Mexico Insurance Market Size, Share, Trends and Forecast by Type and Region, 2026-2034

Mexico Insurance Market Size, Share, Trends & Forecast (2026-2034)

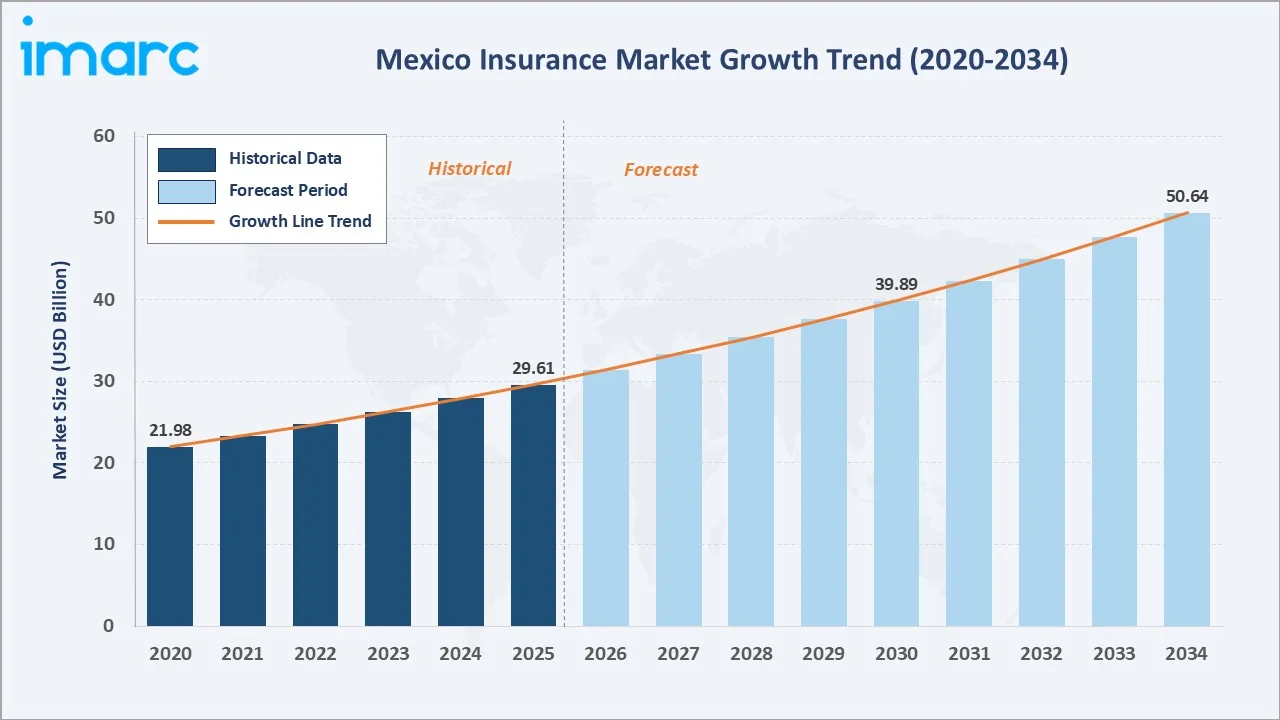

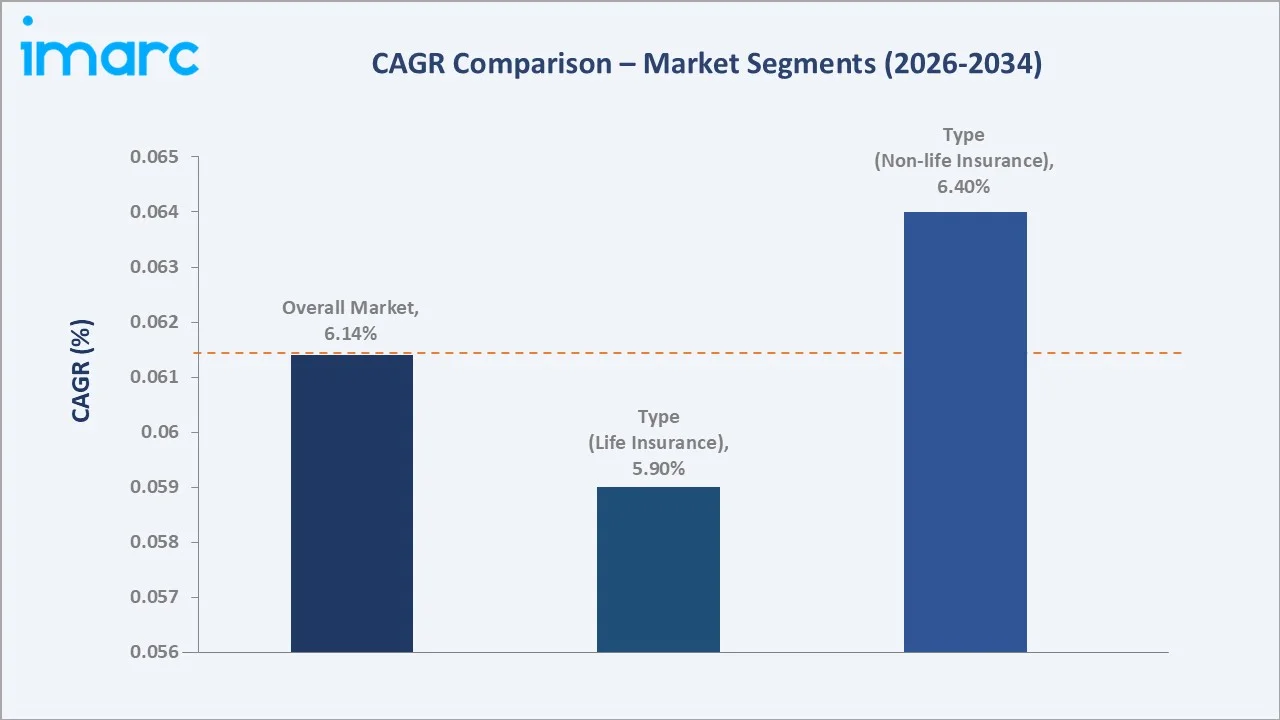

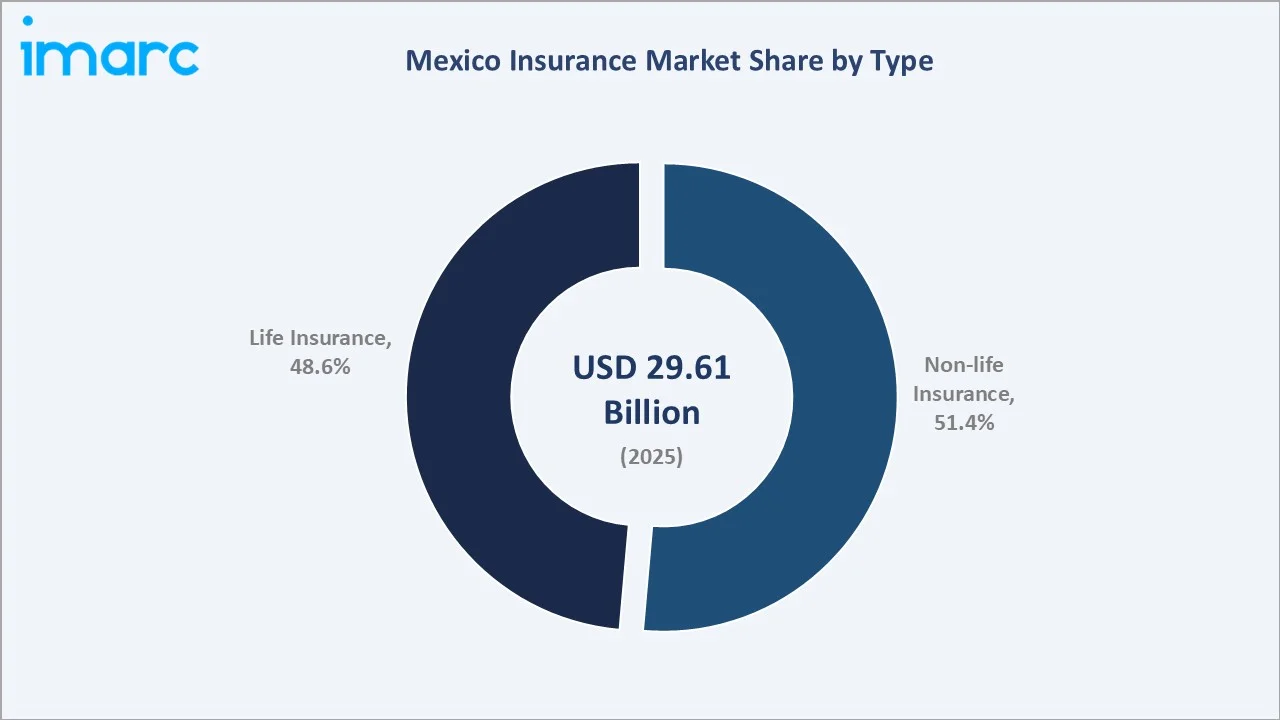

The Mexico insurance market reached USD 29.61 Billion in 2025 and is projected to reach USD 50.64 Billion by 2034, growing at a CAGR of 6.14% during 2026-2034. Rising foreign investment, driving market liberalization, the rapid expansion of e-commerce insurance platforms, growing demand from an aging population for health and life products, and increasing awareness of climate and natural disaster risks are the primary growth drivers shaping the Mexico insurance market outlook.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 29.61 Billion |

