United States Risk Management Market Size, Share, Trends and Forecast by Component, Deployment Mode, Enterprise Size, Industry Vertical, and Region, 2026-2034

United States Risk Management Market Size, Share, Trends & Forecast (2026-2034)

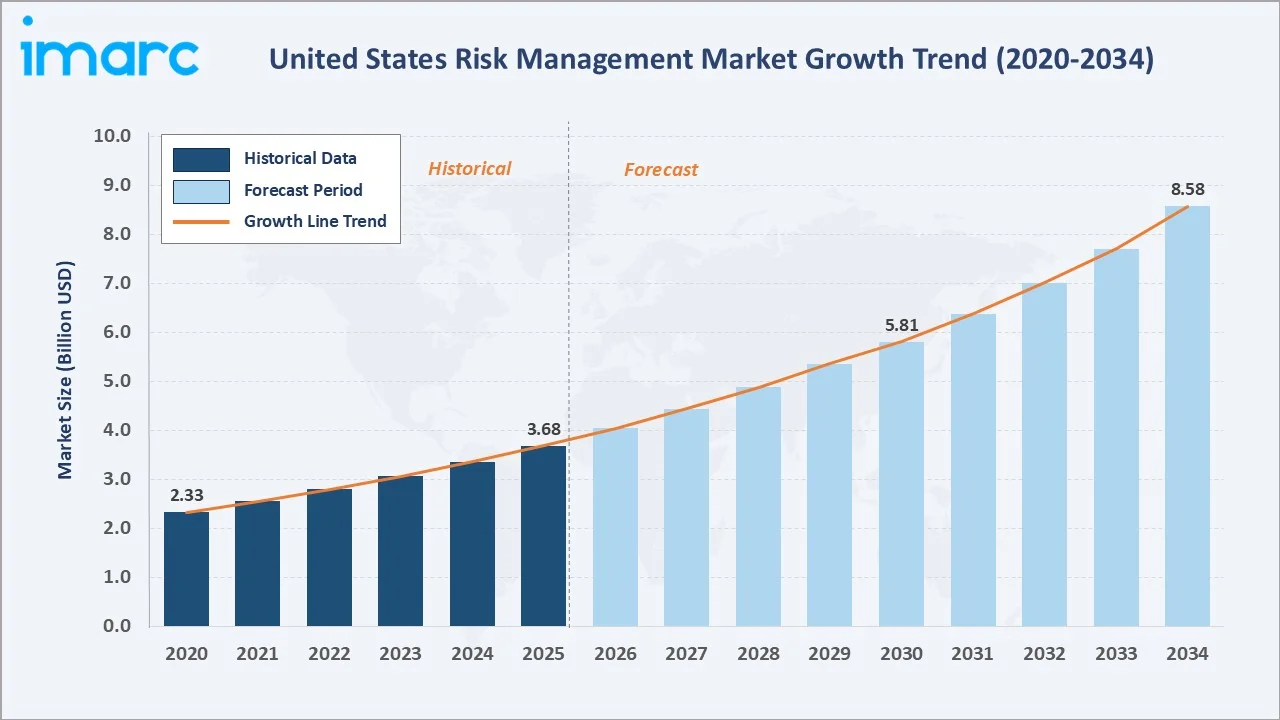

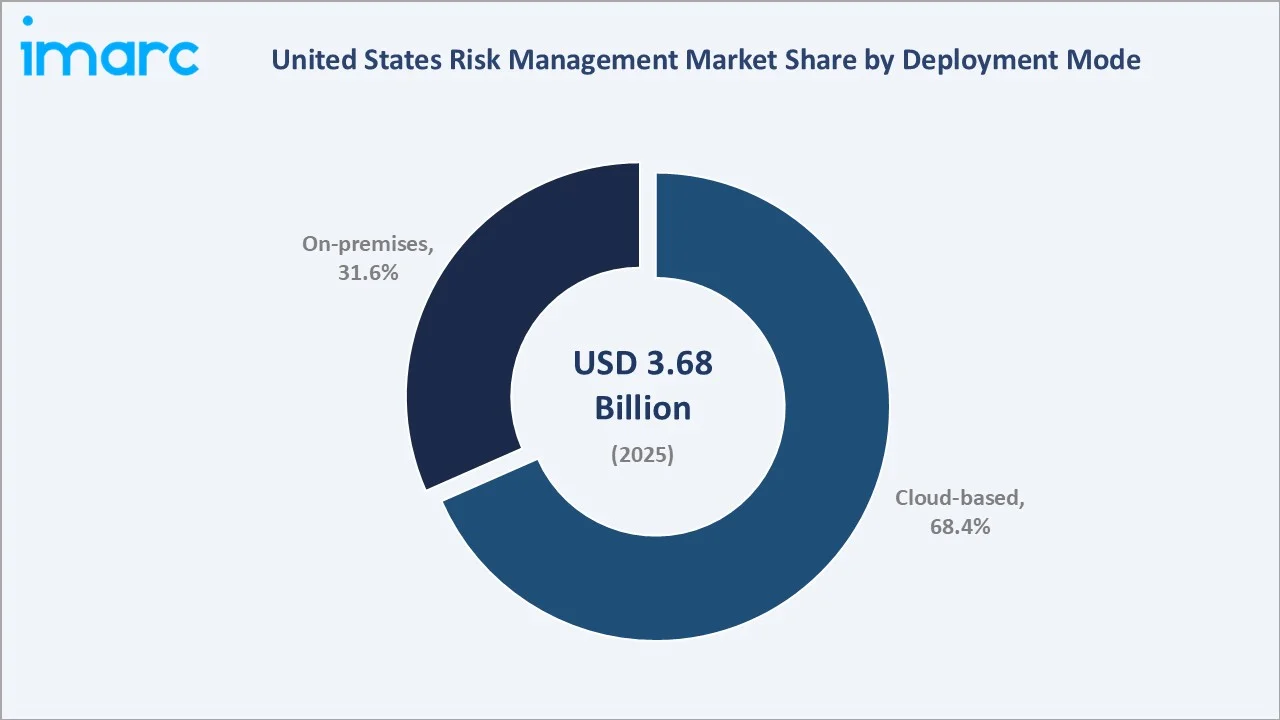

The United States risk management market reached USD 3.68 Billion in 2025 and is projected to reach USD 8.58 Billion by 2034, growing at a CAGR of 9.58% during 2026-2034. Surging cybersecurity threats, expanding regulatory mandates, and rapid enterprise digitalization are accelerating adoption of integrated risk platforms across BFSI, healthcare, IT, and government sectors. Organizations are increasingly deploying AI-powered governance, risk, and compliance (GRC) tools to gain real-time visibility into operational, financial, and compliance risks. Software leads the component segment at 63.8%, while cloud-based deployment dominates at 68.4%. The South leads regionally with a 34.2% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.68 Billion |

|

Forecast Market Size (2034) |

USD 8.58 Billion |

|

CAGR (2026-2034) |

9.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Software (63.8%, 2025) |

|

Dominant Deployment Mode |

Cloud-based (68.4%, 2025) |

|

Leading Region |

South (34.2%, 2025) |

