India Dairy Alternatives Market Size, Share, Trends and Forecast by Source, Formulation, Nutrient, Distribution Channel, Product Type, and Region, 2026-2034

India Dairy Alternatives Market Size, Share, Trends & Forecast (2026-2034)

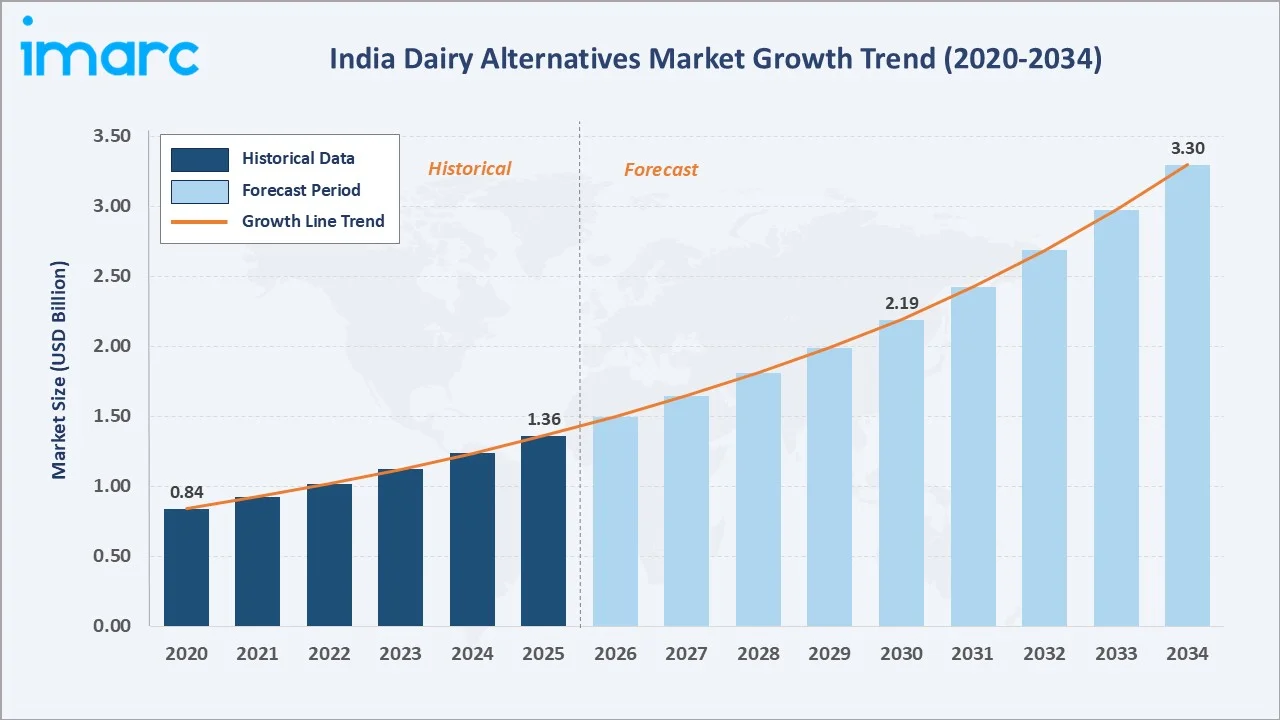

The India dairy alternatives market reached USD 1.36 Billion in 2025 and is projected to reach USD 3.30 Billion by 2034, exhibiting a CAGR of 10.04% during 2026-2034. Growth is anchored by the high prevalence of lactose intolerance across India, rising vegan and flexitarian consumer adoption, urban premiumization through quick-commerce platforms, FSSAI plant-based food regulatory clarity, and FMCG investment in plant-based product launches across milk, yogurt, cheese, and butter categories.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.36 Billion |

|

Market Forecast (2034) |

USD 3.30 Billion |

|

CAGR (2026-2034) |

10.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

Rising lactose intolerance, growing vegan and flexitarian diets, increasing awareness of animal welfare, and demand for clean-label nutrition are supporting the adoption of alternatives such as soy milk, almond milk, oat milk, coconut milk, and plant-based yogurt, cheese, and desserts.

To get more information on this market, Request Sample

The market is also benefiting from urbanization, premiumization, e-commerce growth, and wider availability of innovative dairy-free products across supermarkets, health food stores, cafés, and online platforms.

Executive Summary

India's dairy alternatives market is among the fastest-growing plant-based food categories in Asia, expanding at a 10.04% CAGR through 2034 amid structural demand from lactose-intolerant consumers (60% of the population), rising vegan and flexitarian adoption, and FMCG-led brand investment in plant-based milk, yogurt, cheese, and butter formats.

The market is structurally fragmented, with the top four companies collectively holding approximately 6.88% revenue share, creating substantial room for new entrants, premium niche brands, and direct-to-consumer specialists. Key 2024–2025 milestones include Country Delight's entry into the plant-based beverage market with a new Oats Beverage (June 2025) and Maiva Fresh's unsweetened almond milk debut (September 2024).

