Japan Private LTE Market Size, Share, Trends and Forecast by Component, Technology, Frequency Band, Deployment Model, Industry Vertical, and Region, 2026-2034

Japan Private LTE Market Size, Share, Trends & Forecast (2026-2034)

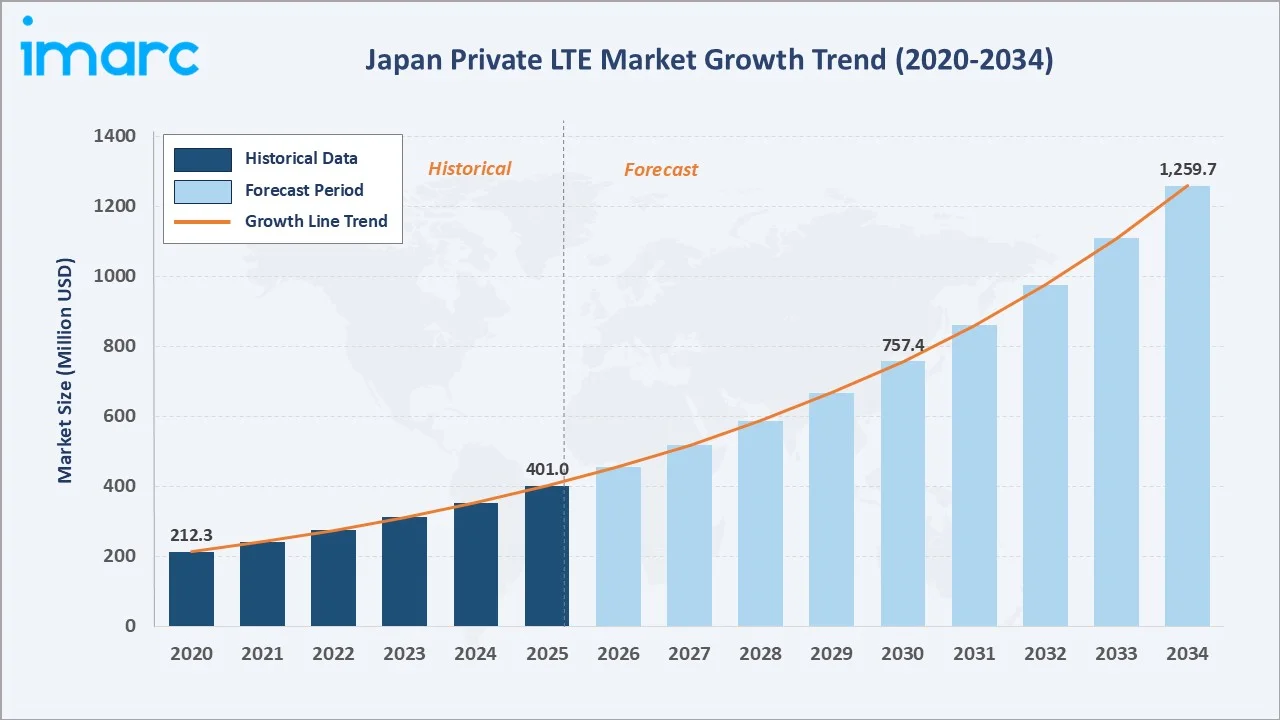

The Japan private LTE market reached USD 401.0 Million in 2025 and is projected to reach USD 1,259.7 Million by 2034, growing at a CAGR of 13.56% during 2026-2034. Japan's accelerating industrial digitalization agenda, the Ministry of Internal Affairs and Communications' (MIC) local 5G licensing system, and surging demand for mission-critical wireless connectivity across manufacturing, utilities, transportation, and smart infrastructure are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 401.0 Million |

