Latin America Biodegradable Plastics Market Size, Share, Trends and Forecast by Type, End Use, and Country, 2026-2034

Latin America Biodegradable Plastics Market Size, Share, Trends & Forecast (2026-2034)

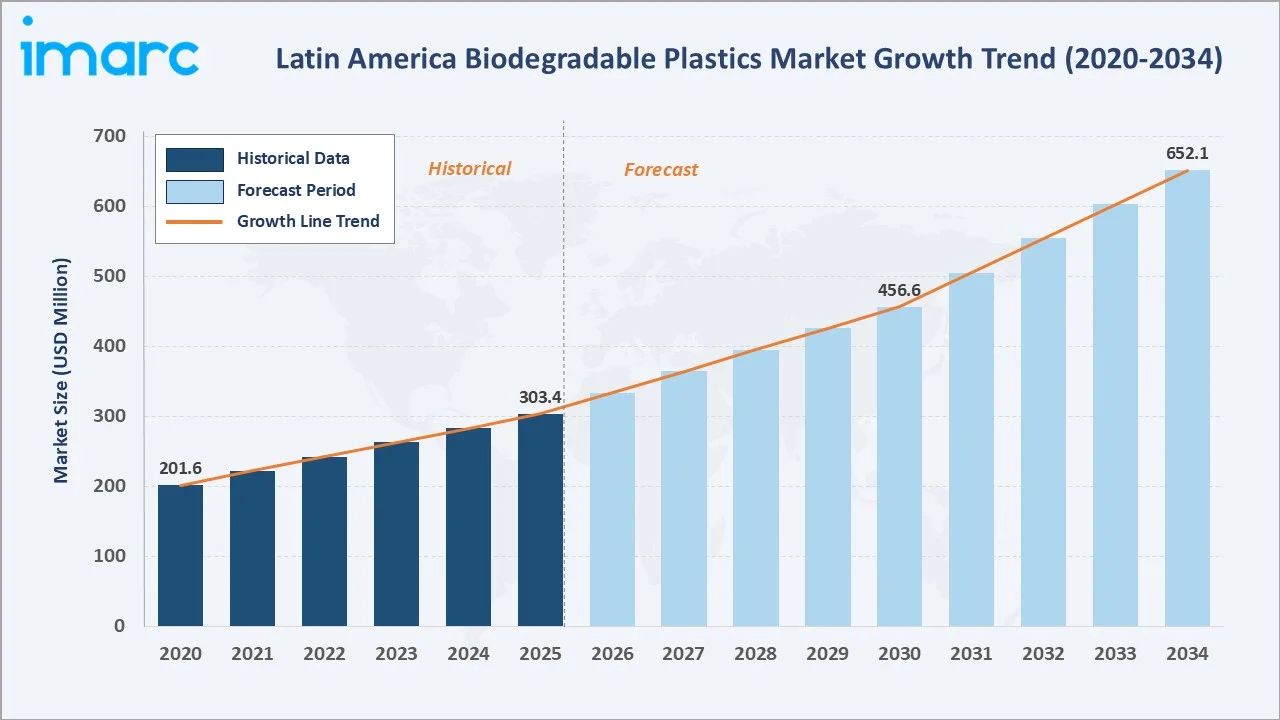

The Latin America biodegradable plastics market reached USD 303.4 Million in 2025 and is projected to reach USD 652.1 Million by 2034, growing at a CAGR of 8.52% during 2026-2034. The market is driven by rising plastic waste pollution, growing bans on single-use plastics, and increasing demand for sustainable packaging across food, retail, and consumer goods sectors. Latin America and the Caribbean generate nearly 17,000 tons of plastic waste daily in open dumpsites. This is driving demand for biodegradable plastics as governments, businesses, and consumers shift toward eco-friendly packaging and disposable alternatives. Starch-based polymers dominate at 32.8%. Packaging leads end-use at 46.7%. Brazil commands 35.9% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 303.4 Million |

|

Forecast Market Size (2034) |

USD 652.1 Million |

|

CAGR (2026-2034) |

8.52% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Starch-based (32.8%, 2025) |

|

Dominant End-Use |

Packaging (46.7%, 2025) |

|

Leading Country |

Brazil (35.9%, 2025) |

The market expanded from USD 201.6 Million in 2020 to USD 303.4 Million in 2025, anchored at USD 456.6 Million in 2030, and forecast to reach USD 652.1 Million by 2034. COVID-19's dual effect created mixed market dynamics in 2020-2021. Post-pandemic, the regulatory acceleration has been decisive: Brazil, Mexico, Colombia, Chile, and Peru all enacted or implemented single-use plastic restrictions between 2020-2023, creating permanent structural demand for certified compostable bioplastic alternatives that is independent of consumer willingness-to-pay for sustainable packaging.

