Brazil Construction Market Size, Share, Trends and Forecast by Sector, and Region, 2026-2034

Brazil Construction Market Size, Share, Trends & Forecast (2026-2034)

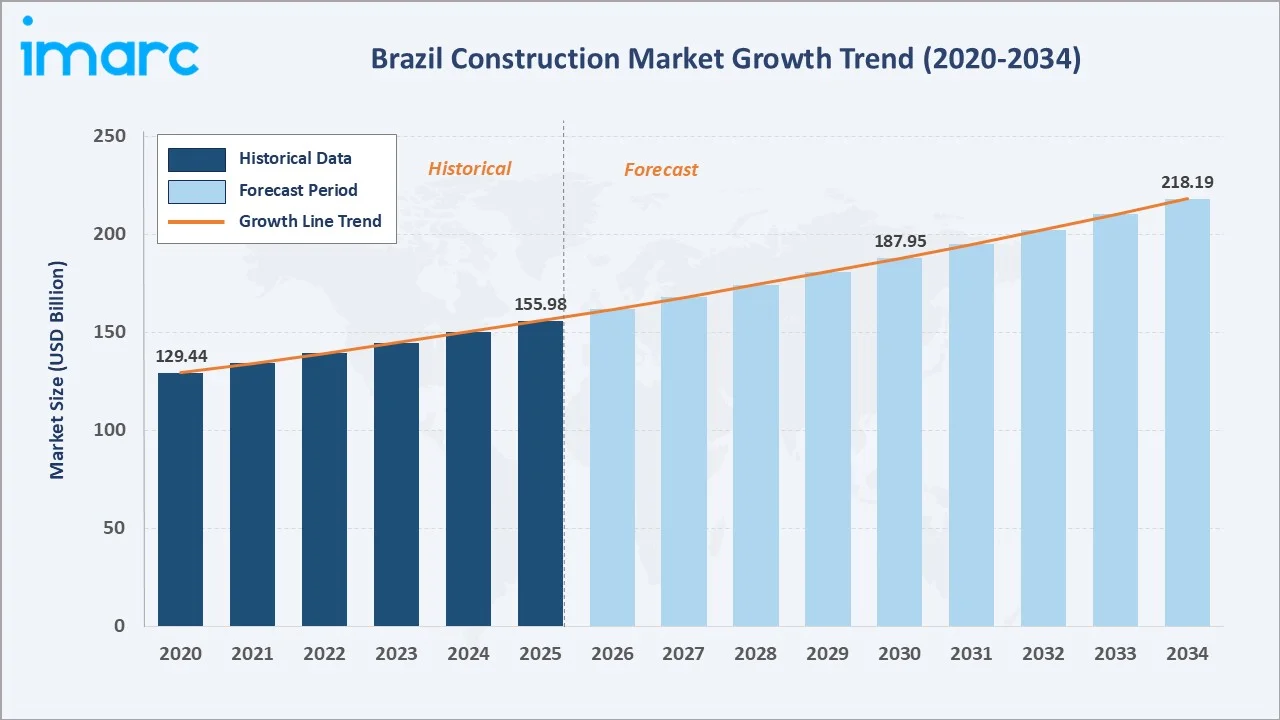

The Brazil construction market reached USD 155.98 Billion in 2025 and is projected to reach USD 218.19 Billion by 2034, growing at a CAGR of 3.80% during 2026-2034. The market is driven by expanding infrastructure investment, rapid urbanization, rising demand for residential and commercial buildings, and government housing initiatives. Brazil’s construction is projected to generate BRL 2.7 trillion in project activity by 2030, highlighting substantial investment momentum. This large project base is driving demand for construction services, materials, equipment, and labor across infrastructure, residential, and commercial segments. Residential construction leads the sectors at 34.6%. The Southeast region commands 41.3% of the national market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 155.98 Billion |

| Forecast Market Size (2034) | USD 218.19 Billion |

| CAGR (2026-2034) | 3.80% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Sector | Residential Construction (34.6%, 2025) |

| Leading Region | Southeast (41.3%, 2025) |

The Brazil construction market expanded from USD 129.44 Billion in 2020 to USD 155.98 Billion in 2025, anchored at USD 187.95 Billion in 2030, and forecast to reach USD 218.19 Billion by 2034. The COVID-19 pandemic had a paradoxical effect on Brazil's construction market. Brazil's construction sector grew significantly, outperforming the broader economy, and sustained above-GDP-growth construction activity through 2022-2025, driven by the infrastructure acceleration.

