Latin America Pet Food Market Size, Share, Trends and Forecast by Pet Type, Product Type, Pricing Type, Ingredient Type, Distribution Channel, and Country 2026-2034

Latin America Pet Food Market Size, Share, Trends & Forecast (2026-2034)

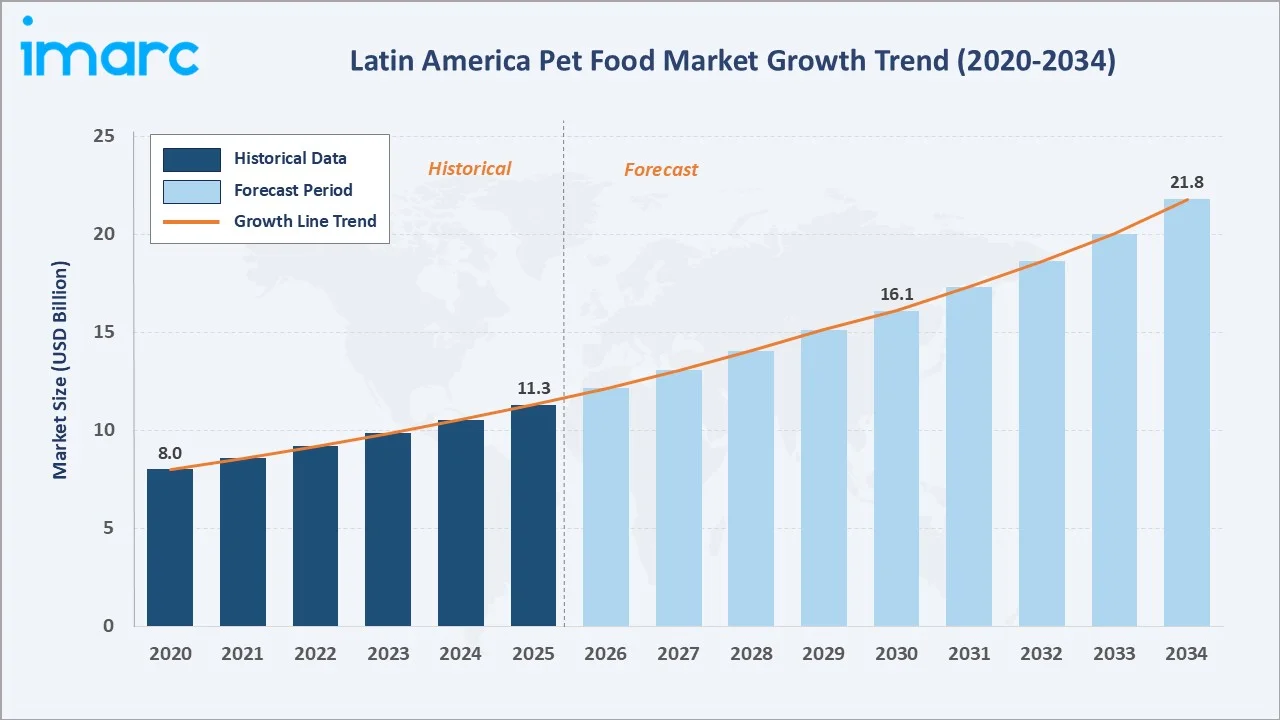

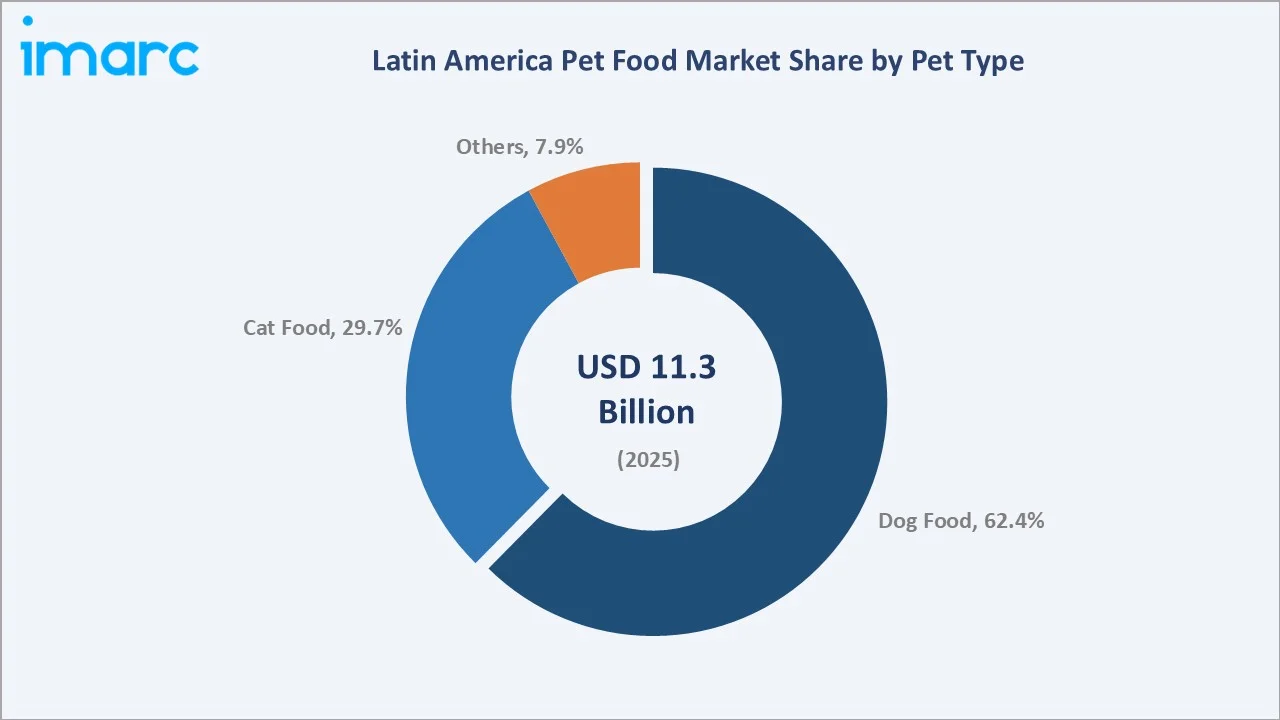

The Latin America pet food market reached USD 11.3 Billion in 2025 and is projected to reach USD 21.8 Billion by 2034, at a CAGR of 7.32% during 2026-2034. Rising pet humanization, growing awareness of pet nutrition, and rapid urbanization fuel the expansion. Dog food dominates with a 62.4% share in 2025, while Brazil leads regionally at 38.2%. Mass products retain the highest demand, though premium adoption is accelerating across key markets.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.3 Billion |

|

Forecast Market Size (2034) |

USD 21.8 Billion |

|

CAGR (2026-2034) |

7.32% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Brazil (38.2%) |

|

Fastest Growing Region |

Colombia & Peru |

|

Dominant Pet Type |

Dog Food (62.4%) |

|

Dominant Pricing Type |

Mass Products (64.8%) |

The chart illustrates the growth trajectory of the Latin American pet food market from 2020 to 2034, highlighting historical trends and future projections supported by increasing pet ownership, premiumization trends, and rising investments in pet nutrition and product innovation.

