India Telehealth Market Size, Share, Trends and Forecast by Component, Communication Technology, Hosting Type, Application, End User, and Region, 2026-2034

India Telehealth Market Size, Share, Trends & Forecast (2026-2034)

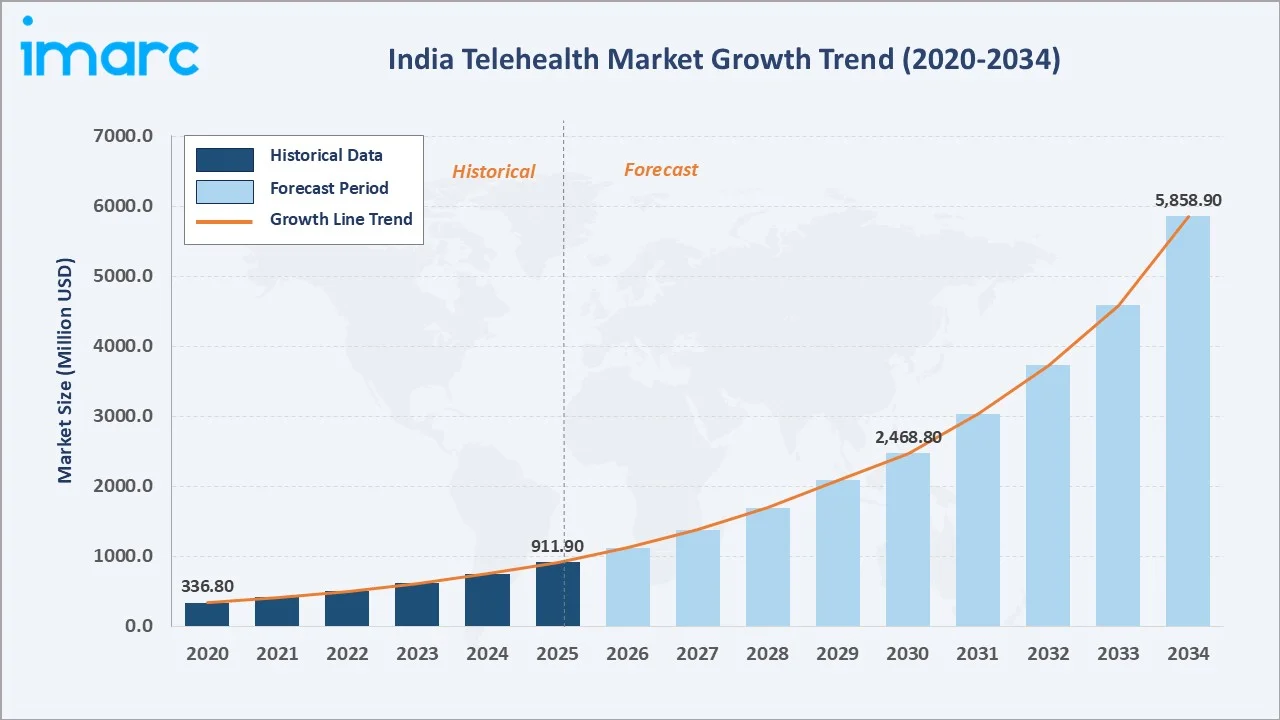

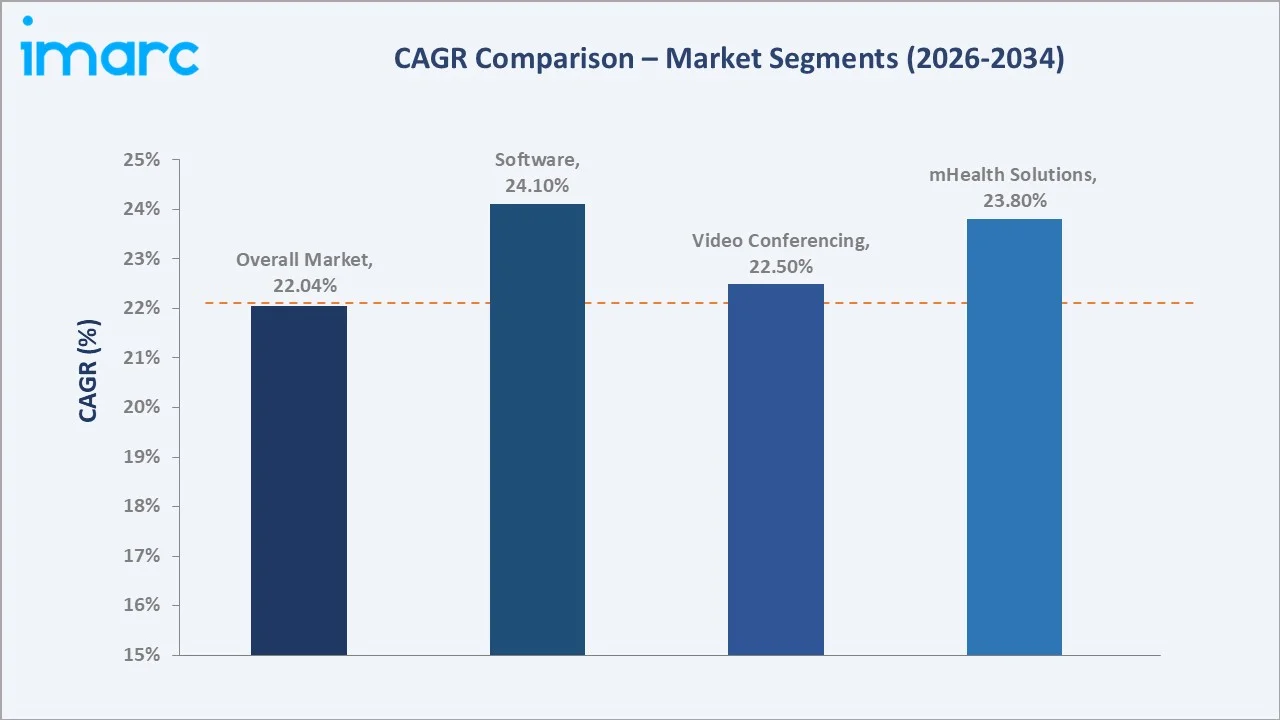

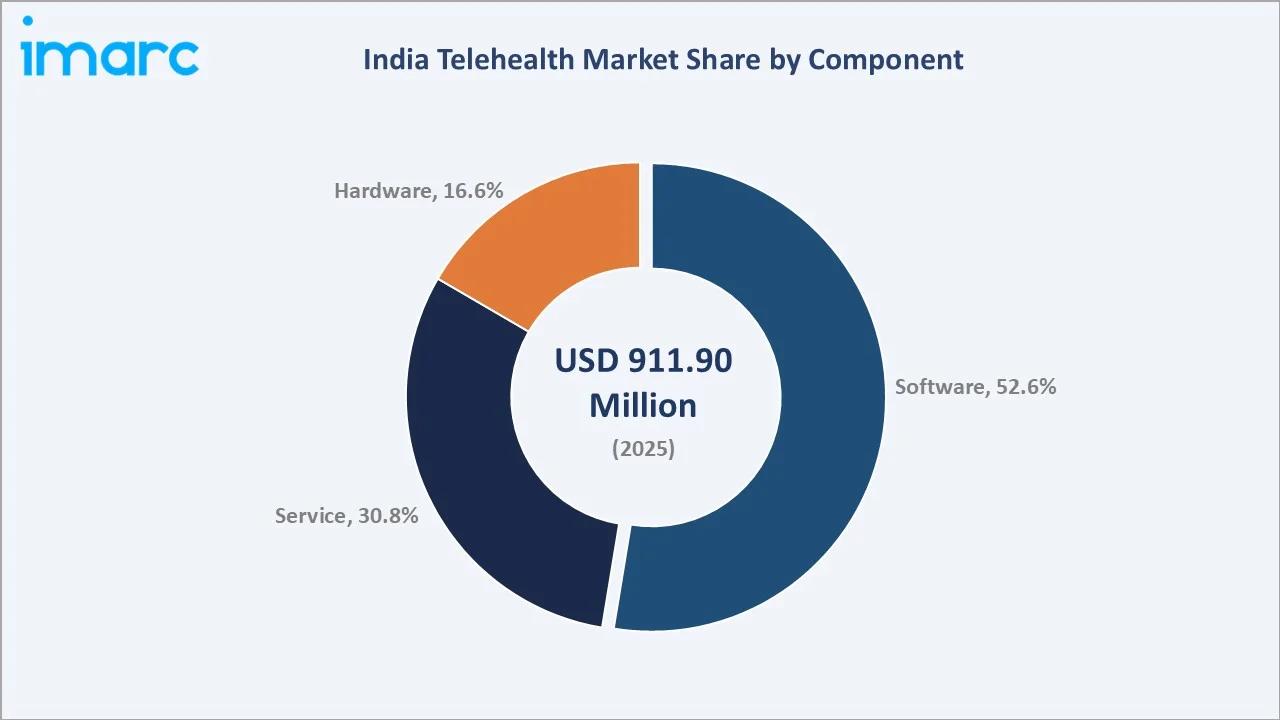

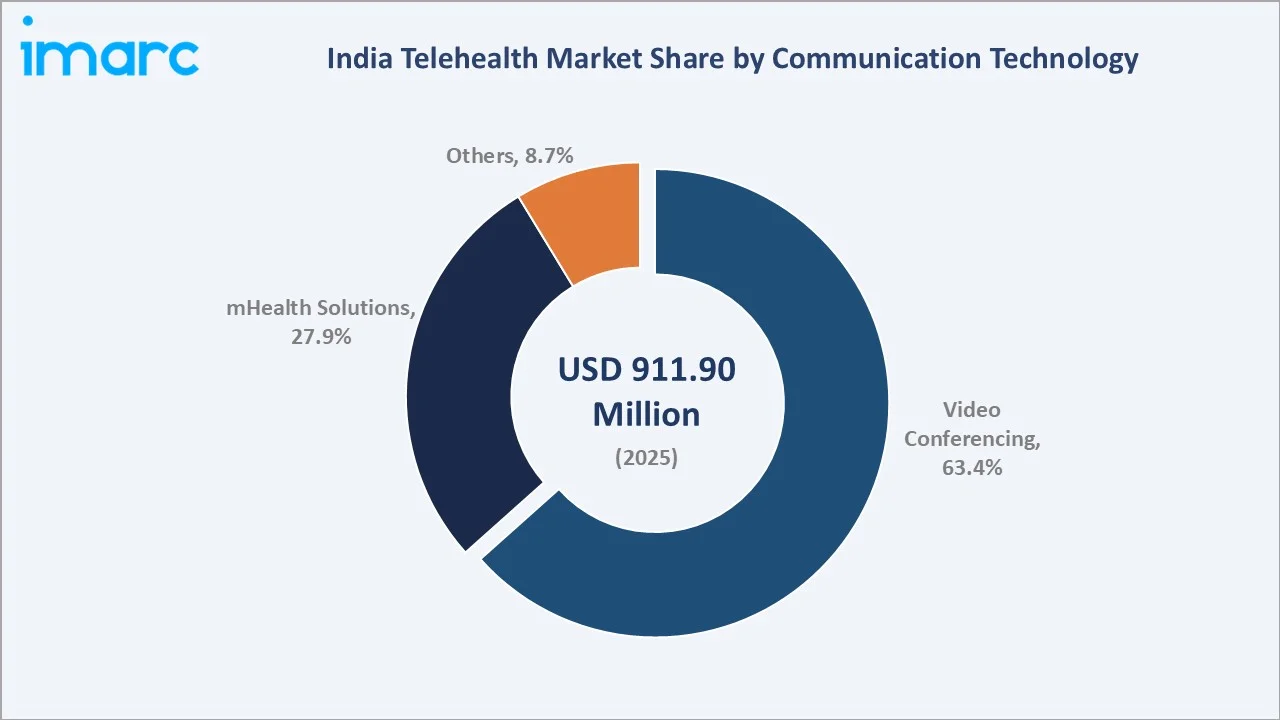

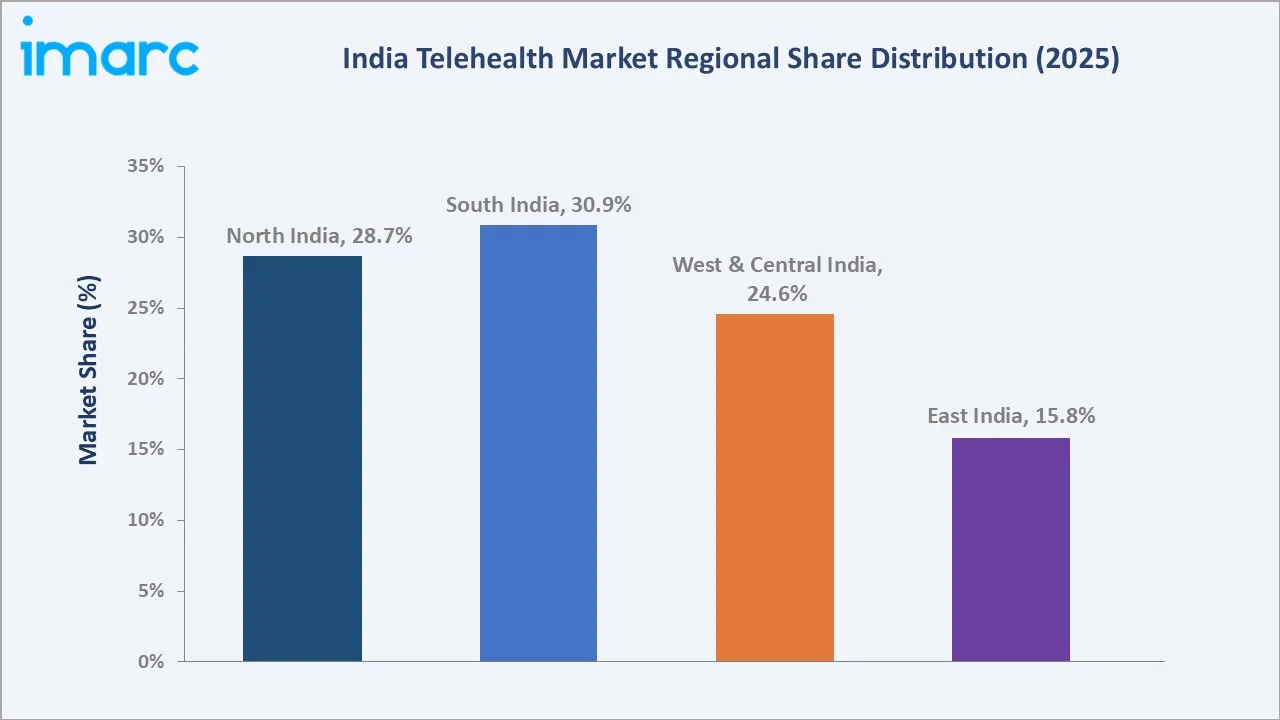

The India telehealth market size reached USD 911.9 Million in 2025 and is projected to reach USD 5,858.9 Million by 2034, growing at a CAGR of 22.04% during 2026-2034. The market is driven by rising smartphone and internet penetration, government support for digital health initiatives, the post-COVID acceptance of remote care, and a growing chronic disease burden. Software dominates the component segment at 52.6% in 2025. Video conferencing leads communication technology at 63.4%. South India commands the highest regional share at 30.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 911.9 Million |

|

Forecast Market Size (2034) |

USD 5,858.9 Million |

|

CAGR (2026-2034) |

22.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Software (52.6%, 2025) |

|

Dominant Communication Tech |

Video Conferencing (63.4%, 2025) |

|

Leading Region |

South India (30.9%, 2025) |

India telehealth market expanded from USD 336.8 Million in 2020 to USD 911.9 Million in 2025, anchored at USD 2,468.8 Million in 2030, and forecast to reach USD 5,858.9 Million by 2034. The market represents one of Asia's fastest-growing digital health segments, driven by structural tailwinds including India's 1 billion-plus internet user base, historically low doctor-to-patient ratios, and the government's Ayushman Bharat Digital Mission (ABDM) creating 90 crore health IDs.

