Pre-Engineered Building Market Size, Share, Trends and Forecast by Product, End-User, and Region, 2026-2034

Global Pre-Engineered Building Market Size, Share, Trends & Forecast (2026-2034)

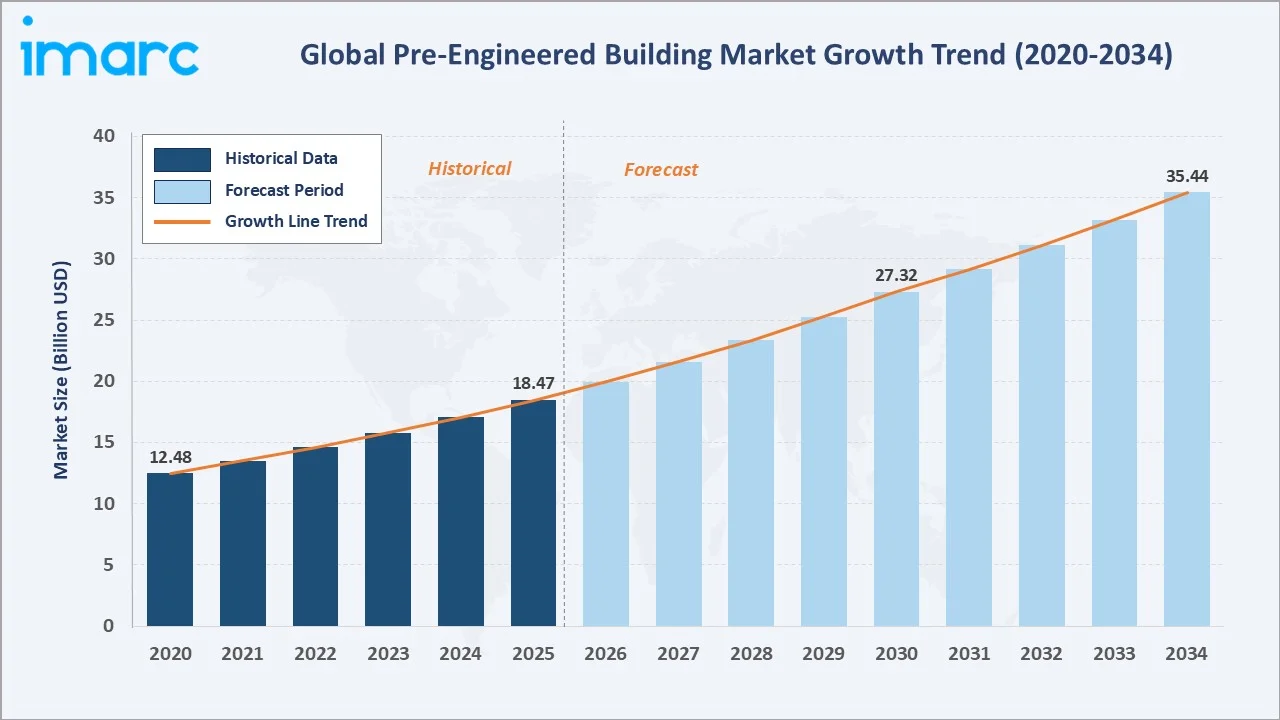

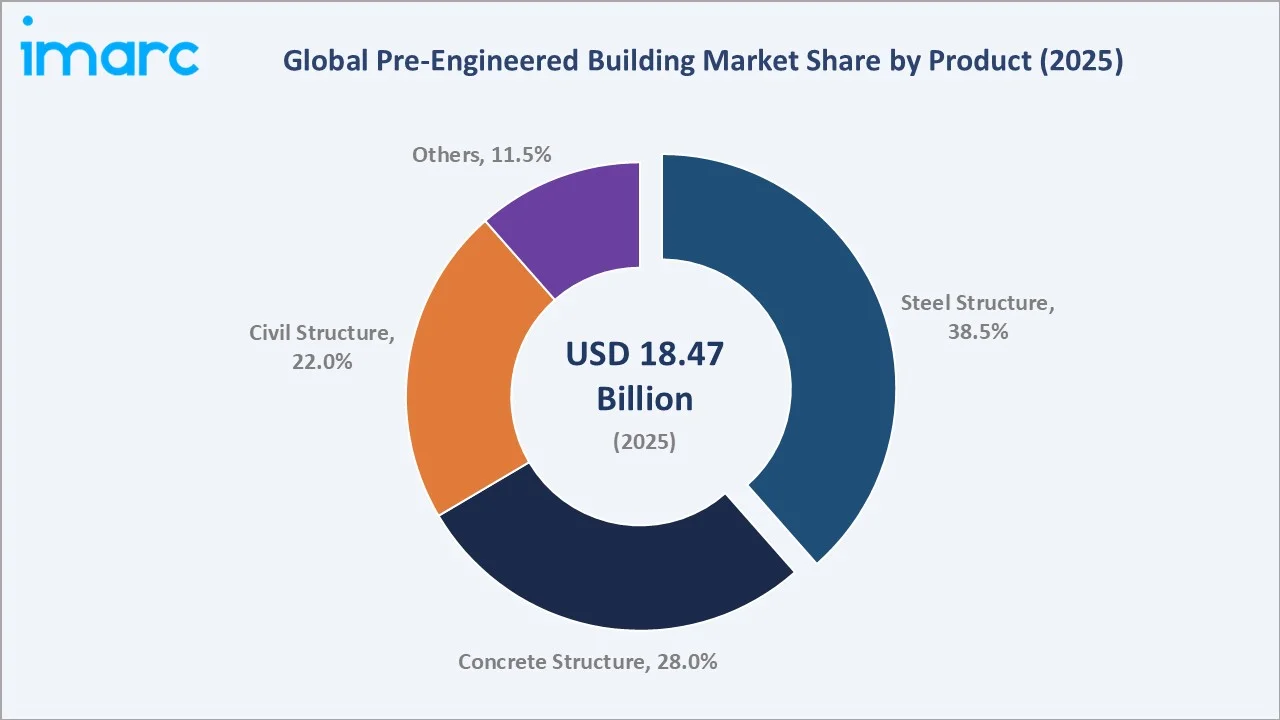

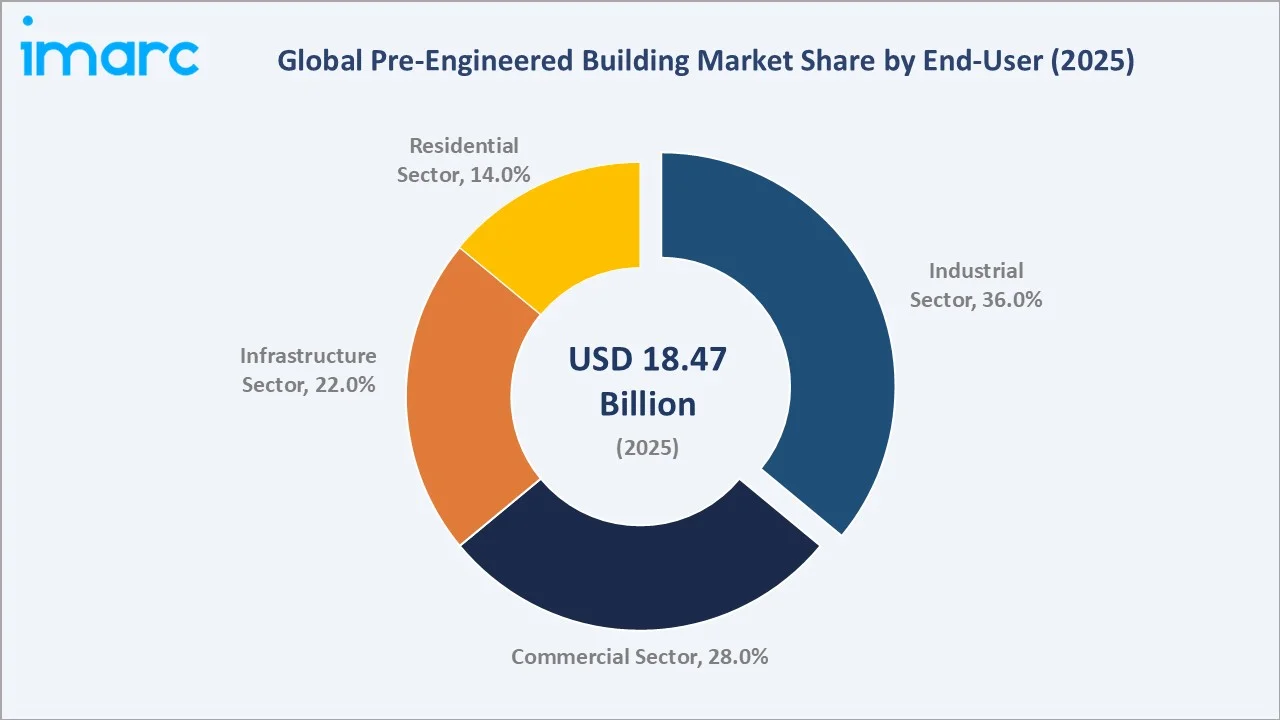

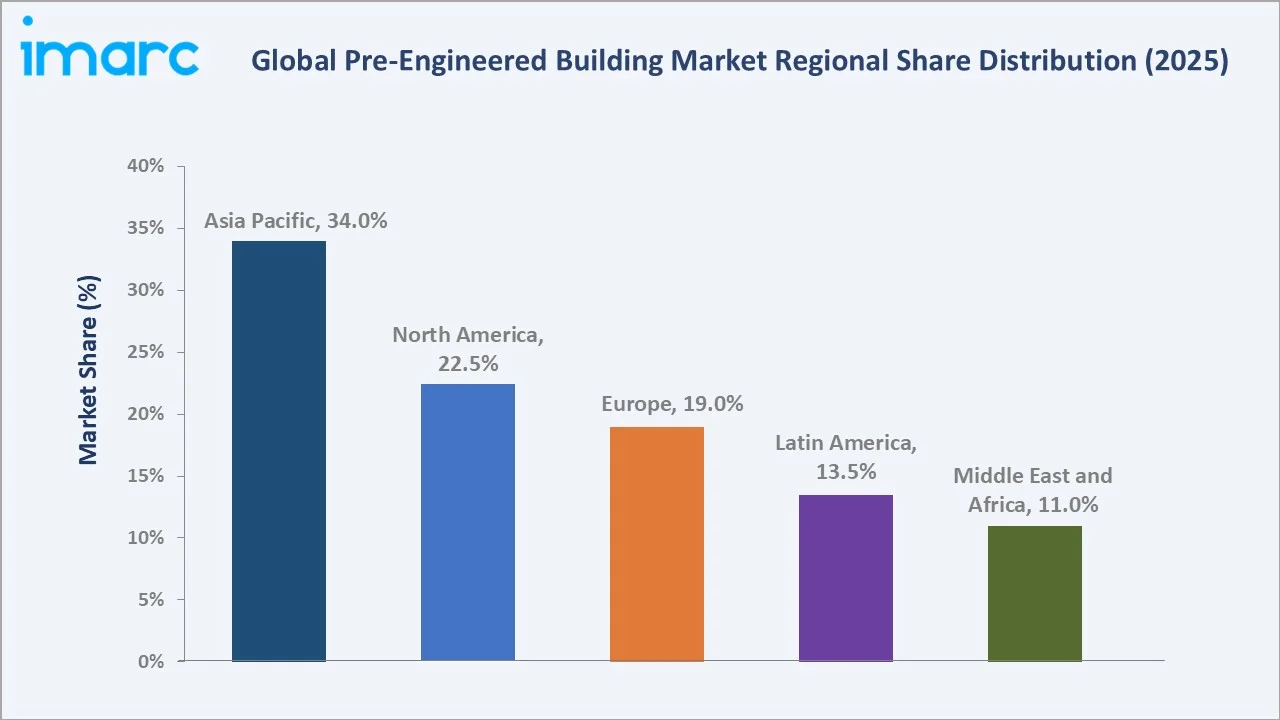

The global pre-engineered building market size was valued at USD 18.47 Billion in 2025 and is projected to reach USD 35.44 Billion by 2034, at a CAGR of 8.15% during 2026-2034. Rapid urbanization, expanding industrial and commercial construction activity, and strong e-commerce-driven warehouse demand are the primary forces propelling market growth. Steel Structure leads product segments with a 38.5% share in 2025, while the Industrial Sector dominates end-user demand at 36.0%. Asia Pacific is both the largest and fastest-growing region, holding 34.0% of global revenue in 2025, underpinned by India's infrastructure expansion and China's manufacturing growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 18.47 Billion |

|

Forecast Market Size (2034) |

USD 35.44 Billion |

|

CAGR (2026-2034) |

8.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (34.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Largest Product Segment |

Steel Structure (38.5%, 2025) |

|

Largest End-User Segment |

Industrial Sector (36.0%, 2025) |

The chart shows the global pre-engineered building market’s growth from 2020 to 2034, highlighting post-2020 recovery and strong projected expansion during the forecast period.