Key Market Insights

|

Indicator |

Value (2025) |

|

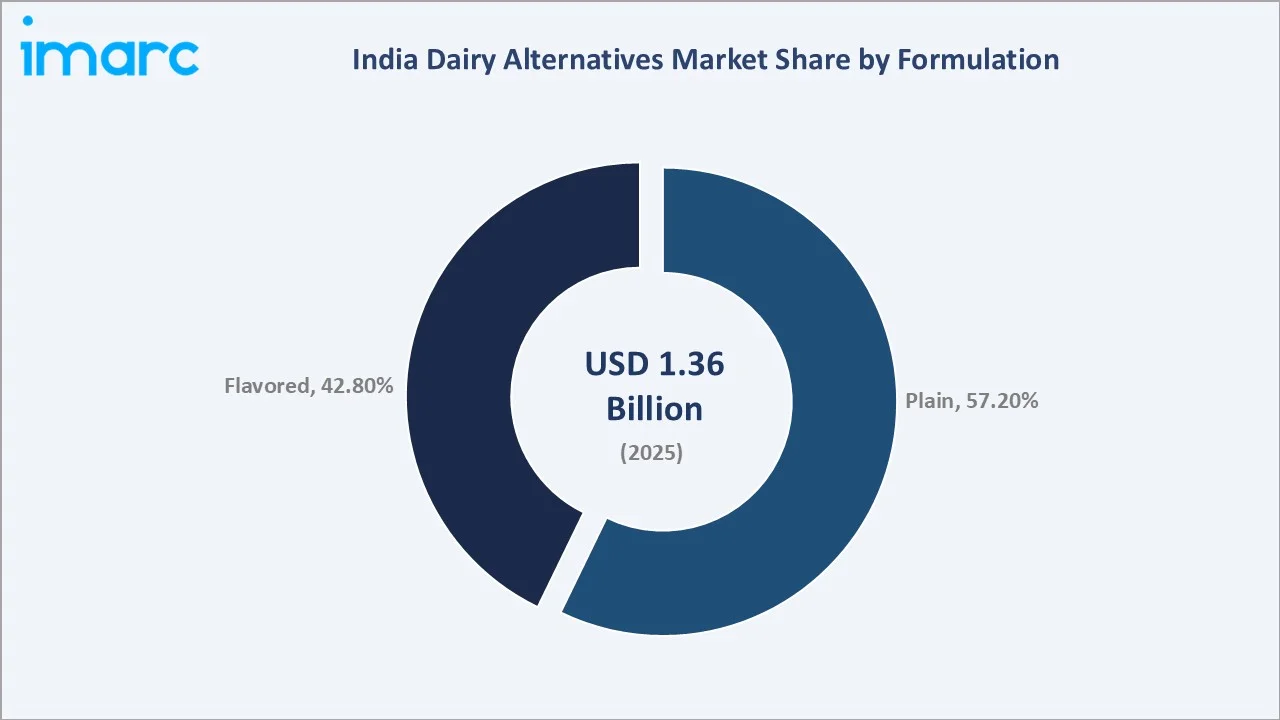

Leading Formulation |

Plain (57.2%) |

|

Fastest-Growing Formulation |

Flavored (~11.0% CAGR) |

|

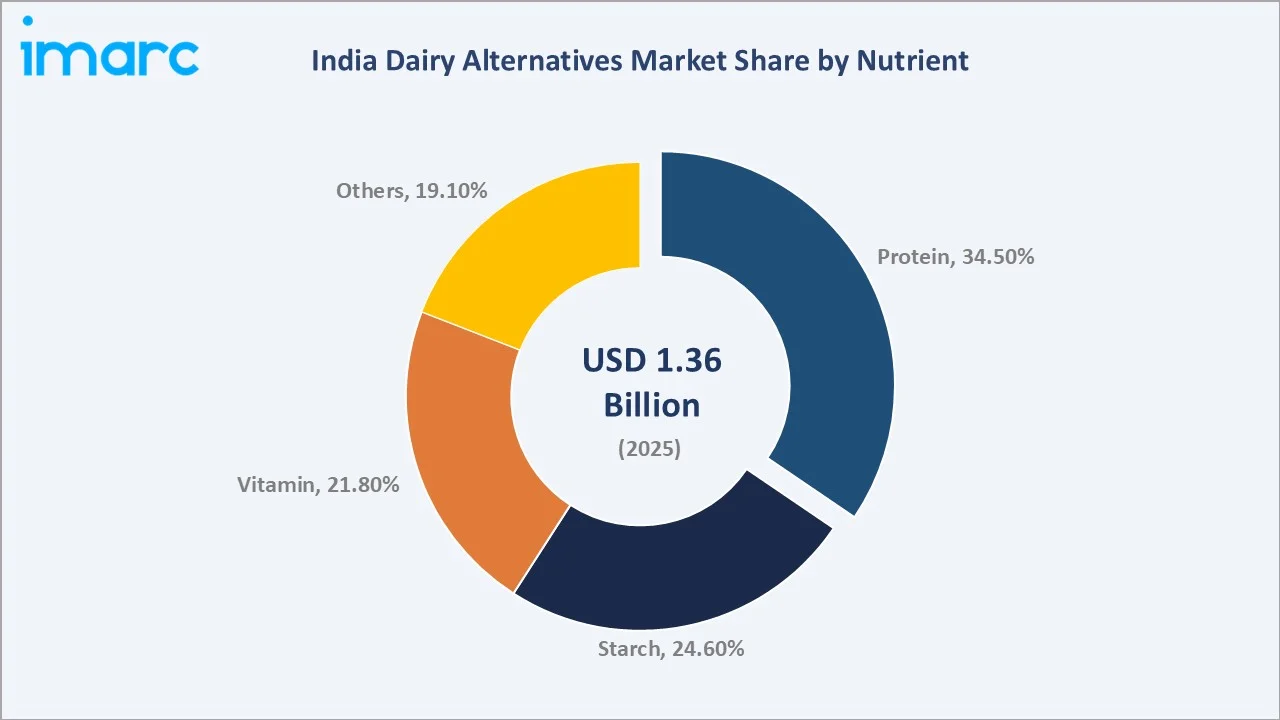

Leading Nutrient |

Protein (34.5%) |

|

Fastest-Growing Nutrient |

Protein (~12.0% CAGR) |

|

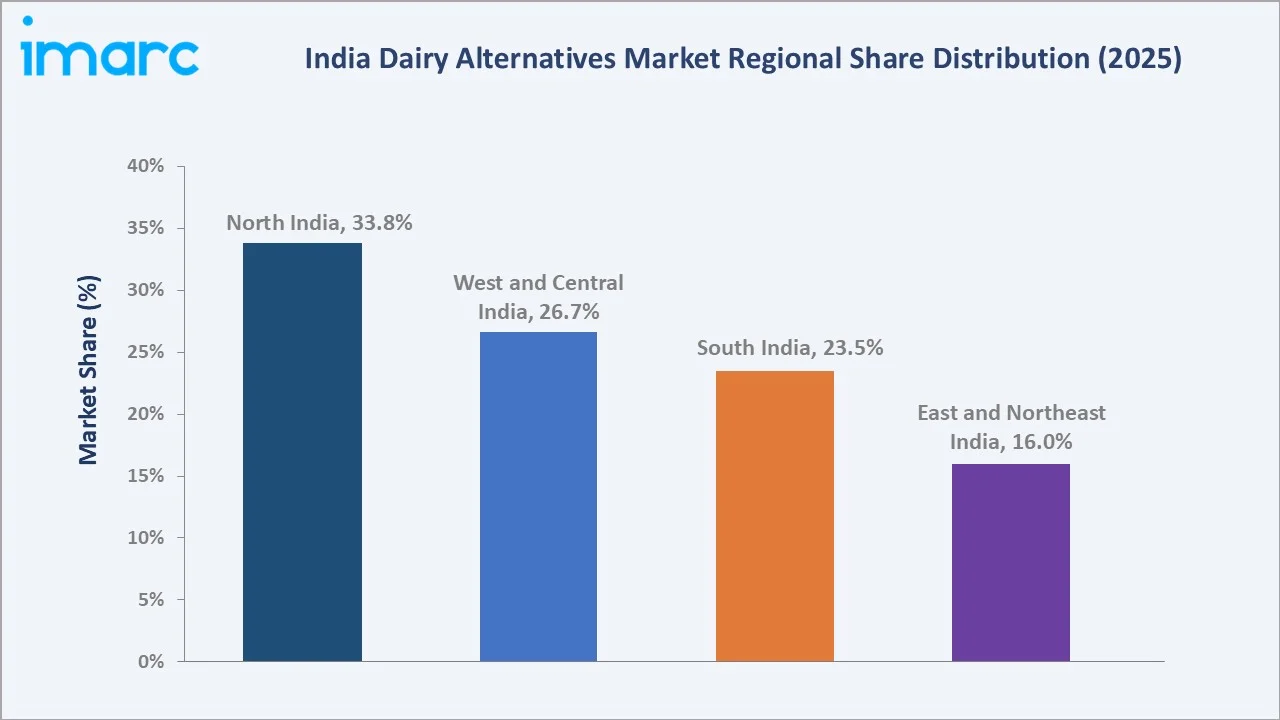

Largest Region |

North India (33.8%) |

|

Key Players |

Drums Food International Private Limited, The Hershey Company, Nourish You, Naturise Consumer Products Pvt Ltd |

Key Analytical Observations Supporting the Above Data:

- Plain formulation accounts for 57.2% of the India dairy alternatives market in 2025, reflecting consumer preference for unflavored plant-based milk variants used in cooking, coffee, tea, and as direct dairy substitutes by lactose-intolerant and health-conscious urban consumers.

- Flavored formulations at 42.8% capture demand for ready-to-drink beverages, chocolate and vanilla plant-based milks, flavored yogurts, and protein-fortified drinks targeting younger consumers, fitness segments, and convenience-driven occasions.

