United States Specialty Paper Market Size, Share, Trends and Forecast by Type, Raw Material, Application, and Region, 2026-2034

United States Specialty Paper Market Size, Share, Trends & Forecast (2026-2034)

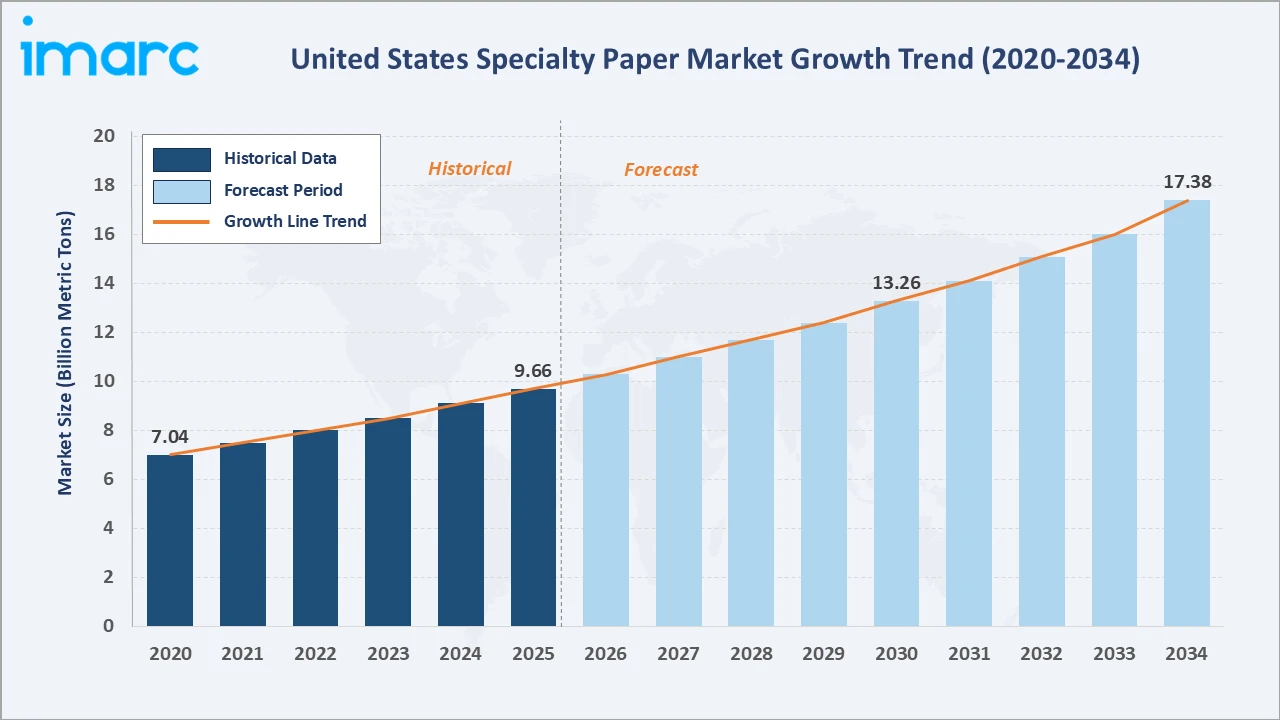

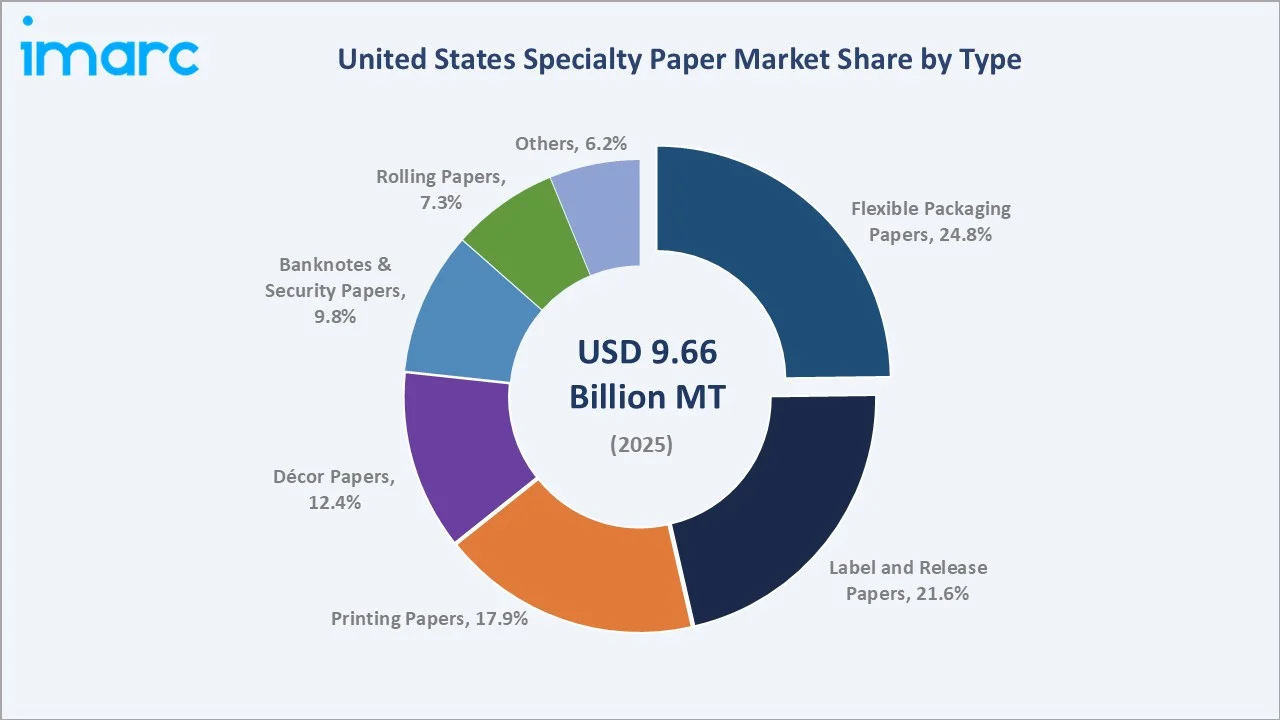

The United States specialty paper market reached 9.66 Billion Metric Tons in 2025 and is projected to reach 17.38 Billion Metric Tons by 2034, growing at a CAGR of 6.54% during 2026-2034. The market is driven by rising demand for sustainable and recyclable packaging solutions, coupled with increasing adoption of high-performance paper in packaging, labeling, healthcare, and food service applications. The US consumer interest in sustainable packaging is strong but price-sensitive: 54% of consumers selected products with sustainable packaging in the past six months, and 39% changed brands because of it, while only 13% were willing to pay a significant premium. This is driving the specialty paper market by encouraging brands to adopt recyclable, paper-based, and eco-friendly packaging solutions, but cost competitiveness remains critical for mass adoption. By type, flexible packaging papers lead at 24.8%. By raw material, pulp leads at 46.7%. South leads regionally at 34.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

9.66 Billion Metric Tons |

|

Forecast Market Size (2034) |

17.38 Billion Metric Tons |

|

CAGR (2026-2034) |

6.54% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Flexible Packaging Papers (24.8%, 2025) |

|

Dominant Raw Material |

Pulp (46.7%, 2025) |

|

Leading Region |

South (34.6%, 2025) |

The United States specialty paper market grew from 7.04 Billion Metric Tons in 2020 to 9.66 Billion Metric Tons in 2025, reflecting steady demand from packaging, labeling, foodservice, and industrial applications. It is projected to reach 13.26 Billion Metric Tons by 2030, supported by the shift toward sustainable and recyclable paper-based materials. By 2034, the market is forecast to attain 17.38 Billion Metric Tons, driven by plastic substitution, e-commerce packaging growth, and rising use of specialty paper in premium and functional applications.

