Latin America Carbon Capture and Storage (CCS) Market Size, Share, Trends and Forecast by Service, Technology, End Use Industry, and Region, 2026-2034

Latin America Carbon Capture and Storage (CCS) Market Size, Share, Trends & Forecast (2026-2034)

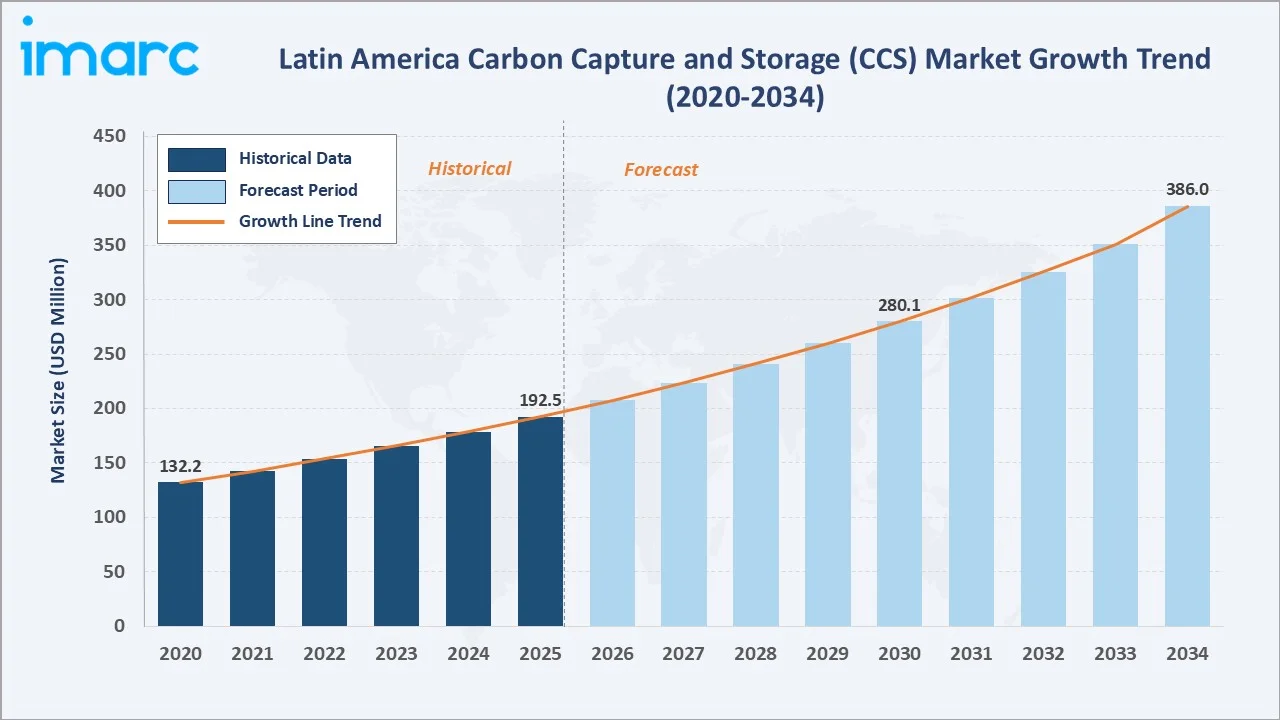

The Latin America carbon capture and storage (CCS) market reached USD 192.5 Million in 2025 and is projected to reach USD 386.0 Million by 2034, growing at a CAGR of 7.80% during 2026-2034. Nationally Determined Contribution (NDC) climate commitments across the region, the strong demand for CO₂-enhanced oil recovery (EOR) in Brazil’s offshore fields, and accelerating international climate finance and carbon credit mechanisms are the primary forces driving sustained market expansion throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Market Size (2025) |

