Personal Care Electrical Appliances Market Size, Share, Trends and Forecast by Product, Type, Distribution Channel, and Region, 2026-2034

Personal Care Electrical Appliances Market Size, Share, Trends & Forecast (2026-2034)

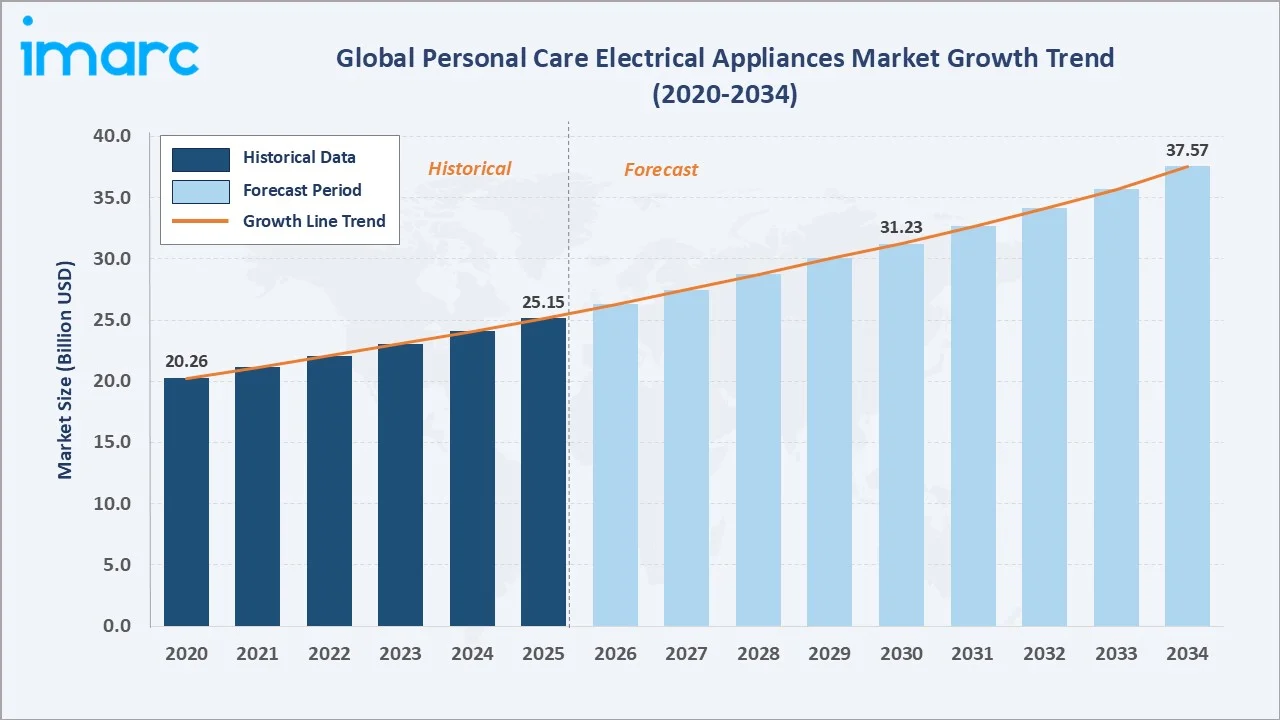

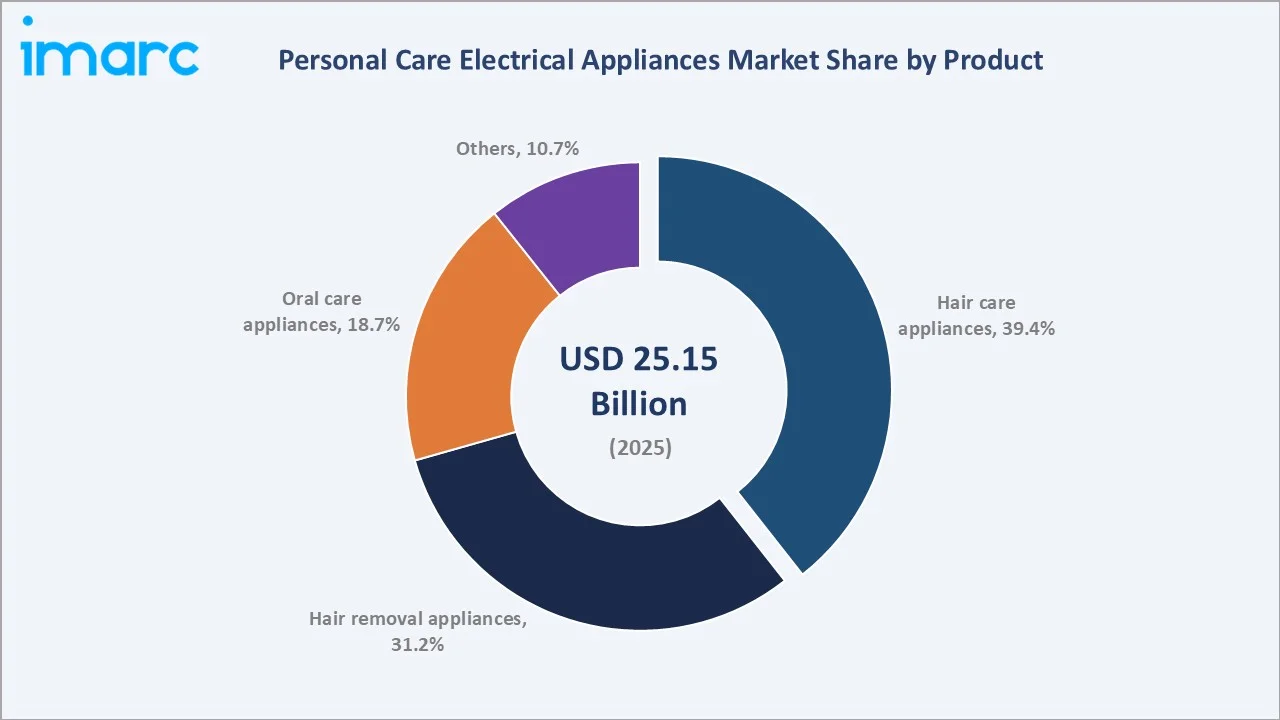

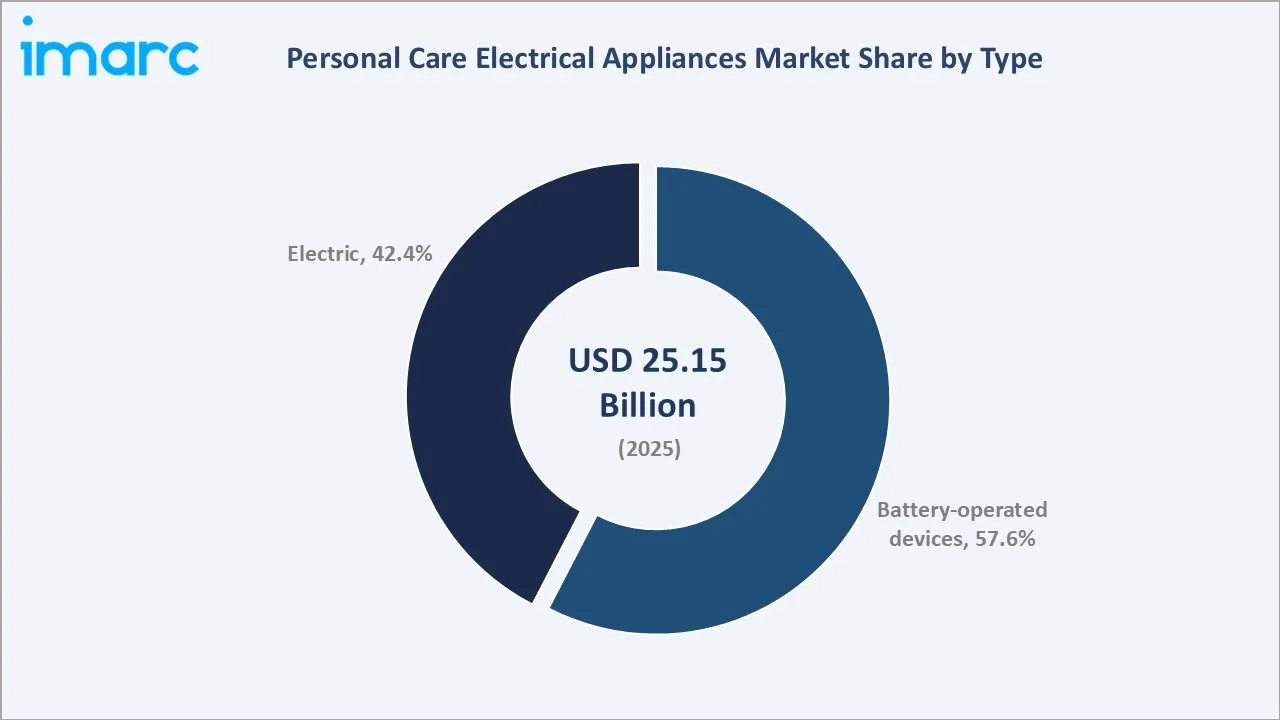

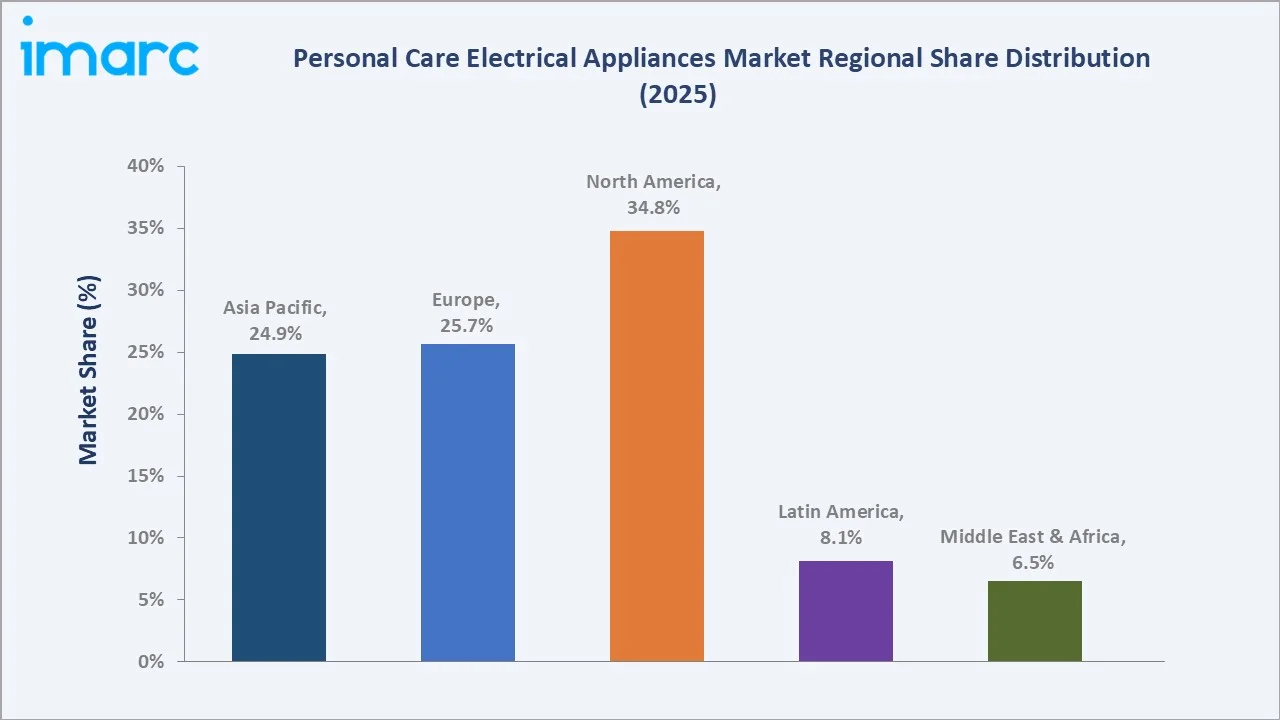

The global personal care electrical appliances market reached USD 25.15 Billion in 2025 and is projected to reach USD 37.57 Billion by 2034, growing at a CAGR of 4.42% during 2026-2034. Rising urbanization, higher disposable incomes, and growing consumer focus on personal grooming and hygiene are driving robust demand. Hair care appliances lead with 39.4% product share (2025), while battery-operated devices dominate the type segment at 57.6%. North America commands 34.8% of global market share, followed by Europe at 25.7% and Asia Pacific at 24.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 25.15 Billion |

|

Forecast Market Size (2034) |

USD 37.57 Billion |

|

CAGR (2026-2034) |

4.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Segment |

Hair Care Appliances (39.4%, 2025) |

|

Dominant Type |

Battery Operated (57.6%, 2025) |

|

Leading Region |

North America (34.8%, 2025) |

The global personal care electrical appliances market expanded from USD 20.26 Billion in 2020 to USD 25.15 Billion in 2025, anchored at USD 31.23 Billion in 2030, and forecast to reach USD 37.57 Billion by 2034. The COVID-19 pandemic accelerated at-home grooming adoption in 2020, triggering sustained demand for personal care appliances. This behavioral shift proved durable post-pandemic, supporting above-trend growth through 2022-2025.

