United States Solar Panel Market Size, Share, Trends and Forecast by Type, End Use, and Region, 2026-2034

United States Solar Panel Market Size, Share, Trends & Forecast (2026-2034)

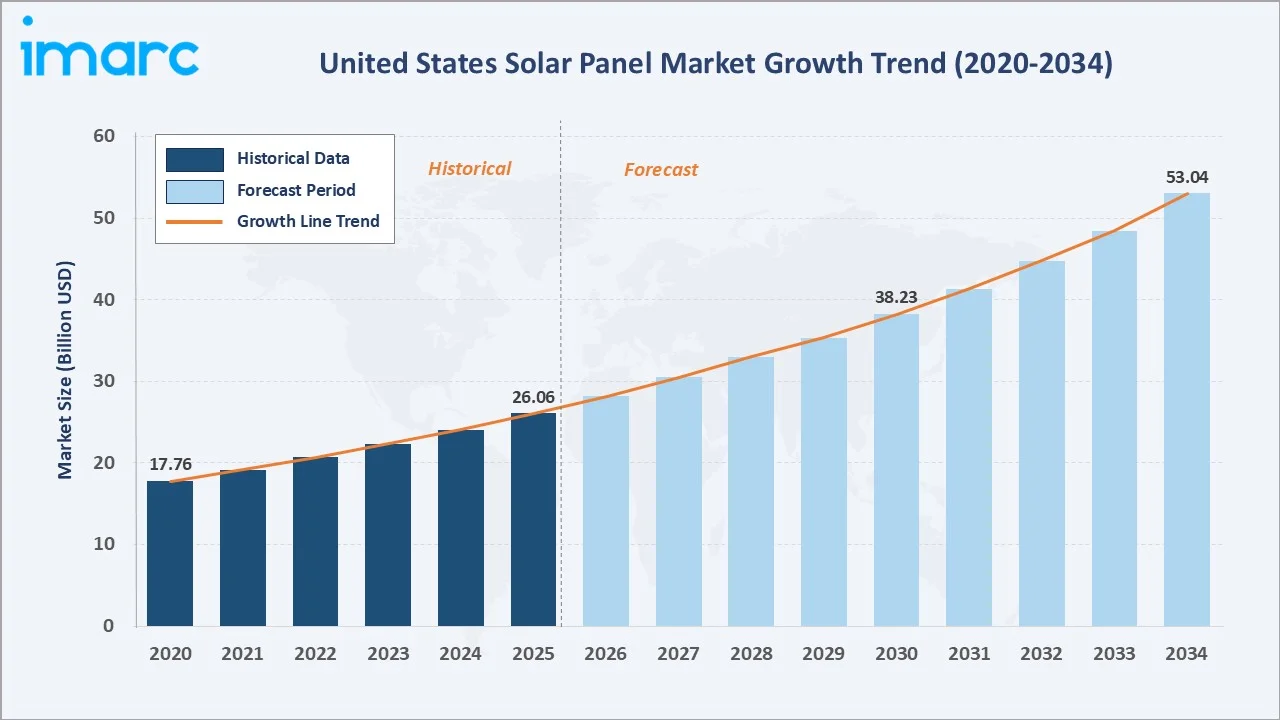

The United States solar panel market reached USD 26.06 Billion in 2025 and is projected to reach USD 53.04 Billion by 2034, growing at a CAGR of 7.97% during 2026-2034. The market is driven by declining module costs, federal Investment Tax Credits, rising electricity prices, and accelerating clean energy commitments by utilities and corporations.