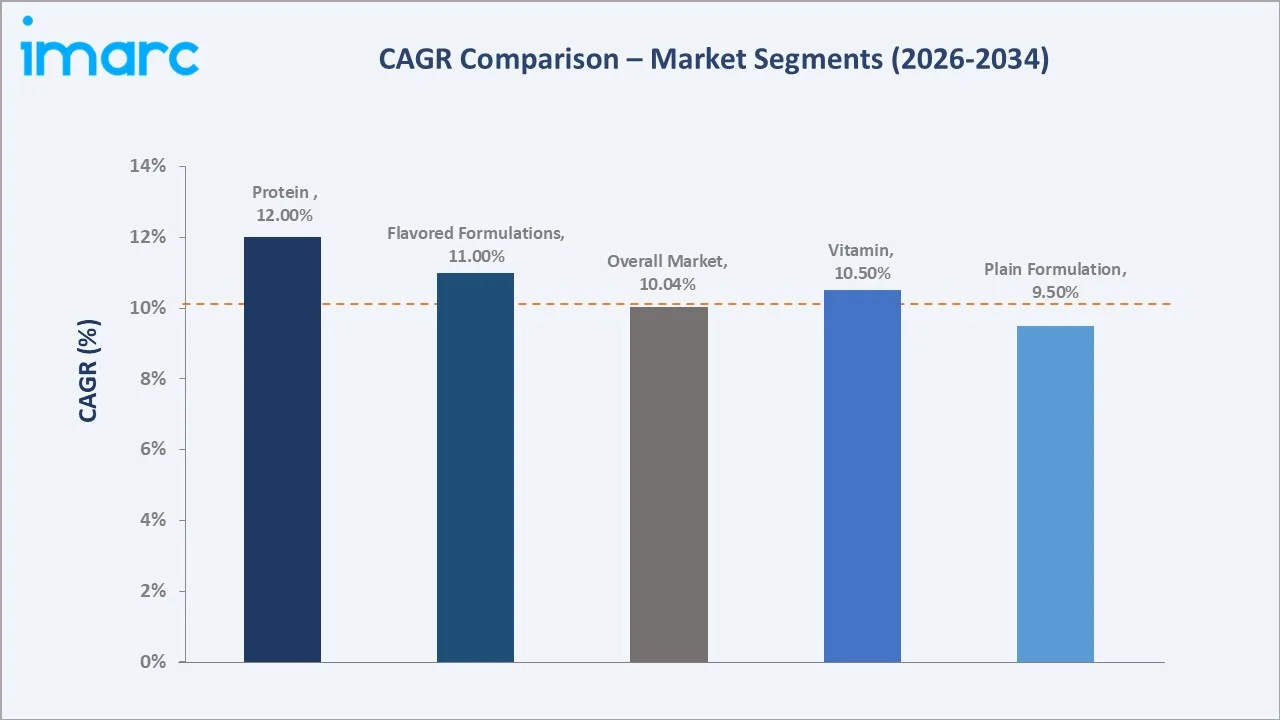

- Protein-fortified nutrient profiles lead at 34.5% in 2025 and are projected to grow at approximately 12.0% CAGR through 2034, supported by rising functional nutrition demand, fitness-led consumption patterns, and brand investment in protein-positioned plant-based beverages.

- Starch-based variants at 24.6% include oat, millet, and rice-based products that capitalize on indigenous Indian grains and natural creaminess, with Country Delight's June 2025 oat beverage entry signaling category expansion.

- North India's 33.8% regional share reflects strong concentration of urban premium consumers in Delhi-NCR, robust quick-commerce density, and established modern trade retail penetration for refrigerated dairy alternatives.

India Dairy Alternatives Market Overview

Dairy alternatives are plant-based food and beverage products designed to replicate the sensory, nutritional, and functional characteristics of conventional dairy. The Indian category spans plant-based milk (soy, almond, oat, coconut, cashew, millet), yogurt, cheese, butter, ice cream, frozen desserts, and protein beverages, formulated to serve lactose-intolerant consumers, vegan and flexitarian dietary segments, and broader health and wellness-driven buyers.

Approximately 60% of the Indian population experiences some form of lactose intolerance, creating large structural demand for dairy alternatives across urban metros and Tier-2 cities. FSSAI has introduced plant-based food guidelines to standardize labelling and product safety, while the Plant-Based Foods Industry Association continues to advocate for category expansion through awareness initiatives and investment facilitation. The competitive landscape includes domestic specialists, large diversified FMCG players, and global brands operating in India.

Market Dynamics

To evaluate market opportunities, Request Sample

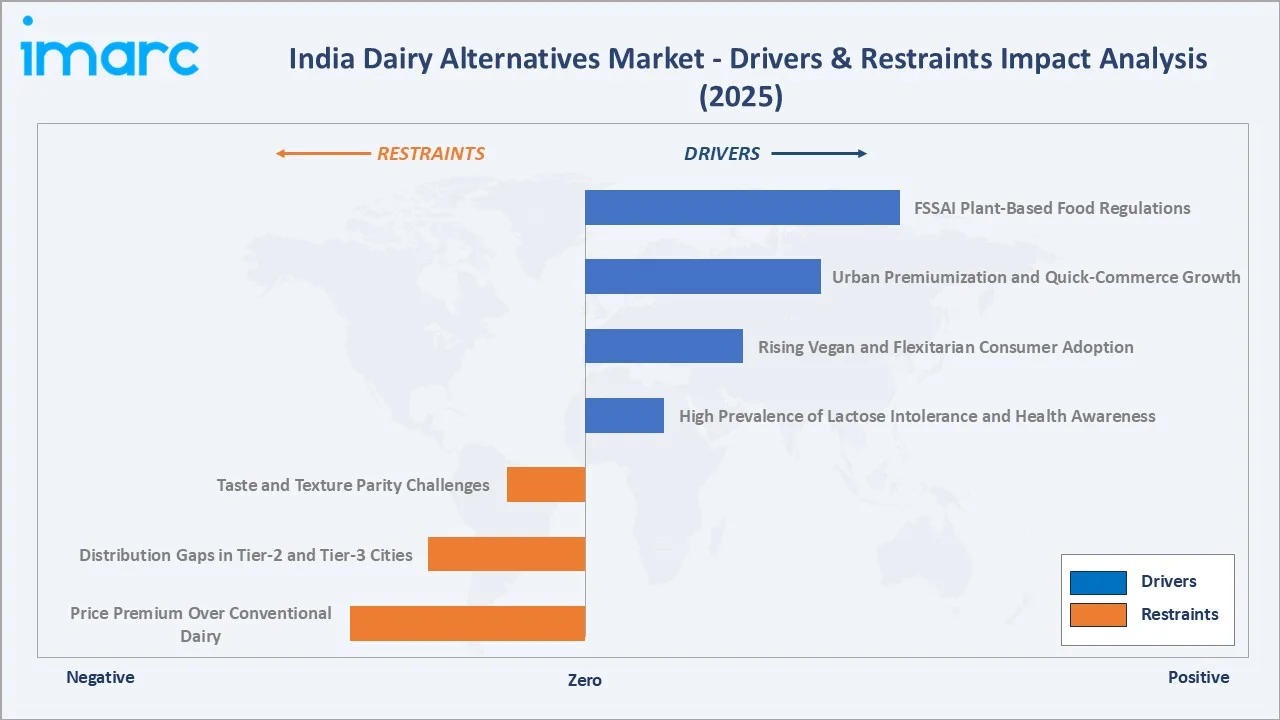

Market Drivers

- High Prevalence of Lactose Intolerance and Health Awareness: Approximately 60% of India's population experiences lactose intolerance, generating sustained demand for plant-based milk and yogurt alternatives. Rising awareness of cholesterol management, weight control, and digestive health is accelerating substitution among health-conscious urban consumers.

- Rising Vegan and Flexitarian Consumer Adoption: Growing vegan and flexitarian dietary preferences, particularly in metro cities including Delhi, Mumbai, Bangalore, and Pune, are driving structural demand. Advocacy organizations including the Plant-Based Foods Industry Association and Good Food Institute India (GFI India) are accelerating consumer awareness and category visibility.