To get more information on this market, Request Sample

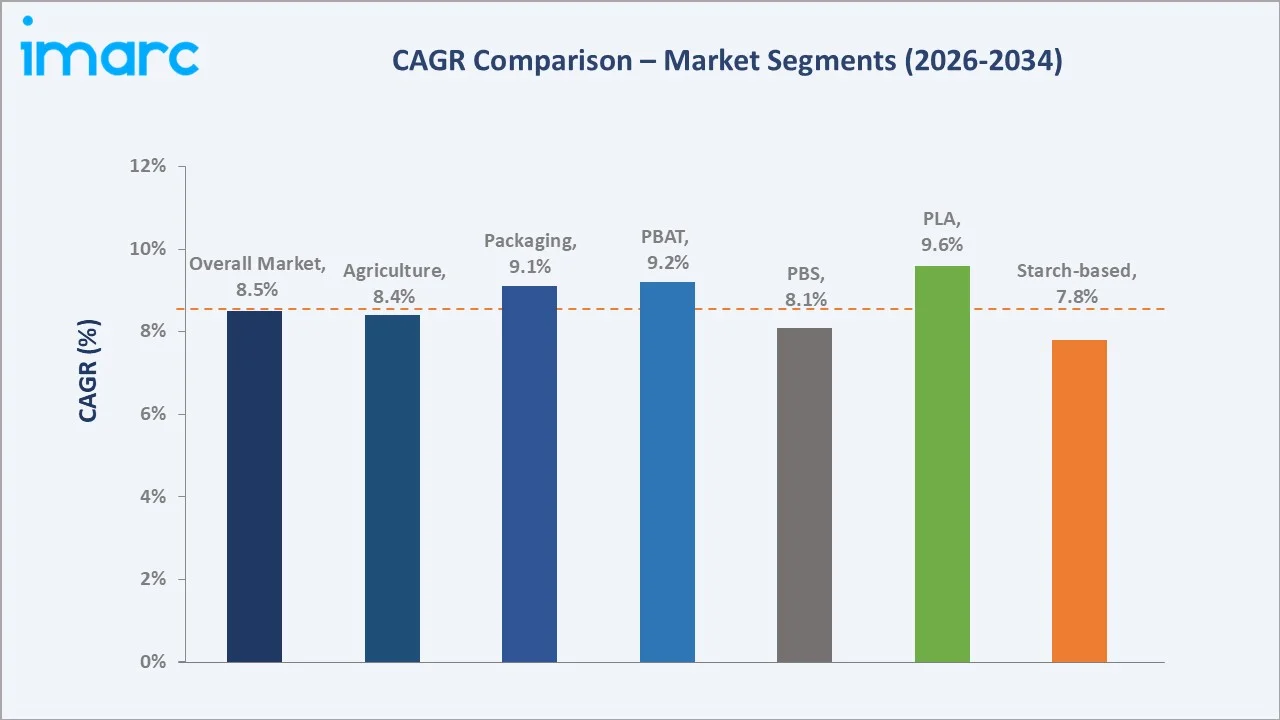

PLA grows fastest at ~9.6% CAGR through the premium food packaging, cold cups, and certified compostable cutlery applications, where PLA's transparency, rigidity, and food-contact safety make it the preferred biodegradable material for upscale foodservice and retail packaging. PBAT grows at ~9.2% CAGR.

Executive Summary

The Latin America biodegradable plastics market reached USD 303.4 Million in 2025, a figure that represents the nascent but accelerating commercial translation of a powerful regulatory, environmental, and corporate sustainability convergence. The market is projected to reach USD 652.1 Million by 2034.

Starch-based at 32.8% dominate through the lowest-cost entry point into biodegradable plastic. Packaging at 46.7% leads through the direct, regulatory-mandated transformation of Latin American retail and foodservice single-use packaging. Brazil, at 35.9%, is the dominant country in the market.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Starch-based - 32.8% share (2025) |

|

Dominant End-Use |

Packaging - 46.7% market share (2025) |

|

Leading Country |

Brazil - 35.9% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Starch-based at 32.8%: The starch-based segment dominates the market due to the easy availability of agricultural raw materials such as corn, cassava, and sugarcane across the region. Its cost-effectiveness, compostability, and wide use in packaging, bags, films, and disposable products further support strong adoption.

- Packaging at 46.7%: The packaging segment dominates the market due to rising demand for sustainable food packaging, shopping bags, films, and disposable containers. Growing restrictions on single-use plastics and increasing brand focus on eco-friendly packaging are further supporting its strong adoption.

- Brazil at 35.9%: Brazil dominates the market due to its large packaging, foodservice, and retail sectors, along with rising pressure to reduce plastic waste. The country’s strong agricultural base also supports the availability of bio-based raw materials such as sugarcane, corn, and cassava for biodegradable plastic production.

Latin America Biodegradable Plastics Market Overview

The Latin America biodegradable plastics market encompasses the production, importation, compounding, conversion, and distribution of certified biodegradable and compostable plastic materials for applications spanning packaging, agriculture, consumer goods, textiles, and medical uses. Biodegradable plastics are polymers that undergo degradation through microbial activity to produce water, carbon dioxide, and biomass, with the key distinction between industrial compostable and home compostable, marine biodegradable, and soil degradable.

The ecosystem integrates biobased feedstock suppliers, biopolymer resin producers, compounding specialists, film and rigid packaging converters, brand owners, composting infrastructure operators, and national regulatory bodies. Macroeconomic factors include rising urbanization, growing packaged food and retail consumption, and increasing pressure on waste management systems.