|

Forecast Market Size (2034) |

USD 50.64 Billion |

|

CAGR (2026-2034) |

6.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (Type) |

Non-life Insurance (51.4% share, 2025) |

|

Largest Region |

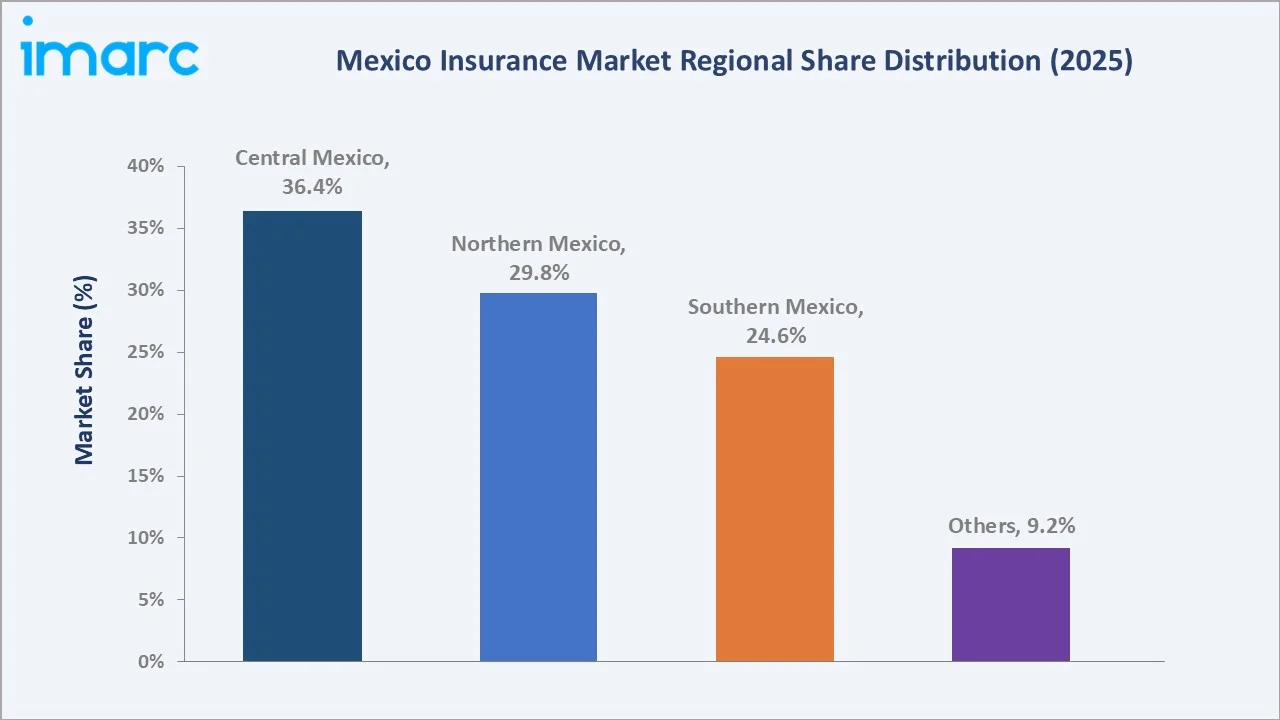

Central Mexico (36.4% share, 2025) |

|

Fastest Growing Region |

Northern Mexico |

Non-life insurance leads the Mexico insurance market with a 51.4% share in 2025, driven by mandatory automobile insurance requirements and growing demand for property and liability coverage. Life insurance follows at 48.6%, propelled by the expanding aging population and growing awareness of financial protection needs. Central Mexico dominates geographically at 36.4%, anchored by Mexico City’s concentration of corporate and individual policyholders, financial services infrastructure, and foreign insurer headquarters.

To get more information on this market, Request Sample

With product lines spanning life insurance, automobile insurance, fire insurance, liability coverage, and emerging parametric and insurtech offerings, the market is expected to continue expanding, supported by increasing financial literacy, digital distribution channel growth, regulatory modernization under the Comisión Nacional de Seguros y Fianzas (CNSF), and growing foreign investment bringing innovative insurance solutions to the Mexican market.

Executive Summary

The Mexico insurance market is on a sustained growth path, underpinned by demographic transformation, accelerating digital adoption, foreign capital inflows, and an expanding regulatory framework aligned with international best practices. The market reached USD 29.61 Billion in 2025 and is forecast to surpass USD 50.64 Billion by 2034, reflecting a steady CAGR of 6.14% over the forecast period.

Central Mexico leads the regional breakdown with a 36.4% revenue share in 2025, driven by Mexico City’s dense concentration of corporate insurance buyers, financial services companies, and foreign insurer operations. Northern Mexico (29.8%) benefits from robust industrial activity, cross-border trade with the United States, and strong employer-sponsored group insurance demand.

Non-life insurance commands the largest segment at 51.4% in 2025, with automobile insurance serving as the structural backbone given Mexico’s mandatory vehicle insurance requirements and large vehicle fleet. Life insurance at 48.6% is the fastest-growing segment in value terms, as demographic aging, rising middle-class incomes, and expanding bancassurance partnerships drive systematic penetration of life and health protection products across previously underserved consumer segments.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Non-life Insurance – 51.4% share (2025) |

|

Second Segment (Type) |

Life Insurance – 48.6% share (2025) |

|

Leading Region |

Central Mexico – 36.4% revenue share (2025) |

|

Fastest Growing Region |

Northern Mexico (industrial growth + cross-border trade) |

|

Top Companies |

MetLife, Inc., AXA, Quálitas Compañía de Seguros, S.A. de C.V., MAPFRE, and Zurich |

|

Key 2024 Development |

Descartes (global insurer) established a Mexico City office for parametric insurance (Oct 2024) |

- Non-life insurance accounts for 51.4% of the Mexico insurance market in 2025, anchored by mandatory automobile insurance requirements across Mexico’s large vehicle fleet and growing commercial property, fire, and liability coverage adoption.

- Life insurance holds 48.6% of the market in 2025 and is growing as Mexico’s aging demographic, increasing middle-class incomes, and expanding bancassurance partnerships systematically extend life and health product penetration.

- Central Mexico leads regionally at 36.4% (2025), driven by Mexico City’s concentration of corporate policyholders, financial services infrastructure, multinational company headquarters, and the highest household income levels nationally.

- Foreign investment is actively reshaping the competitive landscape, with Descartes entering Mexico City in October 2024 to offer parametric insurance covering agriculture, tropical cyclones, renewable energy, and earthquake risks.

- The e-commerce insurance distribution channel is accelerating penetration, supported by Mexico’s USD 54.4 Billion e-commerce market in 2025 and insurtech innovations, including pay-per-kilometer auto insurance (Miituo, November 2024).

Mexico Insurance Market Overview

The Mexico insurance market encompasses life insurance products, including individual and group life, health, and pension plans, alongside non-life insurance covering automobile, fire, property, liability, agricultural, and specialty lines. The market operates under the regulatory oversight of the Comisión Nacional de Seguros y Fianzas (CNSF), which supervises insurer solvency, product approval, and consumer protection standards. Mexico’s insurance penetration rate, measured as gross written premiums as a percentage of GDP, remains significantly below Latin American peers, indicating substantial structural growth potential as financial literacy improves and the regulatory environment evolves.

The insurance value chain in Mexico has undergone a meaningful transformation driven by digital technology adoption, bancassurance expansion through major banking groups, and the entry of foreign insurers bringing new products, risk models, and distribution capabilities. Mexico’s demographic profile, particularly its expected growth of age 65 and older to reach over 30 million by 2050, creates a structurally expanding demand base for life, health, and retirement insurance products.