To get more information on this market, Request Sample

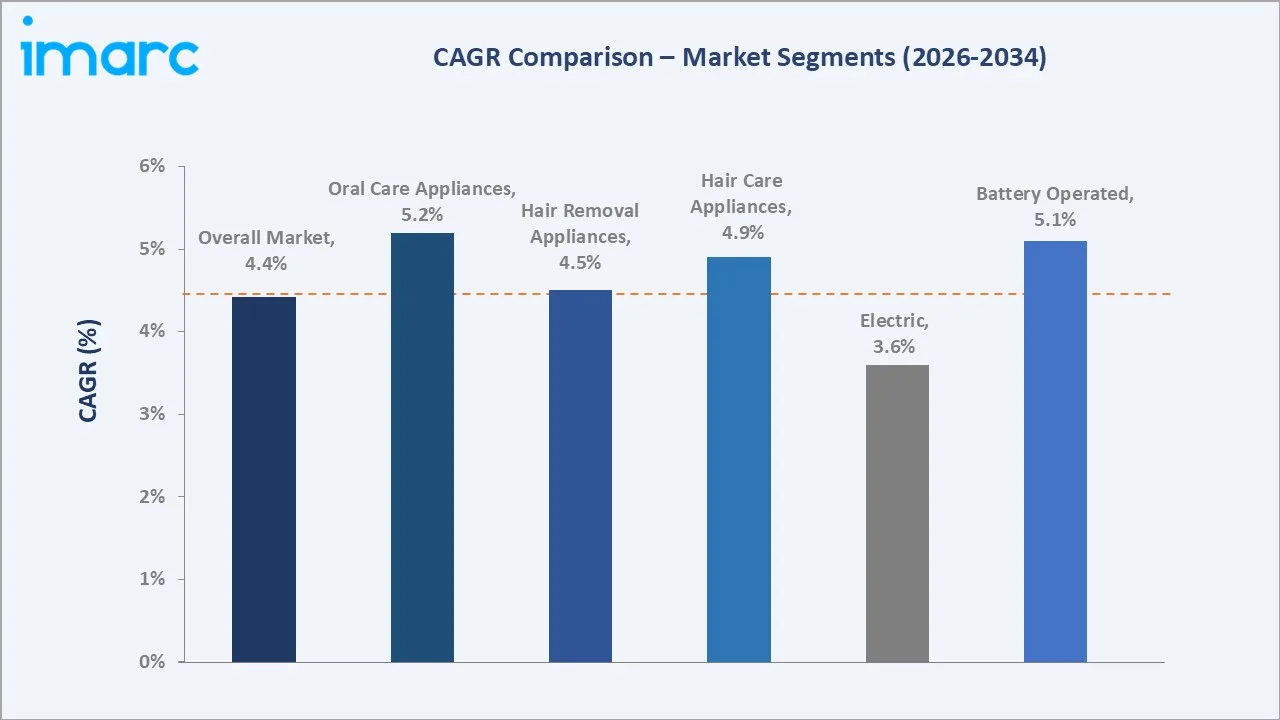

Oral care appliances grow fastest at ~5.2% CAGR, driven by electric toothbrush mainstream adoption and expanding oral irrigator penetration. Battery-operated devices grow at ~5.1% CAGR, outpacing electric (corded) types at ~3.6%, reflecting consumer preferences for cordless portability. Hair care appliances maintain a stable ~4.9% CAGR through continued product premiumization and heat-free technology innovation.

Executive Summary

The global personal care electrical appliances market represents one of the consumer electronics sector's most resilient growth verticals, driven by the convergence of lifestyle evolution, grooming culture expansion, and technological innovation. Reaching USD 25.15 Billion in 2025, the market is projected to reach USD 37.57 Billion by 2034, growing at a CAGR of 4.42%. The market expanded from USD 20.26 Billion in 2020, reflecting a consistent upward trajectory underpinned by urbanization and rising per-capita grooming expenditures.

Hair care appliances command the largest product share at 39.4% (2025), anchored by pervasive demand for hair dryers, straighteners, and stylers. Hair removal appliances follow at 31.2%, boosted by rising adoption of epilators, trimmers, and shavers across gender demographics. Oral care appliances, at 18.7%, represent the fastest-growing sub-segment, with electric toothbrushes gaining mainstream penetration globally. Battery-operated devices lead the type segment at 57.6%, reflecting consumer preference for cordless convenience and portability.

North America dominates regionally with 34.8% share, supported by a mature grooming culture and high consumer spending. Europe (25.7%) and Asia Pacific (24.9%) follow closely, with Asia Pacific representing the highest incremental CAGR potential through expanding middle-class populations. The market outlook through 2034 remains strongly positive, with smart connectivity, AI personalization, sustainable materials, and D2C subscription models acting as key growth catalysts.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Segment |

Hair Care Appliances - 39.4% share (2025) |

|

Second Product Segment |

Hair Removal Appliances - 31.2% share (2025) |

|

Fastest Growing Sub-Segment |

Oral Care Appliances (~5.2% CAGR, 2026-2034) |

|

Dominant Type |

Battery Operated - 57.6% market share (2025) |

|

Leading Region |

North America - 34.8% market share (2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Top Companies |

Philips, Procter & Gamble, Dyson, and Panasonic |

|

Market Opportunity |

Smart AI grooming devices; sustainable eco-friendly appliances; D2C subscription models; emerging market penetration |

Key Analytical Observations Supporting The Above Data:

- Hair Care Appliances at 39.4%: Dominance is anchored by universal demand for hair drying, styling, and treatment solutions. Premium device adoption has accelerated among millennial and Gen Z consumers globally, with heat-free and ionic technology variants driving repeat purchases and above-average ASP growth.

- Hair Removal Appliances at 31.2%: Rising male grooming culture has significantly expanded this segment. Trimmers and shavers are seeing robust unit growth across North America and Asia Pacific. The structural expansion of male grooming globally directly benefits this sub-segment through 2034.

- Oral Care Appliances at 18.7%: Electric toothbrushes account for approximately 67% of this sub-segment (2025). Dentist endorsements, health-consciousness trends, and smart Bluetooth-enabled toothbrushes are accelerating adoption, particularly in premium consumer markets in Europe and North America.

- Battery Operated at 57.6%: Cordless convenience, travel-friendly designs, and significant lithium-ion battery life improvements have made battery-operated devices the default consumer preference across all personal care appliance categories.

- North America at 34.8%: The United States accounts for the majority of the regional share, driven by high per-capita grooming expenditure, strong brand penetration by Philips, Conair, and Remington, and robust e-commerce infrastructure supporting recurring purchases.

- Asia Pacific as Fastest Growing Region: Urbanization in China, India, and Southeast Asia, rising female participation in the workforce, increasing disposable incomes, and growing oral and personal hygiene awareness are collectively driving above-market growth rates through 2034.

Global Personal Care Electrical Appliances Market Overview

The global personal care electrical appliances market encompasses a broad spectrum of electrically and battery-powered devices designed for personal grooming, hygiene, and aesthetic care. The ecosystem integrates hair care appliances including dryers, straighteners, and curlers; hair removal devices such as epilators, shavers, and trimmers; oral care appliances comprising electric toothbrushes and oral irrigators; and a growing range of skin and body care electronics. These products are available across portable, compact, and travel-friendly variants, offered through both online and offline distribution channels.

Macroeconomic drivers include rapid global urbanization, the United Nations projects 68% of the world's population will live in urban areas by 2050, alongside expanding middle-class populations with higher discretionary spending. Increasing investment by manufacturers in R&D, growing e-commerce penetration, and rising consumer awareness of oral and personal hygiene are further accelerating market adoption across emerging and established economies.