Market Dynamics

To evaluate market opportunities, Request Sample

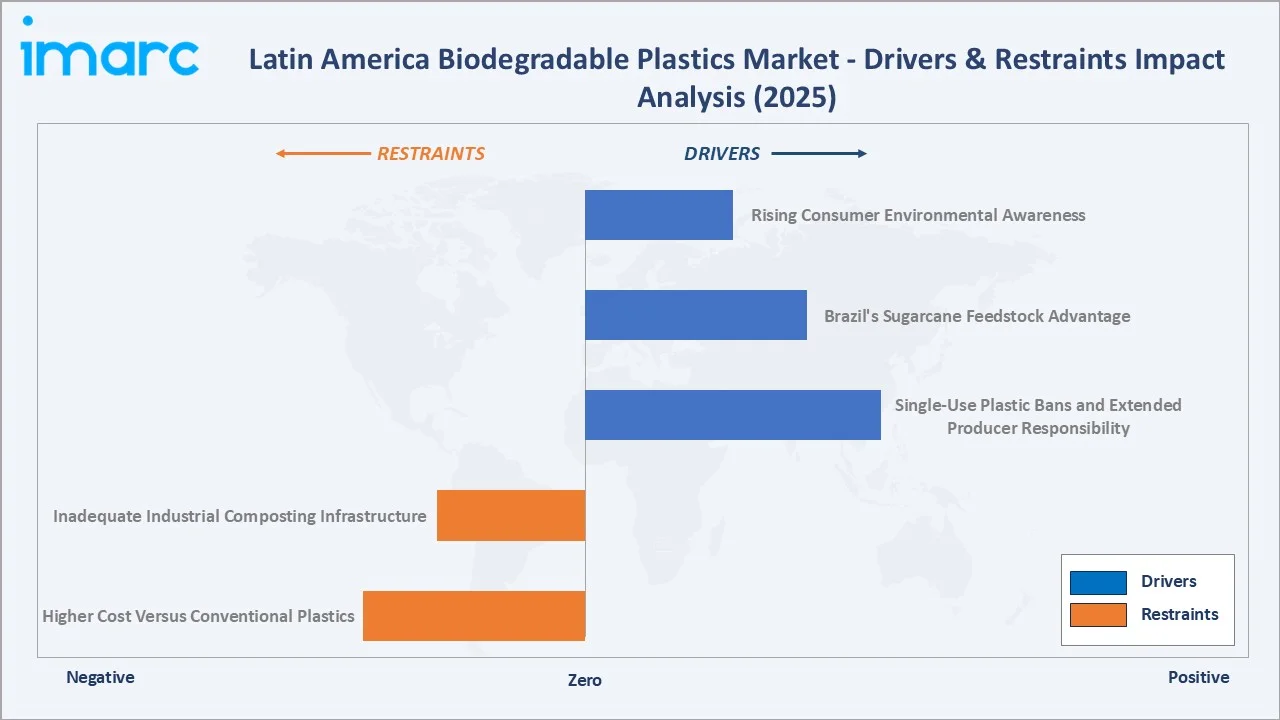

Market Drivers

- Single-Use Plastic Bans and Extended Producer Responsibility: In Mexico, 31 of the country’s 32 states have established bans and restrictions on different single-use products. This single-use plastic bans pushing manufacturers, retailers, and foodservice companies to replace conventional plastics with compostable and biodegradable alternatives. These regulations increase accountability for plastic waste collection, recycling, and disposal, encouraging companies to adopt sustainable packaging materials. As compliance pressure rises, demand for biodegradable bags, films, containers, and food packaging is expanding across the region.

- Brazil's Sugarcane Feedstock Advantage: Brazil’s sugarcane feedstock advantage is providing a strong, renewable raw material base for producing bio-based and biodegradable polymers. The country’s large sugarcane industry supports cost-efficient feedstock availability, improves local production potential, and reduces reliance on imported fossil-based inputs. This strengthens Brazil’s role in sustainable packaging, films, bags, and disposable product applications.

- Rising Consumer Environmental Awareness: Rising consumer environmental awareness is driving the market as more consumers prefer eco-friendly packaging, bags, and disposable products that reduce plastic pollution. Growing concerns over marine waste, landfill pressure, and public health impacts are encouraging brands and retailers to shift toward biodegradable alternatives. This is increasing demand across food packaging, retail, e-commerce, and consumer goods applications.

Market Restraints

- Higher Cost Versus Conventional Plastics: Biodegradable plastics carry significant cost premiums versus conventional petroleum-based plastics. In Latin American markets where household income constraints make consumers price-sensitive to FMCG packaging cost, these premiums are either absorbed by brand owners or partially passed to consumers. Small and medium food businesses face disproportionate packaging cost increases from biodegradable material substitution that create economic hardship without an equivalent consumer willingness-to-pay premium.

- Inadequate Industrial Composting Infrastructure: Inadequate industrial composting infrastructure is hampering the market because many biodegradable plastics require controlled composting conditions to break down properly. Limited composting facilities, weak waste segregation, and poor collection systems reduce the environmental benefits of these materials. This creates uncertainty for end users and slows adoption across packaging, foodservice, and retail applications.

Market Opportunities

- PHA Marine-Biodegradable Polymers Addressing Latin America's Coastal Marine Plastic Pollution Crisis: PHA marine-biodegradable polymers offer materials that can break down more effectively in marine environments compared to conventional plastics. This is especially relevant for coastal regions facing severe plastic leakage, beach pollution, and marine ecosystem damage. Their use in packaging, films, bags, and foodservice items can support sustainability goals and strengthen demand for advanced biodegradable solutions.

- Biodegradable Agricultural Mulch Film Adoption in Latin American Precision Agriculture Creating Large-Volume PBAT Demand: Biodegradable agricultural mulch film adoption supporting precision agriculture, soil moisture retention, weed control, and crop yield improvement. As farmers shift from conventional plastic films to biodegradable alternatives, demand for PBAT-based mulch films is increasing. This creates large-volume growth potential across fruit, vegetable, and specialty crop cultivation in the region.

Market Challenges

- Chinese PBAT Dumping Threatening European and Brazilian Premium Biodegradable Plastic Producers: Chinese PBAT dumping is increasing the availability of low-priced imported biodegradable resins, creating pricing pressure for European and Brazilian premium producers. This can reduce margins, discourage local capacity expansion, and make it harder for higher-quality certified biodegradable products to compete. It may also raise concerns over product consistency, certification standards, and long-term supply sustainability in the region.

- Lack of Unified LATAM Regulatory Harmonization Creating Compliance Complexity for Multi-Country Operations: Lack of unified LATAM regulatory harmonization creates different labeling, compostability, certification, and disposal requirements across countries. This increases compliance costs for companies operating in multiple markets and slows regional product standardization. As a result, manufacturers and packaging brands face delays in approvals, higher testing needs, and uncertainty in scaling biodegradable plastic solutions across Latin America.

Emerging Market Trends

1. Agricultural Biodegradable Mulch Film Trials Demonstrating Commercial Viability in LATAM Conditions

Agricultural biodegradable mulch film trials are emerging as field testing shows their suitability for regional crops, soil conditions, and climate patterns. These trials demonstrate benefits such as weed control, soil moisture retention, reduced plastic residue, and lower post-harvest film removal costs. As commercial viability improves, adoption is expected to increase across fruit, vegetable, and high-value crop farming.

2. Bioplastic Certification Ecosystem Maturing with New LATAM-Specific Standards

Bioplastic certification ecosystem maturation with new LATAM-specific standards is emerging as countries strengthen rules around compostability, biodegradability, labeling, and product claims. Colombia is emerging as a leading player in Latin America’s transition toward sustainable Latin America Bioplastics Market production. To support this shift, the country launched a Bioplastics Cluster with support from the Ministry of Science, Technology, and Innovation (MinCiencias) and the EU-funded Circular Plastics Program of the Americas (CPAP). Clearer certification frameworks help reduce greenwashing, improve consumer and brand trust, and support wider adoption of certified biodegradable packaging and agricultural films. This trend is also helping manufacturers align products with local climate, waste management, and composting conditions across the region.

3. Bio-Based Feedstock Localization Research Creating Potential for LATAM Manufacturing

Bio-based feedstock localization research is emerging as companies and research institutions explore regional raw materials such as sugarcane, corn, cassava, and agricultural residues for polymer production. This can reduce dependence on imported resins, lower feedstock costs, and support localized biodegradable plastic manufacturing. It also strengthens circular economy development by converting regional biomass resources into packaging, films, and disposable product applications.

4. Circular Economy Design Principles Driving Biodegradable-Plus-Composting System Solutions

Circular economy design principles are shifting focus from only producing biodegradable materials to building complete composting and waste-recovery systems. Companies are designing packaging, bags, and agricultural films that align with collection, sorting, composting, and organic waste management infrastructure. This approach supports closed-loop material use, reduces landfill pressure, and improves the real environmental value of biodegradable plastics across the region.

