India Bioplastics Market Size, Share, Trends and Forecast by Product, Application, Distribution Channel, and Region, 2026-2034

India Bioplastics Market Size, Share, Trends & Forecast (2026-2034)

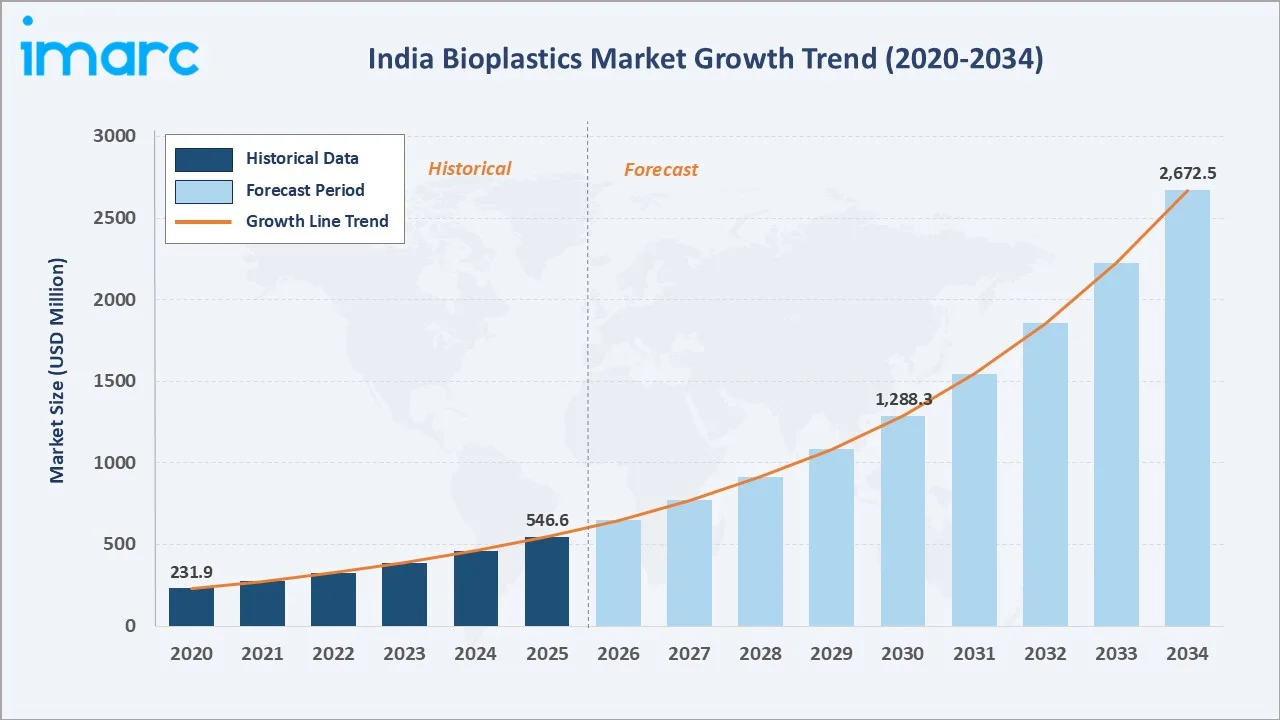

The India bioplastics market reached USD 546.6 Million in 2025 and is projected to reach USD 2,672.5 Million by 2034, exhibiting a CAGR of 18.71% during 2026-2034. Growth is anchored by India's nationwide single-use plastic ban, Extended Producer Responsibility (EPR) enforcement, abundant agri-feedstock availability, and rising sustainable packaging demand from FMCG and e-commerce sectors.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 546.6 Million |

|

Market Forecast (2034) |

USD 2,672.5 Million |

|

CAGR (2026-2034) |

18.71% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The India bioplastics market is gaining momentum as industries shift toward sustainable, biodegradable, and bio-based materials to reduce dependence on conventional plastics. Rising environmental concerns, government restrictions on single-use plastics, growing consumer preference for eco-friendly packaging, and increasing adoption across food packaging, agriculture, consumer goods, textiles, and healthcare are supporting market growth.

To get more information on this market, Request Sample

The expansion of bio-based feedstock availability, investments in compostable packaging, and corporate sustainability commitments are further encouraging manufacturers to develop alternatives such as PLA, PHA, starch blends, and bio-PET.

