United States Insulin Pumps Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

United States Insulin Pumps Market Size, Share, Trends & Forecast (2026-2034)

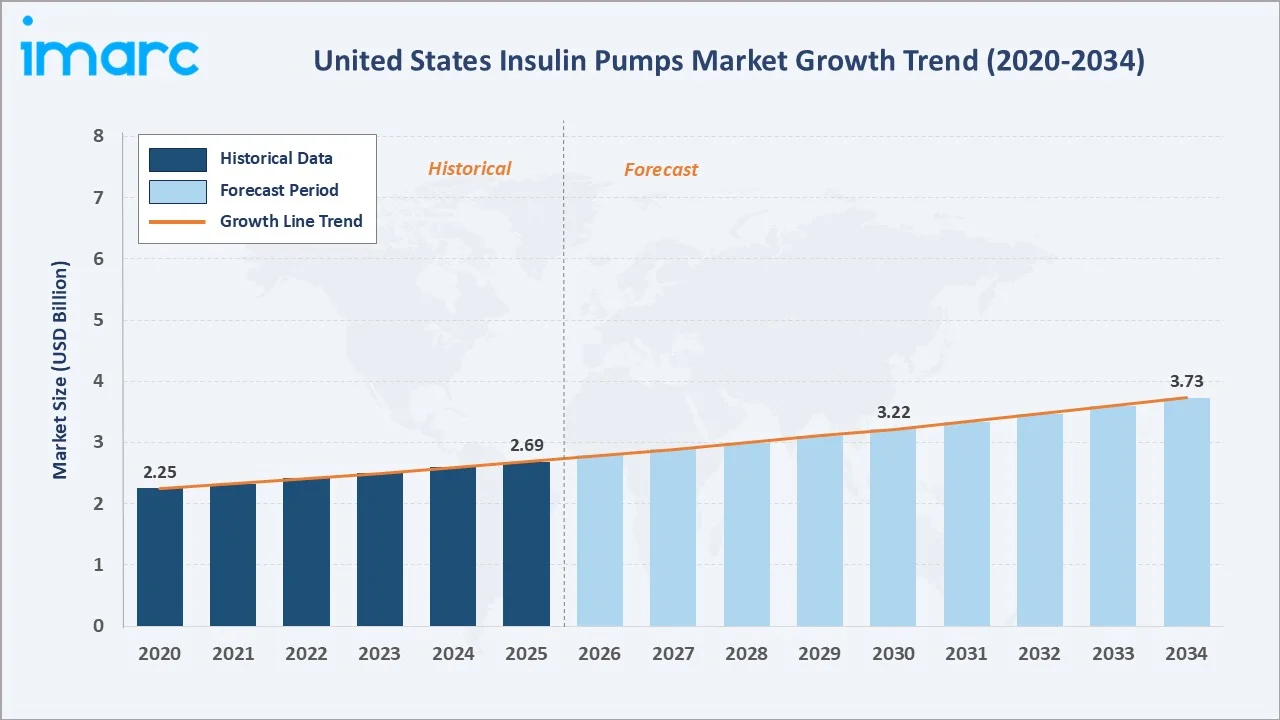

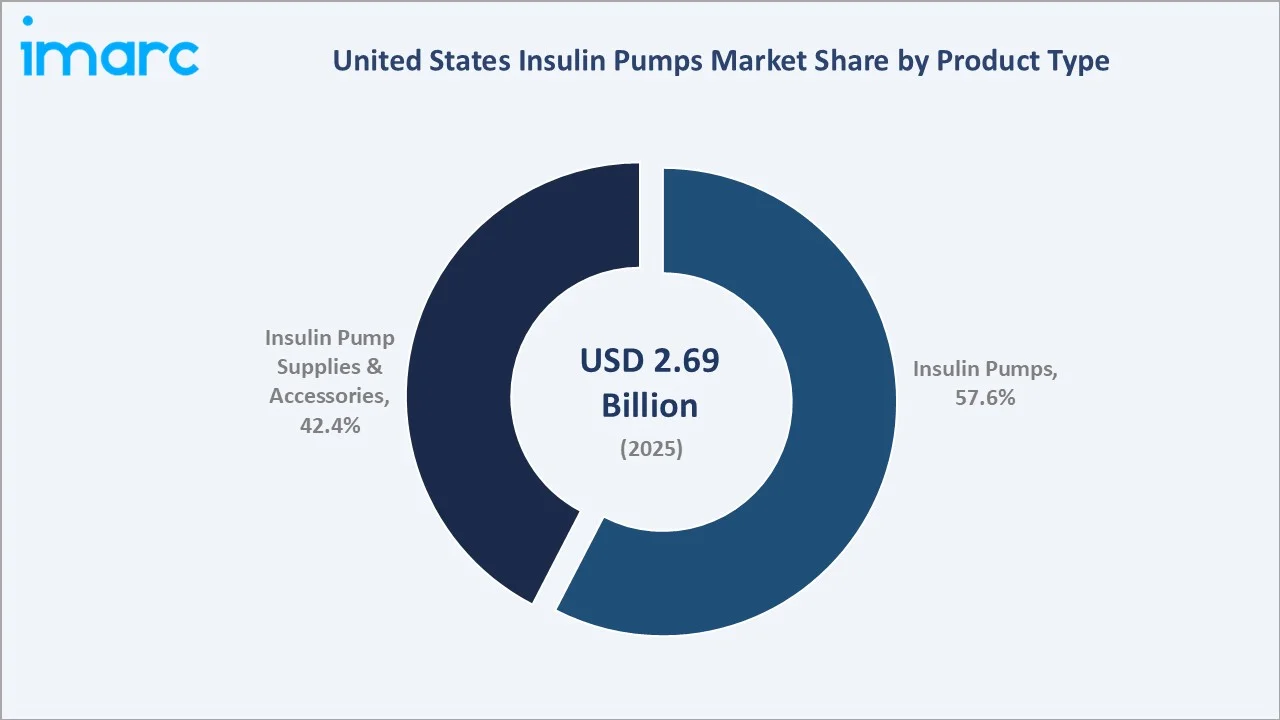

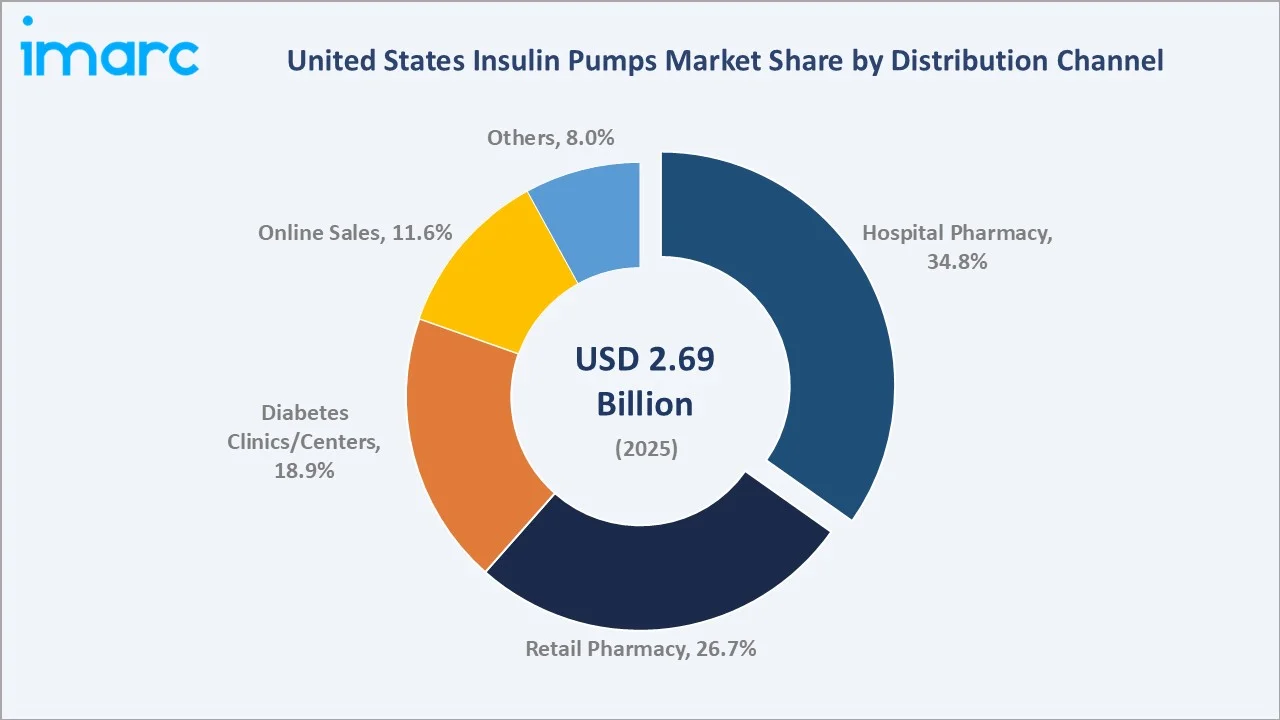

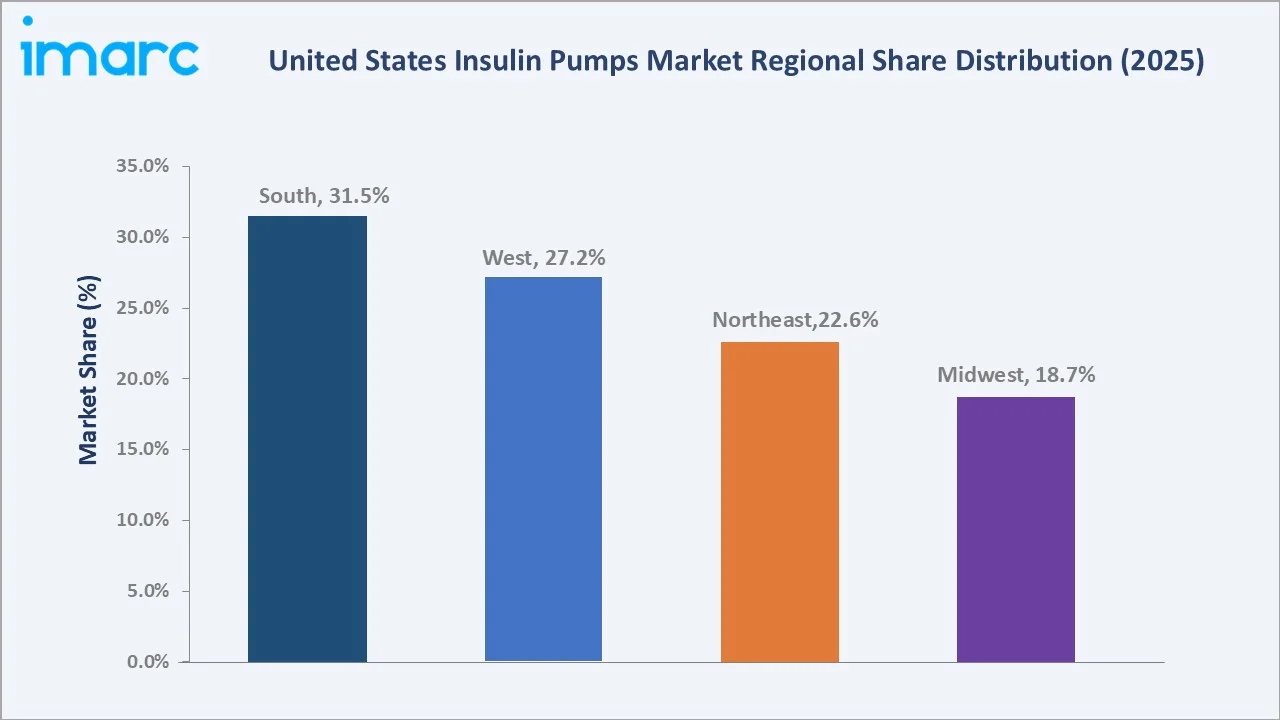

The United States insulin pumps market size was valued at USD 2.69 Billion in 2025 and is projected to reach USD 3.73 Billion by 2034, exhibiting a CAGR of 3.67% during 2026-2034. Rising prevalence of Type 1 and Type 2 diabetes, growing adoption of automated insulin delivery (AID) systems, expanding integration with continuous glucose monitors, and supportive Medicare and private insurance reimbursement frameworks are collectively driving market growth. Insulin pumps account for 57.6% of the product mix in 2025, while Hospital Pharmacy leads distribution with a 34.8% share. The South region commands the largest regional share at 31.5% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.69 Billion |

|

Forecast Market Size (2034) |

USD 3.73 Billion |

|

CAGR (2026-2034) |

3.67% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (31.5% share, 2025) |

|

Fastest Growing Region |

West |

|

Leading Product Type |

Insulin Pumps (57.6%, 2025) |

|

Leading Distribution Channel |

Hospital Pharmacy (34.8%, 2025) |

The chart below tracks US insulin pumps market growth from 2020-2034, capturing post-pandemic recovery and structural demand from rising diabetes prevalence and AID adoption.