The United States risk management market grew from USD 2.33 Billion in 2020 to USD 3.68 Billion in 2025, driven by surging enterprise demand for integrated GRC, ERM, and cybersecurity risk solutions. The market is projected to reach USD 5.81 Billion by 2030, with growth underpinned by AI-driven automation and expanding SME adoption. By 2034, the market is forecast to reach USD 8.58 Billion, supported by escalating regulatory complexity and digital transformation initiatives.

To get more information on this market, Request Sample

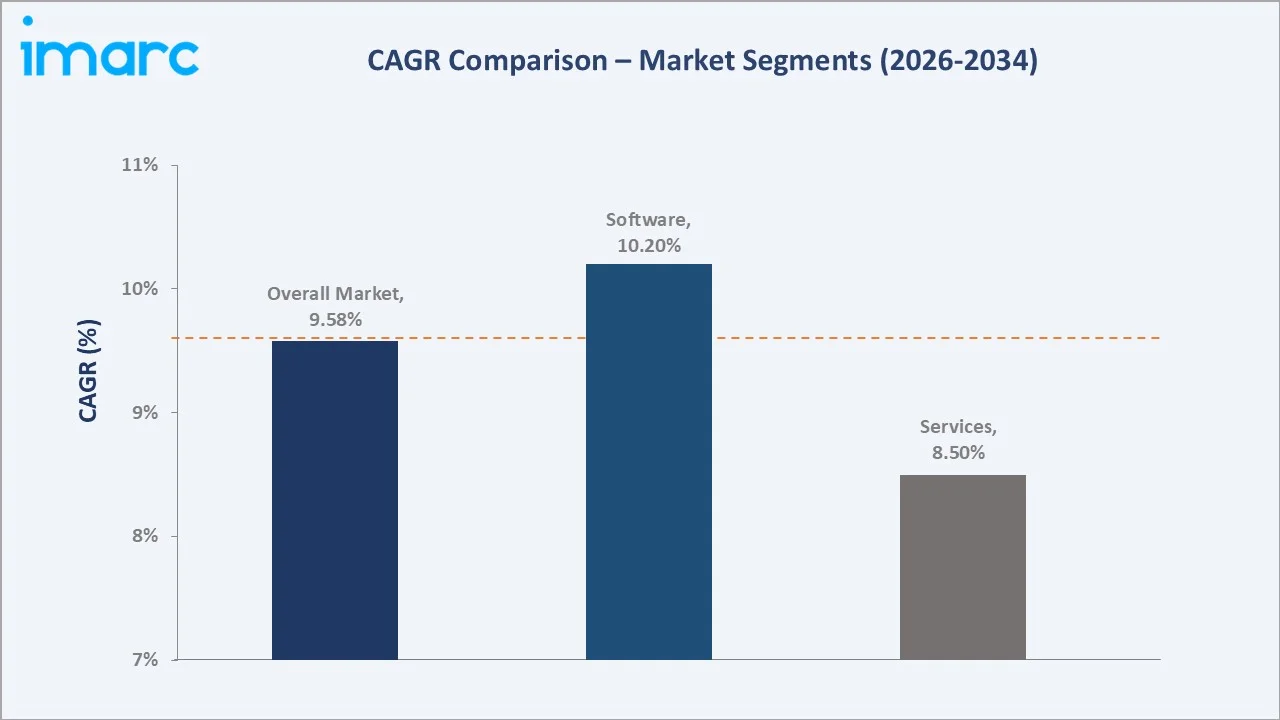

Software grows fastest at ~10.2% CAGR, driven by AI/ML-integrated GRC platforms, automated compliance workflows, and real-time risk dashboards. Services grow at ~8.5% CAGR through risk consulting, managed GRC services, and implementation support for complex enterprise deployments.

Executive Summary

The United States risk management market is on a strong growth trajectory, driven by escalating cyber threats, evolving compliance requirements, and enterprise-wide digital transformation. The market expanded from USD 2.33 Billion in 2020 to USD 3.68 Billion in 2025 and is projected to reach USD 8.58 Billion by 2034.

Organizations across BFSI, healthcare, IT, and retail are investing heavily in integrated GRC platforms to manage operational, financial, regulatory, and cyber risks in real time. The BFSI sector remains the dominant adopter, driven by stringent regulatory frameworks, including Dodd-Frank, Basel III, and SEC cybersecurity disclosure rules.