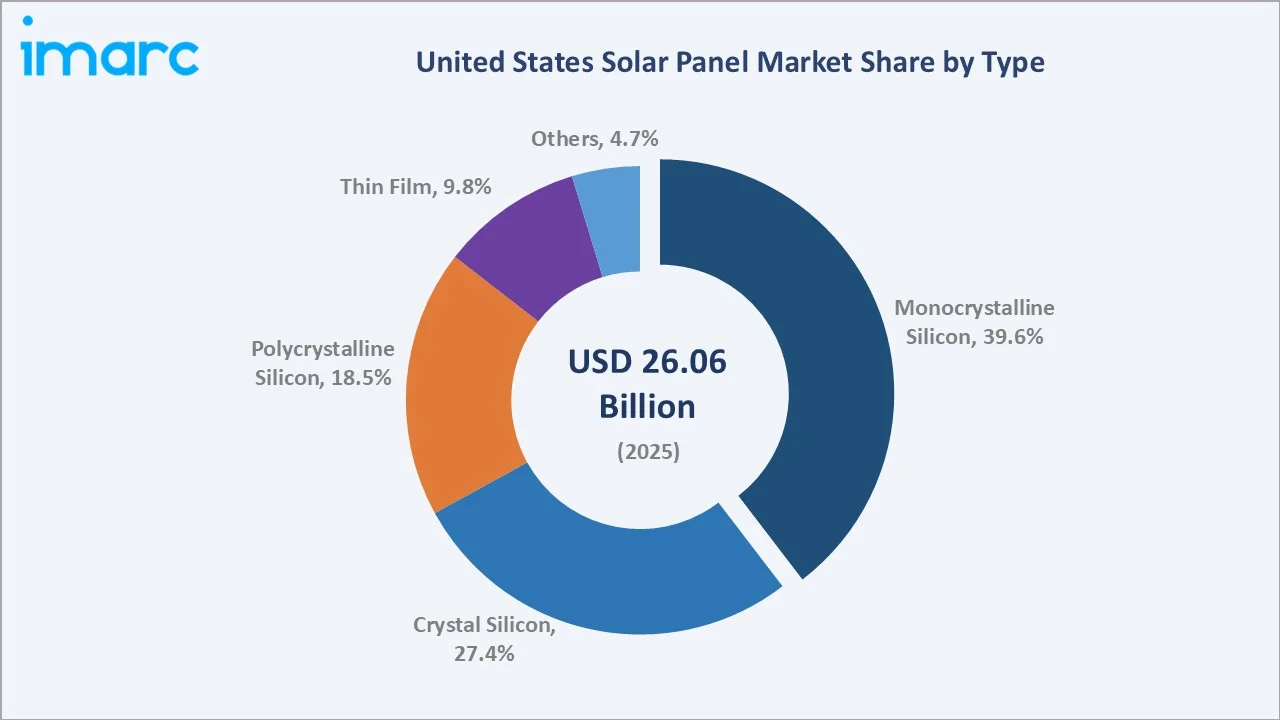

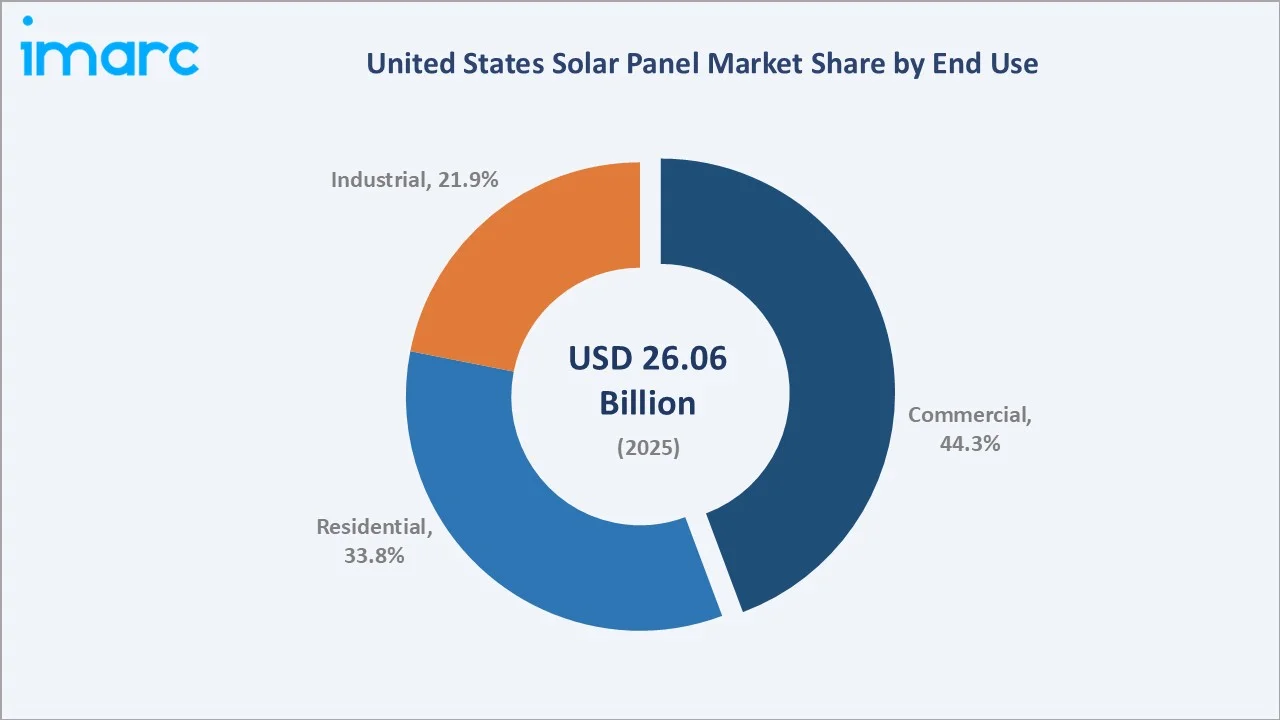

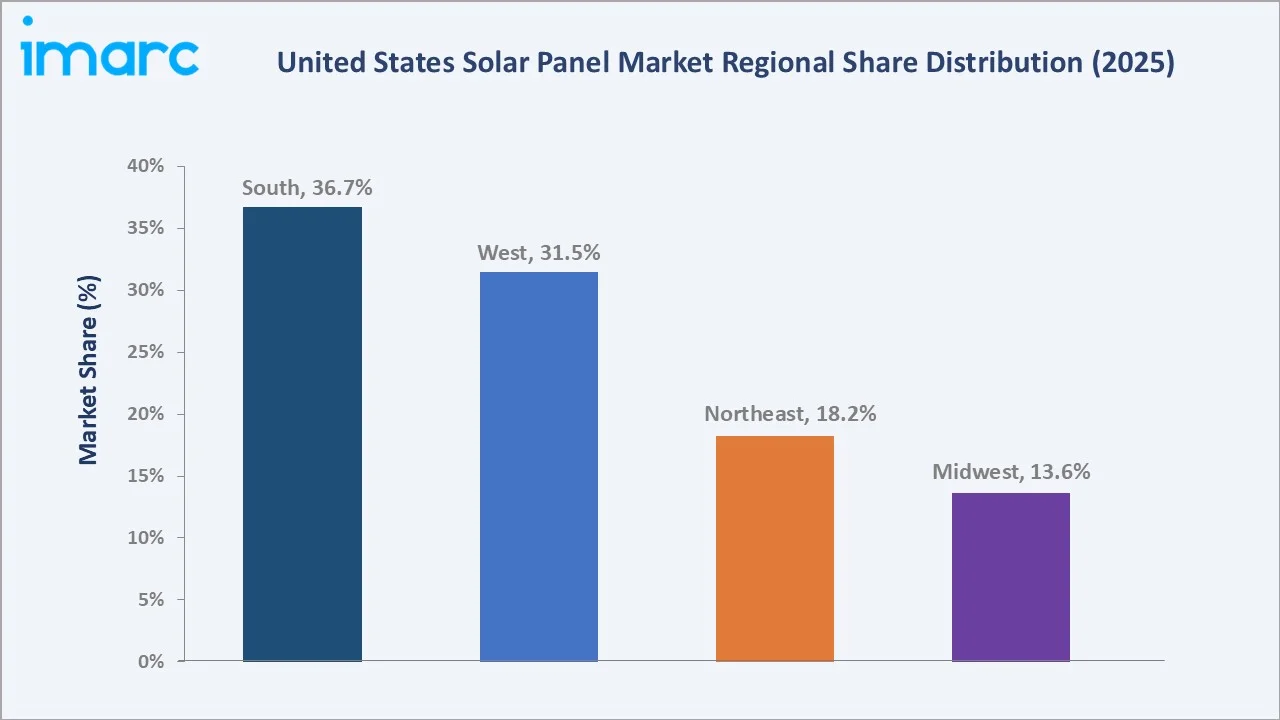

Monocrystalline silicon dominates at 39.6%, commercial end use leads at 44.3%, and the South region commands 36.7% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 26.06 Billion |

|

Forecast Market Size (2034) |

USD 53.04 Billion |

|

CAGR (2026-2034) |

7.97% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Monocrystalline Silicon (39.6%, 2025) |

|

Dominant End Use |

Commercial (44.3%, 2025) |

|

Leading Region |

South (36.7%, 2025) |

The market expanded from USD 17.76 Billion in 2020 to USD 26.06 Billion in 2025, anchored at USD 38.23 Billion in 2030, and forecast to reach USD 53.04 Billion by 2034. Brief supply-chain headwinds in 2021-2022 were overcome as the Inflation Reduction Act accelerated module procurement through 2023-2025.