To get more information on this market, Request Sample

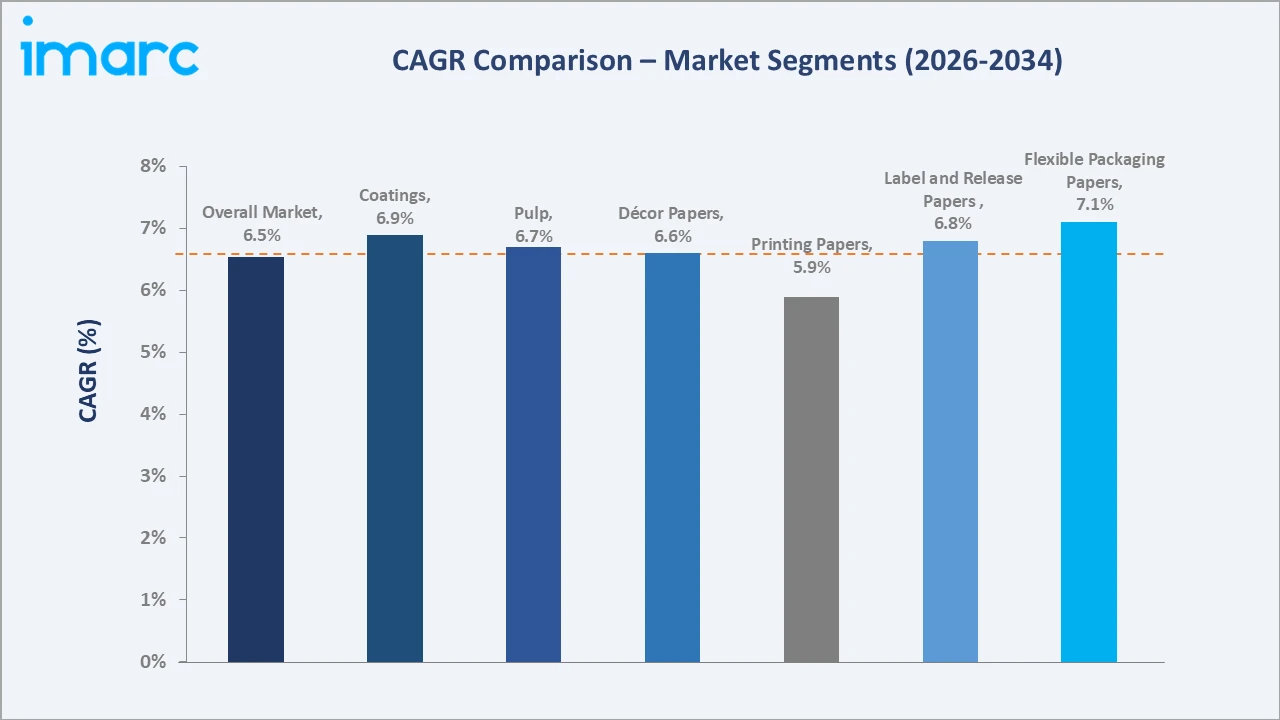

Flexible packaging papers grow fastest at ~7.1% CAGR through e-commerce packaging and plastic-to-paper shift. Coatings raw material grows at ~6.9% CAGR through barrier and functional coating demand.

Executive Summary

The United States specialty paper market is growing steadily, supported by rising demand for sustainable, recyclable, and functional paper-based solutions. Packaging, labeling, foodservice, healthcare, and industrial applications remain key demand areas. The shift away from plastic packaging is encouraging brands to adopt specialty papers with barrier, strength, and printability features. However, consumer willingness to pay premium prices remains limited, making cost-effective innovation important. By 2034, the market is expected to expand strongly as sustainability goals, e-commerce packaging, and premium product presentation drive wider adoption. Flexible packaging papers at 24.8% lead type. Pulp at 46.7% leads raw material. South leads regionally at 34.6%.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Flexible Packaging Papers - 24.8% share (2025) |

|

Dominant Raw Material |

Pulp - 46.7% market share (2025) |

|

Leading Region |

South - 34.6% share (2025) |

|

Market Opportunity |

Sustainable flexible packaging plastic-to-paper shift; security paper anti-counterfeit banknote; décor paper construction renovation; bio-based barrier coating; label release liner e-commerce; recyclable paper composite |

Key Analytical Observations Supporting The Above Data:

- Flexible Packaging Papers at 24.8%: Flexible packaging papers lead due to rising demand for lightweight, recyclable, and plastic-alternative packaging across food, beverages, personal care, and e-commerce. Their printability, barrier performance, and sustainability appeal make them preferred by brands.

