categories. Europe's 25.0% reflects Germany's leading gearbox manufacturing export base, alongside Europe's aging industrial infrastructure and wind energy gearbox investment. North America's 22.5% reflects the USA's oil and gas, mining, and manufacturing reshoring gearbox demand alongside the growing wind energy installation program.

Latin America's 9.0% is growing through Brazil's mining and sugar processing and copper mine expansion, creating above-regional high-torque gearbox demand. The Middle East and Africa's 7.5% is growing through Saudi Arabia's Vision 2030 industrial diversification and Sub-Saharan Africa's critical mineral mining development.

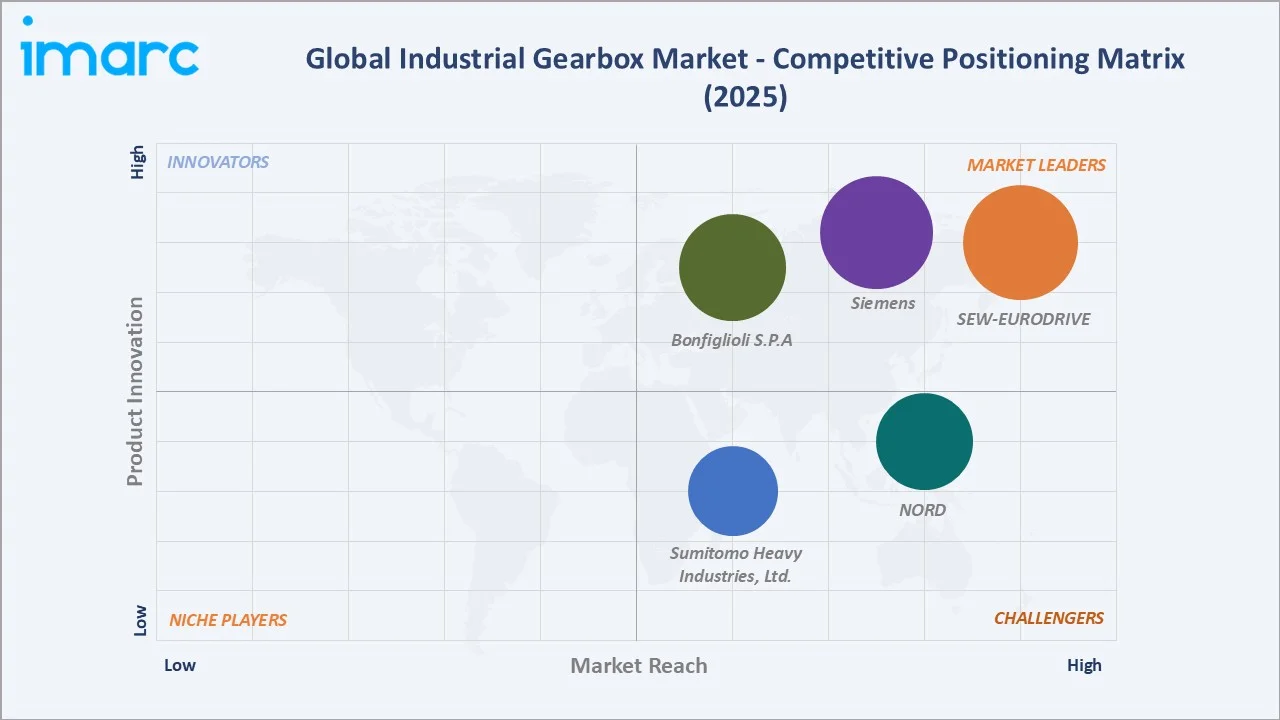

Competitive Landscape

The global industrial gearbox competitive landscape is commercially stratified across three tiers: European technology leaders, USA established players, and Asian manufacturers. The competitive landscape's most commercially consequential characteristic is the aftermarket revenue defensibility.

|

Company |

Key Products |

Market Position |

Core Strength |

|

|

R series helical gear units, F series parallel-shaft helical gear units, K series helical-bevel gear units, S series helical-worm gear units |

Market Leader |

SEW-EURODRIVE plays a central role in industrial gearboxes as a leading manufacturer of high-torque, durable drive solutions for heavy-duty applications like mining, cement, and material handling. |

|

|

SIMOGEAR Gearboxes |

Market Leader |

Siemens plays a critical role in industrial gearboxes by providing high-performance, energy-efficient, and durable gear units designed for automation, manufacturing, and heavy-duty sectors, notably enhancing sustainability through lightweight, compact, and low-maintenance designs. |

|

|

A Series, VF/W Series, RAN Series, AS Series, C Series |

Market Leader |

Bonfiglioli S.p.A. is a prominent leader in the design, manufacture, and distribution of a comprehensive range of gearboxes, electric motors, and drive systems. |

|

|

MAXXDRIVE Right-Angle Gear Units, MAXXDRIVE Parallel Gear Units |

Strong Challenger |

NORD plays a significant role in industrial gearboxes by manufacturing high-performance, modular, and energy-efficient drive technology. |

|

|

HEDCON Worm Gear Reducer, PARAMAX 9000 Series Reducer, PARAMAX SCC Series Reducer for Cranes |

