Japan Green Data Center Market Size, Share, Trends and Forecast by Component, Data Center Type, Industry Vertical, and Region, 2026-2034

Japan Green Data Center Market Size, Share, Trends & Forecast (2026-2034)

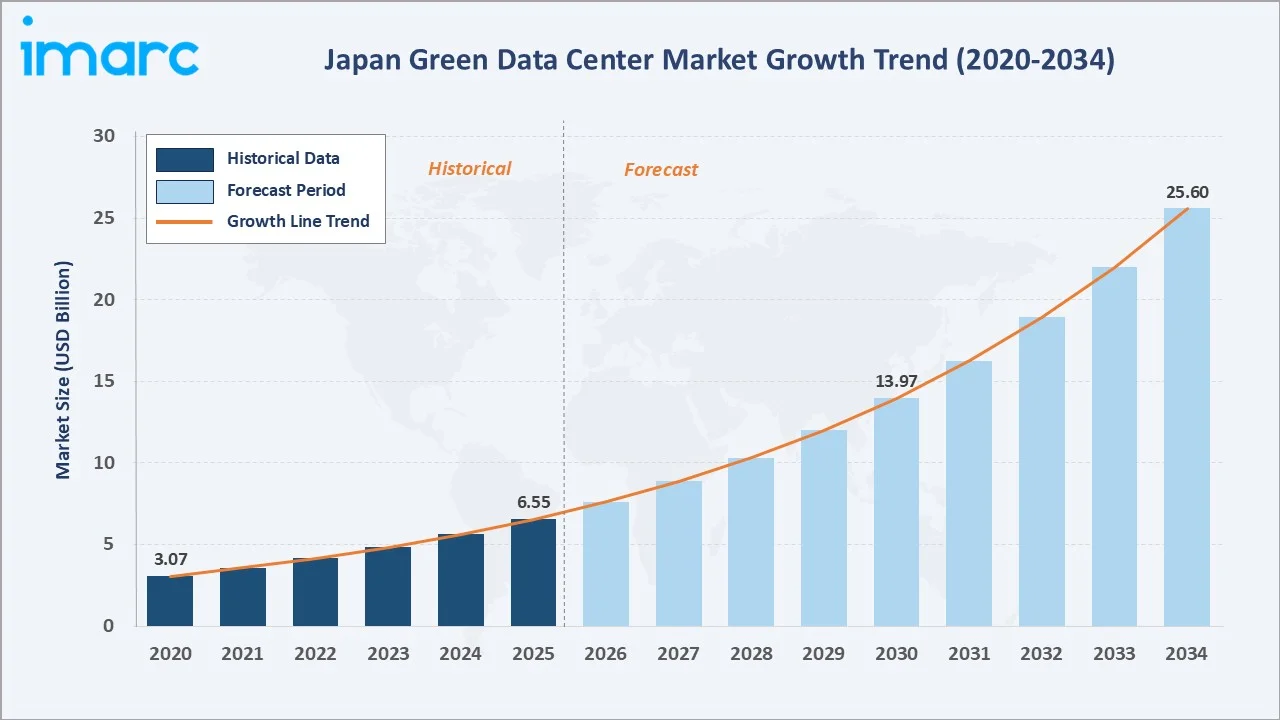

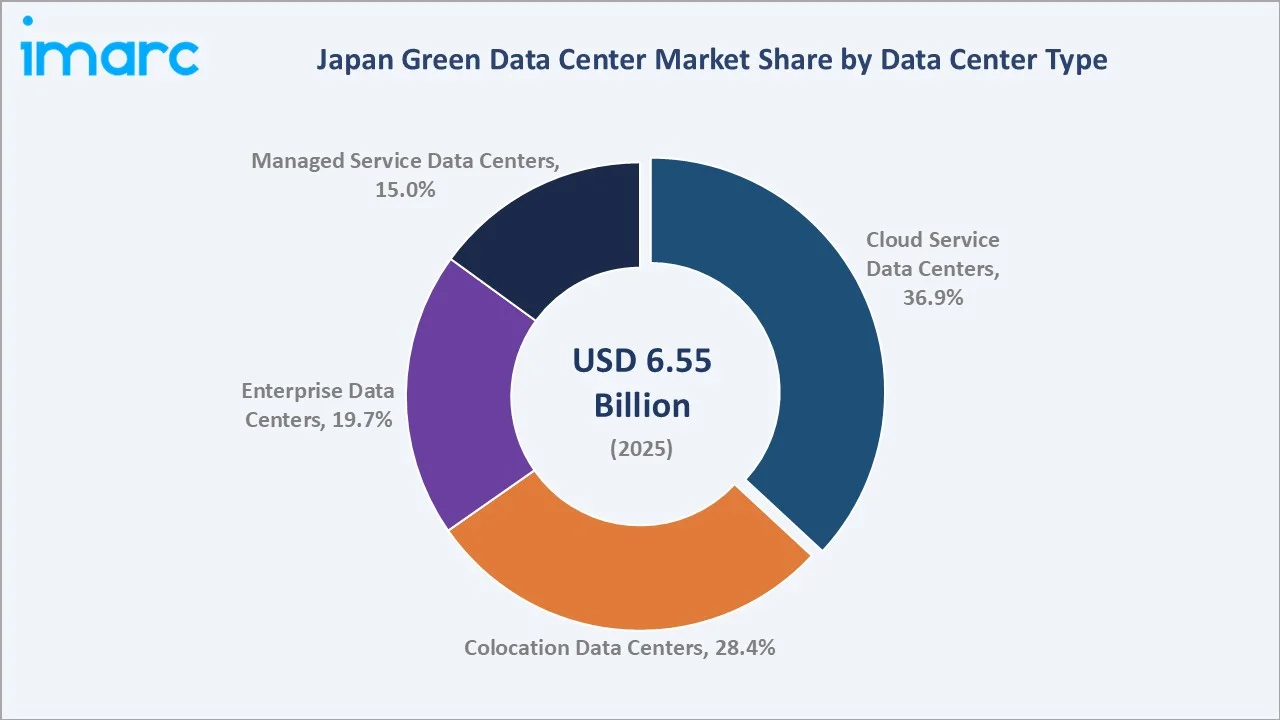

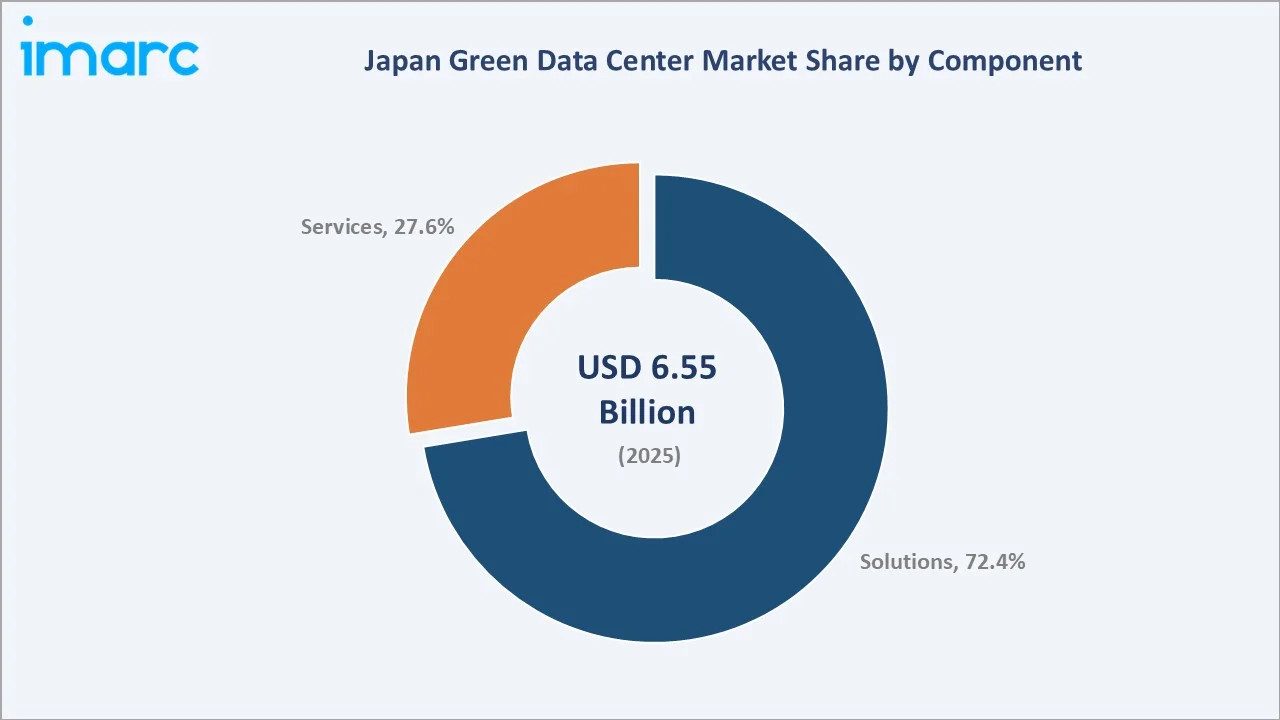

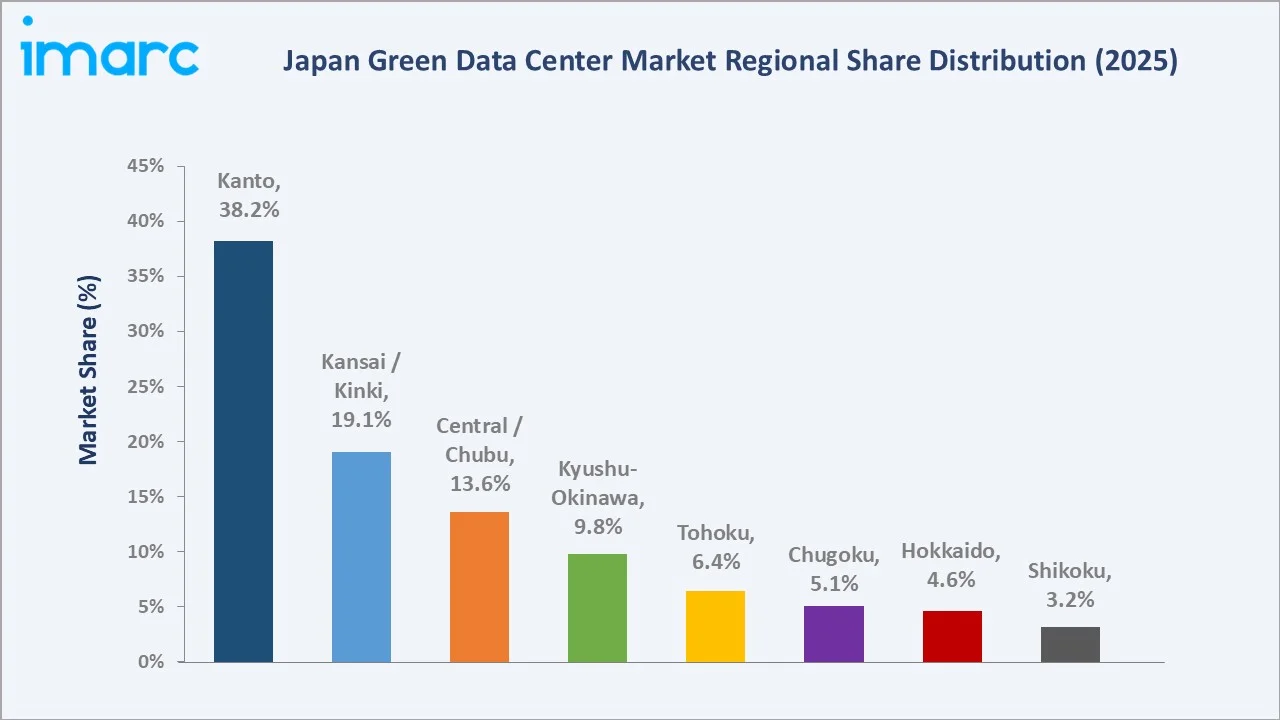

The Japan green data center market size was valued at USD 6.55 Billion in 2025 and is projected to reach USD 25.60 Billion by 2034, exhibiting a CAGR of 16.35% during the forecast period 2026-2034. Surging hyperscale and AI compute demand, the country's Net-Zero 2050 commitment, and growing renewable power availability are driving the Japan green data center market growth. Cloud service data centers lead at 36.9% share in 2025, while solutions account for 72.4% of total revenue. The Kanto region dominates with 38.2% of national demand in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.55 Billion |

|

Forecast Market Size (2034) |

USD 25.60 Billion |

|

CAGR (2026-2034) |

16.35% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto (38.2% share, 2025) |

|

Leading Data Center Type |

Cloud Service Data Centers (36.9%, 2025) |

|

Leading Component |

Solutions (72.4%, 2025) |

The Japan green data center market growth trajectory from 2020 through 2034 contrasts a steady historical expansion against a steep forecast curve, supported by AI compute build-outs, the GX League policy framework, expanding solar and offshore wind capacity, and accelerated cloud adoption across enterprise and government workloads.