Market Dynamics

To evaluate market opportunities, Request Sample

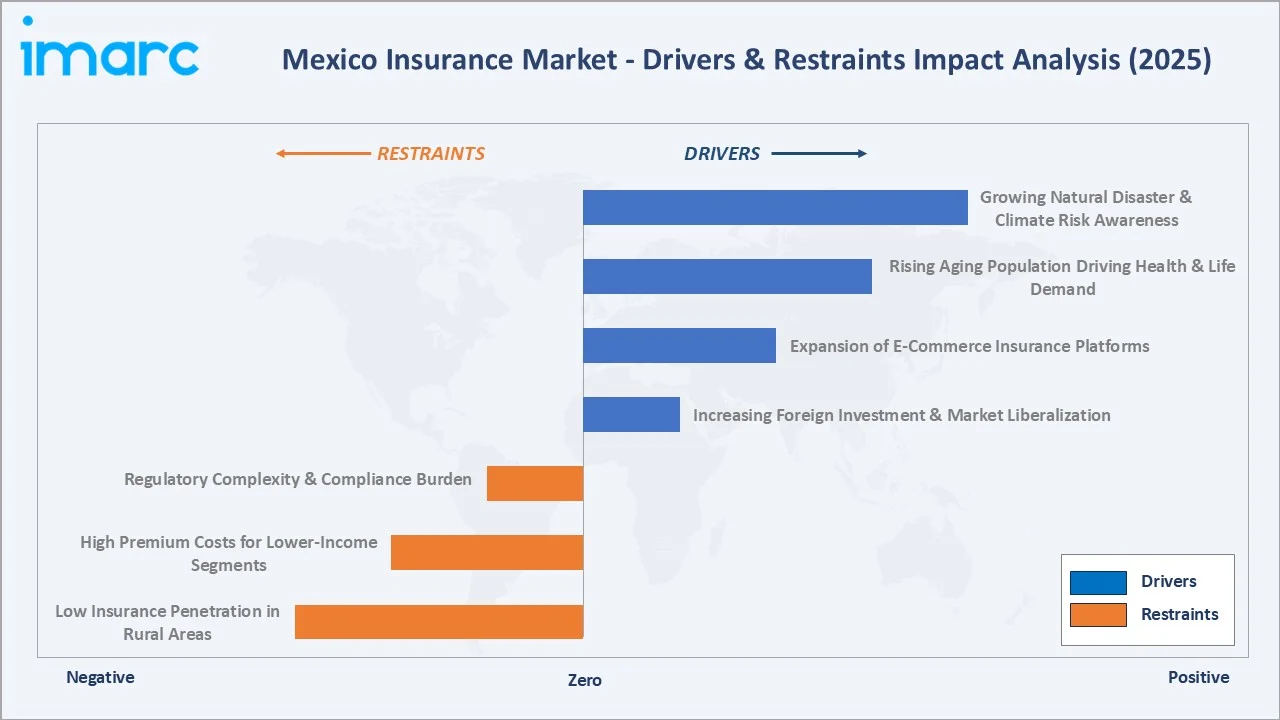

Market Drivers

- Increasing Foreign Investment and Market Liberalization: In October 2024, Descartes, a global corporate insurer, established a new office in Mexico City focused on parametric insurance for agriculture, tropical cyclones, renewable energy, and earthquake risks.

- Expansion of E-Commerce Insurance Platforms: Mexico’s rapidly growing e-commerce sector, which reached USD 54.4 Billion in market size in 2025, is creating powerful distribution channels for insurance products. Online platforms enable price comparison and seamless digital onboarding, dramatically reducing distribution costs and expanding market reach.

- Rising Aging Population Driving Health and Life Demand: Insurers are actively developing product lines targeting chronic disease management, preventive care, and financial security for retired individuals, with Auna’s OncoSalud oncology insurance (July 2024) exemplifying the targeted product innovation responding to this demographic trend.

- Growing Natural Disaster and Climate Risk Awareness: Mexico’s geographic exposure to earthquakes, tropical cyclones, floods, and droughts is driving growing demand for both traditional catastrophe coverage and emerging parametric insurance products. Government programs and multilateral development bank partnerships are actively expanding agricultural and disaster risk insurance penetration in rural and southern regions.

Market Restraints

- Low Insurance Penetration in Rural and Informal Economy Segments: Despite overall market growth, insurance penetration in rural areas and among the significant informal economy workforce remains very low. Financial literacy gaps, limited distribution networks outside major urban centers, and premium affordability constraints among lower-income populations are primary structural barriers to market expansion.

- High Premium Costs for Lower-Income Segments: Absolute premium levels for comprehensive health and life insurance products remain prohibitive for a significant portion of Mexico’s population, particularly in the context of income inequality between urban and rural areas and between formal and informal sector workers.

- Regulatory Complexity and Compliance Burden: Mexico’s evolving regulatory framework, while generally supportive of market development, creates compliance costs and operational complexity for both domestic insurers and foreign entrants navigating CNSF requirements alongside international regulatory standards.

Market Opportunities

- Insurtech and Digital Distribution Innovation: The convergence of mobile penetration, fintech infrastructure, and insurance product innovation creates substantial opportunities for digitally native insurers to reach previously unserved market segments through embedded insurance, microinsurance, and pay-as-you-go coverage models.

- Bancassurance Channel Expansion: Mexico’s major banking groups represent powerful distribution partners for life and health insurance products, with relatively low current bancassurance penetration creating significant headroom for systematic policy growth through banking relationships.

- Parametric and Climate Risk Insurance: Mexico’s vulnerability to natural disasters and growing agricultural sector creates specialized market opportunities for parametric insurance products that provide rapid, transparent claims settlement based on objective trigger events such as rainfall levels, wind speed, or earthquake magnitude.