To get more information on this market, Request Sample

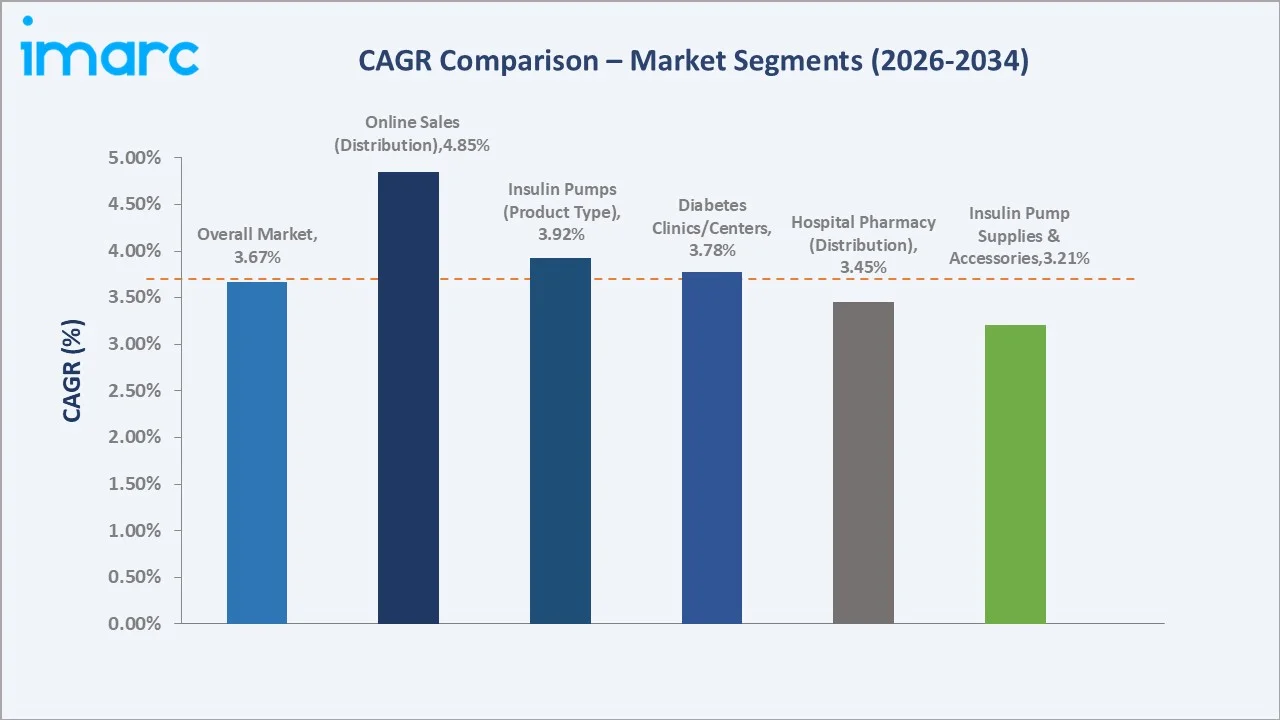

CAGR analysis identifies online sales and insulin pumps as the fastest-growing segments in the US insulin pumps market through 2034, reflecting digital channel expansion and AID system adoption.

Executive Summary

The US insulin pumps market is being reshaped by closed-loop automation, smartphone connectivity, and broader insurance coverage of advanced diabetes technology. Valued at USD 2.69 billion in 2025, the market is projected to reach USD 3.73 billion by 2034 at a CAGR of 3.67%. The CDC estimates that 38.4 million people in the United States have diabetes.

Insulin pumps lead the product mix with a 57.6% share in 2025, driven by increasing adoption of hybrid closed-loop systems such as the Medtronic MiniMed 780G, Omnipod 5, and t:slim X2, which enhance automated insulin delivery and glycemic control. Insulin pump supplies and accessories contribute 42.4%, generating recurring consumable revenue. Hospital pharmacy commands 34.8% of distribution, while online sales is the fastest-rising channel.

The South region leads with a 31.5% share in 2025, reflecting elevated diabetes prevalence in Texas, Florida, and Georgia. The West follows at 27.2% on California's payer ecosystem and digital health adoption. The Northeast (22.6%) and Midwest (18.7%) round out the demand landscape, supported by mature academic medical centers and structured endocrinology networks.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type Segment |

Insulin Pumps - 57.6% share (2025) |

|

Second Product Type Segment |

Insulin Pump Supplies & Accessories - 42.4% share (2025) |

|

Leading Distribution Channel |

Hospital Pharmacy - 34.8% share (2025) |

|

Leading Region |

South - 31.5% share (2025) |

|

Second Region |

West - 27.2% share (2025) |

|

Top Companies |

Medtronic MiniMed, Inc., Insulet Corporation, Tandem Diabetes Care, Inc.. |

Key Analytical Observations Supporting the Above Data:

- Insulin pumps' 57.6% dominance in 2025reflects clinician and patient preference for hybrid closed-loop systems, with Omnipod 5 and MiniMed 780G leading new prescriptions.

- Insulin pump supplies & accessories at 42.4% in 2025represent a recurring revenue stream, since infusion sets and pods are typically replaced every 2-3 days.

- Hospital pharmacy's 34.8% share in 2025 stems from initial pump prescriptions and patient onboarding being centered in endocrinology clinics linked to hospital systems.

- Retail pharmacy at 26.7% reflects Medicare Part D and commercial pharmacy benefit access for refills, especially for tubeless patch pumps dispensed through retail channels.

- South region's 31.5% lead is anchored by high diabetes prevalence; Mississippi (14.7%), Alabama (13.7%), and West Virginia (15.0%) report adult diabetes rates, exceeding the 10.3% United States average.

