GCC Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Country, 2026-2034

GCC Logistics Market Size, Share, Trends & Forecast (2026-2034)

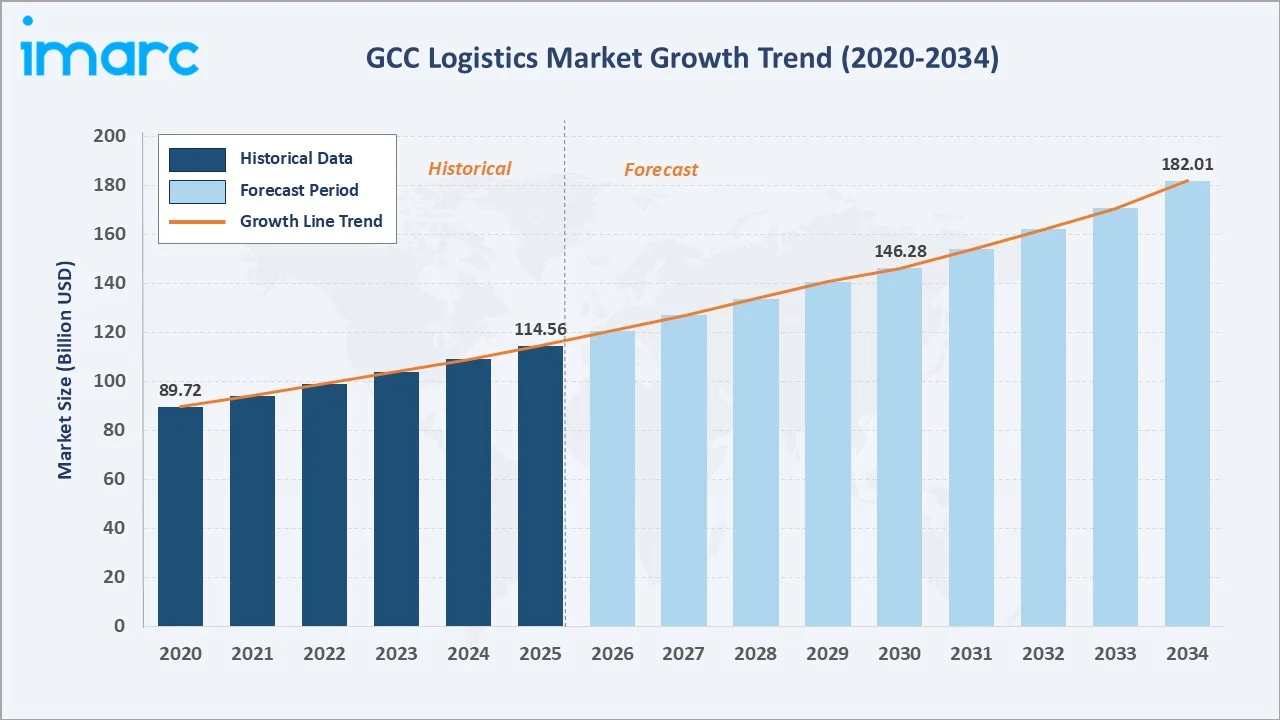

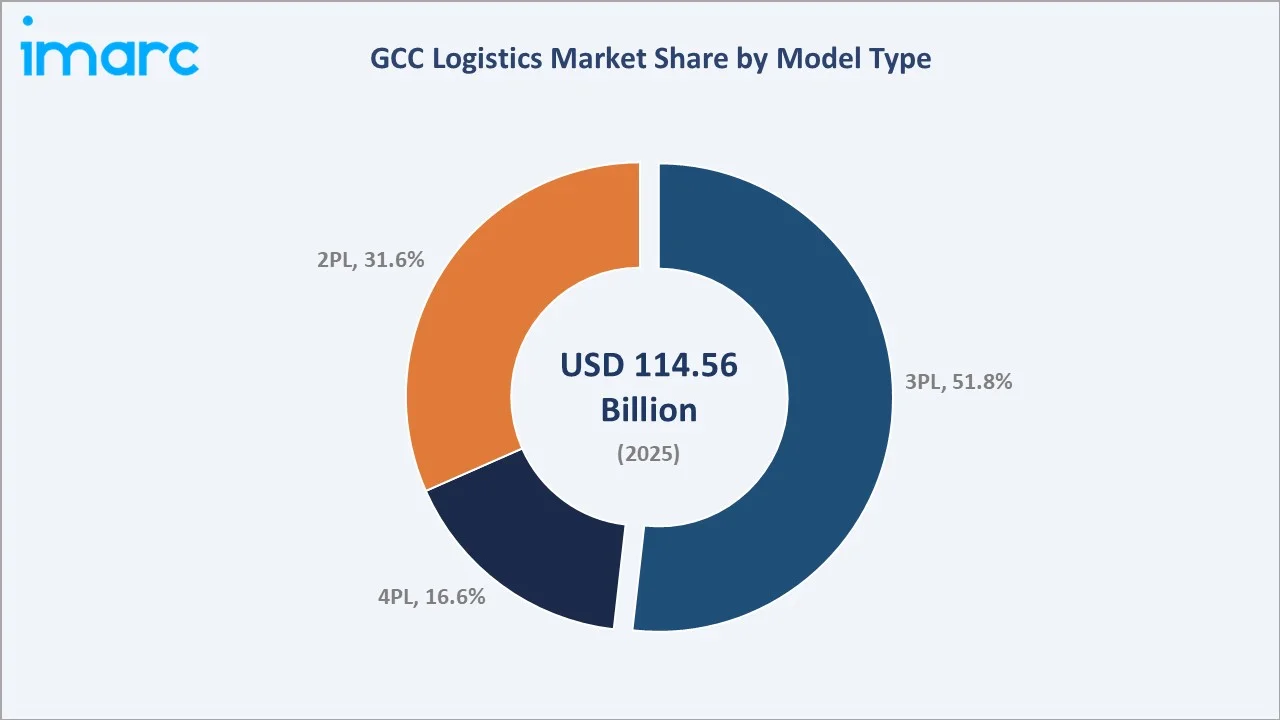

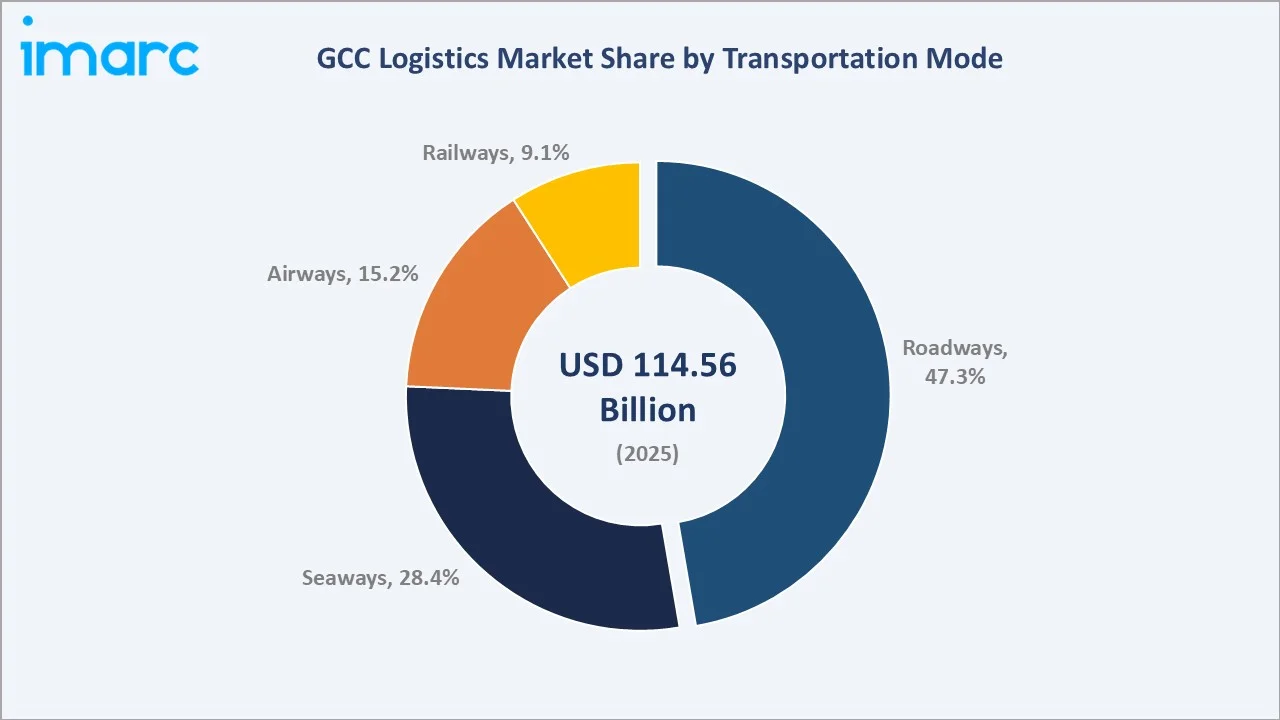

The GCC logistics market reached USD 114.56 Billion in 2025 and is projected to reach USD 182.01 Billion by 2034, growing at a CAGR of 5.01% during 2026-2034. The market is driven by rising investments in transport infrastructure, expanding e-commerce, and increasing regional trade supported by economic diversification initiatives and strategic government policies. The GCC represents more than 60% of total port-related spending in the Middle East, supported by the development of large-scale new ports and the expansion of existing facilities. These modern ports, equipped with advanced automation and capacity to handle ultra-large container vessels, are strengthening trade connectivity, improving cargo handling efficiency, reducing turnaround times, and driving growth in the GCC logistics market. 3PL leads the model type at 51.8%. Roadways lead transportation mode at 47.3%. Saudi Arabia leads regionally at 39.5%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 114.56 Billion |

|

Forecast Market Size (2034) |

USD 182.01 Billion |

|

CAGR (2026-2034) |

5.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Model Type |

3PL (51.8%, 2025) |

|

Dominant Transportation Mode |

Roadways (47.3%, 2025) |

|

Leading Country |

Saudi Arabia (39.5%, 2025) |

The GCC logistics market has expanded steadily, rising from USD 89.72 Billion in 2020 to USD 114.56 Billion in 2025, driven by increasing trade flows, port expansion, and infrastructure modernization. Growth is being supported by strong investments in roads, railways, airports, free zones, and digital supply chain systems. The market is expected to reach USD 146.28 Billion by 2030, reflecting higher demand for freight forwarding, warehousing, cold chain, and e-commerce logistics. By 2034, it is forecast to reach USD 182.01 Billion, supported by the GCC’s strategic role as a global transshipment and trade hub. Government diversification programs, rising non-oil trade, and improved regional connectivity will continue to strengthen market growth.