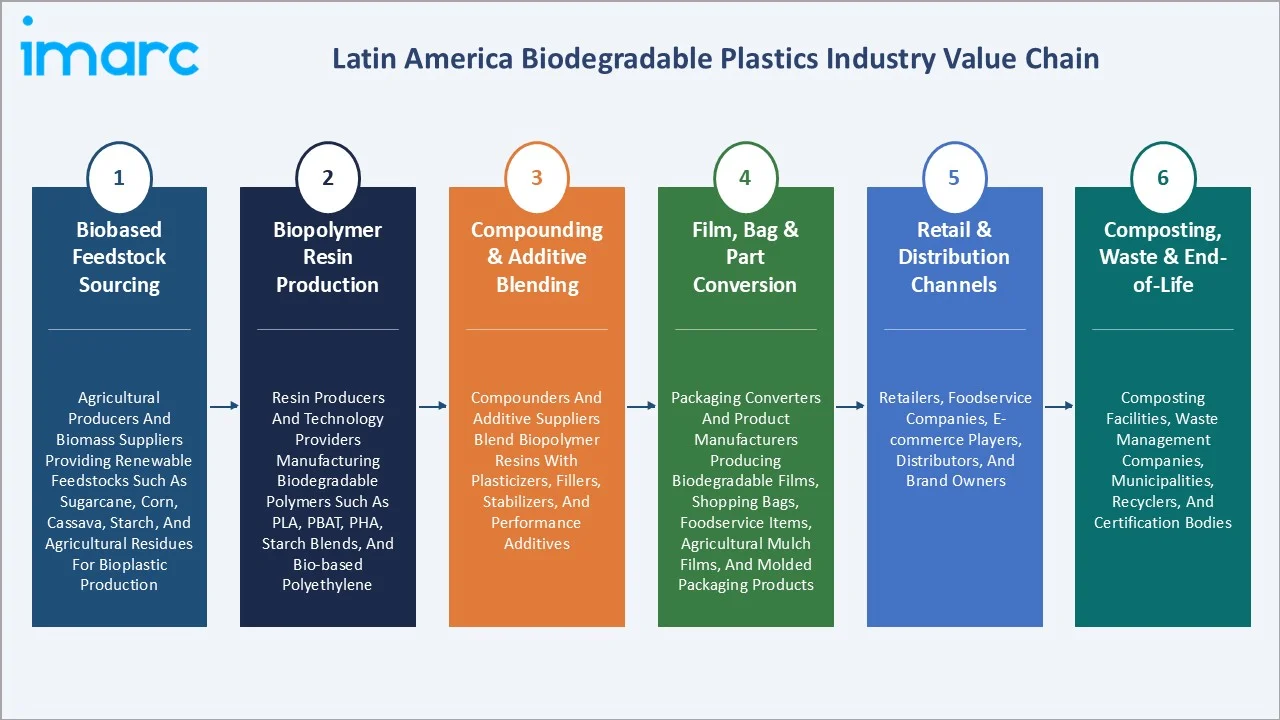

Industry Value Chain Analysis

The Latin America biodegradable plastics value chain integrates biobased feedstock sourcing, biopolymer resin production, compounding and additive blending, film/bag/part conversion, retail and distribution channels, and composting and waste management infrastructure. The value chain's most critical commercial bottleneck is the gap between biopolymer resin production and LATAM end-user markets.

|

Stage |

Key Participants |

|

Biobased Feedstock Sourcing |

Agricultural producers and biomass suppliers providing renewable feedstocks such as sugarcane, corn, cassava, starch, and agricultural residues for bioplastic production. |

|

Biopolymer Resin Production |

Resin producers and technology providers manufacturing biodegradable polymers such as PLA, PBAT, PHA, starch blends, and bio-based polyethylene. |

|

Compounding & Additive Blending |

Compounders and additive suppliers blend biopolymer resins with plasticizers, fillers, stabilizers, and performance additives. |

|

Film, Bag & Part Conversion |

Packaging converters and product manufacturers producing biodegradable films, shopping bags, foodservice items, agricultural mulch films, and molded packaging products. |

|

Retail & Distribution Channels |

Retailers, foodservice companies, e-commerce players, distributors, and brand owners. |

|

Composting, Waste & End-of-Life |

Composting facilities, waste management companies, municipalities, recyclers, and certification bodies. |

The composting and waste management tier is the value chain's most commercially underdeveloped stage. LATAM composting infrastructure development represents both the market's most critical limiting factor and a significant investment opportunity for environmental services companies and municipalities seeking to operationalize circular economy ambitions.

Technology Landscape in the Latin America Biodegradable Plastics Industry

Polylactic Acid (PLA) Technology

Polylactic Acid (PLA) technology enables the production of compostable packaging, foodservice items, films, and molded products from renewable feedstocks such as corn, sugarcane, and cassava. Its good clarity, rigidity, and processability make it suitable for replacing conventional plastics in packaging applications. Growing interest in local bio-based feedstock uses and compostable product development is further supporting PLA adoption across the region.

PBAT (Polybutylene Adipate Terephthalate) Technology

PBAT technology is enabling flexible, compostable materials for bags, films, food packaging, and agricultural mulch films. Its high flexibility, toughness, and compatibility with starch and PLA blends make it suitable for replacing conventional polyethylene in single-use applications. Rising demand for biodegradable packaging and mulch films is supporting PBAT-based product development across the region.

Thermoplastic Starch (TPS) and Starch Blends

Thermoplastic starch (TPS) and starch blends are using locally available feedstocks such as corn, cassava, and sugarcane-derived starch. These materials offer a cost-effective and compostable alternative to bags, films, packaging, and disposable products. Their ability to blend with PLA, PBAT, and other biopolymers improves flexibility, durability, and processability, supporting wider commercial adoption across the region.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Starch-based |

