India Q-Commerce Market Size, Share, Trends and Forecast by Product Type, Platform, and Region, 2026-2034

India Q-Commerce Market Size, Share, Trends & Forecast (2026-2034)

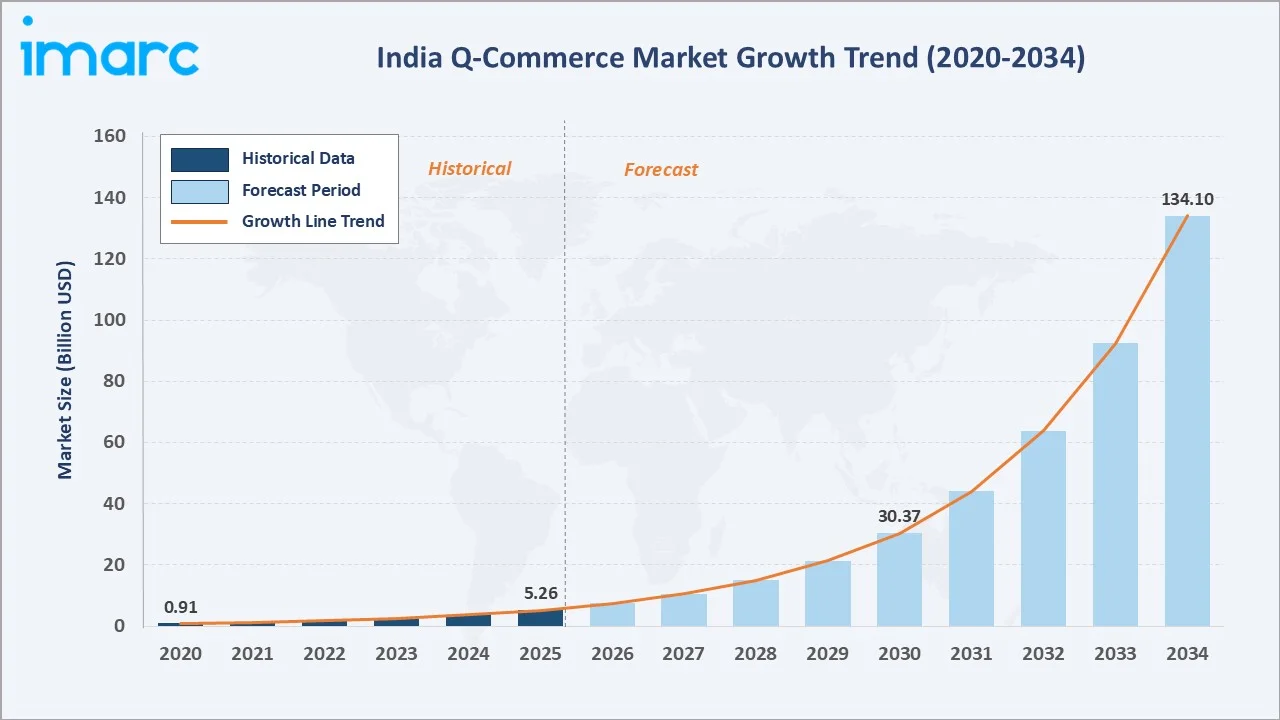

The India q-commerce market was valued at USD 5.26 Billion in 2025 and is projected to reach USD 134.10 Billion by 2034, exhibiting a CAGR of 42.02% during 2026-2034. India's q-commerce sector is growing rapidly, fueled by surging smartphone adoption, expanding dark store networks, rising urban consumer expectations for ultra-fast delivery, and increasing penetration of UPI-based digital payments.

Grocery leads the product type segment at 61.7%, app based dominates the platform segment at 72.4%, and West and Central India command 33.2% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.26 Billion |

|

Forecast Market Size (2034) |

USD 134.10 Billion |

|

CAGR (2026-2034) |

42.02% |

|

Base Year |

2020-2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West and Central India (33.2%, 2025) |

|

Second Largest Region |

North India (27.9%, 2025) |

|

Leading Product Type |

Grocery (61.7%, 2025) |

|

Leading Platform |

App Based (72.4%, 2025) |

The India q-commerce market expanded from USD 0.91 Billion in 2020 to USD 5.26 Billion in 2025, driven by rapid dark store rollouts, growing preference for instant delivery, and the convergence of affordable data with smartphone usage. Anchored at USD 30.37 Billion in 2030, the forecast to USD 134.10 Billion by 2034 is supported by accelerating Tier-2 and Tier-3 city penetration, deepening supply chain efficiency, and growing basket sizes across grocery, pharmacy, and adjacent categories.