|

Forecast Market Size (2034) |

USD 1,259.7 Million |

|

CAGR (2026-2034) |

13.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

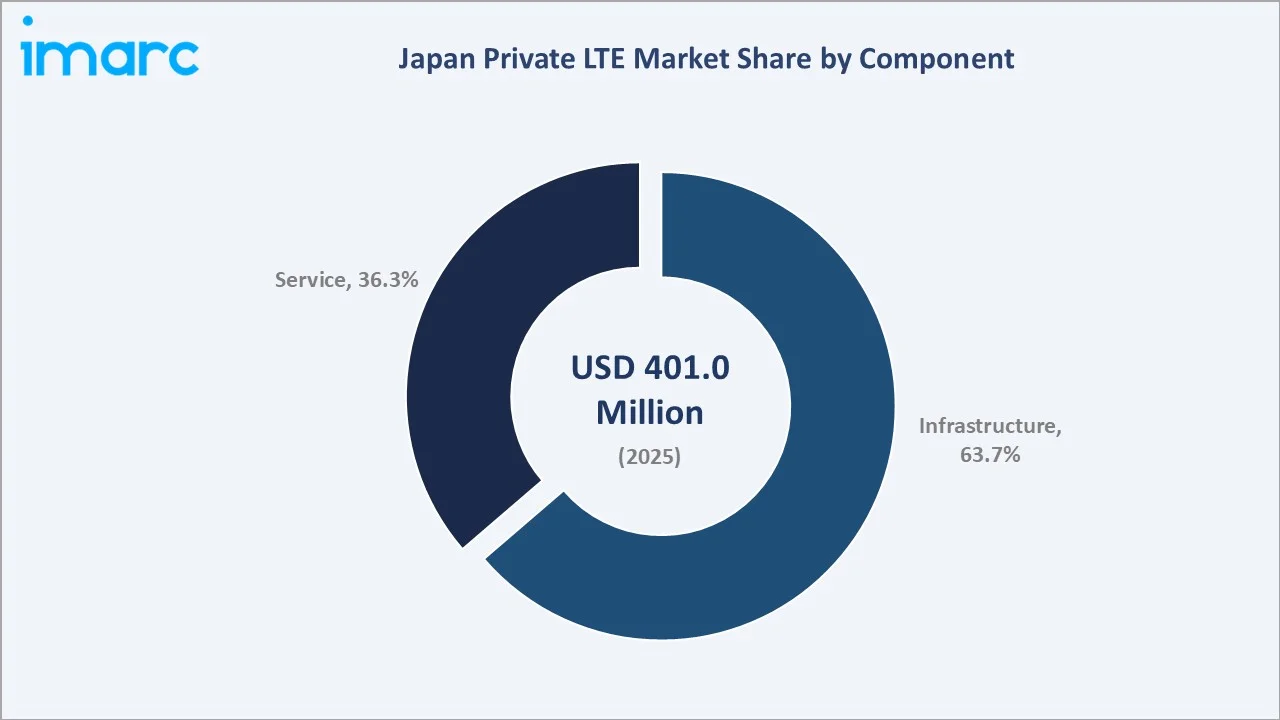

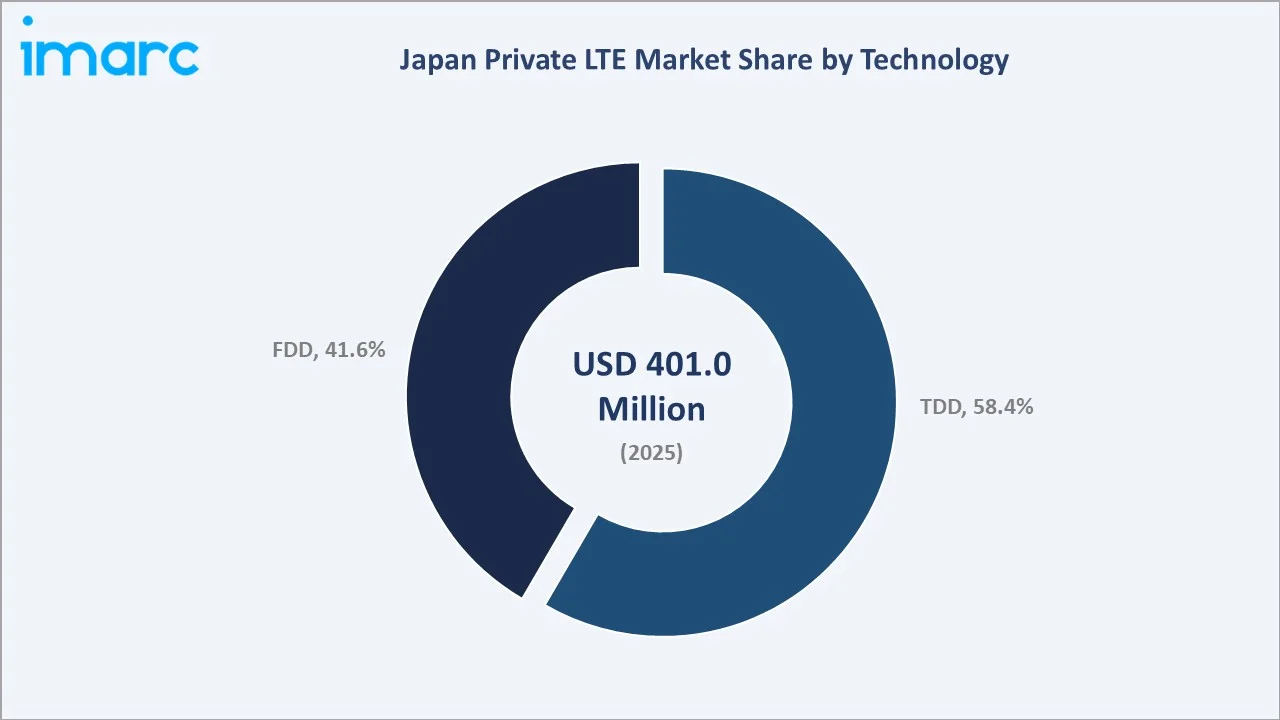

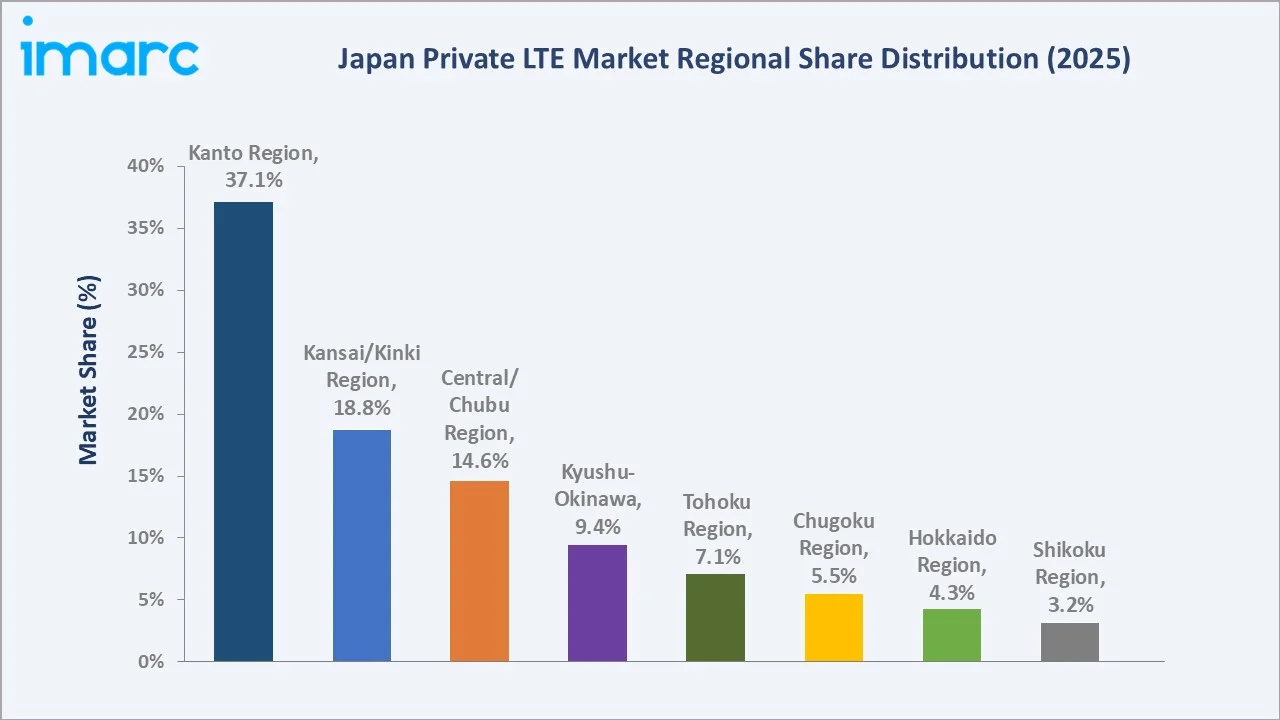

The Kanto region leads regionally, holding a 37.1% market share in 2025, underpinned by the concentration of Japan's largest manufacturing and logistics enterprises in Greater Tokyo. Infrastructure commands a dominant 63.7% share of the component breakdown, while TDD technology retains the largest share of the technology segment at 58.4%.