To get more information on this market, Request Sample

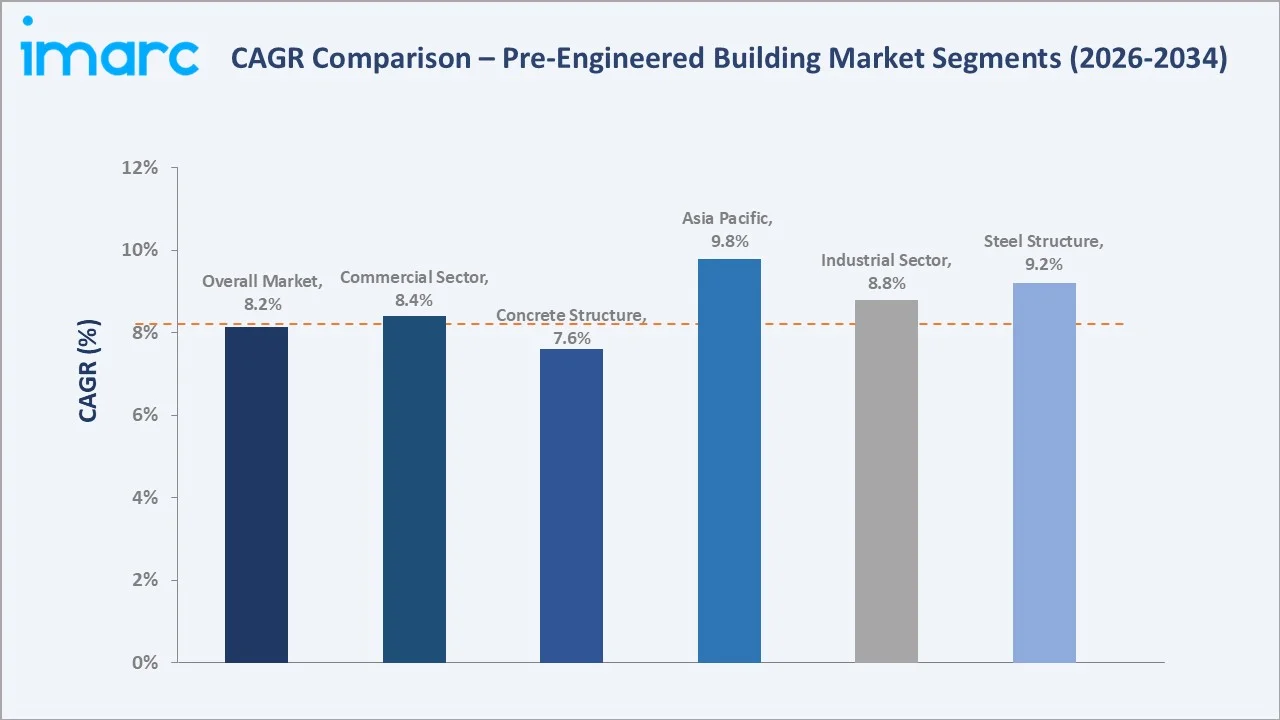

CAGR analysis confirms Asia Pacific and Steel Structure as the highest-growth segments, with the overall market sustained at 8.15% through 2034.

Executive Summary

The global pre-engineered building market is experiencing strong growth driven by rapid urbanization, expanding e-commerce warehousing, and increasing demand for cost-efficient, sustainable construction. Valued at USD 18.47 Billion in 2025, the market is projected to reach USD 35.44 Billion by 2034, growing at a CAGR of 8.15%. Rising construction of manufacturing facilities, logistics hubs, airports, and commercial buildings is further accelerating adoption across key sectors globally.

Steel Structure leads the product segment with a 38.5% share in 2025, driven by recyclability, faster installation, and cost efficiency. The Industrial sector accounts for 36.0% of demand, supported by manufacturing expansion and warehouse development. Key trends include BIM-based design, automated fabrication, green certifications, and IoT-enabled smart building integration.

Asia Pacific leads with a 34.0% share in 2025, driven by India’s National Infrastructure Pipeline and China’s industrial expansion. North America holds 22.5% due to strong commercial and industrial construction, while Europe accounts for 19.0%, supported by sustainability-driven prefabrication demand. By 2034, the market is expected to nearly double from its 2025 base, creating opportunities in innovation, regional expansion, and end-user diversification.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Steel Structure – 38.5% share (2025) |

|

Second Product Segment |

Concrete Structure – 28.0% share (2025) |

|

Leading End-User Segment |

Industrial Sector – 36.0% share (2025) |

|

Leading Region |

Asia Pacific – 34.0% revenue share (2025) |

|

Second Region |

North America – 22.5% revenue share (2025) |

|

Top Companies |

Zamil Steel, BlueScope Steel, Kirby Building Systems, Nucor, Everest Industries |

Key Analytical Observations Supporting The Above Data:

- Steel Structure's 38.5% dominance in 2025 is driven by 20–35% lower costs than reinforced concrete, along with 100% recyclability and strong alignment with LEED and other green building standards.

- Concrete Structure’s 28.0% share in 2025 is supported by its use in heavy industrial and infrastructure projects requiring high fire resistance, thermal stability, and strong load-bearing capacity.

- The Industrial sector’s 36.0% share reflects rising demand for manufacturing plants, cold storage, and logistics hubs, with Asia Pacific leading new pre-engineered building projects.

- Asia Pacific’s 34.0% revenue leadership in 2025 is driven by India’s ₹111 lakh Crore National Infrastructure Pipeline during the period 2020-2025 and China’s ongoing industrial park and SEZ development.

- North America’s 22.5% share in 2025 is driven by U.S. manufacturing reshoring and large-scale data center construction, where steel pre-engineered buildings enable faster deployment and scalability.

- Zamil Steel and BlueScope Steel are among the leading pre-engineered building manufacturers, with Zamil Steel exceeding 500,000 metric tonnes capacity, reinforcing their global leadership.

Global Pre-Engineered Building Market Overview

Pre-engineered buildings are factory-fabricated structural systems transported and assembled on-site. The value chain includes raw material suppliers, design and engineering firms, manufacturers, logistics providers, and erection contractors. These buildings are widely used in industrial facilities, warehouses, airports, commercial complexes, educational institutions, and residential developments due to speed and cost efficiency.

Macroeconomic trends such as urbanization, e-commerce growth, and infrastructure investment are driving market expansion. Pre-engineered buildings enable 30–40% faster construction than conventional methods, supporting time-sensitive projects. Increasing adoption of BIM and 3D design tools improves precision and customization, expanding applications across commercial, industrial, and other end-user segments.

