GCC Private Equity Market Size, Share, Trends and Forecast by Fund Type and Country, 2026-2034

GCC Private Equity Market Size, Share, Trends & Forecast (2026-2034)

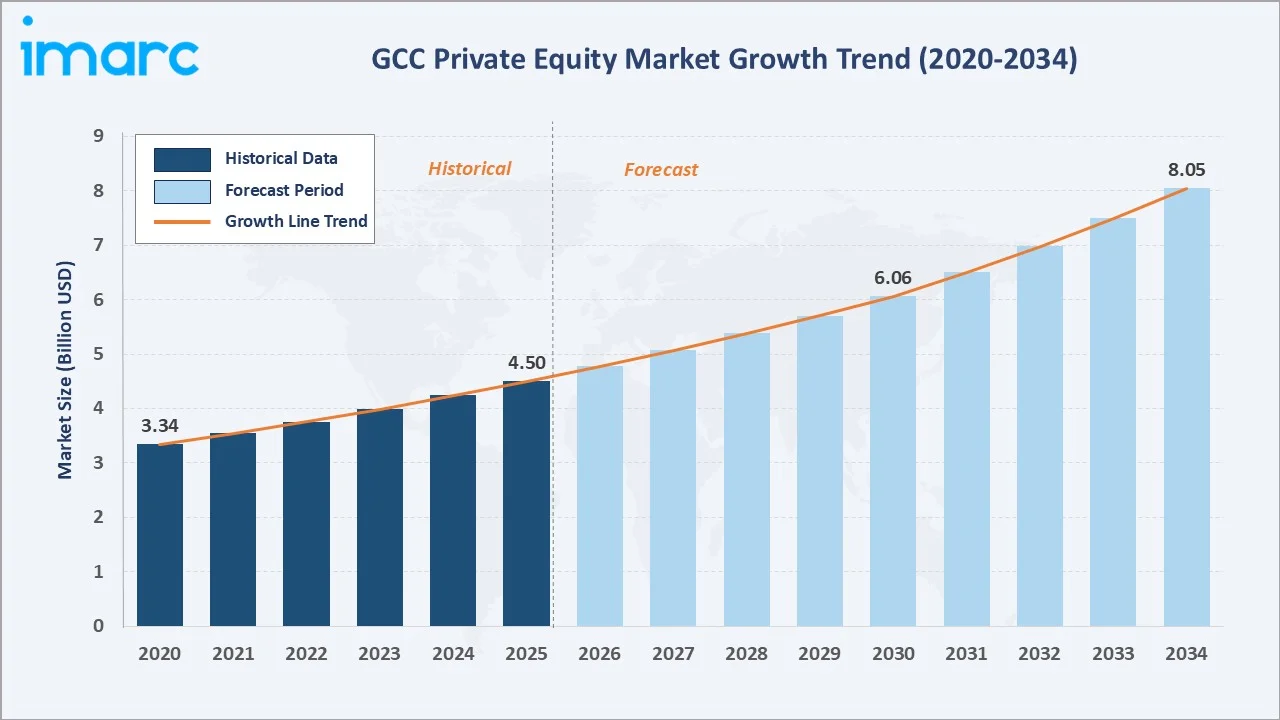

The GCC private equity market reached USD 4.50 Billion in 2025 and is projected to reach USD 8.05 Billion by 2034, growing at a CAGR of 6.14% during 2026-2034. The market is driven by Vision 2030-led economic diversification, a prolonged low-interest-rate environment, and rising sovereign wealth fund participation. Non-oil private sector growth across Saudi Arabia and the UAE has widened the pool of investable companies, while active IPO markets are strengthening the region's exit ecosystem.