To get more information on this market, Request Sample

Japan's private LTE market is underpinned by three structural forces: the government's local 5G licensing system enabling enterprises to operate their own wireless networks, Japan's Industry 4.0 transformation mandate across manufacturing and critical infrastructure, and the increasing inadequacy of public LTE for time-sensitive industrial automation applications. Each force independently increases addressable demand, collectively sustaining above-average CAGR through 2034.

Executive Summary

The Japan private LTE market is experiencing accelerated expansion, driven by the convergence of Japan's industrial digitalization agenda, the MIC's local 5G/LTE licensing system, and critical infrastructure operators' need for secure, high-reliability wireless networks. The market reached USD 401.0 Million in 2025 and is forecast to reach USD 1,259.7 Million by 2034, growing at a CAGR of 13.56%.

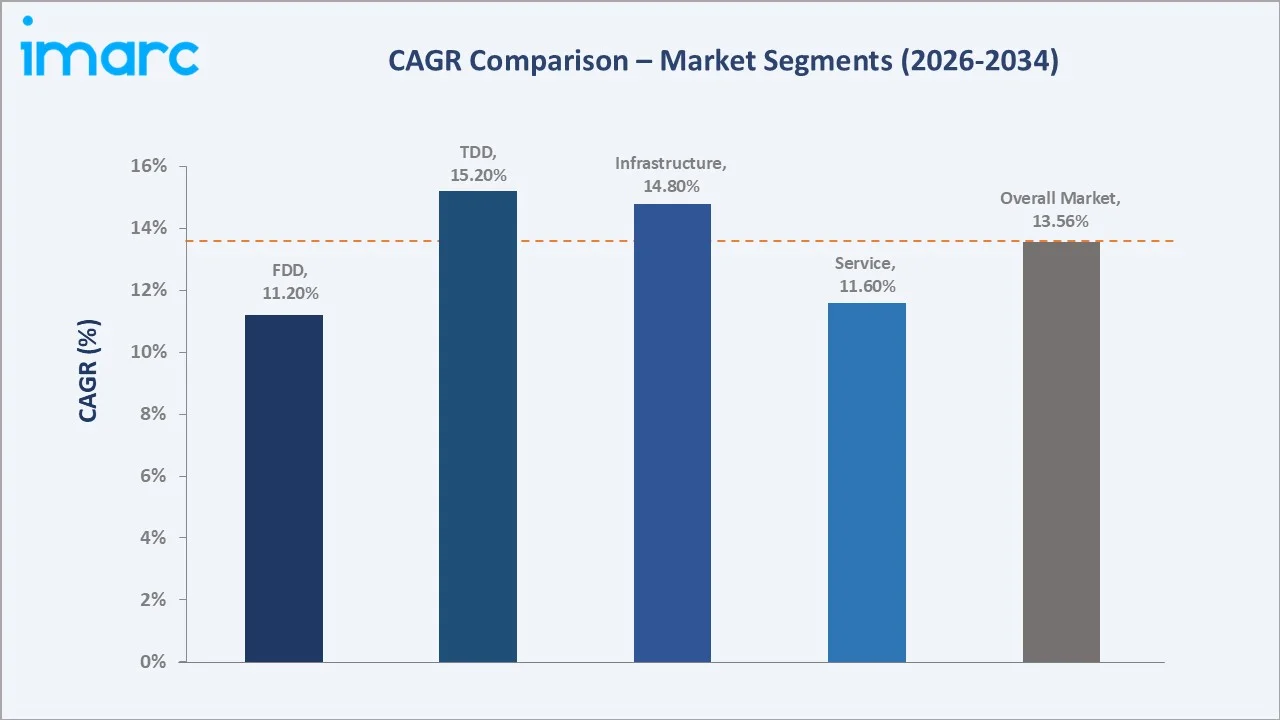

Infrastructure-based components dominate with a 63.7% share in 2025, encompassing radio access network hardware, evolved packet core systems, and network management platforms. TDD (Time Division Duplex) technology leads the technology segment at 58.4%, reflecting its spectral efficiency advantage in asymmetric data-heavy industrial IoT applications where downlink capacity substantially exceeds uplink requirements.

The Kanto region at 37.1% leads regionally, anchored by Greater Tokyo's manufacturing belt and Kanagawa's industrial clusters. The Kansai/Kinki region follows at 18.8%, driven by Osaka's precision machinery and smart port infrastructure. Leading vendors, including NEC Corporation, Fujitsu Limited, NTT, Inc., and Nokia Corporation, dominate the market across infrastructure supply, system integration, and managed service delivery.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Infrastructure – 63.7% share (2025) |

|

Fastest Growing Component |

Infrastructure – ~14.8% CAGR (2026-2034) |

|

Largest Technology |

TDD – 58.4% share (2025) |

|

Fastest Growing Technology |

TDD – ~15.2% CAGR (2026-2034) |

|

Leading Region |

Kanto Region – 37.1% share (2025) |

|

Top Companies |

NEC Corporation, Fujitsu Limited, NTT, Inc., Nokia Corporation |

Key Analytical Observations Supporting The Above Data:

- Infrastructure products account for 63.7% of Japan's private LTE market in 2025. This dominance reflects the capital-intensive nature of greenfield private network deployments, where RAN hardware, EPC systems, and antenna infrastructure represent the primary expenditure category for manufacturing and utility operators establishing network coverage across large industrial sites.

- TDD technology at 58.4% (2025) remains dominant due to its spectral efficiency advantage in industrial IoT environments where downlink data volumes from surveillance cameras, remote monitoring feeds, and AR-assisted maintenance applications substantially exceed uplink traffic from sensors and control signals.

- FDD technology's 41.6% share (2025) reflects its continued preference in applications requiring symmetric, low-latency communications, particularly push-to-talk critical communications, teleprotection for power utilities, and SCADA network backhaul, where consistent bi-directional latency is operationally essential.

- The Kanto region's 37.1% share (2025) reflects Greater Tokyo's position as Japan's primary industrial hub, with Kawasaki's chemical and steel complex, Yokohama's port, and the Keihin industrial belt collectively representing Japan's highest concentration of large-scale private LTE deployments in manufacturing, logistics, and smart infrastructure.

Japan Private LTE Market Overview

Private LTE encompasses dedicated, enterprise-controlled Long-Term Evolution wireless networks operating on licensed, unlicensed, or shared spectrum, providing industrial-grade connectivity independent of public mobile network infrastructure. Japan's private LTE market spans radio access network hardware, evolved packet core software, network management systems, and managed service offerings, serving manufacturing, utilities, transportation, mining, public safety, and smart city verticals.