To get more information on this market, Request Sample

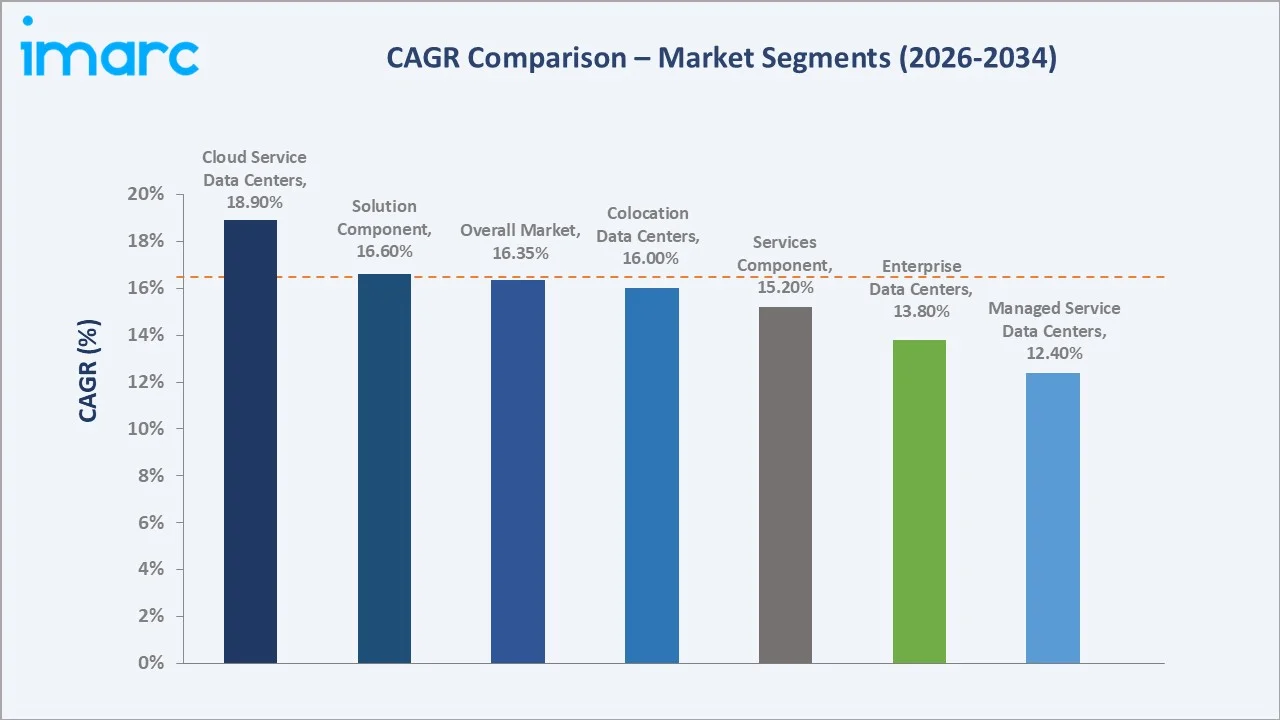

Segment-level CAGR comparisons highlight cloud service data centers and the solutions component as the fastest-growing sub-segments within the broader Japan green data center market forecast through 2034, while traditional managed-service and enterprise data centers grow at a more measured pace.

Executive Summary

The Japan green data center market is undergoing a profound structural transformation. It is shaped by surging AI workloads, the country's binding Net-Zero 2050 commitment declared by Prime Minister Suga in October 2020, and the rapid scale-up of renewable power purchase agreements (PPAs). Valued at USD 6.55 Billion in 2025, the market is projected to reach USD 25.60 Billion by 2034 at a CAGR of 16.35%, expanding strongly from USD 3.07 Billion recorded in 2020.

Cloud service data centers command 36.9% of market revenue in 2025, propelled by hyperscaler expansions from AWS, Google Cloud, Microsoft Azure, and Oracle Cloud across Tokyo and Osaka. Colocation data centers follow at 28.4%, supported by Equinix, NTT, KDDI Telehouse, and AirTrunk capacity. Enterprise data centers contribute 19.7%, while managed service data centers account for 15.0%. Solutions dominate the component mix at 72.4%, anchored by power infrastructure, advanced cooling systems, and energy management software.

The Kanto region leads with a 38.2% revenue share in 2025, anchored by Tokyo, Inzai, and Chiba data center clusters. Kansai/Kinki follows at 19.1% and Central/Chubu at 13.6%. The Japan green data center market outlook remains exceptionally strong as AI hyperscale demand, GX League decarbonization mandates, liquid cooling adoption, and emerging hydrogen-powered backup systems converge across all eight Japanese regions through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Data Center Type |

Cloud Service Data Centers – 36.9% share (2025) |

|

Second Data Center Type |

Colocation Data Centers – 28.4% share (2025) |

|

Largest Component |

Solutions – 72.4% share (2025) |

|

Fastest-Growing Sub-Segment |

Cloud Service Data Centers – ~18.9% CAGR (2026-2034) |

|

Leading Region |

Kanto – 38.2% revenue share (2025) |

|

Top Companies |

NTT Docomo Business Inc., Equinix Inc., KDDI Corporation, AirTrunk Operating Pty Ltd, Digital Edge (Singapore) Holdings Pte Ltd |

|

Forecast Market Size (2034) |

USD 25.60 Billion |

Key Analytical Observations Supporting the Above Data:

- Cloud service data centers' 36.9% dominance in 2025 reflects multi-billion-dollar hyperscaler commitments by AWS, Google Cloud, Microsoft Azure, and Oracle Cloud. AWS announced over JPY 2.2 trillion in Japan cloud infrastructure investment through 2027 alongside multiple new availability zones.

- Colocation data centers' 28.4% share is anchored by Equinix, NTT Communications, KDDI Telehouse, AirTrunk, and Digital Edge facilities concentrated in Tokyo's Inzai and Osaka's Keihanna technology corridors that serve banking, telecom, and platform-economy customers.

- Enterprise data centers' 19.7% position captures large in-house facilities operated by financial institutions, manufacturers, and telecom carriers. While growing slower than hyperscale, enterprise centers are migrating to liquid cooling and renewable PPAs to meet GX League reporting requirements.

- Managed service data centers' 15.0% share reflects demand from mid-market enterprises outsourcing facility operations to NTT, Fujitsu, NEC, and IDC Frontier (SoftBank). The segment grows steadily as cloud migration continues across Japan's enterprise base.

- Solutions' 72.4% revenue share captures power infrastructure, advanced cooling systems, energy management software, UPS units, and racks. Schneider Electric, Vertiv, ABB, and Daikin lead the solutions ecosystem across Japanese green data center deployments.

- Kanto's 38.2% regional dominance is underpinned by Tokyo, Inzai (Chiba), and Yokohama clusters. The region hosts the country's deepest fibre network, abundant utility power capacity, and proximity to enterprise and financial-services demand drivers across Japan's largest economic hub.

Japan Green Data Center Market Overview

Green data centers are facilities designed and operated to minimize environmental impact through high-efficiency cooling, renewable energy procurement, low-PUE (power usage effectiveness) architecture, and circular hardware management. The Japan green data center market spans cloud service, colocation, enterprise, and managed-service facilities, supported by an ecosystem of solutions and services covering power, cooling, monitoring, and sustainability consulting.

The industry sits at the intersection of digital infrastructure, energy policy, and corporate climate strategy. Macroeconomic and policy drivers include the Net-Zero 2050 declaration, the GX League framework launched by METI in 2023, METI's June 2024 GX 2040 policy direction, and tightening corporate ESG disclosure under the Tokyo Stock Exchange Prime Market. The Japan green data center industry analysis must also factor in the country's energy mix, which targets 36-38% renewables in power generation by FY2030 according to the 6th Strategic Energy Plan.