To get more information on this market, Request Sample

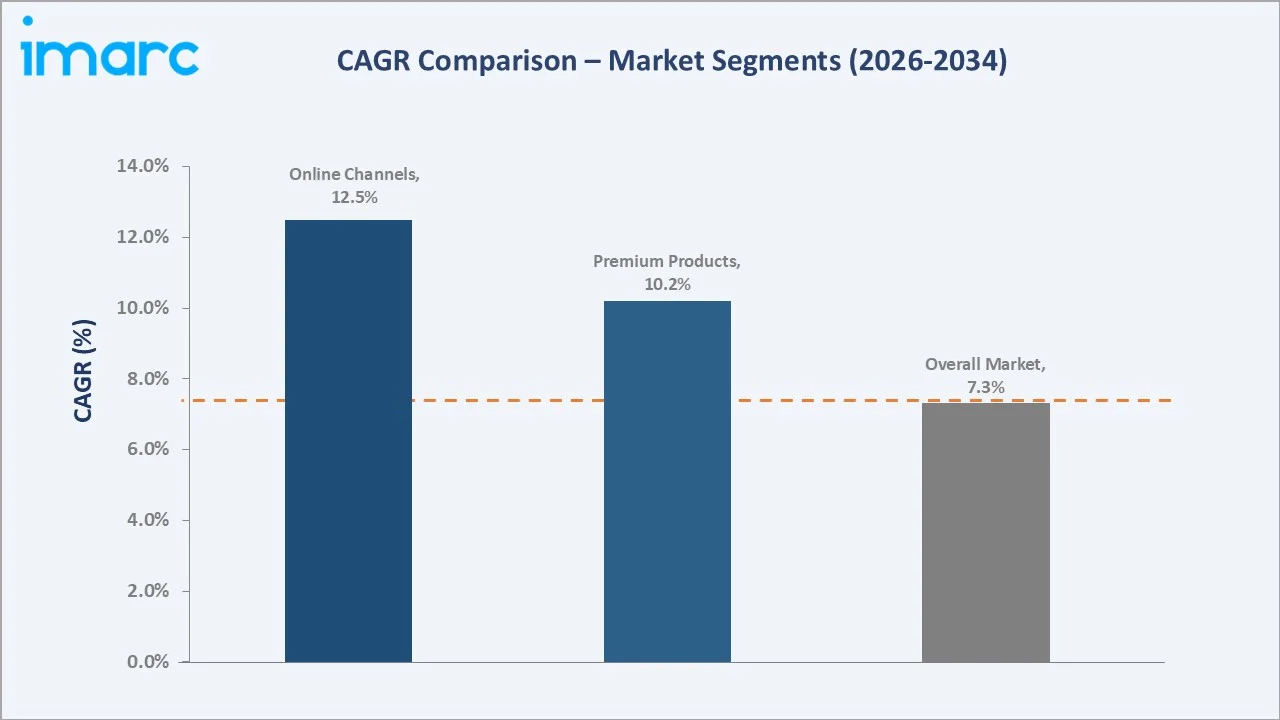

The chart reflects a healthy market CAGR of around 7.3% for the Latin America pet food market, with the highest growth observed in online channels (12.5%) and premium products (10.2%), indicating a strong shift toward digital sales and premium pet nutrition.

Executive Summary

The Latin America pet food market has grown from USD 8.0 Billion in 2020 to USD 11.3 Billion in 2025, representing robust compound growth driven by shifting consumer attitudes toward companion animals. Pet owners increasingly regard their animals as family members - a cultural shift commonly known as "pet humanization" - which directly elevates spending on premium nutrition, functional ingredients, and specialized diets.

Dog food remains the dominant category, accounting for 62.4% of total market revenue in 2025. Cat food follows at 29.7%. Mass products hold a 64.8% share, reflecting broad affordability demands. However, the premium segment at 35.2% is growing at a faster pace, driven by an expanding middle class and growing awareness of pet health and wellness across Brazil, Mexico, and Chile.