Market Dynamics

To evaluate market opportunities, Request Sample

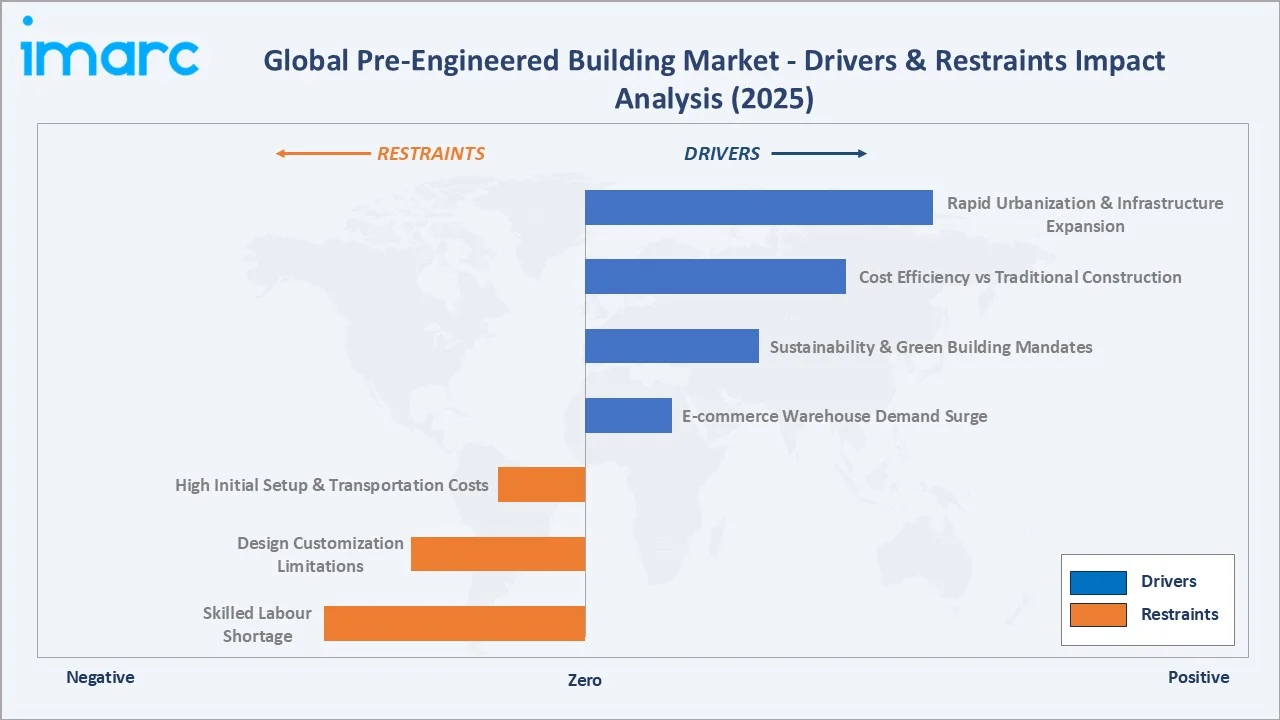

Market Drivers

- Rapid Urbanization and Infrastructure Development: The global urban population exceeded 4.4 billion in 2023 and is projected to reach nearly 7 in 10 people living in cities by 2050, driving construction growth. This is increasing pre-engineered building adoption, especially in Asia Pacific and Latin America, where urban expansion is most rapid.

- E-Commerce Warehouse and Logistics Center Demand: Global e-commerce sales surpassed 5.8 trillion Euros in 2024, boosting demand for large warehouses and distribution centers. Pre-engineered buildings are preferred for these facilities due to wide-span layouts and faster construction compared to traditional structures.

- Sustainability and Green Building Adoption: Government sustainability initiatives such as the EU Green Deal, India’s GRIHA, and LEED in North America are driving demand for low-carbon buildings. Steel pre-engineered buildings support this shift with up to 95% recyclable materials and reduced construction waste.

- Technological Advancements in Pre-engineered Building Design and Manufacturing: Adoption of BIM, 3D design software, and automated CNC fabrication is enhancing pre-engineered building quality, reducing waste, and enabling greater customization, expanding use in more complex construction applications.

Market Restraints

- High Initial Transportation and Logistics Costs: The prefabricated nature of pre-engineered buildings requires specialized transport of large components, which can increase project costs by around 10–15% in remote locations, limiting adoption in geographically challenging markets.

- Design Customization and Architectural Limitations: Standard pre-engineered building designs have limitations in supporting complex architecture, curved structures, and non-standard layouts, restricting their use in premium commercial and high-specification projects.

- Skilled Erection Labour Shortage: Pre-engineered building assembly requires skilled crews for steel connections and alignment. Labour shortages in developing markets can delay projects and increase erection costs.

Market Opportunities

- Asia Pacific Emerging Market Penetration: India’s ₹111 lakh crore infrastructure pipeline, Vietnam’s 400+ industrial zones expansion, and Indonesia’s growing special economic zones collectively represent major near-term pre-engineered building demand opportunities through 2030.

- Cold Chain and Data Center Infrastructure Expansion: Global cold chain expansion and accelerating data center construction are creating new demand for pre-engineered buildings, as steel structures offer wide spans, faster construction, and suitability for temperature-controlled and high-clearance facilities.

- Net-Zero Construction and Modular Building Integration: Rising demand for carbon-neutral construction is creating opportunities for solar-integrated, net-zero pre-engineered buildings using steel frames, photovoltaic roofing, and high-performance insulation systems.

Market Challenges

- Steel Price Volatility: Global structural steel prices surged sharply between 2020 and 2021, with increases exceeding 40–80% before correcting in 2022. Ongoing price volatility creates input cost uncertainty for pre-engineered building manufacturers operating under fixed-price contracts and multi-month delivery timelines.

- Competition from Modular and Conventional Construction: Growing adoption of modular construction and improved traditional building methods are increasing competition for pre-engineered buildings, especially in residential and premium commercial segments where design flexibility is critical.

- Regulatory Compliance Variability Across Markets: Differing seismic, wind, and fire safety standards across countries require design modifications, increasing engineering complexity and limiting standardization for globally active pre-engineered building manufacturers.