Executive Summary

The United States solar panel market reached USD 26.06 Billion in 2025, ranking among the world's largest national solar markets, underpinned by the clean-energy transformation of the national electric grid. The market is projected to reach USD 53.04 Billion by 2034, delivering a 7.97% CAGR over the forecast period.

To get more information on this market, Request Sample

Monocrystalline silicon at 39.6% dominates by capturing the high-efficiency residential and commercial rooftop segment. Commercial end use at 44.3% leads through utility-scale and C&I solar procurement driven by corporate sustainability targets and IRA tax credits. The South region at 36.7% commands the largest share through high solar irradiance and strong state-level renewable energy mandates.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Monocrystalline Silicon – 39.6% share (2025) |

|

Dominant End Use |

Commercial – 44.3% market share (2025) |

|

Leading Region |

South – 36.7% market share (2025) |

|

Market Opportunity |

Bifacial TOPCon; agrivoltaics; floating solar; BIPV; community solar |

Key Analytical Observations Supporting the Above Data:

- Monocrystalline Silicon at 39.6%: Dominates due to the highest efficiency ratings (20–23%), declining manufacturing costs, and preference across residential and commercial rooftop applications for maximum power per unit area. Widespread adoption by major installers across all US regions reinforces segment leadership.

- Commercial at 44.3%: Leads through large-scale rooftop, carport, and ground-mount projects by retail chains, data centres, and municipal utilities leveraging the 30% Investment Tax Credit under the Inflation Reduction Act.

- South at 36.7%: Benefits from the highest solar irradiance in the contiguous US, large available land parcels, and strong renewable portfolio standards in Texas, Florida, and the Carolinas, generating a robust utility-scale project pipeline.

United States Solar Panel Market Overview

The US solar panel market encompasses the design, manufacture, distribution, and installation of photovoltaic (PV) modules across residential, commercial, and industrial applications nationwide. The ecosystem integrates polysilicon producers, cell manufacturers, module assemblers, BOS suppliers, EPC contractors, utilities, and federal and state regulatory bodies.

Macroeconomic tailwinds include the Inflation Reduction Act's 30% Investment Tax Credit, solar cost reduction targets, rising retail electricity tariffs, and corporate net-zero commitments. Section 201 tariffs and IRA domestic content adders are reshaping module procurement toward US-manufactured products.

Market Dynamics

To evaluate market opportunities, Request Sample

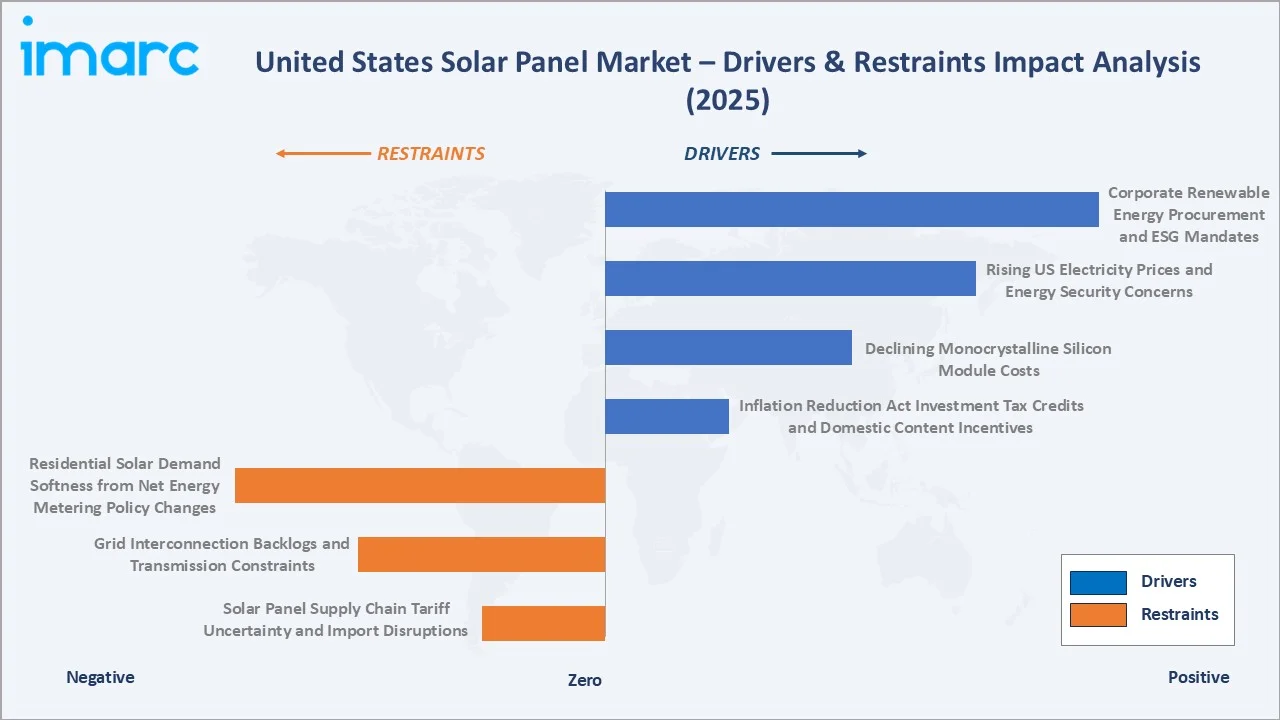

Market Drivers

- Inflation Reduction Act Investment Tax Credits and Domestic Content Incentives: Favorable government incentives, tax credits, and policy support continue to strengthen the economic viability of solar energy projects across residential, commercial, and utility-scale segments. These initiatives encourage capital investment, support project development activities, and create a stable regulatory environment that promotes long-term growth in the United States Solar Panel Market.