32.8% |

2025 |

|

End Use |

Packaging |

46.7% |

2025 |

|

Country |

Brazil |

35.9% |

2025 |

By Type

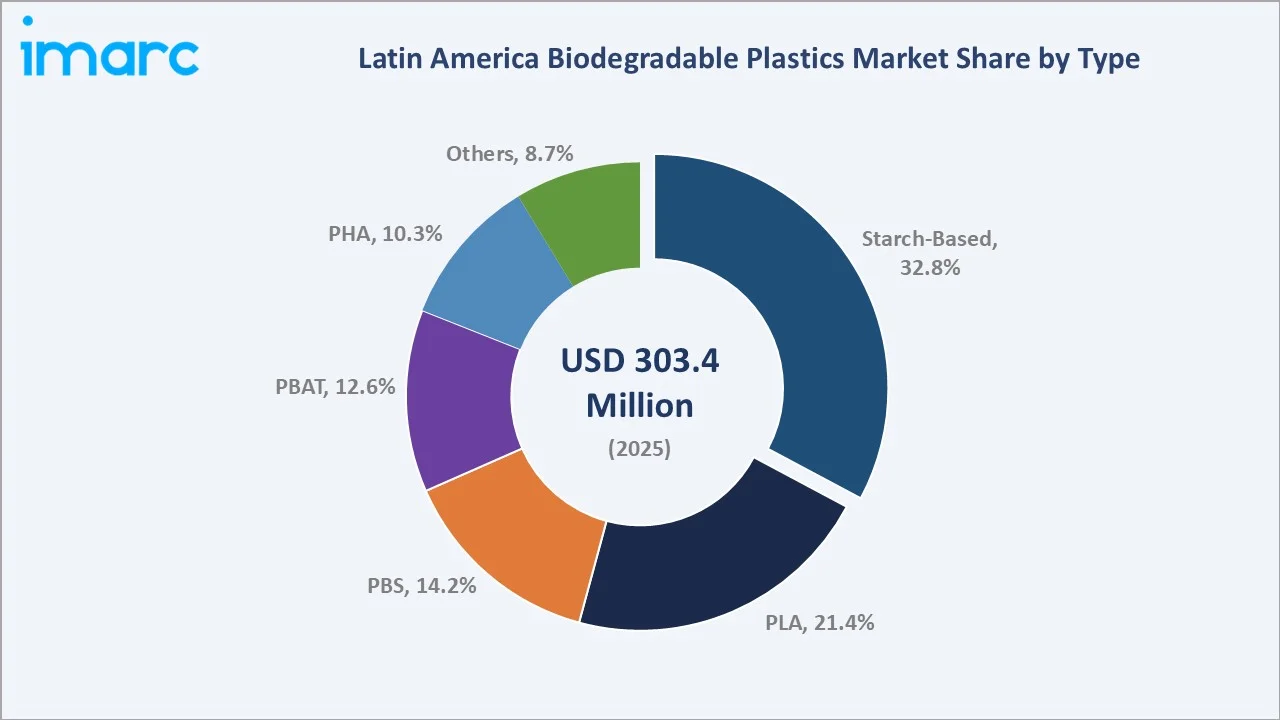

Starch-based polymers lead at 32.8% market share (2025). Starch-based bioplastics encompass thermoplastic starch (TPS) and starch-PBAT blends used primarily in single-use bag applications, loose fill packaging, and compostable food service containers. The starch category's market leadership reflects Brazil's and Mexico's mass-market single-use plastic ban compliance requirements, driving adoption of the lowest-cost certified compostable alternative.

To access detailed market analysis, Request Sample

PLA at 21.4% grows fastest at ~9.6% CAGR. PBS at 14.2% serves cold-chain and water-degradable applications. PBAT at 12.6% grows at ~9.2% through agricultural mulch film. PHA at 10.3% serves premium marine-sensitive applications. Others at 8.7% encompasses bio-PE, bio-PET, PBS blends, and emerging research-stage biopolymers.

By End Use

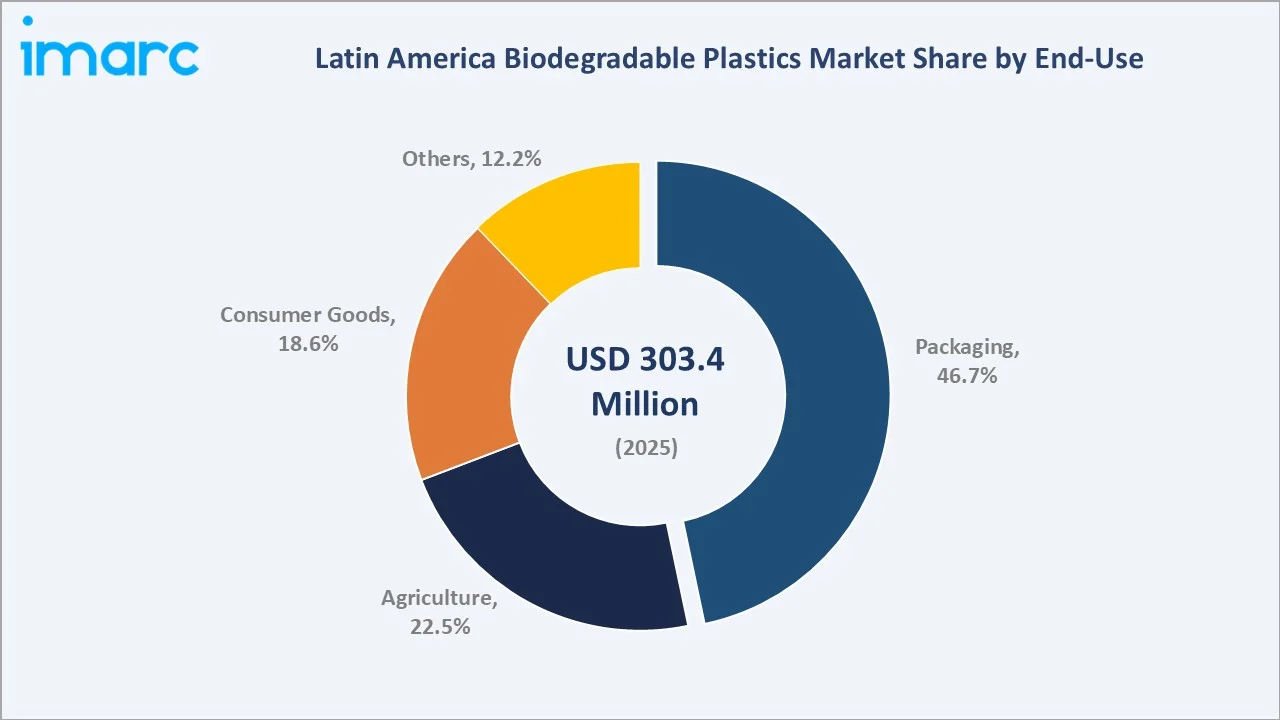

Packaging leads at 46.7% market share (2025). Packaging encompasses single-use compostable shopping bags, food service packaging, food packaging film, and biodegradable secondary packaging. Packaging's dominance is directly regulatory-driven; each new single-use plastic ban jurisdiction converts conventional plastic packaging demand to certified compostable bioplastic procurement in a mandated, non-discretionary manner.