The industry ecosystem spans raw material and component suppliers, OEM and branded product manufacturers, technology enablers for IoT and AI connectivity, multi-channel distributors, and diverse end-user segments ranging from individual households to professional salon operators and wellness centers.

Market Dynamics

To evaluate market opportunities, Request Sample

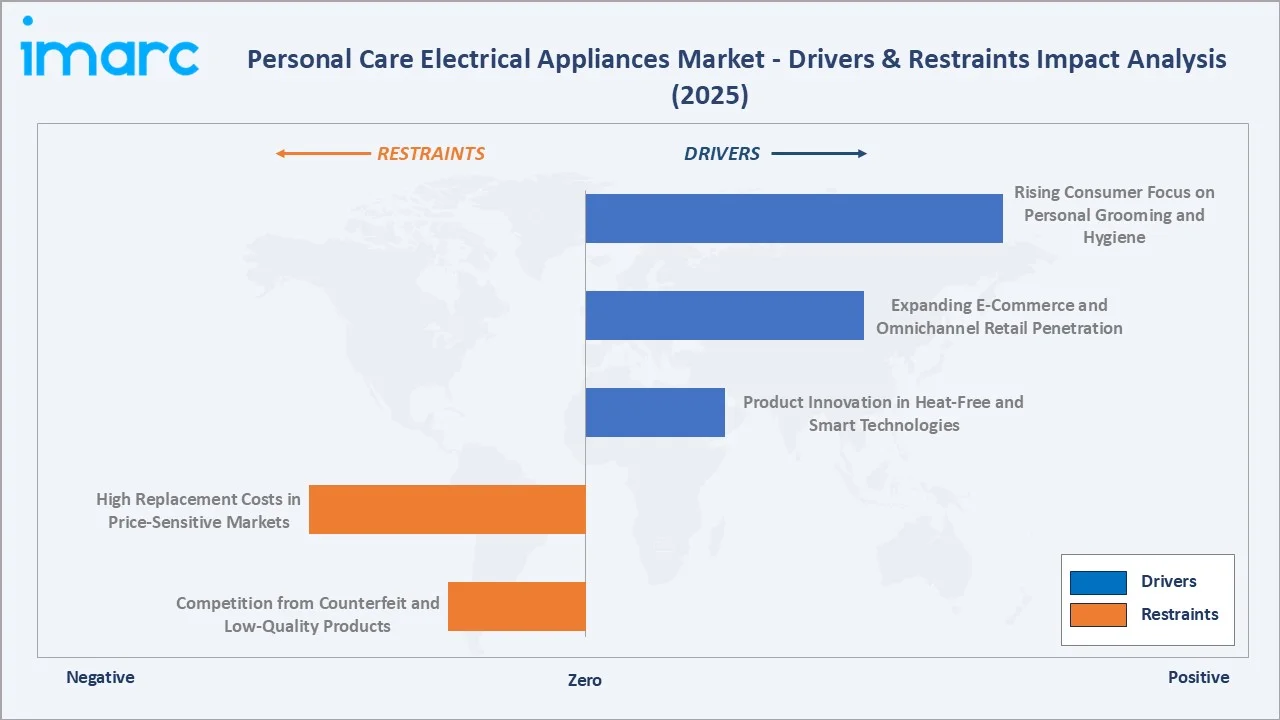

Market Drivers

- Rising Consumer Focus on Personal Grooming and Hygiene: Heightened awareness around personal grooming and oral hygiene is a primary market driver. Consumer expenditure on personal care products has consistently grown at above-inflation rates across mature markets since 2021. Social media beauty content has directly influenced grooming behavior, accelerating product adoption among 18-35-year-old demographics globally. Male consumers are increasingly inclined toward beard grooming and hairstyling, enhancing demand for shavers and trimmers specifically.

- Rapid Urbanization and Growing Middle-Class Income: Urban consumers consistently outspend rural counterparts on personal care appliances. The economic expansion translates directly into higher expenditure on lifestyle and grooming products, particularly in Asia Pacific, Latin America, and the Middle East and Africa.

- Expanding E-Commerce and Omnichannel Retail Penetration: E-commerce platforms have transformed product accessibility and consumer discovery. Online distribution channels for personal care appliances grew significantly post-2020, with platforms such as Amazon, Flipkart, and Tmall driving volume sales. Direct-to-consumer (D2C) brands leveraging digital marketing are capturing incremental market share from traditional retail channels, particularly in North America and Europe.

- Product Innovation in Heat-Free and Smart Technologies: Investment in R&D for ionic, infrared, and AI-enabled devices has expanded the premium product tier. Manufacturers including Dyson and Philips have launched smart hair care devices with app connectivity, personalized heat settings, and damage-reduction technologies. Product manufacturers are also developing budget-friendly variants for all age groups, broadening the addressable consumer base across income segments.

Market Restraints

- High Replacement Costs in Price-Sensitive Markets: Premium personal care appliances carry price points that remain prohibitive for a significant portion of consumers in developing markets. Replacement cycles of 3-5 years for primary devices reduce the addressable market for premium tier products in price-sensitive geographies, limiting penetration depth in high-potential emerging markets.

- Competition from Counterfeit and Low-Quality Products: The proliferation of counterfeit and unbranded low-cost appliances, particularly in Asia Pacific and Latin America, creates pricing pressure and erodes volume growth potential for established brands. Counterfeit products raise consumer safety concerns, potentially suppressing category adoption and damaging consumer trust in the broader personal care appliance market.

Market Opportunities

- AI-Personalized and Smart Connected Grooming Appliances: The integration of AI, IoT connectivity, and companion mobile applications into personal care appliances represents a significant growth opportunity. Smart devices capable of providing personalized recommendations, monitoring usage patterns, and connecting to health platforms are positioned to command premium pricing and drive new product adoption cycles through 2034.

- Untapped Potential in Emerging Market Penetration: India, Southeast Asia, and Sub-Saharan Africa represent substantially under-penetrated markets for personal care appliances. Rising internet penetration, expanding organized retail infrastructure, and growing awareness of personal hygiene products create significant addressable market expansion opportunities for established and emerging brands.

Market Challenges

- Regulatory Compliance Complexity Across Geographies: Manufacturers face diverse and evolving regulatory requirements including CE marking in Europe, UL certification in North America, and BIS certification in India. Compliance complexity increases product development timelines and costs, creating challenges for smaller market entrants seeking to scale internationally.

- Supply Chain Volatility and Component Availability: The market's dependence on semiconductor chips, micro-motor components, and lithium-ion battery cells creates exposure to supply disruptions. Component shortages experienced during 2021-2023 highlighted the sector's vulnerability to geopolitical factors, logistics disruptions, and single-source component dependencies that increase operational risk.