USD 192.5 Million |

|

Market Size (2034) |

USD 386.0 Million |

|

CAGR (2026-2034) |

7.80% |

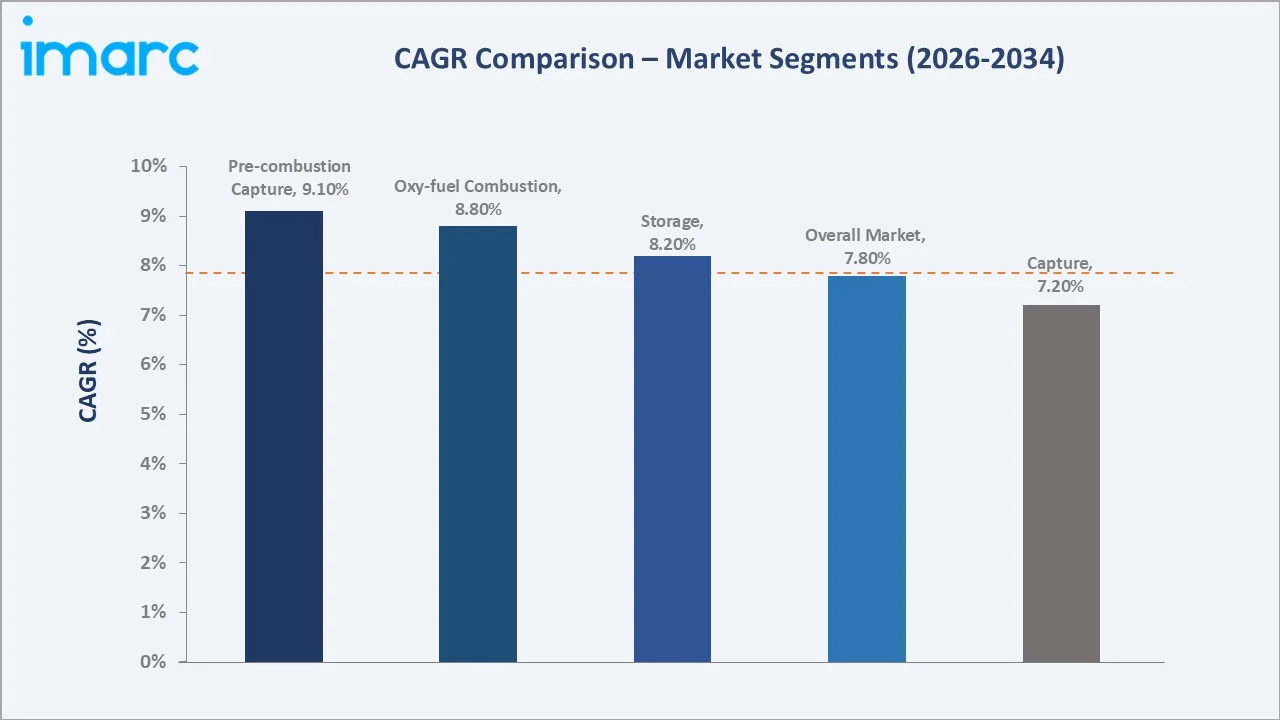

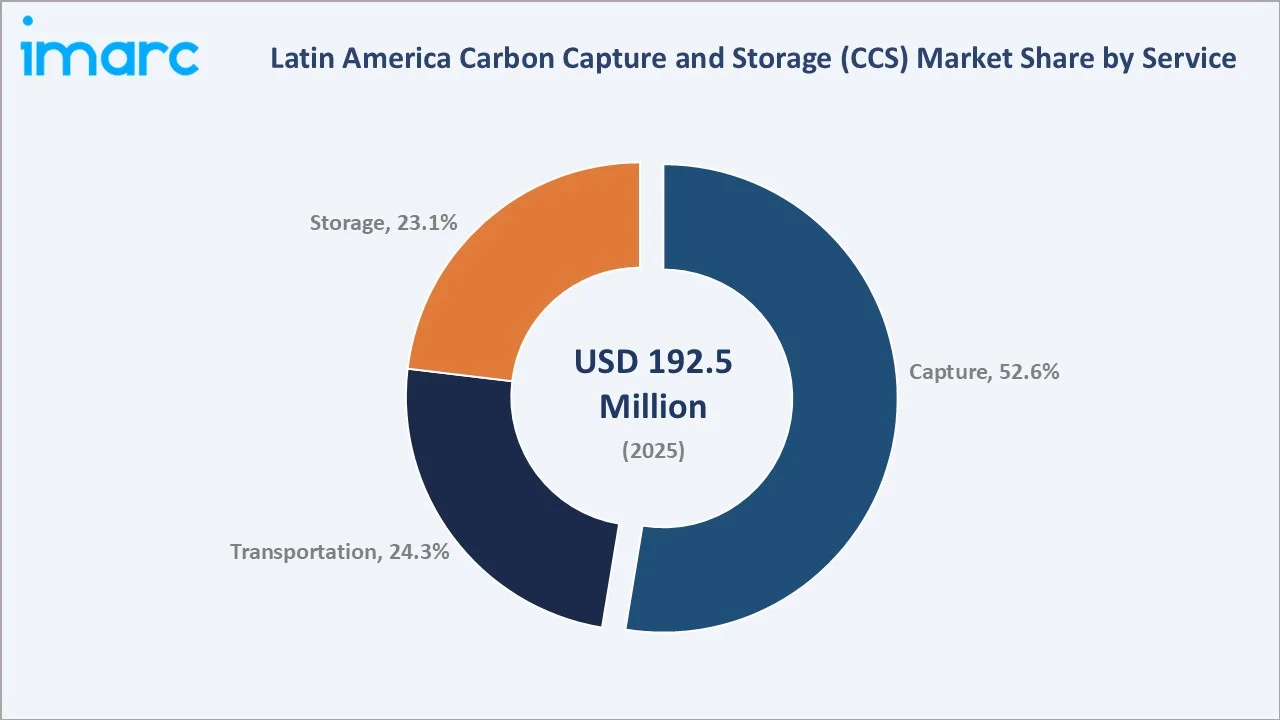

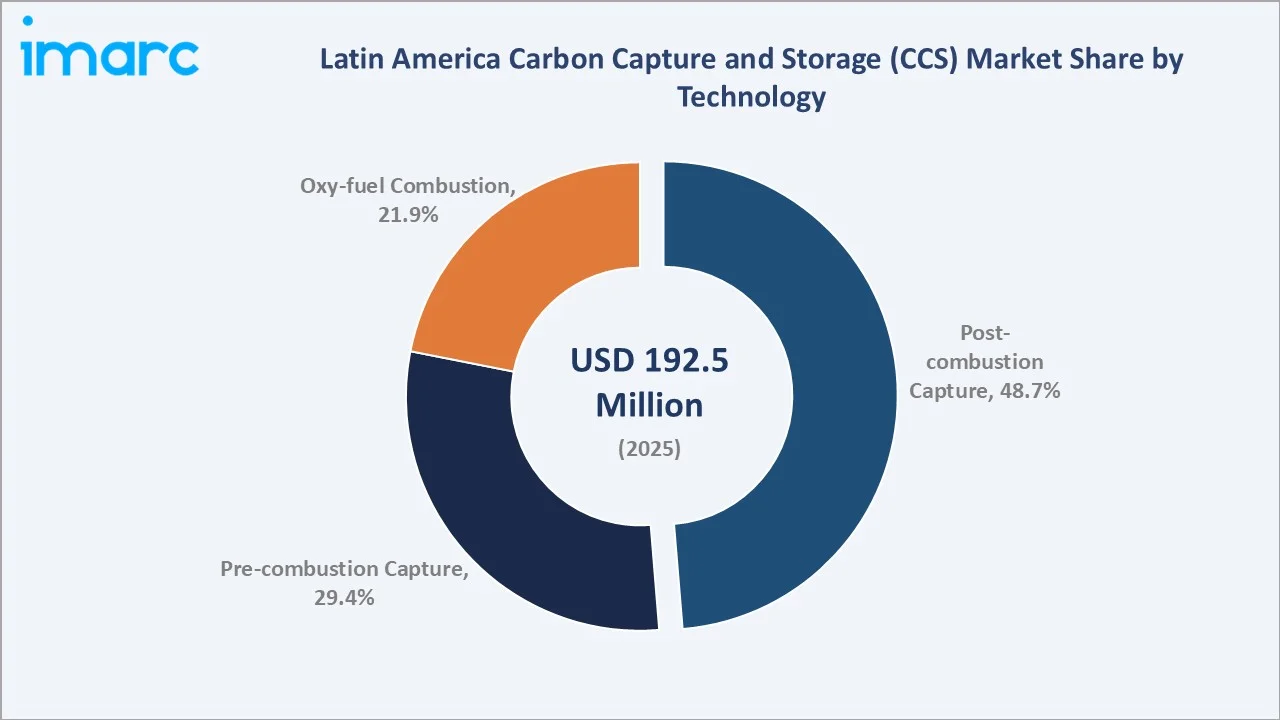

Brazil leads regionally with a 41.2% market share in 2025, anchored by Petrobras’ world-leading CO₂ injection operations in the Santos Basin pre-salt fields and the country’s strong commitment to net-zero by 2050. Capture dominates the service mix at 52.6%, while post-combustion capture leads the technology segment at 48.7%. Pre-combustion capture is the fastest-growing technology at ~9.1% CAGR, driven by hydrogen and blue ammonia project development across Brazil and Argentina.

