Brazil Green Cement Market Size, Share, Trends and Forecast by Product Type, End-Use Industry, and Region, 2026-2034

Brazil Green Cement Market Summary:

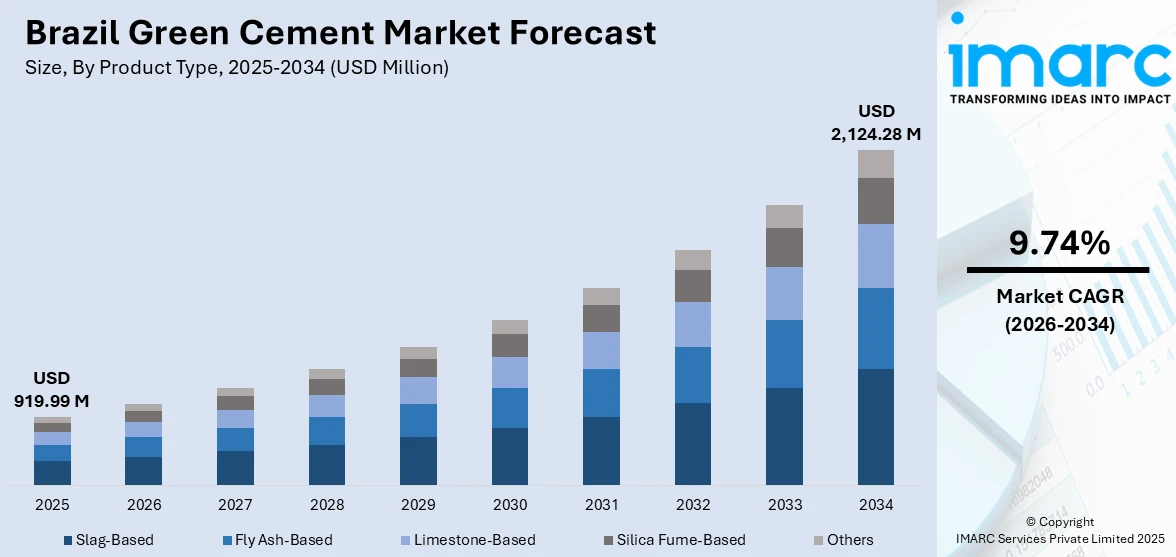

The Brazil green cement market size was valued at USD 919.99 Million in 2025 and is projected to reach USD 2,124.28 Million by 2034, growing at a compound annual growth rate of 9.74% from 2026-2034.

The Brazil green cement market is advancing steadily, driven by rising environmental consciousness and government sustainability mandates. Growing infrastructure investments, expanding construction activities, and increasing adoption of eco-friendly building materials are reshaping the landscape. Advancements in low-carbon manufacturing technologies, renewable energy integration, and circular economy practices position Brazil as an emerging leader in sustainable construction solutions across Latin America.

Key Takeaways and Insights:

- By Product Type: Slag-based green cement dominates the market with a share of 35.7% in 2025, owing to its superior durability, enhanced resistance to chemical attack, and lower carbon emissions compared to conventional Portland cement. Abundant availability of blast furnace slag from steel manufacturing facilities supports production expansion.