- Pulp at 46.7%: Pulp leads as it is the primary raw material used in producing high-strength, recyclable, and biodegradable specialty papers. Its wide availability, processing flexibility, and sustainability benefits support its dominance across packaging, labeling, and industrial paper applications.

- South at 34.6%: South leads due to its strong paper manufacturing base, packaging demand, logistics network, and presence of food, retail, and industrial end users. Expanding e-commerce, foodservice packaging, and converting facilities further support regional dominance.

United States Specialty Paper Market Overview

The United States specialty paper market encompasses flexible packaging papers, décor papers, release liners, printing papers, filter papers, and other high-performance paper grades. It covers applications across food and beverage packaging, labels, e-commerce packaging, healthcare, personal care, construction, and industrial uses. The market includes raw materials such as pulp, recycled fiber, fillers, coatings, binders, and specialty chemicals. It also involves converting, coating, laminating, printing, and finishing processes that enhance barrier properties, strength, texture, and printability. Growing demand for recyclable, biodegradable, and plastic-alternative materials is expanding the market scope. Macroeconomic factors include rising consumer spending on packaged goods, growing e-commerce activity, and increasing demand from foodservice, healthcare, retail, and industrial sectors.

Market Dynamics

To evaluate market opportunities, Request Sample

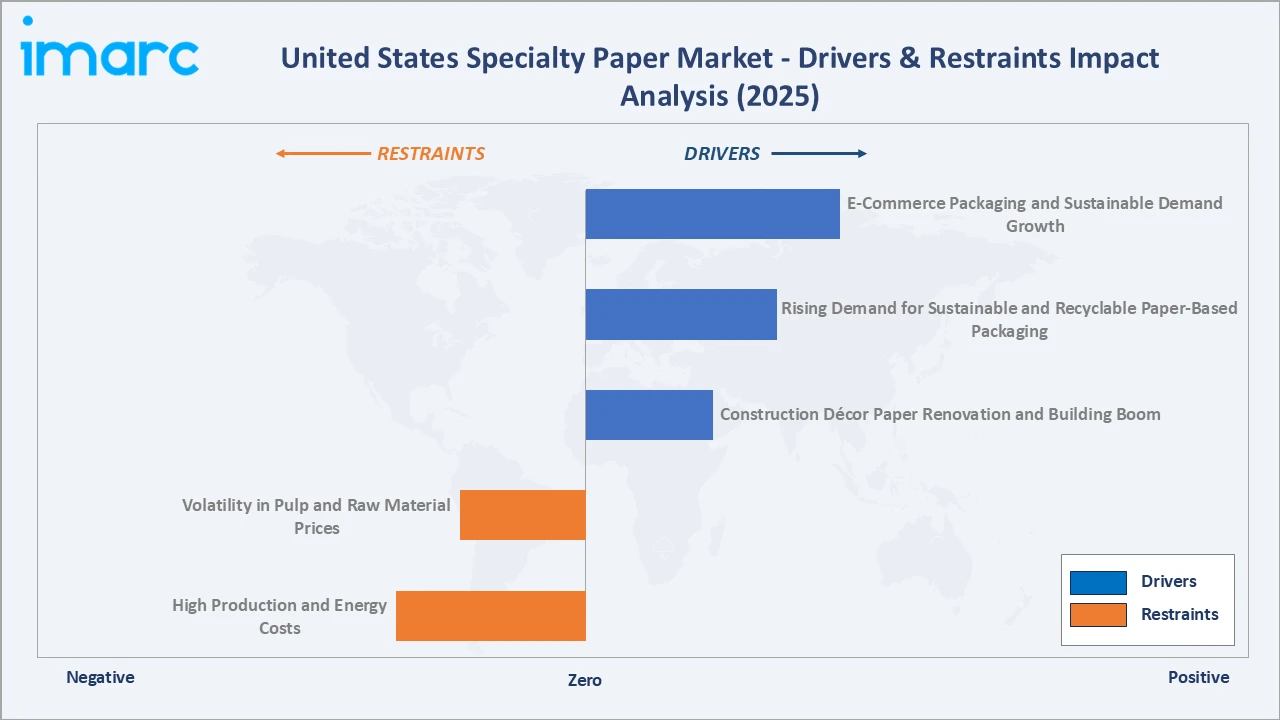

Market Drivers

- E-Commerce Packaging and Sustainable Demand Growth: E-commerce packaging and sustainable demand growth are driving the market as online retail increases the need for lightweight, durable, and printable packaging materials. About 52% of US consumers prefer online orders to arrive in paper packaging, while 68% prefer right-sized packaging. Around 67% favor paper packaging for its compostability, along with its lower environmental impact and recyclability. Additionally, 41% said they would pay more for products packaged sustainably. Rising consumer preference for eco-friendly packaging is further encouraging retailers and FMCG companies to adopt paper-based alternatives.

- Rising Demand for Sustainable and Recyclable Paper-Based Packaging: Rising demand for sustainable and recyclable paper-based packaging is driving the market as brands shift away from plastic and non-recyclable materials. Specialty papers are increasingly used in pouches, wraps, bags, labels, and foodservice packaging due to their recyclability, biodegradability, and printability. Consumer preference for eco-friendly packaging and corporate sustainability targets are accelerating adoption across retail, FMCG, and e-commerce sectors. This trend is encouraging manufacturers to develop stronger, coated, and barrier-enabled papers that can replace conventional plastic packaging.