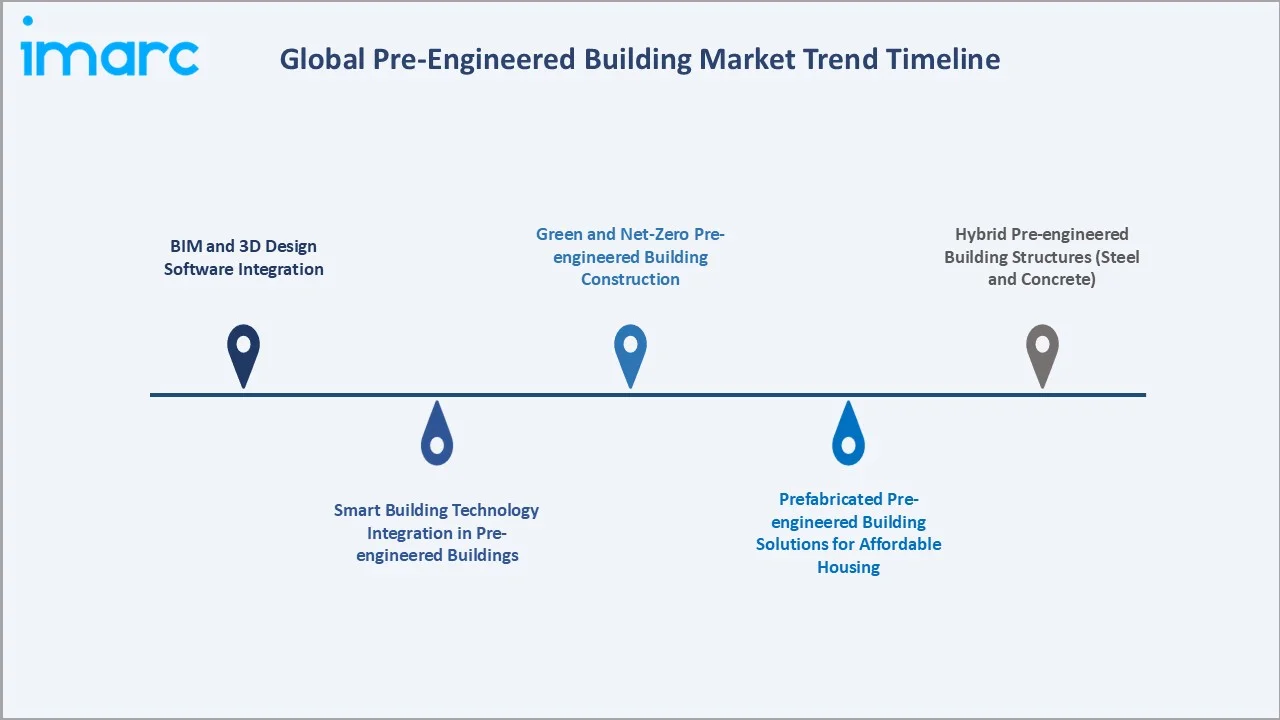

Emerging Market Trends

1. BIM and 3D Design Software Integration

BIM adoption is improving pre-engineered building design accuracy and collaboration through 3D visualization, clash detection, and material optimization. This reduces engineering rework by up to 25–30% and enhances on-site assembly precision, improving overall project efficiency.

2. Green and Net-Zero Pre-engineered Building Construction

Green certifications such as LEED, BREEAM, and GRIHA are influencing pre-engineered building procurement. Manufacturers offering solar-ready roofing, high-performance insulation, and recycled steel gain an advantage, especially among multinational clients with ESG and sustainability commitments.

3. Hybrid Pre-engineered Building Structures Combining Steel and Concrete

Demand for hybrid structures combining steel frames and concrete cores is rising in airports, transit hubs, and multi-storey industrial facilities. These designs combine steel’s speed with concrete’s strength and fire resistance, expanding pre-engineered building applications.

4. Smart Building Technology Integration in Pre-engineered Buildings

IoT sensors, automated HVAC, and building management systems are being integrated into pre-engineered building designs. Smart-ready buildings enable energy monitoring, predictive maintenance, and occupancy optimization, enhancing value for corporate and industrial clients focused on energy efficiency.

5. Prefabricated Pre-engineered Building Solutions for Affordable Housing

Affordable housing programs in India, Southeast Asia, and Africa are boosting residential pre-engineered building demand. Light-gauge steel prefabrication enables faster, cost-efficient construction, while India’s Pradhan Mantri Awas Yojana—targeting over 20 million homes—creates one of the largest residential opportunities globally.

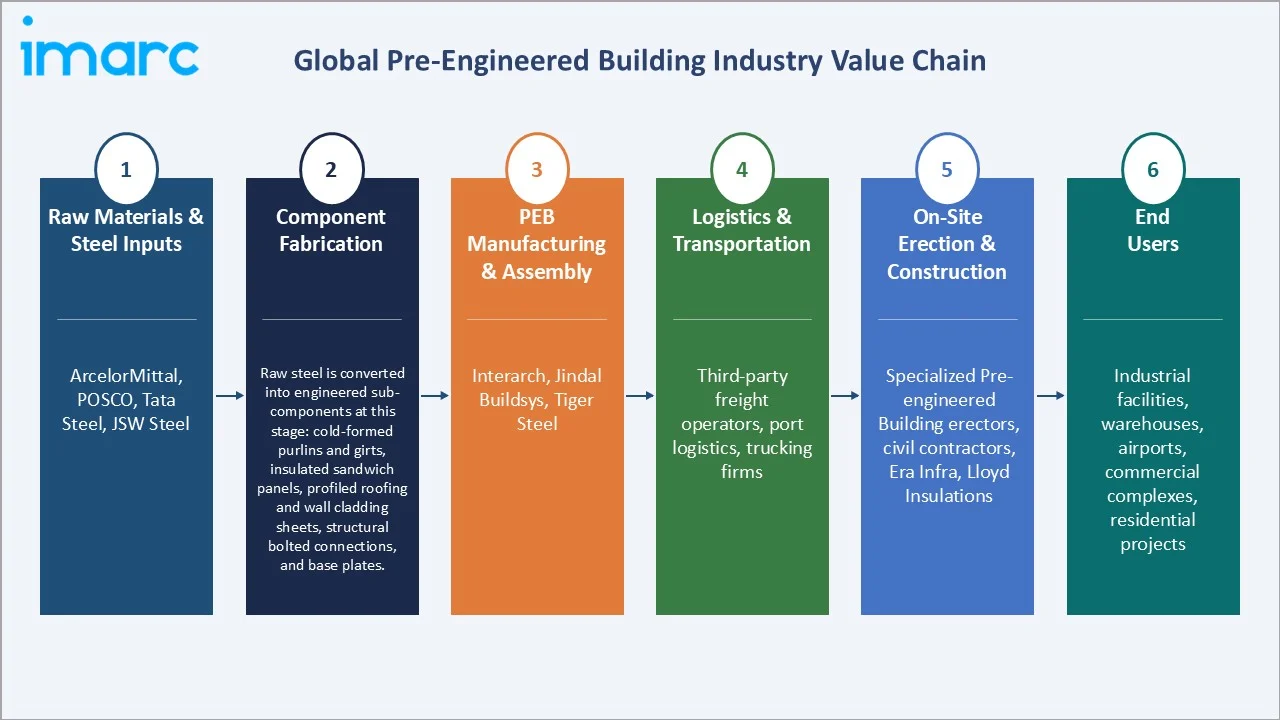

Industry Value Chain Analysis

The pre-engineered building value chain includes six interconnected stages, from raw material procurement to final facility delivery, each with unique competitive dynamics, margins, and operational complexities.