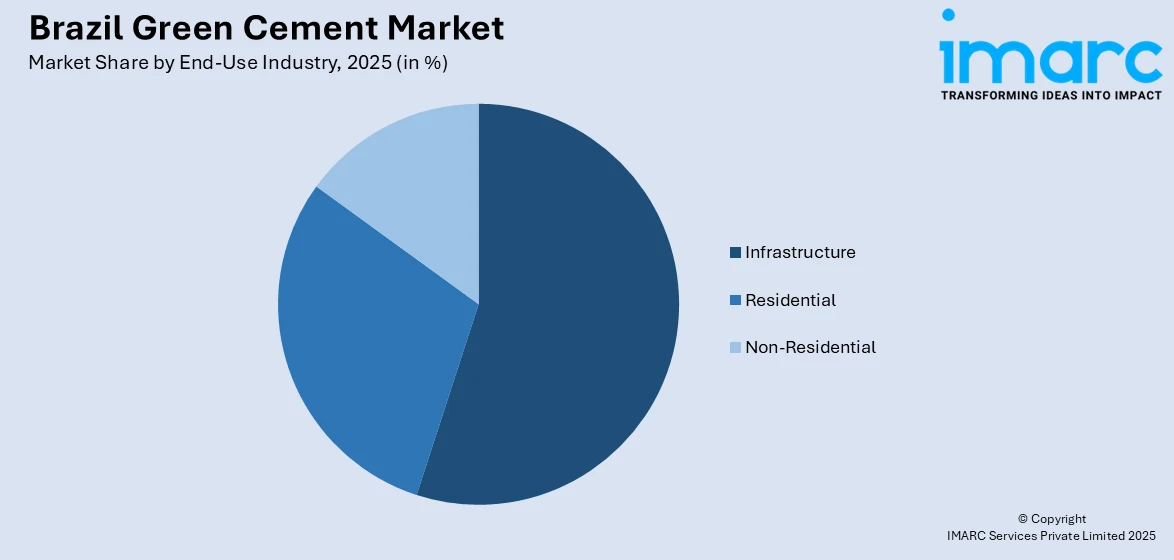

- By End-Use Industry: Infrastructure leads the market with a share of 44.3% in 2025. This dominance is driven by massive government investments through programs such as Novo PAC, increasing demand for sustainable materials in public works, and stringent environmental regulations requiring lower carbon construction practices.

- By Region: Southeast Brazil represents the largest region with 46.5% share in 2025, driven by the concentration of major construction projects in São Paulo and Rio de Janeiro metropolitan areas, proximity to industrial by-product suppliers, and the presence of leading cement manufacturers.

- Key Players: Key players drive the Brazil green cement market by investing in low-carbon technologies, expanding co-processing capabilities, developing innovative product formulations, and forming strategic partnerships. Their commitment to sustainability certifications and environmental product declarations strengthens market positioning.

To get more information on this market Request Sample

The Brazil green cement market is experiencing robust expansion as environmental imperatives converge with economic development priorities. Government initiatives emphasizing sustainable infrastructure, combined with growing private sector awareness of carbon reduction benefits, are accelerating adoption across construction segments. The market is characterized by increasing investment in alternative raw materials, advanced clinker substitution technologies, and renewable energy integration throughout production processes. Leading manufacturers are pioneering environmental product declarations and obtaining international sustainability certifications to meet evolving procurement standards. The convergence of regulatory frameworks promoting green building standards, rising consumer preference for environmentally responsible construction materials, and Brazil's commitment to carbon neutrality targets creates favorable conditions for sustained market growth. These factors position Brazil as a regional leader in sustainable cement production and consumption.

Brazil Green Cement Market Trends:

Low-Carbon Cement Innovation Gaining Momentum

Brazilian cement manufacturers are accelerating investment in innovative low-carbon cement formulations to align with international emission standards. Companies are actively developing limestone-calcined clay cement variants and integrating industrial by-products into blended cement portfolios. These innovations reduce clinker content while maintaining structural performance, addressing environmental concerns without compromising construction quality. The trend reflects broader industry commitment to achieving carbon neutrality goals established for the cement sector, supporting Brazil green cement market growth.

Expansion of Alternative Fuel Co-Processing

Waste-derived fuel utilization is expanding rapidly across major cement production facilities in Brazil. Leading producers have increased co-processing of biomass, urban solid waste, and used tires at plants in São Paulo and Minas Gerais. These initiatives replace petroleum coke with alternative energy sources, significantly reducing greenhouse gas emissions while providing environmentally responsible waste disposal solutions. Enhanced thermal substitution rates at key facilities demonstrate successful implementation of circular economy principles within cement manufacturing operations.

Growing Adoption of Green Building Certifications

Brazil's construction sector is witnessing accelerating adoption of green building certification programs that prioritize sustainable materials including green cement. The country ranked ninth globally in total LEED-certified space in 2024, certifying 125 projects representing over two Million square meters. Environmental product declarations for cement and concrete products enable informed procurement decisions, driving specification of low-carbon materials in certified projects. This certification momentum strengthens demand for verified sustainable construction materials.

Market Outlook 2026-2034:

The outlook for Brazil Green Cement remains optimistic since the country continues to march forward in its developmental goals towards being carbon neutral, while at the same time, its infrastructural development goals are ambitious. The government initiatives of Novo PAC and Minha Casa, Minha Vida also remain instrumental in ensuring the expansion of the construction industry. The developments in the technology of its products, which aid in the reduction of carbon emissions, are expected to help in the meeting of heightened environmental sustainability requirements while meeting the growing needs of the construction industry for eco-friendly building solutions. The market generated a revenue of USD 919.99 Million in 2025 and is projected to reach a revenue of USD 2,124.28 Million by 2034, growing at a compound annual growth rate of 9.74% from 2026-2034.

Brazil Green Cement Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Slag-Based |

35.7% |

|

End-Use Industry |

Infrastructure |

44.3% |

|

Region |

Southeast |

46.5% |

Product Type Insights:

- Fly Ash-Based

- Slag-Based

- Limestone-Based

- Silica Fume-Based

- Others

Slag-based green cement dominates with a market share of 35.7% of the total Brazil green cement market in 2025.