To get more information on this market, Request Sample

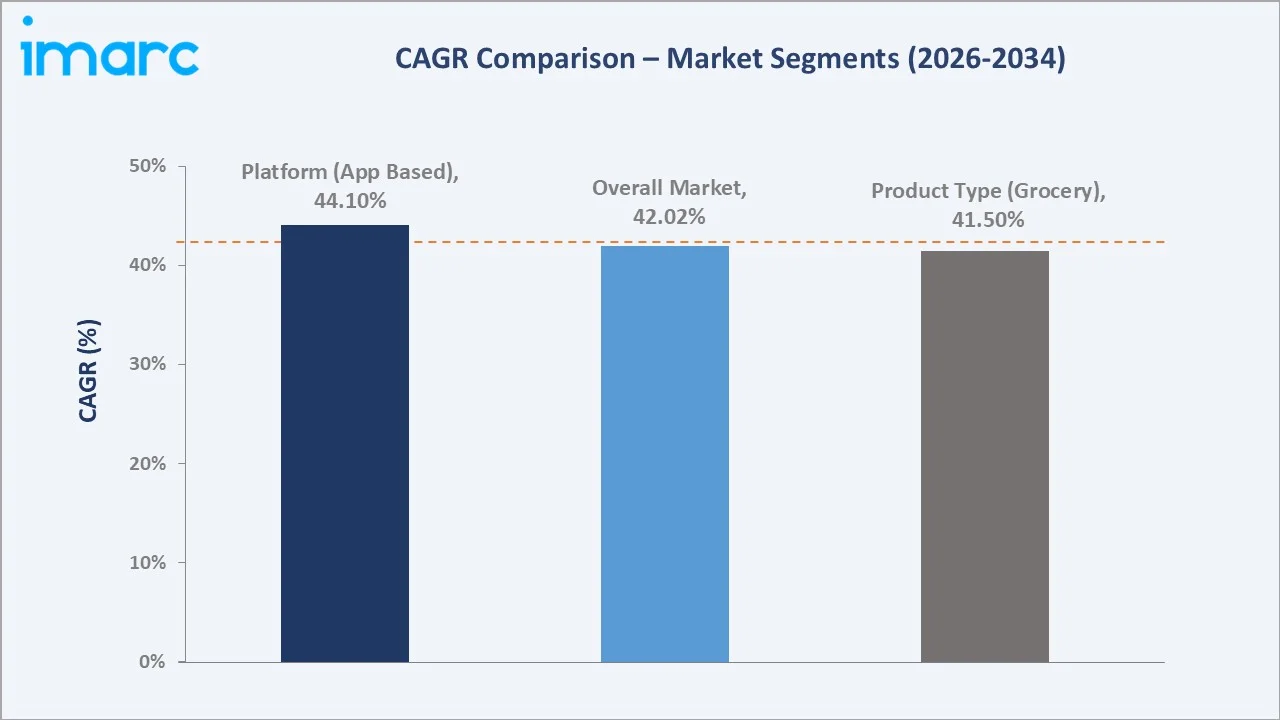

CAGR trajectories across product type and platform sub-segments show pharmacy and app based expanding faster than the overall 42.02% market CAGR, driven by health-conscious consumers, mobile-first engagement, and growing trust in digital platforms for essential purchases.

Executive Summary

The India q-commerce market is on a steep growth trajectory, rising from USD 0.91 Billion in 2020 to USD 5.26 Billion in 2025 and projected to reach USD 134.10 Billion by 2034. The segment has evolved from convenience-focused grocery pilots in metro cities to a full-stack instant commerce ecosystem spanning groceries, pharmacy products, and everyday essentials, with delivery windows compressed to 10–30 minutes. Rising disposable incomes, widespread UPI adoption, and aggressive dark store expansion by well-capitalized platforms are collectively redefining last-mile delivery in India.

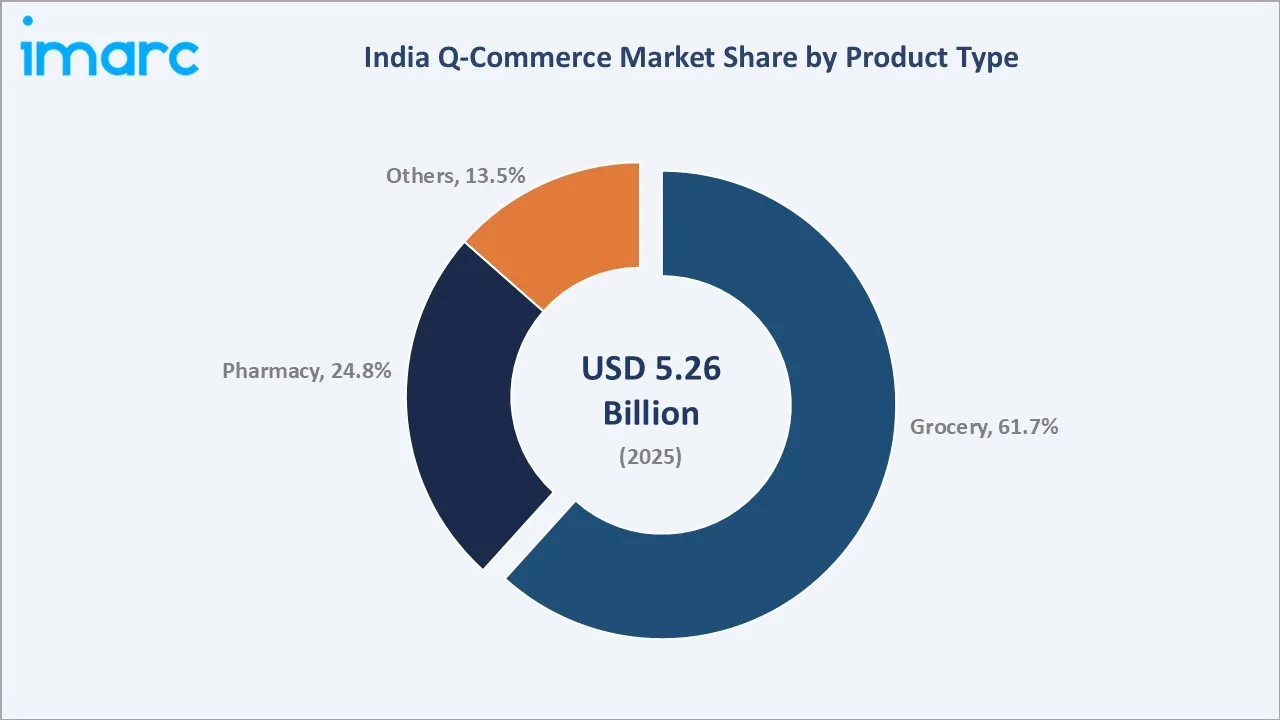

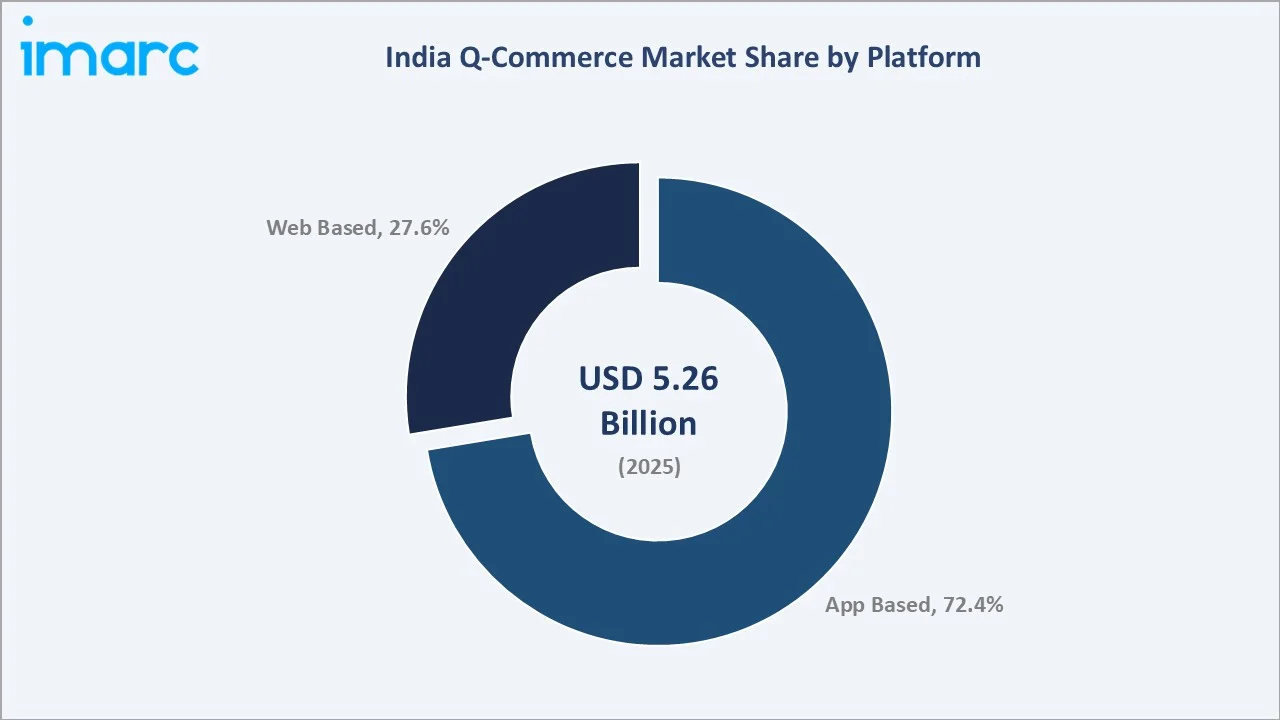

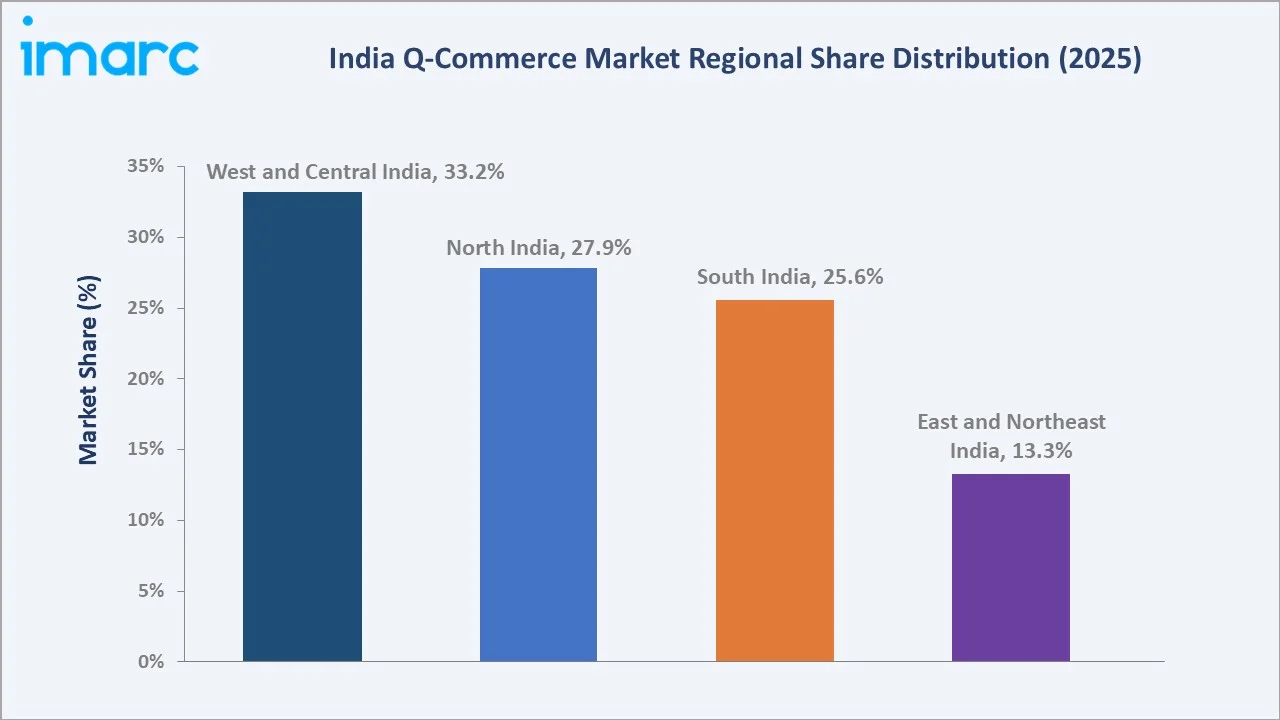

Grocery leads the product type segment at 61.7% in 2025, underpinned by the high repurchase frequency of fresh produce, packaged foods, and household essentials. App based commands 72.4% of the platform segment, supported by seamless mobile onboarding, personalized push notifications, and integrated payment flows. West and Central India command 33.2% of the regional share, anchored by Mumbai, Pune, and Ahmedabad, which have high urban consumer density and well-developed dark store networks.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Grocery – 61.7% share (2025) |