Market Dynamics

To evaluate market opportunities, Request Sample

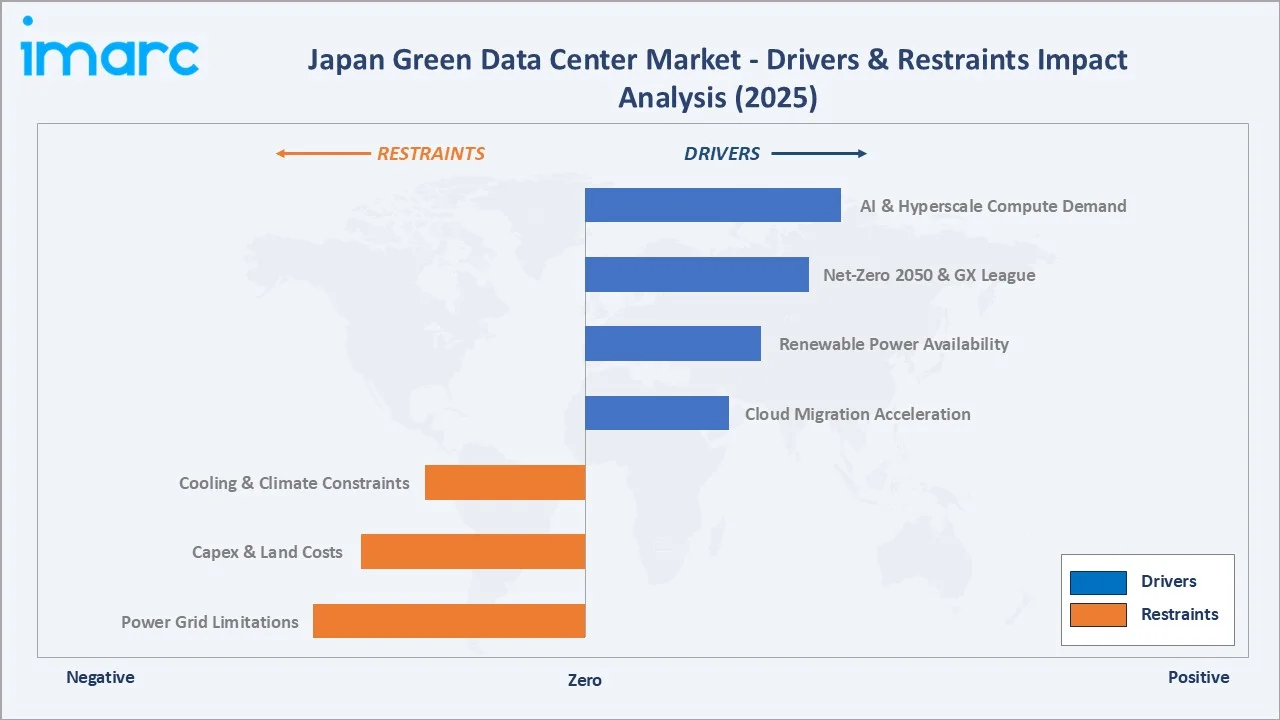

Market Drivers

- AI and Hyperscale Compute Demand: Generative AI workloads, large language model training, and inference at scale drove unprecedented compute demand through 2024-2025. AWS announced approximately JPY 2.2 trillion of Japan cloud infrastructure investment through 2027, while Microsoft committed over $10 billion across two years for new Japan AI data centers.

- Net-Zero 2050 Mandate and GX League: Japan's binding Net-Zero 2050 commitment, alongside the GX League framework launched by METI in 2023, requires major data center operators to disclose Scope 1, 2, and 3 emissions and progress toward science-based reduction targets. This pushes operators toward green-by-design facilities.

- Renewable Power Availability: Japan's renewable power capacity expanded materially through 2024. Corporate PPA volumes signed by data center operators rose sharply, with NTT, KDDI, and Equinix announcing multi-hundred-megawatt solar and offshore wind PPAs to anchor green facility operations.

- Cloud Migration Acceleration: Japan's enterprise cloud migration accelerated through 2023-2025, with banks, manufacturers, and government agencies shifting workloads to AWS Tokyo and Osaka, Google Cloud Tokyo and Osaka, and Microsoft Azure Japan East and West. The shift sustains hyperscale data center demand growth.

Market Restraints

- Power Grid Limitations: Japan's regional grid interconnection capacity, particularly between TEPCO and KEPCO service areas, constrains site selection for high-density AI data centers. Grid upgrade timelines and access queues remain meaningful bottlenecks for new hyperscale builds in Kanto and Kansai.

- Capex and Land Costs: Land prices in Inzai (Chiba) and Greater Osaka have risen sharply since 2022 as hyperscale operators competed for sites. Combined with rising construction costs and currency volatility for imported equipment, total facility capex per megawatt has stayed elevated through 2024-2025.

- Cooling and Climate Constraints: Tokyo's hot, humid summers create year-round cooling load. Free-cooling efficiency is limited compared to Hokkaido or Tohoku, increasing operational PUE. Operators are responding with liquid cooling and immersion-cooling deployments, but retrofit costs are high.

Market Opportunities

- Hokkaido and Tohoku Hyperscale Migration: Cooler climates, abundant land, and growing wind and solar capacity make Hokkaido and Tohoku attractive for next-generation green data center campuses. AirTrunk, Mitsui, Rapidus-adjacent infrastructure, and several hyperscalers announced 2024-2025 site studies in these regions.

- Hydrogen and Fuel Cell Backup: Japan's national hydrogen strategy supports pilot deployments of hydrogen fuel cells for data center backup power. Several Japanese operators announced 2024 pilots replacing diesel generators with hydrogen or ammonia-based clean backup solutions.

Market Challenges

- Skilled Talent Gap: Hiring qualified data center engineers, power systems specialists, and sustainability operations talent remains a structural challenge. METI estimates a multi-thousand-engineer shortfall in digital infrastructure roles persisting through 2030.

- Renewable PPA Pricing and Volatility: Wholesale electricity prices and PPA tariffs swung materially during 2022-2024, complicating long-term financial planning for green data center investments. Operators must hedge power exposure across multi-year horizons to maintain pricing stability for their customers.