To get more information on this market, Request Sample

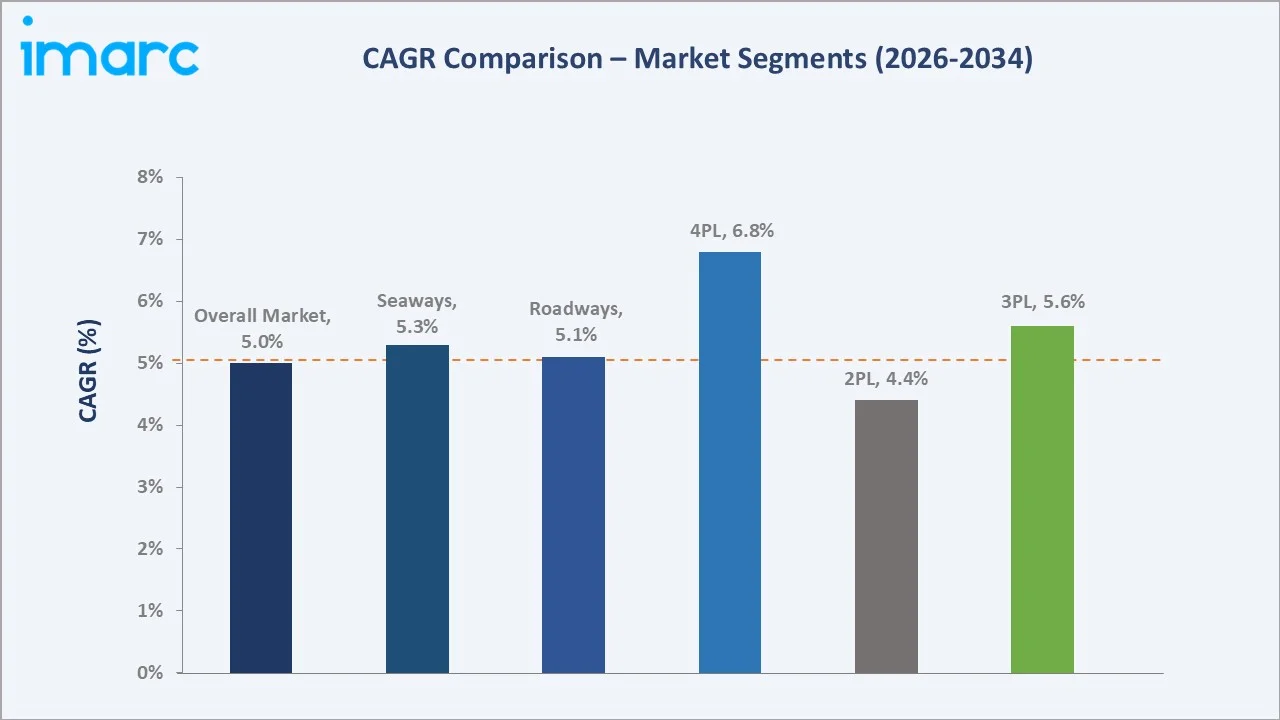

4PL grows fastest at ~6.8% CAGR through Vision 2030 mega-project supply chain orchestration. Airways grow at ~6.2% CAGR through e-commerce express freight and Emirates SkyCargo expansion. Railways grow at ~5.8% CAGR through GCC rail network development and the Saudi Landbridge.

Executive Summary

The GCC logistics market is evolving into a highly integrated trade and supply chain ecosystem, supported by strong infrastructure investments and economic diversification agendas. Rising non-oil trade, expanding industrial zones, and growing e-commerce activity are increasing demand for warehousing, freight forwarding, and last-mile delivery services. Modern ports, airports, rail networks, and cross-border corridors are improving cargo movement and regional connectivity. Digital logistics platforms, automation, and smart warehousing are helping operators enhance efficiency and reduce turnaround times. The market is also benefiting from the GCC’s strategic position between Asia, Europe, and Africa. 3PL at 51.8% leads through integrated outsourced logistics. Roadways at 47.3% lead through the GCC truck network. Saudi Arabia leads regionally at 39.5%.

Key Market Insights

|

Insight |

Data |

|

Dominant Model Type |

3PL - 51.8% share (2025) |

|

Dominant Transportation Mode |

Roadways - 47.3% market share (2025) |

|

Leading Country |

Saudi Arabia - 39.5% share (2025) |

|

Market Opportunity |

GCC railway network; e-commerce last-mile; cold chain pharmaceutical; green hydrogen logistics; digital trade platform |

Key Analytical Observations Supporting The Above Data:

- 3PL at 51.8%: 3PL leads due to rising demand for outsourced transportation, warehousing, inventory management, and value-added supply chain services across retail, manufacturing, healthcare, and e-commerce sectors.

- Roadways at 47.3%: Roadways lead due to their strong regional connectivity, flexible door-to-door delivery capability, and extensive use in domestic freight movement. They remain essential for linking ports, airports, warehouses, industrial zones, retail networks, and last-mile distribution channels across GCC countries.

- Saudi Arabia at 39.5%: Saudi Arabia leads regionally due to its large consumer base, expanding industrial sector, and major investments in ports, airports, roads, railways, and logistics zones.

GCC Logistics Market Overview

The GCC logistics market encompasses transportation, warehousing, freight forwarding, 3PL, cold chain, last-mile delivery, and value-added supply chain services across key sectors such as retail, manufacturing, oil and gas, healthcare, food and beverage, and e-commerce. It includes road, sea, air, and rail logistics supported by ports, airports, free zones, industrial cities, and digital logistics platforms. The market plays a critical role in enabling regional trade, import-export movement, and cross-border supply chain connectivity. Its scope is expanding with rising investments in automation, smart warehousing, multimodal transport, and integrated logistics solutions. Key macroeconomic factors include sustained economic diversification, rising non-oil trade, and increasing government expenditure on transport and logistics infrastructure. Growing manufacturing output, expanding e-commerce, favorable foreign investment policies, and the GCC's strategic location along global trade routes further support long-term market growth.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Expansion of Ports, Airports, Railways, and Multimodal Transport Infrastructure: The expansion of ports, airports, railways, and multimodal transport infrastructure is significantly enhancing the efficiency and capacity of the GCC logistics sector. Saudi Arabia’s logistics infrastructure is expanding rapidly, with airports handling around 140.9 million passengers in 2025, including 76 million international and 65 million domestic travelers, while air cargo reached nearly 1.18 million tons. Rail freight also shows strong activity, with 6,807 SAR freight trips and over 15.6 million tons of goods transported in 2024. Meanwhile, Mawani-managed ports handled 8,317,235 TEUs in 2025, marking a 10.58% increase from 2024. As a result, businesses benefit from faster distribution, greater operational efficiency, and improved access to regional and international markets, driving sustained growth in the GCC logistics market.

- E-commerce and Last-Mile Delivery Growth: E-commerce and last-mile delivery growth are increasing demand for faster, more flexible, and technology-enabled delivery services. Rising online shopping, quick-commerce platforms, and omnichannel retail are boosting the need for urban warehousing, fulfillment centers, and same-day delivery networks. Logistics providers are expanding route optimization, real-time tracking, and automated sorting capabilities to handle higher parcel volumes efficiently. This is strengthening 3PL, warehousing, courier, express, and last-mile logistics services across the region.

- Oil and Gas Energy Export Logistics: Oil and gas energy export logistics supporting large-scale movement of crude oil, refined products, LNG, petrochemicals, and related industrial cargo. Strong export activity creates continuous demand for specialized storage, tanker transport, port handling, pipeline-linked terminals, and freight forwarding services. The presence of major energy hubs also strengthens demand for project logistics, heavy equipment movement, and supply chain support for upstream and downstream operations. This keeps logistics networks active and supports growth in bulk, liquid cargo, and industrial logistics services across the region.

Market Restraints

- High Operating and Transportation Costs: High operating and transportation costs increase expenses for fuel, fleet maintenance, labor, warehousing, and technology adoption. These rising costs reduce profit margins for logistics providers and make services more expensive for end users. Long-distance freight movement, cross-border compliance, and specialized cold chain or bulk cargo handling further add to cost pressure. As a result, smaller operators may struggle to scale, while businesses face challenges in maintaining cost-efficient supply chains.

- Congestion at Major Logistics Hubs: Congestion at major logistics hubs is slowing cargo movement across busy ports, airports, border checkpoints, and urban distribution centers. High freight volumes can lead to longer dwell times, delayed customs clearance, and increased vehicle turnaround time. This raises storage, demurrage, fuel, and labor costs for logistics providers. As a result, supply chain reliability is affected, especially for time-sensitive cargo such as e-commerce parcels, food products, pharmaceuticals, and industrial inputs.

Market Opportunities

- AI, IoT, Robotics, and Autonomous Warehouse Solutions: AI, IoT, robotics, and autonomous warehouse solutions improve operational efficiency, inventory accuracy, and order fulfillment speed. In January 2025, Aramex introduced an advanced automated robotic system at Jeddah Islamic Port. Its automated sorting system includes three feeding lines connected to 120 robotic guided vehicles, enabling the processing of around 4,000 shipments per hour and 96,000 shipments per day. This creates new growth opportunities for technology providers and logistics operators across the GCC.

- Sustainable Logistics and Electric Commercial Vehicle Adoption: Sustainable logistics and the adoption of electric commercial vehicles present a major opportunity as governments and businesses work toward reducing carbon emissions and improving energy efficiency. Logistics companies are increasingly investing in electric delivery fleets, energy-efficient warehouses, and green transportation solutions to meet sustainability targets and lower operating costs. Growing investments in EV charging infrastructure and renewable energy further support this transition. These initiatives are expected to enhance long-term operational efficiency while creating new opportunities in green logistics services and sustainable supply chain management.

Market Challenges

- Managing Last-Mile Delivery Efficiency in Rapidly Growing Urban Centers: Managing last-mile delivery efficiency is challenging due to rapid urbanization, rising parcel volumes, traffic congestion, and growing customer expectations for same-day or next-day delivery. Dense city centers and expanding suburban areas make route planning, fleet utilization, and delivery scheduling more complex. High fuel, labor, and vehicle maintenance costs further pressure delivery margins. As a result, logistics providers must invest in route optimization, micro-fulfillment hubs, and real-time tracking to maintain service quality and cost efficiency.

- Geopolitical Tensions Affecting Regional Trade Routes: Geopolitical tensions affecting regional trade routes are increasing uncertainty around shipping lanes, border movements, and cross-border cargo flows. Disruptions in key maritime corridors can lead to rerouting, longer transit times, higher freight rates, and increased insurance costs. These risks affect supply chain reliability for import-dependent sectors such as retail, manufacturing, food, healthcare, and energy. As a result, logistics providers must build more resilient networks, diversify routes, and maintain contingency capacity to manage potential disruptions.

Emerging Market Trends

1. Smart Port and Digital Trade Platforms

Smart ports and digital trade platforms are emerging as port operators increasingly adopt AI, IoT, automation, and blockchain technologies to streamline cargo handling and trade documentation. These digital solutions improve vessel turnaround times, enhance real-time cargo visibility, and reduce customs clearance delays. Integrated digital platforms also facilitate seamless coordination among shipping lines, customs authorities, freight forwarders, and logistics providers. This trend is enhancing operational efficiency, lowering logistics costs, and strengthening the GCC's position as a global trade and transshipment hub.

2. Drone and Last-Mile Innovations

Drone and last-mile innovation is emerging as companies explore faster, technology-enabled delivery models for urban and remote locations. This trend is especially important for e-commerce, healthcare, food delivery, and time-sensitive shipments. In May 2026, Saudi Arabia’s General Authority of Civil Aviation (GACA) granted its first operational permit for limited drone delivery of medicines and medical logistics across the holy sites in Makkah during the 1447 AH Hajj season. The permit, awarded to Terra Drone Arabia, supports the use of advanced technologies to improve healthcare access and services for pilgrims. As customer expectations for same-day and on-demand delivery rise, logistics providers are investing in advanced last-mile solutions to improve efficiency and reduce delivery costs.

3. Green Logistics and Electric Fleet

Green logistics and electric fleets are emerging as companies prioritize lower carbon emissions and more sustainable supply chain operations. Logistics providers are adopting electric delivery vehicles, energy-efficient warehouses, and renewable energy solutions to reduce fuel consumption and operating costs. Governments are also supporting this transition through sustainability initiatives and investments in EV charging infrastructure. These developments are accelerating the shift toward environmentally responsible logistics while improving long-term operational efficiency.