To get more information on this market, Request Sample

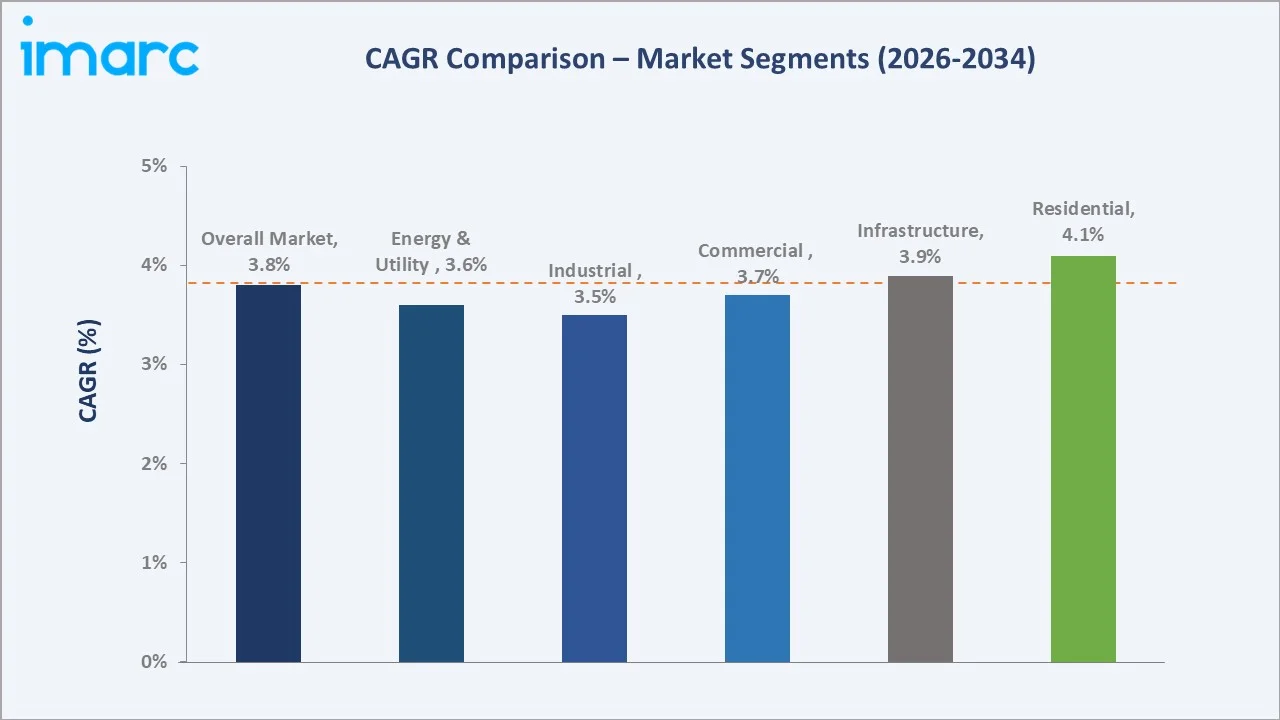

Residential construction grows fastest at ~4.1% CAGR through the combination of Brazil's housing deficit and a growing middle class, creating demand above the subsidy threshold. Infrastructure grows at ~3.9% CAGR underpinned by the federal commitment, state government concessions for highways and sanitation, and international airport privatization and construction investment.

Executive Summary

Brazil's construction market reached USD 155.98 Billion in 2025, representing Latin America's largest national construction market. Brazil's construction industry encompasses the full spectrum of built environment creation, residential housing, transportation infrastructure, commercial real estate, industrial plants, and energy infrastructure. The market is projected to reach USD 218.19 Billion by 2034.

Residential construction at 34.6% leads through the combined force of Brazil's persistent housing deficit, the federal government's programmes, and the private residential market serving Brazil's population. The Southeast at 41.3% commands market dominance through the economic corridor, the country's highest construction volume concentration.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Sector | Residential Construction – 34.6% share (2025) |

| Dominant Region | Southeast – 41.3% market share (2025) |

| Market Opportunity | Data center construction boom; green hydrogen infrastructure; sanitation universalization; nearshoring industrial parks; smart city urbanization; North and Central-West logistics hubs |

Key Analytical Observations Supporting The Above Data:

- Residential Construction at 34.6%: The residential construction segment dominates due to strong housing demand, urbanization, and affordable housing initiatives.

- Southeast Region at 41.3%: The Southeast region dominates due to its concentration of major urban and economic hubs, which generate strong demand for residential, commercial, and infrastructure projects.

Brazil Construction Market Overview

The Brazil construction market encompasses all activities involved in the design, planning, financing, construction, and delivery of the built environment across residential, commercial, industrial, infrastructure, and energy sectors. The market is structured around public sector demand and private sector demand.