Macroeconomic drivers include MIC's local 5G licensing system (enacted 2019), enabling enterprises to directly license wireless spectrum for private network operation, Japan's Society 5.0 industrial transformation mandate, and the increasing inadequacy of Wi-Fi and public LTE for deterministic, low-latency industrial automation. The government's Digital Garden City Nation (DIGIDEN) initiative pledging 99% 5G coverage by FY2030, is directly accelerating enterprise investment in private LTE as a transitional and complementary technology to private 5G deployments.

Market Dynamics

To evaluate market opportunities, Request Sample

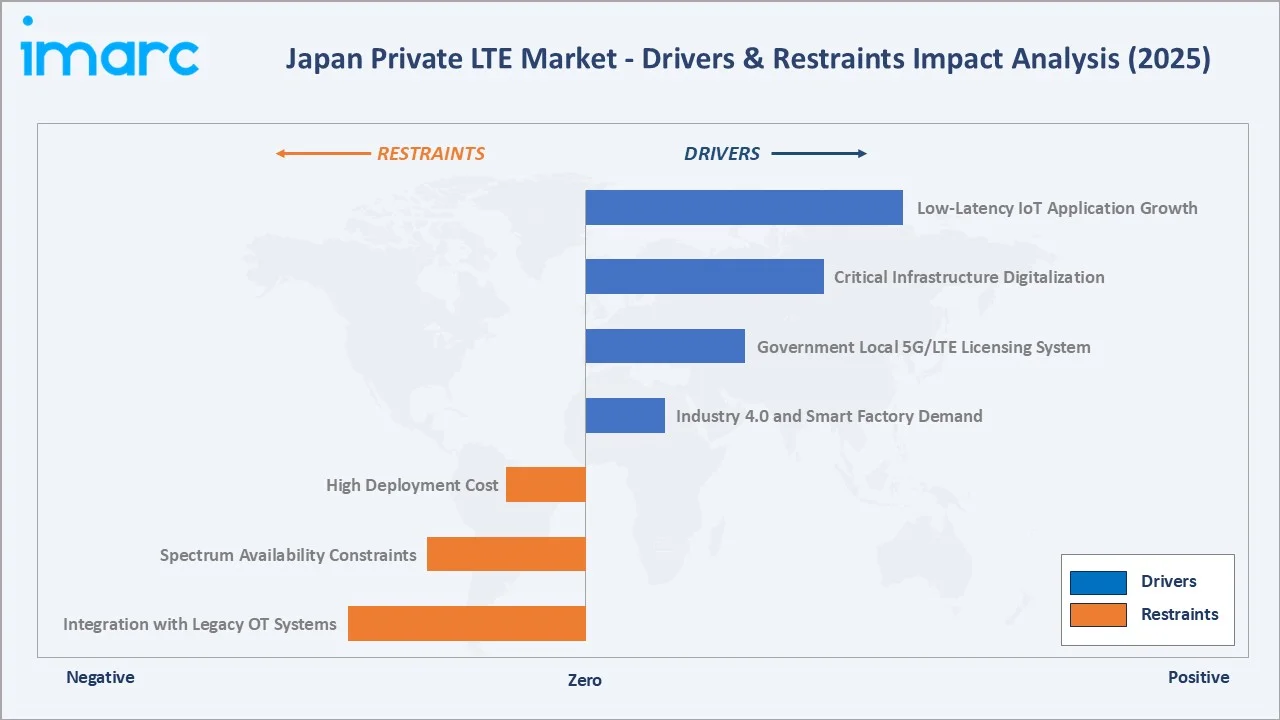

Market Drivers

- Industry 4.0 and Smart Factory Demand: Japan's manufacturing sector, accounting for approximately 21% of GDP, is undergoing a systematic transition to fully connected, data-driven production environments. Private LTE networks are integral to Industry 4.0 architectures, providing the wireless backbone for automated guided vehicles (AGVs), robotic process control, machine vision quality inspection, and predictive maintenance sensor networks across factory floors where physical cabling is impractical.

- Government Local 5G/LTE Licensing System: MIC's local 5G licensing system, introduced in 2019, allows enterprises to directly obtain wireless spectrum licenses for private network operation without relying on public mobile operators. As of April 2024, about 170 local 5G/LTE licenses had been issued across Japan, spanning manufacturing, agriculture, construction, and smart city applications, each representing a discrete private network deployment project.

- Critical Infrastructure Digitalization: Japan's utility operators, port authorities, and railway operators are deploying private LTE networks to replace aging narrowband radio systems with broadband wireless infrastructure supporting HD video surveillance, IoT sensor telemetry, and IP-based SCADA communications across geographically distributed assets.

- Low-Latency IoT Application Growth: Industrial IoT deployments requiring sub-20ms end-to-end latency, including robotic assembly control, autonomous vehicle coordination, and real-time process monitoring, are technically incompatible with public LTE networks subject to variable congestion and shared spectrum contention.

Market Restraints

- High Deployment Cost: A complete private LTE network deployment for a mid-sized manufacturing facility, including RAN hardware, evolved packet core, network management software, and professional services, costs JPY 50–300 million depending on coverage area and performance requirements.

- Spectrum Availability Constraints: Japan's radio frequency spectrum is intensively allocated, with licensed spectrum suitable for private LTE deployments in the 1.9 GHz, 2.6 GHz, and 4.7 GHz bands subject to competitive allocation through MIC's licensing process. Spectrum congestion in dense urban industrial areas and near major airports constrains expansion opportunities for some enterprise applicants.

- Integration with Legacy OT Systems: Japan's manufacturing plants and utility installations operate substantial installed bases of legacy operational technology (OT) equipment designed for proprietary wired or narrowband wireless communication protocols. Integrating private LTE into these heterogeneous OT environments requires extensive middleware development and protocol translation, increasing project complexity and costs by 25–40% over greenfield deployments.

Market Opportunities

- Smart Port and Logistics Automation: Japan's 120+ designated ports are undergoing systematic automation, with private LTE networks enabling real-time container tracking, automated crane control, autonomous yard trucks, and integrated port community system connectivity.

- Mining and Construction Automation: According to the Ministry of Land, Infrastructure, Transport and Tourism, Japan’s construction workforce declined to 4.78 million in 2025, representing a 30% drop from its 1997 peak of 6.85 million. Private LTE networks enabling remote operation of excavators, bulldozers, and drilling equipment are receiving government subsidy support under the i-Construction initiative, creating a JPY 15 billion addressable market for industrial private wireless through 2030.