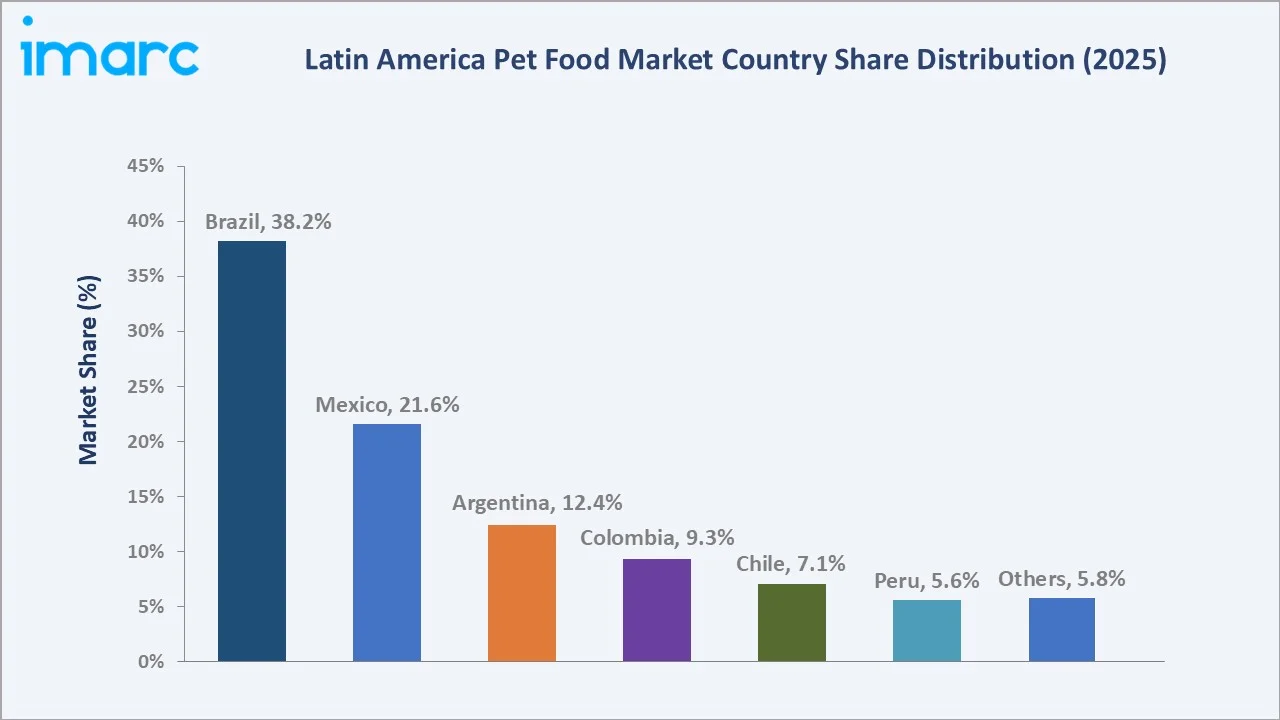

Brazil anchors the regional landscape with a 38.2% share, followed by Mexico at 21.6%. By 2034, the market is projected to reach USD 21.8 Billion as functional ingredients, e-commerce expansion, and regulatory modernization reshape demand across all sub-regions.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Pet Type) |

Dog Food – 62.4% of revenue in 2025 |

|

Leading Region |

Brazil – USD 4.3B; 38.2% regional share |

|

Fastest Growing Region |

Colombia & Peru – double-digit growth |

|

Top Pricing Type |

Mass Products – 64.8%; Premium at 35.2% |

|

Forecast Market Size |

USD 21.8 Billion by 2034 at 7.32% CAGR |

|

Key Growth Driver |

Pet humanization & functional ingredients |

Key Analytical Observations Supporting the Above Data:

- Dog food commands a 62.4% share in 2025, supported by High dog ownership across Brazil and Mexico supports market growth, with dogs being the most preferred pets—owned by about 52% of households in Brazil and nearly 80% of pet owners in Mexico.

- Premium pet food is growing faster than mass products, with brands like Purina Pro Plan and Hill's Science Diet reporting double-digit revenue gains in Brazil.

- Brazil remains the market anchor, contributing USD 4.3 Billion in 2025. Its pet population exceeds 140 million animals, the third largest globally.

- E-commerce is accelerating pet food distribution in Latin America, with online channels emerging as the fastest-growing segment, supported by increasing digital adoption and expanding access to premium and specialized products.

- Functional ingredients such as omega-3, probiotics, and glucosamine are gaining traction in pet food, expanding beyond premium products as demand for health-focused nutrition rises, gradually narrowing the gap between mass and premium offerings.

- Colombia and Peru are emerging pet food markets in Latin America, supported by rising urbanization and increasing pet adoption, which is gradually expanding demand for packaged pet food through modern retail and online channels.

Latin America Pet Food Market Overview

The Latin America pet food market includes manufacturing, distribution, and retail of nutritionally complete pet food. It spans sourcing, processing, packaging, and multi-channel sales. Growth is driven by rising incomes, urbanization, and expanding middle-class populations in Brazil, Mexico, and Colombia. The market reached USD 8.0 Billion in 2020 and has shown steady growth through 2025.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Pet Humanization: Pet humanization is rising in Latin America, driving demand for premium nutrition. Brazil’s pet industry recorded strong growth, supported by premiumization trends.

- Expanding Pet Population: Latin America has a large and growing pet population, with Brazil alone hosting over 60 million dogs and 27 million cats, supporting strong demand for pet food products.

- Rising Disposable Income: Rising incomes and middle-class expansion in Mexico and Colombia are supporting higher pet care spending, encouraging a shift toward premium and specialized pet food products.

- E-Commerce Growth: E-commerce is expanding in Latin America’s pet food market, improving accessibility and supporting growth of premium products through online and modern retail channels.

Market Restraints

- Economic Volatility: Economic instability in Argentina and similar markets affects pet food demand, as high inflation and income pressures shift consumers toward lower-cost products, limiting premium segment growth.

- Informal Market Competition: A significant share of pet owners in Latin America still rely on homemade or informal feeding practices, limiting penetration of commercial pet food, especially in price-sensitive and rural markets.

- Raw Material Price Inflation: Rising costs of key ingredients such as meat and grains have increased pet food production expenses, pressured margins and contributing to higher retail prices across Latin America.

Market Opportunities

- Functional and Veterinary Nutrition: Functional and veterinary pet nutrition is growing in Latin America, driven by demand for health-focused products supporting digestion, joint care, and weight management, especially within premium and specialized pet food segments.

- Sustainable Formulations: Sustainable pet food trends are gaining traction, with increasing adoption of eco-friendly packaging and alternative proteins, supported by rising consumer awareness and environmental concerns across Latin America.

- Rural and Secondary City Penetration: Significant growth opportunities exist in rural and secondary cities, where lower penetration of commercial pet food and rising pet ownership are expected to drive future expansion of formal distribution channels.