Cloud-based deployment at 68.4% is reshaping the market by enabling scalable, cost-effective risk management for both large enterprises and SMEs. Software leads at 63.8% as AI-powered analytics, automated risk assessments, and predictive compliance monitoring gain traction. The South region leads with 34.2% market share in 2025, supported by its strong financial services ecosystem and expanding tech sector.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Software - 63.8% share (2025) |

|

Dominant Deployment Mode |

Cloud-based - 68.4% market share (2025) |

|

Leading Region |

South - 34.2% share (2025) |

|

Market Opportunity |

AI/ML GRC automation; integrated cyber risk management; SME cloud-native risk platforms |

Key Analytical Observations Supporting the Above Data:

- Software at 63.8%: Software at 63.8% leads as organizations prioritize AI-integrated GRC platforms, automated compliance tools, and real-time risk dashboards over standalone services. These solutions reduce manual processes, improve risk visibility, and support audit-ready reporting across complex enterprise environments.

- Cloud-based at 68.4%: Cloud-based at 68.4% leads as enterprises migrate risk management infrastructure to scalable SaaS-based platforms. Cloud deployment lowers upfront capital expenditure, enables seamless updates, supports remote access, and provides multi-region compliance capabilities - making it preferred by both large enterprises and growing SMEs.

- South at 34.2%: South region leads at 34.2% due to its dense concentration of financial institutions, insurance firms, energy companies, and healthcare organizations in states such as Texas, Florida, and North Carolina. These sectors require robust risk management frameworks, particularly for regulatory compliance, cybersecurity, and operational continuity.

United States Risk Management Market Overview

The United States risk management market encompasses enterprise risk management (ERM), governance, risk and compliance (GRC), operational risk, financial risk, cybersecurity risk, and regulatory compliance solutions deployed across industries including BFSI, IT and telecom, retail, healthcare, energy, manufacturing, and government. The market integrates software platforms, managed services, consulting, and analytics tools to enable organizations to identify, assess, mitigate, and monitor risks in real time.

Macroeconomic factors influencing market growth include escalating frequency and severity of cyber incidents, heightened regulatory scrutiny from bodies such as the SEC, OCC, CISA, and NIST, and growing enterprise reliance on cloud infrastructure and digital business processes. The shift toward data-driven decision-making is also elevating demand for advanced risk quantification, scenario modeling, and automated compliance reporting capabilities.

Market Dynamics

To evaluate market opportunities, Request Sample

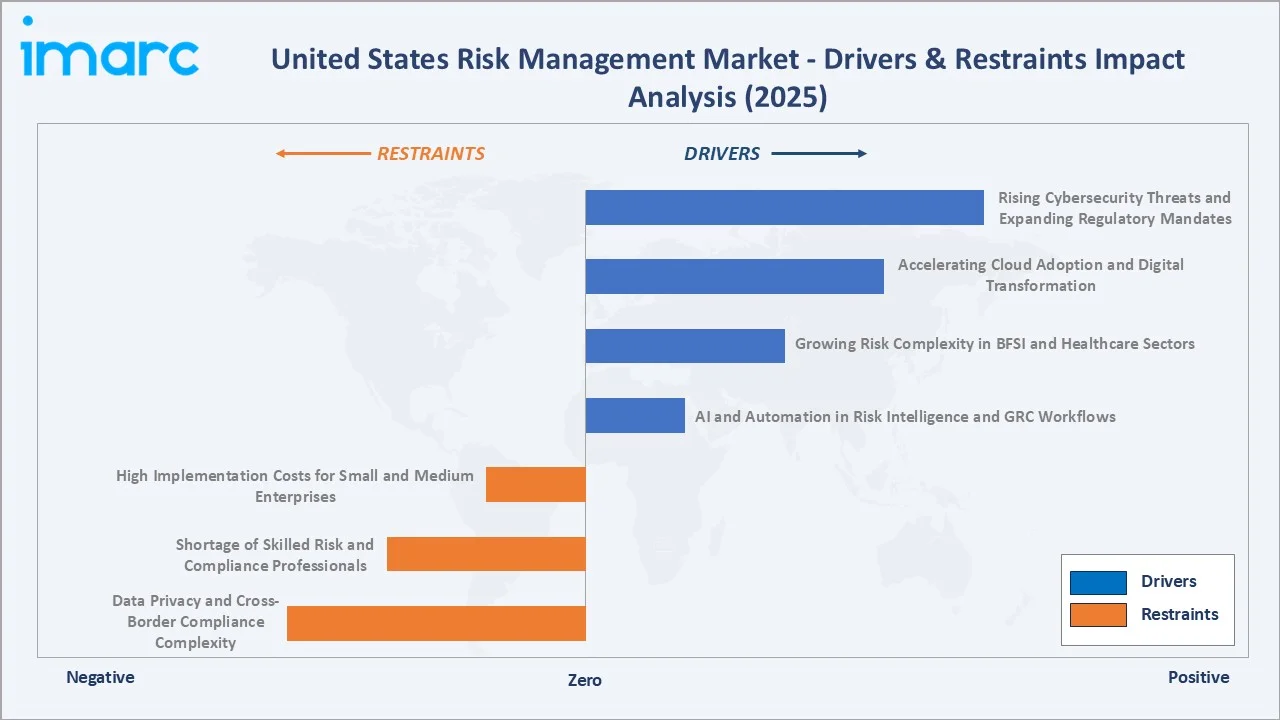

Market Drivers

- Rising Cybersecurity Threats and Expanding Regulatory Mandates: Cyberattacks targeting US enterprises surged in frequency and sophistication in recent years. The 2024 Internet Crime Report showed losses exceeding $16 billion, a 33% increase in losses from 2023, underscoring the urgency for robust risk management frameworks. Simultaneously, regulatory bodies including the SEC, OCC, and CISA have introduced stricter cybersecurity disclosure and risk governance requirements, compelling organizations to invest in integrated risk management platforms.