United States Insulin Pumps Market Overview

Insulin pumps are continuous subcutaneous insulin infusion (CSII) devices that deliver rapid-acting insulin throughout the day, replacing multiple daily injections. The United States ecosystem includes pump manufacturers, CGM partners, infusion-set suppliers, regulatory bodies (FDA), endocrinology clinics, retail and specialty pharmacies, and payers managing reimbursement under Medicare and commercial plans.

Applications span Type 1 diabetes management, intensive Type 2 therapy, gestational diabetes, and pediatric care. Demand is reinforced by rising obesity-linked diabetes incidence, expanded Medicare CGM coverage since 2023, growing telehealth-enabled remote pump adjustments, and macroeconomic stability supporting medical device capex across hospital systems.

Market Dynamics

To evaluate market opportunities, Request Sample

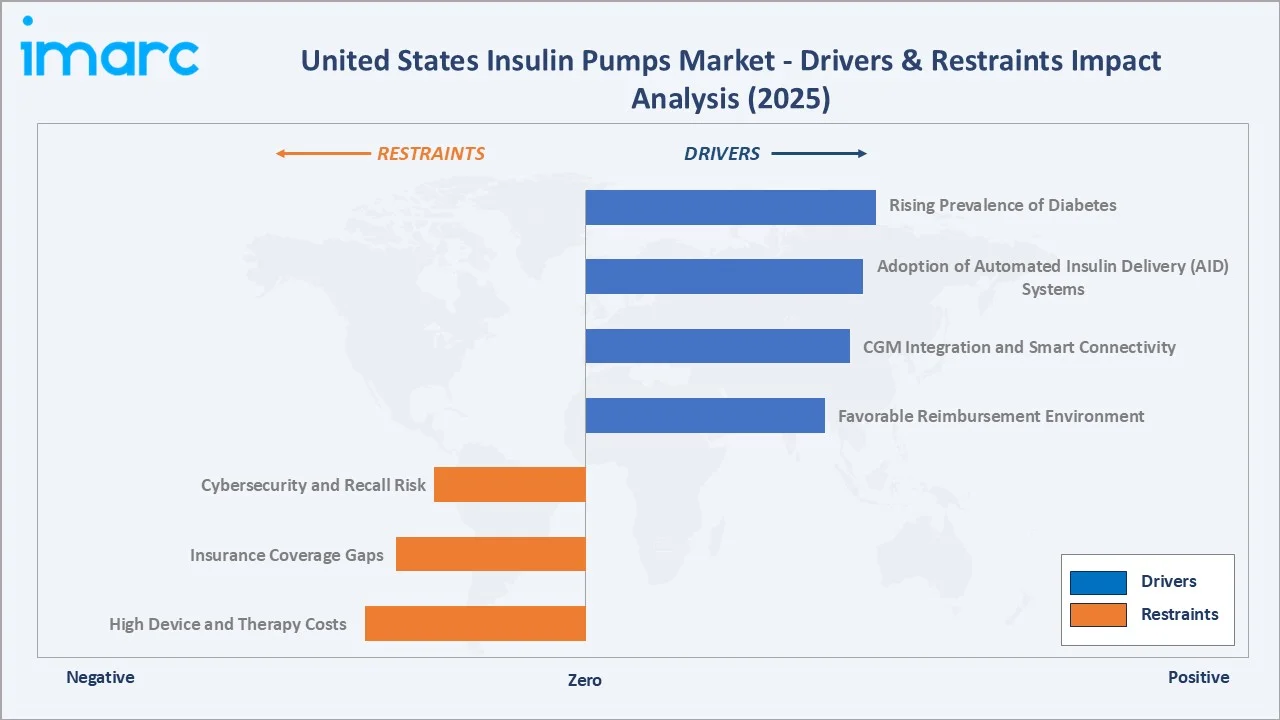

Market Drivers

- Rising Prevalence of Diabetes: The CDC reports that 38.4 million Americans have diabetes, including approximately 2 million with Type 1 diabetes, which directly expands the addressable insulin pump population, particularly among insulin-dependent users.

- Adoption of Automated Insulin Delivery (AID) Systems: Hybrid closed-loop systems such as the Medtronic MiniMed 780G, Tandem t:slim X2 with Control-IQ, and Insulet Omnipod 5 have demonstrated significant improvements in time-in-range and glycemic control in clinical and real-world studies, supporting their increasing adoption in the United States.

- CGM Integration and Smart Connectivity: Integration with CGM systems like Dexcom G7 and in some cases Abbott FreeStyle Libre—enables automated insulin delivery, improving time-in-range, reducing hypoglycemia exposure, and supporting smartphone-based monitoring via mobile apps.

- Favorable Reimbursement Environment: Medicare and most commercial insurers cover insulin pumps and AID systems under durable medical equipment benefits, while expanded CGM coverage since 2023 has lowered out-of-pocket barriers for new pump starts.

Market Restraints

- High Device and Therapy Costs: Insulin pumps typically cost around USD 4,500–7,000, with ongoing annual supply costs that can reach several thousand dollars, creating affordability challenges for under-insured patients despite Medicare support.

- Insurance Coverage Gaps: Coverage variability across Medicaid plans and high-deductible commercial plans creates unequal access, particularly in southern and rural regions where private insurance penetration is lower.

- Cybersecurity and Recall Risk: FDA safety communications and recalls, including those related to Medtronic MiniMed insulin pumps, have raised concerns around cybersecurity and device safety, influencing prescriber and payer confidence.

Market Opportunities

- Type 2 Diabetes Pump Penetration: Type 2 diabetes accounts for 90–95% of all U.S. diabetes cases, yet insulin pump adoption in this group remains low, indicating significant growth potential, particularly for simplified and tubeless systems.

- Pediatric and Young Adult Segment: Devices such as Omnipod 5 (cleared for children as young as 2 years) and Tandem Mobi are expanding use among pediatric and young patients, supporting long-term therapy adoption and recurring supply demand.

- Direct-to-Consumer Online Fulfillment: Digital and direct-to-consumer channels are expanding, with online pharmacy and manufacturer platforms improving access, convenience, and subscription-based supply delivery, supporting market growth.

Market Challenges

- Patient Training and Onboarding Complexity: Advanced insulin pump and AID systems require structured patient training and clinical support, and workforce constraints in diabetes education can limit adoption in underserved areas.

- Skin Adhesion and Wear-Site Issues: Patch pump users frequently report skin irritation and adhesive failure, prompting site rotation challenges; manufacturers including Insulet are investing in next-generation adhesives to improve continuous wear time.