The construction ecosystem integrates heavy construction companies, residential developers, commercial developers, industrial constructors, financial institutions, materials suppliers, equipment suppliers, and regulatory bodies. Macroeconomic factors include rising employment and wages, and sustained public/private investment, which strengthen housing and infrastructure demand.

Market Dynamics

To evaluate market opportunities, Request Sample

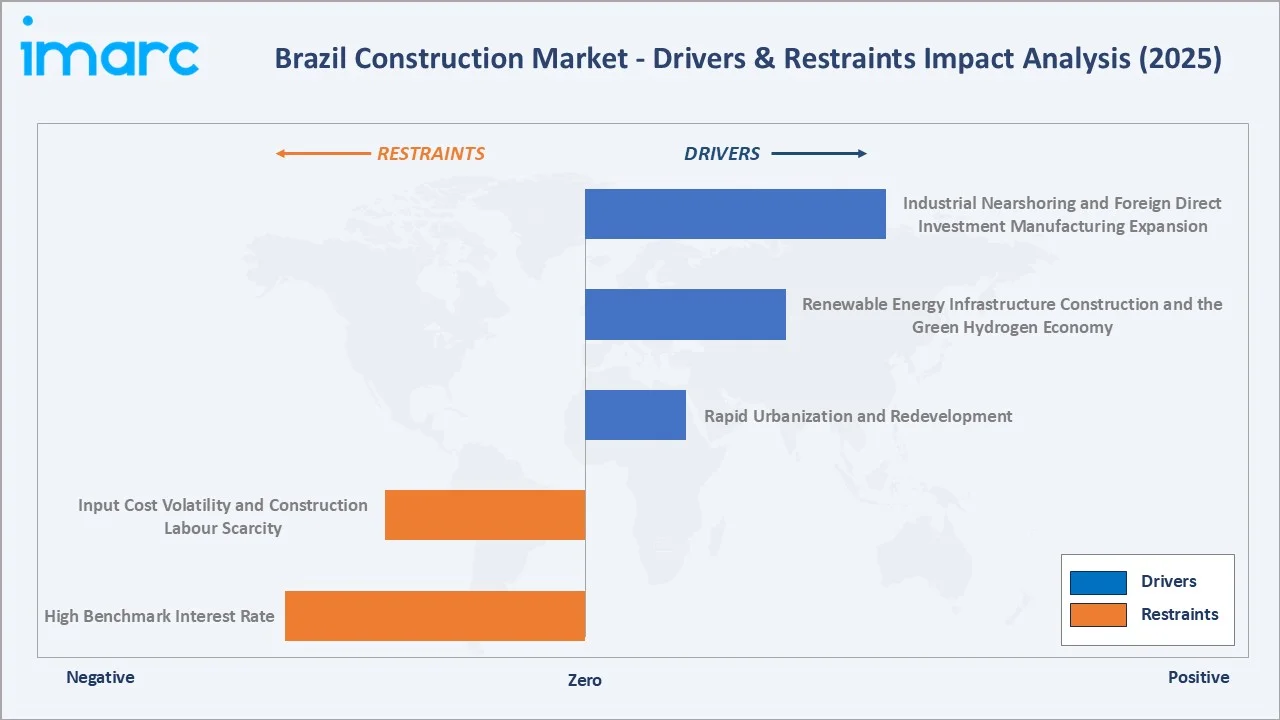

Market Drivers

- Industrial Nearshoring and Foreign Direct Investment Manufacturing Expansion: Industrial nearshoring and rising foreign direct investment are encouraging manufacturers to establish or expand production facilities in Brazil to serve its large domestic and regional markets. Foreign direct investment in Brazil increased by 6,040 USD Million in March 2026. This is increasing demand for factories, warehouses, logistics hubs, utilities, and transport infrastructure. Investments in sectors such as electric vehicles, renewable energy equipment, green fuels, batteries, and advanced manufacturing further strengthen industrial construction activity. Brazil attracted the largest share of Latin America’s FDI, supporting a sustained pipeline of construction projects.

- Renewable Energy Infrastructure Construction and the Green Hydrogen Economy: Renewable energy and green hydrogen development are creating demand for the construction of solar and wind farms, transmission networks, hydrogen production plants, storage facilities, pipelines, and port infrastructure in Brazil. The country’s low-carbon hydrogen framework and related incentives are encouraging investment in large-scale energy-transition projects. As green hydrogen hubs expand, especially near industrial and export ports, they support sustained construction activity across energy, logistics, and industrial infrastructure segments.