- Accelerating Cloud Adoption and Digital Transformation: The rapid migration of enterprise workloads to cloud environments is generating new risk exposures and driving demand for cloud-native risk management solutions. According to the National Institute of Standards and Technology (NIST), cloud security risk is now among the top priorities in federal cybersecurity frameworks. As organizations adopt hybrid cloud architectures, integrated risk management platforms that provide visibility across cloud and on-premises environments are becoming essential.

- Growing Risk Complexity in BFSI and Healthcare Sectors: The BFSI sector operates under stringent regulatory frameworks including Dodd-Frank, Basel III, and SEC cyber disclosure rules, necessitating continuous risk monitoring and compliance reporting. Similarly, healthcare organizations must comply with HIPAA, HITECH, and state-level data protection mandates. These regulatory complexities are driving sustained demand for automated compliance and risk management software across these high-growth verticals.

Market Restraints

- High Implementation Costs for Small and Medium Enterprises: Comprehensive risk management platforms often require significant upfront investment in licensing, integration, and staff training, creating adoption barriers for SMEs. While SaaS-based models are reducing this burden, many smaller organizations still struggle to justify full-scale GRC deployment. This cost sensitivity limits market penetration in the SME segment, particularly in sectors with thinner operating margins.

- Shortage of Skilled Risk and Compliance Professionals: The effective deployment and operation of advanced risk management platforms require certified risk professionals, data analysts, and compliance specialists. The US continues to face a shortage of qualified cybersecurity and risk management talent, with the (ISC)2 Cybersecurity Workforce Study estimating a workforce gap of approx. 500,000 professionals. This shortage slows effective platform adoption and limits the value organizations can extract from risk management investments.

Market Opportunities

- AI and Automation in Risk Intelligence and GRC Workflows: The integration of artificial intelligence and machine learning into GRC platforms is enabling real-time risk detection, predictive compliance monitoring, and automated audit trail generation. AI-powered risk intelligence tools can process vast volumes of structured and unstructured data to surface emerging risks faster than traditional methods. This creates significant opportunity for technology providers offering next-generation risk automation solutions.

- Expanding SME Adoption Through Cloud-Native Risk Platforms: Cloud-native, subscription-based risk management platforms are making enterprise-grade GRC tools accessible to small and medium enterprises. As SMEs increasingly digitize their operations and face growing regulatory scrutiny, demand for affordable, easy-to-deploy risk management software is accelerating. Vendors offering modular, scalable platforms targeted at SMEs are well-positioned to capture this emerging growth segment.

Market Challenges

- Integration Complexity with Legacy IT Systems: Many US enterprises, particularly in BFSI and manufacturing, operate on legacy IT infrastructure that is difficult to integrate with modern risk management platforms. Data silos, incompatible formats, and aging ERP systems increase implementation complexity and costs. This challenge can delay deployments and reduce the return on investment from risk management technology initiatives.

- Data Privacy and Cross-Border Compliance Complexity: Organizations operating across US states and international markets face a fragmented regulatory landscape, with varying data privacy requirements under CCPA, state-level privacy laws, and international regulations such as GDPR. Ensuring risk management platforms remain compliant with evolving, multi-jurisdictional data governance requirements adds operational complexity and increases the compliance burden for risk teams.

Emerging Market Trends

1. AI-Powered GRC Automation and Predictive Risk Analytics

AI-powered GRC automation is transforming how organizations identify and respond to risk. Predictive analytics tools process historical incident data, market signals, and regulatory changes to forecast risk exposure before materialization. This shift from reactive to predictive risk management is creating demand for intelligent risk platforms with embedded ML models, automated workflow triggers, and real-time scoring capabilities.

2. Integrated Cyber Risk Quantification (CRQ)

Cyber Risk Quantification is emerging as a critical practice, enabling organizations to express cybersecurity risks in financial terms for executive and board-level decision-making. Tools leveraging frameworks such as FAIR (Factor Analysis of Information Risk) allow CISOs to prioritize investments and demonstrate ROI. Growing SEC disclosure requirements are further accelerating adoption of CRQ methodologies.

3. Third-Party and Supply Chain Risk Management

Escalating reliance on third-party vendors and global supply chains has intensified focus on third-party risk management (TPRM). Organizations are deploying continuous monitoring tools to assess vendor cyber posture, financial stability, and regulatory compliance in real time. High-profile supply chain attacks have further elevated third-party risk management to a board-level priority.

4. ESG Risk Integration in Enterprise Risk Frameworks

Environmental, Social, and Governance (ESG) risk is being embedded into enterprise risk management frameworks as investors, regulators, and customers demand greater accountability. Evolving state, international, and investor-led climate disclosure requirements are increasing ESG risk reporting needs. This is creating demand for ERM platforms capable of integrating ESG metrics alongside traditional financial and operational risk data.

Industry Value Chain Analysis

The United States risk management value chain integrates data aggregation and intelligence, risk software development, system integration, deployment and managed services, risk analytics and reporting, and compliance and audit support.

|

Stage |

Key Participants |

|

Risk Data Aggregation & Intelligence |

Data providers, threat intelligence firms, financial data aggregators, regulatory monitoring services |

|

Risk Software Development |

GRC platform vendors, cybersecurity risk software firms, AI/ML analytics providers, compliance automation developers |

|

System Integration & Implementation |

IT systems integrators, ERP consultants, cloud migration specialists, managed service providers |

|

Deployment & Managed Services |

Cloud providers, SaaS risk platform operators, outsourced compliance service firms |

|

Risk Analytics & Reporting |

BI and analytics platforms, audit software providers, regulatory reporting specialists |

|

Compliance & Audit Support |

Audit firms, regulatory consultants, legal advisory firms, risk governance specialists |

The risk software development and AI-driven analytics stage represents the most value-added segment of the risk management value chain. This stage generates the highest differentiation through AI/ML algorithms, predictive risk modeling, automated compliance workflows, and real-time dashboarding that convert raw data into actionable risk intelligence. The ability to reduce manual compliance effort, improve audit readiness, and provide board-level risk visibility enables software providers to command premium margins above hardware or implementation services.