4. Cold Chain and Pharmaceutical Logistics Growth

Cold chain and pharmaceutical logistics growth is emerging due to rising demand for temperature-controlled storage and transport of vaccines, biologics, medicines, fresh food, and specialty chemicals. Expanding healthcare investments, food imports, and pharmaceutical distribution networks are increasing the need for refrigerated warehouses, insulated vehicles, and real-time temperature monitoring. Logistics providers are upgrading cold chain infrastructure to ensure product safety, regulatory compliance, and faster delivery. This trend is creating strong growth opportunities in specialized warehousing, pharma logistics, and high-value cargo handling across the GCC.

Industry Value Chain Analysis

The GCC logistics value chain integrates infrastructure & asset development, transportation & freight services, warehousing & distribution, 3PL & supply chain services, technology & digital solutions, and end-use industries.

|

Stage |

Key Participants |

|

Infrastructure & Asset Development |

Port authorities, airport operators, railway operators, road infrastructure agencies, free zone developers, logistics park developers |

|

Transportation & Freight Services |

Road freight operators, shipping lines, air cargo carriers, rail freight operators, multimodal transport providers |

|

Warehousing & Distribution |

Warehouse operators, cold storage providers, fulfillment centers, distribution centers, and inventory management companies |

|

3PL & Supply Chain Services |

3PL providers, freight forwarders, customs brokers, contract logistics companies, express and parcel delivery providers |

|

Technology & Digital Solutions |

Warehouse management system providers, transportation management system providers, IoT solution providers, AI and automation vendors, fleet management software providers |

|

End-Use Industries |

Retail & e-commerce, manufacturing, oil & gas, healthcare & pharmaceuticals, food & beverage, automotive, chemicals, construction, consumer goods |

3PL and supply chain services represent the most value-added stage in the GCC logistics value chain. This stage combines transportation, warehousing, inventory management, customs clearance, freight forwarding, fulfillment, and last-mile delivery into integrated solutions that improve supply chain efficiency and reduce operational costs. Increasing adoption of AI, automation, and real-time tracking further enhances service quality and operational visibility, making 3PL providers strategic partners for businesses across the GCC.

Technology Landscape in the GCC Logistics Industry

Digital Platform and TMS Technology

Digital platforms and transportation management system (TMS) technology enable end-to-end visibility, automated route planning, and real-time shipment tracking. Cloud-based TMS solutions optimize fleet utilization, reduce transportation costs, and improve delivery performance through AI-driven analytics and predictive planning. Integration with warehouse management systems, customs platforms, and ERP software streamlines documentation and enhances supply chain coordination. As a result, logistics providers are improving operational efficiency, customer experience, and data-driven decision-making across the region.

AI-based Quote Generation

AI-based quote generation automates freight pricing and quotation workflows. AI algorithms analyze shipment specifications, capacity, routes, market rates, and customer requirements in real time to generate accurate quotes within seconds. In June 2026, Saudia Cargo and cargo.one announced a partnership to introduce AI workers across Saudia Cargo’s commercial operations. Using cargo.one’s AI-native operating system, these AI workers manage RFQ requests and generate optimized quotes within seconds, 24/7. This enables customers to receive faster quotations while allowing sales teams to focus on complex shipments and higher-value customer support. As logistics providers increasingly digitize commercial operations, AI-powered quotation systems are becoming a key competitive differentiator in the GCC market.

Digital Twin Technology

Digital twin technology creates virtual replicas of warehouses, ports, fleets, and supply chain networks for real-time monitoring and simulation. These digital models enable logistics providers to optimize cargo flows, warehouse operations, and transport routes while predicting bottlenecks before they occur. By combining IoT sensors, AI, and real-time operational data, Digital Twins improve asset utilization, reduce downtime, and support predictive decision-making. As GCC countries invest in smart ports and logistics hubs, Digital Twin technology is becoming a key enabler of efficient, resilient, and data-driven logistics operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Model Type |

3 PL |

51.8% |

2025 |

|

Transportation Mode |

Roadways |

47.3% |

2025 |

|

End Use |

🔒 |

🔒 |

2025 |

|

Country |

Saudi Arabia |

39.5% |

2025 |

By Model Type

3PL leads at 51.8% (2025) through integrated outsourced logistics for GCC shippers across oil and gas, retail, pharma, and construction sectors.

To access detailed market analysis, Request Sample

2PL at 31.6% reflects asset-based GCC and international truck carriers, shipping lines, and airline cargo operators. 4PL at 16.6% grows fastest at ~6.8% CAGR through Vision 2030 mega-project supply chain orchestration, AI-driven TMS platforms, and end-to-end supply chain management outsourcing.

By Transportation Mode

Roadways lead at 47.3% (2025) through GCC-wide truck network, urban last-mile delivery, cross-border GCC trucking, and intra-city distribution.

Seaways at 28.4% supports large-scale movement of containers, bulk cargo, oil, LNG, petrochemicals, and re-export goods through major regional ports. Airways at 15.2% reflect Emirates SkyCargo, Saudi Cargo, and e-commerce express air freight growing. Railways at 9.1% reflect Saudi Landbridge and growing GCC rail freight corridor investment.