Executive Summary

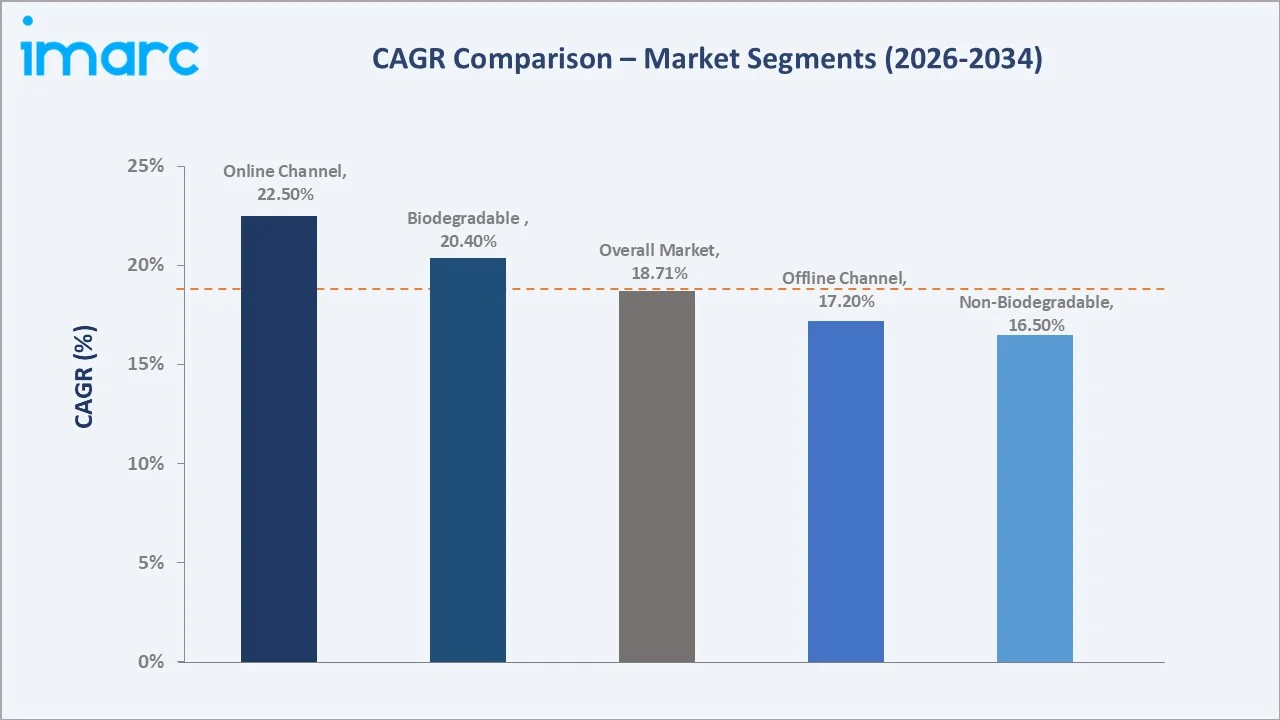

India's bioplastics market is among the fastest-growing sustainable materials categories in Asia, expanding at an 18.71% CAGR through 2034 amid sustained regulatory pressure, structural FMCG demand for eco-friendly packaging, and rising public awareness of single-use plastic pollution.

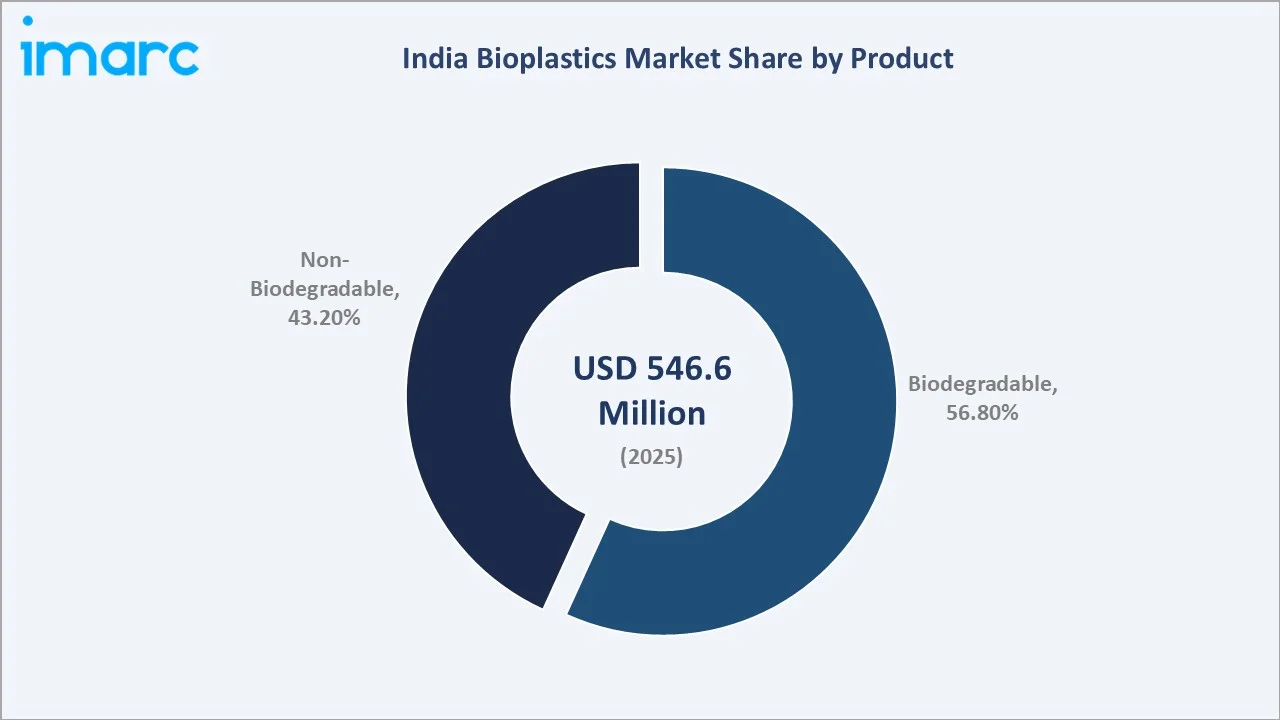

Biodegradable bioplastics including PLA, PBAT, PBS, and starch blends dominate the product mix at 56.8% share, while non-biodegradable bio-based variants such as Bio-PE and Bio-PET account for 43.2%. Domestic production capacity is estimated at approximately 25,000–30,000 tons annually, with around 70% of high-performance polymer demand still met through imports.

The Government of India's 2022 single-use plastic ban, combined with Extended Producer Responsibility enforcement and Uttar Pradesh’s Bioplastic Industry Policy 2024, which offers financial support for biodegradable alternatives, including a 50% capital subsidy for eligible anchor units, continues to expand addressable demand.

North India leads the regional mix at 34.5% in 2025, anchored by Delhi-NCR FMCG manufacturing and policy enforcement. Key 2024–2025 milestones include the inauguration of the first integrated PLA bioplastic plant by Balrampur Chini Mills, Praj Industries' Jejuri demonstration facility for biopolymers plant (inaugurated October 2024), and accelerated supply agreements between domestic compostable bag producers and major e-commerce and quick-commerce platforms.

Key Market Insights

|

Indicator |

Value (2025) |

|

Leading Product |

Biodegradable (56.8%) |

|

Fastest-Growing Product |

Biodegradable (~20.40% CAGR) |

|

Leading Distribution Channel |

Offline (61.1%) |

|

Fastest-Growing Channel |

Online (~22.50% CAGR) |

|

Largest Region |

North India (34.5%) |

|

Key Players |

Praj Industries, BASF, Advance Bio Material Company P.Ltd, and Encode Life |

Key Analytical Observations Supporting the Above Data:

- Biodegradable bioplastics account for 56.8% of the India bioplastics market in 2025, reflecting strong demand for PLA, PBAT, PBS, and starch-blend films in carry bags, food-service ware, and compostable packaging mandated under single-use plastic substitution policies.