Emerging Market Trends

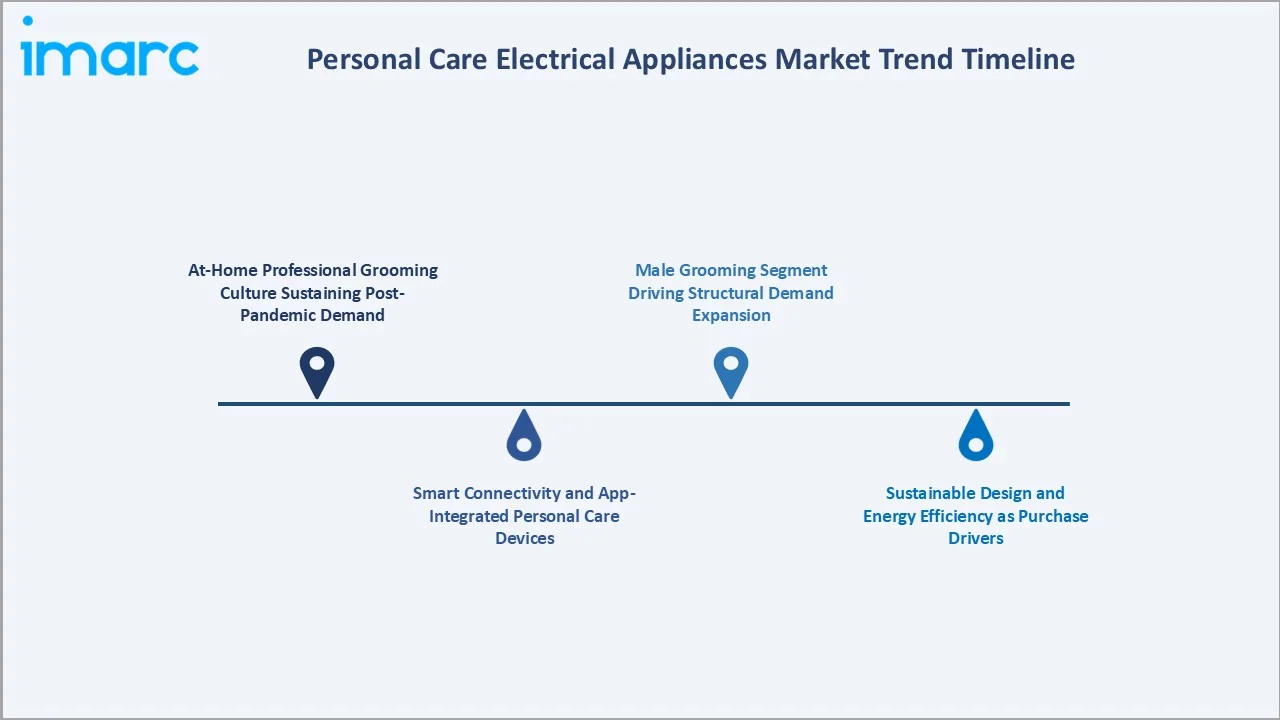

1. At-Home Professional Grooming Culture Sustaining Post-Pandemic Demand

The COVID-19 pandemic established at-home grooming as a mainstream consumer behavior, and this shift has proven durable beyond restrictions. Consumers continue to invest in professional-grade appliances, directly benefiting premium hair care and hair removal appliance categories. Product manufacturers are increasingly launching professional-tier devices targeted at home users, blurring the boundary between salon and household appliance segments.

2. Smart Connectivity and App-Integrated Personal Care Devices

Manufacturers are embedding Bluetooth and Wi-Fi connectivity in premium devices, enabling app-based personalization, usage analytics, and maintenance reminders. Dyson's Airwrap i.d. hair dryer with companion app and Philips Sonicare with built-in pressure sensor represent early market leaders in the connected device segment. Smart device penetration within the premium tier is expected to reach approximately 30% by 2030.

3. Male Grooming Segment Driving Structural Demand Expansion

The male personal care appliances segment is among the fastest-growing within the broader market. Evolving male grooming attitudes, beard styling trends, and increased focus on personal appearance are driving robust demand for trimmers, shavers, and multi-function grooming kits. The structural expansion of the global male grooming market directly accelerates hair removal appliance segment growth through 2034.

4. Sustainable Design and Energy Efficiency as Purchase Drivers

Environmental sustainability is transitioning from a niche preference to a mainstream purchase consideration. EU Ecodesign Directive requirements are mandating energy efficiency improvements, while consumer demand for environmentally responsible products is encouraging brands to innovate in materials, packaging, and energy consumption, particularly among European and North American millennials.

5. Direct-to-Consumer and Subscription Model Expansion

Emerging D2C brands and established manufacturers are exploring subscription-based models for replacement heads, cartridges, and accessories - creating recurring revenue streams while deepening consumer relationships. Oral-B and Philips Sonicare have pioneered this model in oral care, with broader application expected across hair care categories through 2034.

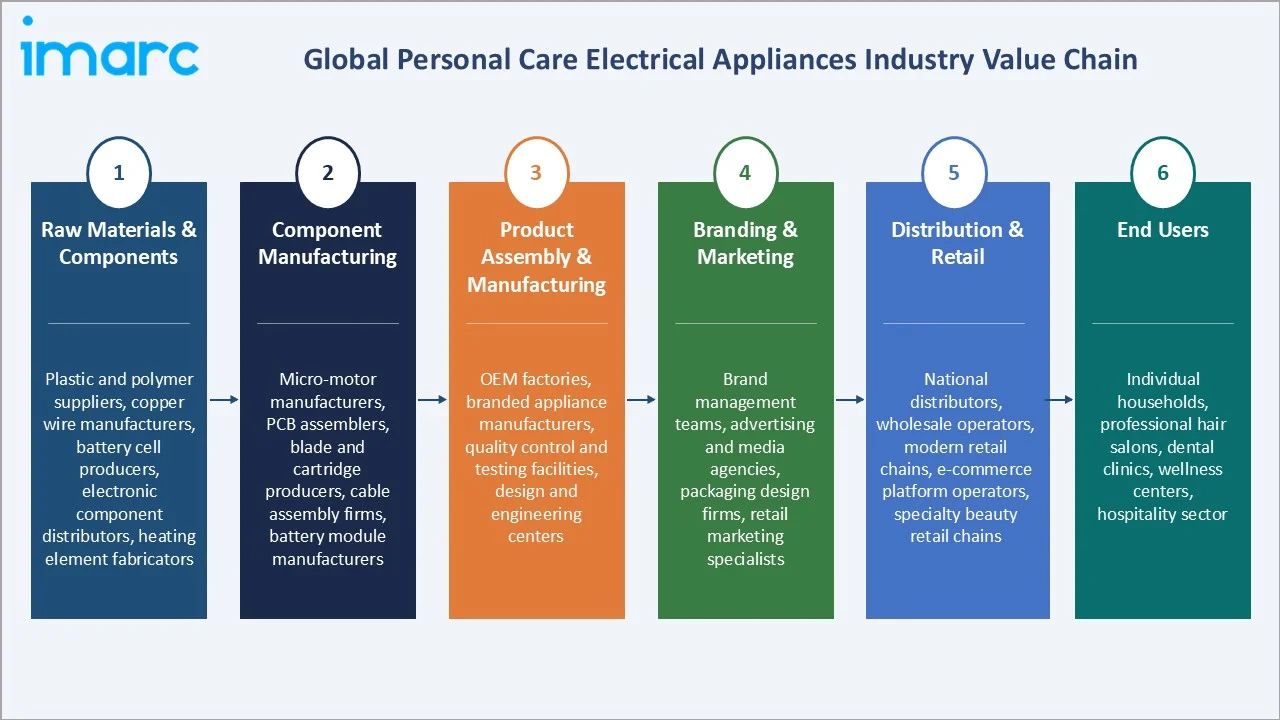

Industry Value Chain Analysis

The personal care electrical appliances value chain integrates raw material and component sourcing, component manufacturing, product assembly and brand integration, marketing and channel management, distribution and retail execution, after-sales services, and diverse end-user consumption. Each stage creates distinct competitive differentiation opportunities for market participants.