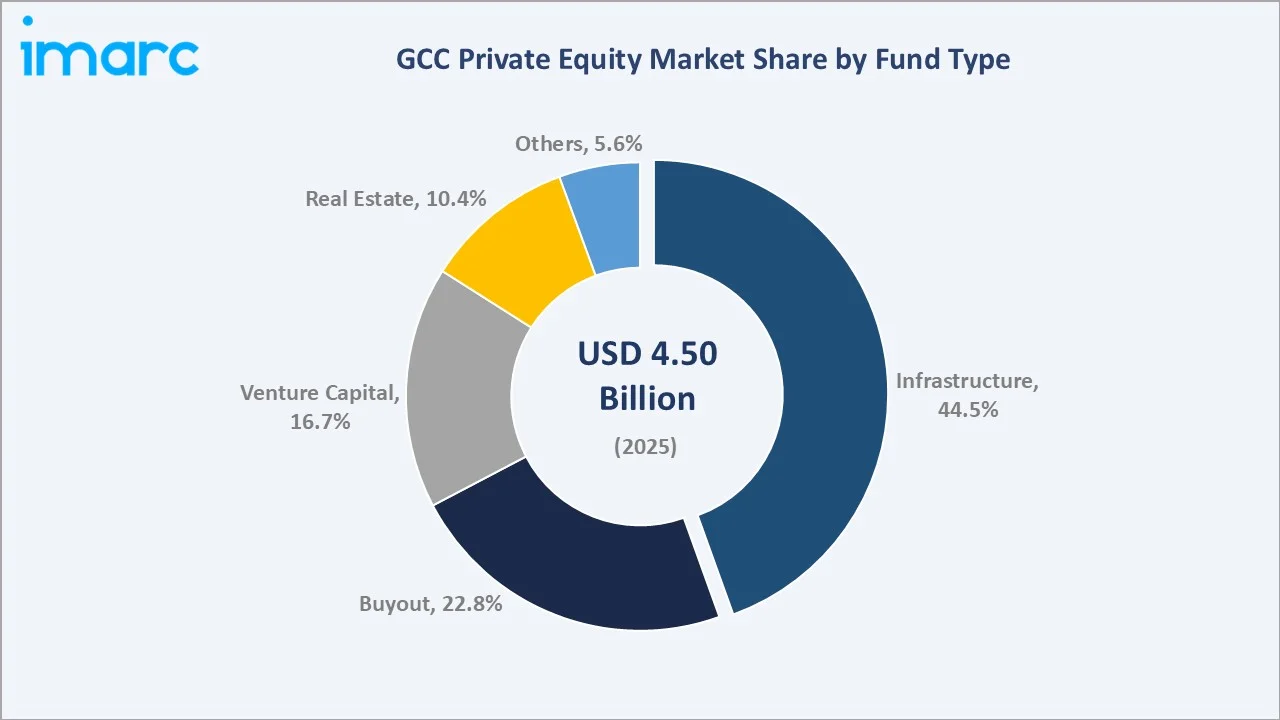

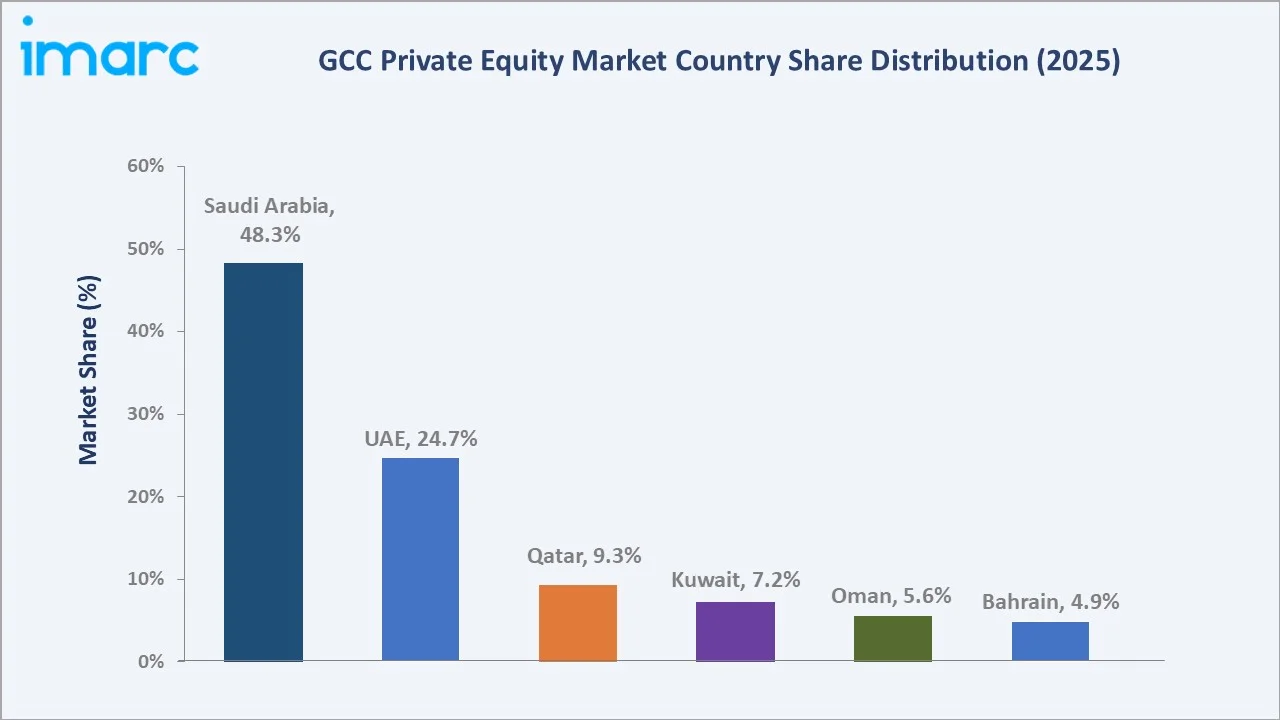

The Infrastructure segment from the fund type dimension dominates at 44.5%. Saudi Arabia leads at 48.3% of the regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.50 Billion |

|

Forecast Market Size (2034) |

USD 8.05 Billion |

|

CAGR (2026-2034) |

6.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Fund Type |

Infrastructure (44.5%, 2025) |

|

Leading Country |

Saudi Arabia (48.3%, 2025) |

The market expanded from USD 3.34 Billion in 2020 to USD 4.50 Billion in 2025, anchored at USD 6.06 Billion in 2030 and forecast to reach USD 8.05 Billion by 2034. Growth accelerated through the historical period as national diversification programs widened the pool of investable companies and is expected to further strengthen in the latter half of the forecast period as sovereign co-investment platforms and family business institutionalization mandates continue to scale.

To get more information on this market, Request Sample

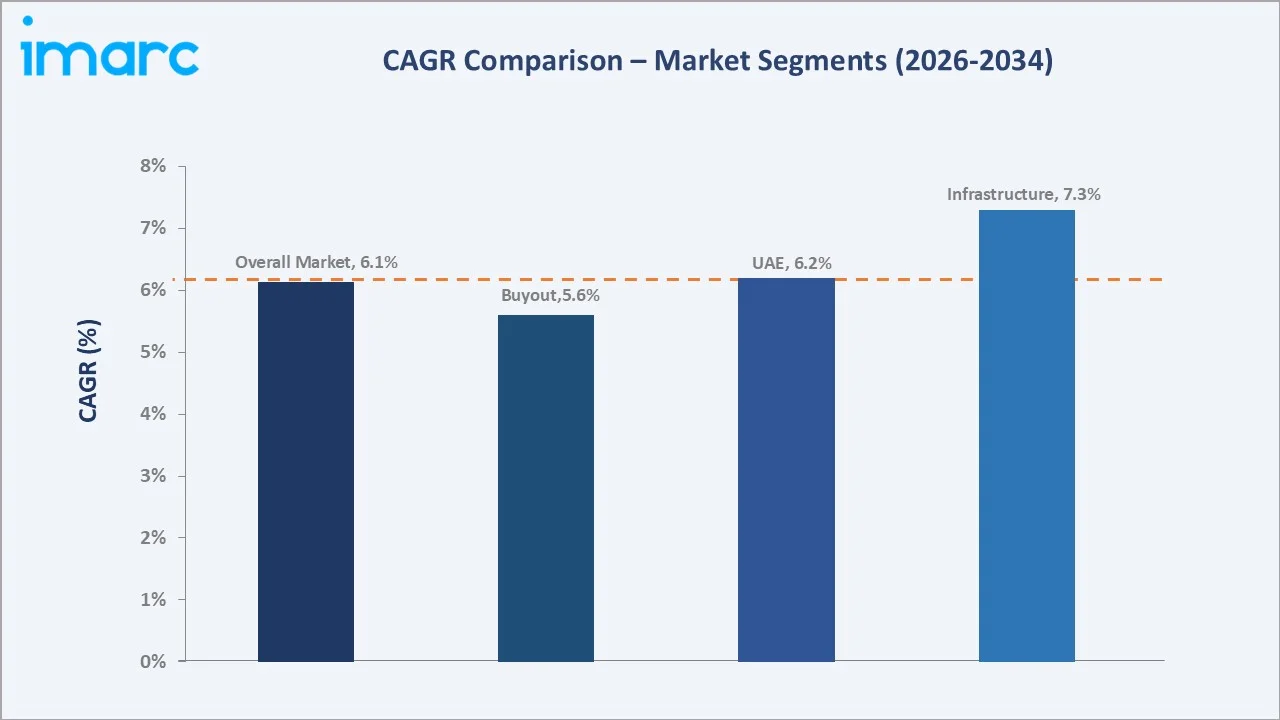

The Venture Capital segment grows fastest at ~8.1% CAGR as GCC family offices and government-backed accelerators expand early-stage technology funding. Infrastructure funds grow at ~7.3% CAGR as PIF, ADIA, and QIA anchor large-scale co-investment platforms in utilities, transport, and digital infrastructure.

Executive Summary

The GCC private equity market reached USD 4.50 Billion in 2025, reflecting the region's transition from an oil-revenue-dependent economy toward a diversified, private-capital-driven investment landscape. Private equity has become a core instrument of the Gulf's Vision-led economic transformation programs, channeling sovereign and institutional capital into technology, healthcare, infrastructure, and consumer sectors. The market is projected to reach USD 8.05 Billion by 2034.

Infrastructure at 44.5% dominates by capturing sovereign wealth fund-anchored utilities, transport, and digital infrastructure co-investment mandates. Saudi Arabia at 48.3% leads through Vision 2030 privatization programs, PIF-backed fund formation, and the Kingdom's expanding mid-market buyout activity. The UAE at 24.7% follows through Abu Dhabi and Dubai's sovereign capital base and deepening family office institutionalization.

Key Market Insights

|

Insight |

Data |

|

Dominant Fund Type |

Infrastructure - 44.5% share (2025) |

|

Dominant Country |

Saudi Arabia - 48.3% market share (2025) |

|

Market Opportunity |

Sharia-compliant private credit vehicles; SME growth-equity platforms; Vision 2030-aligned infrastructure co-investment; secondary market development; family office institutionalization |

Key Analytical Observations Supporting The Above Data:

- Infrastructure at 44.5%: The Infrastructure segment dominates as sovereign wealth funds including PIF, ADIA, and QIA anchor large-scale utilities, transport, water, and digital infrastructure co-investment platforms aligned with national diversification mandates. Its capital-intensive, long-duration nature suits the patient-capital profile of GCC sovereign allocators.

- Saudi Arabia at 48.3%: The Kingdom dominates through Vision 2030 privatization of state assets, an expanding pool of non-oil investable companies, and the Public Investment Fund's role in anchoring both direct deals and third-party fund formation. Non-oil private sector growth reached 5.9% in 2024, widening the addressable deal pipeline.

GCC Private Equity Market Overview

The GCC private equity market encompasses capital raised from sovereign wealth funds, institutional investors, family offices, and high-net-worth individuals to acquire stakes in privately held companies across Saudi Arabia, the UAE, Qatar, Kuwait, Oman, and Bahrain. Fund types of span buyout, venture capital, real estate, and infrastructure strategies, deployed across technology, healthcare, financial services, industrials, and consumer sectors.

The ecosystem integrates general partners managing regional and cross-border funds, limited partners including sovereign wealth funds and family offices, portfolio companies undergoing governance and operational transformation, exchange operators enabling IPO exits, and regulatory bodies including the Saudi Capital Market Authority, ADGM's Financial Services Regulatory Authority, and DIFC. Macroeconomic factors include non-oil GDP growth, prolonged low interest rates, and national diversification programs including Saudi Vision 2030.