- Non-biodegradable bio-based plastics at 43.2% (2025) include Bio-PE, Bio-PET, bio-PP, and polyamide variants used by FMCG, beverage, and personal-care brands seeking renewable-feedstock alternatives without altering existing recycling infrastructure.

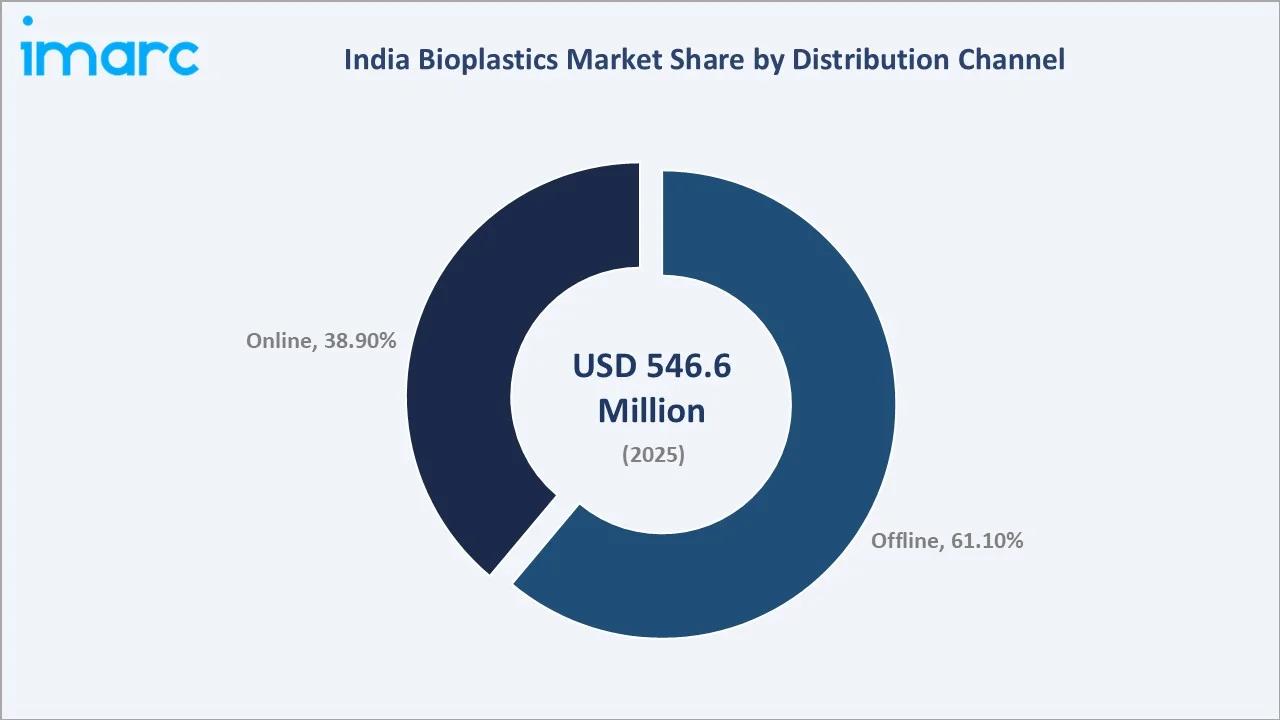

- Offline distribution at 61.1% (2025) remains dominant, supported by traditional B2B contracts between resin producers and converters, modern trade retail packaging supply, and institutional buyers including municipal corporations and government departments.

- Online distribution at 38.9% (2025) is the fastest-growing channel at approximately 22.50% CAGR, fueled by quick-commerce platforms, e-commerce packaging demand, and direct-to-consumer compostable product brands serving urban metro consumers.

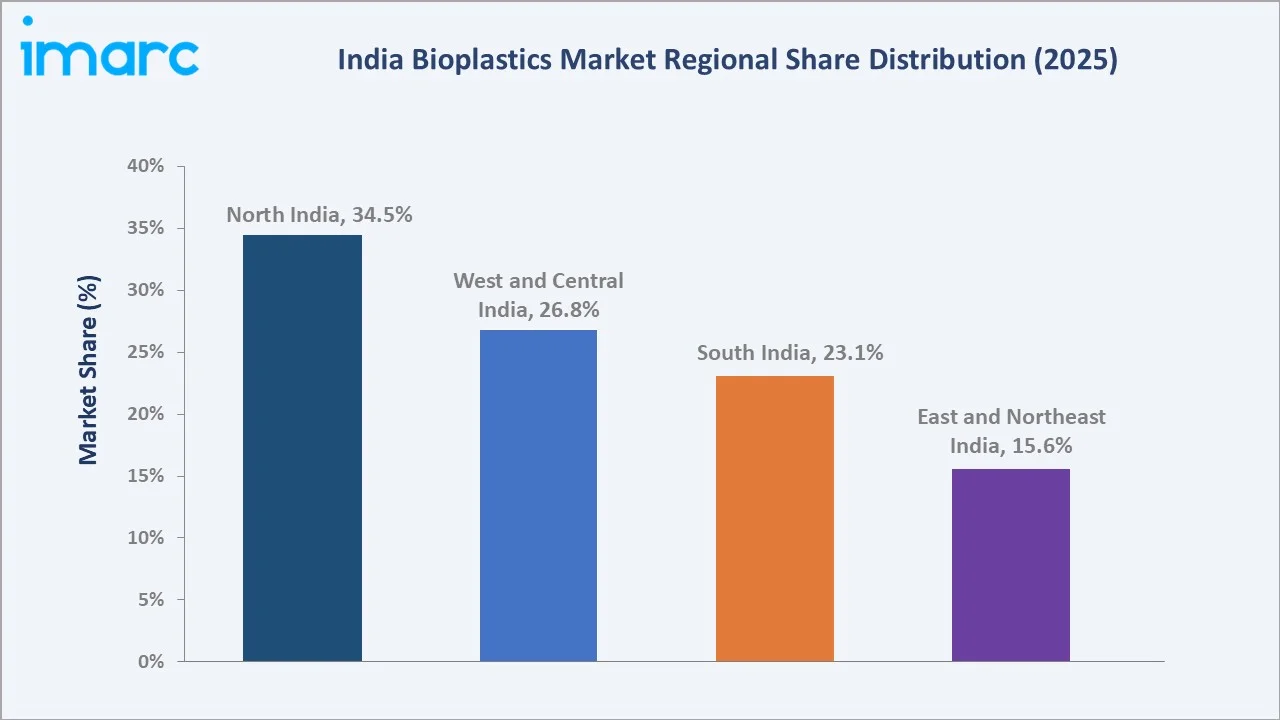

- North India at 34.5% (2025) leads regional share, anchored by Delhi-NCR FMCG manufacturing clusters, strong policy enforcement on single-use plastics, and demand from quick-commerce and food-delivery operators across major urban centers.