Market Challenges

- Regulatory Heterogeneity: Regulatory frameworks vary across Latin American countries, with differing standards for labeling, ingredients, and imports, increasing compliance complexity and slowing cross-border expansion for pet food manufacturers.

- Cold Chain Limitations: Limited cold-chain infrastructure in several Latin American markets restricts distribution of wet and fresh pet food, particularly in smaller cities, constraining growth of premium and perishable product segments.

- Consumer Education Gap: Limited awareness of pet nutrition in lower-income segments restricts adoption of premium pet food, with many consumers prioritizing affordability over nutritional benefits, slowing the shift toward specialized diets.

Emerging Market Trends

1. Premiumization Across Income Segments

Premium pet food demand is expanding across income groups in Latin America, supported by pet humanization and increasing spending on quality nutrition, with brands introducing affordable premium products to widen consumer access.

2. Functional Ingredient Innovation

Functional ingredients such as omega-3, prebiotics, and glucosamine are increasingly incorporated in pet food, driven by health-focused trends, with gradual adoption beyond premium products into broader formulations across Latin America.

3. Digital-First Consumer Engagement

E-commerce and subscription-based pet food models are growing in Latin America, improving convenience and customer retention, with digital platforms playing a critical role in expanding access to premium and specialized pet food products.

4. Sustainable and Clean-Label Products

Sustainability trends are gaining importance, with increasing demand for natural, clean-label, and minimally processed pet food products, as consumers seek transparency, environmentally friendly packaging, and healthier ingredient profiles in Latin America.

5. Veterinary and Prescription Diet Expansion

Veterinary and prescription pet food segments are expanding due to rising awareness of pet health and preventive care, driving demand for specialized diets targeting conditions such as obesity, digestive health, and chronic diseases.

Industry Value Chain Analysis

The Latin America pet food industry value chain runs from raw material and ingredient supply (grains, meat/poultry/fish meals, fats, vitamins, and functional additives, drawn heavily from Brazil and Argentina's large agricultural and protein sectors) through manufacturing and co-packing (dominated by multinationals like Mars, Nestlé Purina, and Colgate-Hill's alongside strong regional players such as Grupo Pilar, Total Alimentos, and BRF's Guabi), then into distribution and retail (specialty pet stores, vet clinics, hypermarkets like Walmart and Carrefour, and fast-growing e-commerce platforms including Petz, Cobasi, and Mercado Libre), and finally to end consumers, pet owners across Brazil, Mexico, Argentina, Colombia, and Chile, with humanization and premiumization trends steadily shifting demand toward super-premium, natural, and functional formats.

|

Stage |

Key Activities |

|

Raw Ingredients & Inputs |

Protein sourcing, grain procurement, vitamins & minerals sourcing |

|

Food Processing & Logistics |

Ingredient blending, preprocessing, storage, inbound logistics |

|

Pet Food Manufacturers & Brands |

Extrusion, canning, formulation, palatability testing, R&D |

|

Distribution & Retail Channels |

Wholesale distribution, cold chain logistics, retail supply (modern trade & specialty stores) |

|

Service Delivery & E-Commerce |

Online marketplaces, direct-to-consumer (DTC), subscription models, last-mile delivery |

|

End Consumers |

Consumption by pet owners (dogs, cats, others) |

Technology Landscape in the Latin America Pet Food Industry

Extrusion and Processing Technology

Extrusion remains the primary technology for dry pet food production globally, including Latin America, due to efficiency and scalability. Manufacturers are investing in advanced processing technologies to improve product quality, consistency, and operational efficiency.

Nutritional Science and Formulation Innovation

Pet food companies are increasingly using advanced formulation tools and data-driven approaches to develop targeted nutrition based on pet age, breed, and health needs, supporting innovation in personalized and functional pet food products.

Sustainable Packaging Technology

Sustainable packaging solutions, including recyclable and reduced-plastic materials, are gaining traction in Latin America, driven by environmental regulations and rising consumer demand for eco-friendly pet food packaging solutions.

Digital and E-Commerce Technology

Digital technologies, including e-commerce platforms, AI-driven recommendations, and subscription models, are transforming pet food retail by enhancing personalization, improving supply chain efficiency, and expanding access to premium products.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Pet Type | Dog Food | 62.4% |

2025 |

| Product Type | 🔒 | 🔒 |

2025 |

| Pricing Type | Mass Products | 64.8% |

2025 |

| Ingredient Type | 🔒 | 🔒 |

2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| Country | Brazil | 38.2% | 2025 |

Segmentation by Pet Type (2025)

Dog food leads the Latin America pet food market with a dominant 62.4% share in 2025. The region's large canine population - over 120 million dogs - sustains consistently high-volume demand. Product variety spans economy dry kibble through to premium grain-free formulations. Dog food growth is expected to remain robust through 2034 given strong demographic and cultural bonds.