To get more information on this market, Request Sample

The market grew from USD 132.2 Million in 2020 to USD 192.5 Million in 2025, an increase of USD 60.3 Million over five years, reflecting the growing deployment of CCS in Brazil’s oil and gas sector and early-stage government-backed pilot projects in Mexico, Colombia, and Argentina. The market is forecast to reach USD 386.0 Million by 2034, driven by the scaling of large-scale CO₂ storage infrastructure, the maturation of the regional carbon credit market, and the entry of major global CCS technology providers, increasing competition, and driving down deployment costs.

Executive Summary

The Latin America CCS market is positioned at an inflection point, transitioning from early-stage oil-field EOR-driven deployment toward a diversified decarbonization infrastructure serving power generation, steel, cement, petrochemicals, and blue hydrogen production across multiple countries. The market stood at USD 192.5 Million in 2025 and is forecast to reach USD 386.0 Million by 2034 at a 7.80% CAGR.

Capture dominates the service mix with a 52.6% share in 2025, reflecting the capital and technology intensity of CO₂ capture systems relative to downstream transportation and storage services. Transportation at 24.3% and storage at 23.1% represent the downstream infrastructure segments requiring the most significant long-term public and private investment to scale the full CCS value chain beyond existing oil-field applications.

Post-combustion capture leads technology at 48.7%, driven by its retrofittability onto existing power plants, steel mills, and cement facilities without fundamental process redesign. Pre-combustion capture at 29.4% is gaining ground in new-build hydrogen production projects, while oxy-fuel combustion capture at 21.9% is advancing in Brazil’s ethanol and biomass sector as BECCS (Bioenergy with Carbon Capture and Storage) technology.

Brazil commands 41.2% of the regional market, anchored by Petrobras’ mature CO₂ EOR operations in the Santos Basin and the country’s world-class geological storage potential. Mexico, at 19.3%, benefits from PEMEX’s developing CCS roadmap and proximity to US CCS policy and financing frameworks under the IRA.

Key Market Insights

|

Insight |

Data |

|

Largest Service |

Capture – 52.6% share (2025) |

|

Fastest Growing Service |

Storage – ~8.2% CAGR (2026-2034) |

|

Largest Technology |

Post-combustion Capture – 48.7% share (2025) |

|

Fastest Growing Technology |

Pre-combustion Capture – ~9.1% CAGR (2026-2034) |

|

Leading Country |

Brazil – 41.2% share (2025) |

|

Top Companies |

SLB Limited, Baker Hughes Company, Honeywell International Inc., Halliburton Company, TechnipFMC plc |

Key Analytical Observations Supporting The Above Data:

- Capture at 52.6% (2025) reflects the front-end capital and technology intensity of CO₂ capture systems, which typically account for 60–75% of total CCS project capital expenditure. The capture stage encompasses solvent absorption, adsorption, membrane separation, and cryogenic separation technologies applied to flue gas streams from power plants, industrial facilities, and oil and gas processing plants across the region.

- Post-combustion capture at 48.7% (2025) dominates as it can be retrofitted to existing industrial and power generation assets without fundamental redesign, making it the lowest-risk adoption pathway for Latin America’s existing fossil-fuel-based industrial base.

- Pre-combustion capture at ~9.1% CAGR is the fastest-growing technology, driven by blue hydrogen production project development in Brazil, Chile’s green and blue hydrogen export strategy targeting European markets, and Colombia’s hydrogen roadmap requiring pre-combustion capture integration with natural gas reforming.

- Brazil’s 41.2% (2025) market leadership reflects Petrobras’ unique position as the world’s largest offshore CO₂ EOR operator, with 10.6 million tons of CO₂ per annum injected into the Santos Basin pre-salt carbonate reservoirs as part of standard field production operations. This creates the world’s largest involuntary CCS infrastructure that is progressively being scaled and formalized as intentional carbon storage.

Latin America Carbon Capture and Storage (CCS) Market Overview

The Latin America CCS market encompasses technologies and services for capturing, compressing, transporting, and geologically storing CO₂ emissions from industrial point sources, including oil and gas processing, power generation, steel and cement manufacturing, petrochemical production, and bioenergy with carbon capture (BECCS) applications.

Latin America’s CCS value chain is characterized by the dominance of the upstream capture and compression stage, the nascent state of dedicated CO₂ transportation pipeline infrastructure in most countries outside Brazil, and the geological diversity of storage options ranging from Brazil’s Santos Basin carbonate reservoirs to saline aquifers in the Argentine Cuyana Basin and depleted gas fields in Colombia’s Llanos Basin.