Regional Market Insights

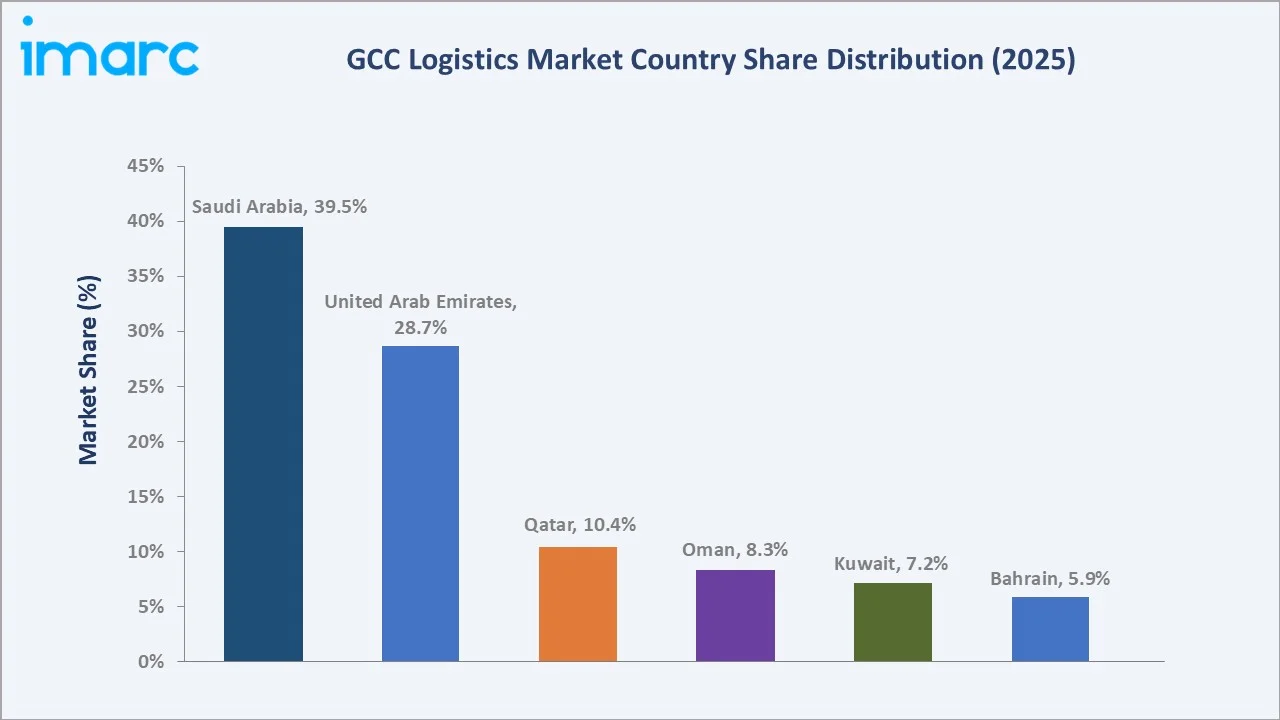

|

Country |

Share (2025) |

Key GCC Logistics Market Drivers & Characteristics |

|

Saudi Arabia |

39.5% |

Reflecting its large domestic economy, strategic location, and significant investments in ports, airports, logistics zones, and multimodal transport infrastructure under Vision 2030. |

|

United Arab Emirates |

28.7% |

Reflecting its position as a global trade and transshipment hub supported by world-class ports, free zones, advanced logistics services, and strong international connectivity. |

|

Qatar |

10.4% |

Reflecting continued investments in logistics infrastructure, Hamad Port, aviation cargo, and diversified supply chain capabilities supporting industrial and trade growth. |

|

Oman |

8.3% |

Reflecting its strategic maritime location, expanding port infrastructure, integrated logistics hubs, and focus on becoming a regional gateway for international trade. |

|

Kuwait |

7.2% |

Reflecting ongoing investments in transport infrastructure, warehousing, cross-border trade, and logistics modernization to strengthen regional supply chain connectivity. |

|

Bahrain |

5.9% |

Reflecting its efficient port and air cargo infrastructure, business-friendly regulatory environment, and growing role in regional distribution, e-commerce, and value-added logistics services. |

Saudi Arabia's 39.5% dominance is owing to its extensive transport infrastructure, large domestic economy, and strategic investments under Vision 2030 aimed at developing the Kingdom into a global logistics hub. UAE's 28.7% follows as a major international trade and transshipment center, supported by world-class ports, airports, and free zones that facilitate global cargo movement.

Qatar's 10.4% and Oman's 8.3% are strengthening their positions through continued investments in port expansion, logistics parks, and multimodal connectivity to diversify their economies. Kuwait's 7.2% enhancement of cross-border freight and warehousing capabilities through infrastructure modernization. Bahrain's 5.9% leverages its efficient port, air cargo network, and business-friendly environment to support regional distribution and e-commerce logistics.