To access detailed market analysis, Request Sample

Cat food holds 29.7% of the market in 2025 and is growing at a slightly faster rate than dog food, driven by increasing urban cat adoption. Others (fish, birds, small mammals) account for 7.9%, representing a niche but steadily growing specialty segment.

Segmentation by Pricing Type (2025)

Mass products account for 64.8% of the market in 2025, reflecting strong demand for affordable pet food across diverse income groups. Major players such as Mars, Incorporated and Mogiana Alimentos lead this segment. However, growth is slower than premium categories, as rising incomes in Brazil and Mexico support gradual consumer trade-up.

Premium products hold 35.2% in 2025 and are expanding faster than mass segments, supported by rising pet humanization and higher spending. Brands like Royal Canin, Hill's Science Diet, and Purina Pro Plan benefit, driven by demand for functional, breed-specific, and veterinarian-recommended nutrition.

Regional Market Insights

Brazil dominates the Latin America pet food landscape with 38.2% of regional revenues in 2025, supported by the continent's largest companion animal population and most mature modern retail infrastructure. Mexico follows with 21.6%, benefiting from robust economic growth and urbanization. Together, Brazil and Mexico account for nearly 60% of regional pet food revenue, while Argentina, Colombia, Chile, and Peru represent a growing collective share with significant expansion potential.

|

Country |

Share (2025) |

Growth Drivers |

Regulatory Impact |

Key Companies |

|

Brazil |

38.2% |

Largest pet population; strong retail infrastructure |

MAPA food safety regulations |

Mars, Nestlé, Mogiana, Total Alimentos |

|

Mexico |

21.6% |

Urban pet adoption surge; rising middle-class spending |

COFEPRIS product registration requirements |

Mars, Nestlé, Colgate-Palmolive |

|

Argentina |

12.4% |

High humanization index; treats demand rising |

SENASA animal feed regulations |

Royal Canin, Mars, local producers |

|

Colombia |

9.3% |

E-commerce growth; growing specialty retail chains |

ICA oversight of pet nutrition claims |

Nestlé, Mars, Colombina |

|

Chile |

7.1% |

Premium segment penetration; health-focused owners |

SAG import/label compliance |

Royal Canin, Nestlé, Hills |

|

Peru |

5.6% |

Rising urbanization; expanding modern trade |

SENASA nutrition labeling rules |

Mars, Nestlé, regional brands |

|

Others |

5.8% |

Ecuador, Bolivia, Uruguay - nascent markets with high potential |

Varies by country |

Mostly imports / regional distributors |

Argentina (12.4%) faces economic instability and inflation, but demand remains resilient as pet care is prioritized, with local players competing effectively. Colombia (9.3%) is a high-growth market driven by rising incomes, urbanization, and increasing adoption of branded pet food. Chile (7.1%) is relatively mature, characterized by high per-capita spending and strong demand for premium, natural, and specialized pet nutrition products. Peru (5.6%), Others account for 5.8%

Competitive Landscape

The Latin America pet food market shows moderate concentration in premium segments, led by Mars Incorporated, Nestlé, and Colgate-Palmolive, driven by strong brands and premiumization trends. Regional companies like Total Alimentos dominate the mass segment, particularly in Brazil, the region’s largest and most price-sensitive market.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

Mars, Incorporated |

Pedigree, Whiskas, Royal Canin, Optimum |

Market Leader |

Mass & premium; widest distribution |

|

Nestlé |

Purina ONE, Pro Plan, Dog Chow |

Market Leader |

R&D; vet channel; premium range |

|

Colgate-Palmolive Company |

Hill’s Pet Nutrition |

Premium Specialist |

Vet endorsement; clinical nutrition |

|

BRF Global |

Gran Plus, Guabi Natural |

Regional Leader (BR) |

Cost efficiency; mass market |

|

Affinity |

Advance, Ultima |

Emerging |

Specialty & functional diets |

Key Company Profiles

Mars Incorporated

Mars Petcare is a leading global pet food company and a dominant player in Latin America, offering a broad portfolio across mass and premium segments, supported by strong distribution, veterinary partnerships, and continuous product innovation across key regional markets.

- Product Portfolio: Mars Petcare offers a wide portfolio including Pedigree and Whiskas (mass segment), and Royal Canin (premium veterinary nutrition), supported by veterinary services, diagnostics, and pet health platforms through its global petcare ecosystem.