- Construction Décor Paper Renovation and Building Boom: Construction décor paper renovation and building activity are increasing demand for decorative laminates, furniture surfaces, flooring, wall panels, and interior finishing materials. Construction remains a major pillar of the US economy, with more than 919,000 construction establishments operating across the country in the first quarter of 2023. As residential remodeling, commercial renovation, and real estate development expand, décor papers are widely used to provide woodgrain, stone, matte, and customized surface effects at a lower cost than natural materials. Their durability, design flexibility, and compatibility with laminate production make them attractive for builders and furniture manufacturers.

Market Restraints

- Volatility in Pulp and Raw Material Prices: Volatility in pulp and raw material prices is increasing production costs and reducing profit margins for manufacturers. Price fluctuations in wood pulp, recycled fiber, chemicals, coatings, and energy make cost planning difficult. These pressures can lead to higher product prices, affecting demand from packaging converters and brand owners. It also limits the ability of manufacturers to offer affordable sustainable paper alternatives at scale.

- High Production and Energy Costs: High production and energy costs are hampering the market as specialty grades require advanced coating, drying, calendaring, and finishing processes. These operations consume significant energy and increase manufacturing expenses. Rising electricity, fuel, labor, and chemical costs reduce producer margins and raise final product prices. This can slow adoption, especially when specialty paper competes with lower-cost plastic or conventional packaging alternatives.

Market Opportunities

- Development of High-Barrier and Functional Specialty Papers: Development of high-barrier and functional specialty papers is creating strong opportunities as brands seek paper-based alternatives to plastic packaging. These papers can offer moisture resistance, grease resistance, oxygen barriers, heat sealability, and improved durability for food, beverages, personal care, and e-commerce packaging. Innovation in recyclable coatings and bio-based barrier materials helps expand usage without compromising sustainability goals. This creates opportunities for manufacturers to capture higher-value applications and differentiate through performance-led paper solutions.

- Growth in Recycled Fiber and Bio-Based Specialty Paper Solutions: Growth in recycled fiber and bio-based specialty paper solutions is creating opportunities as brands seek lower-carbon and circular packaging materials. Recycled fibers help reduce dependence on virgin pulp, while bio-based coatings and additives improve compostability and recyclability. These solutions support corporate sustainability goals and compliance with plastic-reduction regulations. They also allow manufacturers to develop premium eco-friendly grades for packaging, labels, foodservice, and consumer goods applications.

Market Challenges

- Maintaining Barrier Performance While Ensuring Recyclability: Maintaining barrier performance while ensuring recyclability is challenging, as many applications require resistance to moisture, grease, oxygen, and heat. Traditional barrier coatings can improve performance but may reduce recyclability or compostability. Manufacturers must balance functionality with regulatory, brand, and consumer sustainability expectations. Developing recyclable coatings that match plastic-level protection without raising costs remains a key technical challenge.

- Managing Supply Chain and Raw Material Availability: Managing supply chain and raw material availability is challenging due to dependence on pulp, recycled fiber, chemicals, coatings, and additives. Disruptions in wood supply, recycling collection, logistics, or imports can delay production and increase costs. Specialty paper grades often require consistent fiber quality and specific functional inputs, making substitution difficult. These constraints can affect delivery timelines, pricing stability, and the ability to scale sustainable paper solutions.

Emerging Market Trends

1. Sustainable Flexible Packaging and Plastic-to-Paper Shift

Sustainable flexible packaging and plastic-to-paper shift is emerging as brands replace single-use plastics with recyclable and renewable paper-based alternatives. Specialty paper manufacturers are developing high-performance barrier papers that offer moisture, grease, and oxygen resistance while maintaining recyclability and compostability. The rapid growth of e-commerce, food service, and consumer goods packaging is further accelerating demand for lightweight, flexible paper packaging solutions.

2. Smart and Digital Security Paper Innovation

Smart and digital security paper innovation is emerging as demand rises for anti-counterfeiting, authentication, and traceability solutions. Specialty papers are increasingly being integrated with QR codes, RFID, watermarks, holographic features, invisible inks, and tamper-evident technologies. These innovations are gaining traction in banknotes, certificates, passports, legal documents, pharmaceutical packaging, and brand protection applications. As fraud risks and supply chain transparency needs grow, manufacturers are investing in advanced security papers that combine physical protection with digital verification.

3. Food-Safe Barrier Paper Solutions

Food-safe barrier paper solutions are emerging as foodservice brands seek safer and more sustainable alternatives to plastic-coated packaging. These papers provide oil, grease, and moisture resistance for wrappers, bags, liners, and takeaway packaging while maintaining food-contact safety. In June 2025, BiOrigin Specialty Products (BSP) introduced a new oil- and grease-resistant (OGR) paper. Its BioGuard paper uses a 100% food-safe barrier solution to prevent oil and grease from penetrating foodservice wrappers and bags, while also improving processing efficiency for OGR paper converters. The product will be produced in the United States through BSP’s Creative Solutions Network of mills across the US and Canada. This trend is also supporting innovation in OGR papers that combine food protection, regulatory compliance, and converter-friendly processing efficiency.

4. Digitally Printed and Customized Décor Papers

Digitally printed and customized décor papers are emerging due to rising demand for personalized interiors, furniture, laminates, and wall coverings. Digital printing enables short-run production, faster design changes, and high-resolution decorative patterns with lower setup costs. This supports customized woodgrain, stone, textile, and abstract designs for residential, commercial, and hospitality spaces. As consumers and designers seek unique, premium, and flexible décor solutions, specialty paper producers are expanding digitally printable décor paper offerings.