Agriculture at 22.5% encompasses PBAT mulch film, biodegradable twine, planting pots, and irrigation system components. Consumer goods at 18.6% covers personal care packaging, household product containers, and biodegradable disposable goods. Others at 12.2% includes medical, textile, and industrial applications.

Regional Market Insights

|

Country |

Share (2025) |

Key Biodegradable Plastics Market Drivers & Characteristics |

|

Brazil |

35.9% |

Supported by its large packaging, foodservice, retail, and agricultural sectors, along with a strong availability of bio-based feedstocks. |

|

Mexico |

19.3% |

Driven by growing demand for sustainable packaging, expanding retail and food delivery sectors, and increasing regulatory pressure to reduce single-use plastic consumption. |

|

Argentina |

11.4% |

Supported by its agricultural base, the rising use of compostable packaging, and the growing interest in biodegradable films for farming and food applications. |

|

Colombia |

9.2% |

Supported by sustainability initiatives, circular economy programs, and the rising adoption of biodegradable packaging across consumer markets. |

|

Chile |

8.1% |

Benefits from strong environmental awareness, plastic reduction initiatives, and increasing demand for compostable packaging in retail, foodservice, and coastal sustainability applications. |

|

Peru |

6.7% |

Expanding gradually through rising awareness of plastic pollution, growing sustainable packaging demand, and increasing regulatory support for eco-friendly alternatives. |

|

Others |

9.4% |

The others include smaller Latin American markets where biodegradable plastic adoption is increasing through plastic waste reduction efforts, retail sustainability programs, and early-stage compostable packaging demand. |

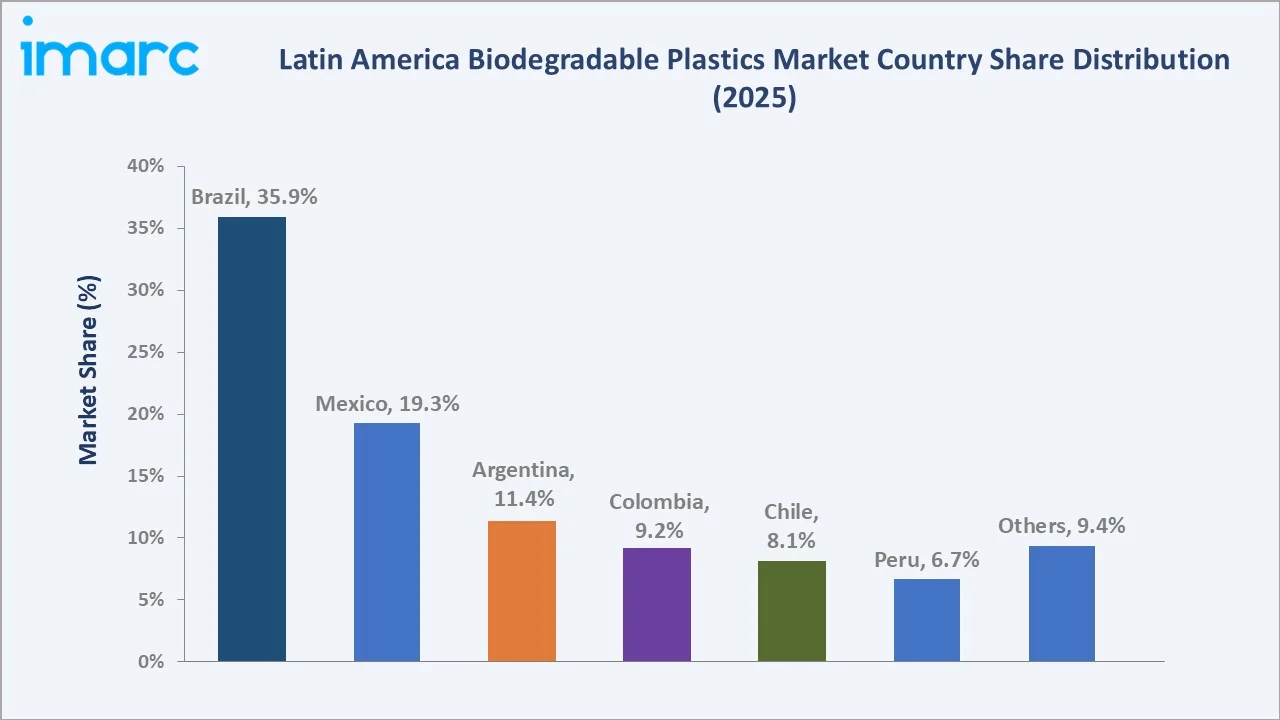

Brazil's 35.9% market leadership is reinforced by the regulatory framework, the Brazilian agricultural sector's PBAT mulch adoption, and the domestic compounding and converting industry. Mexico's 19.3% reflects the most comprehensive single-use plastic ban implementation. Argentina (11.4%), Colombia (9.2%), each have distinctive regulatory and sectoral drivers creating growing national biodegradable plastic markets.

Chile's 8.1% share features Latin America's most advanced legislation and the highest per-capita income, creating consumer willingness-to-pay for premium certified compostable packaging. Peru's 6.7% reflects the earliest hard plastic bag ban, creating market-leading compliance adoption. The Others category (9.4%) encompasses Ecuador, Uruguay, Bolivia, Central America, and Caribbean nations, each developing biodegradable plastic markets through progressive national environmental legislation.