India Bioplastics Market Overview

Bioplastics are polymer materials derived either fully or partly from renewable biomass feedstocks such as sugarcane, corn, cassava, and agricultural waste, or produced through bio-based fermentation routes. The category spans biodegradable variants designed to decompose under industrial or home composting conditions, and non-biodegradable bio-based variants that retain conventional polymer properties while reducing fossil dependency.

India's bioplastics ecosystem is shaped by abundant agricultural feedstock (sugarcane, corn, cassava starch), favorable policy environment, and a growing convergence between FMCG sustainability commitments and consumer awareness.

The Plastic Waste Management Amendment Rules and Extended Producer Responsibility framework have placed binding obligations on producers, importers, and brand owners, accelerating substitution toward bio-based and compostable formats. Despite progress, India remains structurally import-dependent for high-performance resins, with domestic capacity meeting only a fraction of demand.

Market Dynamics

To evaluate market opportunities, Request Sample

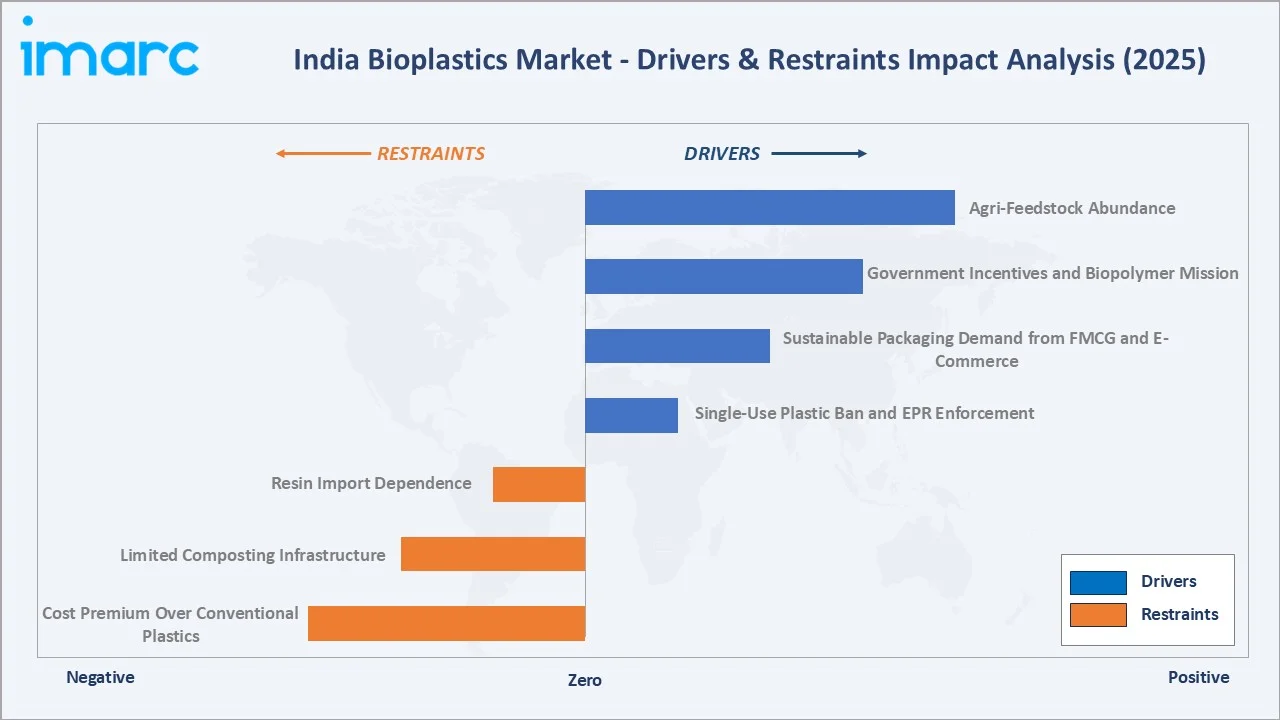

Market Drivers

- Single-Use Plastic Ban and EPR Enforcement: The Government of India's nationwide ban on identified single-use plastic items (effective July 2022) and Extended Producer Responsibility framework under the Plastic Waste Management Rules has created binding substitution demand. As per details provided by SPCB/PCC and the SUP compliance monitoring portal, 1,989 tons of banned single-use plastic items have been seized since July 2022.

- Sustainable Packaging Demand from FMCG and E-Commerce: Major FMCG brands, quick-commerce platforms, and food-service chains are committing to 100% recyclable or compostable packaging by 2025–2030. Around 36% of Indian consumers said they would pay “a lot more” for sustainable packaging, translating into structural demand from packaging converters and brand owners.

- Government Incentives and Biopolymer Mission: To support biodegradable alternatives and strengthen the national ban on identified single-use plastics, the GST on biodegradable bags has been reduced from 18% to 5% (effective September 2025). Praj Industries' Jejuri demonstration for lactic acid, lactide, and PLA represents the first integrated domestic biopolymer demonstration facility.

- Agri-Feedstock Abundance: India's position as one of the world's largest producers of sugarcane, corn, and cassava starch, combined with the availability of agri-residue and biomass, creates a strong feedstock advantage for cost-competitive bioplastics manufacturing.

Market Restraints

- Cost Premium Over Conventional Plastics: Bioplastics typically carry a 50-100% pricing premium over conventional polymers, and certain biodegradable variants such as PLA and PBAT can cost 2–3 times the price of equivalent petrochemical resins, limiting adoption in price-sensitive applications.

- Limited Composting Infrastructure: India has around 50 composting facilities nationally, restricting end-of-life processing for compostable bioplastics and creating waste management gaps for products marketed as biodegradable.