- GLP-1 Therapy Substitution Risk: The growing adoption of GLP-1 receptor agonists such as Ozempic, Mounjaro, and Wegovy is shifting Type 2 diabetes management toward non-insulin therapies, potentially delaying insulin initiation and impacting pump adoption.

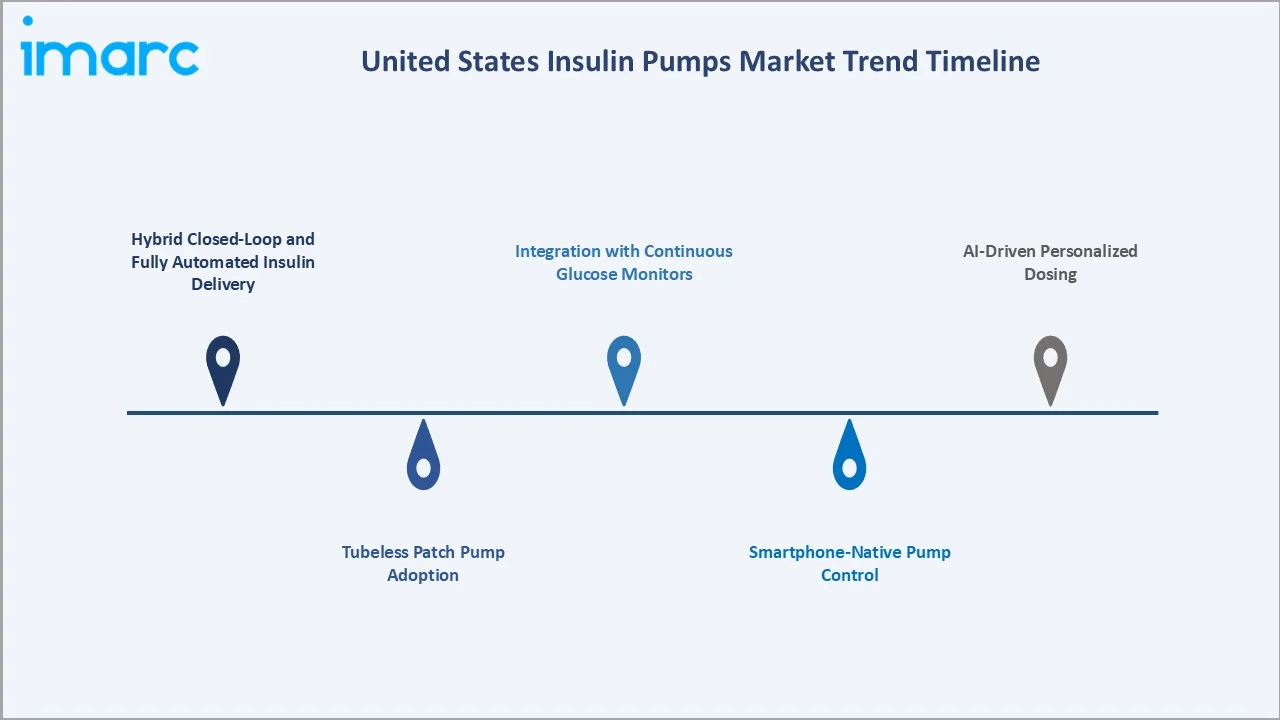

Emerging Market Trends

1. Hybrid Closed-Loop and Fully Automated Insulin Delivery

Closed-loop systems linking pumps with CGMs are now standard. Tandem Control-IQ, MiniMed 780G, and Omnipod 5 use predictive algorithms to deliver auto-correction boluses, improving time-in-range above 70%.

2. Tubeless Patch Pump Adoption

Omnipod-style tubeless pumps continue to gain share. Discreet wearability and smartphone control are driving adoption among children, athletes, and Type 2 patients new to pump therapy.

3. Smartphone-Native Pump Control

Tandem Mobi, Omnipod 5, and MiniMed 780G now support iOS and Android control. App-based dosing, remote monitoring for caregivers, and cloud data sharing with clinicians are becoming default features.

4. Integration with Continuous Glucose Monitors

Pump-CGM interoperability is deepening through partnerships with Dexcom and Abbott. Multi-CGM compatibility lets patients pair their preferred sensor and pushes manufacturers to compete on algorithm performance.

5. AI-Driven Personalized Dosing

Machine learning algorithms analyzing meal patterns and exercise are enabling adaptive basal profiles. Beta Bionics iLet pioneered meal-announcement-only dosing, reducing patient burden while maintaining glycemic control.