Industry Value Chain Analysis

The United States specialty paper value chain integrates raw material sourcing, paper manufacturing, coating and treatment, converting and printing, distribution and supply, and end-use industries.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Pulp producers, recycled fiber suppliers, chemical suppliers, and coating material providers |

|

Paper Manufacturing |

Specialty paper mills, integrated pulp and paper manufacturers |

|

Coating and Treatment |

Barrier coating companies, surface treatment providers, functional additive suppliers |

|

Converting and Printing |

Converters, printers, laminators, packaging fabricators |

|

Distribution and Supply |

Paper distributors, wholesalers, logistics providers |

|

End-Use Industries |

Packaging, foodservice, healthcare, labels, décor, security, and industrial users |

The highest value addition in the United States specialty paper market occurs during the coating and treatment, where base paper is enhanced with specialized properties such as barrier protection, heat resistance, printability, anti-counterfeiting features, release coatings, or medical-grade performance. These advanced processes transform commodity paper into high-performance specialty products tailored for packaging, labels, healthcare, security, and industrial applications, significantly increasing product value and differentiation.

Technology Landscape in the United States Specialty Paper Industry

Papermaking and Coating Technology

Papermaking and coating technology enable the adoption of advanced fiber processing, precision coating, and surface treatment techniques. Manufacturers are developing high-performance papers with enhanced barrier, printability, durability, and functional properties for packaging, healthcare, labels, and industrial applications. The integration of water-based, bio-based, and PFAS-free coating technologies is supporting sustainability while maintaining product performance.

Barrier and Functional Specialty Technology

Barrier and functional specialty technology enables papers with moisture, grease, oxygen, heat, release, and chemical resistance properties. These technologies help replace plastic-based materials in foodservice packaging, labels, medical papers, industrial liners, and flexible packaging. Manufacturers are increasingly using water-based, bio-based, and PFAS-free barrier coatings to meet sustainability and regulatory needs. This is driving innovation in high-performance specialty papers that combine functionality, recyclability, and end-use customization.

Thermal and Heat-Resistant Paper Technology

Thermal and heat-resistant paper technology enables papers that can withstand high temperatures without compromising strength, print quality, or dimensional stability. These specialty papers are increasingly used in thermal labels, baking papers, industrial insulation, release liners, and electrical applications. Manufacturers are advancing heat-resistant coatings and fiber formulations to improve durability, safety, and performance under demanding conditions. The technology is also supporting the development of sustainable, high-performance paper solutions for packaging and industrial end-use applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Flexible Packaging Papers |

24.8% |

2025 |

|

Raw Material |

Pulp |

46.7% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

South |

34.6% |

2025 |

By Type

Flexible packaging papers lead at 24.8% (2025), through kraft barrier paper, specialty kraft paper, bleached kraft packaging paper, and cellulose-based flexible packaging films.

To access detailed market analysis, Request Sample

Label and release papers at 21.6% reflect self-adhesive pressure-sensitive label face stock, silicone-coated release liner, and specialty label papers. Printing papers at 17.9% reflects premium uncoated specialty, coated art paper, and laser/inkjet-compatible specialty printing. Décor papers at 12.4% reflect melamine-impregnated décor paper for MDF furniture and flooring laminate. Banknotes and security papers at 9.8% reflect cotton-fiber currency paper and pharmaceutical anti-counterfeit labels. Rolling papers at 7.3% reflect SWM cigarette paper and growing cannabis rolling paper.

By Raw Material

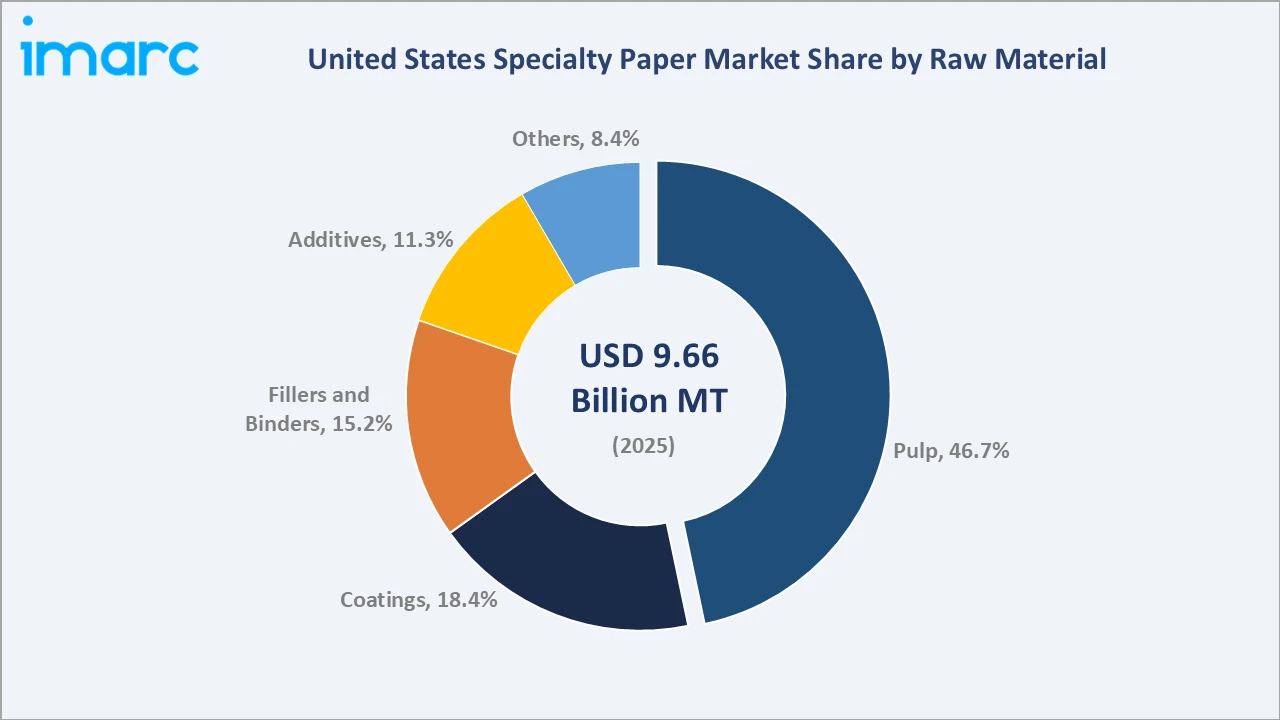

Pulp leads at 46.7% (2025) as it is the primary raw material used to produce high-quality, strong, and functional paper grades. Its versatility allows manufacturers to develop specialty papers with properties such as durability, absorbency, printability, and barrier performance.