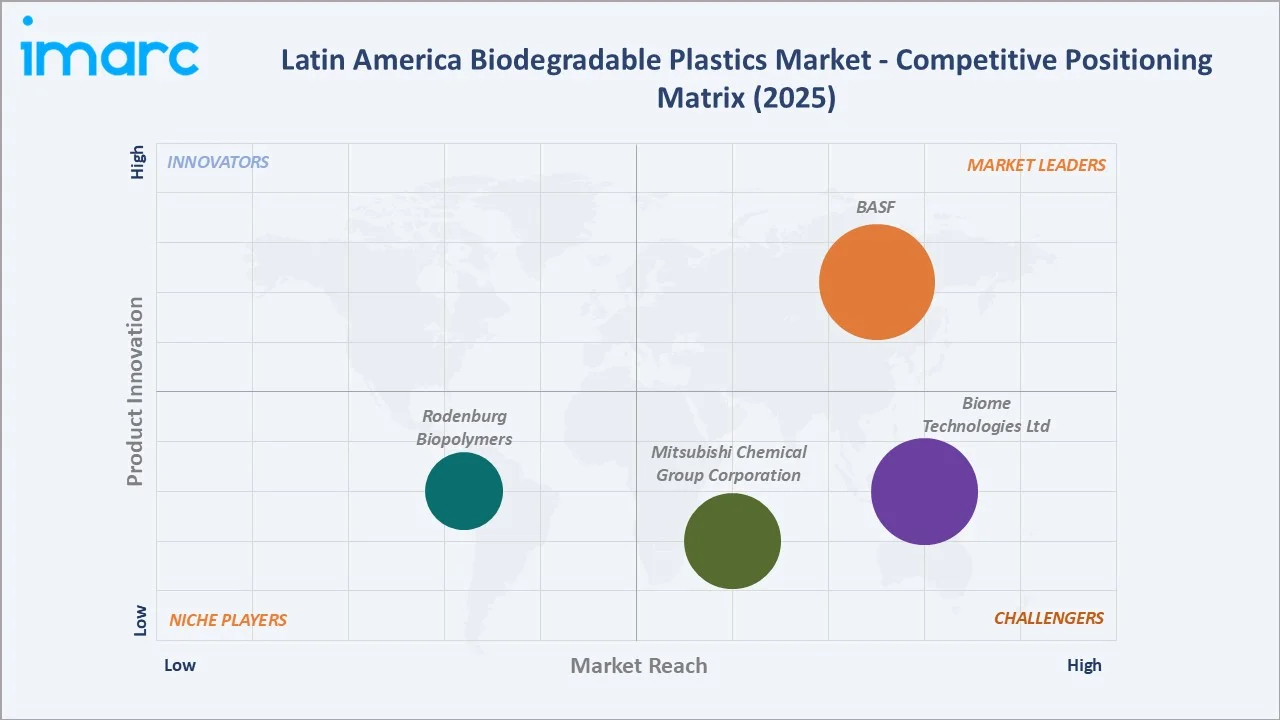

Competitive Landscape

The biodegradable plastics competitive landscape is dominated by European and North American biopolymer resin manufacturers, collectively supplying an estimated 55-65% of LATAM certified compostable bioplastic resin demand by volume. Chinese manufacturers are growing their LATAM market share through price-competitive PBAT and PLA supply, creating competitive pressure on European premium suppliers that is most acute in the cost-sensitive starch-based bag and agricultural mulch film segments.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

BASF |

ecoflex, ecovio |

Market Leader |

BASF has been researching on biodegradable, bio-based and certified compostable biopolymers |

|

Biome Technologies Ltd |

BiomeHT90, BiomeHTX (450), BiomeEP1, BiomeEP2 |

Challenger |

Based on renewable, natural resources, Biome Technologies products are 100% biodegradable and compostable, and suitable for a wide array of plastic processing |

|

Mitsubishi Chemical Group Corporation |

BioPBS |

Strong Challenger |

Polybutylene succinate (PBS) is a biodegradable plastic that decomposes into water and carbon dioxide with the microorganisms in the soil. |

|

Rodenburg Biopolymers |

Solanyl |

Niche Player |

Solanyl is a group of products consisting of a smart series of biobased and biodegradable end compounds, suitable for direct conversion by the various known techniques. |

The competitive landscape is increasingly contested at the converter level rather than the resin level. LATAM-based converting companies that transform imported biopolymer resins into finished compostable bags, films, and containers are the primary commercial interface with end-users and increasingly differentiate on certifications, local technical service, compostable product design, and supply chain reliability rather than resin chemistry alone.

Key Company Profiles

BASF

BASF is one of the world's largest chemical company, with its biopolymers division producing ecoflex and ecovio blend as the global reference commercial biodegradable polymers for agricultural film and shopping bag applications.

- Key Products: ecoflex, ecovio.

- Recent Developments: In April 2026, BASF expanded its certified compostable ecovio portfolio with new grades that meet the increasing recycling needs of flexible barrier packaging. The extended portfolio enables manufacturers of flexible packaging and brand owners to tailor barrier performance and end-of-life options like organics or paper recycling according to application functionalities, processing technologies and regulatory frameworks.

- Strategic Focus: Centered on expanding compostable polymer solutions, especially PBAT-based and certified biodegradable materials, for sustainable packaging, bags, and agricultural film applications.

Mitsubishi Chemical Group Corporation

Mitsubishi Chemical Group Corporation is a global chemical company active in biodegradable polymers through its BioPBS, a bio-based polybutylene succinate material developed for compostable packaging, films, paper coating, and foodservice applications.

- Key Products: BioPBS.

- Strategic Focus: Focused on expanding BioPBS-based compostable solutions for flexible packaging, foodservice, paper coating, and agricultural applications while supporting Latin America’s shift toward sustainable and biodegradable plastic alternatives.

Market Concentration Analysis

The Latin America biodegradable plastics market exhibits moderate-to-high concentration at the resin supply level and fragmentation at the converter and distributor levels. BASF and Mitsubishi Chemical Group Corporation together supply approximately 55-65% of certified compostable biopolymer resin volume for LATAM applications. This concentration reflects the high technical and capital barriers to biopolymer resin production.

Chinese manufacturers are progressively gaining LATAM market share, particularly in PBAT and PLA segments, where Chinese production capacity expansion and export pricing are creating cost competition that European manufacturers must respond to through operational efficiency, product differentiation, or certification quality assurance. The LATAM biodegradable plastics market concentration is expected to decrease through 2034 as Brazilian domestic production investment materializes and Chinese export competition intensifies, creating a more competitive multi-supplier resin market that benefits LATAM converters through lower resin input costs.

Investment & Growth Opportunities

Highest Growth Segments

PLA (~9.6% CAGR), PBAT (~9.2% CAGR), packaging end-use (~9.1% CAGR), agriculture end-use (~8.4% CAGR), PHA marine-biodegradable niche (~12-15% CAGR from a small base), Brazil's certified compostable bag market (~10% national CAGR through PNRS expansion), and the LATAM certified compostable foodservice packaging market (~12% CAGR through restaurant chain adoption) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

LATAM industrial composting infrastructure development represents the biodegradable plastics market's most critical infrastructure investment gap, and its most commercially attractive adjacent opportunity. Public-private partnership structures create viable investment cases. Municipalities that establish industrial composting infrastructure create the backbone condition that transforms certified compostable bioplastic from a questionable environmental claim to a genuinely circular economy solution.