Market Challenges

- Technology Migration to Private 5G: Japan's MIC system encompasses both local LTE and local 5G licensing, and many enterprises evaluating private wireless investment in 2025–2027 are postponing LTE deployments to await 5G-compatible hardware that provides a direct upgrade path. This technology wait-and-see dynamic is moderating new private LTE deployments in the 2024–2025 period, even as the total private wireless market grows.

- Cybersecurity and Network Isolation Requirements: Japan's cybersecurity guidelines for critical infrastructure, issued by the National Cybersecurity Office (NCO), impose stringent air-gap and network segmentation requirements on industrial private LTE deployments.

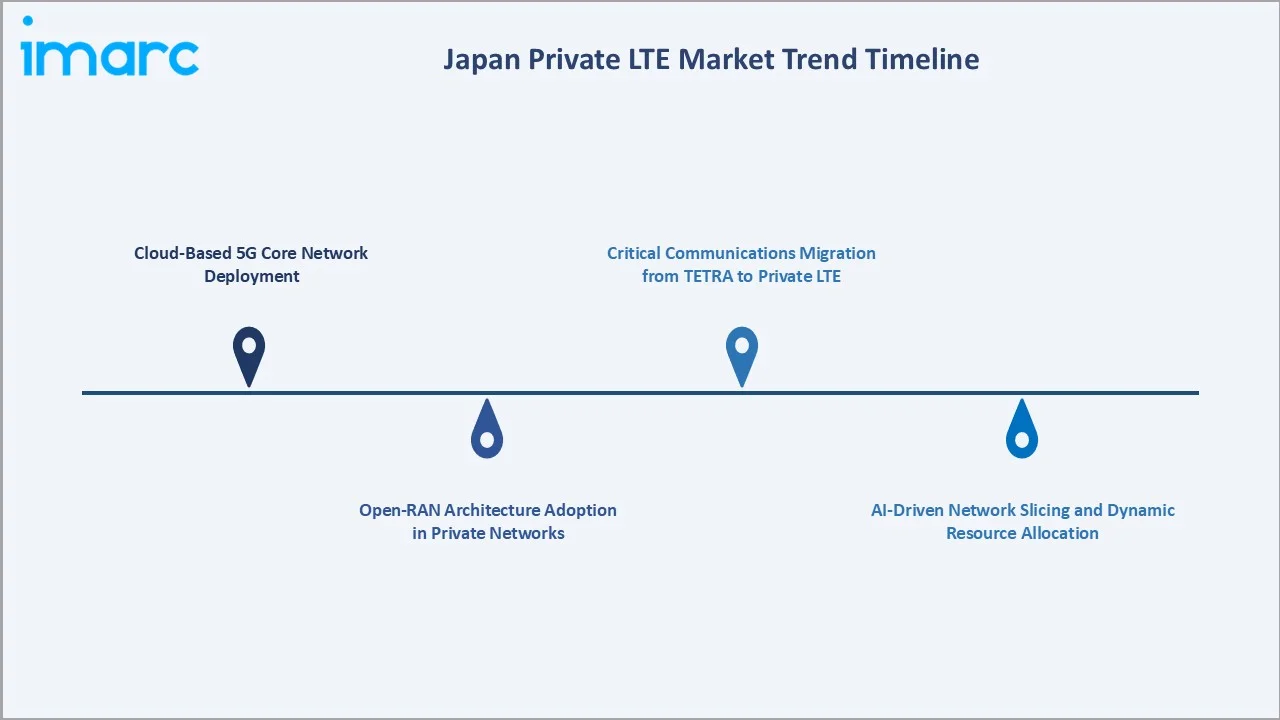

Emerging Market Trends

1. Cloud-Based 5G Core Network Deployment

In March 2026, NTT DOCOMO (subsidiary of NTT, Inc.) and NEC launched Japan’s first commercial 5G Core network on AWS, using a hybrid cloud architecture to improve flexibility, reliability, capacity scaling, and energy efficiency. The companies also achieved world’s first automation of 5G Core design and construction using Agentic AI and GitOps, reducing construction time by around 80%.

2. Open-RAN Architecture Adoption in Private Networks

Japan's private LTE market is emerging as a proving ground for Open-RAN architectures, with Rakuten Mobile's fully virtualized open-RAN network serving as a reference model for enterprise private network deployments. In March 2026, Samsung announced that it would supply Open-RAN-compliant 5G radios to Rakuten Mobile to support its nationwide 5G Open RAN network expansion across Japan. The portfolio includes low-band 700 MHz, mid-band 1.7 GHz, and Massive MIMO 3.8 GHz radios for better coverage and capacity.

3. AI-Driven Network Slicing and Dynamic Resource Allocation

Private LTE networks are increasingly incorporating AI-based network slicing capabilities that dynamically allocate bandwidth, prioritize traffic, and optimize spectral efficiency across heterogeneous IoT workloads. In September 2023, KDDI and Samsung signed an MoU to form a 5G Global Network Slicing Alliance, aimed at launching commercial 5G network slicing services and exploring new business models. The alliance will support customized 5G use cases in Japan, such as smart factories, automated vehicles, and high-bandwidth video streaming.

4. Critical Communications Migration from TETRA to Private LTE

Japan's public safety and utility sectors are progressively migrating narrowband TETRA and analog radio systems to broadband private LTE, driven by the technical superiority of LTE for multimedia communications, location services, and IoT integration. The Total Digital Communications System (TDCS) replacement program and utility sector SCADA modernization initiatives are collectively creating approximately JPY 20 billion private LTE migration opportunity across emergency services, power utilities, and transportation authorities through 2030.