- Rapid Urbanization and Redevelopment: Rapid urbanization is increasing demand for housing, commercial buildings, transport systems, sanitation networks and other essential urban infrastructure across Brazil. More than 87% of Brazil’s 203 million residents lived in urban areas in 2022, with the urban population projected to reach 90% by 2050, well above the global average of 70%. This sustained urban concentration is driving demand for new housing, commercial spaces, transport links, sanitation systems and urban redevelopment, thereby supporting growth in Brazil’s construction market.

Market Restraints

- High Benchmark Interest Rate: A high benchmark interest rate increases borrowing costs for developers, contractors and homebuyers in Brazil, making project financing and mortgages less affordable. With the high Selic rate, developers may postpone new launches while buyers delay property purchases. This slows residential and commercial construction activity, particularly in market-rate projects dependent on credit. Even with gradual monetary easing, elevated real interest rates continue to limit stronger market expansion.

- Input Cost Volatility and Construction Labour Scarcity: Input cost volatility and construction labour scarcity raise project budgets, compressing contractor margins and increasing the risk of delays. Brazil’s construction cost index reflects higher materials and labour costs. Limited availability of workers further raises wages and constrains project execution, discouraging new investment and slowing market growth.

Market Opportunities

- Data Center Construction Boom: The data center construction boom presents a major opportunity as rising demand for cloud computing, artificial intelligence and digital services requires new high-capacity facilities. These projects create demand for specialized construction, power infrastructure, cooling systems, fibre connectivity and supporting utility works. Brazil’s access to renewable energy also strengthens its attractiveness for sustainable data center developments. As digital infrastructure investment expands, it opens new opportunities for contractors, engineering firms and building-material suppliers.

- Sanitation Universalization Infrastructure: Sanitation universalization infrastructure requiring expansion and modernization of water supply, sewage collection, wastewater treatment and drainage systems. The country’s sanitation framework encourages investment, concessions and public-private participation in essential infrastructure. This creates long-term project opportunities for construction companies, engineering firms, equipment providers and materials suppliers, particularly in underserved urban and regional areas.

Market Challenges

- Climate Change Physical Risks to Construction: Climate change physical risks increase exposure to floods, landslides, heatwaves, droughts and severe storms. These events can damage construction sites, disrupt material supply chains, delay project schedules and raise repair and insurance costs. Developers must also invest in resilient designs, drainage systems, flood protection and climate-adapted materials, increasing project complexity and costs. As extreme weather risks grow, projects in vulnerable urban and coastal areas may face greater planning and execution challenges.

- Supply-Chain and Logistics Constraints: Supply-chain and logistics constraints are delaying the movement of cement, steel, machinery and other essential inputs to project sites. The country’s vast geography, uneven transport infrastructure and reliance on long-distance road freight can increase delivery times and transportation costs. Disruptions or shortages may lead to project delays, budget overruns and reduced contractor margins. These issues are especially significant for large-scale infrastructure and remote-area construction projects.

Emerging Market Trends

1. BIM (Building Information Modeling) Mandatory Adoption Transforming Brazilian Construction Productivity

BIM adoption supported by government initiatives promoting its use in public construction and infrastructure projects. BIM enables integrated digital planning, improves collaboration among architects, engineers and contractors, and helps identify design conflicts before construction begins. This reduces rework, material waste, cost overruns and project delays, improving overall productivity. As BIM requirements expand in public works, construction firms are increasingly investing in digital capabilities to remain competitive.

2. Industrialized Construction and Modular Building Systems Gaining Traction

Industrialized construction and modular building systems enable faster, more predictable housing delivery. Off-site manufacturing reduces site disruption, material waste and dependence on labour-intensive construction processes. As developers seek scalable and sustainable building solutions, modular construction is creating new growth opportunities across Brazil’s construction market. In December 2024, CSN introduced a modular data center at its Presidente Vargas facility in Rio de Janeiro, demonstrating the practical application of prefabricated and off-site construction solutions in Brazil. This development highlights growing acceptance of modular systems for faster installation, improved quality control and reduced on-site complexity.

3. Sustainability Certification and Green Building Adoption Growing in Brazilian Commercial Construction

Sustainability certification and green building adoption are gaining momentum as developers seek energy-efficient, resource-conscious and environmentally responsible properties. Certifications encourage the use of efficient lighting, water-saving systems, sustainable materials and improved indoor environments. Green-certified commercial buildings can enhance asset value, reduce operating costs and attract sustainability-focused tenants and investors. This trend is creating opportunities for contractors, consultants and suppliers specializing in sustainable construction solutions.