- Declining Monocrystalline Silicon Module Costs: Continuous advancements in manufacturing processes, economies of scale, and technological innovation have contributed to a steady decline in solar panel costs over the years. Improved affordability, combined with higher module efficiency and performance, has enhanced project returns and expanded solar adoption across a wider range of customer segments and geographic regions.

- Rising US Electricity Prices and Energy Security Concerns: Increasing electricity costs and growing concerns regarding energy reliability are encouraging consumers, businesses, and utilities to invest in solar energy solutions. Solar power offers greater control over long-term energy expenditures while reducing dependence on traditional energy sources. The increasing emphasis on energy security and resilience is further supporting investments in solar and integrated renewable energy systems.

- Corporate Renewable Energy Procurement and ESG Mandates: Growing corporate focus on sustainability, carbon reduction, and environmental responsibility is driving increased investment in renewable energy solutions. Organizations across various industries are adopting solar energy through direct installations, renewable energy procurement agreements, and broader clean energy strategies to achieve sustainability objectives and strengthen their environmental, social, and governance (ESG) performance.

Market Restraints

- Solar Panel Supply Chain Tariff Uncertainty and Import Disruptions: The solar industry relies on a complex global supply chain for raw materials, components, and finished products. Changes in trade policies, import regulations, geopolitical developments, and supply chain disruptions can create uncertainty in procurement activities and affect equipment availability. Such challenges may increase project costs, impact delivery schedules, and create operational complexities for manufacturers, developers, and installers.

- Grid Interconnection Backlogs and Transmission Constraints: The rapid expansion of solar energy projects is placing increasing pressure on existing grid infrastructure. Delays in interconnection approvals, transmission network limitations, and capacity constraints can slow the integration of new solar projects into the electricity system. These infrastructure challenges may extend project development timelines and limit the pace of renewable energy deployment in certain regions.

- Residential Solar Demand Softness from Net Energy Metering Policy Changes: Changes in net metering policies and residential solar compensation frameworks can influence the financial attractiveness of rooftop solar installations. Reduced incentives or modifications to compensation mechanisms may impact consumer investment decisions, lengthen payback periods, and moderate residential solar adoption rates in some markets. As a result, installers and developers may face challenges in maintaining growth momentum within the residential segment.

Market Opportunities

- Agrivoltaics and Floating Solar: Innovative solar deployment models such as agrivoltaics and floating solar systems are creating new growth opportunities within the solar industry. Agrivoltaic projects enable the simultaneous use of land for both agricultural activities and renewable energy generation, improving land-use efficiency and supporting additional revenue opportunities for landowners. Similarly, floating solar installations on reservoirs, lakes, and other water bodies offer an alternative solution in areas where land availability is limited, while also contributing to greater renewable energy capacity expansion.

- Building-Integrated Photovoltaics (BIPV): The integration of solar technology directly into building materials such as rooftops, facades, windows, and exterior structures is gaining increasing attention across residential and commercial construction projects. Growing emphasis on sustainable building design, energy-efficient infrastructure, and green construction practices is creating favorable conditions for BIPV adoption. These solutions provide both electricity generation and architectural functionality, enhancing their attractiveness in modern building developments.

Market Challenges

- Domestic Manufacturing Scale-Up Execution Risk: Expanding domestic solar manufacturing capacity requires substantial investments in production facilities, equipment, supply chain development, and operational capabilities. Challenges associated with scaling manufacturing operations, securing critical inputs, and establishing efficient production networks may affect the pace at which capacity additions are realized. Any delays in manufacturing expansion could impact product availability and influence the industry's ability to meet growing market demand.

- Skilled Workforce Shortage for Solar Installation: The continued growth of the solar industry is increasing demand for skilled professionals involved in manufacturing, engineering, installation, operations, and maintenance activities. However, the availability of adequately trained personnel may not always keep pace with market expansion. Workforce shortages can contribute to higher labor costs, project execution delays, and operational inefficiencies, creating challenges for developers and service providers seeking to support large-scale solar deployment.