Emerging Market Trends

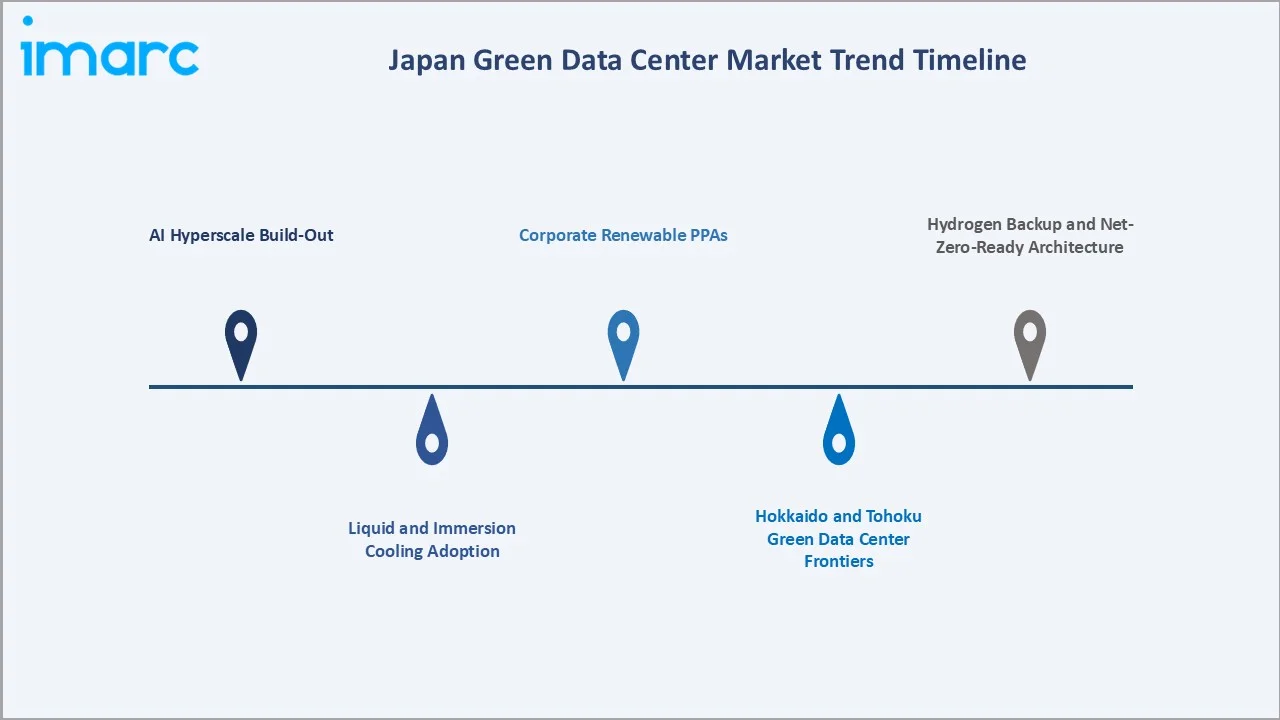

1. AI Hyperscale Build-Out

AI workloads are reshaping Japan's data center landscape. AWS announced approximately JPY 2.2 trillion in Japan cloud infrastructure investment through 2027, while Microsoft committed over $ 10 billion across two years for new Japan AI capacity. AI-grade GPU clusters are driving rack power densities from 8-12 kW to 40-100 kW per rack.

2. Liquid and Immersion Cooling Adoption

Liquid cooling and immersion cooling are scaling rapidly to handle high-density AI compute. Direct-to-chip cooling deployments expanded through 2024-2025 across Tokyo and Osaka facilities, with several Japanese operators commissioning pilot immersion-cooling pods supplied by global vendors and local engineering partners.

3. Corporate Renewable PPAs

Corporate PPA volumes signed by Japanese data center operators rose sharply through 2024. NTT, KDDI, and Equinix announced multi-hundred-megawatt solar and offshore wind PPAs to anchor green facility operations and meet customer Scope 3 emissions reduction commitments under the GX League framework.

4. Hokkaido and Tohoku as Green Data Center Frontiers

Cooler climates, lower land costs, and growing renewable capacity make Hokkaido and Tohoku attractive for green hyperscale campuses. AirTrunk, Mitsui & Co., and several global hyperscalers announced 2024-2025 site evaluations and capacity commitments across Ishikari (Hokkaido) and northern Tohoku prefectures.

5. Hydrogen Backup and Net-Zero-Ready Architecture

Aligned with Japan's national hydrogen strategy, several operators began 2024 pilots of hydrogen fuel cells and ammonia-based clean backup power. Net-zero-ready architecture - including modular power, smart UPS, and AI-driven energy management - is emerging as the new design standard for green Japanese data centers.

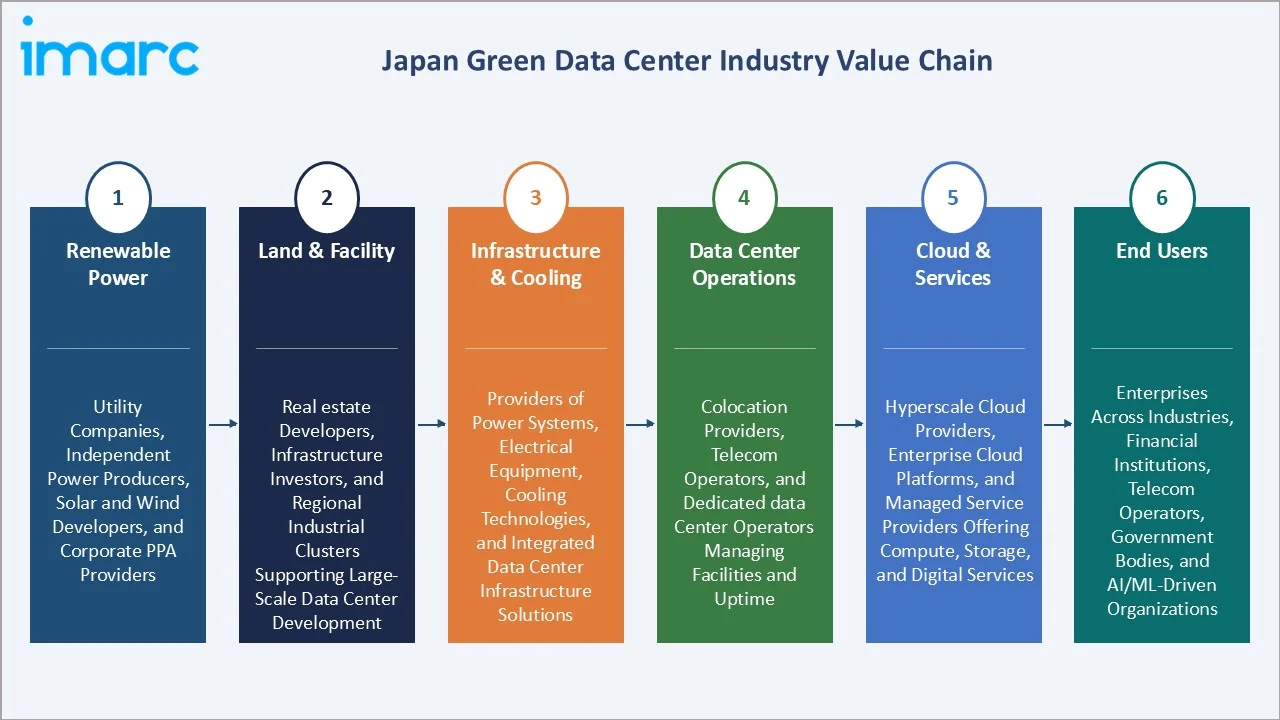

Industry Value Chain Analysis

The Japan green data center industry value chain spans six integrated stages from renewable power generation through end-user workload delivery. Each stage shows distinct margin, capex, and regulatory profiles that shape the broader Japan green data center market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Renewable Power |

Utility companies, independent power producers, solar and wind developers, and corporate power purchase agreement (PPA) providers |

|

Land & Facility |

Real estate developers, infrastructure investors, and regional industrial clusters supporting large-scale data center development |

|

Infrastructure & Cooling |

Providers of power systems, electrical equipment, cooling technologies, and integrated data center infrastructure solutions |

|

Data Center Operations |

Colocation providers, telecom operators, and dedicated data center operators managing facilities and uptime |

|

Cloud & Services |

Hyperscale cloud providers, enterprise cloud platforms, and managed service providers offering compute, storage, and digital services |

|

End Users |

Enterprises across industries, financial institutions, telecom operators, government bodies, and AI/ML-driven organizations |

Hyperscale cloud providers and large colocation operators capture the highest strategic value by combining scale, sustainability credentials, and tier-3/4 reliability. Specialized infrastructure suppliers continue to differentiate through liquid-cooling expertise, modular power solutions, and AI-driven energy management software that helps operators meet GX League reporting requirements.

Technology Landscape in the Japan Green Data Center Industry

Power Infrastructure and Renewable Integration

Japanese green data centers increasingly integrate corporate PPAs, on-site solar, and battery energy storage systems. Lithium-iron-phosphate (LFP) battery deployments have scaled meaningfully since 2023, supporting both peak-shaving and renewable smoothing across major Tokyo and Osaka facilities.