|

Stage |

Key Participants |

|

Raw Materials & Components |

Plastic and polymer suppliers, copper wire manufacturers, battery cell producers, electronic component distributors, heating element fabricators |

|

Component Manufacturing |

Micro-motor manufacturers, PCB assemblers, blade and cartridge producers, cable assembly firms, battery module manufacturers |

|

Product Assembly & Manufacturing |

OEM factories, branded appliance manufacturers, quality control and testing facilities, design and engineering centers |

|

Branding & Marketing |

Brand management teams, advertising and media agencies, packaging design firms, retail marketing specialists |

|

Distribution & Retail |

National distributors, wholesale operators, modern retail chains, e-commerce platform operators, specialty beauty retail chains |

|

End Users |

Individual households, professional hair salons, dental clinics, wellness centers, hospitality sector |

The manufacturing and brand integration stage represents the highest value-add phase of the personal care electrical appliances value chain. Component quality, technology integration, and product safety certification create the primary competitive differentiation at this stage. Distribution channel management - particularly the balance between online and offline channel strategies - determines market penetration depth and brand visibility.

Technology Landscape in the Personal Care Electrical Appliances Industry

Advanced Motor and Heating Element Technology

High-speed brushless motors, now capable of rotating at up to 110,000 rpm in premium hair dryers, represent a significant technological advancement enabling faster drying with lower heat exposure. Infrared and ionic heating technologies reduce moisture loss and minimize thermal damage to hair structures, directly addressing key consumer concerns over prolonged device use and improving outcomes for color-treated and chemically processed hair.

Smart Connectivity and AI Integration

Bluetooth Low Energy (BLE) and Wi-Fi connectivity embedded in premium appliances enable companion app integration for personalized usage data, maintenance reminders, and product recommendations. AI algorithms in emerging smart devices analyze hair or skin type through sensor data, adjusting device settings in real time to optimize grooming outcomes while minimizing damage risk and energy consumption.

Battery Technology and Wireless Charging Advances

Lithium-ion battery improvements, including higher energy density cells and fast-charging capabilities, have significantly extended cordless appliance usability. Products such as electric shavers and oral irrigators now offer 60+ minute run times with 1-hour charge cycles. Wireless charging integration is emerging in premium oral care and hair care devices, improving user convenience and reducing cable dependency.

Sustainable Materials and Eco-Engineering

Manufacturers are incorporating recycled plastics, bio-based polymers, and reduced precious metal content into product designs. Energy-efficient certified appliances and EU Ecodesign-compliant products are gaining market share in environmentally regulated markets. Refillable cartridge systems for electric shavers and rechargeable toothbrush head subscription models are reducing lifecycle waste and building recurring revenue for leading brands.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Hair Care Appliances |

39.4% |

2025 |

|

Type |

Battery Operated |

57.6% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North America |

34.8% |

2025 |

By Product

Hair care appliances lead the product segmentation at 39.4% (2025). The segment encompasses hair dryers, straighteners, curlers, and multi-function styling tools. Universal demand for hair drying and styling devices across all consumer demographics, combined with continuous product innovation in ionic and heat-free technologies, sustains this segment's market leadership. Hair removal appliances follow at 31.2%, driven by male grooming culture expansion and growing adoption of epilators and skin-safe trimmers among female consumers.

To access detailed market analysis, Request Sample

Oral care appliances at 18.7% represent the fastest-growing sub-segment (~5.2% CAGR), underpinned by rising dental hygiene awareness globally. Electric toothbrush household penetration remains low in many developing markets, representing a significant long-term growth runway. The Others segment at 10.7% encompasses skin care devices, massagers, and body grooming appliances, which are gaining traction through cross-category consumer interest in home beauty technology.

By Type

Battery-operated devices lead the type segmentation at 57.6% (2025). Advances in lithium-ion battery technology have extended run times significantly, resolving earlier consumer concerns over battery life and making cordless devices the preferred choice across all hair care, hair removal, and oral care categories. The growth of travel-specific product lines and compact grooming kits has further reinforced battery-operated device preference among mobile, urban consumers.

Electric (corded) devices retain 42.4% of the type segment, primarily in categories where high power output is essential - particularly professional-grade hair dryers and high-performance straighteners. Corded devices maintain a performance advantage in salon and professional settings, sustaining demand within the B2B and premium home consumer segments through 2034.

Regional Market Insights

|

Region |

Share (2025) |

Key Personal Care Electrical Appliances Market Drivers & Characteristics |

|

North America |

34.8% |

Driven by mature grooming culture, high per-capita consumer spending, strong e-commerce infrastructure, and premium brand penetration across the United States and Canada. |

|

Europe |

25.7% |

Driven by EU Ecodesign regulations creating sustainable product demand, high oral care appliance adoption, strong brand penetration by Philips and Braun, and premium market positioning. |

|

Asia Pacific |

24.9% |

Driven by urbanization, rising disposable incomes, expanding female workforce participation, growing oral hygiene awareness, and a large under-penetrated consumer base in India and Southeast Asia. |

|

Latin America |

8.1% |

Supported by growing organized retail infrastructure, rising grooming awareness among urban consumers, and expanding middle-class consumer base in Brazil and Mexico. |

|

Middle East & Africa |

6.5% |

Driven by premium grooming product adoption in GCC states, growing wellness and personal care culture, and expanding e-commerce penetration across the region. |

North America's 34.8% regional leadership is supported by the United States market's high grooming product penetration rates and the dominance of established brands including Conair, Remington, and Andis in the mass and mid-market tiers, alongside the premium positioning of Oral-B and Philips Sonicare in oral care. The region's robust e-commerce infrastructure and prevalence of subscription-based oral care models further sustain volume and value growth.

Asia Pacific (24.9%) is the region with the highest incremental growth potential through 2034. China represents the largest single-country market within the region, with rising urban professional demographics driving premium appliance adoption. India is the fastest-growing national market, supported by expanding organized retail, growing e-commerce penetration, and rising consumer spending on personal care products.