Market Dynamics

To evaluate market opportunities, Request Sample

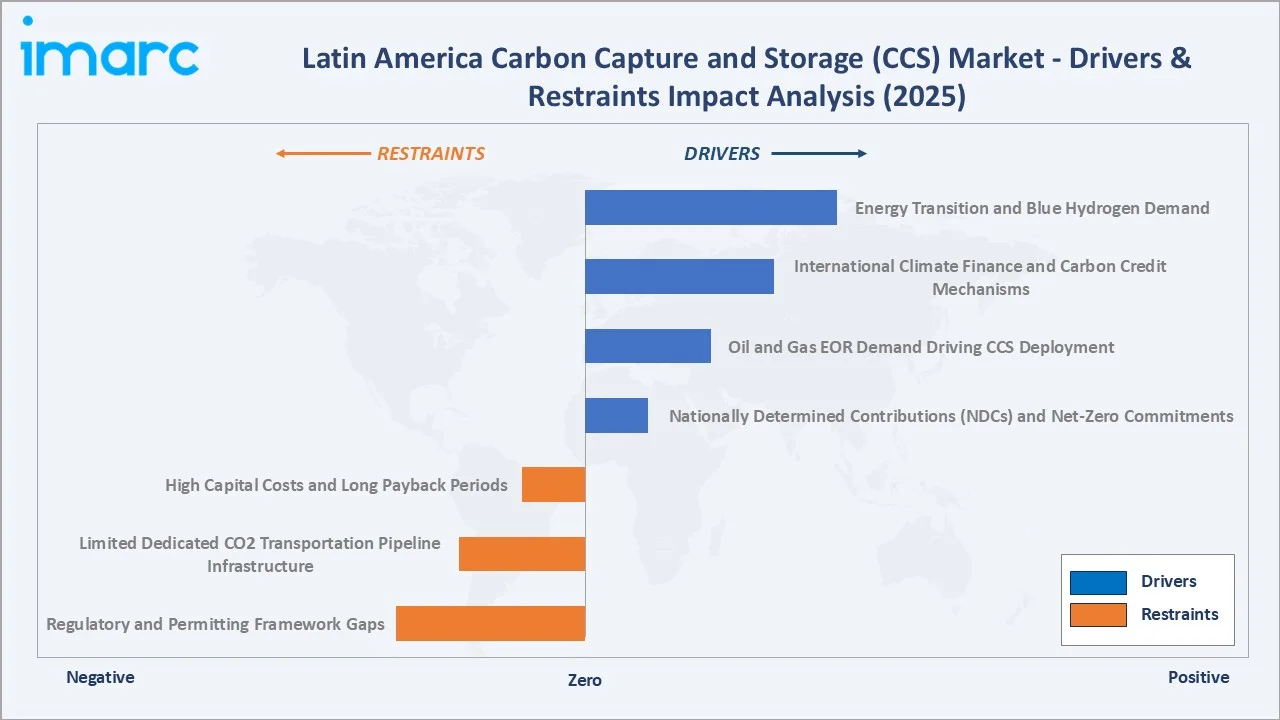

Market Drivers

- Nationally Determined Contributions (NDCs) and Net-Zero Commitments: All major Latin American economies have submitted updated NDCs under the Paris Agreement, committing to significant GHG emission reductions by 2030 and net-zero targets by 2050. Brazil’s NDC targets a 50% GHG reduction by 2030 versus 2005 levels; Colombia, Chile, and Argentina have aligned CCS as an explicitly recognized mitigation technology.

- Oil and Gas EOR Demand Driving CCS Deployment: Brazil’s pre-salt offshore oil fields, which contain naturally occurring CO₂ concentrations of 8–15% in produced gas, require CO₂ separation and injection as an integral operational requirement. Petrobras’ Santos Basin operations already injected approximately 10.6 million tons of CO₂ injected in 2022, making Brazil the world’s largest EOR-CCS operator.

- International Climate Finance and Carbon Credit Mechanisms: The Article 6 carbon market mechanisms established under the Paris Agreement COP frameworks, the Inter-American Development Bank’s climate finance programs, and bilateral green financing agreements between Latin American governments and European institutions are making available billions of dollars in concessional finance for CCS projects.

- Energy Transition and Blue Hydrogen Demand: Chile’s updated 2026–2030 green hydrogen strategy focuses on output-based goals, including 100–200 kt/year of green hydrogen equivalent for domestic consumption by 2030. Brazil’s National Hydrogen Program (PNH2) supports blue hydrogen via pre-combustion CCS. Colombia’s energy transition plans include CCS-enabled blue ammonia for fertilizer export markets.

Market Restraints

- High Capital Costs and Long Payback Periods: Full-chain CCS projects require capital investment in the range of USD 50–200 Million per million tons per annum (MTPA) of CO₂ capacity, with payback periods of 15–25 years depending on revenue from EOR, carbon credits, or government subsidy. Latin America’s higher-cost-of-capital environment creates significant financing challenges for CCS projects without concessional finance, sovereign guarantees, or EOR revenue support.

- Limited Dedicated CO₂ Transportation Pipeline Infrastructure: Apart from Brazil’s Santos Basin, Latin America lacks the onshore CO₂ pipeline grid required to connect distributed industrial emission sources to geological storage sites. Building dedicated CO₂ transportation infrastructure requires regulatory frameworks, right-of-way agreements, and capital investment that are in early stages across most of the region, limiting the scalability of CCS beyond oil-field-integrated applications.

- Regulatory and Permitting Framework Gaps: Comprehensive CCS-specific legal frameworks governing CO₂ storage site licensing, long-term liability allocation, ownership transfer protocols, and measurement, reporting, and verification (MRV) requirements do not yet exist in most Latin American jurisdictions.

Market Opportunities

- BECCS and Negative Emissions from Ethanol and Sugarcane Processing: Brazil’s sugarcane ethanol sector offers a unique and globally significant opportunity for bioenergy with carbon capture and storage (BECCS). The fermentation of sugarcane produces a near-pure CO₂ stream at low capture cost, and geological storage sites are available within pipeline range of several major sugar-ethanol production clusters in São Paulo and Minas Gerais states.

- Regional Carbon Storage Hub Development: The geological diversity of Latin America’s sedimentary basins provides substantial potential for dedicated regional CO₂ storage hubs serving multiple industrial emitters across national borders. The development of shared CO₂ storage infrastructure could significantly reduce per-ton storage costs and enable CCS deployment in countries without domestic storage geology.

Market Challenges

- CO₂ Storage Site Characterization and Permitting Timelines: Identifying, characterizing, and permitting suitable geological CO₂ storage sites requires 5–10 years of subsurface data acquisition, modelling, regulatory review, and community consultation, creating long lead times that constrain the pace at which new storage capacity can be brought online.

- Public Acceptance and Social License: CCS projects in Latin America must navigate social license challenges, including community concerns about CO₂ leakage risk, land rights for pipeline routing and storage site surface access, and the perception that CCS extends the life of fossil fuel industries rather than driving genuine decarbonization.