Slag-based green cement leverages granulated blast furnace slag, an industrial by-product from steel manufacturing, as a partial substitute for clinker in cement production. This substitution significantly reduces carbon dioxide emissions while enhancing cement durability and resistance to chemical attack. The product demonstrates superior performance in aggressive environmental conditions, making it particularly suitable for infrastructure applications requiring long service life. Brazil's robust steel industry ensures consistent slag availability, providing cement manufacturers with reliable feedstock for green cement formulations that meet stringent sustainability requirements.

The segment benefits from growing recognition of slag cement's environmental and technical advantages among construction professionals and project specifiers. Major cement producers are expanding slag cement capacity and obtaining sustainability certifications for their products. The Falcão Bauer Quality Institute has certified slag-based cement products for all construction applications, confirming reduced carbon footprint compared to conventional cement formulations. Integration of slag cement into green building projects supports achievement of environmental certification requirements, further driving demand as sustainability considerations increasingly influence construction material procurement decisions.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Non-Residential

- Infrastructure

Infrastructure leads with a share of 44.3% of the total Brazil green cement market in 2025.

The infrastructure segment dominates green cement consumption driven by substantial government investment in public works projects emphasizing sustainable construction practices. Federal programs prioritize environmentally responsible materials in transportation networks, sanitation systems, and energy infrastructure development. Green cement's enhanced durability characteristics align with infrastructure requirements for long service life and minimal maintenance needs. New federal procurement frameworks are promoting sustainable materials in public builds, incentivizing specification of blended and low-carbon cement formulations for roads, bridges, water treatment facilities, and other critical infrastructure applications.

The reactivation of major infrastructure projects under Brazil's Novo PAC initiative has significantly driven cement demand for roads, bridges, and sanitation systems across multiple regions. In September 2024, the World Bank approved a USD 150 Million loan to improve road infrastructure in Bahia state, benefiting over 2.35 million people as part of a larger USD 1.662 Billion initiative to enhance road infrastructure management nationwide. Such investments emphasize environmental sustainability and increasingly mandate use of lower-carbon construction materials, supporting sustained growth in green cement consumption within the infrastructure segment.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

The Southeast region exhibits a clear dominance with a 46.5% share of the total Brazil green cement market in 2025.

Southeast Brazil has the highest share of the market, driven by economic activity, population density, and resultant construction demand concentrated in São Paulo and Rio de Janeiro metropolitan areas. The region benefits from well-established industrial infrastructure and proximity to major steel manufacturing facilities supplying slag and other supplementary cementitious materials essential for green cement production. Advanced logistics networks and port access facilitate efficient material transportation, supporting cost-competitive green cement manufacturing and distribution throughout the region.

The dominance of the Southeast region is further supported by the presence of major cement producers with multiple facilities capable of advanced co-processing and low-carbon technologies. Robust construction activity across residential, commercial, and infrastructure development projects maintains steady demand for green cement. The developed green building certification framework and increasing trend toward sustainability standards among developers and contractors in the region provide favorable conditions for continuing market leadership in environmentally responsible construction materials.

Market Dynamics:

Growth Drivers:

Why is the Brazil Green Cement Market Growing?

Government Infrastructure Investment Programs

Large infrastructure investment programs of the federal and state governments are considered one of the key drivers fueling the growth of the green cement market in Brazil. Large infrastructure projects focus on the implementation of sustainable building practices and advocate the adoption of eco-friendly building materials in the requirements of the projects. Large infrastructure projects such as transportation projects, e.g., highways, rails, and ports, require high quantities of cement, where the adoption of the green cement formula has been increasingly favored considering the high quality of the material, which not only resists harsh environmental conditions but also promotes sustainability and eco-friendliness. Water and sanitation projects are also adopting eco-friendly materials as part of the environmental requirements of the projects.

Housing Development Programs and Urban Expansion

Housing development programs targeting Brazil's substantial housing deficit generate significant green cement demand across residential construction segments. Government-backed affordable housing initiatives provide financing mechanisms enabling broader market participation while establishing sustainability standards for supported projects. Urban expansion in major metropolitan areas and secondary cities creates construction opportunities where environmental considerations increasingly influence material selection decisions. Rising environmental awareness among homebuyers drives developer attention to sustainable building materials and green certification achievement. The Minha Casa, Minha Vida program has established itself as an essential driver for the cement industry, with program launches growing by 7.9% and sales registering a 15.5% increase in recent periods. The North region demonstrated particular strength, where the program accounted for 60 percent of real estate launches. Higher income ceilings now allow households to access subsidized mortgages, broadening the demand pool for housing construction and associated building materials. These housing initiatives create consistent baseline demand for cement products, with green formulations gaining specification preference as developers seek environmental certifications and respond to consumer sustainability preferences.