- Resin Import Dependence: India imports the majority of high-performance bioplastic resin demand, particularly PLA, PBAT, and PHA, from Thailand, China, and South Korea, exposing the domestic value chain to exchange-rate volatility and supply-chain disruption risk.

Market Opportunities

- Compostable Packaging for Quick-Commerce and Food Delivery: Quick-commerce platforms and food-delivery operators present significant opportunity for compostable carry bags, cutlery, and food containers, with select domestic compostable bag producers supplying major e-commerce, grocery, and food-delivery brands.

- Agricultural and Horticulture Applications: Biodegradable mulch films, plant pots, and agricultural twine present a high-growth use case aligned with crop yields and soil-health objectives, supported by state agriculture department procurement and farmer-producer organization pilots.

Market Challenges

- Consumer Awareness and Labelling Confusion: Distinctions between biodegradable, compostable, and oxo-degradable plastics remain poorly understood by end consumers, creating risk of misleading claims and the need for stronger certification regimes (ISO 17088, CPCB approval, TÜV OK Compost).

- Inconsistent Feedstock Quality and Pricing: Variability in agricultural feedstock quality and seasonal pricing fluctuations affect bioplastic production economics, requiring resilient supply contracts and feedstock diversification strategies.

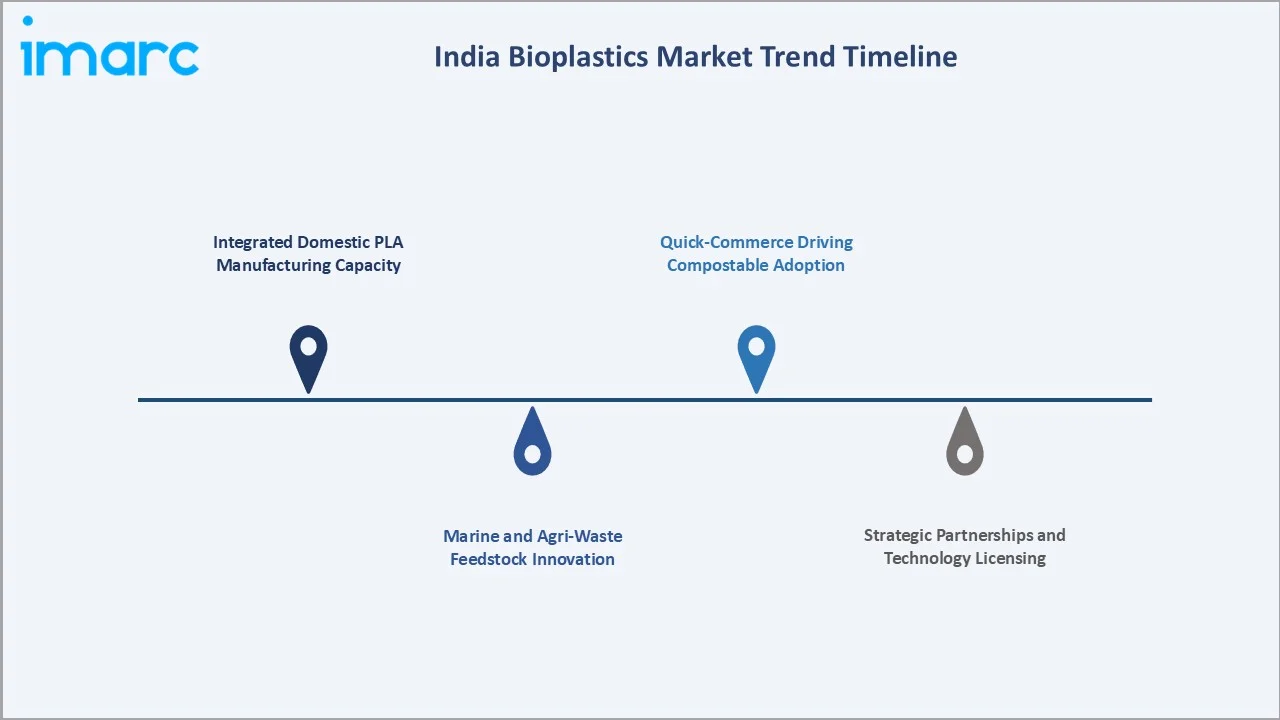

Emerging Market Trends

1. Integrated Domestic PLA Manufacturing Capacity

Balrampur Chini Mills laid the foundation stone for country's first integrated PLA bioplastic plant in 2025, leveraging sugarcane-based renewable feedstock conversion. Praj Industries' Jejuri demonstration facility, operational since 2024, produces 100 TPA of lactic acid and 60 TPA of lactide, equivalent to approximately 55 TPA of PLA.

2. Quick-Commerce and Food-Delivery Driving Compostable Adoption

Quick-commerce platforms, online grocery, and food-delivery operators are emerging as the largest growth drivers for compostable packaging. Major Indian compostable bag producers now supply leading e-commerce, grocery delivery, and food-delivery brands with PLA/PBAT carry bags and food-service ware, with annual production scaling beyond 3,000 tons for top suppliers and TÜV OK Compost certification adoption accelerating.

3. Strategic Partnerships and Technology Licensing

Indian bioplastic players are forming strategic alliances with global technology providers and value-chain partners. Reliance Industries Limited and CIPET are collaborating to develop new bioplastic materials and enhance production processes, while domestic companies are pursuing technology licensing agreements with international biopolymer leaders to accelerate scale-up of PLA, PHA, and PBAT manufacturing.

4. Marine and Agri-Waste Feedstock Innovation

Domestic players are advancing scalable biopolymer production from marine biomass, agri-waste, and starch for industrial packaging applications, with export-oriented pilots underway. Concurrent academic research at IIT-Guwahati and other institutes is yielding new bioplastic formulations targeting cost reduction, broader feedstock flexibility, and improved end-of-life performance.