Investment Themes

- Brazilian sugarcane PLA production investment for LATAM supply chain cost leadership: A PLA production facility in Brazil using sugarcane-derived lactic acid could produce PLA at USD 1.20-1.50/kg (versus USD 1.80-2.50/kg for imported), a 25-40% cost reduction that would transform LATAM PLA market economics.

- PBAT agricultural mulch film market development investment in Brazil's Northeast and Cerrado agriculture: Northeast Brazil and Central-West Cerrado collectively use an estimated 30,000-50,000 tonnes of PE mulch film annually that could be replaced by PBAT biodegradable equivalents. Converting 20% of this demand to PBAT represents USD 30-50 Million in annual PBAT agricultural film revenue. Investment in PBAT film conversion capacity in Northeast Brazil.

Future Market Outlook (2026-2034)

The Latin America biodegradable plastics market is projected to grow from USD 303.4 Million in 2025 to USD 652.1 Million by 2034, delivering an 8.52% CAGR over the forecast period. The market's anchor value of USD 456.6 Million in 2030 represents a LATAM biodegradable plastics industry where Brazil has achieved near-complete certified compostable bag compliance across all state-regulated retail channels, Mexico has implemented national-level single-use plastic prohibition, creating unified biodegradable packaging demand, Chile has driven systematic packaging sustainability investment, and the first LATAM-manufactured PLA and PBAT commercial production has commenced.

Three structural forces define the LATAM biodegradable plastics market growth through 2034 with high confidence. First, regulatory escalation permanence, the political economy of single-use plastic regulation in Latin America is asymmetric. Second, feedstock cost advantage realization. Third, corporate sustainability compliance momentum.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including Regional Sales Directors; bioplastic converter CEOs; agricultural film product managers; sustainability packaging procurement managers; regulatory specialists; and Braskem biopolymer research division technical leadership.

Secondary Research

Secondary research encompassed European Bioplastics (EUBP) Bioplastics Market Data 2025 (global market data with LATAM breakdown); Brazilian biodegradable packaging standard documentation; Brazil Ministry of Environment reports; Mexico plastic regulation implementation reports; Chile packaging implementation data; Colombia compliance reporting; Peru enforcement report; individual company annual reports; and European Bioplastics Facts and Figures. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up country and end-use models calibrated against (i) regulatory compliance demand modelling, quantifying the addressable packaging volume subject to single-use plastic bans in Brazil, Mexico, Colombia, Chile, and Peru and converting to biodegradable plastic demand at certified compostable compliance rates, (ii) agricultural film demand from Latin American horticultural acreage data and mulch film adoption penetration curves, and (iii) voluntary ESG adoption demand from corporate sustainability commitment data for LATAM-operating multinationals. Biopolymer resin price forecasts calibrated against the European Bioplastics price index, BASF and NatureWorks commercial pricing disclosures, and Chinese PBAT export price data. Key inputs include Brazilian sugarcane feedstock cost advantage quantification, the LATAM industrial composting infrastructure investment pipeline, and the single-use plastic ban implementation timeline by country.

Latin America Biodegradable Plastics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Starch-based, PLA, PBS, PBAT, PHA, Others |

| End Uses Covered | Packaging, Agriculture, Consumer Goods, Others |

| Countries Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | BASF, Biome Technologies Ltd, Mitsubishi Chemical Group Corporation, Rodenburg Biopolymers, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Latin America biodegradable plastics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Latin America biodegradable plastics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Latin America biodegradable plastics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Latin America Biodegradable Plastics Market Report

The Latin America biodegradable plastics market reached USD 303.4 Million in 2025, driven by regulatory-mandated single-use plastic bans in Brazil, Mexico, Colombia, Chile, and Peru, creating certified compostable bioplastic demand, Brazil's solid waste framework, PBAT agricultural mulch film adoption, PLA premium food packaging growth, and corporate commitments from multinational brand owners operating in the region.

The market grows at 8.52% CAGR during 2026-2034, reaching USD 652.1 Million by 2034. The high CAGR reflects regulatory escalation, Brazil's sugarcane feedstock advantage maturing toward commercial domestic biopolymer production, PBAT agricultural mulch film LATAM adoption, PHA marine-biodegradable packaging premium segment growth, and corporate ESG packaging commitments from European multinationals' LATAM operations.

Starch-based polymers lead at 32.8% through lowest-cost certified compostable alternative for Brazil's and Mexico's single-use plastic bag compliance.

Packaging leads at 46.7% through direct single-use plastic ban compliance, driving compostable bag, food service container, and retail packaging demand. Packaging grows fastest at ~9.1% CAGR.

Brazil leads at 35.9% (USD 108.9 Million) through the PNRS regulatory framework, sugarcane feedstock advantage, Braskem's bio-based polymer platform, domestic compounding and converting industry, and agricultural sector PBAT mulch adoption. Mexico's 19.3% reflects Latin America's most comprehensive single-use plastic ban (Mexico City 2020). Chile's 8.1% features Latin America's most advanced EPR legislation, driving systematic packaging sustainability.

Leading companies include BASF, Biome Technologies Ltd, Mitsubishi Chemical Group Corporation, and Rodenburg Biopolymers, among others.

The market is projected to reach approximately USD 456.6 Million by 2030 as Brazil achieves near-complete certified compostable bag compliance, composting infrastructure creates urban circular economy completeness, Mexico implements national single-use plastic harmonization, Chile's packaging drives systematic corporate adoption, and the first LATAM-manufactured PLA production creates structural cost reduction for PLA-dependent packaging applications.

Biodegradable means a material breaks down through microbial action into natural elements, but without specifying the timeframe, conditions, or completeness. Compostable (certified) means a material degrades completely within a specified timeframe under defined composting conditions.

Brazil's sugarcane is the world's lowest-cost fermentation feedstock. For PLA production, Brazilian sugarcane-derived lactic acid enables 25-40% lower feedstock cost versus corn-based. For PHA fermentation, Brazilian sugarcane carbon substrates enable fermentation at the world's lowest variable cost.

Three priority opportunities: Brazilian sugarcane PLA production facility, LATAM industrial composting infrastructure, and PBAT agricultural mulch film production in Northeast Brazil.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade