Canada Pulses Market Size, Share, Trends and Forecast by Type, Domestic Consumption and Exports, End-Use, and Region, 2026-2034

Canada Pulses Market Size, Share, Trends & Forecast (2026-2034)

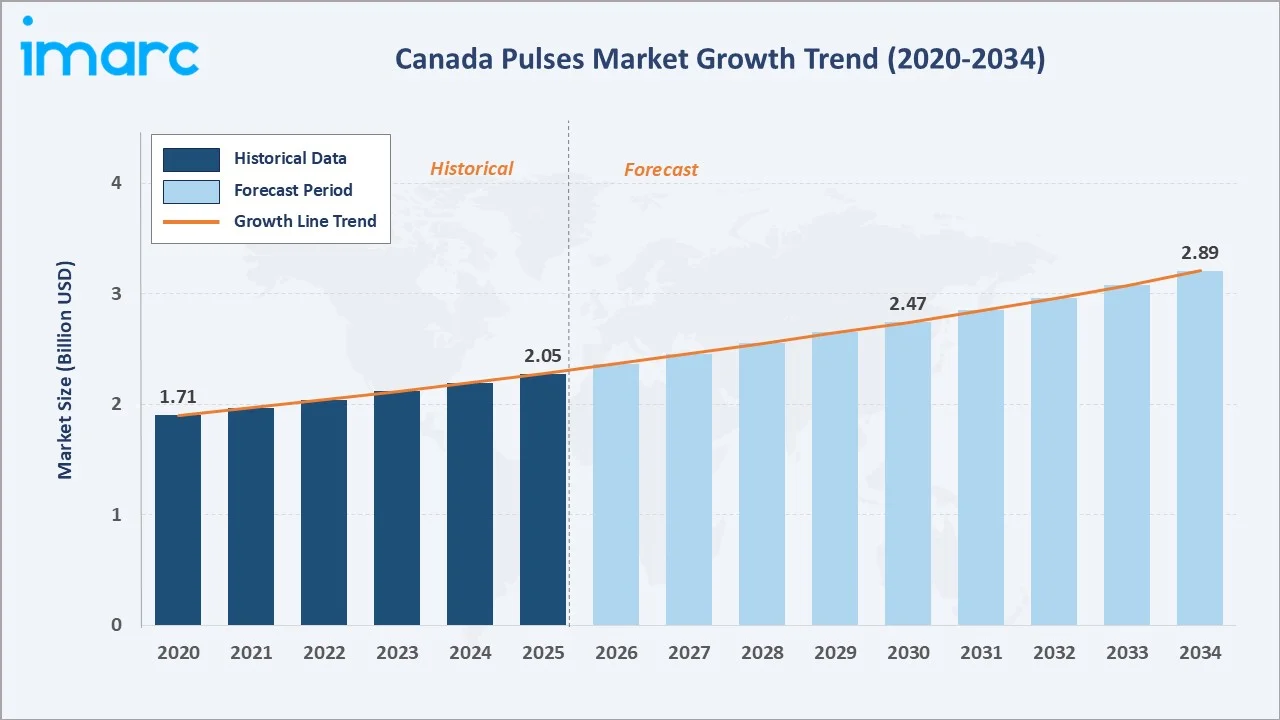

The Canada pulses market reached USD 2.05 Billion in 2025 and is projected to reach USD 2.89 Billion by 2034, growing at a CAGR of 3.75% during 2026-2034. The market is driven by strong export demand for lentils, peas, chickpeas, and beans, supported by Canada’s position as a leading pulse producer and supplier. Around 8.3 million acres of pulses are cultivated annually across the country, mainly in Alberta, Saskatchewan, Manitoba, and Ontario. Canada also exports nearly 5.5 million tonnes of pulses each year, supplying key food markets worldwide, driving the market growth. Dry peas lead type at 33.0%. Exports lead at 72.0%. Saskatchewan leads regionally at 48.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.05 Billion |

|

Forecast Market Size (2034) |

USD 2.89 Billion |

|

CAGR (2026-2034) |

3.75% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Dry Peas (33.0%, 2025) |

|

Dominant Domestic Consumption and Exports |

Exports (72.0%, 2025) |

|

Leading Region |

Saskatchewan (48.0%, 2025) |

The Canada pulses market has shown steady growth, rising from USD 1.71 Billion in 2020 to USD 2.05 Billion in 2025, supported by strong export demand, expanding plant-based protein consumption, and Canada’s established pulse production base. The market is expected to reach USD 2.47 Billion by 2030 as food processors increasingly use lentils, peas, chickpeas, and beans in protein-rich and sustainable food products. By 2034, the market is forecast to touch USD 2.89 Billion, driven by global food security needs, rising health awareness, and growing demand from emerging import markets.