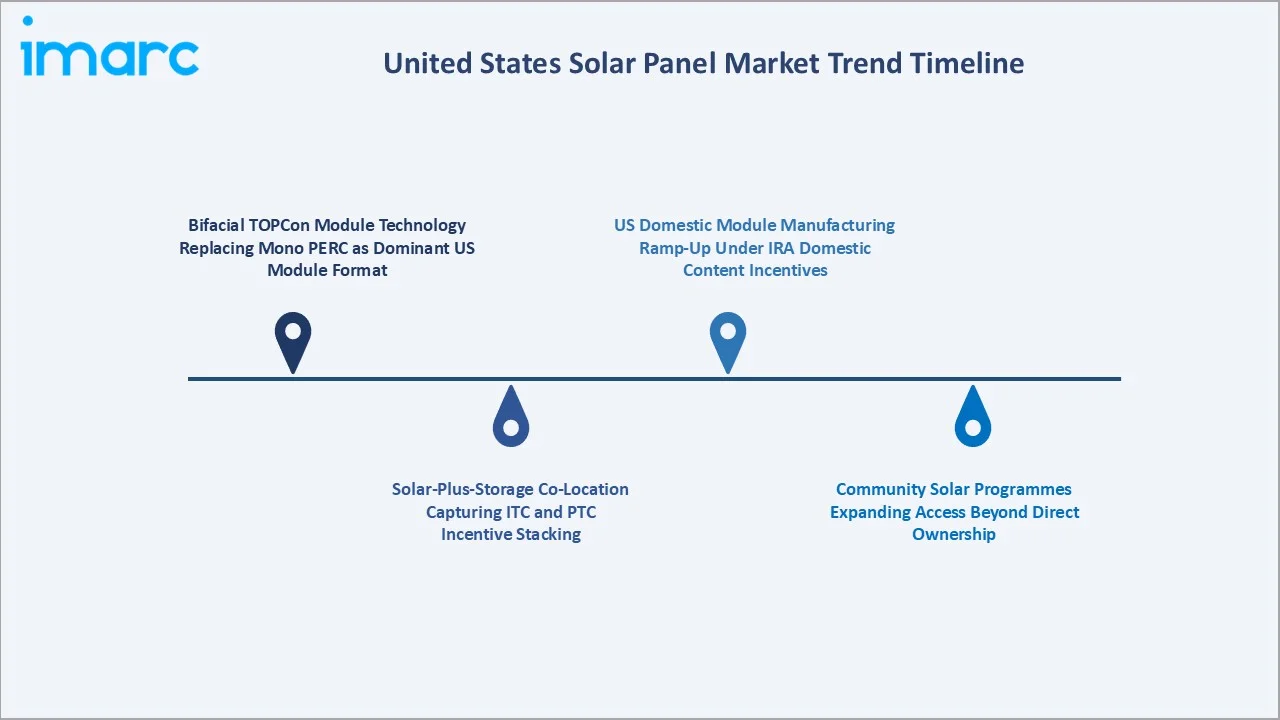

Emerging Market Trends

1. Bifacial TOPCon Module Technology Replacing Mono PERC as Dominant US Module Format

Bifacial TOPCon module technology is displacing mono PERC as the dominant US solar procurement specification. TOPCon modules achieve higher efficiency (22–23%) and greater bifacial gain, reducing levelised cost of electricity. Major US utility and C&I procurement contracts are increasingly specifying TOPCon, accelerating technology transition across the supply chain.

2. Solar-Plus-Storage Co-Location Capturing ITC and PTC Incentive Stacking

IRA provisions permit co-located battery storage charged exclusively from solar to qualify for the Investment Tax Credit. Solar-plus-storage co-location improves project IRRs, creating system-level economics that accelerate utility-scale procurement. Developers are integrating storage into new solar projects to capture full incentive stacking benefits.

3. Community Solar Programmes Expanding Access Beyond Direct Ownership

State-mandated community solar programmes are expanding solar access to renters, low-income households, and commercial tenants who cannot host direct rooftop installations. Subscriber-based models create a new distributed solar demand pool, with community solar capacity additions expected to exceed 5 GW annually by 2028 across major US markets.

4. US Domestic Module Manufacturing Ramp-Up Under IRA Domestic Content Incentives

IRA domestic content adders worth 10–20 percentage points of additional ITC value are triggering US module manufacturing investments by First Solar, Hanwha Q CELLS, and emerging players. US-manufactured modules qualifying for domestic content adders command a 5–12% premium in project pricing, creating durable competitive advantages for domestic producers.

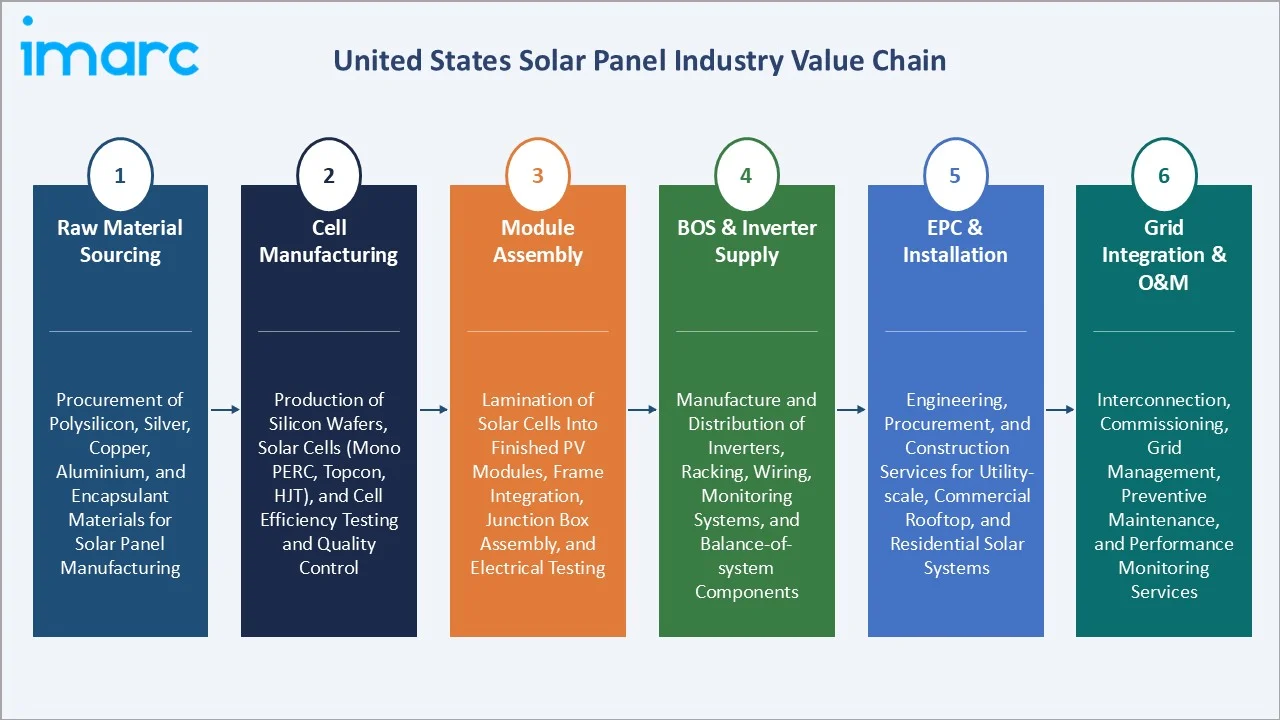

Industry Value Chain Analysis

The US solar panel value chain integrates raw material sourcing, polysilicon and wafer production, cell manufacturing, module assembly, BOS supply, EPC project construction, grid interconnection, and after-sales operations and maintenance. The commercial architecture is progressively consolidating toward integrated module and storage systems as the primary format.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Procurement of polysilicon, silver, copper, aluminium, and encapsulant materials for solar panel manufacturing |

|

Cell Manufacturing |

Production of silicon wafers, solar cells (mono PERC, TOPCon, HJT), and cell efficiency testing and quality control |

|

Module Assembly |

Lamination of solar cells into finished PV modules, frame integration, junction box assembly, and electrical testing |

|

BOS & Inverter Supply |

Manufacture and distribution of inverters, racking, wiring, monitoring systems, and balance-of-system components |

|

EPC & Installation |

Engineering, procurement, and construction services for utility-scale, commercial rooftop, and residential solar systems |

|

Grid Integration & O&M |

Interconnection, commissioning, grid management, preventive maintenance, and performance monitoring services |

The raw material and polysilicon sourcing tier is the most geopolitically sensitive stage of the US solar value chain. The IRA domestic content provisions are creating the strongest structural investment signal in US solar manufacturing in the industry's history.