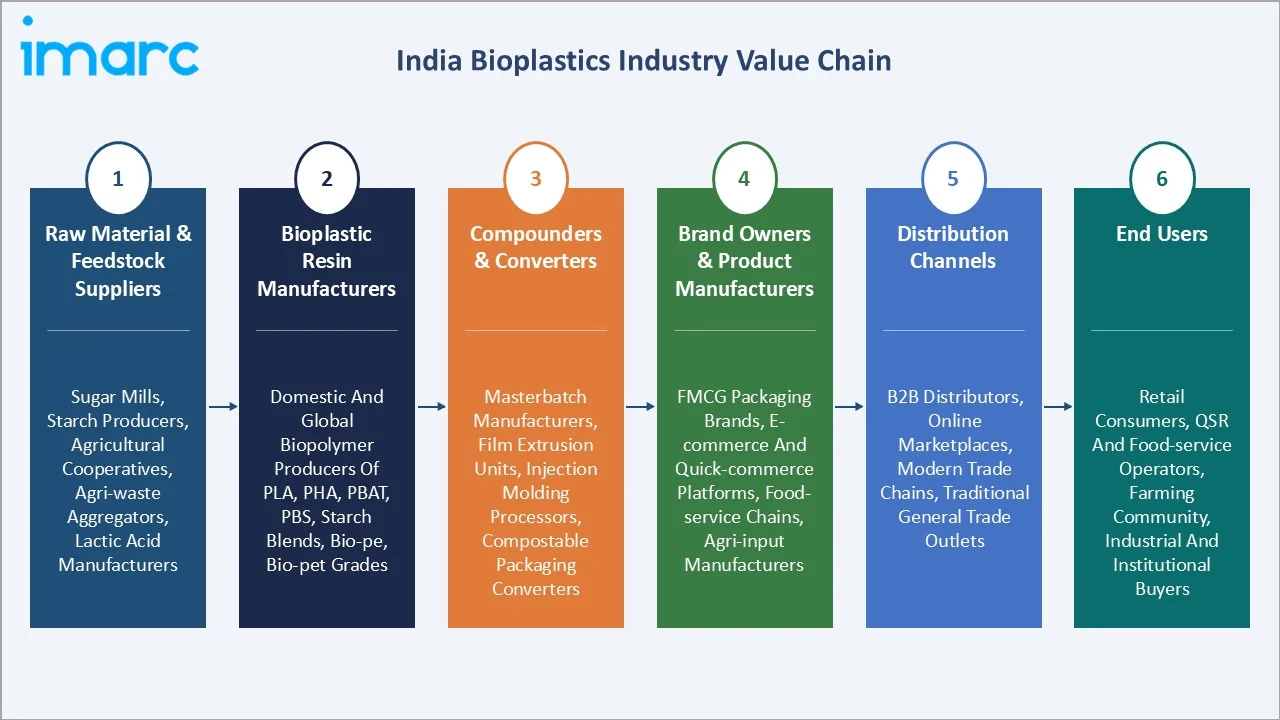

Industry Value Chain Analysis

|

Stage |

Key Players/Activities |

|

Raw Material & Feedstock Suppliers |

Sugar mills and starch producers, agricultural cooperatives, agri-waste aggregators, lactic acid manufacturers |

|

Bioplastic Resin Manufacturers |

Domestic and global biopolymer producers of PLA, PHA, PBAT, PBS, starch blends, Bio-PE, and Bio-PET grades |

|

Compounders & Converters |

Masterbatch manufacturers, film extrusion units, injection molding processors, compostable packaging converters |

|

Brand Owners & Product Manufacturers |

FMCG packaging brands, e-commerce and quick-commerce platforms, food-service chains, agri-input manufacturers |

|

Distribution Channels |

B2B distributors, online marketplaces, modern trade chains, traditional general trade outlets |

|

End Users |

Retail consumers, QSR and food-service operators, farming community, industrial and institutional buyers |

Technology Landscape in the India Bioplastics Industry

Polylactic Acid (PLA) and Starch-Based Bioplastics

PLA, derived from sugarcane, corn starch, or cassava through lactic acid fermentation and polymerization, dominates India's biodegradable category alongside starch-blend formulations. PLA offers transparency, rigidity, and industrial composability, making it suitable for food packaging, cutlery, and 3D-printing filaments. India's first integrated PLA plant by Balrampur Chini Mills and Praj Industries' Jejuri demonstration facility (under construction at Kumbhi, UP) represent flagship domestic technology platforms.

Polyhydroxyalkanoates (PHA) and Next-Generation Biopolymers

PHA, produced through microbial fermentation, offers full marine and home biodegradability and is emerging as a premium biopolymer for high-value applications. Indian R&D programs, supported by institutes such as IIT-Guwahati and the Institute of Chemical Technology, are advancing PHA strain engineering, fermentation efficiency, and downstream processing to reduce cost.

Polybutylene Adipate Terephthalate (PBAT) and Blends

PBAT delivers flexibility, toughness, and biodegradability under industrial composting conditions, and is typically blended with PLA or starch to produce carry bags and flexible film packaging. PBAT capacity expansion is critical to India's carry-bag substitution targets, with several domestic and joint-venture projects under development.

Bio-Based Drop-In Polymers (Bio-PE, Bio-PET)

Bio-based drop-in polymers derived from sugarcane ethanol (Bio-PE) and bio-MEG (Bio-PET) retain the mechanical and recycling properties of conventional polyolefins while reducing fossil-fuel dependency. These polymers serve FMCG and beverage brands seeking renewable-content claims without altering existing recycling infrastructure.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Biodegradable |

56.8% |

2025 |

|

Distribution Channel |

Offline |

61.1% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

North India |

34.5% |

2025 |

By Product

Biodegradable bioplastics dominate with a 56.8% share in 2025, encompassing PLA, PBAT, PBS, PHA, and starch blends used in carry bags, food-service ware, mulch films, and compostable packaging. Demand is anchored by mandatory single-use plastic substitution under Plastic Waste Management Rules, with TÜV OK Compost and CPCB certification accelerating institutional adoption.

To access detailed market analysis, Request Sample

Non-biodegradable plastics account for 43.2% in 2025, comprising polyamide variants used by FMCG and beverage brands seeking renewable-feedstock alternatives. These bio-based drop-in polymers retain conventional polymer properties and integrate with existing recycling infrastructure, supporting circular-economy commitments without operational disruption.

By Distribution Channel

Offline distribution leads with a 61.1% share in 2025, supported by traditional B2B contracts between resin producers and packaging converters, modern trade retail packaging supply, and institutional procurement by municipal corporations and government departments. Distributor and wholesaler networks remain central to industrial and commercial bioplastic sales across major Indian states.