Technology Landscape in the United States Risk Management Industry

AI and Machine Learning in Risk Management

Artificial intelligence and machine learning are fundamentally transforming risk management by enabling real-time risk detection, pattern recognition, and predictive analytics. AI models analyze vast volumes of structured and unstructured data from internal systems, regulatory updates, threat intelligence feeds, and market signals to proactively surface risk patterns. Leading platforms now incorporate natural language processing (NLP) for automated regulatory change monitoring and risk policy analysis, enabling compliance teams to respond faster to evolving regulatory requirements.

Cloud-Based GRC and SaaS Risk Platforms

Cloud-native GRC platforms delivered through a software-as-a-service (SaaS) model have become the dominant technology architecture in the US risk management market. These platforms enable centralized risk data management, cross-functional collaboration, and scalable compliance workflows without the capital expenditure associated with on-premises deployments. Major providers have built multi-tenant cloud environments compliant with FedRAMP, SOC 2, and ISO 27001 standards to serve regulated industries including BFSI and healthcare.

Integrated Cybersecurity Risk Management Technology

As cyber risk becomes a top-tier enterprise priority, integrated cybersecurity risk management platforms that bridge the gap between security operations and GRC functions are gaining adoption. Technologies such as continuous control monitoring (CCM), attack surface management, and SIEM integration are enabling organizations to maintain a real-time view of their cyber risk posture. These solutions align with frameworks including NIST CSF, CIS Controls, and ISO 27001, enabling consistent risk measurement and regulatory reporting.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Software |

63.8% |

2025 |

|

Deployment Mode |

Cloud-based |

68.4% |

2025 |

|

Enterprise Size |

🔒 |

🔒 |

2025 |

|

Industry Vertical |

🔒 |

🔒 |

2025 |

|

Region |

South |

34.2% |

2025 |

By Component

Software leads at 63.8% in 2025, as organizations prioritize AI-integrated GRC platforms, automated compliance monitoring, and real-time risk intelligence dashboards. Software solutions reduce manual compliance effort, improve audit trail generation, and provide board-level risk visibility, making them the preferred investment for enterprise risk programs. Scalable SaaS-based models have further accelerated software adoption across both large enterprises and SMEs.

To access detailed market analysis, Request Sample

Services at 36.2% grow at ~8.5% CAGR through GRC implementation consulting, risk program management, managed compliance services, and training - driven by enterprises that require advisory support alongside platform deployment.

By Deployment Mode

Cloud-based leads at 68.4% in 2025, driven by the broad enterprise migration to SaaS-based GRC platforms that offer scalability, lower total cost of ownership, and simplified regulatory compliance. Cloud deployment eliminates on-premises infrastructure costs and enables continuous platform updates, which is particularly valued in a dynamic regulatory environment.

On-premises at 31.6% remain significant among highly regulated industries such as financial services and government, where data residency, security controls, and legacy system integration requirements favor localized deployments.