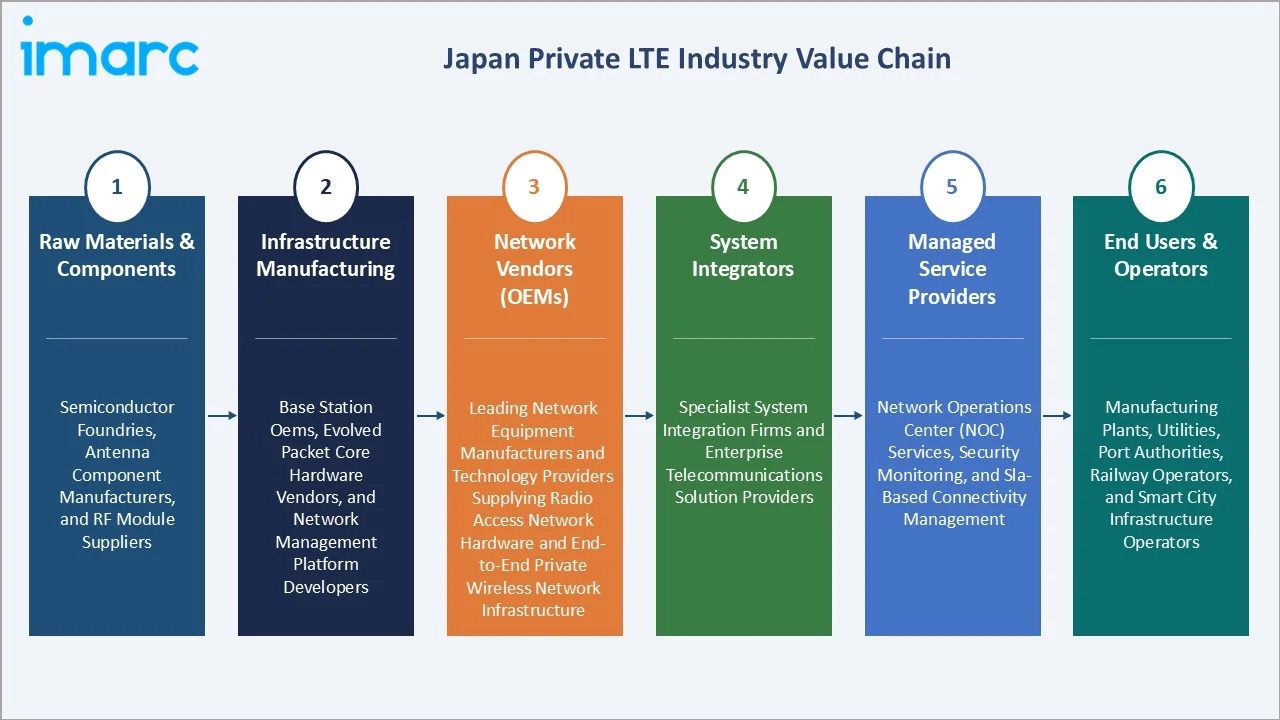

Industry Value Chain Analysis

Japan's private LTE value chain spans semiconductor and component supply through enterprise end-user operations, with each stage occupied by specialized manufacturers, software developers, system integrators, and service providers whose performance directly influences network reliability, deployment speed, and total cost of ownership.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Semiconductor foundries, antenna component manufacturers, and RF module suppliers |

|

Infrastructure Manufacturing |

Base station OEMs, evolved packet core hardware vendors, and network management platform developers |

|

Network Vendors (OEMs) |

Leading network equipment manufacturers and technology providers supplying radio access network hardware and end-to-end private wireless network infrastructure |

|

System Integrators |

Specialist system integration firms and enterprise telecommunications solution providers |

|

Managed Service Providers |

Network operations center (NOC) services, security monitoring, and SLA-based connectivity management |

|

End Users & Operators |

Manufacturing plants, utilities, port authorities, railway operators, and smart city infrastructure operators |

Technology Landscape in the Japan Private LTE Industry

Radio Access Network (RAN) Infrastructure

Japan's private LTE RAN market is served by a combination of global equipment vendors and domestic players. Small cell and neutral-host RAN architectures are gaining traction in indoor industrial environments, with distributed antenna systems (DAS) providing multi-floor coverage in large manufacturing facilities. The shift to Open-RAN disaggregated architectures is enabling the entry of Japanese IT vendors into RAN hardware markets previously dominated by integrated telecom equipment suppliers.

Evolved Packet Core (EPC) and Network Management

Private LTE EPC deployments in Japan are transitioning from dedicated hardware appliances toward virtualized software-defined architectures deployable on commercial-off-the-shelf servers. Cisco Systems Japan and NEC Corporation offer COTS-based virtual EPC solutions, reducing core network hardware costs by 40–60% versus dedicated appliances, enabling cost-effective deployment in mid-market manufacturing facilities. Network management platforms incorporating AI-based anomaly detection and predictive maintenance are becoming standard in new deployments.

Spectrum: Licensed, Shared, and Unlicensed Frameworks

Japan’s private LTE deployments operate across multiple spectrum frameworks, including fully licensed spectrum allocated through the Ministry of Internal Affairs and Communications (MIC), shared spectrum under the 3.7 GHz and 4.5 GHz local 5G bands, and unlicensed spectrum in the 1.9 GHz band for low-priority IoT applications. The evolution of Japan’s local spectrum licensing system since 2019 has been a key regulatory enabler supporting market expansion.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Infrastructure |

63.7% |

2025 |

|

Technology |

TDD |

58.4% |

2025 |

|

Frequency Band |

🔒 |

🔒 |

2025 |

|

Deployment Model |

🔒 |

🔒 |

2025 |

|

Industry Vertical |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

37.1% |

2025 |

By Component

The infrastructure segment dominates with a 63.7% share in 2025. Infrastructure's dominance reflects the capital-intensive nature of greenfield private LTE deployments across Japan's large-scale industrial facilities, automotive plants, chemical complexes, and port terminals, where comprehensive coverage requirements necessitate multi-site RAN infrastructure investments of JPY 50–200 million per project.

To access detailed market analysis, Request Sample

Service represents 36.3% of the market, encompassing installation and commissioning, network operations management, SLA-based monitoring, cybersecurity managed services, and network optimization consulting. The service segment is growing at approximately 11.6% CAGR as enterprise operators shift toward fully managed private LTE service models where vendors assume end-to-end network performance responsibility under multi-year service agreements.

By Technology

TDD commands a 58.4% share in 2025. TDD's dominance reflects its spectral efficiency advantage in industrial IoT environments characterized by asymmetric data flows, high-volume downlink traffic from machine vision systems, remote monitoring video, and AR maintenance guidance, which substantially exceeds uplink traffic from sensors and control signals.

FDD (Frequency Division Duplex) represents 41.6%, reflecting its continued preference in the utility sector, public safety, and transportation applications requiring symmetrical, deterministic bi-directional communications. FDD LTE's separate uplink and downlink frequency bands provide interference-free simultaneous transmission, essential for teleprotection relay coordination in power grids, where microsecond-level signaling must occur concurrently in both directions without contention-based delays.

Regional Market Insights

The Kanto region's market leadership (37.1%, 2025) reflects Greater Tokyo's status as Japan's primary industrial and enterprise hub. The Keihin industrial belt hosts Japan's highest concentration of large-scale manufacturing, chemical, and port facilities requiring private LTE coverage. The region's dominance is reinforced by proximity to Japan's leading private network vendors, system integrators, and enterprise decision-making headquarters, compressing deployment cycles versus secondary markets.