|

Stage |

Key Players / Description |

|

Raw Materials & Steel Inputs |

ArcelorMittal, POSCO, Tata Steel, JSW Steel |

|

Component Fabrication |

Raw steel is converted into engineered sub-components at this stage: cold-formed purlins and girts (Z- and C-sections), insulated sandwich panels, profiled roofing and wall cladding sheets, structural bolted connections, and base plates. |

|

Pre-engineered Building Manufacturing & Assembly |

Interarch, Jindal Buildsys, Tiger Steel Engineering. Activities include structural design using BIM and 3D modelling software, precision CNC cutting and welding of primary steel frames, factory quality control, and kitted packaging for site delivery. |

|

Logistics & Transportation |

Third-party freight operators, port logistics providers, trucking firms |

|

On-Site Erection & Construction |

Specialized Pre-engineered Building erectors, civil contractors, Era Infra, Lloyd Insulations |

|

End Users |

Industrial facilities, warehouses, airports, commercial complexes, residential projects |

Pre-engineered building manufacturers hold the highest value by combining design, fabrication, and project management. Vertically integrated players like Zamil Steel and Nucor Building Systems achieve stronger margins and competitive positioning by controlling operations from raw materials to erection support.

Technology Landscape in the Pre-Engineered Building Industry

BIM and Advanced 3D Design Software

Building Information Modeling platforms such as Autodesk Revit and Tekla Structures enable 3D modeling, automated material estimation, and fabrication-ready drawings. BIM adoption improves coordination and can reduce design rework and project timelines by around 20–30%, significantly enhancing pre-engineered building delivery efficiency.

Automated Steel Fabrication and CNC Manufacturing

Computer-controlled cutting, drilling, and welding are standard in Tier-1 pre-engineered building manufacturing. CNC-driven fabrication improves precision, reduces material waste compared to traditional construction, and increases production throughput, strengthening the cost competitiveness of steel pre-engineered buildings.

Smart Building and IoT Integration

Next-generation pre-engineered buildings increasingly incorporate IoT-ready designs, enabling integration of energy monitoring, automated HVAC, and building management systems. Manufacturers are partnering with smart building technology providers to deliver integrated, energy-efficient solutions for industrial and commercial clients.

Sustainable Materials Innovation

Advanced high-strength steel enables lighter structural members and reduced steel usage while maintaining load capacity. Meanwhile, insulated metal panel systems improve thermal performance and energy efficiency, lowering operational costs and supporting green building certification requirements in pre-engineered building applications.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Steel Structure | 38.5% | 2025 |

| End-User | Industrial Sector | 36.0% | 2025 |

| Region | Asia Pacific | 34.0% | 2025 |

By Product

Steel Structure dominates the global Pre-engineered Building market with a 38.5% share in 2025. Its high strength-to-weight ratio, recyclability, and fast assembly make it the preferred choice for industrial, commercial, and large-scale infrastructure projects.

To access detailed market analysis, Request Sample

Concrete Structure holds a 28.0% share in 2025, driven by heavy infrastructure, multi-storey industrial, and fire-sensitive applications. Civil Structure accounts for 22.0%, covering bridges and transit projects. Others represent 11.5%, including composite and hybrid systems, with growth expected as hybrid steel-concrete pre-engineered designs gain wider adoption.

By End-User

The Industrial Sector commands a 36.0% end-user share in 2025, driven by demand from manufacturing plants, warehouses, and cold storage facilities, with industrialization in Asia Pacific and reshoring in North America supporting continued growth.

The Commercial Sector holds a 28.0% share in 2025, including retail parks, offices, and mixed-use developments. Infrastructure accounts for 22.0%, covering airports, stations, and public facilities. Residential represents 14.0% and is the fastest-growing segment, driven by light-gauge steel housing adoption in affordable housing programs across Asia Pacific and Africa.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

34.0% |

Rapid urbanization, India and China industrial expansion, government infrastructure investment, growing e-commerce warehousing demand |

|

North America |

22.5% |

Large-scale commercial construction, advanced manufacturing facility upgrades, strong adoption of steel Pre-engineered Building structures across the U.S. and Canada |

|

Europe |

19.0% |

Green building standards, industrial sector modernization, adoption of sustainable Pre-engineered Building solutions driven by EU sustainability regulations |

|

Latin America |

13.5% |

Growing commercial real estate, Brazil and Mexico construction activity, expanding logistics and distribution center demand |

|

Middle East & Africa |

11.0% |

GCC mega-project construction, Saudi Vision 2030 infrastructure, Zamil Steel's regional leadership, mining and energy sector demand |

Asia Pacific commands 34.0% of global Pre-engineered Building revenue in 2025, driven by India’s infrastructure expansion and manufacturing push under PLI schemes, alongside rapid industrial park development across China, Vietnam, and Indonesia, where rising manufacturing investments are creating sustained demand for industrial pre-engineered building structures.

North America holds a 22.5% share in 2025, driven by U.S. reshoring, data center growth, and Sun Belt construction. Europe accounts for 19.0% with sustainability-driven adoption. Latin America (13.5%) and Middle East & Africa (11.0%) are expanding due to infrastructure investments and strong regional players like Zamil Steel and Kirby Building Systems.