|

Second Largest Product Type |

Pharmacy – 24.8% share (2025) |

|

Leading Platform |

App Based – 72.4% share (2025) |

|

Second Largest Platform |

Web Based – 27.6% share (2025) |

|

Leading Region |

West and Central India – 33.2% share (2025) |

|

Second Largest Region |

North India – 27.9% share (2025) |

|

Top Companies |

Eternal Ltd., Swiggy Limited, Zepto Limited, Reliance Retail, Amazon.com, Inc. |

Key Analytical Observations Expanding On The Data Above:

- Grocery dominance at 61.7% is driven by the high repurchase frequency of daily essentials, fresh produce, and packaged foods. The segment benefits from strong consumer trust in q-commerce platforms for time-sensitive purchases and larger basket sizes generated by routine household replenishment.

- Pharmacy at 24.8% is supported by growing demand for over-the-counter medicines, health supplements, and personal care products. Rising health and wellness awareness and the expanding adoption of digital healthcare services continue to drive category growth. As per IMARC Group, the India health and wellness market size was valued at USD 164.35 Billion in 2025.

- App based at 72.4% benefits from India's mobile-first consumer behavior, seamless UPI integration, personalized recommendations, and push notification-driven repeat purchases across grocery and pharmacy categories.

- Web based share at 27.6% is supported by consumers who prefer larger-screen browsing, detailed product comparisons, and bulk ordering, particularly for planned household purchases and scheduled deliveries.

- West and Central India at 33.2% leads the market due to the concentration of high-income urban households in Mumbai, Pune, Ahmedabad, and Indore, supported by dense dark store networks and mature digital payment infrastructure.

India Q-Commerce Market Overview

Q-commerce refers to the hyper-localized delivery of groceries, pharmacy products, and everyday essentials within 10–30 minutes of order placement. The model is enabled by strategically located dark stores – small, automated micro-fulfilment centers positioned within 2–5 kilometers of high-density consumer zones – supported by dedicated last-mile delivery networks and real-time inventory management systems.

The Indian ecosystem integrates product suppliers and FMCG brands, dark store operators, technology and logistics platforms, payment service providers, regulatory bodies, and end consumers. The rapid convergence of affordable smartphone access, low-cost mobile data, and mature UPI-based payment rails has created the infrastructure foundation for rapid q-commerce scale-up. Growing urban population density, rising dual-income households, and time constraints across metro and Tier-1 markets continue to drive structural demand for convenience-oriented retail formats.

Market Dynamics

To evaluate market opportunities, Request Sample

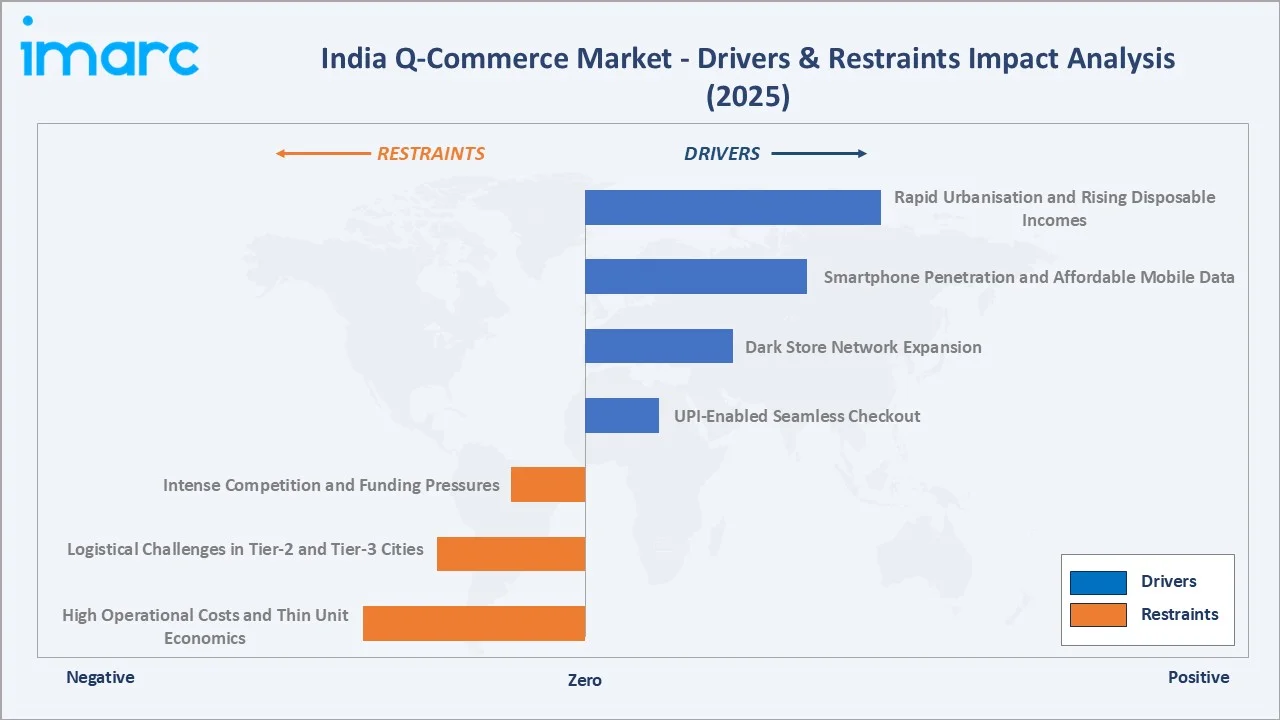

Market Drivers

- Rapid Urbanization and Rising Disposable Incomes: India's urban population is expanding at a steady pace, creating a growing base of time-pressed consumers willing to pay a premium for convenience. Rising middle-class incomes and the growth of dual-income households have increased discretionary spending on instant delivery services.

- Smartphone Penetration and Affordable Mobile Data: India's smartphone user base continues to expand rapidly across metro and non-metro markets. As per government data, India, with over 1 Billion internet users as of November 2025, benefits from some of the lowest mobile data tariffs globally, enabling first-time digital shoppers to access q-commerce apps across Tier-2 and Tier-3 cities.

- Dark Store Network Expansion: Leading q-commerce operators have rapidly deployed micro-fulfilment centers in high-density urban zones, significantly reducing delivery times and expanding serviceable pincodes. Continued capital investment in dark store infrastructure is extending geographic reach and deepening product assortment.

- UPI-Enabled Seamless Checkout: The near-ubiquitous adoption of UPI has eliminated payment friction in the q-commerce purchase flow, enabling low-latency checkout and instant refunds that strengthen consumer trust and repeat purchase rates.

Market Restraints

- High Operational Costs and Thin Unit Economics: The q-commerce model requires dense dark store networks, large delivery fleets, and technology infrastructure, resulting in high capital expenditure and operating costs. Many operators continue to operate at a loss, with profitability contingent on achieving minimum order density and basket size thresholds per dark store.

- Logistical Challenges in Tier-2 and Tier-3 Cities: Expanding beyond Tier-1 metros is constrained by fragmented supply chains, lower order density, underdeveloped warehousing infrastructure, and higher per-delivery costs. These structural challenges slow the pace of geographic expansion and require incremental investment in localized fulfilment assets.

- Intense Competition and Funding Pressures: The market is characterized by aggressive pricing strategies, heavy discounting, and subsidy-driven customer acquisition. Sustained funding pressures in the broader startup ecosystem are compelling operators to accelerate paths to profitability, limiting promotional intensity and expansion velocity.

Market Opportunities

- Pharmacy and Healthcare Delivery Expansion: Regulatory advances in e-pharmacy licensing and rising consumer demand for on-demand healthcare products represent a high-growth opportunity. Q-commerce platforms integrating licensed pharmacies with rapid delivery can capture significant share of India's growing pharmaceutical retail market.

- Private Label and Exclusive Brand Partnerships: Q-commerce platforms can generate higher margins through exclusive supply agreements with FMCG brands and the development of own-label product lines in high-frequency categories such as staples, beverages, and personal care.

Market Challenges

- Last-Mile Delivery Workforce Sustainability: Intense reliance on gig-economy delivery partners raises long-term workforce sustainability concerns around income security, insurance coverage, and attrition. Regulatory scrutiny around gig worker protections could increase platform operating costs.

- Demand Forecasting and Inventory Wastage: Managing perishable inventory, particularly fresh produce and dairy, across a distributed dark store network requires sophisticated demand forecasting. Errors in inventory positioning lead to wastage and margin compression, particularly in high-SKU grocery categories.

Emerging Market Trends

1. Expansion Into Pharmacy and Nutraceuticals

Q-commerce platforms are broadening their product portfolios to include over-the-counter drugs, prescription medicines, vitamins, supplements, and personal care products. The extension into pharmacy is supported by growing e-pharmacy regulation, rising health awareness post-pandemic, and consumer willingness to pay for rapid medication access.

2. AI-Powered Demand Forecasting and Inventory Optimization

Leading operators are deploying machine learning (ML) models that analyze real-time order patterns, weather data, local events, and seasonal trends to optimize inventory placement across dark stores. These systems reduce stockouts, minimize perishable wastage, and improve per-store economics.

3. Hyperlocal Assortment Curation

Operators are increasingly tailoring product assortments at the dark store level based on neighborhood demographics, purchase history, and local consumption patterns. Hyperlocal curation improves fill rates, increases average basket size, and builds platform stickiness among repeat buyers. Regional preferences for particular food categories, brands, and pack sizes are driving a move away from standardized national assortments.

4. Integration of Subscription and Loyalty Models

Q-commerce platforms are building subscription-based membership models that offer free or discounted delivery, priority access to new product categories, and early access to promotions. These loyalty mechanisms increase order frequency, reduce customer acquisition costs over the lifecycle, and create more predictable revenue streams. Bundled memberships with food delivery, streaming, or fintech services are emerging as a key platform differentiation strategy.

5. Expansion of Dark Store Networks Into Tier-2 Cities

Several major operators have initiated systematic rollouts of dark stores in cities such as Jaipur, Lucknow, Coimbatore, and Nagpur, targeting rising digital adoption and growing consumer aspirations. Tier-2 and Tier-3 expansion is supported by lower real estate costs relative to metros and government infrastructure investment in digital connectivity. These markets are expected to contribute an increasing proportion of total q-commerce order volume through 2034.