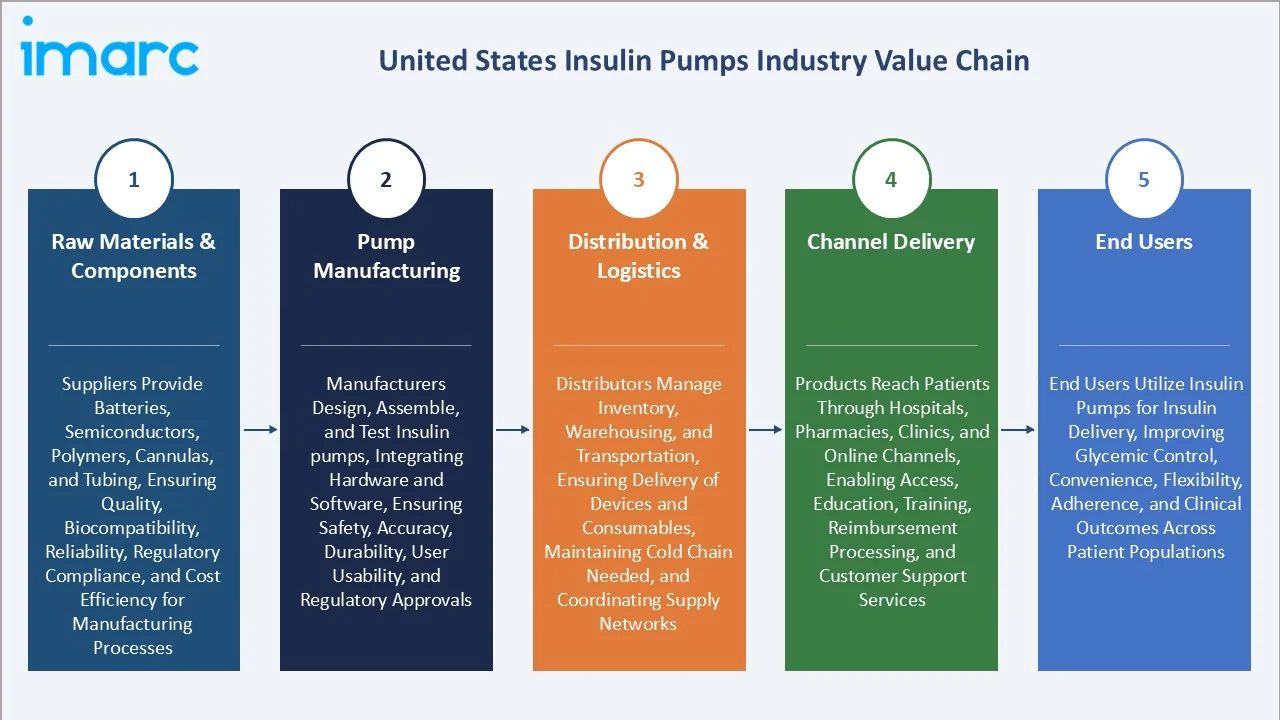

Industry Value Chain Analysis

The US insulin pumps value chain spans five stages, from component sourcing to patient delivery, each with distinct margin profiles and competitive dynamics.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Suppliers provide batteries, semiconductors, polymers, cannulas, and tubing, ensuring quality, biocompatibility, reliability, regulatory compliance, and cost efficiency for manufacturing processes |

|

Pump Manufacturing |

Manufacturers design, assemble, and test insulin pumps, integrating hardware and software, ensuring safety, accuracy, durability, user usability, and regulatory approvals |

|

Distribution & Logistics |

Distributors manage inventory, warehousing, and transportation, ensuring delivery of devices and consumables, maintaining cold chain needed, and coordinating supply networks |

|

Channel Delivery |

Products reach patients through hospitals, pharmacies, clinics, and online channels, enabling access, education, training, reimbursement processing, and customer support services |

|

End Users |

End users utilize insulin pumps for insulin delivery, improving glycemic control, convenience, flexibility, adherence, and clinical outcomes across patient populations |

Pump manufacturers capture the largest value share through device hardware, while consumables generate steady recurring revenue. Distributors and pharmacies hold thinner margins but play a critical role in patient onboarding and refill logistics across geographically dispersed users.

Technology Landscape in the United States Insulin Pumps Industry

Battery and Microelectronics

Rechargeable lithium-ion/polymer batteries power modern AID pumps for several days. t:slim X2 insulin pump uses USB charging, while Omnipod 5 relies on disposable pod batteries, balancing usability and design constraints.

Materials Innovation and Patch Adhesion

Next-generation hydrocolloid and silicone-based adhesives are extending wear time to Few days. Insulet and Tandem are also miniaturizing reservoir-and-cannula assemblies to improve user comfort, reduce skin irritation, and support broader patch pump adoption among Type 2 patients.

Smart Connectivity and Cloud Platforms

Insulin pumps integrate Bluetooth and mobile apps with platforms like CareLink and t:connect, enabling remote monitoring and data sharing with clinicians, improving therapy optimization and population-level diabetes management.

Algorithm and Automation

Predictive algorithms based on machine learning are core competitive differentiators. Control-IQ, SmartGuard, and SmartAdjust adjust basal rates every 5 minutes based on CGM trends, while Beta Bionics iLet's autonomous algorithm eliminates carb counting for many users.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Insulin Pumps | 57.6% | 2025 |

| Distribution Channel | Hospital Pharmacy | 34.8% | 2025 |

| Region | South | 31.5% | 2025 |

By Product Type

Insulin pumps account for 57.6% of the United States market in 2025, driven by hybrid closed-loop systems such as MiniMed 780G, t:slim X2, and Omnipod 5, with increasing adoption of tubeless patch pumps.

To access detailed market analysis, Request Sample

Insulin pump supplies and accessories contribute 42.4% in 2025, encompassing infusion sets, reservoirs, cartridges, insertion devices, and skin adhesives. The segment generates resilient recurring revenue, with consumables typically replaced every 2-3 days, supporting predictable demand visibility for manufacturers.

By Distribution Channel

Hospital pharmacy leads at 34.8% in 2025, reflecting initial pump prescribing in endocrinology clinics tied to hospital systems and inpatient diabetes management. Pump-naive patients are commonly initiated through hospital-affiliated CDCES programs, anchoring this channel's leadership in new starts.

Retail pharmacy holds 26.7% on Medicare Part D and commercial pharmacy-benefit access, particularly for tubeless patch pumps. Diabetes Clinics/Centers (18.9%) drive prescription continuity, Online Sales (11.6%) lead growth via direct-to-consumer fulfillment, and Others (8.0%) cover specialty distributors and DME suppliers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

31.5% |

Highest US diabetes prevalence, large population centers in Texas and Florida, expanding Medicare beneficiary base, growing endocrinology networks |

|

West |

27.2% |

California payer ecosystem, digital health adoption, manufacturer R&D presence (Insulet, Tandem in San Diego), tech-savvy patient population |

|

Northeast |

22.6% |

Concentration of academic medical centers, dense endocrinology specialist networks, strong commercial insurance coverage, high pump adoption rates |

|

Midwest |

18.7% |

Established hospital systems (Mayo Clinic, Cleveland Clinic), structured employer-sponsored insurance, growing rural telehealth-enabled pump initiation |

The South commands a 31.5% share in 2025, reflecting the region's elevated diabetes burden; states such as Mississippi (14.7%), Alabama (13.7%), Louisiana (14.5%), and West Virginia (15.0%) consistently report adult diabetes prevalence, well above the national average of 10.3% per CDC data. The region's large insured population in Texas and Florida further supports sustained pump demand.

The West (27.2%) is anchored by California's strong payer ecosystem, digital health adoption, and proximity to manufacturers including Insulet and Tandem Diabetes Care. The Northeast (22.6%) leverages dense academic medical centers and high commercial insurance penetration, while the Midwest (18.7%) is supported by integrated hospital systems and growing telehealth-enabled pump onboarding in rural counties.