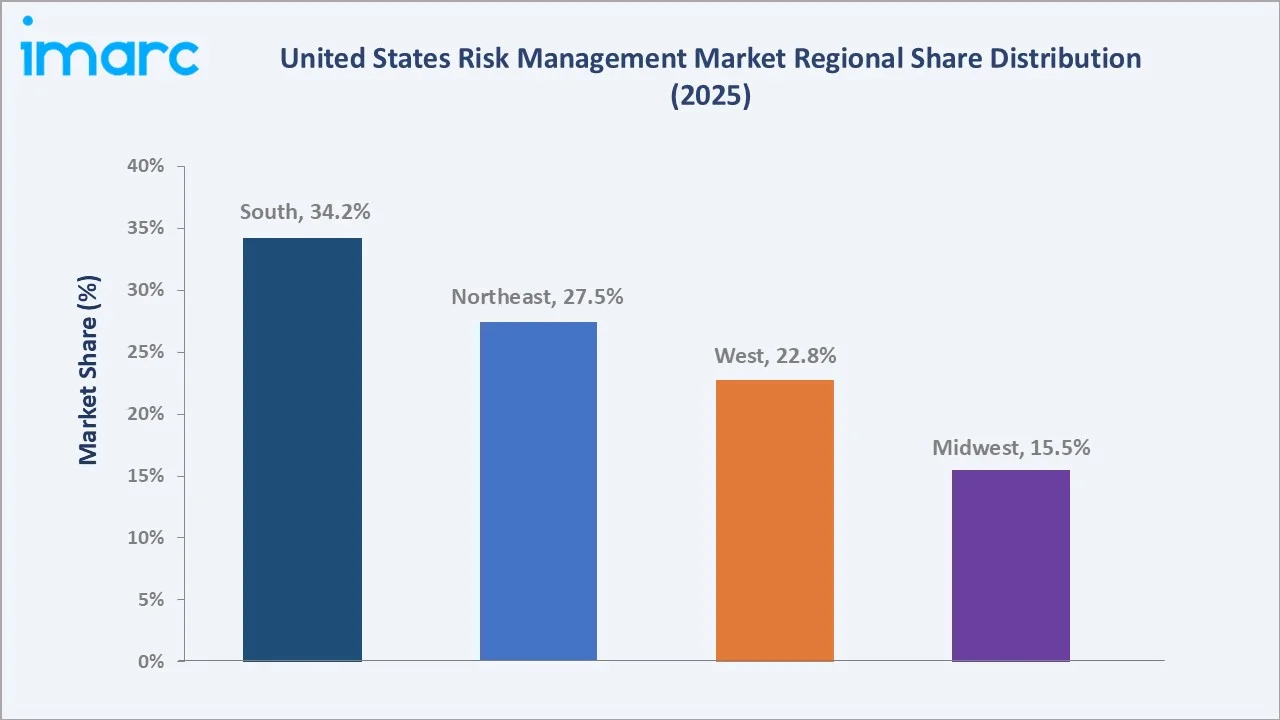

Regional Market Insights

|

Region |

Share (2025) |

Key US Risk Management Market Drivers & Characteristics |

|

South |

34.2% |

Reflects a dense concentration of financial institutions, energy firms, healthcare networks, and insurance companies. Strong regulatory compliance activity across Texas, Florida, and North Carolina drives sustained demand for integrated risk management platforms. |

|

Northeast |

27.5% |

Reflects its position as the US financial services and insurance hub, with major banks, asset managers, and insurance companies concentrated in New York and Connecticut driving advanced GRC and financial risk management adoption. |

|

West |

22.8% |

Reflects the concentration of technology companies, cloud infrastructure providers, and digital-first enterprises in California and Washington, driving demand for cybersecurity risk and cloud-native GRC solutions. |

|

Midwest |

15.5% |

Reflects manufacturing, healthcare, and industrial enterprise base requiring operational risk management, supply chain risk, and regulatory compliance solutions across Illinois, Ohio, and Michigan. |

The South region's 34.2% dominance reflects the concentration of BFSI, energy, and healthcare organizations that operate under some of the most demanding risk and regulatory compliance environments in the US. The Northeast at 27.5% is anchored by its deep financial services ecosystem, with New York serving as the center of US capital markets risk management activity.

West at 22.8% benefits from technology sector growth, expanding cybersecurity risk spending, and a strong venture-backed GRC startup ecosystem. Midwest at 15.5% is supported by manufacturing sector risk compliance needs, growing healthcare data security requirements, and expanding industrial risk management deployments.

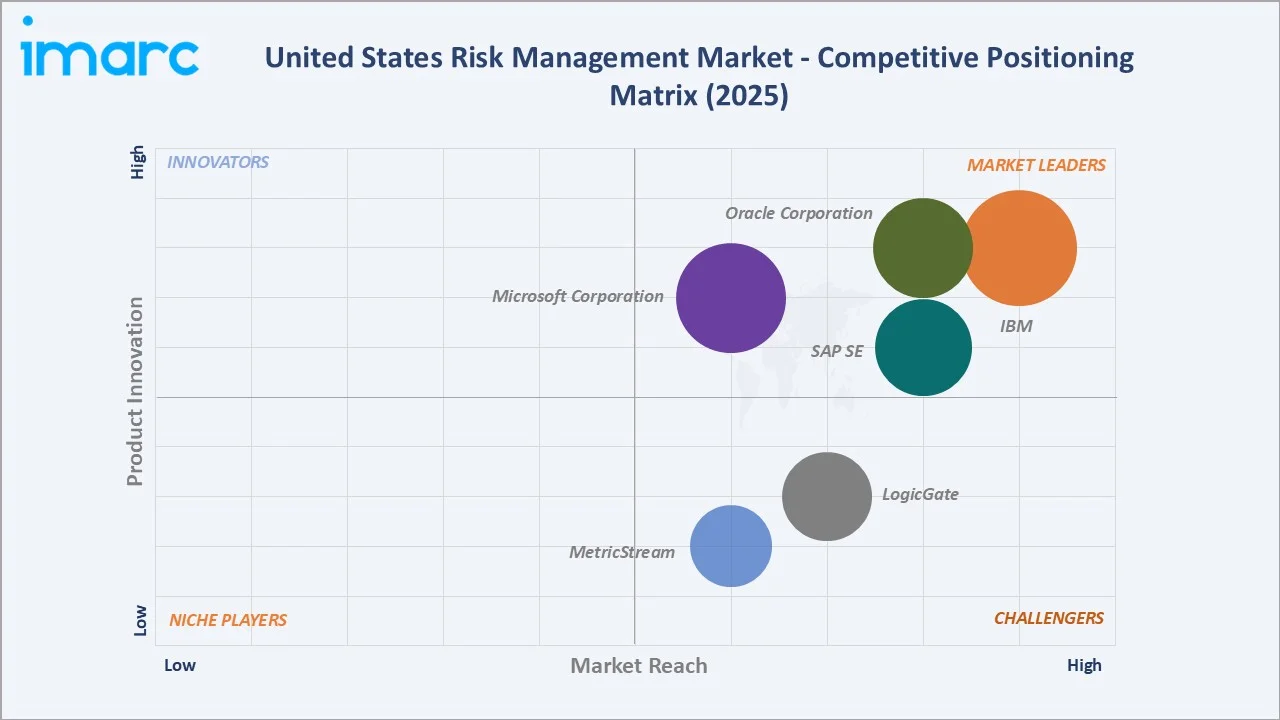

Competitive Landscape

The United States risk management market is moderately concentrated, with competition among large enterprise software providers, specialized GRC platform vendors, cybersecurity risk specialists, and consulting-led risk management firms. Competitive differentiation centers on AI-powered risk analytics, automation of compliance workflows, depth of regulatory coverage, and integration capability with enterprise systems including ERP, ITSM, and security operations platforms.