- Urban Premiumization and Quick-Commerce Growth: Quick-commerce platforms such as Blinkit, Zepto, and Swiggy Instamart are expanding 10–15 minute delivery of fresh refrigerated plant-based products. Quick commerce currently represents nearly half of online grocery sales and is expected to account for around two-thirds of the segment by 2030.

- FSSAI Plant-Based Food Regulations: FSSAI has introduced standardized plant-based food guidelines, providing regulatory clarity on labelling, ingredients, and safety. Combined with national vegan food rules, this supports manufacturer scale-up, retail listing, and consumer confidence.

Market Restraints

- Price Premium Over Conventional Dairy: Plant-based milk and yogurt typically retail at 2–3 times the price of equivalent dairy products, limiting accessibility in price-sensitive segments and constraining penetration beyond urban metros and affluent consumer cohorts.

- Distribution Gaps in Tier-2 and Tier-3 Cities: Distribution gaps in tier-2 and tier-3 cities remain a key restraint for the India dairy alternatives market, as plant-based milk, yogurt, and cheese products are still concentrated mainly in metros and premium retail channels. Lower consumer awareness, higher price sensitivity, and weaker availability across local stores restrict wider adoption beyond urban centers.

- Taste and Texture Parity Challenges: Plant-based variants struggle to replicate the casein protein structure essential for foam stability in coffee, creaminess in desserts, and stretch in cheese applications, creating product performance gaps in foodservice and culinary applications.

Market Opportunities

- Millet and Indigenous Grain-Based Formulations: Brands including Urban Platter and One Good are leveraging millet, oat, and indigenous grain formulations to deliver natural creaminess, sustainable feedstock advantages, and alignment with India's International Year of Millets positioning.

- Protein-Fortified Functional Beverages: Hershey India Private Limited’s Sofit plant protein drink and similar functional protein offerings target fitness, weight management, and meal replacement use cases. The protein nutrient segment is projected to grow at approximately 12.0% CAGR through 2034.

Market Challenges

- Consumer Awareness and Category Education: Many Indian consumers remain unfamiliar with the nutritional positioning, applications, and benefits of plant-based dairy alternatives. Brand education investment and sampling-led marketing remain critical to expanding the addressable base.

- Cold-Chain Logistics for Fresh Variants: Fresh refrigerated plant-based products require robust cold-chain infrastructure, which remains uneven across India, particularly in Tier-2 and Tier-3 markets, limiting retail expansion and increasing inventory risk for converters.

Emerging Market Trends

1. Plant-Based Yogurt and Probiotic Innovation

In June 2020, Epigamia launched its dairy-free coconut yogurt with improved texture achieved through probiotic fermentation, anchoring the plant-based cultured-dairy segment. Maiva Fresh introduced its unsweetened almond milk in September 2024, while Hershey India Private Limited (subsidiary of The Hershey Company) developed Sofit Plus soy protein drink as part of a 2021 CSR initiative for underprivileged children.

2. Millet, Oat, and Indigenous Grain Formulations

Indigenous grain-based formulations are gaining traction. Country Delight's June 2025 oats beverage entry, alongside Urban Platter’s and One Good's millet-based product lines, capitalize on India's International Year of Millets positioning and natural creaminess. These formulations offer lower water footprint, domestic feedstock advantages, and alignment with consumer sustainability expectations.

3. Strategic Consolidation and M&A Activity

Nourish You acquired 100% of Bengaluru-based plant-based dairy startup One Good, marking one of India’s largest alternative-dairy M&A deals. The acquisition strengthens Nourish You’s plant-based portfolio by combining its millet milk and retail presence with One Good’s vegan milk, yoghurt, butter, ghee, and cheese alternatives.