Emerging Market Trends

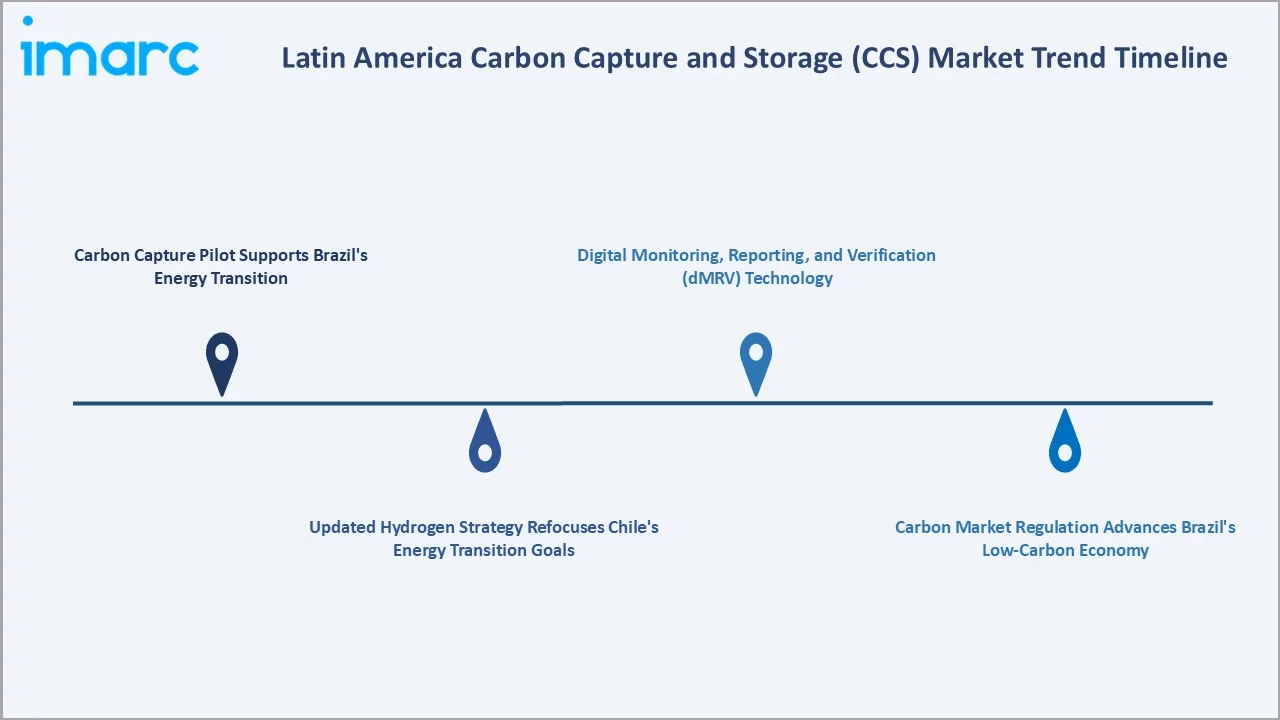

1. Carbon Capture Pilot Supports Brazil’s Energy Transition

In September 2025, Petrobras received approval for the São Tomé CCS Pilot Project in Macaé, Rio de Janeiro, Brazil’s first dedicated carbon capture and storage project designed to capture, transport, and permanently store CO₂ in deep geological formations. The pilot is expected to start in 2028, capturing up to 100,000 tonnes of CO₂ annually for three years, while helping Brazil test CCS technologies, monitoring systems, and regulatory standards for future commercial-scale carbon management projects.

2. Updated Hydrogen Strategy Refocuses Chile’s Energy Transition Goals

Chile’s updated 2026–2030 green hydrogen strategy shifts from the earlier 25 GW electrolyzer capacity target by 2030 toward output-based goals, targeting 100–200 kt/year of green hydrogen equivalent for domestic use by 2030, 300–700 kt/year for exports by 2035, and 2.0–3.5 million tons/year by 2050. It also revises cost expectations to below USD 4/kg by 2030 and under USD 2/kg by 2045, while highlighting over USD 5 billion in hydrogen investments and 5 GW of electrolysis capacity in projects under development or assessment.

3. Carbon Market Regulation Advances Brazil’s Low-Carbon Economy

Brazil is advancing its regulated carbon market through Law No. 15,042/2024, which established the Brazilian Emissions Trading System (SBCE) and created a framework for emissions to be traded as financial assets. Full market operation is projected from 2030, opening opportunities in renewable energy, forestry, sustainable land use, and low-carbon technologies.

4. Digital Monitoring, Reporting, and Verification (dMRV) Technology

Advanced satellite-based CO₂ plume monitoring, IoT-enabled subsurface pressure and saturation sensing, and AI-powered reservoir management systems are transforming the monitoring, reporting, and verification (MRV) requirements for CCS projects. SLB Limited’s DELFI cognitive E&P environment is being adapted for CO₂ storage monitoring applications in Brazil and Mexico, improving the accuracy and frequency of storage verification data required for carbon credit certification.

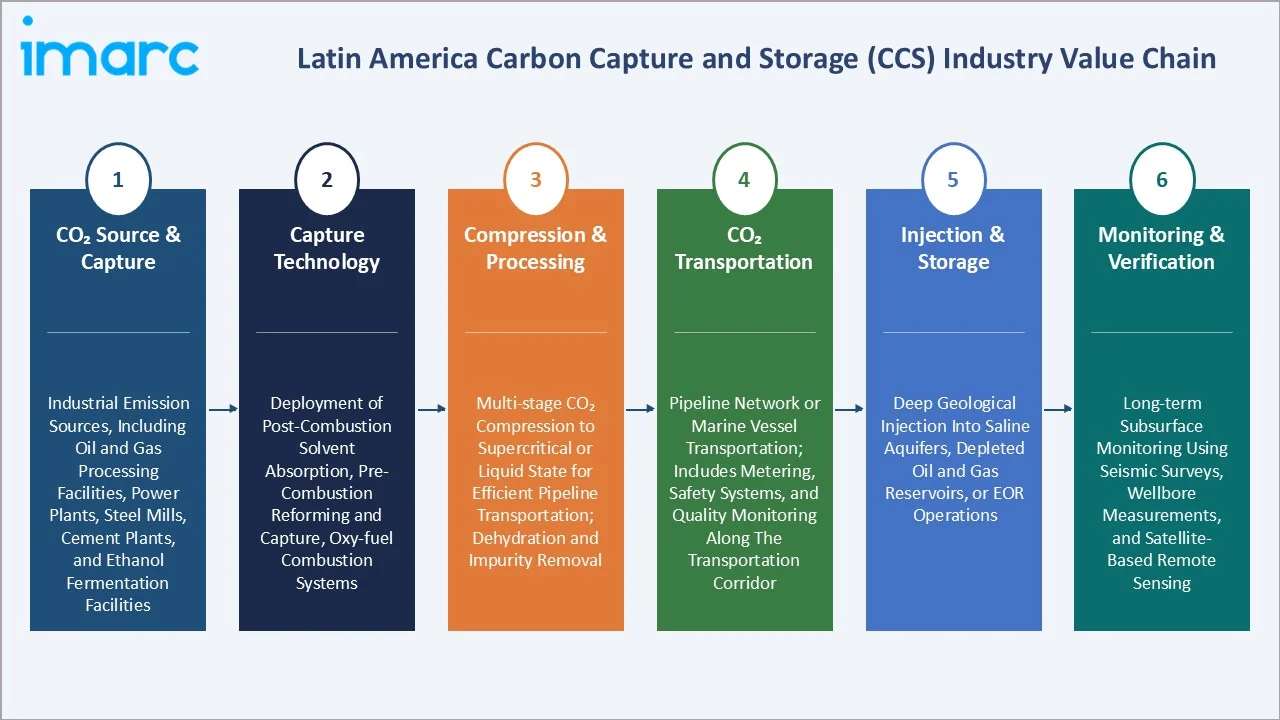

Industry Value Chain Analysis

The value chain spans six interconnected stages from CO₂ source identification through final monitored storage, each requiring specialized engineering, regulatory compliance, and operational capabilities. The chain is distinguished by the dominance of the oil and gas sector in both the capture (EOR) and storage stages.