Market Dynamics

To evaluate market opportunities, Request Sample

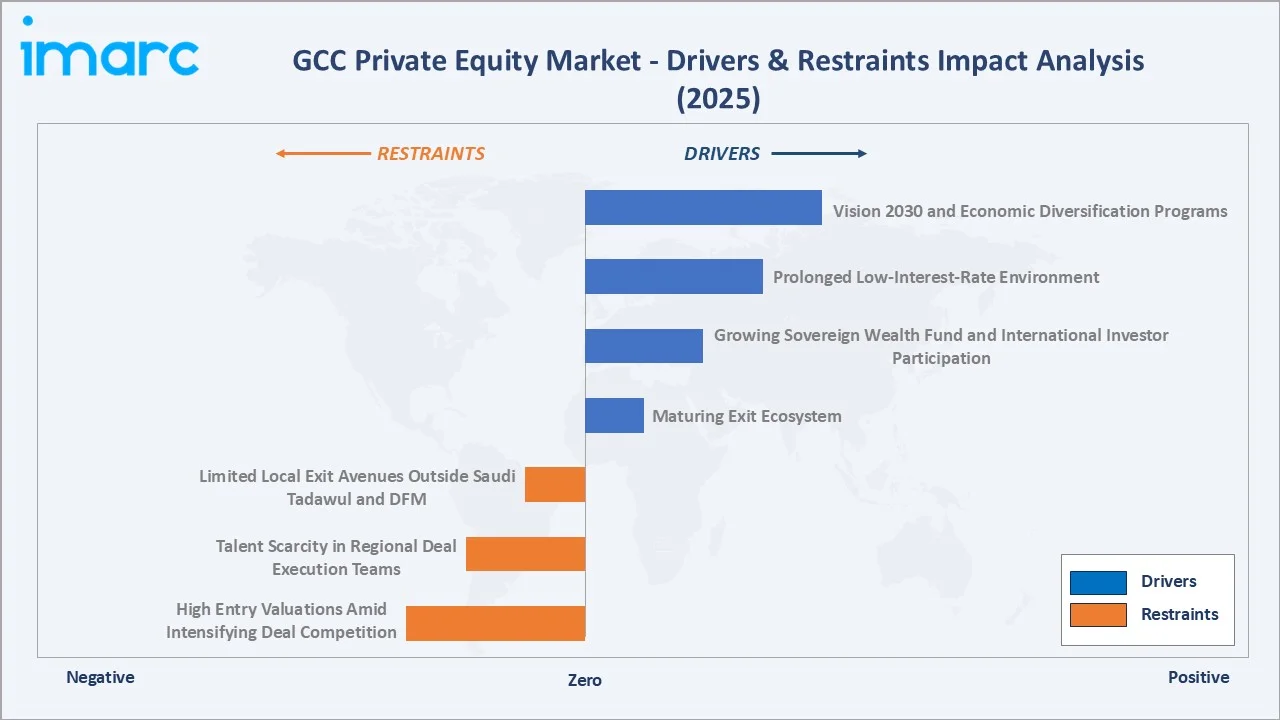

Market Drivers

- Vision 2030 and Economic Diversification Programs: Saudi Arabia's Vision 2030 and complementary diversification programs across the UAE, Qatar, Kuwait, Oman, and Bahrain are opening previously restricted sectors to private capital, establishing specialized economic zones, and privatizing state-owned assets. The Saudi government aims to raise the private sector's contribution to GDP from 40% to 65%, creating sustained deal flow for private equity sponsors.

- Prolonged Low-Interest-Rate Environment: A prolonged low-interest-rate environment across the GCC has pushed institutional allocators and high-net-worth individuals toward alternative assets offering higher risk-adjusted returns than traditional fixed-income instruments. This has increased capital commitments to private equity funds targeting mid-market and growth-stage companies.

- Growing Sovereign Wealth Fund and International Investor Participation: Sovereign wealth funds including PIF, ADIA, and QIA are anchoring larger, more complex private equity transactions and co-investing alongside international general partners. In 2025, Qatar Investment Authority partnered with KKR to establish a USD 3.5 billion infrastructure fund, illustrating the scale of cross-border capital now targeting the region.

- Maturing Exit Ecosystem: Active regional IPO markets, which raised over USD 2.3 billion in Q2 2025 alone, are reducing the liquidity risk historically associated with GCC private equity. Deepening secondary markets and strategic trade sale activity are giving sponsors multiple credible paths to realize returns on mid-market and growth investments.

Market Restraints

- Limited Local Exit Avenues Outside Saudi Tadawul and DFM: Beyond the Saudi Tadawul and Dubai Financial Market, regional public listing venues remain comparatively shallow, constraining exit optionality for sponsors in Qatar, Kuwait, Oman, and Bahrain. This concentration increases reliance on strategic trade sales and cross-border secondary transactions to realize returns.

- Talent Scarcity in Regional Deal Execution Teams: The rapid expansion of GCC private equity activity has outpaced the growth of experienced regional deal-execution talent, including transaction professionals skilled in due diligence, portfolio value creation, and cross-border structuring, constraining the pace at which new funds can be deployed.

- High Entry Valuations Amid Intensifying Deal Competition: Growing competition among regional and international sponsors for a limited pool of quality mid-market targets is compressing available deal flow and placing upward pressure on entry multiples, narrowing the margin for underwriting error across the holding period.

Market Opportunities

- Sharia-Compliant Private Credit and Structured Equity: Growing demand for Sharia-compliant financing structures, including structured equity and asset-backed vehicles, is creating opportunities for sponsors able to combine regulatory compliance with competitive risk-adjusted returns for regional and international limited partners.

- Family Office Institutionalization: The evolution of GCC family offices from passive wealth preservers into active co-investors is creating new sources of limited partner capital and direct investment activity, opening opportunities for sponsors to structure dedicated family office co-investment platforms.

Market Challenges

- Geopolitical and Oil-Price Volatility: Regional geopolitical tensions and oil-price volatility periodically affect investor sentiment and sovereign fiscal positions, introducing episodic uncertainty into fundraising cycles even as long-term diversification mandates remain intact.

- Cross-Border Regulatory Harmonization Across GCC Jurisdictions: Differing regulatory, tax, and fund domiciliation frameworks across Saudi Arabia, the UAE, Qatar, Kuwait, Oman, and Bahrain add structuring complexity for sponsors executing cross-border transactions, requiring specialized legal and compliance capabilities to manage multi-jurisdictional deal execution.

Emerging Market Trends

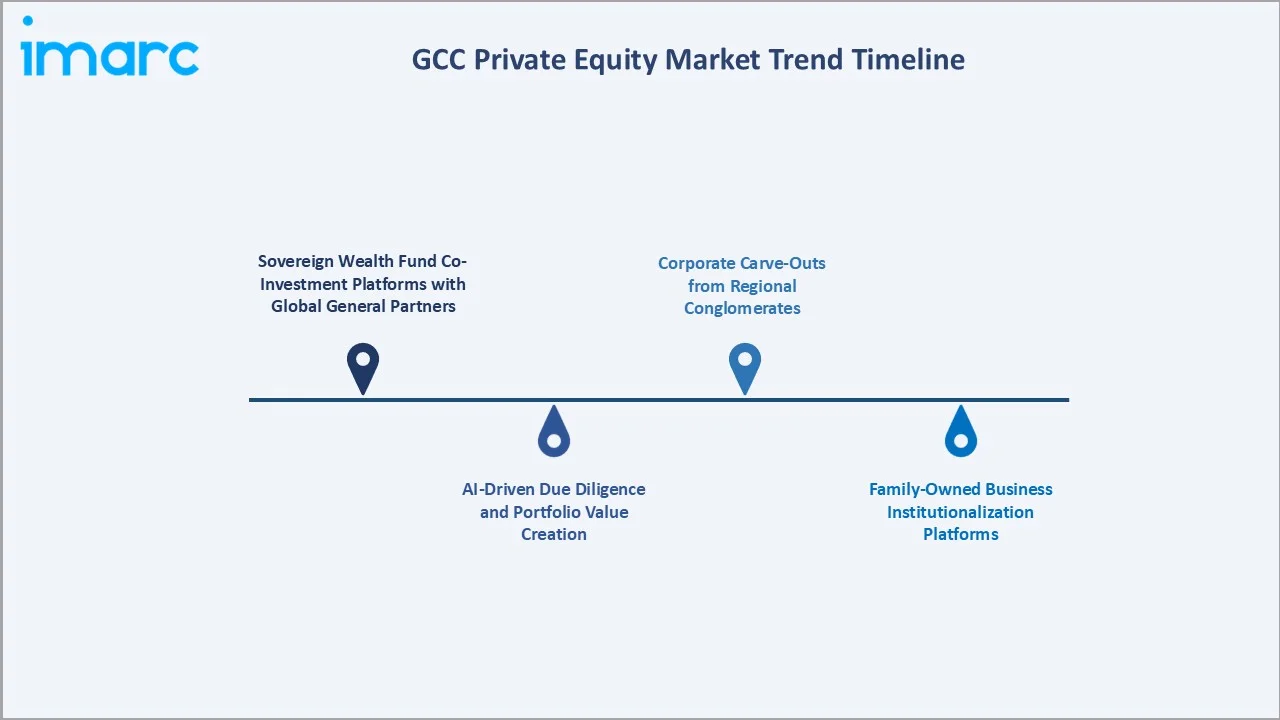

1. Sovereign Wealth Fund Co-Investment Platforms with Global General Partners

The growing adoption of co-investment platforms by GCC sovereign wealth funds is reshaping the regional private equity landscape. Rather than participating solely as passive limited partners, these investors are increasingly engaging in active deal sourcing, capital deployment, and strategic collaboration with international investment managers across diversified asset classes.

2. AI-Driven Due Diligence and Portfolio Value Creation

GCC private equity firms are adopting AI-powered analytics to compress due diligence timelines, with automated financial modeling and risk assessment. Technology-focused portfolio value creation, including AI implementation across portfolio companies, is emerging as a differentiator in a competitive mid-market deal environment.

3. Family-Owned Business Institutionalization Platforms

Regional sponsors are structuring dedicated platforms to professionalize family-owned businesses, which form a major share of the Gulf economy. Investcorp's Golden Horizon Partnership has already backed multiple Saudi family-owned platforms, with the sponsor becoming the first institutional investor to take a board seat alongside founding families in more than 60% of its regional investments.

4. Corporate Carve-Outs from Regional Conglomerates

Large regional conglomerates are increasingly willing to spin off non-core business divisions to sharpen strategic focus, creating a growing pipeline of carve-out opportunities for private equity sponsors.

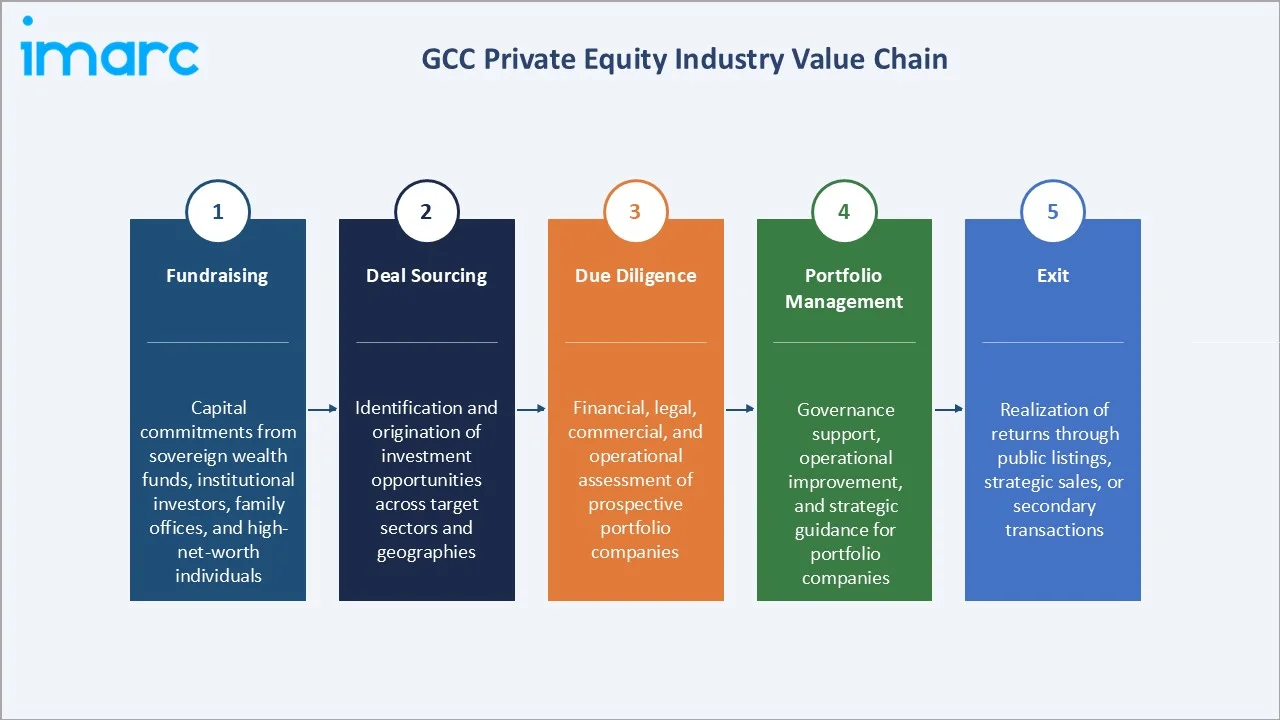

Industry Value Chain Analysis

The GCC private equity value chain integrates capital formation and fundraising, deal origination and sourcing, due diligence and transaction structuring, portfolio value creation, and exit realization. The chain's commercial architecture is increasingly shaped by sovereign wealth funds acting simultaneously as capital providers and active co-investors alongside traditional general partners.

|

Stage |

Key Participants |

|

Fundraising |

Capital commitments from sovereign wealth funds, institutional investors, family offices, and high-net-worth individuals |

|

Deal Sourcing |

Identification and origination of investment opportunities across target sectors and geographies |

|

Due Diligence |

Financial, legal, commercial, and operational assessment of prospective portfolio companies |

|

Portfolio Management |

Governance support, operational improvement, and strategic guidance for portfolio companies |

|

Exit |

Realization of returns through public listings, strategic sales, or secondary transactions |

The capital formation and fundraising stage is the value chain's most strategically critical link, given the outsized role of sovereign wealth funds in anchoring both domestic and cross-border fund structures. The exit and realization stage is undergoing the most rapid transformation as regional IPO markets mature and provide sponsors with credible public-market liquidity alongside traditional trade sale exits.

Technology Landscape in the GCC Private Equity Industry

AI-Powered Due Diligence and Deal Analytics

AI-powered due diligence tools are streamlining investment evaluation by automating financial modeling, document review, and risk assessment. These tools are reducing due diligence timelines by up to 40% for GCC sponsors, allowing deal teams to evaluate a larger pipeline of opportunities without expanding headcount. Their growing adoption is accelerating deal velocity across the region's competitive mid-market segment.

Digital Fund Administration and Reporting Platforms

Digital fund administration platforms are improving transparency, compliance, and reporting efficiency for GCC general partners managing increasingly complex multi-jurisdictional fund structures. These platforms support real-time portfolio monitoring and simplify regulatory reporting across Saudi, UAE, and other regional frameworks, making them increasingly central to institutional-grade fund operations.

Data-Driven Portfolio Value Creation

Machine learning-based analytics are increasingly embedded within portfolio companies to improve operational efficiency, demand forecasting, and customer insights. Technology-focused value creation initiatives now account for a meaningful share of private equity deployment value in the region, reflecting sponsors' growing emphasis on data-driven operational improvement alongside traditional governance and financial engineering levers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Fund Type |

Infrastructure |

44.5% |

2025 |

|

Country |

Saudi Arabia |

48.3% |

2025 |

By Fund Type

The Infrastructure segment leads at 44.5% in 2025, encompassing sovereign wealth fund-anchored utilities, transport, water, and digital infrastructure co-investment vehicles, the most capital-intensive and highest-value fund category in the GCC private equity market.

To access detailed market analysis, Request Sample

The Buyout segment at 22.8% captures control-oriented mid-market transactions across family-owned businesses and corporate carve-outs. Venture Capital at 16.7% represents the fastest-growing segment, driven by government-backed accelerators and family office participation in early-stage technology funding. Real Estate at 10.4% and Others at 5.6%, including private credit and structured equity, round out the fund type distribution.

Regional Market Insights

|

Country |

Share (2025) |

Key Market Drivers & Characteristics |

|

Saudi Arabia |

48.3% |

Driven by economic diversification initiatives, government-backed investment programs, and a growing pipeline of private companies |

|

UAE |

24.7% |

Supported by a strong financial ecosystem, sovereign capital availability, and an established base of institutional investors |

|

Qatar |

9.3% |

Driven by sovereign wealth fund activity and growing investment in infrastructure and technology sectors |

|

Kuwait |

7.2% |

Reflects steady capital deployment by domestic institutional investors into regional funds |

|

Oman |

5.6% |

An emerging market supported by ongoing economic diversification and growth capital demand |

|

Bahrain |

4.9% |

Home to a long-established alternative investment industry and a mature regulatory framework |

Saudi Arabia, at 48.3%, leads through Vision 2030's privatization pipeline, PIF-anchored fund formation, and the Kingdom's deepening mid-market buyout activity. The UAE, at 24.7%, reflects Abu Dhabi and Dubai sovereign capital depth alongside DIFC and ADGM's regulatory infrastructure supporting fund domiciliation.