- Recent Developments: Mars Petcare strengthened its footprint in Brazil through a ~US$5 million (R$30 million) investment in a new distribution center in Extrema, Minas Gerais, aimed at expanding supply chain efficiency and increasing reach for brands like Pedigree and Whiskas across key regions. The facility is expected to handle over 70,000 tons annually, supporting growing demand driven by rising pet ownership and premiumization trends in Brazil’s expanding pet food market.

- Strategic Focus: Mars Petcare focuses on strengthening its leadership in mass pet food while accelerating premiumization through Royal Canin and expanding its integrated pet health ecosystem across veterinary, nutrition, and digital platforms in Latin America.

Nestle

Nestlé Purina is a leading pet food company and a key player in Latin America, supported by strong research capabilities, a wide brand portfolio across price tiers, and deep penetration in veterinary and retail channels across major regional markets.

- Product Portfolio: Nestlé Purina offers a diversified portfolio including Pro Plan (premium and veterinary diets), Purina ONE (mid-premium), Dog Chow and Cat Chow (mass segment), and Friskies, supported by R&D, veterinary nutrition solutions, and digital pet care platforms.

- Recent Developments: Nestlé (Purina) strengthened its manufacturing footprint in Brazil through continued investments, culminating in a major BRL 2.5 billion (~USD 470 million) wet pet food facility in Vargeão, complementing its Ribeirão Preto operations and significantly expanding production capacity to meet rising demand and exports across Latin America. The new facility is expected to nearly double Purina’s wet pet food capacity in Brazil, reinforcing the country’s role as a strategic hub for premium pet nutrition and regional supply.

- Strategic Focus: Nestlé Purina focuses on expanding its veterinary and premium nutrition segments while leveraging R&D, digital engagement, and e-commerce to strengthen its presence across Latin America’s evolving pet care ecosystem.

Colgate-Palmolive Company

Hill’s Pet Nutrition, a subsidiary of Colgate-Palmolive, is a leading premium pet food company specializing in science-based and veterinary diets, with a strong presence in Latin America supported by clinical nutrition expertise and established relationships with veterinary professionals.

- Product Portfolio: Hill’s Pet Nutrition offers Science Diet (everyday nutrition), Prescription Diet (therapeutic veterinary diets), and wellness-focused formulas, supported by clinical research, veterinarian partnerships, and digital tools for pet health management.

- Recent Developments: Hill’s Pet Nutrition expanded its direct-to-consumer digital capabilities with the launch of its online platform, enabling pet owners to access science-based nutrition and purchase products with veterinary guidance, reinforcing its vet-led distribution and digital engagement strategy. In parallel, the company continued advancing Prescription Diet innovations and global rollouts, strengthening access to therapeutic nutrition solutions through both veterinary clinics and digital channels.

- Strategic Focus: Hill’s Pet Nutrition focuses on strengthening its veterinary channel leadership while expanding prescription diet adoption and leveraging digital platforms to enhance direct engagement and recurring sales across Latin America.

Market Concentration Analysis

The Latin America pet food market exhibits moderate-to-high concentration at the top tier, with the leading five players - Mars Incorporated, Nestlé, and Colgate-Palmolive - collectively holding an estimated 55-60% of total market revenues in 2025. This concentration is highest in Brazil and Mexico, the region's two largest markets.

Leading multinational players such as Mars Incorporated, Nestlé (Purina), and Colgate-Palmolive Company (Hill’s), the Latin America pet food market remains highly fragmented. A large base of regional manufacturers, local brands, and distributor-led/import-dependent players together contribute a substantial share of market revenues.

Private-label offerings are still at an early stage but are gradually expanding, particularly through organized retail channels such as hypermarkets in Brazil. At the same time, consolidation is gaining momentum, with increased merger and acquisition activity in recent years as global players invest in or acquire local companies to strengthen distribution networks and expand regional presence.

Investment & Growth Opportunities

Functional and Veterinary Nutrition

Functional and veterinary pet nutrition is among the fastest-growing segments in Latin America, driven by rising pet humanization and demand for specialized diets. Premium and therapeutic products are expanding faster than mass categories, supported by veterinary channels and increasing awareness of pet health and clinical nutrition.

E-Commerce and Direct-to-Consumer Platforms

E-commerce is a rapidly growing channel in Latin America’s pet food market, supported by increasing digital adoption and convenience-driven purchasing. Brands are investing in direct-to-consumer and subscription models to improve customer retention, strengthen brand loyalty, and enhance margins through recurring revenue streams.