|

Stage |

Description |

|

CO₂ Source & Capture |

Industrial emission sources, including oil and gas processing facilities, power plants, steel mills, cement plants, and ethanol fermentation facilities |

|

Capture Technology |

Deployment of post-combustion solvent absorption, pre-combustion reforming and capture, oxy-fuel combustion systems |

|

Compression & Processing |

Multi-stage CO₂ compression to supercritical or liquid state for efficient pipeline transportation; dehydration and impurity removal |

|

CO₂ Transportation |

Pipeline network or marine vessel transportation; includes metering, safety systems, and quality monitoring along the transportation corridor |

|

Injection & Storage |

Deep geological injection into saline aquifers, depleted oil and gas reservoirs, or EOR operations |

|

Monitoring & Verification |

Long-term subsurface monitoring using seismic surveys, wellbore measurements, and satellite-based remote sensing |

Technology Landscape in the Latin America CCS Industry

Solvent Absorption and Advanced Post-Combustion Capture

Post-combustion capture using amine-based chemical absorbents remains the dominant CCS technology in Latin America, accounting for 48.7% of the market in 2025. The regenerable solvent process, which absorbs CO₂ from flue gas using aqueous amine solutions and releases it under heat for compression and storage, is proven at an industrial scale with reference plants operating in North America, Europe, and Asia.

Pre-Combustion Capture and Hydrogen Production Integration

Pre-combustion capture, which converts fossil fuel or biomass feedstocks to hydrogen and CO₂ through gasification or steam methane reforming (SMR) before combustion, is the fastest-growing CCS technology in Latin America at approximately 9.1% CAGR. The technology is uniquely positioned to serve the emerging blue hydrogen economy, as the pre-combustion CO₂ stream is produced at higher pressure and concentration than post-combustion flue gas, reducing capture cost to USD 25–45/tCO₂.

Digital Reservoir Management and AI-Driven Storage Optimization

Advanced reservoir simulation, machine learning-based injection optimization, and real-time subsurface monitoring are transforming the storage and MRV stages of the CCS value chain. SLB Limited’s DELFI platform is enabling higher CO₂ injection rates, improved plume management, and more cost-effective long-term storage verification.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Capture |

52.6% |

2025 |

|

Technology |

Post-combustion Capture |

48.7% |

2025 |

|

End Use Industry |

🔒 |

🔒 |

2025 |

|

Country |

Brazil |

41.2% |

2025 |

By Service

Capture dominates with a 52.6% share in 2025. The capture service segment encompasses the design, engineering, procurement, construction, and operation of CO₂ capture systems at industrial point sources. In Latin America, the oil and gas sector drives capture service demand through Petrobras’ Santos Basin EOR operations, PEMEX’s processing facilities, and Ecopetrol’s refining complex.

To access detailed market analysis, Request Sample

Transportation at 24.3% reflects the cost and complexity of building and operating CO₂ pipeline networks connecting distributed industrial emitters to centralized storage hubs. Storage at 23.1% encompasses the geological injection and long-term containment of CO₂ in saline aquifers, depleted hydrocarbon reservoirs, and EOR-coupled storage operations, requiring specialized subsurface engineering, well services, and MRV capabilities.

By Technology

Post-combustion capture dominates with a 48.7% share in 2025. This technology’s market leadership reflects its retrofittability onto existing industrial assets, its proven track record at commercial scale, and the large installed base of fossil-fuel-based power generation and industrial facilities across Latin America that represent the primary near-term CCS deployment opportunity.

Pre-combustion capture at 29.4% serves the natural gas reforming, gasification, and emerging blue hydrogen production sectors. Oxy-fuel combustion capture at 21.9% is advancing in Brazil’s biomass and ethanol sector, where the combination of renewable carbon in sugarcane ethanol and geological CO₂ storage creates the potential for genuinely negative carbon emissions.

Regional Market Insights

Brazil’s market leadership (41.2%, 2025) is anchored by Petrobras’ world-scale CO₂ EOR operations in the Santos Basin pre-salt fields, where CO₂ management is an integral operational requirement rather than an add-on climate initiative. Brazil’s natural geological advantages, combined with the country’s strong NDC commitments, create the most supportive CCS investment environment in Latin America.

-market-rd-update-prachi-8.webp)

Mexico at 19.3% represents the second-largest CCS market, driven by PEMEX’s developing CCS program and the significant influence of US CCS policy and the Inflation Reduction Act financing mechanisms on cross-border energy transition investment.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Brazil |

41.2% |

World-leading Petrobras EOR-CCS operations; large Santos Basin storage capacity; SBCE carbon market launch; BECCS potential from sugarcane ethanol sector |

|

Mexico |

19.3% |

PEMEX CCS roadmap development; proximity to US IRA climate finance; natural gas processing facilities as capture sources; geological storage potential in the Gulf of Mexico basins |

|

Argentina |

10.1% |

Vaca Muerta shale gas development creating CCS-linked blue hydrogen potential; Cuyana Basin saline aquifer storage; YPF CCS feasibility studies |

|

Colombia |

9.2% |

Ecopetrol CCS-EOR in Llanos Basin; national hydrogen roadmap; inter-Andean saline aquifer storage studies; advancing CCS regulatory framework |

|

Chile |

7.4% |

National Hydrogen Strategy targeting blue hydrogen export; Magallanes Basin gas and storage potential; strong EU climate alignment |

|

Peru |

6.0% |

Offshore natural gas processing CCS potential; Pluspetrol and REPSOL EOR studies; nascent but growing regulatory engagement |

|

Others |

6.8% |

Ecuador, Bolivia, Uruguay, and the Central American markets with early-stage CCS policy development and a limited but growing project pipeline |