|

Company Name |

Brand / key Product |

Market Position |

Core Strength |

|

IBM |

IBM OpenPages |

Market Leader |

IBM OpenPages is a leading enterprise GRC platform offering AI-powered risk analytics, regulatory change management, and integrated operational risk monitoring across BFSI, healthcare, and government sectors. |

|

SAP SE |

SAP Risk Management |

Market Leader |

SAP GRC provides deep integration with SAP ERP environments, enabling automated access controls, process risk management, and regulatory compliance monitoring for large enterprises. |

|

Oracle Corporation |

Oracle Fusion Cloud Risk Management and Compliance (also known as Oracle Risk Management Cloud) |

Market Leader |

Oracle Risk Management Cloud delivers financial risk management, audit, and compliance capabilities tightly integrated with Oracle ERP and EPM platforms for enterprise clients. |

|

Microsoft Corporation |

Microsoft Purview Insider Risk Management/ Microsoft Priva Risk Management |

Market Leader |

Microsoft Purview Insider Risk Management offers native integration within the Microsoft 365 ecosystem, robust privacy-by-design architecture, and ability to automatically correlate multi-channel signals to detect intellectual property theft, data leakage, and security violations. |

|

MetricStream |

MetricStream ConnectedGRC |

Challenger |

MetricStream provides a purpose-built GRC platform with modular applications for enterprise risk, IT risk, cyber risk, and regulatory compliance, with strong presence across financial services and life sciences. |

|

LogicGate |

Risk Cloud |

Challenger |

LogicGate's Risk Cloud platform offers a no-code, highly configurable GRC environment targeting mid-market enterprises seeking flexible, rapidly deployable risk management workflows. |

Companies are increasingly investing in AI-driven risk intelligence, continuous control monitoring, third-party risk management capabilities, and ESG risk integration to strengthen their competitive positions. Strategic partnerships with cloud hyperscalers and systems integrators are also becoming a key growth strategy.

Key Company Profiles

IBM

IBM is a leading technology and consulting company with a strong presence in the US risk management market through its IBM OpenPages GRC platform. IBM OpenPages provides enterprise-grade governance, risk, and compliance management capabilities, including operational risk, financial risk, IT risk, and regulatory compliance monitoring.

- Key Product: IBM OpenPages

- Recent Developments: In March 2026, IBM introduced OpenPages 9.2 which reflects a model with which intelligence can be configured into the platform to help organizations operate with greater speed, consistency and control.

- Strategic Focus: Strengthening AI-powered GRC automation, expanding regulatory content libraries, and deepening integration with IBM Cloud and hybrid cloud environments. IBM targets large enterprises and regulated industries including BFSI, healthcare, and energy.

SAP SE

SAP SE is a global enterprise software leader with a significant presence in the US risk management market through its SAP GRC suite. SAP GRC enables organizations to manage access controls, process controls, and risk management within SAP ERP environments.

- Key Product: SAP Risk Management

- Recent Developments: In May 2026, SAP SE introduced Autonomous Enterprise to aid enhance critical business workflows, so that humans and AI can integrate to meet the rising demands of global business profitably, strategically, and safely.

- Strategic Focus: Deepening integration of risk management into core ERP workflows, expanding cloud-native GRC capabilities, and addressing ESG compliance requirements for enterprise clients across manufacturing, BFSI, and retail.

Oracle Corporation

Oracle Corporation is a major enterprise technology provider with Oracle Risk Management Cloud as its flagship product in the US risk management market. Oracle's solutions support financial risk, access control, audit, and regulatory compliance across large enterprise environments.

- Key Product: Oracle Fusion Cloud Risk Management and Compliance (also known as Oracle Risk Management Cloud)

- Strategic Focus: Expanding cloud-native risk management within the Oracle Cloud Infrastructure ecosystem, with a focus on financial services risk quantification, audit automation, and cross-enterprise compliance reporting.

Microsoft Corporation

Microsoft Corporation is a dominant player in the US risk management market through its Microsoft Purview Compliance Manager and broader compliance and security suite. Microsoft's integrated approach embeds risk and compliance management within enterprise productivity and cloud environments.

- Key Products: Microsoft Purview Insider Risk Management/ Microsoft Priva Risk Management

- Strategic Focus: Expanding end-to-end data governance and risk management capabilities across the Microsoft ecosystem, targeting enterprises managing complex multi-cloud and hybrid compliance environments.

Market Concentration Analysis

The United States risk management market exhibits a moderately concentrated structure, with a mix of large enterprise software vendors, specialized GRC platform providers, and cybersecurity-focused risk management firms. Established technology leaders including IBM, SAP, Oracle, and Microsoft hold strong positions through their deep ERP integration, broad regulatory coverage, and large enterprise customer bases.

Market competition is increasingly centered on AI-powered risk analytics, cloud-native GRC delivery models, continuous compliance monitoring, and real-time cyber risk quantification. Mid-tier challengers including MetricStream and LogicGate are gaining traction through purpose-built GRC platforms that offer greater configurability and faster deployment timelines compared to large enterprise suites.

Strategic partnerships between GRC platform providers, cloud hyperscalers, management consulting firms, and cybersecurity vendors are becoming a key competitive strategy. While established players dominate large enterprise programs, specialized niche providers are expanding market share in high-growth segments including third-party risk management, ESG risk integration, and SME cloud-native GRC.

Investment & Growth Opportunities

Highest Growth Segments

Software components (~10.2% CAGR), Small and Medium-sized Enterprises (~11% CAGR), and industry verticals led by IT and Telecom and BFSI (~10–10.5% CAGR) represent the US risk management market's highest-growth investment vectors through 2034, against an overall market CAGR of ~9.58%. Healthcare and Energy and Utilities verticals are also gaining momentum, while on-premises deployment and large enterprise segments are expected to grow at a more moderate pace in line with or below the market average.