Qatar, at 9.3%, is anchored by QIA-led infrastructure and technology co-investment platforms. Kuwait, at 7.2%, reflects Kuwait Investment Authority's deployment into regional venture and growth vehicles, while Oman, at 5.6%, and Bahrain, at 4.9%, represent smaller but strategically important markets, with Bahrain hosting the region's most established alternative investment ecosystem through Investcorp.

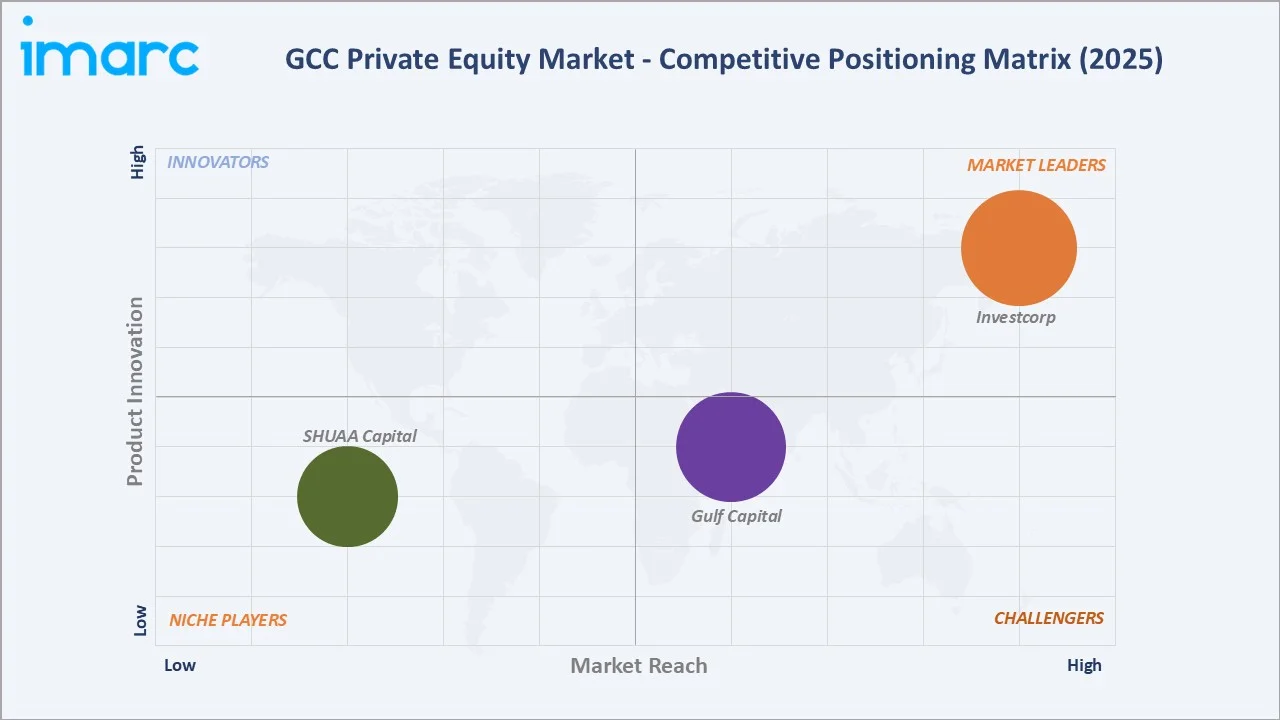

Competitive Landscape

The GCC private equity competitive landscape is moderately concentrated, led by sovereign wealth fund-affiliated managers and long-established alternative asset managers, with a growing tier of Saudi and UAE mid-market sponsors competing for family-owned business and corporate carve-out mandates.

|

Company Name |

Key Funds / Platforms |

Market Position |

Core Strength |

|

Investcorp |

Private Equity |

Market Leader |

Bahrain-based alternative asset manager with the region's deepest track record in GCC family-business partnerships. |

|

Gulf Capital |

Gulf Capital Private Equity Partners, Growth Capital funds |

Strong Challenger |

Abu Dhabi-headquartered thematic investor with two decades of mid-market buyout and growth capital experience. |

|

SHUAA Capital |

SHUAA private and public market investment funds |

Niche Player |

Dubai-based investment firm combining asset management, investment banking, and private market strategies across MENA. |

Key players include Investcorp, Gulf Capital, SHUAA Capital, and others.

Key Company Profiles

Investcorp

Investcorp is a Bahrain-headquartered global alternative investment manager with a leading presence in the GCC private equity market through its regional mid-market buyout and growth capital platforms.

- Key Products: Private Equity

- Recent Developments: In June 2026, Investcorp acquired a strategic stake in Metra, a UAE-headquartered IT distribution group, through its Saudi Pre-IPO Growth Fund. This partnership marks a significant milestone for Metra, a third-generation family business and one of the region’s most prominent technology distribution platforms, as it continues to expand across the GCC region.

- Strategic Focus: Expanding investments in family-owned GCC businesses, corporate carve-outs, healthcare, and growth-stage companies, with more of the regional deals made alongside founding families.

Gulf Capital

Gulf Capital is an Abu Dhabi-headquartered alternative investment firm with more than two decades of experience across private equity, private debt, growth capital, and real estate in the GCC region.

- Key Products: Gulf Capital Private Equity Partners, Growth Capital funds

- Strategic Focus: Deepening thematic investments in technology, fintech, healthcare, and sustainability sectors, while maintaining its position as one of the most active mid-market sponsors investing from the GCC into wider Asia.

Market Concentration Analysis

The GCC private equity market is moderately concentrated at the sovereign-affiliated tier, with the top three key players collectively anchoring an estimated 35-45% of large-cap regional transaction value.