Market Challenges

- Financial Literacy and Insurance Awareness Gaps: A significant proportion of the Mexican population, particularly outside major metropolitan areas, lacks awareness of insurance product benefits and the concept of risk transfer, requiring sustained industry and government investment in financial education programs.

- Claims Settlement Trust Deficit: Historical consumer experiences with delayed or disputed insurance claims have created trust deficits in some market segments, requiring insurers to invest in transparent claims processing, digital tracking tools, and customer communication to rebuild confidence in insurance products.

Emerging Market Trends

1. Increasing Foreign Investment and International Market Entry

Increased foreign investment is one of the defining structural trends reshaping the Mexico insurance market. International insurers are entering Mexico with fresh capital, advanced actuarial capabilities, and innovative product concepts adapted to local risk profiles. Foreign capital is simultaneously enhancing insurer financial strength, enabling underwriting of larger and more complex risks, and encouraging the broader digitalization of insurance distribution and operations.

2. Expansion of E-Commerce and Digital Insurance Platforms

The expansion of e-commerce and digital insurance platforms is fundamentally transforming how Mexican consumers access, compare, and purchase insurance products, representing one of the most consequential Mexico insurance market trends. This shift toward digital-native insurance products is particularly effective in reaching younger, urban, digitally engaged consumer segments that have historically been underserved by traditional insurance distribution.

3. Rising Aging Population Driving Health and Life Insurance Demand

Mexico’s evolving demographic profile is creating powerful structural demand growth for health and life insurance products that will sustain the Mexico insurance market growth trajectory through 2034 and beyond. In July 2024, Auna launched OncoSalud, Mexico’s first integrated oncology insurance product, covering cancer prevention, early detection, and treatment at USD 40 monthly with up to USD 0.5 million annual coverage, directly responding to the healthcare needs of an aging population.

4. Insurtech Innovation and Digital Transformation

Artificial intelligence applications in risk scoring, fraud detection, and personalized product recommendation are becoming standard capabilities among leading insurers. Mobile-first insurance applications, open API ecosystems enabling embedded insurance integration with e-commerce and financial platforms, and blockchain-based claims verification are collectively reshaping the operational model of the Mexican insurance industry.

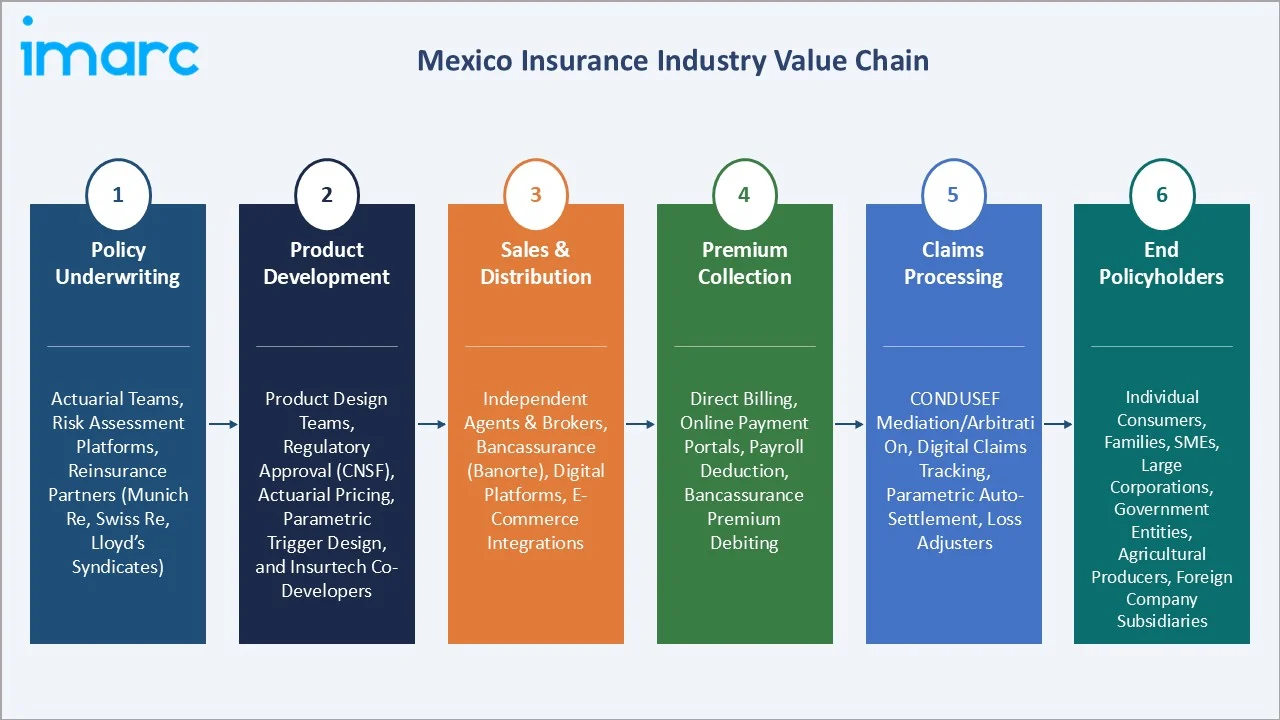

Industry Value Chain Analysis

The Mexico insurance value chain encompasses policy underwriting, product development, distribution, premium collection, and claims processing, with each stage subject to CNSF regulatory oversight. The integration of digital technology is restructuring traditional relationships between insurers, brokers, bancassurance partners, and policyholders, enabling more efficient and personalized interactions across the value chain.