Coatings at 18.4% reflect functional and barrier coatings, growing fastest at ~6.9% CAGR through plastic-free barrier packaging and silicone release liner demand. Fillers and binders at 15.2% include calcium carbonate fillers, kaolin clay filler, and starch and latex binders for strength and coating holdout. Additives at 11.3% include wet-strength resins, internal sizing agents, and optical brightening agents (OBAs). Others at 8.4% include specialty chemicals.

Regional Market Insights

|

Region |

Share (2025) |

Key US Specialty Paper Market Drivers & Characteristics |

|

South |

34.6% |

Driven by its strong pulp and paper manufacturing base, abundant forestry resources, expanding food packaging industry, and growing investments in sustainable paper production. |

|

Midwest |

27.1% |

Supported by its well-established industrial manufacturing sector, robust converting and packaging operations, and high demand from food processing, healthcare, and consumer goods industries. |

|

Northeast |

21.3% |

Reflecting strong demand for premium printing, labeling, security, healthcare, and specialty packaging papers, along with a focus on innovation and high-value paper applications. |

|

West |

17.0% |

Supported by increasing demand for sustainable packaging, e-commerce, foodservice applications, and environmentally friendly specialty paper solutions across consumer and technology-driven industries. |

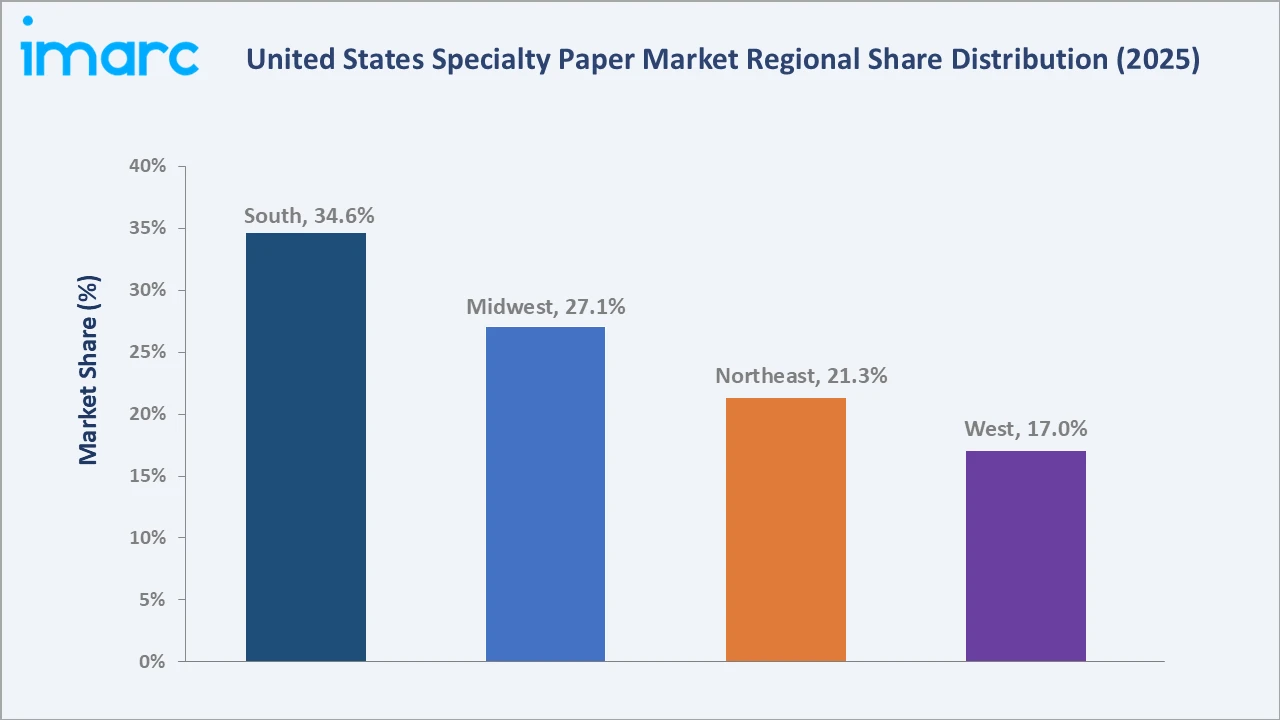

The South's 34.6% dominates due to its abundant forestry resources, strong pulp and paper manufacturing base, and extensive production of packaging and industrial papers. The Midwest's 27.1% is a major hub for converting, printing, and food packaging applications, supported by its large manufacturing and consumer goods industries.

The Northeast's 21.3% owing to high demand for premium specialty papers used in healthcare, security, labels, and high-value printing applications, along with continuous product innovation. The West's 17.0% is driven by expanding e-commerce, sustainable packaging initiatives, and increasing adoption of recyclable and bio-based specialty paper solutions across foodservice, retail, and technology sectors.