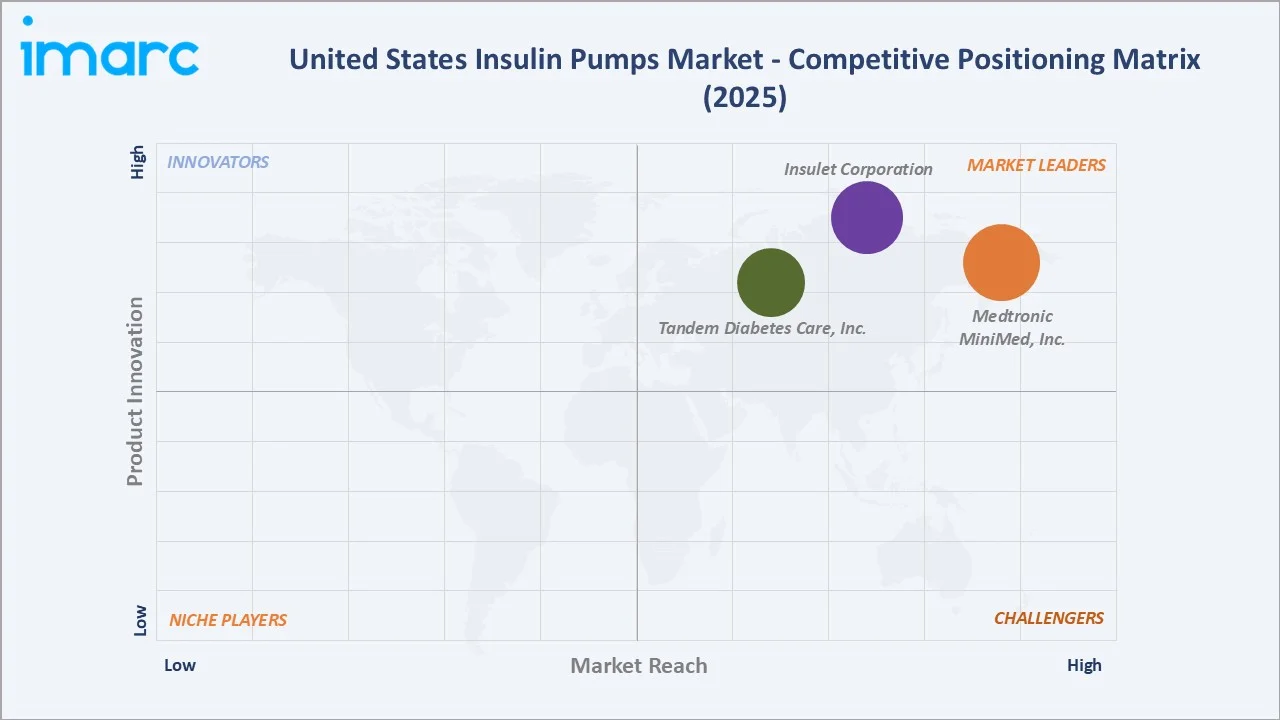

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Medtronic MiniMed, Inc. |

MiniMed 780G |

Leader |

Largest installed base, integrated AID + CGM, global scale |

|

Insulet Corporation |

Omnipod 5 |

Leader |

Tubeless patch pump leadership, pharmacy channel access |

|

Tandem Diabetes Care, Inc. |

t:slim X2 |

Leader |

Touchscreen UX, software-update capability, Mobi miniaturization |

The United States insulin pumps market is dominated by Medtronic MiniMed, Inc., Insulet Corporation, and Tandem Diabetes Care, Inc. Insulet generated about USD 2.1 billion revenue in 2024, driven by Omnipod, while Tandem reported around USD 940 million revenue in 2024, supported by pump adoption and product launches.

Key Company Profiles

Medtronic MiniMed, Inc.

Medtronic MiniMed, Inc. is a global medical technology company with a strong diabetes segment. In FY2025, its diabetes business generated roughly $2.8 billion, contributing a 8.2% of total revenue, with plans announced to separate this division.

- Product & Service Portfolio: MiniMed 780G, MiniMed 770G, Guardian 4 CGM, Simplera Sync CGM, InPen, and the CareLink digital data management platform for integrated diabetes management.

- Recent Developments: In 2025, Medtronic plc announced plans to spin off its diabetes business into an independent, publicly traded company, aiming to enhance operational focus and unlock shareholder value. The separation is expected to create a more agile entity dedicated to advancing insulin pump and CGM technologies, while allowing Medtronic to prioritize higher growth medtech segments. The move will include the company’s insulin pump portfolio, continuous glucose monitoring systems, and digital diabetes platforms, with completion subject to regulatory approvals and market conditions.

- Strategic Focus: Medtronic is prioritizing automated insulin delivery (AID) expansion, tighter CGM–pump integration, broader global access, and portfolio simplification through the planned diabetes business separation.

Insulet Corporation

Insulet Corporation, headquartered in Acton, Massachusetts, specializes in tubeless insulin delivery via its Omnipod platform. The company reported approximately $2.1 billion revenue in 2024, driven by strong adoption of Omnipod 5 and continued global expansion.

- Product & Service Portfolio: Omnipod 5, Omnipod DASH, and a smartphone-based control app integrated with CGM systems for automated insulin delivery.

- Recent Developments: Insulet Corporation announced two major advancements in 2024, receiving U.S. FDA clearance for its Omnipod 5 for adults with Type 2 diabetes—marking a significant expansion beyond its core Type 1 market. The company also unveiled integration of Omnipod 5 with Abbott Laboratories’s FreeStyle Libre 2 Plus CGM, strengthening its multi-sensor ecosystem and enhancing automated insulin delivery capabilities

- Strategic Focus: Insulet's strategy emphasizes Type 2 expansion, multi-CGM compatibility, pharmacy channel growth, and international scale-up of Omnipod 5.

Tandem Diabetes Care, Inc.

Tandem Diabetes Care, Inc., headquartered in San Diego, develops insulin pumps and digital diabetes solutions. The company reported approximately $940 million worldwide revenue in 2024 driven by new pump adoption, launch of Tandem Mobi, and continued expansion of its Control-IQ technology.

- Product & Service Portfolio: t:slim X2 insulin pump with Control-IQ technology, Tandem Mobi, t:connect mobile app, Tandem Source data platform, and integration with Dexcom, Inc. CGM systems.