|

Stage |

Key Participants / Examples |

|

Policy Underwriting |

Actuarial teams, risk assessment platforms, reinsurance partners (Munich Re, Swiss Re, Lloyd’s syndicates) |

|

Product Development |

Product design teams, regulatory approval (CNSF), actuarial pricing, parametric trigger design, and insurtech co-developers |

|

Sales & Distribution |

Independent agents and brokers, bancassurance (Banorte), digital platforms, e-commerce integrations |

|

Premium Collection |

Direct billing, online payment portals, payroll deduction (group schemes), bancassurance premium debiting |

|

Claims Processing |

CONDUSEF mediation/arbitration for consumer claims disputes, digital claims tracking, parametric auto-settlement, and independent loss adjusters |

|

End Policyholders |

Individual consumers, families, SMEs, large corporations, government entities, agricultural producers, foreign company subsidiaries |

Technology Landscape in the Mexico Insurance Industry

Artificial Intelligence and Predictive Analytics

Insurers are deploying AI-powered risk scoring models that integrate non-traditional data sources, including telematics, social media behavior patterns, and geospatial climate risk data, to refine underwriting decisions and price risk more competitively. Predictive analytics platforms are enabling proactive customer engagement for policy renewal and upselling, improving customer lifetime value metrics across the leading insurer portfolios.

Telematics and Usage-Based Insurance

Miituo’s November 2024 launch of pay-per-kilometer car insurance using driving behavior telematics represents a market-defining example of technology enabling product innovation that expands market accessibility for low-mileage and safety-conscious drivers. Telematics data also enables insurers to build more accurate risk profiles, reducing adverse selection and enabling competitive pricing for demonstrably low-risk policyholders.

Digital Distribution and Embedded Insurance Platforms

E-commerce platforms, ride-sharing applications, travel booking services, and mortgage platforms are embedding relevant insurance products into transactional flows, dramatically improving conversion rates compared to traditional outbound insurance marketing. This distribution innovation is particularly powerful in reaching younger and digitally native Mexican consumers who may not have engaged with insurance through traditional channels.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Non-life Insurance | 51.4% | 2025 |

| Region | Central Mexico | 36.4% | 2025 |

By Type

Non-life Insurance leads the type segment with a 51.4% share in 2025. This segment’s dominance is anchored by Mexico’s mandatory automobile insurance requirements, which create a large structural base of premium revenue from the country’s expanding vehicle fleet. Beyond automobile coverage, non-life insurance encompasses fire and property insurance for residential and commercial risks, liability insurance for professional and corporate exposures, agricultural insurance supported by government programs, and specialty lines including marine, engineering, and surety.

To access detailed market analysis, Request Sample

Life Insurance accounts for 48.6% of the market, encompassing individual and group life, health and medical expense insurance, personal accident coverage, and pension and retirement savings products. This segment is the primary beneficiary of Mexico’s aging demographic trend, rising middle-class incomes, and expanding bancassurance distribution through major banking groups.

Regional Market Insights

Central Mexico (36.4%, 2025) is the dominant insurance market, anchored by Mexico City’s unrivaled concentration of corporate headquarters, financial services companies, international organizations, and high-income individual policyholders. The region generates the highest commercial insurance premiums nationally across group life and health, commercial property, directors & officers liability, and emerging cyber insurance lines.

|

Region |

Share (2025) |

Key Growth Drivers |

Insurance Demand Profile |

|

Central Mexico |

36.4% |

Corporate demand; highest incomes; foreign company HQs; financial services concentration |

Commercial property, group life & health, liability, D&O, cyber |

|

Northern Mexico |

29.8% |

Nearshoring manufacturing; US-Mexico trade; industrial expansion; high auto density |

Automobile, commercial property, engineering, and employer group schemes |

|

Southern Mexico |

24.6% |

Agricultural insurance programs; tourism sector; government-backed coverage; disaster risk |

Agricultural, catastrophe, travel, and government employee group health |

|

Others |

9.2% |

Specialty markets; remote areas; government infrastructure; energy projects |

Engineering, energy, parametric, marine, and government surety |

Northern Mexico (29.8%) is experiencing accelerated premium growth driven by the nearshoring manufacturing boom, with companies relocating production from Asia to take advantage of proximity to the United States market. This industrial expansion is generating substantial demand for commercial property, machinery and equipment, employer liability, and group employee benefits insurance. Automobile insurance demand is proportionally high in the north, given the vehicle-dependent transportation infrastructure.