Investment Themes

AI-Driven GRC Automation and Risk Intelligence

AI-powered GRC platforms that automate regulatory change monitoring, risk scoring, control testing, and audit workflows represent a high-priority investment area. These solutions reduce compliance costs by up to 40-60% compared to manual processes, making them attractive for both enterprise and mid-market buyers. Investment in AI risk intelligence platforms that integrate external threat feeds, internal data, and regulatory signals offers strong commercial opportunity.

Cyber Risk Quantification and Financial Risk Modeling

As SEC cyber rules require disclosure of material cyber incidents and related risk management, strategy, and governance information, demand for CRQ tools is accelerating. Platforms that use quantitative frameworks such as FAIR to express cyber risk in monetary terms are attracting strong interest from Fortune 500 companies and regulated financial institutions. Early investment in this segment captures the growing intersection of cybersecurity, finance, and regulatory reporting.

Third-Party and Supply Chain Risk Management Platforms

Third-party risk management is among the fastest-growing segments as organizations scale continuous monitoring of vendor cyber posture, financial stability, and regulatory compliance. Investment in automated TPRM platforms capable of handling thousands of vendor relationships with AI-driven risk scoring and continuous monitoring capabilities presents significant commercial opportunity.

Future Market Outlook (2026-2034)

The US risk management market is projected to grow from USD 3.68 Billion in 2025 to USD 8.58 Billion by 2034, delivering a 9.58% CAGR over the forecast period through AI-driven GRC transformation, expanding regulatory compliance requirements, growing SME adoption, and rising cyber risk management spending. The market's anchor value of USD 5.81 Billion in 2030 reflects US risk management at a critical AI and cloud adoption inflection.

Three structural forces define the United States risk management market growth through 2034. First, accelerating regulatory complexity across BFSI, healthcare, energy, and technology sectors will drive sustained demand for integrated compliance and risk management platforms. Second, the growing convergence of cybersecurity and enterprise risk management will create demand for unified risk intelligence solutions that bridge GRC and security operations. Third, AI and automation adoption will fundamentally restructure risk management workflows, replacing manual compliance processes and enabling real-time risk visibility at enterprise scale.

As organizations increasingly embed risk management into core digital operations and board-level strategy, the market will see sustained growth across software, services, and cloud-native risk platforms through 2034. SME adoption, international regulatory alignment, and ESG risk integration will open new growth vectors beyond the traditional large enterprise BFSI-focused market.

Research Methodology

Primary Research

Primary research comprised interviews with risk management software vendors, GRC consultants, chief risk officers, compliance leaders, BFSI executives, healthcare compliance teams, and IT risk specialists. The research captured insights on technology adoption trends, platform selection criteria, regulatory priorities, pricing, and risk management program maturity. These inputs validated market sizing, competitive dynamics, and growth opportunity assessments.

Secondary Research

Secondary research encompassed company websites, annual reports, investor presentations, SEC filings, NIST publications, OCC regulatory guidance, CISA frameworks, industry association reports, GRC analyst research, and regulatory change monitoring databases. It also included analysis of enterprise software spending trends, cloud migration patterns, cybersecurity investment data, and GRC market competitive developments.

Forecasting Models

Forecasting models combined historical market trends, enterprise IT spending growth, regulatory compliance investment patterns, and GRC platform adoption rates across industry verticals. A bottom-up approach assessed demand by component, deployment mode, enterprise size, industry vertical, and region, while a top-down analysis validated overall market potential. Forecasts incorporated technology adoption trends including AI-driven risk automation, cloud-native GRC deployment, and emerging cyber risk quantification methodologies.

United States Risk Management Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Software, Services |

| Deployment Modes Covered | On-premises, Cloud-based |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| Industry Verticals Covered | BFSI, IT and Telecom, Retail, Healthcare, Energy and Utilities, Manufacturing, Government and Defense, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | IBM, SAP SE, Oracle Corporation, Microsoft Corporation, MetricStream, LogicGate, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States risk management market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States risk management market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States risk management industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Risk Management Market Report

The US risk management market reached USD 3.68 Billion in 2025, driven by rising cyber threats, expanding compliance mandates, and enterprise GRC platform adoption across BFSI, healthcare, and IT sectors.

The US risk management market grows at 9.58% CAGR during 2026-2034, reaching USD 8.58 Billion by 2034, supported by AI-driven GRC automation, cloud adoption, and escalating regulatory requirements.

Software leads at 63.8% in 2025, driven by enterprise demand for AI-integrated GRC platforms, automated compliance tools, and real-time risk dashboards across BFSI, healthcare, and IT sectors.

Cloud-based deployment dominates at 68.4% in 2025, driven by enterprise SaaS platform adoption, lower total cost of ownership, and scalable compliance management across hybrid cloud environments.

The South region leads at 34.2% in 2025, driven by dense concentration of financial institutions, insurance firms, healthcare networks, and energy companies in Texas, Florida, and North Carolina.

Leading companies include IBM, SAP SE, Oracle Corporation, Microsoft Corporation, MetricStream, and LogicGate, among others.

The market is projected to reach USD 5.81 Billion by 2030, supported by rising AI-powered risk automation, expanding cloud-native GRC adoption, and growing regulatory compliance requirements across all sectors.

Top opportunities include AI-driven GRC automation platforms, cyber risk quantification tools aligned with SEC disclosure requirements, third-party risk management solutions, and cloud-native SME risk platforms.

Key drivers include escalating cybersecurity threats, expanding SEC and CISA compliance mandates, rapid cloud adoption, growing BFSI and healthcare risk requirements, and increasing board-level risk governance focus.

Major challenges include high implementation costs for SMEs, shortage of qualified risk and compliance professionals, integration complexity with legacy IT systems, and managing multi-jurisdictional regulatory compliance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)