Saudi-based mid-market sponsors, account for an estimated 20-25% of regional deal volume by count, reflecting the Kingdom's deepening mid-market ecosystem. Market concentration is gradually declining as new Saudi and UAE mid-market entrants gain track record and as international sponsors establish dedicated regional platforms.

Investment & Growth Opportunities

Highest Growth Segments

Venture Capital fund type (~8.1% CAGR), Infrastructure (~7.3% CAGR), Saudi Arabia country exposure (~6.9% CAGR), and UAE country exposure (~6.2% CAGR) represent the highest-growth investment vectors through 2034, reflecting the combined pull of technology-sector capital formation and sovereign infrastructure deployment.

Emerging Investment Opportunities

Sharia-compliant private credit and structured equity vehicles represent the GCC private equity market's fastest-emerging opportunity, as regional and international limited partners seek yield alongside regulatory and cultural alignment. Family office co-investment platforms are similarly under-penetrated relative to the scale of Gulf private wealth, creating a structurally growing demand pool through 2034.

Investment Themes

- Family Business Institutionalization Platforms as a Structural GCC Opportunity: Family-owned enterprises form most of the non-oil Gulf economy yet remain significantly under-penetrated by institutional private capital relative to developed markets. Sponsors that can combine capital with governance expertise are positioned to capture a multi-decade institutionalization opportunity as founding generations plan succession.

- Sovereign Co-Investment Platform Participation for International General Partners: International sponsors that can structure dedicated co-investment platforms alongside PIF, ADIA, Mubadala, or QIA gain access to some of the world's largest and most patient pools of capital, alongside local market knowledge that would otherwise be difficult to replicate independently.

Future Market Outlook (2026-2034)

The GCC private equity market is projected to grow from USD 4.50 Billion in 2025 to USD 8.05 Billion by 2034, delivering a 6.14% CAGR over the forecast period. The market's anchor value of USD 6.06 Billion in 2030 represents a private equity industry during its most significant institutionalization phase, as family businesses increasingly professionalize, sovereign co-investment platforms mature, and regional IPO markets deepen. Infrastructure funds are expected to maintain their leading share as national diversification programs continue anchoring large-scale co-investment mandates, while Venture Capital's above-market growth reflects the region's expanding technology and fintech investment ecosystem.

Three structural forces define GCC private equity market growth through 2034 with strong confidence. Vision 2030 and parallel national diversification programs continue to widen the pool of investable non-oil companies at a pace that outstrips current sponsor deployment capacity. Sovereign wealth fund co-investment platforms are deepening capital availability while transferring international best practices to regional deal execution teams. The maturing regional IPO and secondary market ecosystem is progressively de-risking exits, encouraging a new generation of limited partners to increase allocations to the asset class.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025-2026), including private equity fund managers, sovereign wealth fund investment officers, family office principals, and regional investment banking advisors active in GCC deal execution.

Secondary Research

Secondary research encompassed company annual reports and investor presentations; Saudi Central Bank (SAMA) and International Monetary Fund macroeconomic data; Dubai International Financial Centre family office registration statistics; regional stock exchange IPO data from Saudi Tadawul and Dubai Financial Market; and industry press coverage of GCC private equity fund launches and transactions. Over 45 secondary sources were reviewed.

Forecasting Models

Market value forecasts were developed using a bottom-up model incorporating: (i) historical GCC private equity deal value and fund formation trends by country and fund type; (ii) macroeconomic growth projections for non-oil GDP across GCC economies; (iii) sovereign wealth fund allocation trends to domestic private equity; and (iv) triangulation against comparable emerging-market private equity growth trajectories.

GCC Private Equity Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Fund Types Covered | Buyout, Venture Capital (VCs), Real Estate, Infrastructure, Others |

| Countries Covered | Saudi Arabia, UAE, Qatar, Bahrain, Kuwait, Oman |

| Companies Covered | Investcorp, Gulf Capital, SHUAA Capital, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the GCC private equity market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the GCC private equity market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the GCC private equity industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the GCC Private Equity Market Report

The GCC private equity market reached USD 4.50 Billion in 2025, driven by the Infrastructure fund type dominant at 44.5%, Saudi Arabia leading at 48.3% of regional market share, Vision 2030-led privatization creating an expanding investable company pool, and rising sovereign wealth fund co-investment activity across the region.

The GCC private equity market grows at 6.14% CAGR during 2026-2034, reaching USD 8.05 Billion by 2034. This growth reflects continued Vision 2030 diversification, deepening sovereign wealth fund co-investment platforms, family business institutionalization, and a maturing regional exit ecosystem.

Infrastructure leads at 44.5%, capturing sovereign wealth fund-anchored utilities, transport, and digital infrastructure co-investment mandates. This segment grows at ~7.3% CAGR through 2034 as national diversification programs continue prioritizing large-scale infrastructure development.

Saudi Arabia leads at 48.3% through Vision 2030 privatization programs and PIF-anchored fund formation. Saudi Arabia grows at ~6.9% CAGR through 2034, reflecting the Kingdom's expanding non-oil private sector and mid-market buyout activity.

Saudi Arabia and the UAE jointly command 73.0% of the GCC private equity market in 2025, led by Saudi Arabia's Vision 2030 pipeline and the UAE's sovereign capital depth and family office ecosystem.

Leading companies include Investcorp, Gulf Capital, SHUAA Capital, and others.

The GCC private equity market is projected to reach approximately USD 6.06 Billion by 2030, with sovereign co-investment platforms becoming a standard structure for large transactions, family business institutionalization accelerating, and regional IPO markets continuing to deepen.

Three priority investment opportunities: family business institutionalization platforms, Sharia-compliant private credit and structured equity vehicles, and sovereign co-investment platform participation for international general partners seeking access to Gulf capital pools.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)