Competitive Landscape

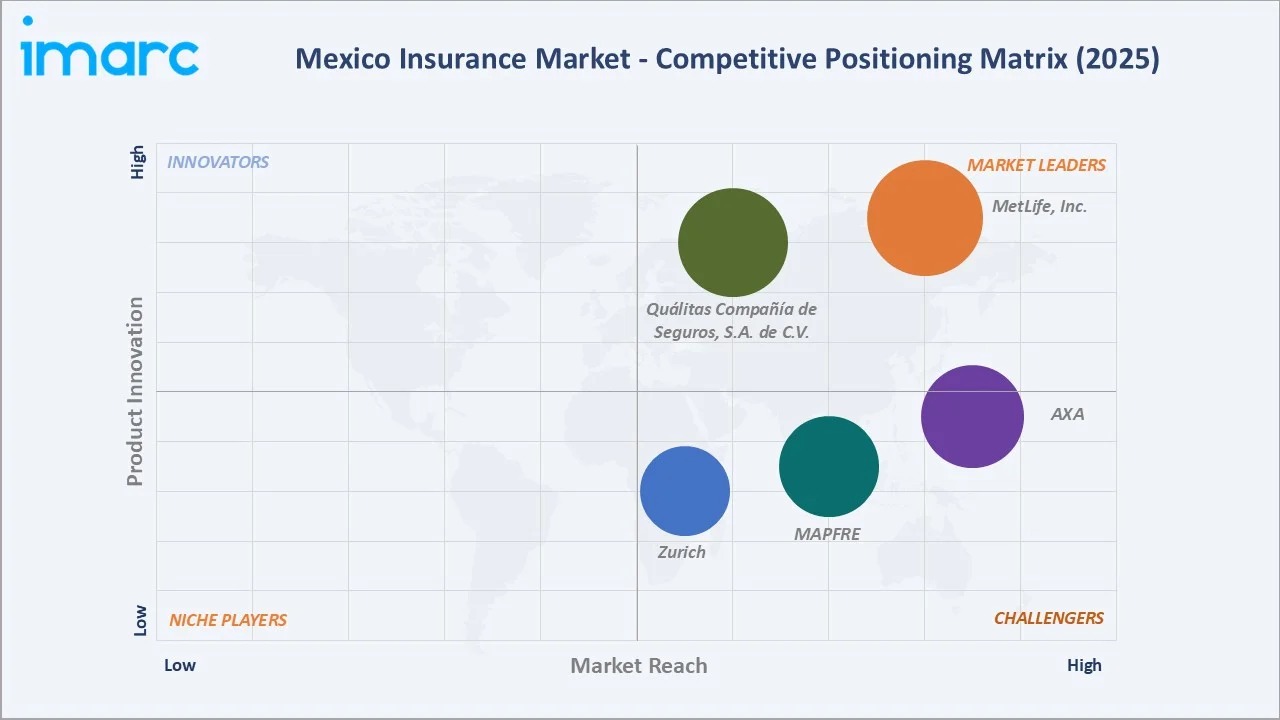

The Mexico insurance market exhibits a moderately concentrated competitive structure, with domestic incumbents, including Quálitas Compañía de Seguros, S.A. de C.V., maintaining strong positions in their respective segments alongside major international insurers, including MetLife, Inc., AXA, MAPFRE, and Zurich. The top five insurers collectively account for approximately 40–45% of total gross written premiums in 2025.

|

Company |

Key Lines |

Market Position |

Core Strength |

|

MetLife, Inc. |

Life, health, pension |

Market Leader |

Global brand recognition; strong bancassurance partnerships; leading individual life and group employee benefits |

|

AXA |

Life, auto, property, health |

Strong Challenger |

Diversified product range; digital innovation investments; strong employer group health coverage and bancassurance channel |

|

Quálitas Compañía de Seguros, S.A. de C.V. |

Automobile insurance |

Leader |

Mexico’s leading automobile insurer, with a deep dealer network integration, a specialist focus, and a dominant market share in the auto segment |

|

MAPFRE |

Auto, property, life, and agricultural |

Challenger |

Spanish multinational with strong agricultural and catastrophe insurance capabilities; growing rural market presence |

|

Zurich |

Commercial, property, liability, engineering |

Challenger |

Specialist in commercial and industrial lines; strong engineering and infrastructure project insurance |

Competitive dynamics are being reshaped by three concurrent forces: the accelerating entry of foreign insurers bringing capital, technology, and specialized products; the growth of insurtech companies deploying digital-first distribution and product innovation models; and the strategic expansion of bancassurance arrangements between leading insurance groups and Mexico’s major banking institutions.

Key Company Profiles

MetLife Inc.

MetLife Inc., headquartered in New York, is one of Mexico’s leading life and group benefits insurers, with particular strength in corporate employee benefits, bancassurance partnerships, and individual life and health products. MetLife leverages its global actuarial and investment management capabilities to offer competitive long-term life and pension products.

- Product Portfolio: Group life and health, individual life, supplemental health, accident and disability, pension savings, and retirement annuity products.

- Recent Developments: MetLife’s Q4 2025 results show Latin America’s adjusted earnings of about USD 227 million (up ~13%), driven by strong growth across the region, including Mexico.

- Strategic Focus: Bancassurance channel optimization; employer group benefits market leadership; digital individual life sales growth; pension and retirement product development for Mexico’s aging workforce.

Quálitas Compañía de Seguros, S.A. de C.V.

Quálitas, headquartered in Mexico City, is Mexico’s dominant automobile insurance specialist, holding the largest market share in the Mexican auto insurance segment through its comprehensive vehicle dealer network integration, competitive pricing, and efficient digital claims processing.

- Product Portfolio: Automobile insurance (comprehensive and third-party liability), motorcycle insurance, commercial vehicle coverage, and fleet insurance for corporate clients.

- Recent Developments: Qualitas adopted Octo Telematics’ commercial fleet telematics solution, enabling customers to track vehicles and improve driver safety through data‑driven insights, reflecting the rising use of telematics and usage‑based insurance tools.

- Strategic Focus: Automobile insurance market share defense through technology investment; telematics and usage-based product development; fleet insurance growth with commercial and corporate clients; digital claims processing efficiency.

AXA

AXA is one of Mexico’s most diversified insurance companies, with strong positions across life, health, automobile, and property segments alongside growing capabilities in digital distribution and corporate insurance lines. AXA’s global technology investments and innovation programs are actively applied in its Mexican operations.

- Product Portfolio: Life insurance, individual and group health, automobile, homeowners, commercial property, travel, and specialty corporate insurance lines.

- Recent Developments: In March 2026, AXA announced the five‑year renewal of the strategic partnership with Shift Technology to extend their AI‑powered collaboration, already active in 15 countries, including Mexico, to enhance claims, fraud detection, and underwriting with advanced algorithms.

- Strategic Focus: Digital and direct insurance distribution growth; health insurance innovation for individual and employer group segments; corporate property and liability market expansion; insurtech partnership investments.

Market Concentration Analysis

The Mexico insurance market exhibits moderate concentration, with the top five insurers holding approximately 40–45% of gross written premium in 2025. The automobile insurance segment shows the highest concentration, with Quálitas holding a dominant individual segment share, while the life and health segment is more fragmented among a larger number of domestic and international providers.