Sustainability Regulations and Decarbonization Commitments

Increased environmental regulations and industry decarbonization commitments continue to favor the adoption of green cement across the Brazilian construction markets. The production of cement contributes a great deal to carbon dioxide emissions, and thus developers face increased regulatory pressure for transition toward lower-carbon methods in the manufacture of the product. Government sustainability frameworks support emission reduction targets on the cement industry, making necessary transformations through alternative raw materials, energy efficiency improvements, and innovative production technologies. Carbon footprint considerations will significantly be integrated into the environmental standards of the construction sector and, therefore, material specifications; this will create particular competitive advantages through the availability of verified low-carbon cement products. The Brazilian Cement Industry has made immense progress regarding environmental performance through heavy investment by leading producers in the decarbonization of the production. New federal procurement frameworks encourage the use of sustainable materials in public builds through promotion of blended and low-carbon cement formulations. Environmental product declarations enable clear transparency in the communication of cement carbon footprints, enabling information specification decisions from construction professionals. Green building certification programs requiring sustainable material documentation further institutionalize demand for environmentally verified cement products, creating sustained market growth drivers.

Market Restraints:

What Challenges the Brazil Green Cement Market is Facing?

Higher Production Costs Compared to Conventional Cement

Green cement production typically involves higher costs than conventional cement manufacturing due to specialized raw material processing, advanced production technologies, and sustainability certification requirements. These elevated costs translate to premium pricing that may limit adoption among price-sensitive construction projects and budget-constrained builders. While long-term durability benefits offset initial cost premiums for many applications, upfront expense considerations continue affecting procurement decisions in competitive bidding situations.

Energy and Fuel Price Volatility

Energy and fuel price volatility significantly impacts green cement production economics and market stability. Diesel and electricity price fluctuations, particularly those driven by drought-linked hydroelectric dependency, raise operational costs affecting kiln operations and overall manufacturing expenses. Cement producers have reported temporary production scheduling adjustments during peak energy pricing periods to control input costs, potentially affecting supply consistency and market development momentum.

Raw Material Supply and Quality Variability

Raw material supply challenges and quality variability pose ongoing constraints for green cement market development. Availability of supplementary cementitious materials depends on industrial by-product generation from steel manufacturing and other sectors, creating supply chain dependencies outside cement industry control. Limestone quality variability and increased scrutiny over quarry rehabilitation plans affect long-term resource planning, with several projects postponed due to community opposition and delayed environmental consultations.

Competitive Landscape:

Competition within the green cement market of Brazil is partly portrayed by the pace of established cement manufacturers into sustainable production and product portfolios. For differentiation, they're laying their bets on investments in low-carbon technologies, development of co-processing capabilities, and achieving environmental certifications. Their focus is on the development of new cement formulations that reduce clinker content while meeting structural performance requirements. Strategic industrial suppliers will ensure the reliable supply of supplementary cementitious materials to the participants. Demonstrated environmental performance, carbon footprint transparency, and capability to meet green building certification requirements represent new key factors that competitively position the players in the green cement market. The manufacturers also establish more extended distribution networks and reinforce customer relationships with technical support services to facilitate the specification of green cements for a wide range of construction uses.

Recent Developments:

- In October 2024, Votorantim Cimentos launched Blenture, a new brand of cement and concrete designed to reduce CO₂ emissions and promote sustainable construction practices. Blenture products offer a 30 percent lower carbon footprint while maintaining quality, strength, and performance standards required for demanding construction applications.

Brazil Green Cement Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Fly Ash-Based, Slag-Based, Limestone-Based, Silica Fume-Based, Others |

|

End-Use Industries Covered |

Residential, Non-Residential, Infrastructure |

|

Regions Covered |

Southeast, South, Northeast, North, Central-West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Green Cement Market Report

The Brazil green cement market size was valued at USD 919.99 Million in 2025.

The Brazil green cement market is expected to grow at a compound annual growth rate of 9.74% from 2026-2034 to reach USD 2,124.28 Million by 2034.

Slag-based green cement dominated the market with a share of 35.7%, driven by superior durability, enhanced chemical resistance, and environmental benefits from utilizing industrial by-products in cement formulation.

Key factors driving the Brazil green cement market include government infrastructure investment programs, housing development initiatives, sustainability regulations, growing adoption of green building certifications, and industry decarbonization commitments.

Major challenges include higher production costs compared to conventional cement, energy and fuel price volatility affecting manufacturing economics, raw material supply dependencies, quality variability, and regional infrastructure gaps limiting market access in remote areas.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)