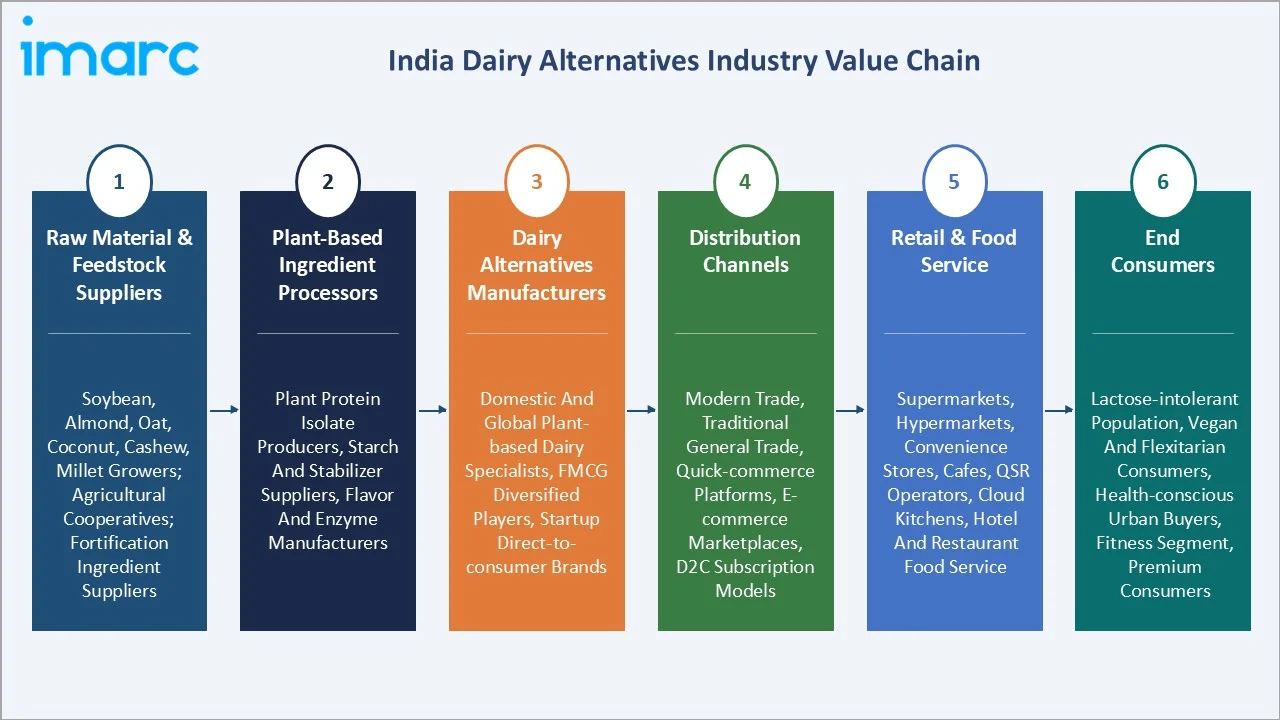

Industry Value Chain Analysis

|

Stage |

Key Players / Activities |

|

Raw Material & Feedstock Suppliers |

Soybean, almond, oat, coconut, cashew, and millet growers; agricultural cooperatives; fortification ingredient suppliers |

|

Plant-Based Ingredient Processors |

Plant protein isolate producers, starch and stabilizer suppliers, flavor and enzyme manufacturers |

|

Dairy Alternatives Manufacturers |

Domestic and global plant-based dairy specialists, FMCG diversified players, and startup direct-to-consumer brands |

|

Distribution Channels |

Modern trade chains, traditional general trade outlets, quick-commerce platforms, e-commerce marketplaces, direct-to-consumer subscription models |

|

Retail & Food Service |

Supermarkets, hypermarkets, convenience stores, cafes, QSR operators, cloud kitchens, hotel and restaurant food service |

|

End Consumers |

Lactose-intolerant population, vegan and flexitarian consumers, health-conscious urban buyers, fitness segment, premium consumers |

Technology Landscape in the India Dairy Alternatives Industry

Soy-Based Platforms

Soy-based dairy alternatives represent India's most established plant-based segment, supported by abundant domestic soybean cultivation and decades of consumer familiarity with soy milk and soy-based foods. Brands deliver protein-rich alternatives for everyday consumption, with established supply chains across Madhya Pradesh, Maharashtra, and Rajasthan supporting cost-competitive production.

Almond, Coconut, and Cashew-Based Variants

Almond-based platforms have gained substantial traction in urban premium segments, supported by nutritional positioning around vitamin E and low-calorie profiles. Coconut and cashew-based variants serve premium dessert, yogurt, and barista applications. Sofit, So Good, and Epigamia anchor almond milk availability across Mumbai, Delhi, and Bangalore retail.

Oat and Millet-Based Innovation

Oat and millet-based formulations represent the highest-growth innovation segment, leveraging indigenous grain creaminess and low water footprint. Country Delight's June 2025 oats beverage, Urban Platter and One Good millet-based offerings, and emerging startup launches collectively scale this segment.

Plant-Based Yogurt, Cheese, and Butter Technologies

Plant-based cultured-dairy technologies enable yogurt, cheese, and butter alternatives. Epigamia's dairy-free coconut yogurt, supported by probiotic fermentation, exemplifies the segment, while emerging plant-based cheese and butter brands target premium and HoReCa channels. Precision fermentation and high-pressure processing technologies are being explored to improve sensory parity.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Formulation | Plain | 57.2% | 2025 |

| Nutrient | Protein | 34.5% | 2025 |

| Source | 🔒 | 🔒 | 2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| Product Type | 🔒 | 🔒 | 2025 |

| Region | North India | 33.8% | 2025 |

By Formulation

Plain formulation dominates with a 57.2% share in 2025, reflecting strong consumer preference for unflavored plant-based milk variants used in cooking, coffee, tea, and as direct dairy substitutes. Plain variants are particularly favored by lactose-intolerant consumers and health-conscious urban buyers seeking neutral-tasting alternatives suitable for everyday meal preparation.

To access detailed market analysis, Request Sample

Flavored formulations account for 42.8% in 2025, capturing demand for ready-to-drink beverages, chocolate and vanilla plant-based milks, flavored yogurts, and protein-fortified drinks. The flavored segment is projected to grow at approximately 11.0% CAGR through 2034, supported by younger consumer adoption, indulgent occasion-based consumption, and convenience-driven demand.

By Nutrient

Protein-fortified products lead with a 34.5% share in 2025, supported by rising functional nutrition demand, fitness-led consumption, and brand investment in protein-positioned plant-based beverages. Hershey India Private Limited’s Sofit and emerging high-protein plant beverages anchor this segment, which is projected to grow at approximately 12.0% CAGR through 2034.

Starch-based products at 24.6% include oat, millet, and rice-based formulations, capitalizing on natural creaminess and indigenous grain advantages. Vitamin-fortified variants at 21.8% serve health-conscious consumers seeking calcium, vitamin D, and B12 supplementation.

Regional Market Insights

North India leads at 33.8% in 2025, supported by Delhi-NCR's concentration of urban premium consumers, robust quick-commerce platform density, and established modern trade retail penetration for refrigerated dairy alternatives. The region benefits from cosmopolitan consumption patterns, the presence of multinational FMCG headquarters, and high awareness of plant-based food categories.