Online distribution captures 38.9% of the market in 2025 and is the fastest-growing channel at approximately 22.50% CAGR, fueled by quick-commerce platforms, e-commerce packaging demand, direct-to-consumer compostable product brands, and B2B online marketplaces.

Regional Market Insights

North India leads at 34.5% in 2025, supported by Delhi-NCR's FMCG manufacturing cluster, strong policy enforcement on single-use plastics, and high concentration of quick-commerce and food-delivery operators driving compostable packaging demand. Punjab, Haryana, and Uttar Pradesh add agricultural feedstock advantages for sugarcane- and corn-based biopolymer production.

West and Central India at 26.8% holds the second-largest share, anchored by Maharashtra and Gujarat's industrial clusters and the presence of leading biopolymer R&D and demonstration plants, including Praj Industries' Jejuri facility.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

34.5% |

FMCG and packaging manufacturing hub; strong single-use plastic ban enforcement; quick-commerce density; agricultural feedstock base |

|

West and Central India |

26.8% |

Industrial cluster; presence of leading biopolymer R&D and demonstration plants; rising consumer goods market; sugarcane availability |

|

South India |

23.1% |

Strong sugar and starch industry base; growing e-commerce demand; FMCG and food-service expansion; institutional sustainability adoption |

|

East and Northeast India |

15.6% |

Emerging adoption with rising state-level policy enforcement; tea, jute, and agricultural sectors providing feedstock potential; High FMCG and retail demand |

South India at 23.1% benefits from sugar and starch industry concentration, while East and Northeast India at 15.6% reflects emerging adoption with rising regulatory enforcement and feedstock potential from the tea, jute, and agricultural sectors.

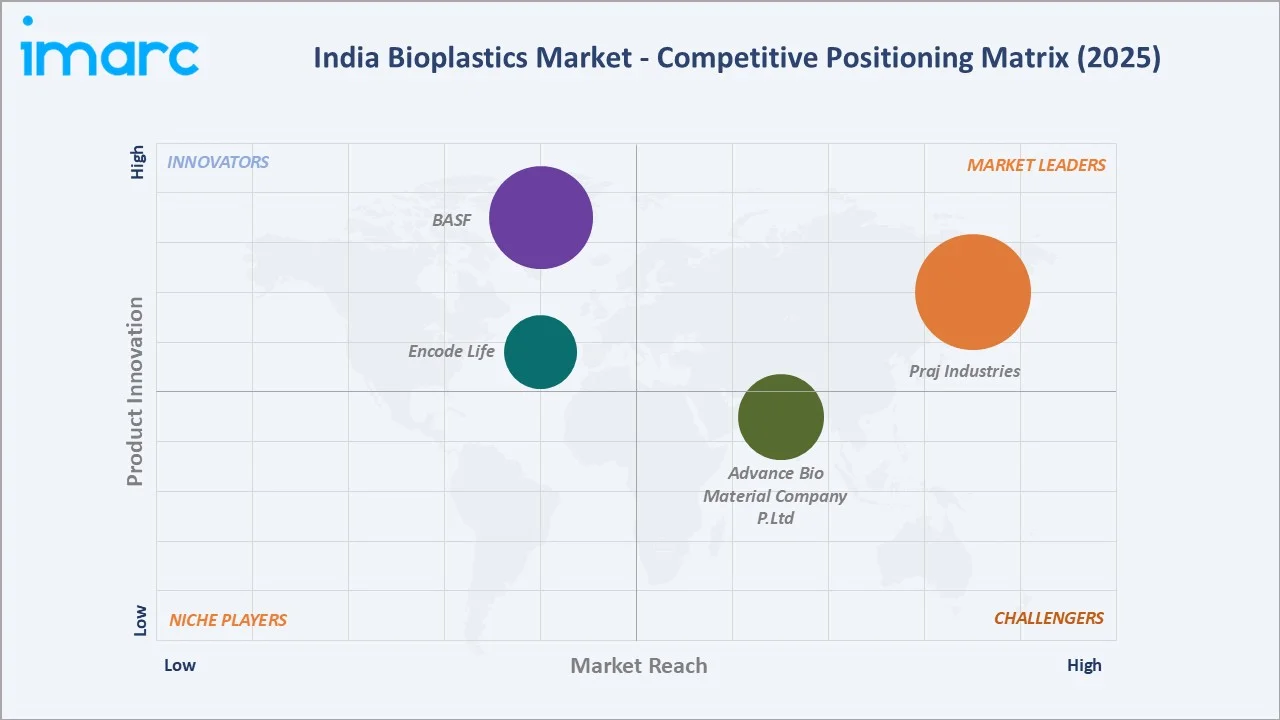

Competitive Landscape

India's bioplastics market is moderately fragmented, with leading players spanning domestic biopolymer specialists, large diversified industrial conglomerates, and Indian operations of multinational chemical companies. Key players include Praj Industries, BASF, Advance Bio Material Company P.Ltd, and Encode Life.

|

Company Name |

Brands |

Market Position |

Core Strength |

|

Praj Industries |

BioPrism |

Market Leader |

Integrated lactic acid, lactide, and PLA production capability; biopolymer demonstration plant; strong industrial biotechnology platform |

|

BASF |

ecoflex, ecovio |

Innovator |

Ecoflex (PBAT) and ecovio compostable polymer brands; technology partnerships with Indian converters; advanced biopolymer formulations |

|

Advance Bio Material Company P.Ltd |

ADFLEX |

Emerging Player |

Fully integrated bioplastics process; resins are 100% compostable and biodegradable within 180 days |

|

Encode Life |

Encode Life |

Early-Stage Innovator |

Establishing industrial-scale PLA biopolymer plant; comprehensive end-of-life solutions |

The competitive structure reflects a balance between integrated upstream resin producers and downstream compostable-product specialists.

Key Company Profiles

Praj Industries

Praj Industries, headquartered in Pune, Maharashtra, is a leading Indian process engineering and industrial biotechnology company. Praj operates an integrated biopolymer demonstration facility at Jejuri and the Parimal and Pramod Chaudhari Centre of Excellence and Innovation for Biopolymers (PPC-COEI) at the Institute of Chemical Technology, Mumbai.