Market consolidation activity is expected to gradually increase through 2034, driven by regulatory solvency requirements that favor scale and capital adequacy, technology investment needs that create fixed cost advantages for larger operators, and the acquisition strategies of international insurance groups seeking to expand Mexican market exposure. The insurtech segment is simultaneously introducing new competitive dynamics through digitally native business models that compete on distribution efficiency and customer experience rather than traditional scale advantages.

Investment & Growth Opportunities

Fastest Growing Segments

Individual life and health insurance (estimated CAGR above 7%), digital and embedded insurance distribution platforms, and parametric natural disaster insurance represent the three highest-growth investment vectors in the Mexican insurance market through 2034. The individual life segment in particular benefits from very low current penetration relative to Mexico’s income levels and demographic profile, suggesting structural long-term growth as financial literacy improves and digital distribution reduces acquisition costs.

Regional Expansion Opportunities

Southern Mexico represents the most compelling regional growth opportunity, driven by government-backed agricultural insurance program expansion, growing tourism sector demand for specialized coverage, and increasing natural disaster insurance awareness following recent catastrophe events. Northern Mexico’s nearshoring manufacturing boom creates concentrated commercial insurance demand growth for property, engineering, employer liability, and group employee benefits products in border states, including Nuevo León, Coahuila, Chihuahua, and Baja California.

Venture and Institutional Investment Themes

- Key investment themes include insurtech platforms enabling digital insurance distribution, telematics and usage-based insurance technology, parametric insurance product development and distribution for agricultural and disaster risks, and AI-powered underwriting and claims processing automation.

- Private equity interest is targeting mid-size Mexican insurance brokerages as consolidation platform investments, alongside insurtech companies with demonstrated digital distribution capabilities and growing customer bases.

- Impact capital opportunities exist in microinsurance programs targeting Mexico’s large informal economy workforce, agricultural insurance for smallholder farmers, and health microinsurance expanding coverage to lower-income segments.

Future Market Outlook (2026-2034)

The Mexico insurance market is positioned for consistent, value-creating growth through 2034. From a base of USD 29.61 Billion in 2025, the market is projected to reach USD 50.64 Billion by 2034, representing a total incremental value of USD 21.03 Billion over the forecast decade at a CAGR of 6.14%.

The convergence of demographic aging, rising middle-class incomes, accelerating digital insurance adoption, foreign capital inflows, and regulatory modernization creates a self-reinforcing growth dynamic. Insurers that invest in digital distribution capabilities, develop products specifically addressing Mexico’s aging population health needs, and build parametric insurance expertise for the country’s significant natural disaster exposure will capture a disproportionate share of this growth.

The Mexico insurance market forecast reflects a market transitioning from low penetration toward structural deepening, as a growing proportion of the population engages with insurance products for the first time through digital channels and bancassurance, while existing policyholders upgrade toward more comprehensive coverage levels.

Research Methodology

Primary Research

Primary research comprised structured interviews and surveys with over 80 industry participants during 2024–2025, including insurance executives, regulatory officials, insurance brokers and agents, bancassurance partnership managers, insurtech founders, and independent actuaries across Mexico City, Monterrey, and Guadalajara.

Secondary Research

Secondary research encompassed CNSF regulatory publications, insurance industry association reports from the Asociación Mexicana de Instituciones de Seguros, company annual reports, IMF and World Bank financial sector assessments, population data from CONAPO and CELADE, and trade publications covering the Mexican insurance and financial services industries.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating gross written premium data, insurance penetration benchmarking against comparable Latin American markets, demographic projections, and regulatory development timelines. A base-case CAGR of 6.14% reflects consensus estimates validated against CNSF-reported market data.

Mexico Insurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | MetLife, Inc., AXA, Quálitas Compañía de Seguros, S.A. de C.V., MAPFRE, Zurich, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico insurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Insurance Market Report

The Mexico insurance market reached USD 29.61 Billion in 2025. It is projected to reach USD 50.64 Billion by 2034.

The Mexico insurance market is expected to grow at a CAGR of 6.14% during the forecast period from 2026-2034, supported by foreign investment, digital insurance expansion, demographic aging, and improving financial literacy.

Non-life Insurance leads with a 51.4% share in 2025, anchored by mandatory automobile insurance requirements, growing commercial property coverage, and expanding liability insurance demand from Mexico’s industrial and corporate sectors.

Central Mexico dominates with a 36.4% market share in 2025, driven by Mexico City’s concentration of corporate insurance buyers, financial services companies, international organization headquarters, and the highest household income levels in the country.

The Mexico insurance market is driven by rising foreign investment bringing capital and innovative products, the rapid expansion of e-commerce and digital insurance distribution platforms, growing demand from an aging population for health and life products, and increasing awareness of natural disaster and climate risk exposures requiring specialized coverage solutions.

Key players include MetLife, Inc., AXA, Quálitas Compañía de Seguros, S.A. de C.V., MAPFRE, and Zurich, among other domestic and international insurers operating across life, non-life, and specialty insurance segments.

Digital technology is transforming the Mexican insurance market through e-commerce distribution platforms, telematics-based usage-sensitive insurance products (such as Miituo’s pay-per-kilometer automobile insurance), AI-powered underwriting and fraud detection, and mobile-first policy management applications that improve customer engagement and operational efficiency.

Key challenges include very low insurance penetration in rural areas and among the informal economy workforce, high premium costs relative to lower-income consumer segments, financial literacy gaps limiting insurance awareness, historical trust deficits related to claims settlement experiences, and the regulatory complexity of navigating CNSF requirements alongside international compliance frameworks.

Significant opportunities exist in individual life and health insurance digitization, parametric agricultural and disaster risk insurance, bancassurance channel deepening, insurtech distribution platforms, microinsurance for informal economy workers, and commercial insurance for nearshoring manufacturing operations in Northern Mexico.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)