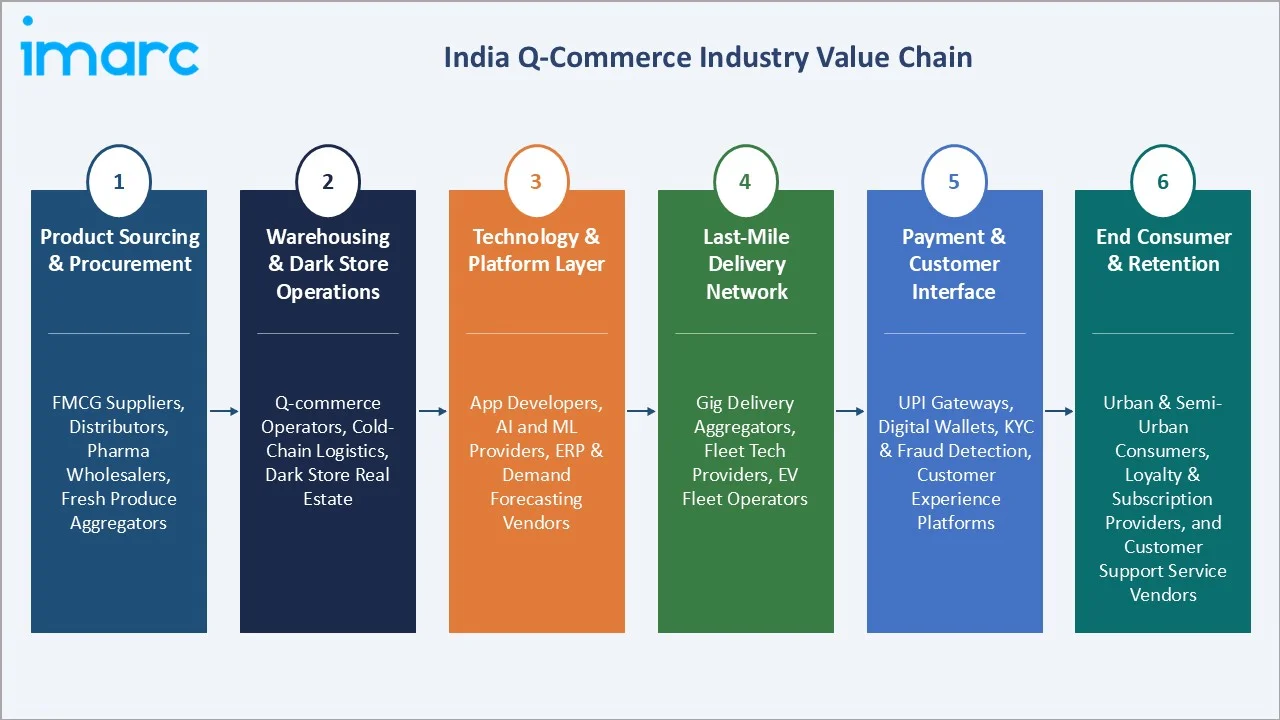

Industry Value Chain Analysis

The India q-commerce value chain spans six stages from product sourcing and warehousing through last-mile fulfilment and post-purchase customer retention. Technology infrastructure and dark store operations command the highest value-add, while last-mile delivery capability and payment integration increasingly determine competitive sustainability.

|

Stage |

Key Players / Examples |

|

Product Sourcing & Procurement |

FMCG suppliers, regional distributors, pharmaceutical wholesalers, and fresh produce aggregators providing inventory to dark store networks |

|

Warehousing & Dark Store Operations |

Q-commerce platform operators managing micro-fulfilment centers, cold chain logistics providers, and real estate firms leasing dark store locations |

|

Technology & Platform Layer |

Mobile app developers, AI and ML solution providers, ERP and inventory management vendors, and demand forecasting software companies |

|

Last-Mile Delivery Network |

Gig delivery partner aggregators, fleet management technology providers, and EV fleet operators supporting last-mile fulfilment |

|

Payment & Customer Interface |

UPI-enabled payment gateways, digital wallet providers, KYC and fraud detection specialists, and customer experience platforms |

|

End Consumer & Retention |

Individual urban and semi-urban consumers, loyalty program providers, subscription platform managers, and customer support service vendors |

Vertically integrated operators that manage dark store operations, proprietary technology platforms, and last-mile delivery networks are best positioned to capture value across the chain and sustain competitive differentiation.

Technology Landscape in the India Q-Commerce Industry

Dark Store Management Systems

Advanced warehouse management systems are being deployed across dark stores to optimize pick-and-pack operations, manage SKU placement based on order frequency, and synchronize inventory levels in real time. These systems enable consistent sub-10-minute picking cycles even at high order volumes, directly supporting the delivery SLA commitments that drive consumer trust.

AI and Demand Forecasting

AI and ML models underpin inventory replenishment, dynamic pricing, and logistics optimization across the q-commerce stack. Predictive demand engines analyze historical order data, local event calendars, weather patterns, and seasonal trends to minimize stockouts and reduce perishable wastage at the dark store level.

Mobile-First Platforms and Embedded Payments

Native mobile applications tightly integrated with UPI, digital wallets, and instant settlement rails dominate the consumer interface. Biometric login, one-tap reorder, and personalized product discovery powered by recommendation algorithms support high repeat purchase rates and extended consumer lifetime value.

EV Fleet and Route Optimization

Leading operators are transitioning last-mile delivery fleets to electric two-wheelers, supported by AI-powered route optimization tools that minimize delivery times while reducing carbon emissions. EV adoption improves operational cost efficiency over multi-year fleet lifecycles and aligns with regulatory sustainability mandates.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Grocery |

61.7% |

2025 |

|

Platform |

App Based |

72.4% |

2025 |

|

Region |

West and Central India |

33.2% |

2025 |

By Product Type

Grocery commands a 61.7% majority share in 2025, driven by the essential and high-frequency nature of food and household replenishment purchases. The segment benefits from consumer familiarity, large basket sizes, and the suitability of dark store operations for chilled, ambient, and fresh categories. Growing product depth across organic, premium, and regional food categories is further expanding addressable grocery spend on q-commerce platforms.