- Product Portfolio: Lactic acid, lactide, polylactic acid (PLA), and emerging PHA bioplastic technology platforms; bioethanol and biorefinery solutions.

- Recent Developments: In April 2025, Praj Industries and thyssenkrupp Uhde's polymer subsidiary Uhde Inventa-Fischer (UIF) formed a strategic partnership to jointly offer end-to-end integrated technology for PLA production. The collaboration combines Praj’s lactic acid technology with UIF’s PLAneo process to support cost-effective and sustainable bioplastic manufacturing.

- Strategic Focus: Integrated biopolymer production technology; end-to-end PLA value chain leadership; PHA commercialization; partnerships with global technology providers for accelerated scale-up.

Advance Bio Material Company P.Ltd

Advance Bio Material Company P.Ltd, headquartered in Mulund West, Mumbai, Maharashtra, is an integrated Indian bioplastics manufacturer dedicated to developing high-performance compostable polymers and sustainable packaging solutions.

- Product Portfolio: ADFLEX-FT1 / FT2, ADFLEX-FT3, ADFLEX-FT4 / FT4-Clear, ADFLEX-FT5, ADFLEX-FT6, ADFLEX FT-IBM, and ADFLEX FT-CP.

- Strategic Focus: Advance Bio Material's strategy centers on being a fully vertically integrated bioplastics company, enabling it to serve the entire packaging supply chain with compostable alternatives to single-use plastic.

Market Concentration Analysis

India's bioplastics market is moderately fragmented. The market is structurally bifurcated: large industrial conglomerates (Praj Industries) and global technology leaders (BASF) focus on upstream resin production and bio-based drop-in polymers, while specialist compostable-product companies dominate downstream converted-product segments.

Investment & Growth Opportunities

Fastest Growing Segments

- Biodegradable bioplastics (PLA, PBAT, PHA) are projected to grow at approximately 20.40% CAGR through 2034, supported by mandatory single-use plastic substitution and FMCG sustainability commitments.

- The online distribution channel is the fastest-growing channel at approximately 22.50% CAGR, driven by quick-commerce, e-commerce, and direct-to-consumer compostable product brands.

Emerging Market Expansion

- Quick-commerce and food-delivery platforms present concentrated near-term demand for compostable carry bags, cutlery, and food containers, with major operators rapidly transitioning to certified compostable formats.

- Agricultural and horticulture applications (biodegradable mulch films, plant pots, twine) offer expansion potential supported by state agriculture department procurement and farmer-producer organization pilots.

Venture and Institutional Investment Trends

- Domestic resin manufacturing investments, including the foundation laying of Balrampur Chini Mills' first integrated PLA plant in February 2025 and announced PBAT capacity additions, are expected to reduce import dependence.

- Strategic alliances with global bioplastics technology providers and Indian converters are accelerating technology transfer, with international PLA and PBAT producers seeking joint ventures with Indian feedstock owners.

Future Market Outlook (2026-2034)

India's bioplastics market is positioned for sustained, policy-led expansion through 2034. From USD 546.6 Million in 2025, the market is projected to reach USD 2,672.5 Million by 2034, representing incremental value of approximately USD 2,125.9 Million at an 18.71% CAGR, increasingly composed of domestic PLA, PBAT, and PHA production capacity alongside compostable converted-product platforms.

Biodegradable bioplastics are expected to expand their share toward 60.0% by 2034 as PBAT and PLA capacity scales and compostable substitution accelerates in carry bags and food-service ware. North India will retain regional leadership, while the share of domestic resin production will rise materially as new integrated plants come online. Industrial composting infrastructure scaling, EPR enforcement maturity, and quick-commerce platform demand will collectively drive sustained investment.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, comprising Indian biopolymer manufacturers, compostable product converters, FMCG packaging buyers, quick-commerce operators, certification bodies, and policy stakeholders, validating market sizing, segmentation, regional shares, and adoption trends.

Secondary Research

Secondary research covered Ministry of Environment, Forest and Climate Change publications, Central Pollution Control Board data, Plastic Waste Management Rules and EPR notifications, company annual reports, industry association publications, and research publications from IIT-Guwahati, Institute of Chemical Technology Mumbai, and CIPET.

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating policy-driven substitution rates, domestic capacity additions, import volumes, end-use application growth, and FMCG sustainability commitments. The 18.71% CAGR reflects validation against announced domestic resin plant pipelines, EPR enforcement timelines, and quick-commerce platform sustainability commitments through 2034.

India Bioplastics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Applications Covered | Flexible Packaging, Rigid Packaging, Agriculture and Horticulture, Consumer Goods, Textile, Automotive and Transportation, Others |

| Distribution Channels Covered | Online, Offline |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Praj Industries, BASF, Advance Bio Material Company P.Ltd, Encode Life, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India bioplastics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India bioplastics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India bioplastics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Bioplastics Market Report

The India bioplastics market reached USD 546.6 Million in 2025 and is projected to reach USD 2,672.5 Million by 2034.

The market is expected to grow at a CAGR of 18.71% during 2026-2034, driven by single-use plastic ban enforcement, FMCG sustainable packaging demand, and domestic resin capacity expansion.

North India leads with a 34.5% share in 2025, supported by Delhi-NCR's FMCG manufacturing cluster and strong single-use plastic ban enforcement.

Biodegradable bioplastics dominate with a 56.8% share in 2025, encompassing PLA, PBAT, PBS, PHA, and starch-blend films used in carry bags and food-service ware.

Offline distribution holds 61.1%, supported by B2B contracts between resin producers and converters, modern trade supply, and institutional procurement.

Key players include Praj Industries, BASF, Advance Bio Material Company P.Ltd, and Encode Life.

Online distribution is growing at approximately 22.50% CAGR through 2034, driven by quick-commerce platforms, e-commerce packaging demand, and direct-to-consumer compostable product brands.

Key challenges include cost premium over conventional plastics, limited industrial composting infrastructure, resin import dependence, and consumer awareness and labelling clarity.

Domestic PLA, PBAT, and PHA manufacturing capacity expansion, compostable packaging for quick-commerce, and agricultural mulch film applications represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)