The Kansai/Kinki region at 18.8% represents Japan's second-largest private LTE market, driven by Osaka's dense manufacturing and smart port modernization programs. The ports of Osaka and Kobe are among Japan's most actively digitalized port facilities, with private LTE networks supporting autonomous crane operations, container tracking, and integrated logistics management systems.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

37.1% |

High concentration of large-scale manufacturing, logistics, and port facilities requiring dedicated private wireless coverage; dense enterprise headquarters driving network investment decisions |

|

Kansai/Kinki Region |

18.8% |

Active port modernization and smart logistics automation programs; growing pharmaceutical and electronics manufacturing connectivity requirements |

|

Central/Chubu Region |

14.6% |

Dense automotive manufacturing cluster driving industrial IoT and AGV connectivity demand; port terminal automation programs; chemical and steel sector private network deployments |

|

Kyushu-Okinawa Region |

9.4% |

Expanding semiconductor manufacturing; growing automotive supply chain IoT connectivity; agriculture and food processing sector connectivity programs |

|

Tohoku Region |

7.1% |

Government-supported resilient communications infrastructure programs; manufacturing sector recovery and modernization; expanding electronics and semiconductor facility connectivity requirements |

|

Chugoku Region |

5.5% |

Heavy industrial and chemical complex automation connectivity; steel and refining sector process management wireless deployments |

|

Hokkaido Region |

4.3% |

Precision agriculture IoT connectivity programs; industrial port private wireless deployments; expanding food processing and dairy sector automation connectivity initiatives |

|

Shikoku Region |

3.2% |

Chemical and industrial complex automation connectivity; medical device manufacturing wireless requirements; regional utility grid modernization and smart infrastructure programs |

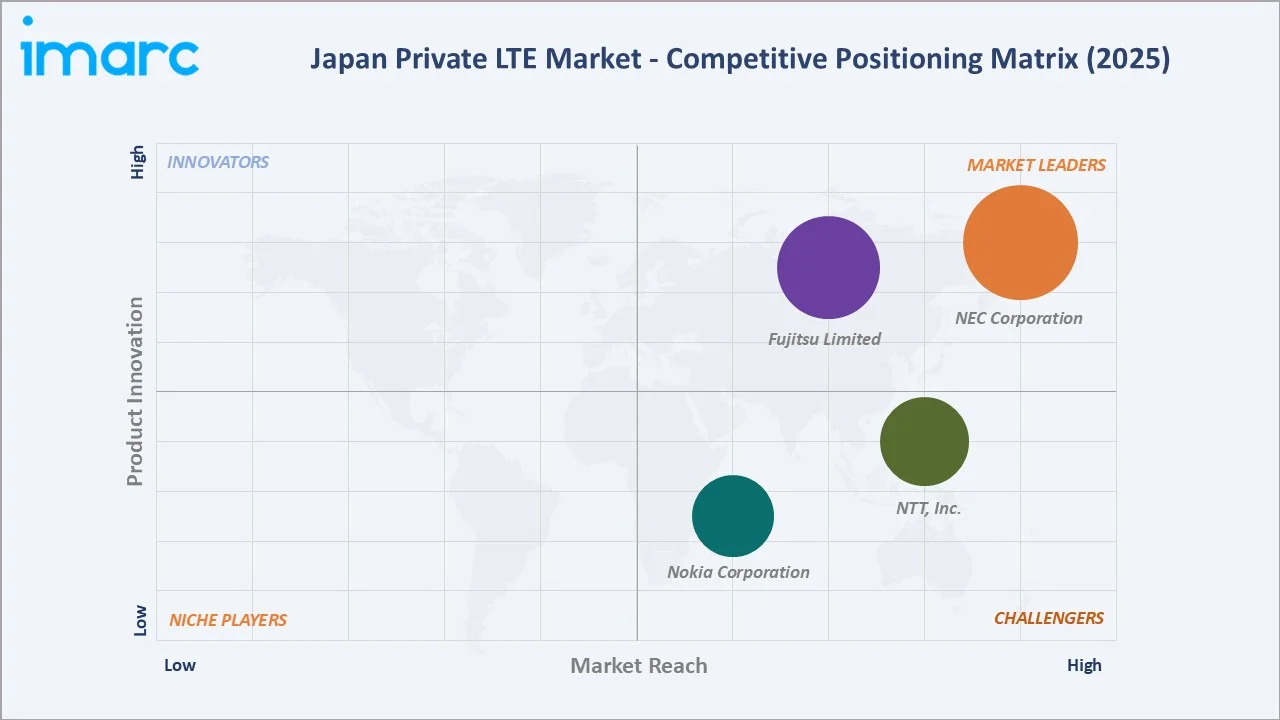

Competitive Landscape

Japan's private LTE market exhibits moderate concentration, with the top four vendors collectively holding approximately 52–58% of market revenue in 2025.

|

Company Name |

Brands/Services |

Market Position |

Core Strength |

|

NEC Corporation |

Open vRAN, Open Radio Unit, 4G/5G Converged Core, Enterprise Network Solutions |

Market Leader |

Comprehensive end-to-end private wireless network portfolio; strong enterprise OT/IT integration capabilities across industrial verticals |

|

Fujitsu Limited |

Fujitsu Private 5G |

Market Leader |

Advanced virtualized and open radio access network architecture; established relationships with domestic enterprise and government customers |

|

NTT, Inc. |

NTT Private 5G |

Strong Challenger |

Broad enterprise private network managed service capabilities; nationwide infrastructure and spectrum management expertise |

|

Nokia Corporation |

Nokia Digital Automation Cloud (DAC), Modular Private Wireless (MPW) |

Challenger |

Global private wireless technology leadership with proven industrial deployment references; modular and scalable network solutions |

Japanese domestic vendors, NEC Corporation and Fujitsu Limited, maintain competitive advantages through deep OT/IT integration expertise and long-standing relationships with Japan's major industrial enterprises, while global infrastructure vendors, including Nokia Corporation, compete on technical performance and global support capabilities.

Key Company Profiles

NEC Corporation

NEC Corporation is one of Japan's largest domestic private LTE/5G vendors, with a comprehensive portfolio spanning RAN hardware, EPC software, and end-to-end managed service delivery.

- Service Portfolio: Open vRAN, open radio unit, 4G/5G converged core, and enterprise network solutions.