To access detailed market analysis, Request Sample

Pharmacy at 24.8% in 2025 is the second-largest segment, accelerated by expanding e-pharmacy regulation, post-pandemic health awareness, and growing demand for rapid access to OTC medicines and health supplements.

By Platform

App based accounts for 72.4% of the India q-commerce market in 2025, driven by mobile-first consumer behavior, seamless UPI payment integration, push notification-enabled repeat purchases, and personalized product discovery. The app channel also enables precise location-based dark store routing, real-time order tracking, and gamified loyalty reward systems that sustain high engagement.

Web based at 27.6% in 2025 serves desktop and browser-based shoppers, particularly in enterprise and B2B procurement contexts, and remains relevant in markets with lower smartphone penetration or for older consumer demographics that prefer non-app purchasing flows.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West and Central India |

33.2% |

High urban population density, mature digital payment adoption, large concentration of dark stores, strong FMCG distribution networks |

|

North India |

27.9% |

Large metro and Tier-1 city base, growing middle-class consumer spending, high smartphone penetration, extensive delivery partner networks |

|

South India |

25.6% |

Rising IT workforce, rapid digital adoption, high education and income levels, growing health and wellness consumption |

|

East and Northeast India |

13.3% |

Emerging smartphone adoption, expanding digital infrastructure, growing youth consumer base, untapped demand in Tier-2 cities |

West and Central India at 33.2% in 2025 leads the regional landscape, anchored by Mumbai, Pune, Ahmedabad, and Indore. High urban population density, a mature digital payment ecosystem, and the highest concentration of operational dark stores in the country support sustained regional leadership across both grocery and pharmacy segments.

North India at 27.9% is driven by Delhi-NCR, Lucknow, and Jaipur, where high population density and growing digital infrastructure support rising q-commerce order volumes.

Competitive Landscape

The India q-commerce market is moderately consolidated at the platform level, with a small number of well-capitalized operators commanding the majority of order volume through established dark store networks, strong brand recognition, and deep technology capabilities. Brand strength, dark store density, delivery SLA consistency, payment integration, and category breadth form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Eternal Ltd. |

Blinkit |

Leader |

Dark store-led hyperlocal delivery with expanding pharmacy and electronics categories |

|

Swiggy Limited |

Instamart |

Leader |

Integrated food and q-commerce super-app model with growing dark store coverage |

|

Zepto Limited |

Zepto |

Challenger |

10-minute delivery model with rapid dark store network expansion across metro cities |

|

Reliance Retail |

JioMart |

Challenger |

Omnichannel retail integration with q-commerce across grocery and daily essentials |

|

Amazon.com, Inc. |

Amazon Now |

Emerging |

Leveraging logistics and Prime subscriber base for grocery delivery expansion |

Key players include Eternal Ltd., Swiggy Limited, Zepto Limited, Reliance Retail, and Amazon.com, Inc., among others.

Key Company Profiles

Eternal Ltd.

Eternal Ltd. is a leading India-based technology and on-demand delivery company headquartered in Gurugram, Haryana, and listed on Indian stock exchanges. It operates a portfolio of consumer platforms including q-commerce, food delivery, and ticketing, with Blinkit serving as the company's primary q-commerce engine.

- Product Portfolio: Blinkit platform offering rapid delivery of groceries, fresh produce, dairy, pharmacy products, electronics, home care, baby care, and pet care categories, supported by an extensive dark store network across major Indian cities.

- Recent Developments: Blinkit crossed 2,243 dark stores as of Q4 FY26 and achieved adjusted EBITDA profitability for the first time, marking a significant operational milestone.

- Strategic Focus: Expanding dark store density across metro and Tier-2 cities, deepening product categories beyond grocery, growing the pharmacy vertical, and driving sustainable profitability through inventory-led operational improvements.

Swiggy Limited

Swiggy Limited is a prominent India-based on-demand delivery platform headquartered in Bengaluru, Karnataka, listed on Indian stock exchanges. The company operates q-commerce services under the Instamart brand alongside its core food delivery business, forming part of a broader super-app ecosystem serving millions of consumers across hundreds of Indian cities.

- Product Portfolio: Instamart platform providing rapid delivery of groceries, fresh produce, dairy, household essentials, snacks, beverages, and pharmacy products, integrated with the Swiggy app to enable cross-category ordering within a single consumer interface.

- Recent Developments: Swiggy Limited has been expanding its dark store network, investing in supply chain technology to improve inventory management, and broadening category coverage to strengthen its competitive position in the quick commerce segment.

- Strategic Focus: Building a differentiated quick commerce proposition within the Swiggy super-app, scaling dark store coverage across metro and non-metro cities, and improving unit economics through higher order density and an expanded product assortment.

Reliance Retail

Reliance Retail is India's leading retail company, headquartered in Mumbai, Maharashtra. The company operates JioMart, its digital commerce and quick delivery platform, leveraging an extensive network of physical retail stores, cold chain infrastructure, and the Jio telecom ecosystem to serve consumers across a wide range of categories.

- Product Portfolio: JioMart platform offering delivery of groceries, fresh produce, household essentials, electronics, and fashion products, with quick delivery enabled through a combination of dedicated dark stores and the company's existing retail store network.

- Recent Developments: Reliance Retail has been expanding its quick delivery capabilities, adding dark stores to complement its existing retail locations, growing order volumes across new cities and pincodes, and extending its delivery promise to electronics and apparel categories.

- Strategic Focus: Leveraging its physical retail footprint as fulfilment infrastructure, integrating digital and offline channels through an omnichannel model, and scaling quick delivery reach across metro, Tier-2, and Tier-3 cities using the Jio subscriber base.