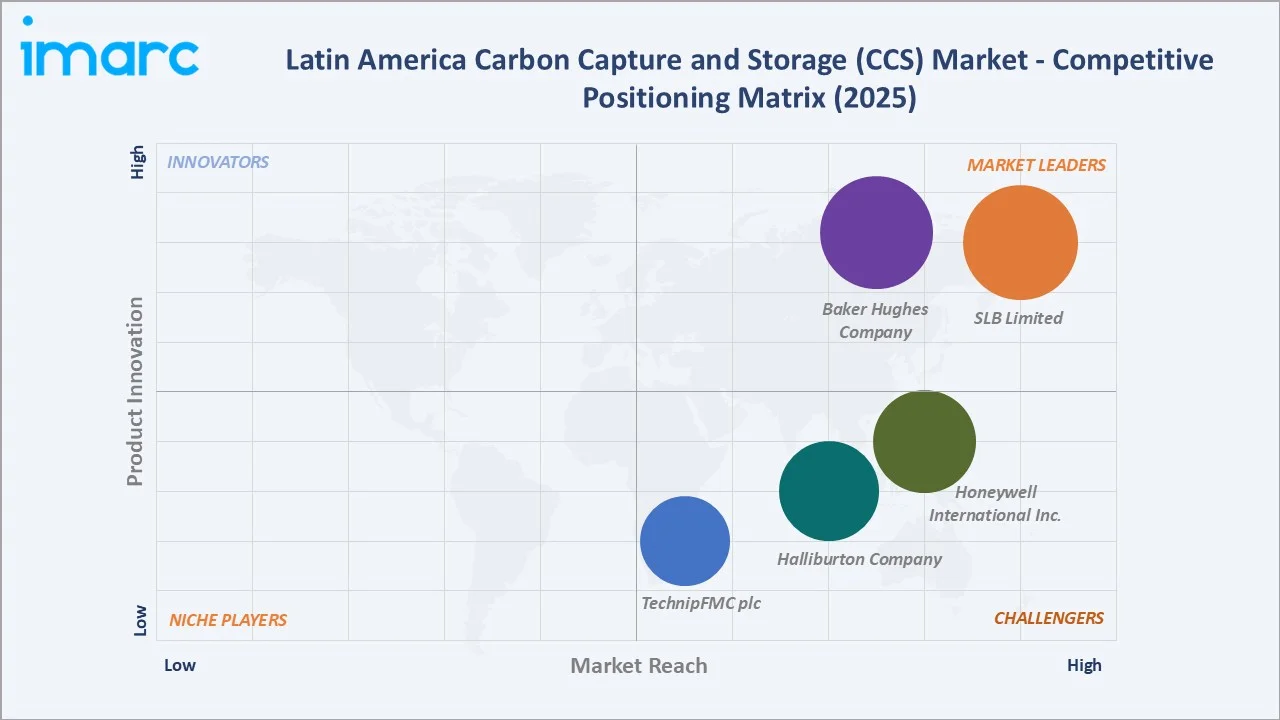

Competitive Landscape

Latin America’s CCS market is moderately concentrated among a small number of large international oilfield services and engineering companies. The competitive landscape is shaped by the dominance of national oil companies as both the primary CCS asset owners and operators, creating a project structure where international technology and services companies compete for engineering, procurement, and construction (EPC) and long-term O&M contracts.

|

Company Name |

Key Service Offering |

Market Position |

Core Strength |

|

SLB Limited |

Carbon capture, utilization, & sequestration, carbon storage screening and ranking solution, carbon storage evaluation solution, among others |

Market Leader |

Broadest full-chain CCS technology and services portfolio; DELFI digital platform for storage management; deepest Latin America subsurface data and expertise |

|

Baker Hughes Company |

CCUS project design and advisory services, carbon capture, carbon transportation, carbon utilization, carbon storage, and digital solutions for CCUS projects |

Market Leader |

Leading CO₂ compression technology; strong Brazil offshore track record |

|

Honeywell International Inc. |

Honeywell UOP Advanced Solvent Carbon Capture (ASCC) technology, post-combustion capture systems, pre-combustion reforming technology, digital MRV solutions |

Strong Challenger |

UOP process technology leadership for capture and hydrogen production; advanced digital MRV and emissions monitoring capabilities; strong EPC partner network |

|

Halliburton Company |

CO2 site selection and planning, understand CO2 properties and characteristics, design & construct wells for carbon sequestration, MMV for long-term CO₂ storage security |

Strong Challenger |

Deep well services expertise critical for CO₂ injection well construction; iEnergy digital platform; broad Latin America oilfield services footprint supporting CCS expansion |

|

TechnipFMC plc |

Integrated Carbon Transportation and Storage

|

Challenger |

Offshore CCS engineering expertise aligned with Petrobras Santos Basin needs; subsea technology for deepwater CO₂ injection; strong Latin America EPC project execution track record |

Entry barriers are high due to the technical complexity, regulatory knowledge, and subsurface data requirements of CCS project development.

Key Company Profiles

SLB Limited

SLB Limited is one of the world’s largest oilfield services companies and the leading provider of CCS technology and services in Latin America. SLB’s CCS capabilities span the full value chain from subsurface characterization and CO₂ capture technology to digital storage management and MRV solutions.

- Service Portfolio: Carbon capture, utilization, & sequestration, carbon storage screening and ranking solution, carbon storage evaluation solution, well integrity assessment for carbon storage, Optiq, facility planner on Delfi, symmetry process simulation software, Olga dynamic multiphase flow simulator.

- Recent Developments: In June 2025, SLB launched Sequestri carbon storage solutions, a full value-chain portfolio of technologies and services designed to make carbon storage projects safer, more efficient, and more economical.

- Strategic Focus: Full-chain CCS digital integration through DELFI; storage site characterization and certification services; carbon management consulting for industrial decarbonization clients.

Baker Hughes Company

Baker Hughes Company is one of the leading energy technology companies providing CCS-related compression, turbomachinery, well construction, and digital monitoring services across Latin America.

- Service Portfolio: CCUS project design and advisory services, carbon capture, carbon transportation, carbon utilization, carbon storage, and digital solutions for CCUS projects.

- Recent Developments: In April 2026, Baker Hughes Company reported Q1 2026 revenue of USD 6.59 billion, up 2% year-on-year, with orders rising 26% YoY to USD 8.16 billion. Adjusted EBITDA increased 12% YoY to USD 1.16 billion, supported by strong industrial & energy technology demand.