To get more information on this market, Request Sample

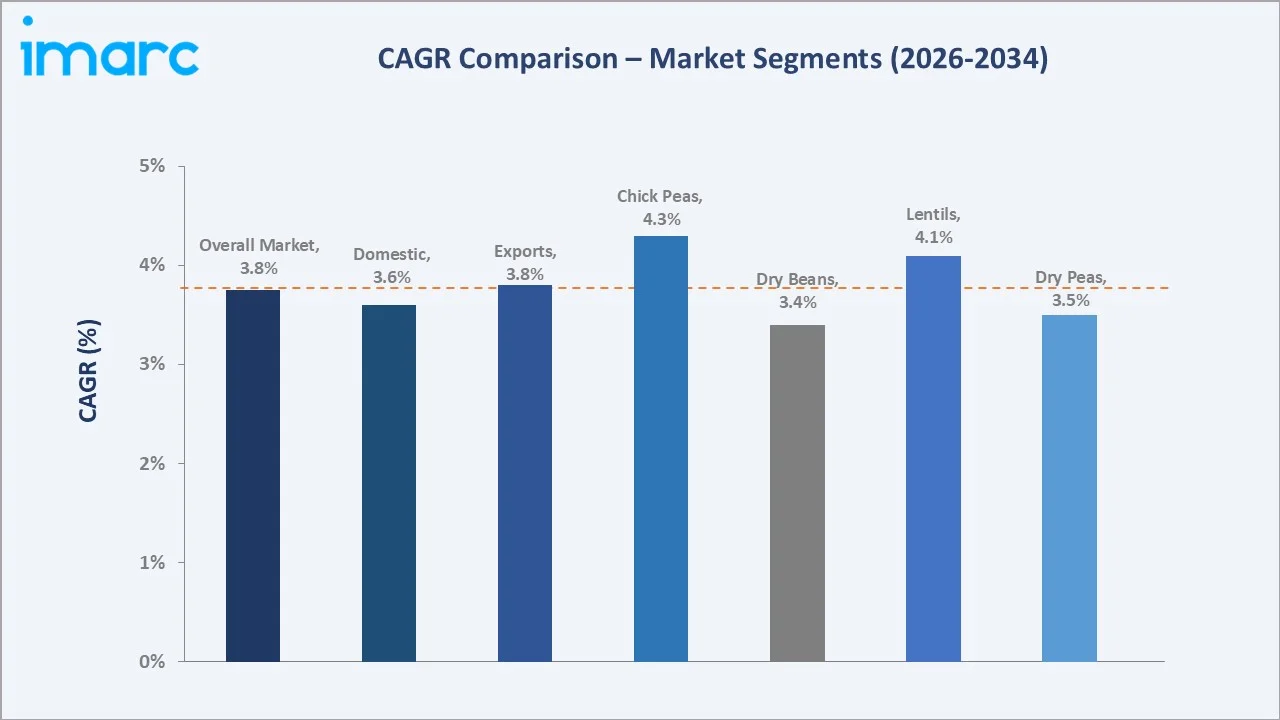

Chickpeas grow fastest at ~4.3% CAGR through rising hummus, chickpea protein, and South Asian cooking demand. Lentils grow at ~4.1% CAGR through expanding plant-based protein ingredient and India demand. Exports grow at ~3.8% CAGR through expanding South and Southeast Asia Consumption.

Executive Summary

The Canada pulses market is witnessing steady growth, supported by the country’s strong position as a leading global producer and exporter of lentils, peas, chickpeas, dry beans, and faba beans. The market increased from USD 1.71 Billion in 2020 to USD 2.05 Billion in 2025 and is projected to reach USD 2.89 Billion by 2034. Growth is driven by rising global demand for plant-based proteins, sustainable crops, and protein-rich food ingredients. Strong cultivation across Alberta, Saskatchewan, Manitoba, and Ontario, along with robust export volumes, continues to strengthen Canada’s role in global pulse trade. Dry peas at 33.0% lead through the world-export-leader. Exports at 72.0% lead through demand from India, China, and Bangladesh. Saskatchewan leads regionally at 48.0%.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Dry Peas - 33.0% share (2025) |

|

Dominant Domestic Consumption and Exports |

Exports - 72.0% market share (2025) |

|

Leading Region |

Saskatchewan - 48.0% share (2025) |

|

Market Opportunity |

Pulse protein ingredient for plant-based food; value-added pulse processing (flour, starch, protein isolate); chickpea pasta and lentil snack; precision agriculture yield optimization |

Key Analytical Observations Supporting the Above Data:

- Dry Peas at 33.0%: Dry peas dominate the market due to their large cultivation base, strong export demand, and wide use in food, feed, starch, and plant-based protein applications. Their cost competitiveness, high protein content, and demand from markets such as China and South Asia further support their leading share.

- Exports at 72.0%: Exports dominate the market as a major share of production is shipped to international markets, supported by strong demand from Asia, the Middle East, Africa, and Europe.

- Saskatchewan at 48.0%: Saskatchewan dominates due to its vast arable land, favorable prairie climate, and strong specialization in lentil and dry pea cultivation. The province also benefits from established grain-handling infrastructure, export logistics, and experienced pulse growers, strengthening its leading market share.

Canada Pulses Market Overview

Canada's pulse market encompasses a wide range of crops, including dry peas, lentils, chickpeas, dry beans, and faba beans, serving both domestic and international demand. The market is strongly export-oriented, with Canada supplying pulses to Asia, the Middle East, Africa, Europe, and other global food markets. Production is concentrated across key prairie provinces, especially Saskatchewan, Alberta, and Manitoba, supported by suitable agro-climatic conditions and large-scale farming systems. Pulses are increasingly used in food processing, plant-based protein products, animal feed, and sustainable crop rotation systems. Rising demand for nutritious, protein-rich, and environmentally sustainable foods continues to strengthen the market outlook. Macroeconomic factors include rising global food demand, expanding plant-based protein consumption, export trade dynamics, and commodity price movements.