Market Concentration Analysis

The India q-commerce market is moderately concentrated at the platform level, with the top three operators, including Eternal Ltd., Swiggy Limited, and Zepto Limited, collectively accounting for the large majority of urban q-commerce order volume through their combined dark store networks and mobile platform user bases.

Barriers to entry include the capital-intensive nature of dark store build-out, the need for scalable last-mile delivery networks, technology investment in demand forecasting and inventory management, and the high customer acquisition costs in a competitive mobile app marketplace. These factors favor well-capitalized incumbents with established supply chains and large active user bases.

Consolidation is accelerating as smaller operators face funding constraints and larger platforms continue to add dark store locations, expand category coverage, and integrate q-commerce within broader super-app ecosystems. Strategic investments by big conglomerates are further reinforcing competitive positioning in the market.

Investment & Growth Opportunities

Fastest-Growing Segments

Pharmacy is the fastest-growing product type segment, driven by expanding e-pharmacy regulation, rising health awareness, and growing demand for rapid access to medicines and health supplements. Platform expansion into adjacent health categories, such as nutraceuticals, wellness devices, and diagnostic kits, represents significant incremental revenue potential. App based is also growing faster than the web based platform, supported by continued smartphone adoption and the superior consumer experience enabled by native mobile applications.

Emerging Markets

South India is the fastest-growing region, led by rapid digital adoption in Bengaluru, Hyderabad, and Chennai and an expanding young professional consumer base. East and Northeast India at 13.3% represents the most significant untapped opportunity, with rapidly improving digital infrastructure and growing aspirational consumption in cities such as Kolkata, Guwahati, and Bhubaneswar.

Venture & Investment Trends

Investment is concentrated in dark store technology, AI-powered demand forecasting platforms, cold chain logistics solutions, and EV fleet providers serving the q-commerce last-mile. Capital is also flowing into private label product development, B2B quick-commerce platforms serving small retailers and kirana stores, and subscription-based loyalty platforms that drive recurring revenue for q-commerce operators.

Future Market Outlook (2026-2034)

The India q-commerce market is forecast to expand from USD 5.26 Billion in 2025 to USD 134.10 Billion by 2034 at a CAGR of 42.02%, adding approximately USD 128.84 Billion in incremental market value over the forecast period.

Four forces will define the market through 2034: continued expansion of dark store networks into Tier-2 and Tier-3 cities; maturation of AI-driven supply chain management reducing operational costs; deepening of pharmacy, nutraceutical, and lifestyle categories beyond core grocery; and the integration of q-commerce within broader digital super-app ecosystems offering food delivery, fintech, and entertainment services.

By 2034, q-commerce in India is expected to represent a mainstream retail channel for essential and convenience purchases across urban and semi-urban India, with operating models achieving positive unit economics at the dark store level and market leaders generating sustainable profitability through delivery fee income, private label margins, advertising revenue, and subscription membership models.

Research Methodology

Primary Research

Primary research included structured interviews with q-commerce platform executives, dark store operations leaders, FMCG brand managers, last-mile logistics providers, technology vendors, and investor analysts, validating market sizing, regional demand patterns, segment mix, and competitive positioning assessments.

Secondary Research

Secondary sources included Ministry of Commerce and Industry reports, NASSCOM digital economy publications, Reserve Bank of India digital payments data, SEBI filings from listed operators, company annual reports, investor presentations, press releases, and market analyses from industry associations and retail research organizations.

Forecasting Models

Market forecasts used top-down and bottom-up models combining total addressable market estimates for rapid delivery, dark store count trajectories, average order value trends, category penetration rates, and consumer adoption curves. Scenario analysis addressed regulatory developments, funding environment shifts, and competitive intensity among leading operators.

India Q-Commerce Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Grocery, Pharmacy, Others |

| Platforms Covered | App Based, Web Based |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Eternal Ltd., Swiggy Limited, Zepto Limited, Reliance Retail, Amazon.com Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India Q-commerce market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India Q-commerce market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India Q-commerce industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Q-Commerce Market Report

The India q-commerce market was valued at USD 5.26 Billion in 2025, driven by rapid smartphone adoption, dark store expansion, and rising consumer demand for ultra-fast delivery of groceries and essentials.

The market is projected to grow at a CAGR of 42.02% from 2026 to 2034, reaching USD 134.10 Billion, supported by geographic expansion, category broadening, and continued urbanization.

Grocery leads with 61.7% share in 2025, driven by high repurchase frequency, large basket sizes, and consumer reliance on q-commerce platforms for daily household replenishment.

App based commands 72.4% of the market in 2025, supported by mobile-first consumer behaviors, seamless UPI integration, and personalized engagement through native mobile applications.

West and Central India leads with 33.2% share in 2025, anchored by Mumbai, Pune, and Ahmedabad, which have the highest urban consumer density and most mature dark store coverage.

Leading players include Eternal Ltd., Swiggy Limited, Zepto Limited, Reliance Retail, and Amazon.com, Inc., among others.

Expansion of e-pharmacy regulation and rising demand for rapid access to OTC medicines and health supplements are accelerating pharmacy delivery on q-commerce platforms.

AI is being used for demand forecasting, inventory optimization, route planning, personalized product recommendations, and fraud detection, improving operational efficiency and consumer experience across platforms.

Key challenges include high operational costs, thin unit economics, last-mile workforce sustainability, inventory wastage in perishable categories, and logistical complexity in expanding beyond Tier-1 cities.

Dark stores are the core infrastructure of q-commerce, enabling sub-10-minute pick-and-pack operations. Their strategic placement within 2–5 kilometers of consumer zones, combined with AI-driven inventory management, enables consistent delivery SLA commitments that drive consumer trust.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)