- Strategic Focus: CO₂ compression and turbomachinery for CCS; digital compressor monitoring and control for CCS operations.

Market Concentration Analysis

Latin America’s CCS market exhibits high concentration in the technology and services layer, where a small number of global oilfield services and engineering companies command dominant positions in subsurface characterization, capture technology, compression, and MRV services. At the project ownership level, national oil companies control the majority of CCS assets and create a concentrated buyer market that shapes competitive dynamics for technology and service providers.

Market fragmentation is increasing in the project development layer as independent CCS project developers, utilities, industrial companies, and international oil companies enter the region with CCS project proposals. The anticipated growth of BECCS in Brazil’s ethanol sector is expected to create a more diverse project ownership landscape, with agricultural cooperatives, ethanol producers, and infrastructure funds participating alongside traditional oil and gas operators.

Investment & Growth Opportunities

Fastest Growing Segments

Pre-combustion capture (~9.1% CAGR), oxy-fuel combustion capture (~8.8% CAGR), and storage (~8.2% CAGR) represent the primary high-growth investment vectors through 2034. Brazil’s SBCE carbon market, once it reaches a carbon price of USD 30–40/tCO₂, will materially improve project economics across all CCS technologies and is expected to trigger a step-change increase in CCS investment decisions in 2027–2030.

Emerging Market Expansion

Chile’s blue hydrogen CCS market is expected to scale from negligible to approximately USD 30–40 Million by 2030 as the Magallanes Basin projects advance through FEED and FID stages. Colombia’s Llanos Basin EOR-CCS opportunity is estimated at 0.5–1.0 MTPA of CO₂ by 2030 based on Ecopetrol’s reservoir studies. Mexico’s Gulf of Mexico basin offers geological storage for 1–2 GTPA of CO₂, providing capacity to serve not only PEMEX’s own emissions but potentially US industrial emitters seeking cross-border storage under bilateral climate agreements.

Venture and Institutional Investment Trends

- The Inter-American Development Bank (IDB) and IDB Invest committed USD 500 Million for energy transition projects in Latin America in 2025–2026, with CCS identified as an eligible technology for concessional financing.

- BNDES announced an additional R$2.2 billion to support renewable energy investments, including a new BNDES Finame Renewable Energy line with R$2 billion for equipment financing and R$228 million for the Climate Fund.

Future Market Outlook (2026-2034)

Latin America’s CCS market is positioned for gradual growth through 2034, driven by the maturation of Brazil’s EOR-CCS infrastructure, the scaling of blue hydrogen production projects in Chile and Argentina, the launch of Brazil’s SBCE carbon market, and the progressive deployment of BECCS in the sugarcane ethanol sector.

The technology mix will shift meaningfully by 2034, with pre-combustion capture’s share growing from 29.4% to approximately 35–38% as blue hydrogen projects reach commercial scale, and oxy-fuel/BECCS growing from 21.9% to approximately 25–28% as Brazil’s sugarcane-to-BECCS infrastructure scales.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 65 industry participants in 2024–2025, including CCS project managers at Petrobras, PEMEX, Ecopetrol, and YPF; technology and service executives; government officials from Brazil’s Ministry of Mines and Energy, Mexico’s SENER, Colombia’s Ministry of Energy; and climate finance specialists at the IDB, World Bank, and BNDES.

Secondary Research

Secondary research encompassed company annual reports and sustainability disclosures; Brazil’s CNPE CCS regulatory documents; IETA and ICAP carbon market analysis; IEA Carbon Capture database; Global CCS Institute project tracker; ABIHPEC, and national energy ministry data; and academic literature on Latin America’s geological CO₂ storage potential.

Forecasting Models

Market size estimations were derived using bottom-up project-level revenue modelling combined with top-down macroeconomic carbon price and NDC compliance scenario analysis. A CAGR of 7.80% reflects the central scenario validated against IEA Net Zero Scenario Latin America projections, BNDES investment pipeline data, and IMARC’s primary expert panel review.

Latin America Carbon Capture and Storage (CCS) Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Capture, Transportation, Storage |

| Technologies Covered | Post-combustion Capture, Pre-combustion Capture, Oxy-fuel Combustion Capture |

| End Use Industries Covered | Oil and Gas, Coal and Biomass Power Plant, Iron and Steel, Chemical, Others |

| Countries Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | SLB Limited, Baker Hughes Company, Honeywell International Inc., Halliburton Company, TechnipFMC plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Latin America carbon capture and storage (CCS) market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Latin America carbon capture and storage (CCS) market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Latin America carbon capture and storage (CCS) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Latin America Carbon Capture and Storage (CCS) Market Report

The Latin America CCS market reached USD 192.5 Million in 2025 and is forecast to reach USD 386.0 Million by 2034.

The market is expected to grow at a CAGR of 7.80% during 2026-2034, driven by NDC climate commitments, EOR-CCS expansion, blue hydrogen development, and BECCS deployment in Brazil’s sugarcane sector.

Brazil leads with a 41.2% share in 2025, anchored by Petrobras’ world-scale Santos Basin CO₂ EOR operations, BECCS potential from sugarcane ethanol, and the SBCE carbon market launch.

Capture dominates with a 52.6% share in 2025, reflecting the capital intensity of CO₂ capture systems at oil and gas, power generation, and industrial emission sources.

Post-combustion capture leads with a 48.7% share in 2025, driven by its retrofittability onto existing industrial assets and proven commercial track record.

Some of the key players in the market include SLB Limited, Baker Hughes Company, Honeywell International Inc., Halliburton Company, and TechnipFMC plc.

Pre-combustion capture is growing at approximately 9.1% CAGR because it is the enabling technology for blue hydrogen production, which is central to Chile’s, Brazil’s, and Argentina’s hydrogen export strategies, and produces a high-pressure, high-concentration CO₂ stream that significantly reduces capture costs compared to post-combustion systems.

Key challenges include high capital costs and long payback periods, limited CO₂ pipeline infrastructure outside Brazil, regulatory framework gaps for CO₂ storage permitting and long-term liability, CO₂ storage site characterization timelines, and social license requirements for pipeline routing and storage site access.

BECCS in Brazil’s sugarcane ethanol sector, blue hydrogen with pre-combustion CCS in Chile and Argentina, CO₂ storage hub infrastructure development, Colombia and Mexico EOR-CCS, and digital MRV services represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)