Market Dynamics

To evaluate market opportunities, Request Sample

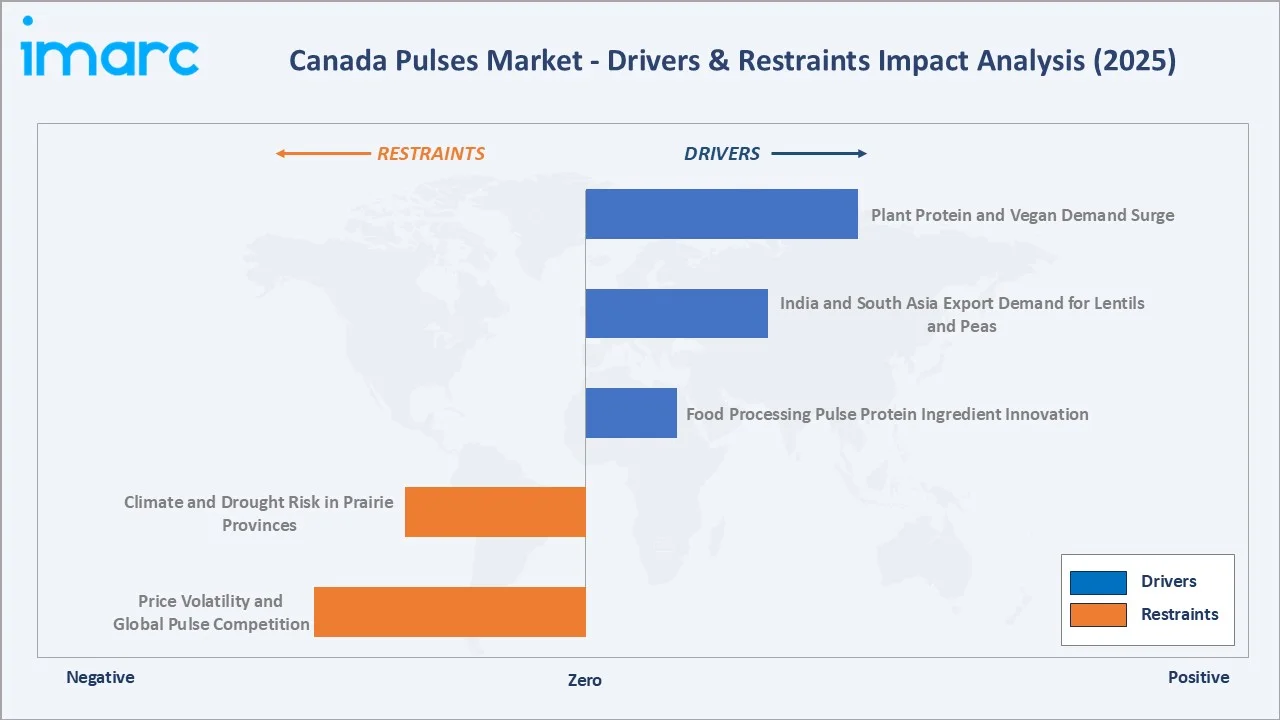

Market Drivers

- Plant Protein and Vegan Demand Surge: Canadian consumers are increasingly preferring nutritious, high-protein, and plant-based food alternatives. According to a survey by Humane World for Animals, 54% of Canadians are either already trying to increase their intake of plant-based foods or are interested in doing so. The survey further shows that 24% of Canadians are actively working to consume more plant-based foods, while another 30% are considering increasing their intake in the future. As more consumers shift toward plant-based diets, demand rises for protein-rich ingredients such as dry peas, lentils, chickpeas, and beans. These pulses are widely used in meat substitutes, protein powders, snacks, bakery products, and ready-to-eat meals. Their clean-label appeal, high fiber content, and lower environmental footprint make them attractive for food manufacturers.

- India and South Asia Export Demand for Lentils and Peas: India and South Asia export demand for lentils and peas is strongly driving the market, as these regions have large vegetarian populations and high pulse consumption in daily diets. Canada is a key supplier of red lentils, yellow peas, and other pulses used in dals, snacks, flours, and traditional foods. In 2024, Canada shipped 1.4 million tonnes of peas and 600,000 tonnes of lentils to India, valued at USD 1.4 billion. Domestic production gaps, population growth, and food security needs in South Asian markets support consistent import demand. This strengthens Canada’s export volumes, improves price realization for growers, and encourages continued investment in pulse cultivation and processing.

- Food Processing Pulse Protein Ingredient Innovation: Food processing pulse protein ingredient innovation is driving the market as manufacturers increasingly use pea, lentil, chickpea, and bean proteins in plant-based meat, dairy alternatives, bakery, snacks, and nutrition products. Pulses offer high protein, fiber, clean-label appeal, and functional properties such as binding, texture enhancement, and emulsification. This is encouraging investment in pulse fractionation, protein concentrates, flours, and isolates across Canada. As food companies seek sustainable and allergen-friendly alternatives to soy and animal protein, demand for Canadian pulses continues to strengthen.

Market Restraints

- Climate and Drought Risk in Prairie Provinces: Climate and drought risk in the Prairie Provinces directly affect crop yields, quality, and harvest consistency. Pulses such as lentils and peas are highly sensitive to moisture stress, especially during flowering and pod-filling stages. Drought conditions in Saskatchewan, Alberta, and Manitoba can reduce output, increase price volatility, and weaken export reliability. Unpredictable weather also raises irrigation, crop insurance, and farm input costs, pressuring grower margins and limiting stable market expansion.

- Price Volatility and Global Pulse Competition: Price volatility and global pulse competition are creating uncertainty in farmer incomes, export margins, and buyer contracts. Prices of lentils, peas, and chickpeas are influenced by weather shocks, currency movements, freight costs, and changing import policies in key markets. At the same time, rising production from competitors such as Australia, Russia, Turkey, and India increases pressure on Canada’s export share. This limits pricing power for Canadian suppliers and can reduce profitability during periods of oversupply or weaker global demand.

Market Opportunities

- Growth in Pulse-Based Snacks and Ready Meals: Growth in pulse-based snacks and ready meals presents a strong opportunity as consumers increasingly seek convenient, protein-rich, and healthier food options. Pulses such as peas, lentils, chickpeas, and beans are being used in chips, crackers, pasta, soups, frozen meals, and ready-to-eat bowls. Their high fiber, plant protein, and clean-label appeal make them attractive to food manufacturers targeting health-conscious and vegan consumers. This trend can support higher value-added processing in Canada and reduce dependence on bulk raw pulse exports.

- Advanced Pulse Disease-Control Solutions: Advanced pulse disease-control solutions help growers protect crops from yield-damaging diseases such as ascochyta, root rot, and seed-borne infections. Innovations like multi-active seed treatments can improve crop establishment, reduce disease pressure, and enhance harvest quality. In December 2025, Bayer Crop Science Canada introduced EverGol Rise, a new pulse seed treatment designed to improve disease protection for Canadian growers. The product combines four active ingredients to deliver stronger control against difficult pathogens such as ascochyta, while also improving ease of application. This can increase farmer confidence in pulse acreage, improve export reliability, and strengthen Canada’s competitiveness in global pulse markets.

Market Challenges

- Currency Exchange-Rate Fluctuations: Currency exchange-rate fluctuations are challenging as exports are often priced in US dollars, while farmers and processors bear many costs in Canadian dollars. A stronger Canadian dollar can reduce export competitiveness and lower returns for suppliers in price-sensitive markets. Meanwhile, currency volatility affects contract pricing, buyer affordability, and profit margins across the supply chain. It also adds uncertainty for exporters dealing with major import markets such as India, China, Bangladesh, and the Middle East.

- Freight and Logistics Bottlenecks: Freight and logistics bottlenecks are challenging as pulses grown in Prairie Provinces rely heavily on rail networks and ports for export movement. Delays in rail transport, container shortages, port congestion, or high shipping costs can disrupt delivery schedules and weaken buyer confidence. Since Canada exports a large share of its pulse output, logistics issues directly affect export margins and contract reliability. These bottlenecks can also reduce price competitiveness against suppliers located closer to key import markets.

Emerging Market Trends

1. Yellow Pea Protein for Plant-Based Food Ingredient

Yellow pea protein is emerging as food manufacturers increasingly use it in plant-based meat, dairy alternatives, protein bars, beverages, and nutritional products. Yellow peas offer high protein content, neutral taste, good functionality, and lower allergen concerns compared with soy. Canada’s strong dry pea production base provides a reliable raw material supply for pea protein concentrates and isolates. This trend is encouraging investment in pulse fractionation, value-added ingredient manufacturing, and export-oriented plant protein supply chains.