West and Central India at 26.7% holds the second-largest share, anchored by Mumbai and Pune's affluent consumer concentration, established refrigerated logistics network, and dedicated dairy-alternative retail aisles in modern trade outlets.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

33.8% |

Urban premium consumer base; high quick-commerce density; cosmopolitan consumption patterns; strong modern trade retail penetration |

|

West and Central India |

26.7% |

Affluent consumer concentration; established refrigerated logistics network; FMCG manufacturing presence; new product launch test market |

|

South India |

23.5% |

High lactose intolerance prevalence; vegetarian and vegan dietary traditions; tech-savvy workforce; Urban demand growth |

|

East and Northeast India |

16.0% |

Emerging adoption driven by urban consumption; rising awareness; modern trade retail expansion; growing health-conscious consumer base |

South India at 23.5% benefits from high lactose intolerance prevalence, deep-rooted vegetarian traditions, and a tech-savvy consumer base supporting strong online purchase patterns, while East and Northeast India at 16.0% reflects emerging adoption with rising urban awareness.

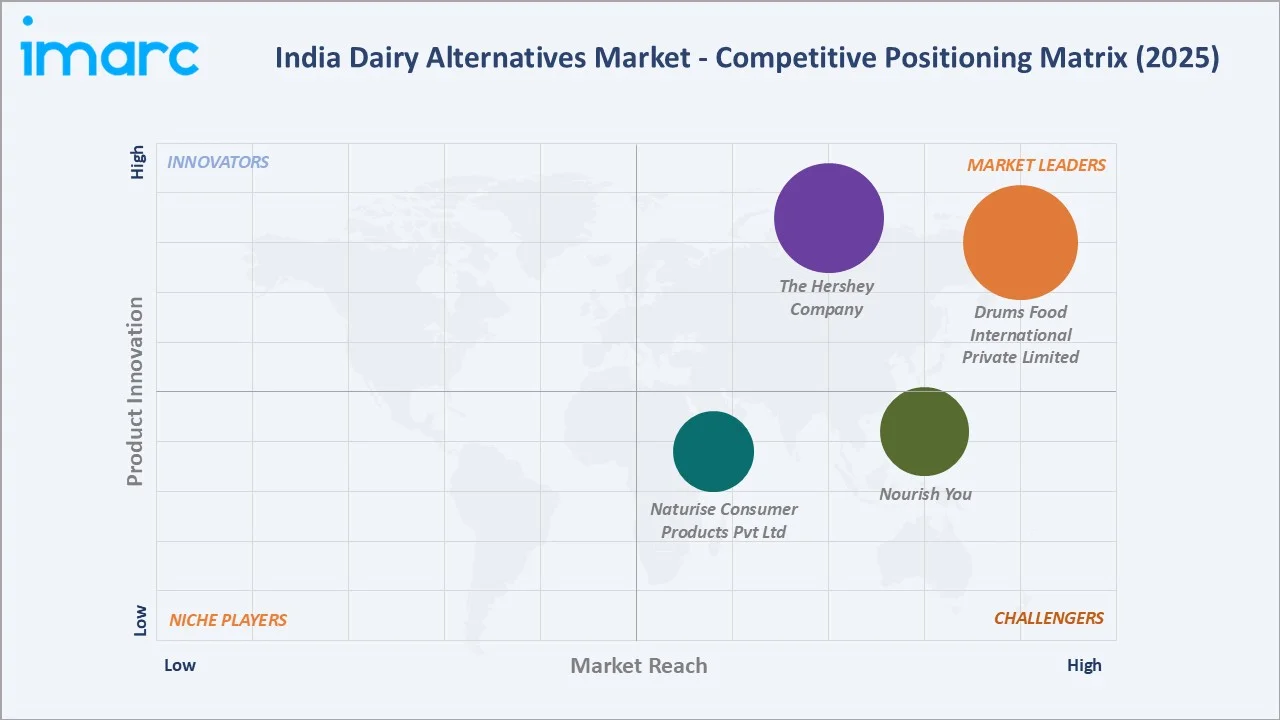

Competitive Landscape

India's dairy alternatives market is structurally fragmented, with the top four companies collectively holding approximately 6.88% revenue share. Leading players include Drums Food International Private Limited, The Hershey Company, Nourish You, and Naturise Consumer Products Pvt Ltd.

|

Company Name |

Brands |

Market Position |

Core Strength |

|

Drums Food International Private Limited |

Epigamia |

Market Leader |

Premium plant-based yogurt and beverage portfolio; strong urban modern trade and HoReCa presence; brand-led category expansion |

|

The Hershey Company |

Sofit |

Market Leader |

Soy-based and protein-fortified plant beverage leadership; wide distribution network; multinational backing and R&D capability |

|

Nourish You |

Nourish You, One Good |

Strong Challenger |

Direct-to-consumer leadership; quick-commerce expansion to 50+ cities; millet and sustainable feedstock innovation |

|

Naturise Consumer Products Pvt Ltd |

Only Earth |

Strong Challenger |

Plant-based milk portfolio across almond, oat, and coconut; modern trade and e-commerce presence |

Companies are competing through product innovation, clean-label formulations, locally relevant ingredients such as soy, almond, oat, coconut, millet, and peanut, and wider availability through supermarkets, cafés, e-commerce, and quick-commerce platforms.

Key Company Profiles

Drums Food International Private Limited

Drums Food International Private Limited operates the Epigamia brand, one of India's leading premium dairy and plant-based product portfolios. Epigamia was among the first Indian brands to launch branded plant-based yogurt and continues to anchor the dairy alternatives category through innovation in coconut-based and plant-fortified products.

- Product Portfolio: Plant-based yogurts (coconut milk yogurt), Greek yogurt, lactose-free dairy products, plant-based desserts, smoothies, protein beverages, and curated artisanal portfolio.

- Recent Developments: In May 2025, French food major Danone is reportedly planning to increase its stake in Epigamia from around 30% to 60% by acquiring part or all of Belgian investor Verlinvest’s holding, strengthening its presence in India’s premium yogurt and health-focused dairy segment.