4. Public-Private Partnership Model Expansion Attracting Private Capital to Brazilian Infrastructure

Expansion of public-private partnerships (PPPs) mobilizing private capital for infrastructure development. PPPs enable the construction and modernization of roads, urban mobility networks, sanitation facilities, schools and public buildings while sharing investment and operational responsibilities. This model helps advance large-scale projects despite public budget constraints and improves long-term asset management. In February 2026, Brazil’s federal and municipal governments introduced a new public-private partnership (PPP) model centered on rental-based social housing instead of homeownership. This trend supports Brazil’s construction market by creating new residential project opportunities, expanding affordable housing delivery and strengthening collaboration between the public sector, developers and institutional investors.

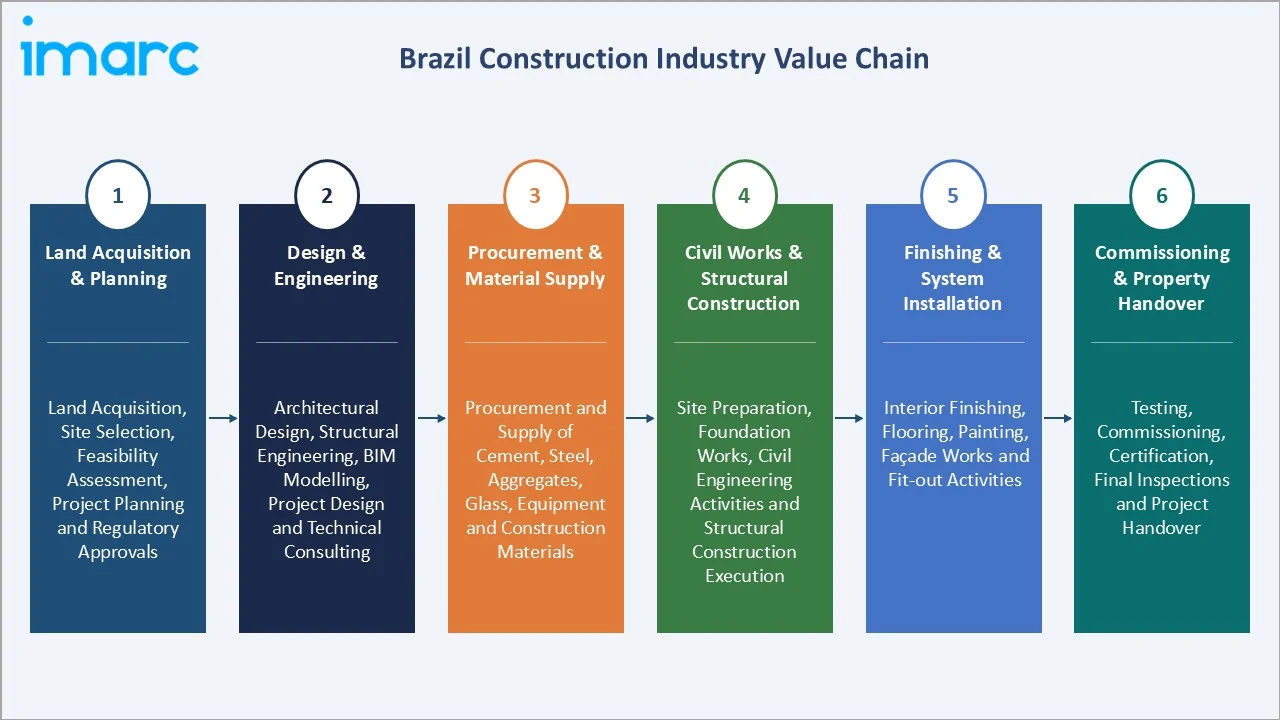

Industry Value Chain Analysis

Brazil's construction value chain integrates land acquisition and planning, design and engineering, procurement and material supply, civil works and structural construction, finishing and system installation, and project commissioning and property handover.

| Stage | Key Participants |

|---|---|

| Land Acquisition & Planning | Land acquisition, site selection, feasibility assessment, project planning and regulatory approvals |

| Design & Engineering | Architectural design, structural engineering, BIM modelling, project design and technical consulting |

| Procurement & Material Supply | Procurement and supply of cement, steel, aggregates, glass, equipment and construction materials |

| Civil Works & Structural Construction | Site preparation, foundation works, civil engineering activities and structural construction execution |

| Finishing & System Installation | Interior finishing, flooring, painting, façade works and fit-out activities |

| Commissioning & Property Handover | Testing, commissioning, certification, final inspections and project handover |

The civil works and structural construction stage is the value chain's employment and economic activity peak. The commissioning stage's professional certification requirement and municipal occupancy permit create formal quality gates that distinguish the formal construction sector from the informal self-construction sector, which bypasses these requirements but represents a significant proportion of low-income residential construction in Brazilian urban and rural areas.