2. Chickpea Protein and Hummus Mainstream Demand

Chickpea protein and mainstream hummus demand are emerging as consumers increasingly adopt protein-rich, plant-based, and Mediterranean-style foods. Chickpeas are widely used in hummus, dips, snacks, salads, ready meals, and gluten-free flours, supporting stronger demand from food processors and retailers. Their clean-label profile, high fiber content, and suitability for vegan and flexitarian diets make them attractive for value-added product innovation. This trend creates opportunities for Canadian growers and processors to expand chickpea-based ingredients, branded foods, and export-ready processed products.

3. Precision Agriculture and Pulse Yield Optimization

Precision agriculture and pulse yield optimization are emerging as growers increasingly use GPS mapping, soil sensors, satellite imagery, drones, and variable-rate input application. These tools help farmers monitor soil moisture, detect crop stress, manage disease risk, and apply fertilizers or crop protection products more efficiently. In drought-prone Prairie regions, precision farming supports better water and input management, improving yield stability. This trend also helps reduce production costs, enhance crop quality, and strengthen Canada’s competitiveness in global pulse exports.

4. Lentil Pasta and Pulse Snack Innovations

Lentil pasta and pulse snack innovations are emerging as consumers shift toward healthier, gluten-free, high-protein, and fiber-rich food options. In July 2025, Italian pasta producer Andriani introduced its Felicia healthy pasta brand in Canada, targeting consumers who prefer clean-label foods, simple ingredients, and nutrient-rich superfoods. The Felicia range includes popular pasta formats such as penne and spaghetti, made from ingredients like organic buckwheat, brown rice, oats, chickpeas, lentils, peas, and beans. Lentils are increasingly used in pasta, chips, crackers, extruded snacks, soups, and ready-to-cook meals due to their strong nutritional profile and clean-label appeal. This trend supports value-added processing of Canadian lentils beyond bulk exports. It also creates opportunities for food manufacturers to develop premium, plant-based products for health-conscious, vegan, and flexitarian consumers.

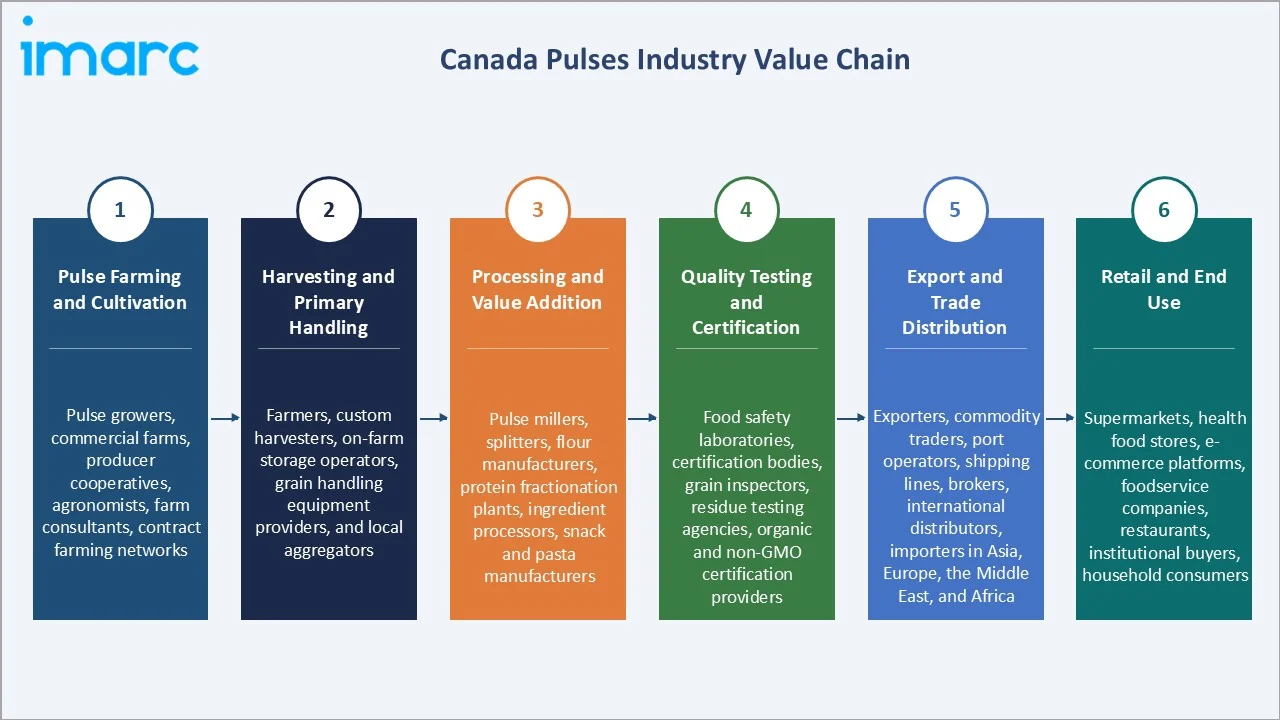

Industry Value Chain Analysis

Canada pulse value chain integrates pulse farming and cultivation, harvesting and primary handling, processing and value addition, quality testing and certification, export and trade distribution, and retail and end use.

|

Stage |

Key Participants |

|

Pulse Farming and Cultivation |

Pulse growers, commercial farms, producer cooperatives, agronomists, farm consultants, contract farming networks |

|

Harvesting and Primary Handling |

Farmers, custom harvesters, on-farm storage operators, grain handling equipment providers, and local aggregators |

|

Processing and Value Addition |

Pulse millers, splitters, flour manufacturers, protein fractionation plants, ingredient processors, snack and pasta manufacturers |

|

Quality Testing and Certification |

Food safety laboratories, certification bodies, grain inspectors, residue testing agencies, organic and non-GMO certification providers |

|

Export and Trade Distribution |

Exporters, commodity traders, port operators, shipping lines, brokers, international distributors, importers in Asia, Europe, the Middle East, and Africa |

|

Retail and End Use |

Supermarkets, health food stores, e-commerce platforms, foodservice companies, restaurants, institutional buyers, household consumers |

The processing and value addition stage is the most value-added segment of the Canada pulses value chain. At this stage, raw pulses are transformed into higher-value products such as pulse flours, protein concentrates, protein isolates, starches, snacks, pasta, and plant-based food ingredients. Value addition significantly increases profit margins compared with exporting unprocessed pulses and enables manufacturers to serve fast-growing markets for plant-based foods, functional ingredients, and specialty nutrition products.