Technology Landscape in the United States Solar Panel Industry

Monocrystalline Silicon (Mono PERC) Technology

Monocrystalline PERC technology delivers efficiency ratings of 20–22% and long-term performance reliability. Its widespread availability across all US installer channels, declining manufacturing costs, and broad OEM support make it the current volume-leading solar panel technology in both residential and commercial US applications.

Tunnel Oxide Passivated Contact (TOPCon) Technology

TOPCon technology achieves efficiency ratings of 22–24% through improved carrier passivation, reducing recombination losses. TOPCon bifacial panels generate 10–20% additional rear-side energy from reflected light. TOPCon is increasingly the preferred specification for new US utility-scale and C&I procurement, displacing mono PERC in premium market segments.

Cadmium Telluride (CdTe) Thin Film Technology

CdTe thin film technology, commercialised primarily by First Solar, achieves 18–22% module efficiency with superior temperature coefficient performance in hot climates. Its 100% domestic US manufacturing qualification for IRA domestic content adders and strong utility-scale track record make it the leading alternative to crystalline silicon in large ground-mount US projects.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Monocrystalline Silicon |

39.6% |

2025 |

|

End Use |

Commercial |

44.3% |

2025 |

|

Region |

South |

36.7% |

2025 |

By Type

Monocrystalline silicon leads at 39.6% in 2025, capturing the high-efficiency segment most relevant to space-constrained rooftop applications and performance-oriented commercial buyers seeking maximum power output per installed area.

To access detailed market analysis, Request Sample

Crystal silicon at 27.4% serves broad utility-scale projects where system cost is more critical than efficiency premium. Polycrystalline silicon at 18.5% is declining versus monocrystalline as price gaps narrow. Thin film at 9.8% is dominated by First Solar CdTe modules in large utility installations qualifying for IRA domestic content adders.

By End Use

Commercial end use leads at 44.3% through utility-scale, C&I rooftop, and community solar installations driven by the IRA Investment Tax Credit and corporate PPA procurement, creating stable long-term demand across the forecast period.

Residential at 33.8% is driven by homeowners seeking electricity bill savings and energy independence, with solar-plus-storage adoption accelerating following NEM policy revisions. Industrial at 21.9% reflects large manufacturing sites and logistics hubs optimising energy procurement costs through on-site solar generation.

Regional Market Insights

|

Region |

Share (2025) |

Key Solar Market Drivers & Characteristics |

|

South |

36.7% |

High irradiance; Texas, Florida, Carolinas RPS; large land availability; IRA utility-scale projects |

|

West |

31.5% |

California mandates; Arizona/Nevada utility-scale; strong C&I and residential rooftop demand |

|

Northeast |

18.2% |

SREC markets; New York CLCPA; community solar growth; dense commercial rooftop demand |

|

Midwest |

13.6% |

Agricultural solar; coal retirement replacement; rural utility projects; Indiana and Ohio growth |

The South leads at 36.7% due to its highest solar irradiance levels in the contiguous US, large available land parcels, and strong utility-scale project pipelines in Texas, Florida, and the Carolinas. Texas alone accounts for over 12% of national solar installations, driven by low land costs and deregulated electricity markets.

The West, at 31.5%, is anchored by California's aggressive solar mandates, including the New Building Mandate, which requires solar on all new residential construction. Arizona and Nevada contribute large utility-scale projects leveraging Mojave and Sonoran Desert irradiance resources for long-term PPA agreements.

The Northeast at 18.2% benefits from SREC markets, New York's Climate Leadership and Community Protection Act targets, and growing community solar programmes. The Midwest at 13.6% is emerging as a growth market as agrivoltaic projects and utility-scale solar displace retiring coal generation capacity.

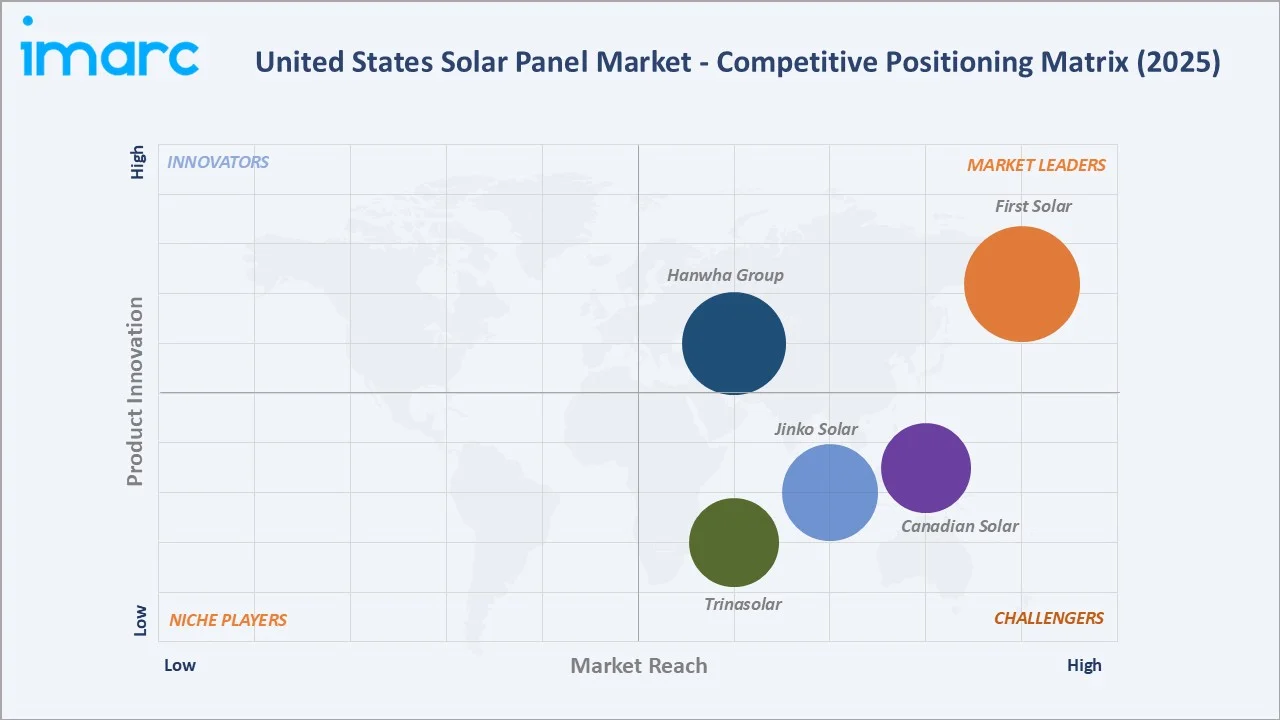

Competitive Landscape

The US solar panel market competitive landscape is moderately concentrated, with global integrated manufacturers, domestic-focused producers, and speciality technology firms competing across utility, commercial, and residential segments. IRA domestic content incentives are actively reshaping the competitive positioning of all major players.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