- Recent Developments: Tandem Diabetes Care, Inc. announced key advancements in 2024, including the U.S. launch of the Tandem Mobi, a compact, fully smartphone-controlled insulin pump designed to enhance user convenience and expand its automated insulin delivery portfolio. In parallel, the company received U.S. FDA clearance for its Control-IQ+ technology in 2025, extending its application to adults with Type 2 diabetes and strengthening its position in the evolving AID market.

- Strategic Focus: Tandem is focused on advancing software-enabled pump platforms, scaling adoption of Tandem Mobi, expanding into Type 2 diabetes, and enhancing interoperability with leading CGM providers such as Dexcom.

Market Concentration Analysis

The US insulin pumps market is highly concentrated at the top tier. Medtronic, Insulet, and Tandem Diabetes Care collectively account for approximately 85-90% of new pump starts and installed-base revenue in 2025, supported by FDA-cleared AID algorithms, broad payer coverage, and integrated CGM partnerships.

Mid-tier and emerging players, including Ypsomed, Beta Bionics, SOOIL, and Modular Medical, compete for niche segments such as carb-count-free dosing (iLet), open-source algorithm compatibility (Dana), and low-cost Type 2 pumps (MODD1). Market structure remains oligopolistic but with growing competitive pressure on patch and Type 2 categories.

Consolidation trends include Medtronic's 2025 announcement to spin off its diabetes business, signaling a focused-pure-play structure ahead. M&A activity remains modest but acquisitions of algorithm partners, CGM compatibility licensees, and digital-health platforms are likely to intensify as AID becomes standard of care for insulin-dependent patients.

Investment & Growth Opportunities

Fastest-Growing Segments

Online and direct-to-consumer channels are expanding rapidly, supported by digital pharmacy models, telehealth prescriptions, and subscription-based systems such as Insulet Corporation’s Omnipod. E-commerce and pharmacy partnerships are reshaping insulin pump distribution in the United States.

The Type 2 diabetes segment represents a major growth opportunity, driven by a large insulin-using population and increasing clinical evidence supporting automated insulin delivery (AID). Recent studies (e.g., CREATE trial (closed-loop therapy Type 2) show improved glycemic outcomes, supporting broader reimbursement expansion.

Emerging Patient Segments

Insulin pump adoption among Type 2 diabetes patients remains low but is increasing, indicating strong future growth potential. Pediatric use is expanding following regulatory approvals (e.g., Omnipod 5 for young children), while gestational diabetes remains an emerging but less penetrated segment for advanced insulin delivery systems.

Venture & Strategic Investment Trends

Investment activity is focused on AID systems, CGM–pump integration, and next-generation patch pumps. Companies such as Beta Bionics have attracted significant funding, reflecting strong investor interest in automated and AI-driven insulin delivery technologies.

Future Market Outlook (2026-2034)

The US insulin pumps market forecast projects sustained value expansion from USD 2.69 Billion in 2025 to USD 3.73 Billion by 2034, growing at a CAGR of 3.67%, representing over USD 1.0 Billion in incremental value. Growth will be driven by Type 2 expansion, AID standard-of-care positioning, and online channel scaling.

Three transformational shifts will reshape the industry through 2034. First, fully closed-loop and bi-hormonal pumps integrating insulin and glucagon will move from research into commercial pipelines. Second, AI-driven personalized dosing will reduce patient burden by minimizing manual carb counting. Third, multi-CGM interoperability will become a baseline requirement, dissolving brand lock-in across pump and sensor combinations.

By 2034, insulin pumps will evolve from device-centric products into integrated digital therapy platforms combining hardware, algorithms, cloud data, and clinician services. Manufacturers investing in AI, cybersecurity, and pharmacy channel scale are positioned to capture the highest-value Type 1 and Type 2 opportunities.

Research Methodology

Primary Research

Primary research involved structured interviews and surveys conducted in 2024-2025 with US insulin pumps stakeholders including endocrinologists, certified diabetes care and education specialists, DME distributors, payer medical directors, and patient advocacy representatives.

Secondary Research

Secondary sources include the CDC National Diabetes Statistics Report, FDA medical device filings and 510(k) clearances, company annual reports (Medtronic, Insulet, Tandem), peer-reviewed publications, and trade publications including DiabetesMine and ADA Standards of Medical Care.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating diabetes prevalence trends, pump-penetration rates, AID adoption curves, and payer reimbursement scenarios under base, optimistic, and conservative cases.

United States Insulin Pumps Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Insulin Pumps, Insulin Pump Supplies and Accessories |

| Distribution Channels Covered | Hospital Pharmacy, Retail Pharmacy, Online Sales, Diabetes Clinics/ Centers, Others |

| Region Covered | Northeast, Midwest, South, West |

| Companies Covered | Medtronic MiniMed, Inc., Insulet Corporation, Tandem Diabetes Care, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Insulin Pumps Market Report

The US insulin pumps market was valued at USD 2.69 Billion in 2025, supported by rising diabetes prevalence, AID adoption, and broad insurance coverage.

The market is projected to reach USD 3.73 Billion by 2034, expanding at a CAGR of 3.67% during 2026-2034.

Insulin Pumps lead with a 57.6% share in 2025, supported by hybrid closed-loop AID systems including MiniMed 780G, Omnipod 5, and Tandem t:slim X2.

Hospital Pharmacy commands a 34.8% share in 2025, driven by initial prescription and onboarding through endocrinology clinics tied to integrated hospital systems.

The South leads with a 31.5% share in 2025, anchored by elevated diabetes prevalence in Texas, Florida, Mississippi, and Alabama.

Key drivers include rising diabetes prevalence, AID adoption, CGM integration, favorable Medicare and commercial reimbursement, and direct-to-consumer fulfillment.

The West is among the fastest-growing regions, supported by California's payer ecosystem, digital health adoption, and tech-savvy patient cohorts.

Leading companies include Medtronic MiniMed, Inc., Insulet Corporation, and Tandem Diabetes Care, Inc., among others.

Insulin pump supplies and accessories hold a 42.4% share in 2025, generating recurring consumable revenue from infusion sets, reservoirs, and pods.

Online sales growth is fueled by manufacturer direct-to-consumer platforms, Amazon Pharmacy, specialty distributors, and discreet home delivery preferred by working-age users.

AID algorithms, CGM integration, smartphone control, AI-driven dosing, and cloud platforms are transforming pumps into integrated digital therapy systems.

Type 1 diabetes patients represent the largest current pump-using cohort, while Type 2 diabetes presents the largest growth opportunity given low pump penetration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)