Technology Landscape in the Canada Pulses Industry

Processing and Fractionation Technology

Processing and fractionation technology enable the conversion of raw pulses into high-value ingredients such as protein concentrates, protein isolates, starches, and fiber fractions. Advanced dry and wet fractionation technologies improve protein extraction efficiency while preserving nutritional quality and functionality. These technologies support the growing demand for plant-based foods, nutritional supplements, and functional food ingredients. As investment in pulse processing facilities expands across Canada, fractionation is helping the industry move beyond commodity exports toward higher-margin, value-added products.

Advanced Seed Treatment Technologies

Advanced seed treatment technologies improve early-stage crop protection against seed-borne and soil-borne diseases. Multi-active formulations help control pathogens such as ascochyta and root rot, supporting stronger germination, healthier crop establishment, and better yield stability. These technologies also improve operational efficiency through all-in-one treatments that reduce application complexity for growers. As disease pressure and climate variability increase, seed treatment innovation is becoming essential for protecting pulse productivity and export-quality output.

Optical Sorting and Machine Vision Technologies

Optical sorting and machine vision technologies are improving the accuracy and speed of cleaning, grading, and quality assessment processes. Advanced cameras, sensors, and AI-powered vision systems can identify and remove defective, discolored, damaged, or foreign materials with high precision. These technologies help processors meet stringent export and food safety standards while reducing manual labor requirements. As demand for premium-quality pulses and value-added ingredients grows, optical sorting is becoming a critical tool for enhancing efficiency, product consistency, and global market competitiveness.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Dry Peas |

33.0% |

2025 |

|

Domestic Consumption and Exports |

Exports |

72.0% |

2025 |

|

End-Use |

Retail Store |

🔒 |

2025 |

|

Region |

Saskatchewan |

48.0% |

2025 |

By Type

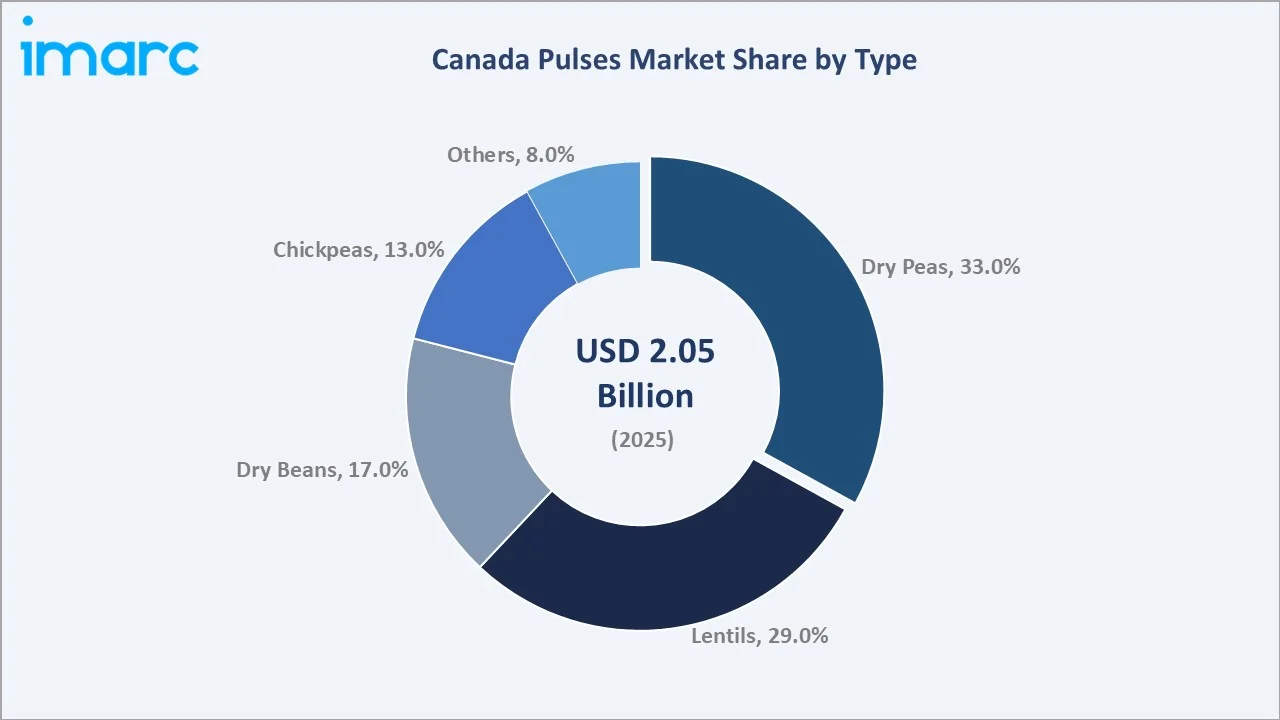

Dry peas lead at 33.0% (2025), due to their large cultivation base, strong export demand, and wide use in food, feed, starch, and plant protein applications. Their cost competitiveness and suitability for pea protein extraction further strengthen their dominant position.

To access detailed market analysis, Request Sample

Lentils at 29.0% reflect Canada's lentil export leadership through red, green, and black lentils. Dry beans at 17.0% reflect Manitoba navy, black, and kidney beans for North American food manufacturing. Chickpeas at 13.0% grow fastest at ~4.3% CAGR through hummus, chickpea protein, and South Asian cooking demand. Others at 8.0% include faba beans, soybeans, and specialty pulses.