Liquid Cooling, Immersion Cooling, and Free Cooling

Direct-to-chip liquid cooling and single-phase immersion cooling are now standard considerations for new AI builds. Free-cooling air handlers and adiabatic systems remain widely deployed in Hokkaido and Tohoku, where ambient temperatures support year-round high-efficiency operations.

Energy Management Software and DCIM

Data center infrastructure management (DCIM) platforms from Schneider Electric, Vertiv, and Japanese system integrators provide real-time PUE monitoring, equipment-level energy analytics, and AI-driven optimization. These platforms have become essential for GX League Scope 1 and 2 reporting compliance.

Hydrogen, Ammonia, and Clean Backup Power

Aligned with Japan's national hydrogen strategy, several Japanese data center operators announced 2024 pilots of hydrogen fuel cells and ammonia-based clean backup power. These deployments target replacement of diesel generators by 2030-2034 and represent a high-margin frontier for clean-tech equipment suppliers across the country.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the Japan green data center market, along with forecasts at the national and regional level from 2026 to 2034. The market has been categorized based on data center type and component.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Solutions | 72.4% | 2025 |

| Data Center Type | Cloud Service Data Centers | 36.9% | 2025 |

| Industry Vertical | 🔒 | 🔒 | 2025 |

| Region | Kanto Region | 38.2% | 2025 |

By Data Center Type

Cloud service data centers lead the Japan market with a 36.9% share in 2025. This segment is propelled by hyperscaler expansion across Tokyo and Osaka, with AWS announcing approximately JPY 2.2 trillion of cloud infrastructure investment through 2027 and Microsoft committing over $10 billion across two years for new Japan AI data centers. The category is also the fastest-growing sub-segment, projected to advance at roughly 18.9% CAGR through 2034 on the back of generative AI workloads.

To access detailed market analysis, Request Sample

Colocation data centers hold 28.4% of revenue and are anchored by Equinix Tokyo, NTT Communications, KDDI Telehouse, AirTrunk Tokyo and Osaka, and Digital Edge facilities. Demand is fuelled by hyperscale customers, banks, and telecom carriers seeking carrier-neutral connectivity and renewable-powered capacity. Enterprise data centers contribute 19.7%, driven by large in-house facilities operated by financial institutions, manufacturers, and telecom carriers across Kanto and Kansai. Managed service data centers account for 15.0%, supported by NTT, Fujitsu, NEC, and IDC Frontier (SoftBank) operations that serve mid-market enterprises across the country.

By Component

Solutions are the dominant component at 72.4% of Japan green data center market revenue in 2025. This share captures power infrastructure (UPS systems, switchgear, transformers, generators), advanced cooling systems (CRAC/CRAH units, liquid cooling, immersion cooling), racks and structured cabling, energy management software, and DCIM platforms. Schneider Electric, Vertiv, ABB, Mitsubishi Electric, Daikin, and NEC lead the solutions ecosystem across Japanese green facility deployments.

Services account for 27.6% of Japan green data center revenue in 2025. The category covers consulting, system integration, design and engineering, installation and commissioning, sustainability advisory, GX League reporting support, and ongoing maintenance contracts. Services are growing steadily as operators upgrade legacy facilities to meet Net-Zero 2050 commitments and require specialist expertise across renewable PPA structuring, liquid cooling deployment, and AI-grade rack infrastructure. NTT Facilities, Fujitsu, NEC, and Schneider Electric lead the services side of the market.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto |

38.2% |

Tokyo, Inzai, Yokohama clusters; deepest fibre network; financial-services demand |

|

Kansai / Kinki |

19.1% |

Osaka data center hub, Keihanna technology cluster, hyperscaler Osaka availability zones |

|

Central / Chubu |

13.6% |

Nagoya manufacturing hub, automotive sector cloud workloads, Aichi enterprise demand |

|

Kyushu-Okinawa |

9.8% |

Fukuoka tech corridor, growing AI campus interest, southern connectivity to Asia |

|

Tohoku |

6.4% |

Cool climate, renewable power capacity, AirTrunk and hyperscale site evaluations |

|

Chugoku |

5.1% |

Hiroshima industrial base, growing colocation deployments, regional cloud demand |

|

Hokkaido |

4.6% |

Cold-climate free cooling, Ishikari new-build cluster, abundant wind capacity |

|

Shikoku |

3.2% |

Smaller regional market, niche enterprise and managed-service workloads |

The Kanto region leads with a 38.2% revenue share in 2025. Tokyo, Inzai (Chiba), and Yokohama host the country's deepest fibre network, abundant utility power capacity, and proximity to Japan's financial-services and platform-economy demand. Kanto is home to AWS Tokyo, Google Cloud Tokyo, Microsoft Azure Japan East, and the largest Equinix, NTT Communications, and KDDI Telehouse colocation footprints in the country.

Kansai/Kinki holds 19.1% of national revenue, anchored by Osaka as the country's secondary data center hub. AWS Osaka, Google Cloud Osaka, and Microsoft Azure Japan West availability zones support the region's growth, with operators such as Equinix, NTT, and AirTrunk continuing to expand Osaka colocation capacity through 2024-2025. The Keihanna technology cluster also contributes specialty deployments.

Central/Chubu contributes 13.6%, led by Nagoya and the broader Aichi prefecture manufacturing base. Automotive sector cloud workloads, supplier-network connectivity, and regional enterprise demand drive steady colocation and managed-service growth. Kyushu-Okinawa accounts for 9.8%, anchored by Fukuoka's growing tech corridor and rising hyperscale interest. Tohoku at 6.4% is gaining attention for its cool climate and abundant renewable power, with AirTrunk and hyperscale operators announcing 2024-2025 site evaluations. Chugoku (5.1%), Hokkaido (4.6%), and Shikoku (3.2%) round out the regional landscape, with Hokkaido in particular emerging as a key green data center frontier given its cold-climate free-cooling advantages and Ishikari's new-build cluster.