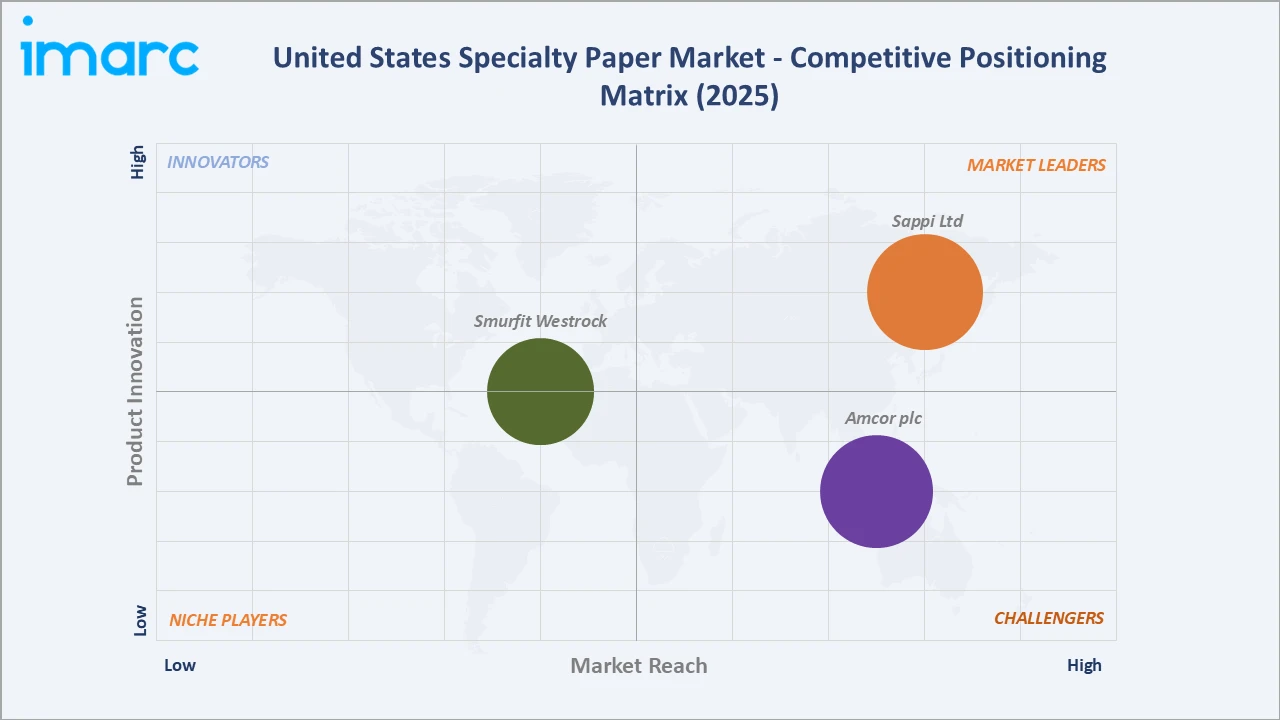

Competitive Landscape

The United States specialty paper market is moderately competitive, with established paper manufacturers, converters, and coating technology providers competing on quality, innovation, sustainability, and customization. Key players focus on developing high-performance papers for packaging, labels, foodservice, healthcare, security, décor, and industrial applications. Companies are investing in recyclable, compostable, PFAS-free, and bio-based specialty paper solutions to meet changing regulatory and consumer preferences.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Sappi Ltd |

Casting & Release Papers, Label papers & Release liners |

Market Leader |

Sappi Ltd is a premier supplier of specialty papers in the United States, driving a shift toward renewable, woodfiber-based packaging and release papers. Operating through Sappi North America, they provide sustainable, high-performance paperboard, casting, and release papers for the luxury, food, and automotive industries. |

|

Amcor plc |

AmFiber paper-based packaging solutions |

Strong Challenger |

Amcor plc plays a major role in the US specialty and paper-based packaging market by driving the shift from traditional plastics to sustainable paper alternatives. Through its specialized manufacturing capabilities, the company enables brands in the food, healthcare, and consumer goods sectors to meet environmental regulations while maintaining barrier performance and shelf appeal. |

|

Smurfit Westrock |

ReliaKraft Specialty High Tensile Kraft paper, ReliaKraft Mask Green paper |

Established Player |

Smurfit Westrock plays a massive role in the US specialty and kraft paper sectors by supplying high-performance, sustainable, and custom-engineered substrates. Through an extensive North American manufacturing footprint, they produce specialized kraft papers, liquid packaging, and barrier-coated boards for heavy-duty industrial, retail, and pharmaceutical applications. |

Product differentiation is largely driven by barrier performance, printability, strength, functional coatings, and end-use-specific customization. The market is also witnessing strategic partnerships, capacity upgrades, and domestic manufacturing expansion to improve supply reliability and serve high-growth packaging and industrial segments.

Key Company Profiles

Sappi Ltd

Sappi Ltd. is a leading producer of specialty papers with a strong presence in the United States through its manufacturing facilities and converting operations. The company offers a broad portfolio of specialty papers for flexible packaging, foodservice, labels, release liners, casting and release papers, and industrial applications. Sappi focuses on developing sustainable, fiber-based solutions with advanced barrier, printability, and functional coating technologies to replace conventional plastic packaging.

- Key Products: Casting & Release Papers, Label papers & Release liners.

- Strategic Focus: Expanding its portfolio of sustainable, fiber-based specialty papers to replace plastic in flexible packaging and foodservice applications. Investing in high-performance barrier and functional coating technologies, including recyclable and PFAS-free paper solutions. Strengthening its presence in packaging, labels, release liners, and industrial specialty paper segments through continuous product innovation.

Amcor plc

Amcor plc is a packaging company active in flexible packaging, rigid packaging, cartons, closures, pouches, wrappers, laminates, and healthcare packaging solutions. In the United States specialty paper market, Amcor is relevant through its focus on fiber-based and sustainable packaging alternatives for food, beverage, pharmaceutical, personal care, and consumer goods applications. The company emphasizes responsible packaging innovation, recyclability, lightweighting, and material substitution to help brands reduce plastic use.

- Key Products: AmFiber paper-based packaging solutions.

- Strategic Focus: Expanding sustainable and fiber-based packaging solutions that support the shift away from conventional plastics. The company emphasizes recyclable, lightweight, and high-barrier paper-based packaging for food, beverage, healthcare, personal care, and consumer goods applications.