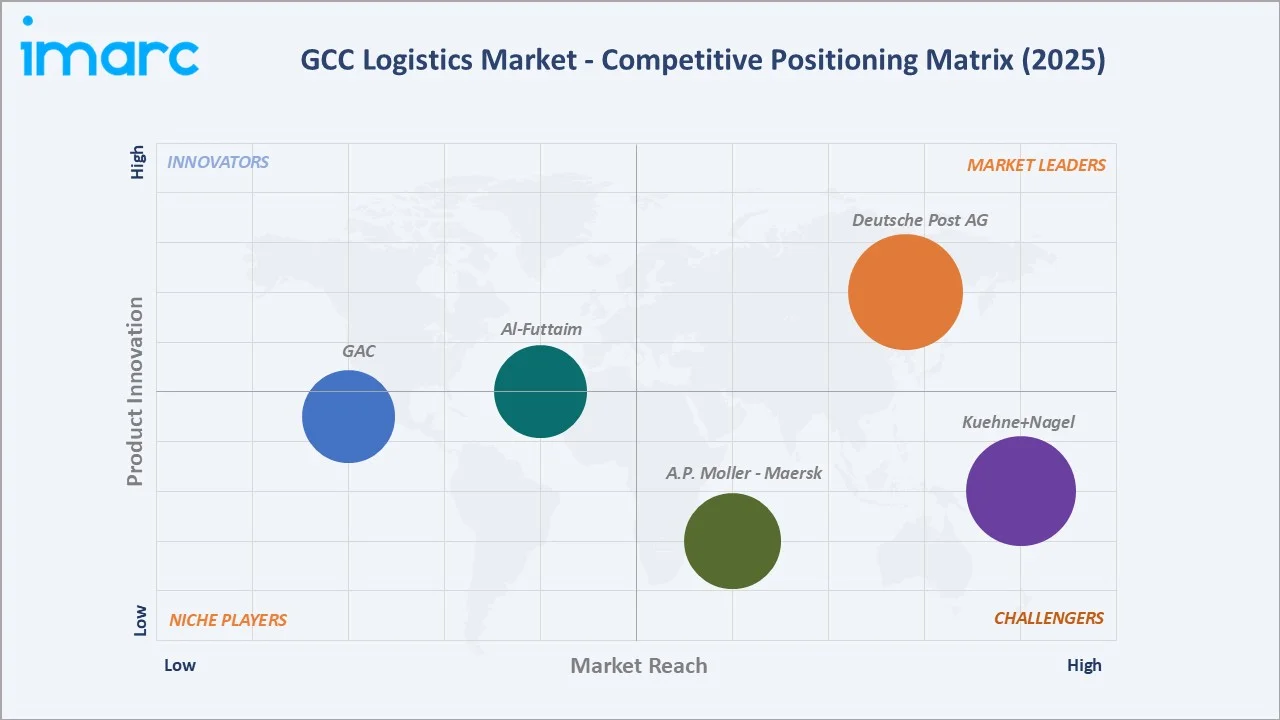

Competitive Landscape

The GCC logistics market is moderately consolidated, with a mix of global logistics providers, regional transportation companies, and national postal and freight operators competing across freight forwarding, warehousing, contract logistics, and express delivery. Market participants are expanding their presence through investments in smart warehouses, automated sorting systems, digital logistics platforms, and multimodal transportation networks. Strategic partnerships, acquisitions, and capacity expansion remain key competitive strategies to strengthen regional coverage and service offerings.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

Deutsche Post AG |

DHL Supply Chain |

Market Leader |

Deutsche Post AG, operating as the DHL Group, plays a foundational role in GCC logistics by driving cross-border e-commerce, ensuring supply chain resilience, and heavily investing in local infrastructure and sustainability across the region. |

|

Kuehne+Nagel |

Kuehne+Nagel |

Strong Challenger |

Kuehne+Nagel serves as a vital infrastructure backbone for GCC supply chains, operating major hubs in the United Arab Emirates and Saudi Arabia. The company acts as an end-to-end global freight forwarder and 3PL, specializing in air, sea, and road logistics, custom-tailored cross-border transit, and highly regulated cold chains for the pharma, aerospace, and energy sectors. |

|

A.P. Moller - Maersk |

Maersk |

Strong Challenger |

A.P. Moller - Maersk acts as a premier integrated logistics provider in the GCC, transitioning from a pure ocean carrier into an end-to-end supply chain manager. It anchors regional trade through massive terminal infrastructure and customs-bonded parks, while rerouting regional cargo via vital land bridges to sustain resilience amid Middle East shipping disruptions. |

|

Al-Futtaim |

Al-Futtaim Logistics |

Established Player |

Al-Futtaim, through its Al-Futtaim Logistics, is a major regional force in the GCC supply chain, providing end-to-end logistics, 4PL solutions, and automotive distribution across the Middle East. |

|

GAC |

GAC Logistics |

Established Player |

In the GCC region, GAC acts as a foundational pillar for logistics and supply chain management. It pioneered third-party contract logistics in the region and continues to drive regional trade flow through its massive infrastructural presence. |

Companies are also focusing on AI-driven supply chain management, real-time tracking, and value-added logistics services to improve operational efficiency and customer experience. The growing demand for e-commerce fulfillment, cold chain logistics, and integrated 3PL solutions continues to intensify competition across the GCC.

Key Company Profiles

Deutsche Post AG

Deutsche Post AG, operating through its DHL Group brand, is one of the leading logistics providers in the GCC, offering integrated services across express delivery, freight forwarding, contract logistics, supply chain management, and e-commerce fulfillment. The company has a strong presence across key GCC markets, including Saudi Arabia, the UAE, Qatar, Oman, Kuwait, and Bahrain, supported by strategically located logistics hubs, warehouses, and distribution centers. DHL serves diverse industries such as healthcare, retail, automotive, technology, energy, and industrial manufacturing with multimodal transportation solutions.

- Key Brands: DHL Supply Chain.

- Strategic Focus: Focused on expanding its integrated logistics and supply chain capabilities across the GCC through investments in warehousing, contract logistics, and multimodal transportation. The company is accelerating digital transformation by deploying AI, automation, robotics, IoT-enabled tracking, and advanced warehouse management systems to improve operational efficiency and shipment visibility.

Kuehne+Nagel

Kuehne+Nagel is a leading logistics company with a strong presence across the GCC, offering comprehensive solutions in sea freight, air freight, road logistics, contract logistics, customs brokerage, and supply chain management. The company operates through strategically located offices, logistics hubs, and warehousing facilities across key GCC markets, including Saudi Arabia, the UAE, Qatar, Oman, Kuwait, and Bahrain. It serves industries such as healthcare, pharmaceuticals, oil and gas, retail, automotive, industrial manufacturing, and perishables with integrated end-to-end logistics services.

- Key Brands: Kuehne+Nagel.

- Strategic Focus: Focused on expanding its integrated logistics network across the GCC by strengthening sea freight, air freight, road logistics, and contract logistics capabilities. The company is investing in digital supply chain solutions, real-time shipment visibility, AI-enabled analytics, and warehouse automation to improve operational efficiency and customer experience.

Market Concentration Analysis

The GCC logistics market is moderately consolidated, with a combination of global logistics companies, regional freight operators, and government-backed logistics providers competing across transportation, warehousing, freight forwarding, and contract logistics. International players leverage extensive global networks, advanced digital capabilities, and integrated end-to-end supply chain solutions, while regional companies compete through local market expertise and strong domestic distribution networks. Competition is increasingly centered on investments in automation, AI, smart warehousing, multimodal transportation, and e-commerce fulfillment capabilities. Strategic partnerships, mergers, acquisitions, and infrastructure expansion are further strengthening market positions. As demand for integrated 3PL, cold chain, and value-added logistics services grows, the market is expected to witness continued consolidation among leading players.