Rural and Tier-2 Market Expansion

Significant growth potential exists in non-urban areas, where many pet owners still rely on informal or homemade feeding practices. Expanding distribution networks and improving affordability can unlock demand, enabling companies to penetrate underserved markets and drive incremental volume growth across Latin America.

Sustainable Packaging and Ingredients

Sustainability is emerging as a key investment area, with growing consumer preference and regulatory focus on eco-friendly packaging and responsible sourcing. Companies are increasingly adopting recyclable materials, bio-based packaging, and alternative proteins to differentiate offerings and align with evolving environmental standards.

Future Market Outlook (2026-2034)

The Latin America pet food market is positioned for sustained and compounding growth over the 2026-2034 forecast period, with the total addressable market expanding from USD 11.3 Billion in 2025 to USD 21.8 Billion by 2034 - equivalent to a 7.32% CAGR. This trajectory is underpinned by structural demand drivers that are unlikely to reverse: demographic shifts toward pet ownership, urbanization, income growth, and deepening pet humanization.

The Latin America pet food market is evolving with increasing adoption of digital tools such as AI-driven recommendations, personalized nutrition, and subscription-based models, particularly among premium brands. Premiumization is a key growth driver, supported by pet humanization and higher spending on quality nutrition. Sustainability is also gaining importance, with companies advancing eco-friendly packaging and transparent ingredient sourcing amid rising regulatory and consumer expectations.

Brazil and Mexico remain the largest pet food markets in Latin America, while countries such as Colombia, Chile, and Peru are witnessing faster growth due to rising pet ownership and premiumization. E-commerce is expanding steadily but remains a smaller share of sales, with strong future potential. Companies investing in digital capabilities, premium products, and regional expansion are well positioned to capture growth.

Research Methodology

Primary Research

Primary research involved structured interviews with senior executives at pet food manufacturers, distributors, and specialty retailers across Brazil, Mexico, Argentina, Colombia, and Chile. A total of over 80 industry participants were engaged in 2024-2025. Consumer surveys capturing pet ownership behavior and purchase intent were also conducted across five Latin American markets.

Secondary Research

Secondary research incorporated data from national regulatory bodies (MAPA, COFEPRIS, SENASA), industry associations (ANFALPET Brazil, APPA), trade publications, company annual reports, SEC filings, and third-party syndicated data sources. Historical market data was referenced from 2020 to establish the validated baseline of USD 8.0 Billion.

Forecasting Models

Market forecasts were constructed using a combination of bottom-up country-level modeling and top-down macroeconomic calibration. Growth drivers were weighted using elasticity models. Scenario analysis - base case, bull, and bear - was employed to validate the 7.32% CAGR projection. Forecast confidence intervals were cross-validated against third-party consensus estimates.

Latin America Pet Food Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Pet Types Covered | Dog Food, Cat Food, Others |

| Product Types Covered | Dry Pet Food, Wet and Canned Pet Food, Snacks and Treats |

| Pricing Types Covered | Mass Products, Premium Products |

| Ingredient Types Covered | Animal Derived, Plant Derived |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Others |

| Countries Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | Mars, Incorporated, Nestlé, Colgate-Palmolive Company, BRF Global, Affinity, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Latin America pet food market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Latin America pet food market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Latin America pet food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Latin America Pet Food Market Report

The Latin America pet food market was valued at USD 11.3 Billion in 2025 and is expected to reach USD 21.8 Billion by 2034, growing at a CAGR of 7.32%.

Brazil leads with a 38.2% market share in 2025, contributing approximately USD 4.3 Billion. It hosts the world's third-largest pet population with over 140 million animals.

The Latin America pet food market is projected to grow at a CAGR of 7.32% during the forecast period from 2026 to 2034.

Dog food dominates with a 62.4% revenue share in 2025, driven by high canine ownership rates particularly in Brazil and Mexico.

Key drivers include rising pet humanization, expanding pet populations exceeding 300 million animals, growing online Platform adoption at 12.5% YoY growth, and rising disposable incomes.

The Latin America pet food market is projected to reach USD 16.1 Billion by 2030, driven by premiumization and rural penetration strategies.

Key players include Mars, Incorporated, Nestlé, Colgate-Palmolive Company, BRF Global, and Affinity.

Premium products account for 35.2% of the market in 2025, growing at 10.2% – significantly above the overall market's 7.32% CAGR.

Key trends include premiumization, functional ingredient adoption, clean-label demand, subscription-based e-commerce growth, and veterinary diet expansion.

Premium products are growing faster at 10.2% annually versus the market average of 7.32%, driven by health-conscious pet ownership trends in Brazil, Mexico, and Chile.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)