- Strategic Focus: Premium plant-based yogurt category leadership, expansion into plant-based cheese and dessert formats, multi-channel distribution including quick-commerce and HoReCa partnerships.

The Hershey Company

The Hershey Company operates the Sofit plant-based beverage brand, a leading player in soy-based and protein-fortified plant beverages in India. Sofit anchors mainstream availability of plant-based drinks through wide modern trade and general trade distribution.

- Product Portfolio: Sofit Soy Drink, Sofit Almond Drink, flavored plant-based beverages across vanilla, chocolate, and natural variants.

- Recent Developments: The Hershey Company reported Q1 2026 net sales of USD 3.10 billion, above estimates of USD 3.03 billion, with adjusted EPS of USD 2.35, supported by stronger demand for healthier food & drinks.

- Strategic Focus: Mainstream soy and almond beverage category leadership, protein-fortified functional nutrition expansion, leveraging Hershey Company global R&D and brand assets in the Indian market.

Market Concentration Analysis

India's dairy alternatives market is highly fragmented. The top four companies collectively hold approximately 6.88% revenue share, with no single firm commanding more than 15% share. The market structure includes established FMCG players, specialist plant-based brands, direct-to-consumer specialists, and global multinationals.

Investment & Growth Opportunities

Fastest Growing Segments

- Protein-fortified dairy alternatives are projected to grow at approximately 12.0% CAGR through 2034, supported by fitness and functional nutrition demand and brand investment in high-protein plant-based beverages.

- Flavored formulations and plant-based yogurt are expanding faster than overall market growth, driven by indulgent consumption occasions, younger consumer adoption, and probiotic-fermented product innovation.

Emerging Market Expansion

- Tier-2 and Tier-3 city expansion presents significant headroom as cold-chain infrastructure scales and quick-commerce platforms extend coverage beyond metros.

- Plant-based yogurt, cheese, and butter segments offer premium expansion opportunities, with Epigamia's coconut yogurt category leadership signaling broader cultured-dairy alternative potential.

Venture and Institutional Investment Trends

- Direct-to-consumer brands including Country Delight are attracting venture capital flows, with quick-commerce-led distribution models offering capital-efficient scale-up paths.

- Indigenous millet and oat-based formulation companies are positioned for sustained growth, supported by India's International Year of Millets positioning, water-footprint advantages, and consumer alignment with sustainability values.

Future Market Outlook (2026-2034)

India's dairy alternatives market is positioned for sustained, premiumization-led expansion through 2034. From USD 1.36 Billion in 2025, the market is projected to reach USD 3.30 Billion by 2034, representing incremental value of approximately USD 1.94 Billion at a 10.04% CAGR, increasingly composed of protein-fortified beverages, plant-based yogurt and cheese, and indigenous grain-based formulations.

Flavored formulations are expected to gain share toward 47.0% by 2034 as ready-to-drink consumption expands. Protein-fortified products will retain nutrient segment leadership, while millet, oat, and indigenous grain-based formulations gain mainstream traction.

North India will retain regional leadership, with South India closing the gap as lactose-intolerance-driven adoption scales and quick-commerce platforms extend reach. Consolidation through strategic M&A is expected to bring scale to a currently fragmented category.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, comprising Indian plant-based dairy manufacturers, FMCG brand executives, modern trade retail buyers, quick-commerce category managers, FSSAI policy stakeholders, and Plant-Based Foods Industry Association representatives, validating market sizing, segmentation, and regional adoption patterns.

Secondary Research

Secondary research covered FSSAI plant-based food guidelines, Plant-Based Foods Industry Association data, company annual reports and press releases, BIS/NSO data, NielsenIQ publications, and industry coverage from BigBasket, Amazon, and quick-commerce platform launch announcements.

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating lactose-intolerance prevalence, urban premium consumer growth, formulation and nutrient segment penetration, quick-commerce platform adoption, and announced product launches. The 10.04% CAGR reflects validation against announced FMCG plant-based product pipelines, quick-commerce expansion timelines, and consumer survey data through 2034.

India Dairy Alternatives Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Almond, Soy, Oats, Hemp, Coconut, Rice, Others |

| Formulations Covered |

|

| Nutrients Covered | Protein, Starch, Vitamin, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Product Types Covered | Cheese, Creamers, Yogurt, Ice Creams, Milk, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Drums Food International Private Limited, The Hershey Company, Nourish You, Naturise Consumer Products Pvt Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India dairy alternatives market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India dairy alternatives market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India dairy alternatives industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Dairy Alternatives Market Report

The India dairy alternatives market reached USD 1.36 Billion in 2025 and is projected to reach USD 3.30 Billion by 2034.

The market is expected to grow at a CAGR of 10.04% during 2026-2034, driven by lactose intolerance prevalence, vegan and flexitarian adoption, quick-commerce growth, and FSSAI regulatory support.

North India leads with a 33.8% share in 2025, supported by Delhi-NCR's urban premium consumer concentration and quick-commerce density.

Plain formulation dominates with a 57.2% share in 2025, reflecting consumer preference for unflavored plant-based milk variants used in cooking, coffee, and as direct dairy substitutes.

Protein-fortified products hold 34.5%, supported by functional nutrition demand and fitness-driven consumption patterns.

Key players include Drums Food International Private Limited, The Hershey Company, Nourish You, and Naturise Consumer Products Pvt Ltd.

Protein-fortified products are projected to grow at approximately 12.0% CAGR through 2034 due to functional nutrition demand, fitness-led consumption, and brand investment in protein-positioned plant-based beverages.

Key challenges include price premium over conventional dairy (2-3x), Tier-2 and Tier-3 distribution gaps, taste and texture parity, cold-chain logistics, and consumer category education.

Millet and oat-based formulations, protein-fortified functional beverages, plant-based yogurt and cheese expansion, and direct-to-consumer quick-commerce models represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)