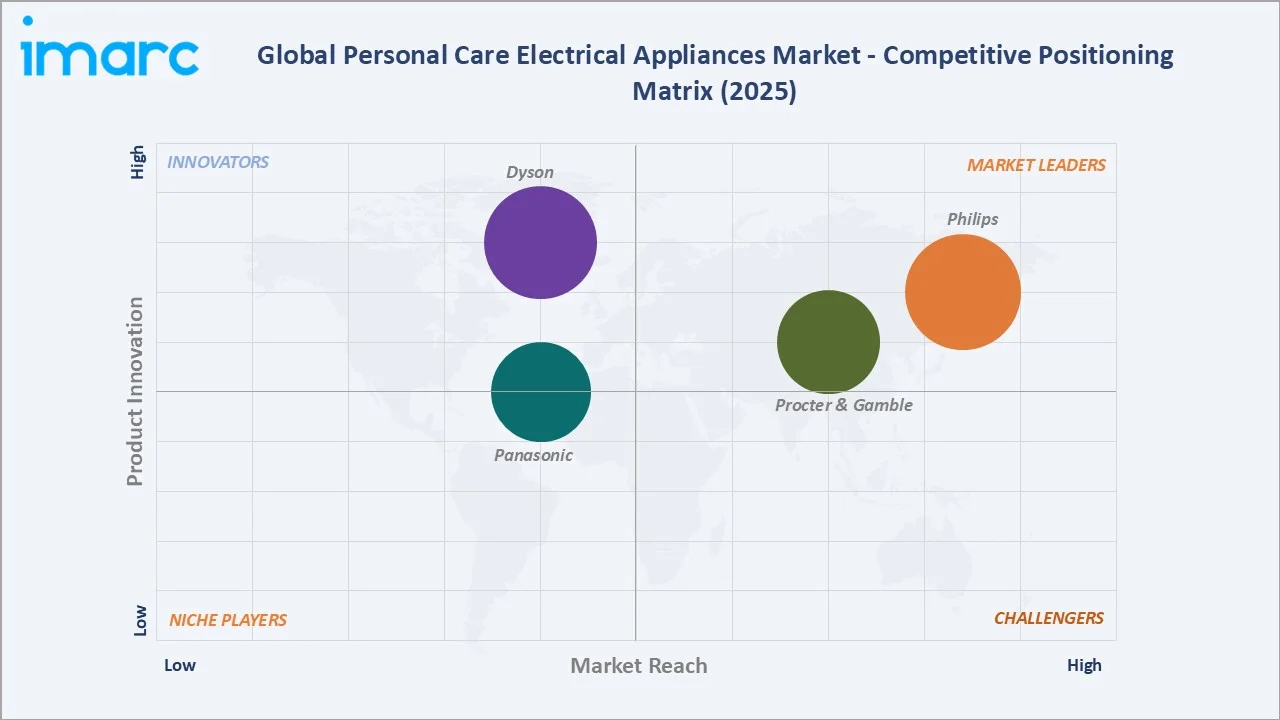

Competitive Landscape

The global personal care electrical appliances market features a highly competitive landscape dominated by multinational consumer electronics and personal care conglomerates, alongside strong regional players and a growing number of D2C disruptors. Philips, Procter & Gamble, Dyson, and Panasonic collectively hold significant market share across multiple product categories. Competitive differentiation is increasingly driven by technology innovation, brand equity, digital marketing capabilities, and e-commerce execution strength.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Philips |

Electric Beard Trimmers & Multi Grooming Kits, Shavers, Hair Styling Appliances, Body Groomers |

Market Leader |

Philips plays a central role by providing a broad personal care appliance portfolio combining advanced technology, clinical endorsements, and global distribution across 100+ markets. |

|

Procter & Gamble |

Electric Shavers & Groomers, Trimmers & Styling, Toothbrushes |

Market Leader |

Operates Braun and Oral-B, which plays a central role through premium brand equity, technology leadership in shaving and oral care categories, and deep distribution across retail and e-commerce channels globally. |

|

Dyson |

Electric Hair Straightener, Hair Dryer, Hair Styler |

Innovator |

Dyson plays a central role through engineering differentiation, premium ASP positioning, disruptive product design, and a strong direct-to-consumer digital sales model. |

|

Panasonic |

Electric Hair Dryers and Stylers, Shavers, Toothbrushes |

Established Player |

Panasonic plays a central role through Japanese engineering quality, broad product range across hair care and hair removal, and a strong distribution footprint in Asia Pacific. |

The competitive landscape is characterized by intensifying investment in smart device technology and premium positioning, with market leaders leveraging R&D capabilities and established brand equity to defend market share against emerging D2C disruptors. Consolidation is increasing through strategic acquisitions targeting technology capabilities, particularly in smart connectivity, AI, and sustainable design. Regional players maintain positions in price-sensitive market segments in Asia Pacific and Latin America.

Key Company Profiles

Philips

Philips is a global leader in personal care electrical appliances, offering a comprehensive portfolio spanning oral care, hair care, hair removal, and skin care device categories. The company is headquartered in Amsterdam, Netherlands, and operates across more than 100 countries, leveraging its HealthTech positioning to differentiate products through clinical validation and digital health integration.

- Key Products: Electric Beard Trimmers & Multi Grooming Kits, Shavers, Hair Styling Appliances, Body Groomers, and others.

- Recent Developments: In October 2025, Philips India launched Philips OneBlade Intimate, a unisex grooming device made for sensitive zones.

- Strategic Focus: Philips focuses on premium positioning, clinical efficacy endorsements, digital health integration, and expanding its connected device ecosystem. The company prioritizes sustainable product design under its ESG commitments, including energy-efficient product certification and recyclable packaging across its personal care appliance portfolio.

Procter & Gamble

Procter & Gamble is a premier personal care appliance company and owns two major personal care equipment brands, Braun (grooming) and Oral-B (oral care).

- Key Products: Electric Shavers & Groomers, Trimmers & Styling, Toothbrushes, and others.

- Recent Developments: In January 2025, P&G’s oral care brand, Oral-B launched its Oral-B iO Series 2 (iO2), which is designed to deliver 150% more plaque removal in difficult-to-reach areas of the mouth.

- Strategic Focus: P&G concentrates on technology leadership in shaving and oral care, premium market positioning, smart device ecosystem development, and leveraging global consumer insights and retail distribution capabilities to maintain category leadership in grooming and oral care appliance segments.

Market Concentration Analysis

The global personal care electrical appliances market is moderately concentrated at the brand tier, with the top players - Philips, Procter & Gamble, Dyson, and Panasonic - collectively accounting for an estimated 45-55% of global market revenue (2025). Market concentration varies significantly by product sub-segment, with oral care appliances being the most concentrated and hair care appliances being the most fragmented due to the large number of regional and private-label brands competing at mid-to-low price points.