By Domestic Consumption and Exports

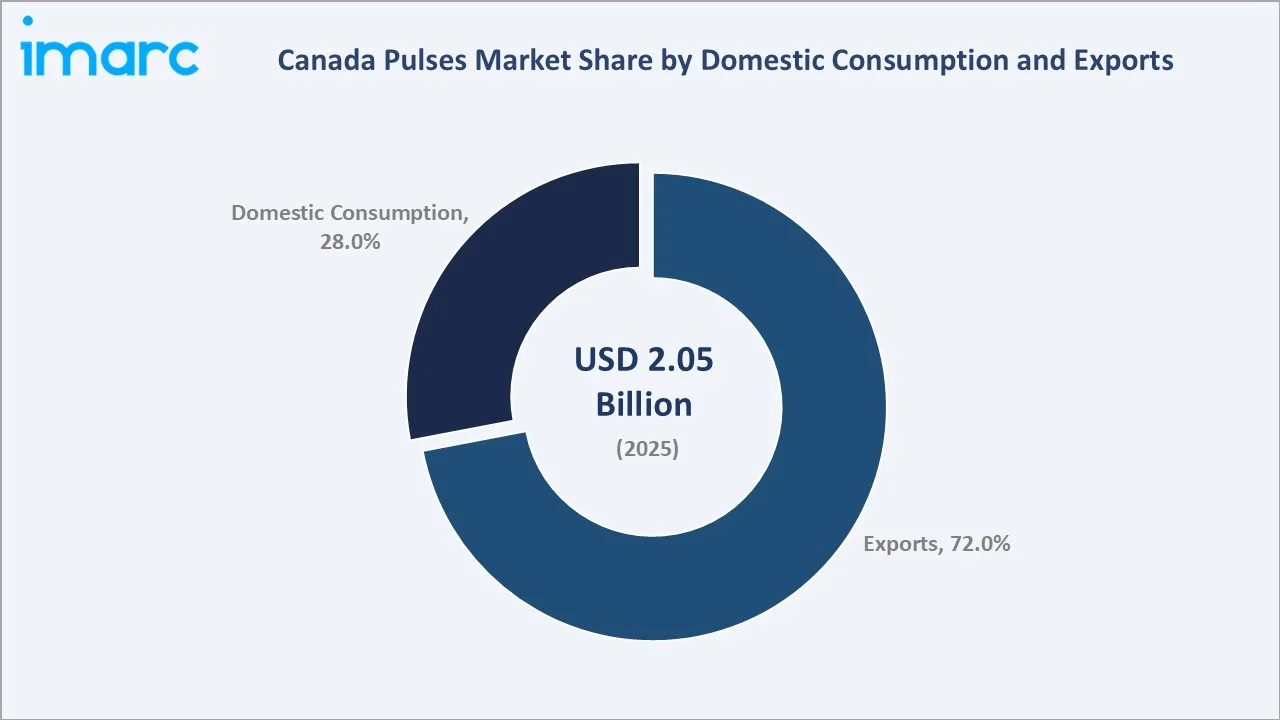

Exports lead at 72.0% (2025), as a major share of domestic production is shipped to international buyers across Asia, South Asia, the Middle East, Africa, and Europe. Canada’s strong production base, quality standards, and established grain-handling infrastructure support its export-led market position.

Domestic consumption at 28.0% reflects Canadian food manufacturing, grocery retail, food service, and pet food use. Domestic consumption grows at ~3.6% CAGR through expanding plant-based food manufacturing, clean-label grocery consumer, and pulse-based food innovation.

Regional Market Insights

|

Region |

Share (2025) |

Key Canada Pulses Market Drivers & Characteristics |

|

Saskatchewan |

48.0% |

Reflecting its vast arable land, favorable growing conditions, and concentration of lentil and dry pea cultivation. |

|

Alberta |

22.0% |

Reflects strong production of dry peas, chickpeas, and faba beans, supported by expanding pulse acreage, modern farming practices, and access to major grain-handling infrastructure. |

|

Manitoba |

15.0% |

Driven by diversified pulse cultivation, including peas and edible beans, supported by crop rotation benefits and growing domestic processing activities. |

|

Ontario |

9.0% |

Reflects its focus on edible beans and specialty pulse crops, supported by proximity to food processors, consumer markets, and export channels into the United States. |

|

Others |

6.0% |

Other provinces, including British Columbia, Quebec, and Atlantic Canada, contribute through niche pulse production, specialty crops, regional food processing, and growing interest in sustainable agriculture. |

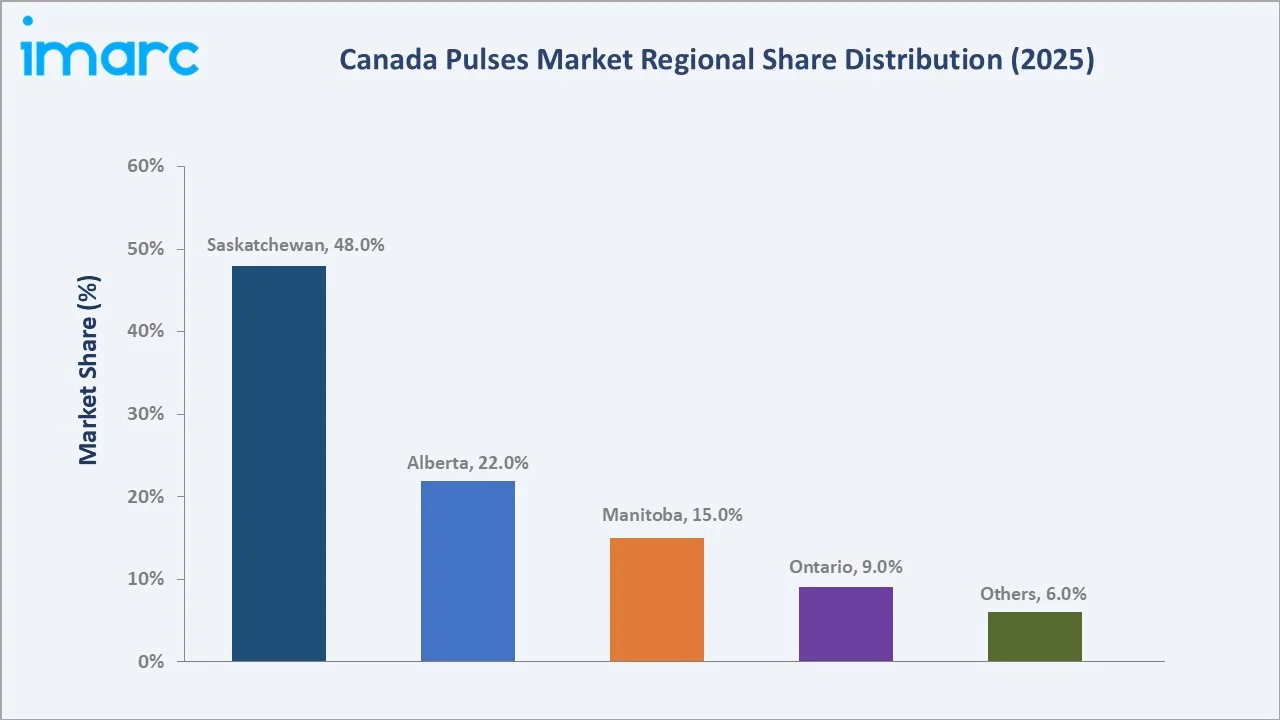

Saskatchewan's 48.0% dominance is supported by its large prairie farmland, favorable growing conditions, and strong concentration of lentil and dry pea production. Alberta's 22.0% driven by dry peas, chickpeas, and faba beans, along with modern farming systems and export logistics.