Established Player |

Sumitomo Heavy Industries, Ltd., through its Sumitomo Drive Technologies division, is a global leader in power transmission, producing durable, high-efficiency, and precision gearboxes for heavy-duty industrial applications. |

The competitive landscape is being reshaped by three forces: Chinese gearbox manufacturers' quality improvement, digitalization service competition, and remanufacturing market competition.

Key Company Profiles

SEW-EURODRIVE

SEW-EURODRIVE is a global leader in drive technology and industrial automation solutions, with a strong presence in the industrial gearbox market. The company designs and manufactures a comprehensive portfolio of gear units, geared motors, industrial gearboxes, drive electronics, and motion control systems for applications across manufacturing, material handling, mining, and energy sectors.

- Key Products: R series helical gear units, F series parallel-shaft helical gear units, K series helical-bevel gear units, S series helical-worm gear units.

- Recent Developments: In July 2024, SEW-EURODRIVE launched XMiner Industrial Gear Units, designed for demanding mining and aggregates applications such as conveyors, crushers, and apron feeders. Based on the proven X.e series platform, the units are supported by local engineering, stocking, and assembly in Wellford, South Carolina, enabling faster and more reliable service for North American customers.

- Strategic Focus: Expanding its portfolio of high-performance industrial gearboxes and integrated drive solutions for heavy industries such as mining, material handling, logistics, and manufacturing.

Sumitomo Heavy Industries, Ltd.

Sumitomo Heavy Industries, Ltd. is a diversified industrial machinery and engineering company with a strong presence in the industrial gearbox market through its power transmission and control business. The company manufactures a wide range of industrial gearboxes, speed reducers, gear motors, cycloidal drives, and power transmission systems used in industries such as mining, material handling, manufacturing, energy, water treatment, and infrastructure.

- Key Products: HEDCON Worm Gear Reducer, PARAMAX 9000 Series Reducer, PARAMAX SCC Series Reducer for Cranes.

- Recent Developments: In January 2025, Sumitomo Heavy Industries launched its new easy-to-install, zero-backlash DA Series gear head for servo motors, under its Fine CYCLO high-precision gearbox portfolio. The product is designed for precision positioning applications and can be used in machine tools, semiconductor manufacturing equipment, and other advanced machinery.

- Strategic Focus: Developing high-precision, high-reliability gearbox solutions for industrial automation, robotics, semiconductor manufacturing, machine tools, and material handling applications.

Market Concentration Analysis

The global industrial gearbox market is moderately concentrated in the premium catalogue gearbox segment and highly fragmented in the heavy custom gearbox segment. Chinese domestic gearbox manufacturers collectively commanding an estimated 15-20% of global market value at below-European premium brand pricing reflect the industrial gearbox market's ongoing commoditization pressure in the standard catalogue gearbox tier. Market concentration is evolving through digital service differentiation, creating service contract revenue that sustains above-commodity pricing through data dependency and predictive maintenance value creation above pure mechanical product quality differentiation.

Investment & Growth Opportunities

Highest Growth Segments

Planetary gearbox for wind energy (~4.8% CAGR), angled axis solar tracker gearbox (~15-20% CAGR from emerging mass-volume application), IoT-enabled smart gearbox premium tier (~8-12% CAGR), mining high-torque mill gearbox (~5-6% CAGR through critical mineral capex), industrial robot joint precision gearbox (~6-8% CAGR through automation expansion), and MRO aftermarket replacement gearbox (~3.5% CAGR from aging industrial base) represent the highest-growth industrial gearbox investment vectors through 2034.

Emerging Investment Opportunities

The hydrogen economy's emerging industrial infrastructure represents the most commercially nascent but potentially most commercially significant new industrial gearbox application beyond 2030, with electrolysis capacity, creating structured gearbox demand from the global energy transition above the conventional industrial base's replacement-driven market.

Investment Themes

- Wind energy planetary gearbox manufacturing capacity investment for offshore wind market: Investment in multi-MW planetary gearbox manufacturing capability creates the technical qualification threshold for wind turbine OEM supply relationships that represent the most commercially stable long-term industrial gearbox revenue streams through 20-year wind farm service life.