Technology Landscape in the Brazil Construction Industry

Digital Construction Technologies

Digital construction technologies are improving project planning, coordination and execution. Tools such as BIM, drones, IoT sensors, digital twins and construction management software help reduce errors, delays and cost overruns. They also support real-time monitoring, better resource allocation and stronger quality control. In March 2026, buildingSMART Brazil was approved as a Full Chapter of buildingSMART International. This milestone reflects Brazil’s growing adoption of openBIM practices, driven by strong industry participation, collaborative efforts and a broader shift toward digital transformation in construction. This supports Brazil’s construction by promoting standardized data sharing, better collaboration among project stakeholders, and wider use of digital workflows, ultimately improving project efficiency, transparency and productivity.

Sustainable Construction Materials

Sustainable construction materials encouraging the use of low-carbon cement, recycled materials, engineered wood and energy-efficient building components. These materials help reduce environmental impact while improving resource efficiency and supporting green building standards. Their adoption is also driving innovation in material processing, prefabrication and circular construction practices. As sustainability goals strengthen, demand for advanced eco-friendly materials is increasing across residential, commercial and infrastructure projects.

Off-Site and Prefabricated Construction Systems

Off-site and prefabricated construction systems are shifting building activities from project sites to controlled manufacturing environments. These systems improve construction speed, quality consistency and resource efficiency while reducing material waste and labour dependence. They also support digital design integration, modular construction and industrialized building methods. As adoption increases, prefabrication is enhancing productivity and modernizing construction practices across residential and infrastructure projects.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Sector | Residential Construction | 34.6% | 2025 |

| Region | Southeast | 41.3% | 2025 |

By Construction Sector

Residential construction leads at 34.6% (2025). The residential sector encompasses social housing, market-rate residential, and premium residential. The sector's ~4.1% CAGR reflects the structural housing deficit, programme expansion, and urbanization, creating sustained demand. Infrastructure (transportation) construction at 24.8% encompasses federal highway construction, state highway expansion, railway projects, port infrastructure, airport construction, urban mobility systems, and sanitation infrastructure.

To access detailed market analysis, Request Sample

Commercial construction at 18.7% includes office, retail, logistics, and data center construction. Industrial construction at 12.9% encompasses manufacturing plants, agribusiness processing, and oil and gas industrial facilities. Energy and utility construction at 9.0% captures wind, solar, transmission, and sanitation construction.