First Solar |

Series 6, Series 7 |

Market Leader |

Domestic thin-film manufacturing expertise with strong regulatory compliance and IRA incentive alignment |

|

Hanwha Group |

Q.TRON BLK M-G2+/AC, Q.PEAK DUO BLK ML-G10+/AC, Q.TRON BLK M-G2+, Q.PEAK DUO ML-G12S/BFG |

Market Leader |

Large-scale domestic manufacturing presence with vertically integrated production capabilities |

|

Canadian Solar |

BiHiKu6, BiHiKu5, BiHiKu, HiKu6, HiKu5, HiKu, Ku5, Ku, HiDM5 |

Strong Challenger |

Diversified product portfolio with strong project development and bifacial module capabilities |

|

Jinko Solar |

Tiger Neo, Tiger Pro |

Strong Challenger |

High-volume production capacity with advanced cell technology and growing domestic manufacturing base |

|

Trinasolar |

Vertex S+, Vertex N |

Strong Challenger |

High-efficiency large-format module offerings with broad commercial and utility-scale market coverage |

Key players include First Solar, Hanwha Group, Canadian Solar, Jinko Solar, Trinasolar, and others.

Key Company Profiles

First Solar

First Solar is a US-based manufacturer of thin-film photovoltaic modules and a utility-scale solar power plant developer, headquartered in Tempe, Arizona. The company manufactures exclusively in the United States, making it uniquely positioned to capture IRA domestic content incentives.

- Key Products: Series 6 and Series 7

- Recent Developments: In September 2024, First Solar inaugurated its new USD 1.1 billion vertically integrated solar manufacturing facility in Lawrence County, Alabama, adding 3.5 GW of annual solar module production capacity to its U.S. operations. With the addition of the Alabama plant, First Solar’s total U.S. manufacturing capacity is expected to approach 11 GW once fully ramped up, supporting the growing demand for domestically produced solar modules in the United States.

- Strategic Focus: Scaling US domestic CdTe thin-film manufacturing to supply utility-scale solar projects across the Southeast and Southwest while capturing IRA domestic content tax credit adders.

Hanwha Group

Hanwha Group is a global solar technology company wholly owned by Hanwha Solutions Corporation of South Korea. Its US subsidiary operates the largest solar module manufacturing facility in the Western Hemisphere in Dalton, Georgia, producing Q.ANTUM technology cells and modules.

- Key Products: Q.TRON BLK M-G2+/AC, Q.PEAK DUO BLK ML-G10+/AC, Q.TRON BLK M-G2+, Q.PEAK DUO ML-G12S/BFG

- Recent Developments: In June 2026, Qcells, part of Hanwha Group, commenced solar cell production at its Cartersville, Georgia, facility, marking a major milestone in the development of the United States' first fully integrated solar manufacturing supply chain. The facility will manufacture key solar components, including ingots, wafers, cells, and modules, helping strengthen domestic solar production and reduce reliance on imported components.

- Strategic Focus: Achieving full US vertical integration from cell to module manufacturing to qualify for the maximum IRA domestic content adder and establishing long-term supply partnerships with US utilities and commercial solar developers.

Canadian Solar

Canadian Solar is a global solar technology and clean energy company with significant manufacturing operations and project development activities in the United States through its Recurrent Energy project development subsidiary.

- Key Products: BiHiKu6, BiHiKu5, BiHiKu, HiKu6, HiKu5, HiKu, Ku5, Ku, HiDM5

- Strategic Focus: Expanding bifacial TOPCon module supply for US utility-scale projects while growing the Recurrent Energy project pipeline through IRA-supported solar and storage development contracts.

Market Concentration Analysis

The US solar panel market is moderately concentrated at the module supply level, with the top 5-6 key players collectively accounting for an estimated 50–60% of total US solar module revenue. Domestic manufacturers account for approximately 25–35% of the US module supply.

Market concentration is shifting as IRA domestic content incentives accelerate domestic manufacturing investments and reduce reliance on imported modules. The competitive landscape is expected to evolve toward a higher share for US-manufactured modules through the forecast period as new and expanded domestic facilities reach full production capacity.