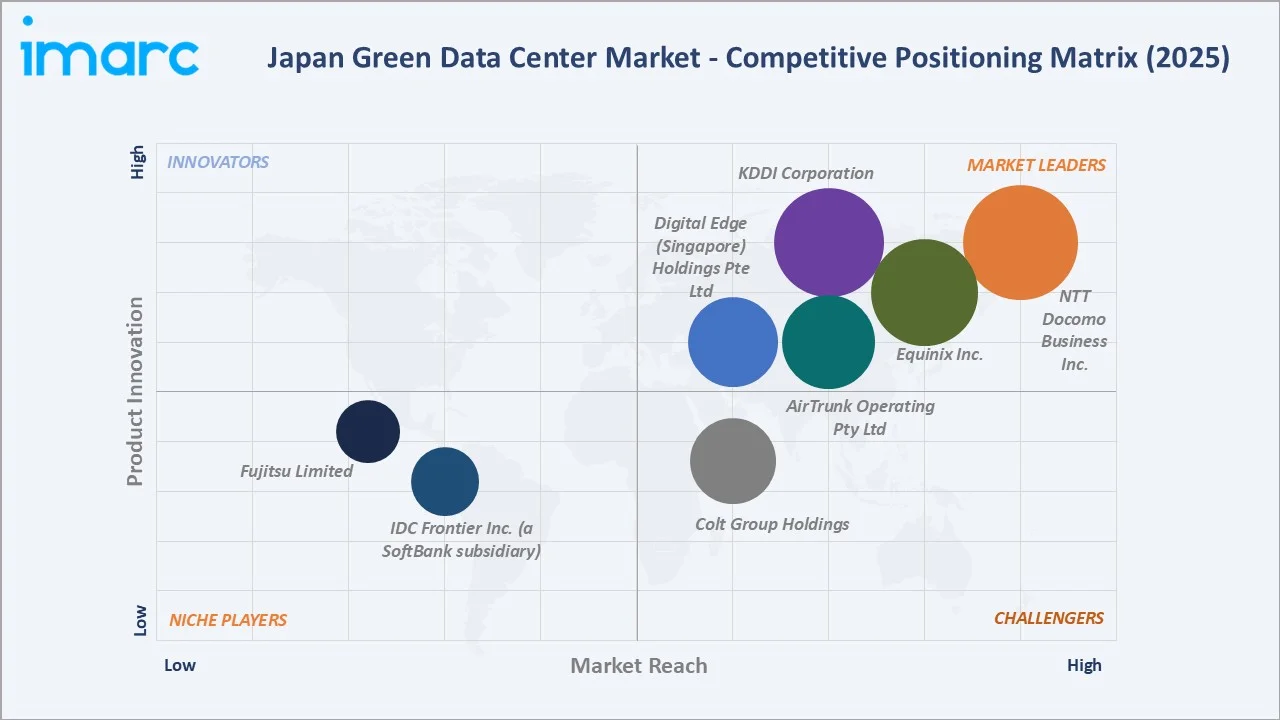

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

NTT Docomo Business Inc. |

Green Nexcenter |

Leader |

Largest domestic operator, deep fibre, multi-region footprint |

|

Equinix Inc. |

Equinix |

Leader |

Global colocation leader, carrier-neutral, hyperscaler customers |

|

KDDI Corporation |

KDDI Data Center Service |

Leader |

Telecom-anchored colocation, deep enterprise relationships |

|

AirTrunk Operating Pty Ltd |

AirTrunk |

Leader |

Hyperscale-grade build-to-suit, rapid capacity expansion |

|

Digital Edge (Singapore) Holdings Pte Ltd |

Digital Edge |

Leader |

Pan-Asia hyperscale platform, sustainability focus |

|

Colt Group Holdings Ltd |

Colt Data Centre Services |

Challenger |

Pan-Asia colocation, hyperscale-ready capacity |

|

IDC Frontier Inc. (a SoftBank subsidiary) |

IDC Frontier Data Center |

Established |

Domestic colocation, SoftBank-backed scale |

|

Fujitsu Limited |

Fujitsu Data Centers |

Established |

Japanese systems integrator, cloud and managed services |

The competitive landscape in the Japan green data center market is moderately concentrated. Tier-1 operators such as NTT Communications, Equinix, KDDI Telehouse, AirTrunk, and Digital Edge compete on hyperscale-grade build-to-suit capacity, sustainability credentials, and carrier-neutral connectivity. Mid-market players differentiate through specialist managed services, niche regional coverage, and tailored enterprise solutions. Strategic capital deployment remains highly active - AirTrunk continued multi-hundred-megawatt expansions through 2024, Equinix advanced multiple Tokyo and Osaka builds, and NTT Communications announced significant green data center capex for 2025-2027.

Key Company Profiles

NTT Docomo Business Inc.

NTT Docomo Business Inc. is the largest domestic green data center operator in Japan, headquartered in Tokyo and a wholly owned subsidiary of Nippon Telegraph and Telephone (NTT). The company operates an extensive multi-region data center footprint and combines deep fibre infrastructure with hyperscale-grade colocation services.

- Product & Platform Portfolio: NTT's portfolio spans the NexCenter colocation platform, NTT Global Data Centers, managed cloud services, hybrid-cloud connectivity through NTT Smart Connect, sustainability advisory, and AI-grade rack infrastructure across Tokyo, Yokohama, Osaka, and other Japanese metros.

- Recent Developments: In 2024, NTT DATA significantly expanded its global data center footprint, opening 10 new facilities and adding over 370 MW of capacity to support rising demand from AI and cloud workloads. The company also accelerated land acquisitions across key markets in North America, Europe, and Asia, positioning itself for future capacity expansion exceeding 800 MW.

- Strategic Focus: NTT's strategy centres on scaling hyperscale-grade green capacity, deepening renewable power procurement, expanding liquid and immersion cooling capabilities, and supporting Japanese enterprises and global hyperscalers with end-to-end sustainable digital infrastructure through 2034.

Equinix Inc.

Equinix Inc. operates the largest carrier-neutral colocation footprint in Japan, headquartered globally in Redwood City, California, with Japan operations centred on Tokyo and Osaka. Equinix Japan serves hyperscalers, financial institutions, telecom carriers, and global enterprises through its International Business Exchange (IBX) data centers.

- Product & Platform Portfolio: Equinix Japan’s portfolio includes the TY-series (Tokyo) and OS-series (Osaka) IBX data centers, Equinix Fabric digital interconnection, Equinix Metal bare-metal infrastructure, network exchange services, and a broad ecosystem of more than 2,000 partners and customers across the region.

- Recent Developments: In 2026, Equinix signed a 15-year virtual power purchase agreement with ENEOS Renewable Energy Corporation to procure 121 MW of solar power from the Sanda Mega Solar Power Plant in Japan. The deal is the largest single-site data center PPA in the country and marks Equinix’s second renewable energy agreement in the Japanese market.

- Strategic Focus: Equinix Japan's strategic focus centres on hyperscale-ready expansion, 100% renewable energy coverage by 2030, AI-grade liquid cooling deployment, and strengthening its carrier-neutral interconnection ecosystem to capture the next wave of cloud and AI demand across the Japanese market through 2034.

KDDI Corporation

KDDI Corporation is one of Japan's three major telecommunications carriers, headquartered in Tokyo. Its data center business operates under the KDDI Telehouse brand, which is part of the global Telehouse network and serves enterprise, telecom, and financial-services customers across Japan and internationally.

- Product & Platform Portfolio: KDDI Telehouse's portfolio spans Telehouse Tokyo (Tama, CC2, OS1) data centers, carrier-neutral colocation, network exchange, managed connectivity, sustainability advisory, and integrated mobile-fixed-cloud services delivered alongside KDDI's broader telecom and cloud platform.

- Recent Developments: In January 2026, KDDI Corporation launched operations of the Osaka Sakai Data Center in January 2026, positioning it as an AI-focused facility designed to support high-performance computing and generative AI workloads. The site benefits from proximity to Osaka’s industrial hub, enabling low-latency, high-reliability services for industries such as pharmaceuticals and manufacturing.

- Strategic Focus: KDDI Telehouse's strategy focuses on integrated telecom-data-center offerings, hyperscale-ready capacity expansion, deepening sustainability credentials through renewable PPAs and high-efficiency cooling, and supporting Japanese enterprises and global carriers with carrier-neutral green data center capacity through 2034.

Market Concentration Analysis

The Japan green data center market exhibits moderate concentration. The top five operators - NTT Docomo Business Inc., Equinix Inc., KDDI Corporation, AirTrunk Operating Pty Ltd, Digital Edge (Singapore) Holdings Pte Ltd - collectively account for an estimated 45-55% of Japan green data center capacity in 2025. The remaining share is distributed across Colt DCS Japan, IDC Frontier (SoftBank), Fujitsu Cloud, and a long tail of mid-market and regional operators across the eight Japanese regions.