- Recent Developments: In January 2026, NEC developed a new 5G Sub-6GHz Massive MIMO Radio Unit in Japan, designed to improve communication throughput, compactness, and energy efficiency. Scheduled for launch in Japan in the first half of FY2026, the unit offers around 48% higher uplink and 54% higher downlink throughput, while reducing normal power consumption by about 42%.

- Strategic Focus: Open-RAN leadership; smart factory and smart port private wireless; OT/IT convergence solutions; government and public safety network modernization.

Fujitsu Limited

Fujitsu Limited is one of the leading providers of private LTE and virtualized RAN solutions in Japan. The company’s private LTE solutions combine domestic manufacturing of radio units with cloud-native EPC software, enabling cost-competitive deployments that align with Japan's Open-RAN ecosystem priorities.

- Product Portfolio: Fujitsu Private 5G, virtualized RAN solutions, and 1FINITY optical networking platform.

- Strategic Focus: Open-RAN private network cost leadership; agriculture and construction IoT connectivity; local government smart city private LTE programs; global expansion leveraging Japan's Open-RAN ecosystem.

Market Concentration Analysis

Japan's private LTE market exhibits moderate concentration, with the top four vendors collectively holding 52–58% of total revenue in 2025. Below the top tier, a competitive mid-market of 10–15 specialized vendors and system integrators serves specific vertical segments with differentiated technology propositions.

Consolidation is occurring primarily through capability expansion rather than M&A, with established telecom operators building enterprise private network divisions to compete directly with infrastructure-vendor-led deployments. This operator-versus-vendor dynamic is accelerating innovation in managed service models, where operators leverage existing spectrum management and NOC capabilities to offer fully outsourced private LTE services at lower TCO than enterprise self-deployment.

Investment & Growth Opportunities

Fastest Growing Segments

TDD technology (~15.2% CAGR), infrastructure hardware for smart port deployments (~16% CAGR), managed service offerings (~14% CAGR), and private LTE for smart agriculture (~20% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address a combined incremental market of approximately USD 500 million within Japan's private LTE ecosystem by 2030.

Emerging Market Expansion

Kyushu's emerging semiconductor manufacturing cluster represents an incremental USD 60+ million private LTE opportunity by 2030. Hokkaido's agriculture sector, receiving significant government subsidies for precision farming IoT, represents a structurally underpenetrated opportunity for lightweight private LTE deployments serving GPS-guided farm equipment and environmental monitoring sensor networks.

Venture and Institutional Investment Trends

- Japan's government Digital Garden City Nation Strategy allocates JPY 100+ billion for regional smart infrastructure investment through FY2027, with private wireless networks identified as critical connectivity infrastructure for smart agriculture, smart logistics, and regional healthcare telemedicine applications, creating a significant government-funded demand stream for private LTE deployments outside major metropolitan centers.

- MIC's continued expansion of local spectrum licensing procedures is accelerating enterprise private LTE project economics by compressing pre-deployment timelines, directly improving project NPV calculations for industrial capital expenditure approvals.

Future Market Outlook (2026-2034)

Japan's private LTE market is positioned for sustained expansion through 2034. From a base of USD 401.0 Million in 2025, the market is projected to reach USD 1,259.7 Million by 2034, representing total incremental value creation of USD 858.7 million at a CAGR of 13.56%. This growth is supported by Japan's demographic-driven imperative for industrial automation, the irreversible commitment to Society 5.0 digital transformation, and the technical impossibility of meeting industrial IoT performance requirements on shared public network infrastructure.

The technology landscape will undergo significant evolution through 2034, with private LTE and local 5G increasingly deployed as complementary rather than competing technologies within enterprise campuses. Private LTE's coverage efficiency and lower deployment cost will sustain its relevance for large outdoor industrial sites, while private 5G handles ultra-high-density indoor IoT and URLLC applications requiring sub-5ms latency.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including private LTE network vendors, system integrators, enterprise IT and OT managers, spectrum licensing consultants, and institutional investors across Japan, Finland, Sweden, and the United States. Expert input validated market sizing, technology adoption rates, and regional deployment pipeline data.

Secondary Research

Secondary research encompassed vendor annual reports, MIC radio frequency licensing statistics, GSMA Intelligence, Omdia Private LTE data, 3GPP technical specifications for LTE-Advanced Pro, and industry publications (RCR Wireless, FierceTelecom, Nikkei XTECH, ITmedia Mobile).

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating local spectrum license issuance data (MIC), enterprise private network CAPEX trends, average selling price trajectories, and vendor revenue disclosures. A base-case CAGR of 13.56% reflects consensus estimates validated against MIC licensing pipeline data, vendor order backlog disclosures, and announced enterprise private network investment programs from FY2020 to FY2025.

Japan Private LTE Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Infrastructure, Service |

| Technologies Covered | FDD, TDD |

| Frequency Bands Covered | Licensed, Unlicensed, Shared Spectrum |

| Deployment Models Covered | Centralized, Distributed |

| Industry Verticals Covered | Healthcare, IT and Telecom, Manufacturing, Retail and E-commerce, Government and Defense, Government and Defense, Oil and Gas, Education, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | NEC Corporation, Fujitsu Limited, NTT Inc., Nokia Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan private LTE market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan private LTE market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan private LTE industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Private LTE Market Report

The Japan private LTE market reached USD 401.0 Million in 2025 and is projected to reach USD 1,259.7 Million by 2034.

The market is expected to grow at a CAGR of 13.56% during 2026-2034, driven by industrial digitalization, government local spectrum licensing, and critical infrastructure modernization.

The Kanto region leads with a 37.1% share in 2025, anchored by Greater Tokyo's automotive, chemical, and port industrial base and the Keihin industrial belt.

Infrastructure dominates with a 63.7% share in 2025, encompassing base stations, evolved packet core hardware, and network management platforms for private LTE deployments.

TDD holds the largest share at 58.4%, driven by its spectral efficiency advantage for asymmetric downlink-heavy industrial IoT applications, including machine vision and remote monitoring.

Some of the key players in the market include NEC Corporation, Fujitsu Limited, NTT, Inc., and Nokia Corporation.

TDD is growing at ~15.2% CAGR because Japan's expanding smart factory and smart port deployments generate asymmetric traffic patterns, high-volume downlink for surveillance video, and AR maintenance, which TDD's flexible slot configuration optimally addresses.

Key challenges include high deployment costs for SMEs, spectrum availability constraints in dense urban areas, legacy OT system integration complexity, and technology migration hesitation as enterprises evaluate private 5G as an alternative.

Smart port automation, precision agriculture IoT, public safety network modernization, Open-RAN private network deployments, and Private LTE-as-a-Service (PLaaS) business models represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)