The hair care appliance sub-segment reflects the highest fragmentation level, with a long tail of regional brands, private-label manufacturers, and D2C startups capturing meaningful market share in price-sensitive segments. No single company holds above 15% of the total hair care appliance market globally, though Philips and Dyson lead in value terms within the premium tier. In contrast, the electric toothbrush segment within oral care is substantially more concentrated, with Oral-B (P&G) and Philips Sonicare collectively controlling approximately 70-75% of the premium electric toothbrush market globally (2025).

Market concentration is increasing at the premium technology platform tier through strategic M&A, partnership activity, and organic investment in smart device capabilities. Companies acquiring digital platform and AI competencies are consolidating competitive advantages. The D2C channel has created a structural pathway for emerging brands to bypass traditional retail concentration barriers, leading to rising competitive fragmentation at the lower-to-mid price tier. Overall, market concentration trends suggest continued bifurcation: increasing consolidation among premium and technology-differentiated products, alongside sustained fragmentation at the mass-market price tier.

Investment & Growth Opportunities

Highest Growth Segments

Oral care appliances (~5.2% CAGR), battery-operated multi-function grooming kits (~5.1% CAGR), and AI-integrated smart hair care devices represent the highest-growth investment vectors through 2034. The oral irrigator sub-segment within oral care is growing particularly rapidly, driven by dental professional recommendations and mainstream retail expansion. Smart connected personal care devices, growing from a smaller base, are expected to generate the highest incremental revenue opportunity within the premium tier through 2034.

Emerging Investment Opportunities

India, Indonesia, Vietnam, and Sub-Saharan Africa represent significantly under-penetrated markets with rapidly improving addressable market conditions. Rising internet penetration, expanding organized retail presence, and growing consumer awareness of personal hygiene create compelling market entry windows. Companies establishing distribution and brand presence in these markets through 2025-2028 are positioned for above-market returns as consumer income levels rise.

Investment Themes

- Smart and AI-enabled device development: Investing in AI-personalization capabilities and connected device ecosystems to command premium price points and build recurring consumer relationships through companion apps and subscription services for replacement consumables.

- Sustainability-focused product innovation: Developing energy-efficient, recyclable-material-based appliances to capture the growing eco-conscious consumer segment, particularly in Europe and North America, which increasingly accepts a price premium for sustainable products.

- D2C and subscription model expansion: Building direct-to-consumer digital channels and subscription-based models for consumables - replacement heads, cartridges, blades - to establish recurring revenue streams and reduce dependence on traditional retail distribution margins.

- Emerging market distribution infrastructure: Investing in localized distribution partnerships, price-accessible product tiers, and targeted brand awareness campaigns to capture structural demand growth in Asia Pacific, Latin America, and the Middle East and Africa regions through 2034.

Future Market Outlook (2026-2034)

The global personal care electrical appliances market is projected to grow from USD 25.15 Billion in 2025 to USD 37.57 Billion by 2034, delivering a 4.42% CAGR over the forecast period. The market's anchor value of USD 31.23 Billion in 2030 reflects the structural momentum of urbanization, rising incomes, and technology-driven product premiumization. By 2034, smart-connected devices are expected to represent approximately 25-30% of total market value in the premium consumer segment.

Three structural forces define the market outlook through 2034. First, sustained global urbanization, particularly in Asia Pacific and Africa, will broaden the addressable consumer base by hundreds of millions of new urban grooming consumers. Second, technology-driven premiumization will expand average selling prices and revenue per unit as AI, IoT, and advanced material innovations differentiate product tiers and create new category entry points. Third, the mainstreaming of oral care appliances, still at relatively low household penetration rates in many developing markets, provides a structural growth engine within the broader market.

Key milestones anticipated through 2034 include: smart device penetration reaching approximately 30% of premium segment value by 2030; oral care appliances surpassing 22% product share by 2034 through continued electric toothbrush adoption; and Asia Pacific overtaking Europe in absolute market share by approximately 2031, reflecting the region's above-market CAGR trajectory and structural demographic tailwinds.

Research Methodology

Primary Research

Primary research comprised structured interviews with 60+ industry stakeholders (2025-2026) including product R&D directors at leading appliance manufacturers, category managers at major retail chains, brand strategists at personal care conglomerates, and regional distribution executives. Consumer panel surveys spanning North America, Europe, and Asia Pacific were conducted to validate purchasing behavior trends and price sensitivity data across key demographics.

Secondary Research

Secondary research encompassed publicly available government statistics from the U.S. Bureau of Economic Analysis, Eurostat, and India's Ministry of Statistics; company annual reports, investor presentations, and press releases from Philips, Procter & Gamble, Dyson, and Panasonic; industry association publications; retail channel data; and patent filing databases. Over 70 secondary sources were reviewed and validated for quality and recency.

Forecasting Models

Market revenue forecasts were developed using a bottom-up approach segmented by product category, type, distribution channel, and geography. Historical growth rates (2020-2025), macroeconomic indicators, industry capacity data, and expert interviews formed the basis of forecast assumptions. Scenario analysis encompassing base, optimistic, and conservative growth trajectories was conducted to validate the CAGR estimates presented in this report.

Personal Care Electrical Appliances Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Hair Care Appliances, Hair Removal Appliances, Oral Care Appliances, and Others |

| Types Covered | Electric, Battery Operated |

| Distribution Channels Covered | Online, Offline |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Philips, Procter & Gamble, Dyson, Panasonic, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Personal Care Electrical Appliances Market Report

The market reached USD 25.15 Billion in 2025, driven by rising grooming awareness, urbanization, product innovation, and expanding e-commerce channels globally. It is projected to reach USD 37.57 Billion by 2034.

The market grows at 4.42% CAGR during 2026-2034. Oral care appliances grow fastest at approximately 5.2% CAGR, followed by battery-operated devices at approximately 5.1% CAGR.

Hair care appliances lead with 39.4% market share (2025), driven by universal demand for hair dryers, straighteners, curlers, and multi-function styling tools across all consumer demographics.

Battery-operated devices dominate at 57.6% (2025), reflecting consumer preference for cordless convenience, travel-friendly design, and significantly improved lithium-ion battery run times.

North America leads with 34.8% (2025), supported by mature grooming culture, high per-capita spending, strong brand penetration, and robust e-commerce infrastructure across the United States.

Asia Pacific is the fastest-growing region, driven by urbanization, rising disposable incomes, expanding female workforce participation, and large under-penetrated consumer bases in India and Southeast Asia.

Leading companies include Philips, Procter & Gamble, Dyson, and Panasonic, among others competing across global and regional consumer market tiers.

The market is projected to reach USD 31.23 Billion by 2030, with smart connected devices and oral care appliances representing the highest incremental revenue contributors to market growth.

Key drivers include rising grooming awareness, urbanization, e-commerce expansion, product innovation in smart and heat-free technologies, growing male grooming culture, and increasing female workforce participation.

The market was valued at USD 20.26 Billion in 2020. Growth through 2025 was supported by at-home grooming adoption during COVID-19 and sustained post-pandemic behavioral change in consumer grooming habits.

Key trends include AI-personalized smart devices, sustainable eco-friendly design, male grooming expansion, D2C subscription model growth, app-connected appliances, and premiumization of oral care products.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)