Manitoba's 15.0% contributes through diversified pulse cultivation and crop rotation practices. Ontario's 9.0% is more focused on edible beans and specialty pulses. Other provinces, at 6.0%, have smaller shares but support niche production and regional processing.

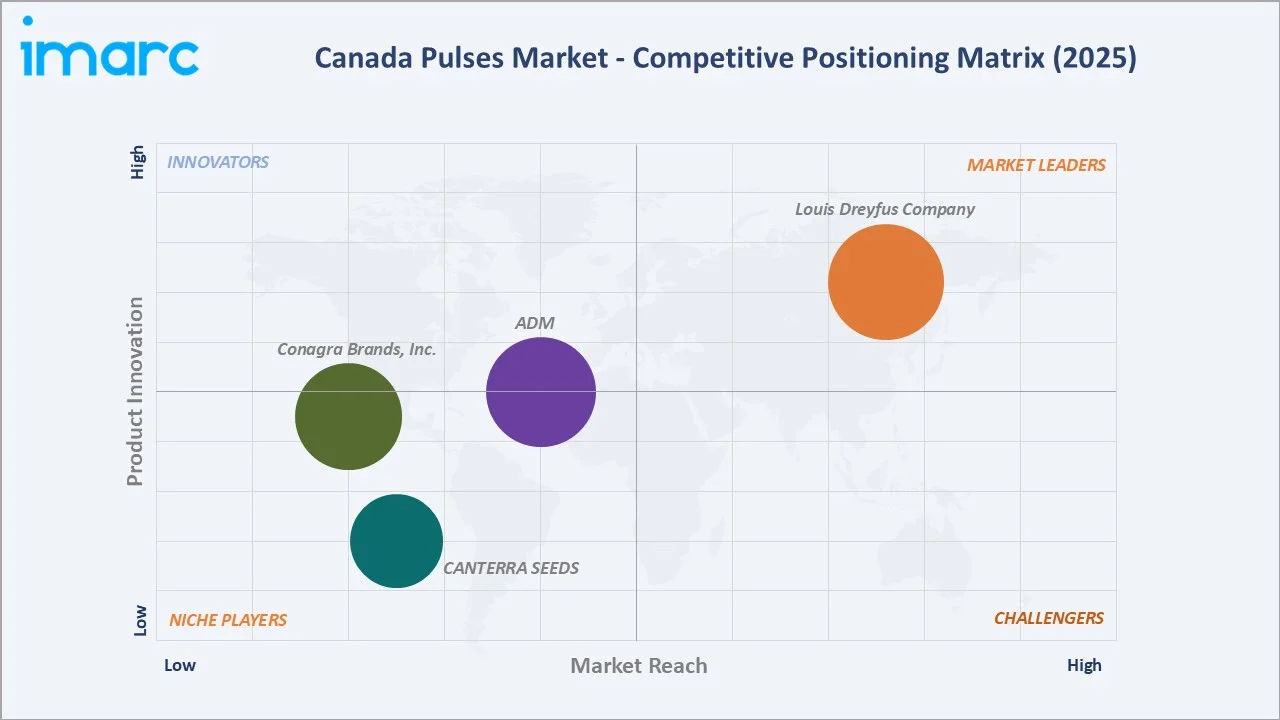

Competitive Landscape

The Canada pulses market is moderately concentrated, with a mix of large grain handling companies, pulse processors, exporters, and ingredient manufacturers competing across domestic and international markets. Competition is driven by sourcing capabilities, processing scale, export networks, product quality, and value-added ingredient offerings. Leading players are investing in pulse fractionation facilities, protein extraction technologies, and sustainable supply chains to capitalize on growing demand for plant-based foods.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Louis Dreyfus Company |

Black Matpe, Chickpeas, Faba Beans, Lupins, Pigeon Peas, Red Lentils, Yellow Peas |

Market Leader |

The Louis Dreyfus Company acts as a major merchant linking Canadian pulse production hubs to international consumer markets. By leveraging its origination strengths, the company sources crops like red lentils, yellow peas, chickpeas, and faba beans from Canada to distribute to high-demand regions. |

|

ADM |

Chickpeas, Green lentil, Green peas, Red lentil, Little red bean, Yellow peas |

Established Player |

ADM operates as a critical link in the Canadian pulse supply chain, connecting local growers to domestic and global markets. The company acquires, processes, and distributes pulses like lentils, chickpeas, and peas to meet the surging worldwide demand for plant-based human and animal nutrition. |

|

Conagra Brands, Inc. |

Ranch Style Beans |

Established Player |

Conagra Brands, Inc. operates in Canada as a major manufacturer and distributor of branded consumer food and foodservice ingredients. The company incorporates agricultural pulse ingredients into its shelf-stable and frozen food portfolios. |

|

CANTERRA SEEDS |

Edible Beans, Yellow Peas, Lentils, Clearfield-Lentils |

Niche Player |

CANTERRA SEEDS operates as a leading Canadian, farmer-owned seed company that plays a foundational role in Western Canadian agriculture. |

Strategic partnerships with growers, food manufacturers, and global distributors are strengthening market positions. Companies are also focusing on traceability, food safety certifications, and innovation in pulse-based ingredients to differentiate themselves in both commodity and specialty segments.

Key Company Profiles

Louis Dreyfus Company

Louis Dreyfus Company is a leading merchant and processor of agricultural commodities with a significant presence in Canada's grain and pulse value chain. The company sources, handles, stores, processes, and exports a wide range of pulse crops, including peas, lentils, chickpeas, and beans, through its integrated origination and logistics network.

- Key Products: Black Matpe, Chickpeas, Faba Beans, Lupins, Pigeon Peas, Red Lentils, Yellow Peas.

- Strategic Focus: Strengthening pulse origination networks across key producing provinces, particularly Saskatchewan and Alberta, to secure a reliable supply of peas, lentils, chickpeas, and beans.