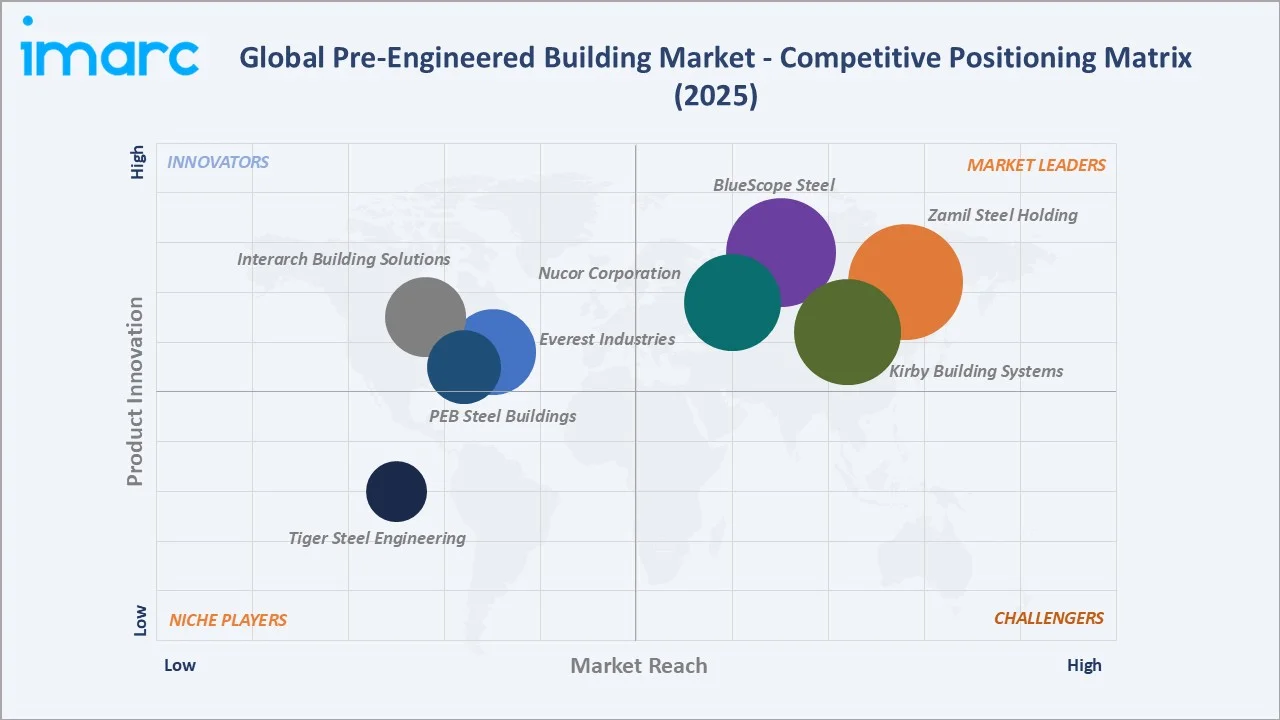

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Zamil Steel Holding Company Ltd. |

Zamil Steel |

Leader |

MENA & Asia Pacific dominance, integrated design-manufacture-erect model |

|

BlueScope Steel Limited |

BUTLER®, LYSAGHT® |

Leader |

Global scale, innovative steel solutions, Australia and Asia Pacific leadership |

|

Kirby Building Systems LLC |

Kirby Building Systems |

Leader |

Middle East and Africa specialist, full turnkey Pre-engineered Building solutions |

|

Nucor Corporation |

Nucor Building Systems |

Leader |

North America largest steelmaker, vertically integrated Pre-engineered Building manufacturing |

|

Everest Industries Limited |

Everest Pre-Engineered Steel Buildings |

Challenger |

India focused, diversified building solutions, growing industrial client base |

|

Interarch Building Solutions Ltd. |

Interarch, TRACDEK |

Challenger |

India leader, design excellence, ISO certified manufacturing capabilities |

|

PEB Steel Buildings Co., Ltd. |

Pebsteel |

Challenger |

Southeast Asia and Middle East specialist, cost-competitive Pre-engineered Building solutions |

|

Tiger Steel Engineering LLC |

Tiger Steel |

Emerging |

UAE based, fast-growing project pipeline across GCC markets |

The global pre-engineered building market features a tiered competitive landscape, led by Zamil Steel, BlueScope Steel, Kirby Building Systems, and Nucor, supported by integrated manufacturing, global delivery networks, and strong client relationships across industrial, infrastructure, and commercial sectors.

Key Company Profiles

Zamil Steel Holding Company

Zamil Steel Holding Company, headquartered in Dammam, Saudi Arabia, is a leading global manufacturer of pre-engineered steel buildings. Founded in 1977, the company operates manufacturing facilities across Saudi Arabia, India, Vietnam, Egypt, and the UAE, serving customers in over 95 countries. Zamil Steel has supplied more than 90,000 buildings worldwide, with annual production capacity exceeding 6 million square meters, supported by growing industrial infrastructure demand across the Middle East, Asia Pacific, and Africa.

- Product & Service Portfolio: Pre-engineered building systems, structural steel, insulated panels, roofing systems, accessories, and turnkey erection services.

- Recent Developments: In April 2025, Zamil Steel signed a contract with Hamat Holding for the Masar Mall project in Makkah, supplying 15,000 tonnes of structural steel, strengthening its commercial PEB infrastructure presence.

- Strategic Focus: Geographic expansion, sustainable steel buildings, industrial warehouse demand, and digital engineering integration.

BlueScope Steel Limited

BlueScope Steel Limited, headquartered in Melbourne, Australia, is a global steel and building solutions provider operating in over 18 countries with approximately 16,500 employees. Through LYSAGHT and Butler brands, the company delivers pre-engineered building solutions across Asia-Pacific and North America markets.

- Product & Service Portfolio: BlueScope Steel offers pre-engineered building systems through Butler and LYSAGHT, along with coated steel products including COLORBOND®, ZINCALUME®, roofing, walling, structural framing, and engineered building solutions for industrial and commercial construction applications.

- Recent Developments: In 2024, BlueScope marked a US$700 million expansion at its North Star facility in Delta, Ohio, creating 100+ jobs and adding 850,000-ton capacity, strengthening low-carbon steel supply for North American pre-engineered buildings.

- Strategic Focus: BlueScope Steel focuses on low-carbon steel innovation, North American manufacturing expansion, and growth of global pre-engineered building solutions through Butler Manufacturing and LYSAGHT distribution networks.

Kirby Building Systems LLC

Kirby Building Systems, part of Alghanim Industries, is a global pre-engineered steel building manufacturer operating across the Middle East, Africa, India, and Southeast Asia, with seven manufacturing facilities, over 5,000 employees, and more than 100,000 buildings delivered globally.

- Product & Service Portfolio: Kirby Building Systems provides pre-engineered buildings, structural steel systems, storage solutions, accessories, and turnkey engineering, fabrication, and erection services for industrial, commercial, logistics, infrastructure, and aviation applications.

- Recent Developments: In 2025, Kirby Building Systems opened a 40,000-square-foot Centre of Engineering Excellence in Hyderabad, housing 550 specialists to enhance digital design capabilities and accelerate pre-engineered building project delivery.

- Strategic Focus: Kirby Building Systems focuses on expanding GCC and African markets, increasing regional manufacturing capacity, and enhancing digital engineering capabilities to accelerate pre-engineered building project delivery.