Market Concentration Analysis

The United States specialty paper market is moderately concentrated, with a mix of large integrated paper manufacturers, global packaging companies, and specialized converters. Leading players hold strong positions through advanced coating technologies, established distribution networks, and broad product portfolios across packaging, labels, healthcare, décor, and industrial papers. However, several niche producers compete effectively by offering customized, high-performance, and sustainable specialty paper solutions. Market concentration is increasing as companies invest in PFAS-free coatings, recyclable barrier papers, and fiber-based packaging alternatives. Overall, competition remains balanced, with innovation, sustainability, and end-use customization serving as key differentiators.

Investment & Growth Opportunities

Highest Growth Segments

Flexible packaging papers (~7.1% CAGR), coatings raw material (~6.9% CAGR), label and release papers (~6.8% CAGR), décor papers (~6.6% CAGR), South mill region (~6.8% CAGR), and bio-based barrier specialty (~8% CAGR from growing base) represent the US specialty paper highest-growth investment vectors through 2034.

Investment Themes

- Plastic-to-paper sustainable flexible packaging: Investments are accelerating in recyclable, fiber-based flexible packaging and advanced barrier paper technologies as brands replace plastic with sustainable paper alternatives for food, retail, and e-commerce packaging.

- Security and anti-counterfeit specialty paper: Investment is increasing in specialty papers integrated with watermarks, RFID, holograms, QR codes, and other authentication technologies to strengthen document security, brand protection, and product traceability.

Future Market Outlook (2026-2034)

The United States specialty paper market is projected to grow from 9.66 Billion Metric Tons in 2025 to 17.38 Billion Metric Tons by 2034, delivering a 6.54% CAGR through sustainable flexible packaging plastic-to-paper shift, e-commerce packaging demand explosion, security paper anti-counterfeit and smart authentication innovation, décor paper US construction and renovation boom, and bio-based barrier coating technology. The market's anchor value of 13.26 Billion Metric Tons in 2030 represents US specialty paper at the plastic-to-paper inflection mainstream and smart security specialty mainstream.

Three structural forces define United States specialty paper growth through 2034: the shift from plastic to sustainable fiber-based packaging, rising demand for functional barrier papers, and increasing need for high-value applications such as security, healthcare, labels, and décor papers. Sustainability regulations and brand commitments are accelerating adoption of recyclable, compostable, and PFAS-free specialty papers. At the same time, innovation in coatings, digital printing, and anti-counterfeit technologies is expanding product performance and end-use customization. These forces are positioning specialty paper as a key material in packaging transformation and premium industrial applications.

Research Methodology

Primary Research

Primary research comprised interviews and discussions with specialty paper manufacturers, raw material suppliers, converters, distributors, packaging companies, and industry experts across the value chain. Insights were gathered to validate market size, growth trends, pricing dynamics, technology adoption, demand patterns, competitive developments, and future opportunities in the United States specialty paper market.

Secondary Research

Secondary research encompassed an extensive review of company annual reports, investor presentations, industry associations, government publications, trade journals, regulatory documents, and credible news sources. It also included the analysis of market databases, technical papers, and publicly available industry statistics to assess market trends, competitive dynamics, technological advancements, and end-use demand in the United States specialty paper market.

Forecasting Models

Forecasting models used a combination of historical trend analysis, demand-side assessment, and bottom-up/end-use market estimation. Growth projections were validated through macroeconomic indicators, packaging demand, sustainability trends, and technology adoption patterns. Scenario analysis was applied to assess baseline, optimistic, and conservative growth outcomes through 2034.

United States Specialty Paper Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion Metric Tons |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Label and Release Papers, Printing Papers, Flexible Packaging Papers, Rolling Papers, Décor Papers, Banknotes and Security Papers, Others |

| Raw Materials Covered | Pulp, Fillers and Binders, Additives, Coatings, Others |

| Applications Covered | Packaging and Labeling, Printing and Writing, Industrial Use, Building and Construction, Food Service, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Sappi Ltd, Amcor plc, Smurfit Westrock, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States specialty paper market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States specialty paper market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States specialty paper industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Specialty Paper Market Report

The United States specialty paper market reached 9.66 Billion Metric Tons in 2025, driven by rising demand for sustainable, recyclable, and fiber-based packaging alternatives across foodservice, e-commerce, healthcare, and consumer goods sectors. Growth is further supported by innovations in barrier coatings, PFAS-free papers, security papers, and customized specialty applications.

The United States specialty paper market grows at 6.54% CAGR during 2026-2034, reaching 17.38 Billion Metric Tons by 2034. The CAGR reflects e-commerce packaging growth, sustainable plastic-free specialty paper, security paper anti-counterfeit, and décor paper US construction boom structural demand.

Flexible packaging papers lead at 24.8% due to rising demand for sustainable, lightweight, and recyclable alternatives to plastic packaging. Their use is expanding across foodservice, e-commerce, retail, and consumer goods applications, supported by advances in barrier coatings, grease resistance, and printability.

Pulp leads at 46.7% as it is the core raw material for producing strong, durable, and high-quality specialty papers. Its renewable, recyclable, and versatile nature supports demand across packaging, labels, foodservice, décor, and industrial paper applications.

The South leads at 34.6% due to its strong pulp and paper manufacturing base, abundant forestry resources, and well-developed packaging supply chain. Demand is further supported by foodservice, industrial packaging, and sustainable paper production across the region.

Leading companies include Sappi Ltd, Amcor plc, and Smurfit Westrock, among others.

The market is projected to reach approximately 13.26 Billion Metric Tons by 2030, supported by rising demand for sustainable, recyclable, and high-performance specialty paper products. Growth will be driven by expanding applications in flexible packaging, foodservice, labels, healthcare, and industrial uses.

Three priority investment opportunities are emerging in the United States specialty paper market. First, plastic-to-paper sustainable flexible packaging is attracting significant investments as brands transition to recyclable and fiber-based packaging solutions. Second, food-safe barrier and functional specialty papers are gaining traction to meet demand for high-performance, PFAS-free packaging in food and healthcare applications. Third, security and anti-counterfeit specialty papers present strong growth potential, driven by increasing requirements for authentication, traceability, and document protection across government, pharmaceutical, and consumer goods sectors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)