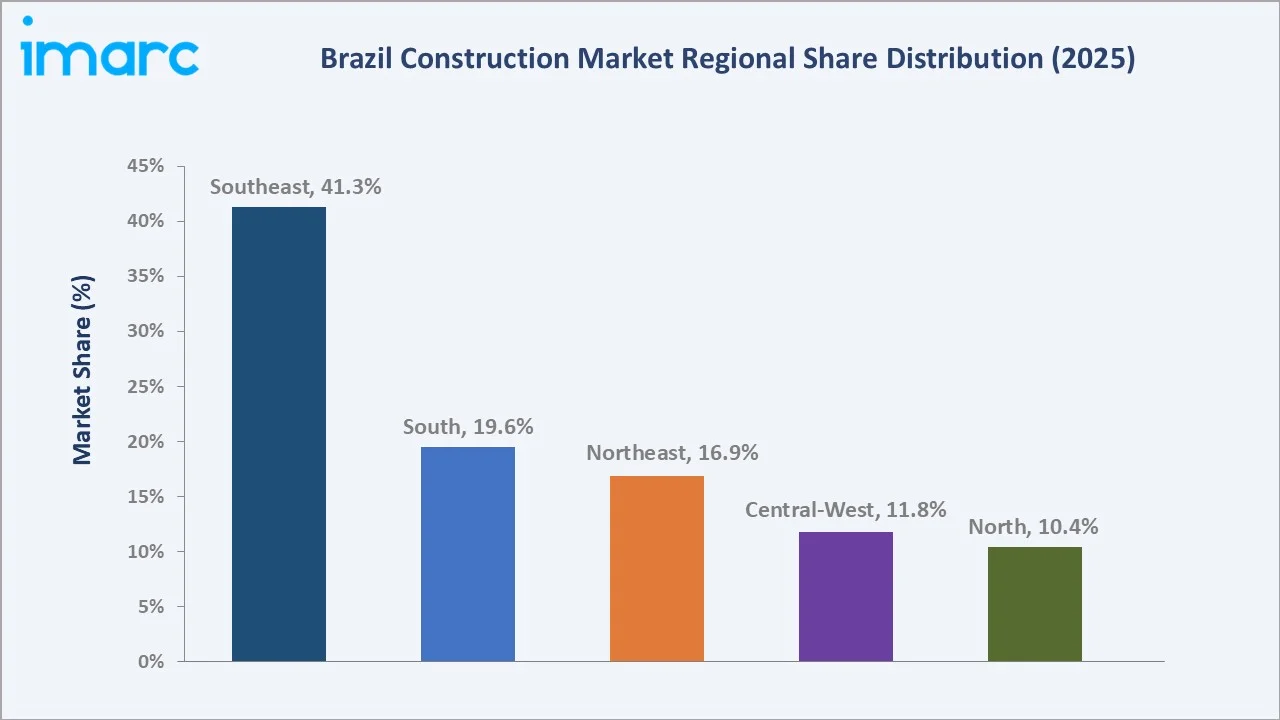

Regional Market Insights

| Region | Share (2025) | Key Construction Market Drivers & Characteristics |

|---|---|---|

| Southeast | 41.3% | Driven by the concentration of major metropolitan and economic centers, supporting strong demand across residential, commercial, industrial and infrastructure projects. |

| South | 19.6% | Supported by its industrial base, manufacturing activities, urban development and logistics infrastructure investments, driving steady construction demand. |

| Northeast | 16.9% | Driven by urban expansion, tourism-related developments, affordable housing projects and growing investment in transport, sanitation and renewable energy infrastructure. |

| Central-West | 11.8% | Benefits from agribusiness expansion, logistics development, warehousing demand and infrastructure projects supporting agricultural production and regional connectivity. |

| North | 10.4% | Supported by infrastructure modernization, mining and energy investments, urban development and connectivity projects, offering long-term construction growth opportunities. |

The Southeast's construction market dominance is reinforced by the data center investment boom, oil and gas industrial construction, and mining rehabilitation construction. The South benefits from industrial development, logistics networks, and stable urban construction, while the Northeast is driven by housing, tourism, sanitation, and renewable energy projects.

The Central-West gains momentum from agribusiness-linked logistics and warehousing, and the North offers long-term opportunities through energy, mining, connectivity, and infrastructure modernization.

Competitive Landscape

Brazil's construction market competitive landscape is stratified across heavy infrastructure, residential development, and commercial and industrial construction.

| Company Name | Key Brands | Market Position | Core Strength |

|---|---|---|---|

| Cyrela | Living, Cyrela, and Vivaz | Market Leader | Cyrela is a major force in the Brazilian construction and real estate market, widely recognized as one of the largest and most prominent developers in the country, particularly within the luxury segment. |

| Tecnisa | Tecnisa | Strong Challenger | Tecnisa is a prominent Brazilian real estate developer and construction firm specializing in high-quality residential and commercial projects. |

| Eztec | Eztec | Established Player | Eztec is a major player in Brazil's real estate sector, specializing in engineering, construction, and real estate development activities under the Eztec brand. |

| Multiplan Empreendimentos Imobiliários S.A. | Multiplan | Established Player | Multiplan Empreendimentos Imobiliários S.A. plays a leading role in the Brazilian construction and real estate sector, primarily as a premier developer, owner, and manager of high-quality shopping centers, mixed-use complexes, and commercial properties. |

Major players compete through project execution capabilities, public-private partnerships, infrastructure expertise, sustainable construction solutions, and digital technologies such as BIM and modular construction. Companies are also expanding through strategic partnerships, concessions, and investments in residential, industrial, logistics, and renewable energy projects.

Key Company Profiles

Cyrela

Cyrela is one of Brazil’s leading residential real estate developers and construction companies, primarily focused on high-end and mid-to-high income residential projects. The company develops apartments, condominiums and mixed-use projects across major Brazilian cities through brands such as Cyrela, Living, and Vivaz.

- Key Brands: Cyrela, Living, and Vivaz.

- Strategic Focus: Expanding premium and mid-income residential developments in major urban markets, supported by strong land bank management, partnerships, digital sales, and sustainable construction practices.

Tecnisa

Tecnisa is a Brazilian real estate developer and construction company focused on residential and mixed-use developments, primarily in major urban centers. The company operates across project development, construction, sales and property management, with a portfolio spanning mid- to high-income housing segments.

- Key Brands: Tecnisa.

- Strategic Focus: Residential development in São Paulo, emphasizing innovation, digital sales, operational efficiency, and selective launches in mid- and high-income housing projects.

Market Concentration Analysis

Brazil's construction market is highly fragmented at the overall industry level. This fragmentation reflects the labor-intensive, geographically distributed nature of residential construction, where small local builders serve local residential markets without competitive scale requirements, the project-specific nature of construction requiring different specialist capabilities across segments, and the historically low barriers to entry in basic residential construction. Concentration is higher within specific construction market segments.