- IoT condition monitoring service platform integration with industrial gearbox hardware: The industrial gearbox predictive maintenance market represents the most commercially transformative revenue model evolution for gearbox manufacturers from one-time capital equipment sale toward recurring annual monitoring subscription. Investment in vibration sensor integration, edge computing firmware, and cloud analytics platform creates the monitoring service platform that converts gearbox hardware revenue into multi-year service contract revenue at above-hardware gross margins.

Future Market Outlook (2026-2034)

The global industrial gearbox market is projected to grow from USD 32.44 Billion in 2025 to USD 46.27 Billion by 2034, delivering a 3.90% CAGR over the forecast period. The market's anchor value of USD 39.29 Billion in 2030 represents the industrial gearbox industry at its most commercially active structural phase. Asia Pacific's manufacturing and renewable energy investment reaching full commercial velocity, European wind energy repowering creating the continent's most significant gearbox replacement program in two decades, and North America's manufacturing reshoring and clean energy investment creating above-historical-trend new industrial gearbox procurement.

Three structural forces define the industrial gearbox market's growth through 2034: the renewable energy transition creates the most commercially certain above-trend demand driver, industrial automation creates the second commercially certain driver, and the aging industrial installed base creates the third commercially certain driver.

Research Methodology

Primary Research

Primary research comprised structured interviews with global industrial gearbox industry stakeholders, including R&D directors, technical sales managers, procurement engineers, maintenance managers, wind energy OEM drivetrain engineers, and an industry survey from industrial facility operators across Asia Pacific, Europe, and North America.

Secondary Research

Secondary research encompassed gear manufacturers' market outlook, global wind report, world energy outlook, global mining capex forecast, company annual reports, world robotics report, and renewable power generation costs. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using an end-use sector model: global industrial gearbox demand estimated by summing seven major end-use sectors multiplied by sector-specific gearbox intensity ratio and sector-specific capital expenditure forecast. Replacement cycle overlay applied using estimated global installed gearbox population by vintage decade with design life assumptions.

Industrial Gearbox Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Helical Gearbox, Planetary Gearbox, Bevel Gearbox, Spur Gearbox, Worm Gearbox, Others |

| Designs Covered | Parallel Axis, Angled Axis, Others |

| Applications Covered | Construction and Mining Equipment, Automotive, Chemicals, Rubber and Plastic, Wind Power, Material Handling, Power Generation, Agriculture, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | SEW-EURODRIVE, Siemens, Bonfiglioli S.P.A, NORD, Sumitomo Heavy Industries Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the industrial gearbox market from 2020-2034.

- The research report study provides the latest information on the market drivers, challenges, and opportunities in the global industrial gearbox market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the industrial gearbox industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Industrial Gearbox Market Report

The global industrial gearbox market reached USD 32.44 Billion in 2025, driven by rising automation, expanding manufacturing activity, and growing demand for efficient power transmission systems. Increasing adoption across wind energy, mining, construction, material handling, and process industries further supports market growth.

The global industrial gearbox market grows at 3.90% CAGR during 2026-2034, reaching USD 46.27 Billion by 2034. The overall growth is sustained by wind energy expansion, industrial automation, mining critical mineral investment, and the aging industrial installed base's replacement cycle.

Helical gearbox leads at 28.5% through the gear type's superior commercial characteristics, smooth meshing, mechanical efficiency, and torque range applicability, creating the most commercially versatile gearbox type serving virtually every industrial sector.

Parallel axis design leads at 46.0% through the configuration's optimal commercial economics for horizontal-to-horizontal industrial drive, manufacturing simplicity creating the lowest cost per kilowatt transmitted of any gearbox design through established gear hobbing on standard CNC equipment.

Asia Pacific leads at 36.0% through China's manufacturing output, creating the world's most concentrated single-region industrial gearbox procurement, India's Manufacturing and wind energy target creating above-CAGR emerging market growth, and Japan's precision automation sector creating Asia Pacific's highest per-unit-value gearbox demand.

Leading companies include SEW-EURODRIVE, Siemens, Bonfiglioli S.P.A, NORD, and Sumitomo Heavy Industries, Ltd., among others.

The global industrial gearbox market is projected to reach approximately USD 39.29 Billion by 2030, with planetary gearboxes reaching 24-25% market share through wind energy installation, above helical's progressive market share erosion, IoT condition monitoring becoming a standard gearbox specification in cement, mining, and power generation sector procurement above current optional add-on status, and solar tracker worm gearbox transformation.

Three priority investment opportunities: Wind energy planetary gearbox manufacturing for offshore wind premium segment creating the most commercially high-value per-unit gearbox procurement, IoT condition monitoring service platform creating recurring monitoring subscription revenue above hardware sale at 3-5x lifetime customer value versus transactional gearbox supply, and mining critical mineral sector high-torque mill gearbox engineering investment targeting copper, lithium, and nickel mine development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)