Investment & Growth Opportunities

Highest Growth Segments

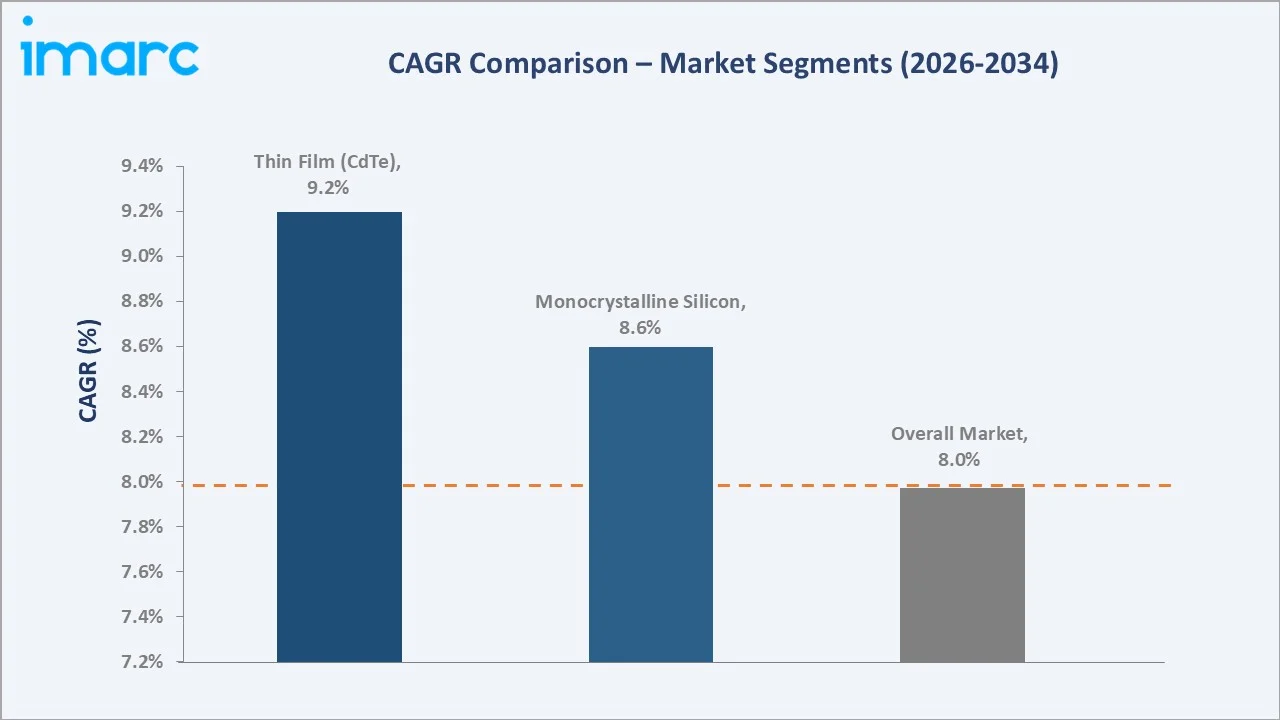

Monocrystalline silicon (~8.6% CAGR), thin film CdTe (~9.2% CAGR), commercial end use (~8.4% CAGR), agrivoltaics and floating solar (~20%+ CAGR from emerging base), BIPV (~15% CAGR), and community solar (~12% CAGR) represent the highest-growth investment vectors in the US solar panel market through 2034.

Emerging Investment Opportunities

US domestic module manufacturing investment represents the market's most policy-supported capital deployment opportunity. IRA domestic content adders worth 10–20 percentage points of additional ITC value create durable competitive advantages for US-manufactured modules in utility-scale and C&I procurement through the IRA programmatic horizon.

Investment Themes

- IRA domestic content manufacturing investment for utility-scale module supply: US-manufactured modules qualifying for the 10% domestic content adder command a 5–12% premium in PPA pricing over imported alternatives, creating sustainable margin advantages for domestic manufacturers through 2034.

- Solar-plus-storage co-location capturing ITC and PTC incentive stacking: Co-located battery storage charged exclusively from solar qualifies for the Investment Tax Credit, improving project IRRs and accelerating utility-scale and C&I solar-storage procurement decisions.

Future Market Outlook (2026-2034)

The US solar panel market is projected to grow from USD 26.06 Billion in 2025 to USD 53.04 Billion by 2034, delivering a 7.97% CAGR over the forecast period. The market's structural growth is anchored by the IRA's decade-long incentive horizon, continued module cost declines, and corporate net-zero commitments creating durable solar demand through 2034.

Monocrystalline silicon and TOPCon bifacial will maintain technology dominance through 2034 as efficiency improvements reduce the levelised cost of electricity. The South and West will retain regional leadership while the Midwest accelerates as coal retirements create utility-scale solar replacement opportunities across the heartland.

Three structural forces define US solar market growth through 2034: the IRA policy certainty creating a decade-long investment horizon; the grid decarbonisation imperative requiring 1,000+ GW of new solar capacity by 2035; and continuous module cost decline expanding the economically addressable market to new demand segments and geographies.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders, including utility solar procurement managers, EPC project directors, residential solar installers, module manufacturer executives, and federal and state energy policy specialists, conducted in 2025.

Secondary Research

Secondary research encompassed company annual reports, SEIA/Wood Mackenzie US Solar Market Insight, EIA Electric Power Monthly, NREL solar resource and cost studies, IRS IRA tax credit guidance documents, FERC interconnection queue data, and others. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts developed using a segmented bottom-up model: (i) US solar installation volume by segment; (ii) average module price per watt by technology type; (iii) total module revenue from installation volume multiplied by segment-specific module ASP; (iv) technology mix adjustment for monocrystalline versus thin film share evolution through 2034.

United States Solar Panel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Crystal Silicon, Monocrystalline Silicon, Polycrystalline Silicon, Thin Film, Others |

| End Uses Covered | Commercial, Residential, Industrial |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | First Solar, Hanwha Group, Canadian Solar, Jinko Solar, Trinasolar, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States solar panel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States solar panel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States solar panel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Solar Panel Market Report

The US solar panel market reached USD 26.06 Billion in 2025, driven by IRA Investment Tax Credits, monocrystalline module cost declines, corporate renewable PPAs, and rising grid electricity tariffs accelerating adoption across commercial, residential, and industrial end-use segments nationwide.

The market grows at 7.97% CAGR during 2026-2034, reaching USD 53.04 Billion by 2034. Growth reflects IRA policy continuity, continued cost reduction, utility-scale project pipeline expansion, and bifacial TOPCon technology improvements driving new market segment penetration.

Monocrystalline silicon leads at 39.6%, capturing high-efficiency residential and commercial rooftop demand, with the widest availability across US installer channels and declining manufacturing costs strengthening segment dominance through the forecast period.

Commercial end use leads at 44.3% through utility-scale and C&I rooftop procurement, driven by the IRA's 30% base Investment Tax Credit, corporate net-zero PPAs, and utility renewable portfolio standard compliance requirements, creating sustained long-term demand.

The South leads at 36.7% through the highest solar irradiance in the contiguous US, large land availability for utility-scale projects, and proactive renewable energy mandates in Texas, Florida, and the Carolinas supporting a robust project pipeline.

Leading companies include First Solar, Hanwha Group, Canadian Solar, Jinko Solar, Trinasolar, and others.

The market is projected to reach approximately USD 38.23 Billion by 2030, supported by IRA domestic content manufacturing ramp-up, solar-plus-storage co-deployment, agrivoltaic project growth, and commercial solar achieving grid parity across all US states and customer segments.

Three priority opportunities: IRA domestic content manufacturing for utility-scale module supply, capturing the domestic content adder premium; solar-plus-storage co-location leveraging ITC stacking for superior project economics; and community solar programme expansion, increasing addressable market beyond direct ownership constraints across all US regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)