ADM

ADM is an agricultural processing, merchandising, and food ingredient company with a strong presence across grain and oilseed supply chains, including the Canadian pulses sector. The company participates in pulse sourcing, storage, transportation, processing, and export activities through its extensive origination and logistics network. ADM leverages Canada's large production of peas, lentils, chickpeas, and beans to supply both domestic processors and international customers.

- Key Products: Chickpeas, Green lentil, Green peas, Red lentil, Little red bean, Yellow peas.

- Strategic Focus: Expanding its plant-based nutrition portfolio by increasing the use of Canadian peas, lentils, and other pulses in protein concentrates, isolates, fibers, and specialty food ingredients.

Market Concentration Analysis

The Canada pulses market is moderately concentrated, with large global grain traders and agri-processors competing alongside regional pulse processors, exporters, and cooperatives. Major players hold strong positions through origination networks, storage assets, processing capacity, and export channels. However, the market also includes many mid-sized and local handlers, keeping competition active at the grower and processor level. Concentration is higher in export trading and bulk handling, while value-added pulse processing remains more fragmented. Competitive advantage is shaped by supply security, logistics efficiency, quality certification, and investment in pulse protein and fractionation technologies.

Investment & Growth Opportunities

Highest Growth Segments

Chickpeas (~4.3% CAGR), lentils (~4.1% CAGR), pea protein isolate value-added (~8-10% CAGR from smaller base), chickpea protein and pasta (~7-9% CAGR), exports to EU plant-based (~5-6% CAGR through pea protein), and domestic plant-based food manufacturing represent Canada pulse highest-growth investment vectors through 2034.

Investment Themes

- Pulse protein fractionation and ingredient: Investment in pulse protein fractionation facilities offers significant growth potential as demand for plant-based proteins, functional ingredients, and clean-label foods continues to rise. Canada's abundant supply of peas and lentils provides a strong feedstock base for producing high-value protein isolates, concentrates, starches, and fibers, enabling a shift from commodity exports to value-added processing.

- Precision agriculture and climate resilience for pulse yield optimization: Investments in precision agriculture technologies such as drones, satellite monitoring, soil analytics, and variable-rate application systems can improve pulse yields while reducing input costs. Climate-resilient farming solutions help growers manage drought, disease, and weather variability, supporting stable production and strengthening Canada's long-term competitiveness in global pulse markets.

Future Market Outlook (2026-2034)

Canada's Pulses market is projected to grow from USD 2.05 Billion in 2025 to USD 2.89 Billion by 2034, delivering a 3.75% CAGR over the forecast period through structural export demand from India and South Asia, global plant protein movement driving pea and chickpea protein ingredient, domestic plant-based food manufacturing expansion, and precision agriculture yield improvement. The market's anchor value of USD 2.47 Billion in 2030 represents Canada's pulse market at a value-added inflection.

Three structural forces define Canada pulse market growth through 2034. First, rising demand for plant-based proteins and functional food ingredients is increasing the use of peas, lentils, and chickpeas in food processing and nutrition products. Second, Canada's strong export position and growing demand from South Asia, the Middle East, and other international markets continue to support production expansion. Third, investments in pulse fractionation, precision agriculture, improved seed technologies, and climate-resilient farming practices are enhancing productivity while enabling greater value addition across the supply chain.

Research Methodology

Primary Research

Primary research comprised interviews and discussions with pulse growers, grain handlers, exporters, processors, ingredient manufacturers, industry associations, and agricultural experts across Canada. These interactions were conducted to validate market size estimates, production trends, export dynamics, technology adoption, and future growth opportunities within the pulses industry.

Secondary Research

Secondary research encompassed company reports, government agriculture databases, trade statistics, industry publications, association reports, and credible news sources. These sources were used to assess production patterns, export demand, competitive landscape, technology trends, and policy developments in the Canada pulses market.

Forecasting Models

Forecasting models utilized a combination of time-series analysis, production and export trend assessment, consumption modeling, and macroeconomic indicator evaluation to project market growth. The forecasts incorporated factors such as plant-based protein demand, pulse acreage trends, international trade flows, technological advancements, and evolving consumer preferences across key end-use sectors.

Canada Pulses Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons, Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Lentils, Dry Beans, Dry Peas, Chick Peas, Others |

| Domestic Consumption and Exports Covered | Domestic Consumption, Exports |

| End-Uses Covered | Retail Store, Snack Food Industry, Flour Industry, Others |

| Regions Covered | Saskatchewan, Alberta, Manitoba, Ontario, Others |

| Companies Covered | Louis Dreyfus Company, ADM, Conagra Brands, Inc., CANTERRA SEEDS,etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Canada Pulses Market Report

The Canada pulses market reached USD 2.05 Billion in 2025, driven by rising global demand for plant-based proteins, clean-label foods, and sustainable crop ingredients. Strong export demand from South Asia, the Middle East, Africa, and Europe continues to support large-scale production of peas, lentils, chickpeas, and beans.

The Canada pulses market grows at 3.75% CAGR during 2026-2034, reaching USD 2.89 Billion by 2034. The CAGR reflects India and South Asia export demand, global plant protein movement, domestic plant-based food manufacturing, and precision agriculture yield improvement.

Dry peas lead at 33.0% due to their wide cultivation base, strong export demand, and use in food, feed, starch, and pea protein applications. Their cost competitiveness and suitability for plant-based ingredients further support dominance.

Exports lead at 72.0% as a large share of production is shipped to global markets. Strong demand from Asia, South Asia, the Middle East, Africa, and Europe supports Canada’s export-driven market position.

Saskatchewan leads at 48.0% due to its vast prairie farmland, favorable climate, and strong concentration of lentil and dry pea cultivation. Established grain-handling infrastructure and export connectivity further support its dominant position.

Leading companies include Louis Dreyfus Company, ADM, Conagra Brands, Inc., and CANTERRA SEEDS, among others.

The market is projected to reach approximately USD 2.47 Billion by 2030, supported by strong export demand and rising use of pulses in plant-based food ingredients. Growth will also be driven by value-added processing, pulse protein innovation, and Canada’s established production base.

Three priority investment opportunities in the Canada pulses market include pulse protein fractionation and ingredient manufacturing, precision agriculture and climate-resilient farming technologies, and value-added pulse-based food products such as snacks, pasta, and ready meals. Growing global demand for plant-based proteins is encouraging investment in processing facilities, while digital farming solutions are improving productivity and sustainability. At the same time, innovation in consumer-facing pulse foods is creating higher-margin opportunities beyond traditional commodity exports.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)