Investment & Growth Opportunities

Highest Growth Segments

4PL mega-project (~6.8% CAGR), airways express freight (~6.2% CAGR), railways (~5.8% CAGR), cold chain pharma (~6.5% CAGR), green logistics EV fleet (~7% CAGR from emerging base), and Oman (~7% CAGR from growing base) represent GCC logistics' highest-growth investment vectors through 2034.

Investment Themes

- GCC railway and Saudi Landbridge freight shift: Investments in GCC rail corridors and the Saudi Landbridge project are creating opportunities for multimodal freight transportation by reducing transit times, lowering logistics costs, and strengthening connectivity between ports, industrial zones, and inland markets.

- E-commerce last-mile and drone delivery: Rapid growth in e-commerce is driving investments in AI-powered last-mile delivery, drone logistics, micro-fulfillment centers, and automated delivery technologies to improve delivery speed, reduce operating costs, and enhance customer satisfaction.

Future Market Outlook (2026-2034)

The GCC logistics market is projected to grow from USD 114.56 Billion in 2025 to USD 182.01 Billion by 2034, delivering a 5.01% CAGR over the forecast period through Saudi Vision 2030 mega-project logistics structural scale, GCC railway network development, 4PL digital supply chain orchestration, and green logistics e-fleet integration. The market's anchor value of USD 146.28 Billion in 2030 represents GCC logistics at Saudi Landbridge railway commercial scale and 4PL mega-project mainstream inflection.

Three structural forces define GCC logistics growth through 2034. First, sustained government investments in ports, airports, railways, logistics parks, and multimodal transport corridors are strengthening regional and global trade connectivity. Second, rapid expansion of e-commerce, manufacturing, and non-oil industries is driving demand for integrated 3PL, warehousing, cold chain, and last-mile delivery services. Third, the adoption of AI, automation, smart warehousing, and digital logistics platforms is improving operational efficiency, supply chain visibility, and customer service, positioning the GCC as a leading global logistics and transshipment hub.

Research Methodology

Primary Research

Primary research comprised structured interviews and discussions with logistics service providers, freight forwarders, warehouse operators, shipping companies, port authorities, airport cargo operators, e-commerce companies, and industry experts across the GCC. Insights gathered through these interactions were used to validate market size estimates, technology adoption trends, competitive dynamics, service demand, pricing patterns, and future growth opportunities across key logistics segments.

Secondary Research

Secondary research encompassed company reports, government publications, port and airport statistics, trade databases, industry journals, press releases, and regulatory documents. These sources were used to assess market trends, infrastructure developments, logistics investments, competitive positioning, and macroeconomic factors influencing the GCC logistics market.

Forecasting Models

Forecasting models combined historical market performance with econometric analysis, trade flow assessment, and demand forecasting techniques to estimate future market growth. The analysis incorporated macroeconomic indicators, infrastructure investments, e-commerce expansion, freight volumes, and logistics capacity additions across the GCC. Scenario-based modeling and trend analysis were further used to evaluate the long-term impact of technology adoption, policy initiatives, and regional trade developments on the market through 2034.

GCC Logistics Market Report:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Countries Covered | Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Bahrain |

| Companies Covered | Deutsche Post AG, Kuehne+Nagel, A.P. Moller - Maersk, Al-Futtaim, GAC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the GCC logistics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the GCC logistics market.

- The study maps the leading, as well as the fastest-growing, markets. It further enables stakeholders to identify the key country-level markets within the region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the GCC logistics industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the GCC Logistics Market Report

The GCC logistics market reached USD 114.56 Billion in 2025, driven by rising investments in ports, airports, railways, logistics zones, and multimodal transport infrastructure, which are strengthening regional and global trade connectivity. Growth is further supported by expanding e-commerce, rising non-oil trade, industrial diversification, and increasing adoption of digital logistics solutions across the region.

The GCC logistics market grows at 5.01% CAGR during 2026-2034, reaching USD 182.01 Billion by 2034. The CAGR reflects Saudi Vision 2030, GCC e-commerce growth, and energy logistics structural demand.

3PL leads at 51.8% as businesses increasingly outsource transportation, warehousing, inventory management, customs clearance, and fulfillment services to improve operational efficiency and reduce costs.

Roadways lead at 47.3% due to their wide connectivity, flexibility, and ability to support door-to-door freight movement across cities, ports, airports, warehouses, and industrial zones. They remain the preferred mode for domestic distribution, cross-border trade, and last-mile delivery across the region.

Saudi Arabia leads at 39.5% due to its large economy, expanding industrial base, and strong investments in transport infrastructure, logistics zones, ports, airports, and rail networks. Vision 2030 initiatives are further supporting multimodal connectivity, trade facilitation, and the Kingdom’s development as a major regional and global logistics hub.

Leading companies include Deutsche Post AG, Kuehne+Nagel, A.P. Moller – Maersk, Al-Futtaim, and GAC, among others.

The market is projected to reach approximately USD 146.28 Billion by 2030, supported by rising investments in transport infrastructure, logistics parks, and multimodal connectivity. Growth will be driven by expanding e-commerce, non-oil trade, and demand for integrated 3PL and warehousing services.

Three priority investment opportunities are emerging across the GCC logistics market. First, expanding multimodal logistics infrastructure, including the GCC Railway and Saudi Landbridge projects, offers significant potential to improve regional freight connectivity and trade efficiency. Second, rapid e-commerce growth is driving investments in automated fulfillment centers, AI-enabled last-mile delivery, and drone-based logistics solutions. Third, increasing demand for smart and sustainable logistics is creating opportunities in warehouse automation, AI-powered supply chain platforms, electric commercial fleets, and cold chain infrastructure for healthcare and food logistics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)