Market Concentration Analysis

The global pre-engineered building market is moderately concentrated, with Zamil Steel Holding Company Ltd., BlueScope Steel Limited, Kirby Building Systems LLC, and Nucor Corporation accounting for roughly 25–30% of global revenue in 2025. Their extensive manufacturing networks, strong client relationships, and technology investments create significant barriers for smaller players.

Market fragmentation increases at regional and national levels, with numerous independent pre-engineered building manufacturers serving local construction markets. In India, companies such as Everest Industries, Interarch Building Products, Jindal Buildsys, and Lloyd Insulations compete actively for industrial and commercial projects.

Consolidation is increasing due to ESG compliance, demand for certified pre-engineered building solutions, and high capital requirements for advanced manufacturing. Large players are acquiring regional manufacturers to expand coverage, while smaller firms focus on niche expertise or cost leadership to remain competitive.

Investment & Growth Opportunities

Fastest-Growing Segments

The residential sector is expected to be the fastest-growing pre-engineered building segment through 2034, driven by affordable housing initiatives in India, Southeast Asia, and Sub-Saharan Africa. Light-gauge steel frame solutions enable faster construction, supporting large-scale housing programs. India's Pradhan Mantri Awas Yojana, targeting over 20 million homes, presents a major growth opportunity for residential PEB manufacturers.

The Infrastructure Sector – currently at 22.0% – is projected to grow at above-market rates through 2034, driven by airport expansion programs, metro rail infrastructure, and public utility construction across Asia Pacific, the Middle East, and Latin America.

Emerging Market Expansion

Africa is emerging as a strong growth market for pre-engineered building manufacturers, driven by rising infrastructure development needs. Demand is growing from remote mining, oil and gas, and power projects, while long-term urbanization is expected to boost commercial and industrial adoption in key markets such as Nigeria, Kenya, and South Africa.

Venture & Strategic Investment Trends

Private equity and corporate investment in pre-engineered buildings is rising, focusing on capacity expansion, digital design platforms, and automation technologies. Manufacturers are also investing in sustainable materials and green steel partnerships to offer low-carbon solutions and meet growing ESG requirements.

Future Market Outlook (2026-2034)

The global pre-engineered building market is projected to grow from USD 18.47 Billion in 2025 to USD 35.44 Billion by 2034, adding over USD 17 Billion at a CAGR of 8.15%. Growth is driven by Asia-Pacific industrial expansion, e-commerce infrastructure, healthcare and data center construction, and rising adoption of green building standards.

Three transformational dynamics will reshape the Pre-engineered Building market through 2034. First, digital design convergence – integrating BIM, AI-assisted structural optimization, and automated manufacturing – will compress design-to-delivery cycles and improve customization capabilities, broadening the addressable application range. Second, sustainability imperatives will transform material sourcing and product certification, with green steel Pre-engineered Building solutions commanding premium market positioning. Third, modular and hybrid Pre-engineered Building innovations will penetrate previously inaccessible residential and mixed-use construction markets, expanding the total addressable market beyond traditional industrial and commercial boundaries.

By 2034, pre-engineered buildings are expected to represent a meaningfully higher proportion of total global construction output compared to 2025 levels. Operators investing in digital manufacturing, sustainable product development, and emerging market geographic expansion are best positioned to capture disproportionate value from the sector's continued structural growth.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted during 2024–2025 with key pre-engineered building stakeholders, such as procurement leaders, Tier-1 manufacturers, structural consultants, project managers, and building standards authorities across Asia Pacific, North America, Europe, and the Middle East.

Secondary Research

Secondary sources included company annual reports (BlueScope Steel, Nucor, Everest Industries, Interarch Building Products), industry associations (MBMA, SCI), government infrastructure programs, and trade publications such as Metal Architecture Magazine and Construction Week.

Forecasting Models

Market size and growth forecasts were estimated using bottom-up and top-down models, incorporating regional construction growth, industrial capex trends, PEB penetration, steel demand forecasts, historical trends, and scenario analysis for 2026–2034.

Pre-Engineered Building Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Concrete Structure, Steel Structure, Civil Structure, Others |

| End-Users Covered | Industrial Sector, Commercial Sector, Infrastructure Sector, Residential Sector |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Zamil Steel Holding Company Ltd., BlueScope Steel Limited, Kirby Building Systems LLC, Nucor Corporation, Everest Industries Limited, Interarch Building Solutions Ltd., PEB Steel Buildings Co., Ltd., Tiger Steel Engineering LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pre-engineered building market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global pre-engineered building market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pre-engineered building industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Pre-Engineered Building Market Report

The global pre-engineered building market was valued at USD 18.47 Billion in 2025, driven by rapid urbanization, industrial sector expansion, and rising demand for cost-effective construction solutions.

The market is projected to reach USD 35.44 Billion by 2034, growing at a CAGR of 8.15% during 2026-2034, supported by infrastructure development, e-commerce growth, and green building adoption.

Steel Structure leads with a 38.5% share in 2025, driven by its superior strength, recyclability, rapid assembly capabilities, and cost advantages over conventional construction materials.

The Industrial Sector commands a 36.0% share in 2025, driven by growing demand for manufacturing plants, warehouses, cold storage facilities, and distribution centers globally.

Asia Pacific leads with a 34.0% share in 2025, driven by India and China industrial growth, infrastructure investment, and rapid urbanization across Southeast Asian economies.

Key drivers include rapid urbanization, e-commerce warehouse demand, sustainability mandates, cost-efficiency advantages, infrastructure modernization, and technological advancements in Pre-engineered Building design.

Asia Pacific is the fastest-growing region, driven by India's infrastructure push, China's industrial expansion, and growing manufacturing investment across Vietnam, Indonesia, and the Philippines.

Leading companies include Zamil Steel Holding Company Ltd., BlueScope Steel Limited, Kirby Building Systems LLC, Nucor Corporation, Everest Industries Limited, Interarch Building Solutions Ltd., PEB Steel Buildings Co., Ltd., and Tiger Steel Engineering LLC.

Concrete Structure holds a 28.0% share in 2025, primarily used for infrastructure and heavy industrial applications where fire resistance and load-bearing capacity are critical requirements.

Rapid e-commerce expansion is driving demand for large-format warehouses and distribution centers, where Pre-engineered Buildings offer cost-efficient, fast-construction alternatives well-suited for logistics infrastructure.

BIM integration, 3D modeling software, automated steel fabrication, and IoT-enabled smart building systems are improving Pre-engineered Building design precision, reducing material waste, and shortening construction timelines.

The global pre-engineered building market is projected to grow at a CAGR of 8.15% during 2026-2034, driven by industrial expansion, sustainable construction adoption, and infrastructure development globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)