The market is undergoing rapid expansion alongside selective consolidation. Hyperscale build-to-suit campuses by AirTrunk and Digital Edge concentrate capacity at the high end, while Equinix and NTT continue selective M&A and joint-venture activity. Japanese trading houses such as Mitsui & Co. and Mitsubishi Corporation are deploying significant capital into data center joint ventures with global partners through 2024-2025, reshaping the competitive landscape through 2034.

Investment & Growth Opportunities

Fastest-Growing Sub-Segments

Cloud service data centers represent the highest-growth sub-segment at approximately 18.9% CAGR through 2034. AI-grade hyperscale capacity, liquid cooling solutions, and corporate renewable PPAs are the highest-momentum opportunities for capital deployment. Hokkaido and Tohoku represent emerging green hyperscale campus frontiers with abundant cool climate and renewable power.

Emerging Sub-Markets

Edge data centers near 5G aggregation points, hydrogen-fuelled backup power systems, single-phase immersion cooling deployments, and AI-driven energy management software all represent above-trend growth pockets through 2034. The continued expansion of corporate PPAs from solar IPPs and offshore wind developers further supports the green segment's long-term economics.

Strategic Investment Trends

Strategic capital continues to reshape the competitive landscape. AirTrunk continued multi-hundred-megawatt hyperscale expansions through 2024-2025. Mitsui & Co. and Mitsubishi Corporation are deploying significant capital into data center joint ventures with global partners. Private equity, infrastructure funds, and Japanese trading houses are actively financing Japan green data center build-outs through 2034.

Future Market Outlook (2026-2034)

The Japan green data center market forecast projects exceptional value expansion from USD 6.55 Billion in 2025 to USD 25.60 Billion by 2034 at a CAGR of 16.35%. The Kanto region is expected to retain leadership, while Hokkaido, Tohoku, and Kyushu gain share on the back of cool-climate cooling efficiency, abundant renewables, and hyperscale campus build-outs. Cloud service data centers, solutions components, and high-density AI capacity are forecast to outpace overall market growth through 2034.

Three structural shifts will shape the Japan green data center market through 2034. First, generative AI workloads will drive rack-density requirements from 8-12 kW to 40-100 kW per rack, accelerating liquid cooling and high-voltage DC power adoption. Second, GX League decarbonization mandates and Net-Zero 2050 commitments will make corporate renewable PPAs, hydrogen backup pilots, and Scope 1-2-3 reporting baseline requirements. Third, Hokkaido and Tohoku will emerge as material green hyperscale frontiers given their cool climate and renewable power abundance.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with Japan green data center stakeholders, including operators' commercial leaders, hyperscaler infrastructure heads, sustainability and ESG directors at major Japanese enterprises, METI policy specialists, and renewable PPA originators. These interviews validated revenue sizing, segmentation estimates, and capacity-utilization benchmarks across the Japanese market.

Secondary Research

Secondary sources included METI strategic energy plans, GX League framework publications, Japan Data Center Council (JDCC) industry data, Bank of Japan economic releases, company annual reports and integrated reports, IEA Japan country profiles, the Tokyo Stock Exchange Prime Market sustainability disclosures, and trade publications such as DataCenter Dynamics, Nikkei Asia, and Impress Watch's data center coverage.

Forecasting Models

Market size estimates and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating hyperscaler capex announcements, megawatt-capacity build pipelines, AI-workload demand trajectories, renewable power availability, and historical category-evolution patterns. Scenario analysis was performed across base, optimistic, and conservative cases.

Japan Green Data Center Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Data Center Types Covered | Colocation Data Centers, Managed Service Data Centers, Cloud Service Data Centers, Enterprise Data Centers |

| Industry Verticals Covered | Healthcare, BFSI, Government, Telecom and IT, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | NTT Docomo Business Inc., Equinix Inc., KDDI Corporation, AirTrunk Operating Pty Ltd, Digital Edge (Singapore) Holdings Pte Ltd, Colt Group Holdings Ltd, IDC Frontier Inc. (a SoftBank subsidiary), Fujitsu Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan green data center market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan green data center market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan green data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Green Data Center Market Report

The Japan green data center market was valued at USD 6.55 Billion in 2025, supported by surging AI compute demand, the Net-Zero 2050 commitment, growing renewable power availability, and hyperscaler expansion across Tokyo, Osaka, and emerging regional clusters.

The market is projected to reach USD 25.60 Billion by 2034, growing at a CAGR of 16.35% during 2026-2034, driven by AI hyperscale capacity, GX League decarbonization mandates, liquid cooling adoption, and renewable PPA expansion across all eight Japanese regions.

Cloud service data centers lead with a 36.9% share in 2025, propelled by AWS, Google Cloud, Microsoft Azure, and Oracle Cloud expansions across Tokyo and Osaka. AWS announced approximately JPY 2.2 trillion of Japan cloud infrastructure investment through 2027.

Solutions dominate at 72.4% in 2025, capturing power infrastructure, advanced cooling systems, racks, and energy management software. Schneider Electric, Vertiv, ABB, Daikin, and NEC lead the solutions ecosystem across Japanese deployments.

Cloud service data centers are the fastest-growing sub-segment, advancing at an estimated 18.9% CAGR through 2034. AI workloads, hyperscaler expansion, and corporate cloud migration are the primary drivers across Japan's largest economic regions and emerging hubs.

The Kanto region leads with a 38.2% share in 2025. Tokyo, Inzai (Chiba), and Yokohama clusters host the country's deepest fibre network, abundant utility power capacity, and proximity to financial-services and platform-economy demand drivers across Japan.

Key drivers include AI and hyperscale compute demand, Japan's Net-Zero 2050 mandate, GX League decarbonization framework, expanding renewable power availability, accelerating cloud migration, and growing corporate PPA volumes signed by Japanese data center operators.

Major players include NTT Docomo Business Inc., Equinix Inc., KDDI Corporation, AirTrunk Operating Pty Ltd, Digital Edge (Singapore) Holdings Pte Ltd., Colt Group Holdings Ltd, IDC Frontier Inc., Fujitsu Limited.

Key restraints include power grid interconnection limitations, elevated land and capex costs in Inzai and Osaka, cooling and humidity constraints in Tokyo, skilled talent gaps, and renewable PPA pricing volatility that complicates long-term financial planning for green facility investments.

AI workloads are driving rack power densities from 8-12 kW to 40-100 kW per rack, accelerating liquid cooling and immersion cooling adoption. AWS announced JPY 2.2 trillion and Microsoft over JPY 440 billion of Japan AI cloud infrastructure investment commitments.

Sustainability is reshaping operations through corporate renewable PPAs, hydrogen and ammonia backup pilots, liquid cooling adoption, and DCIM-based GX League reporting. Net-Zero 2050 commitments and Tokyo Stock Exchange Prime Market disclosures are key compliance drivers.

Investment opportunities include hyperscale build-to-suit campuses, liquid and immersion cooling deployments, hydrogen-fuelled backup power, edge data centers near 5G aggregation, AI-driven energy management software, and Hokkaido and Tohoku green hyperscale frontiers through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)