Investment & Growth Opportunities

Highest Growth Segments

Data center construction (~20% CAGR), sanitation infrastructure construction (~6% CAGR from sanitation mandate), offshore wind pre-construction and civil works (~25% CAGR), BEV manufacturing industrial park construction (~15% CAGR), Amazon bioeconomy infrastructure (~8% CAGR), MCMV residential (~4.1% CAGR), represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Brazil's sanitation universalization programme represents the most structurally certain long-term construction investment opportunity. The Basic Sanitation Law's regulatory clarity provides investment-grade certainty that attracts institutional capital.

Investment Themes

- Data center construction specialization for hyperscaler and colocation market in Brazil's infrastructure investment wave: The 2024-2028 hyperscaler data center investment wave creates a specialized construction market requiring capabilities in Tier III/IV data center civil construction, MEP (mechanical, electrical, plumbing) systems engineering, and low-latency fibre connectivity installation that general civil contractors typically lack.

- Affordable housing development innovation: Brazil's housing deficit will not be solved by government subsidy alone. Brazilian construction technology startups represent the innovation ecosystem developing alternatives to conventional affordable housing construction that address the cost and speed constraints.

Future Market Outlook (2026-2034)

Brazil's construction market is projected to grow from USD 155.98 Billion in 2025 to USD 218.19 Billion by 2034, delivering a 3.80% CAGR over the forecast period. The market's anchor value of USD 187.95 Billion in 2030 represents a Brazilian construction industry at a structural inflection point. The 2026-2030 phase is the period of peak infrastructure construction investment, with railway construction progressing, offshore wind development consent and construction start, and green hydrogen production facility construction beginning after 2027-2028 project sanctions. Three structural forces define Brazil's construction market growth through 2034 with confidence. Brazil's demographic dividend creates inescapable housing demand. Infrastructure catch-up investment is politically irreversible across government administrations. The digital economy construction wave has no political or economic dependency.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including CEO-level executives, Infrastructure Project Directors, Government Affairs and Policy Directors, Project Finance Directors, commercial real estate professionals, materials company executives, construction technology consultants, and construction industry syndicate data.

Secondary Research

Secondary research encompassed annual construction industry reports, construction employment statistics, construction material sales data, housing deficit studies, project finance disbursement data, financial stability and credit data, company annual reports, programme implementation reports, electricity sector annual reports, regional sanitation sector data, and Brazil commercial real estate market data. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a sector-based bottom-up model: (i) residential sector; (ii) infrastructure sector; (iii) commercial and industrial; (iv) energy and utility.

Brazil Construction Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Commercial Construction, Residential Construction, Industrial Construction, Infrastructure (Transportation) Construction, Energy and Utility Construction |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Cyrela, Tecnisa, Eztec, Multiplan Empreendimentos Imobiliários S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil construction market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil construction market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil construction industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Construction Market Report

Brazil's construction market reached USD 155.98 Billion in 2025, representing Latin America's largest construction market. The market is driven by residential construction at 34.6%, infrastructure at 24.8%, Southeast region dominance at 41.3%, and the construction industry stabilization, creating a more compliant but smaller-capacity heavy construction sector.

Brazil's construction market grows at 3.80% CAGR during 2026-2034, reaching USD 218.19 Billion by 2034. This growth reflects housing deficit structural demand, infrastructure investment execution, data center commercial construction boom, sanitation universalization utility construction, and industrial nearshoring plant construction, collectively sustaining above-GDP construction market growth through the forecast period.

Residential construction leads at 34.6% through Brazil's housing deficit and urban densification residential demand.

The Southeast region leads at 41.3% through São Paulo's GDP concentration, Rio de Janeiro's petroleum industry, and mining sector. São Paulo specifically is experiencing the data center construction boom, creating above-trend commercial construction growth.

Leading companies include Cyrela, Tecnisa, Eztec, and Multiplan Empreendimentos Imobiliários S.A., among others.

Brazil's construction market is projected to reach approximately USD 187.95 Billion by 2030, with infrastructure construction in the peak execution phase, sanitation concession construction programmes in mid-execution, nearshoring industrial plant construction, and offshore wind first-wave construction commencing.

Brazil's data center construction market is experiencing a boom driven by hyperscaler capital expenditure commitments. Data center construction is valuable to Brazil's construction market for three reasons: high construction value per square metre, technical specialization requirements, and concentration in Greater São Paulo, creating economic impact.

Three priority investment themes: data center construction specialization, sanitation universalization construction, and Northeast renewable energy and green hydrogen infrastructure positioning.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)