To get more information on this market, Request Sample

The software segment, comprising telehealth platforms, EHR systems, and AI-driven diagnostic tools, accounts for 52.6% of market revenue in 2025, reflecting the platform-first architecture of India's telehealth ecosystem. Video conferencing-based consultation at 63.4% of communication technology revenue underscores the dominance of real-time teleconsultation as India's primary care delivery mode.

Executive Summary

India telehealth market at USD 911.9 Million in 2025 represents one of the most commercially dynamic digital health markets in Asia. The market is projected to reach USD 5,858.9 Million by 2034, delivering a 22.04% CAGR over the forecast period. The government's eSanjeevani platform alone has facilitated over 400 million remote consultations as of mid-2025, with over 230,000 nationwide providers, demonstrating telehealth's structural integration into India's national health delivery system.

Key growth drivers include India's 1 billion-plus internet users, the lowest mobile data costs globally, and a chronic disease burden affecting over 100 million diabetics and 220 million hypertensive patients. The post-COVID acceleration shifted patient mindsets permanently, with online consultations surging 300% during lockdowns in 2020. Government policy reinforced this structural shift through the Telemedicine Practice Guidelines (2020), ABDM (2021), and the Tele-MANAS mental health program (2022), which fielded over 17 lakh calls by early 2025.

Software at 52.6% leads the component segment, driven by platform-centric telehealth models that bundle teleconsultation, e-pharmacy, and diagnostics into unified digital health ecosystems. Video conferencing at 63.4% of communication technology reflects the dominance of real-time specialist consultations. South India at 30.9% leads regionally, supported by Bengaluru and Chennai's tech-savvy populations and robust digital infrastructure. The competitive landscape is moderately fragmented, with Apollo TeleHealth, Tata 1mg, and Practo representing the top three platforms by user engagement.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Software – 52.6% share (2025) |

|

Dominant Comm. Technology |

Video Conferencing – 63.4% market share (2025) |

|

Leading Region |

South India – 30.9% share (2025) |

|

Top Companies |

Apollo Hospitals Enterprise Limited (AHEL), Tata Group, Practo Technologies, and MediBuddy |

|

Market Opportunity |

AI-driven diagnostics, remote patient monitoring in Tier-2/3 cities, chronic disease management platforms, mental health teleconsultation |

Key Analytical Observations Supporting The Above Data:

- Software at 52.6%: Platform-centric architecture dominates as telehealth companies embed teleconsultation, e-pharmacy, and AI diagnostic capabilities into unified software ecosystems. India's SaaS-first digital health model drives software revenue above hardware-intensive alternatives.

- Video Conferencing at 63.4%: Real-time video consultation replicates the in-person clinical interaction closest, making it the preferred modality for specialist consultations. Government platforms like eSanjeevani leverage video conferencing at scale, facilitating 0.4-0.45 million consultations daily.

- South India at 30.9%: Bengaluru, Hyderabad, and Chennai's IT-sector workforce density, above-average digital literacy, and established healthcare infrastructure position South India as India's leading telehealth adopter.

- AI Integration Opportunity: AI-powered diagnostics achieving 95% diagnostic sensitivity in under 30 seconds represent the next frontier of telehealth value creation, with the government's eSanjeevani AI-CDSS having supported over 282 million consultations.

India Telehealth Market Overview

India telehealth market is positioned at a unique intersection of structural demand and policy-driven supply. The country's doctor-to-patient ratio of 1:811 (1.23 per 1,000) with specialists heavily concentrated in urban centers, creates a persistent access gap that telehealth addresses through digital connectivity. The market encompasses software platforms, hardware devices, and services that enable remote diagnosis, patient monitoring, medication management, and mental health support.

India's telehealth ecosystem integrates domestic platform operators, hospital-backed telemedicine services, government-run public platforms, and international health IT providers. Macroeconomic enablers include India's 1 billion internet users, one of the world's lowest mobile data costs, a young median population of 28.7 years, and a rapidly expanding middle class with growing health insurance penetration.

Market Dynamics

To evaluate market opportunities, Request Sample

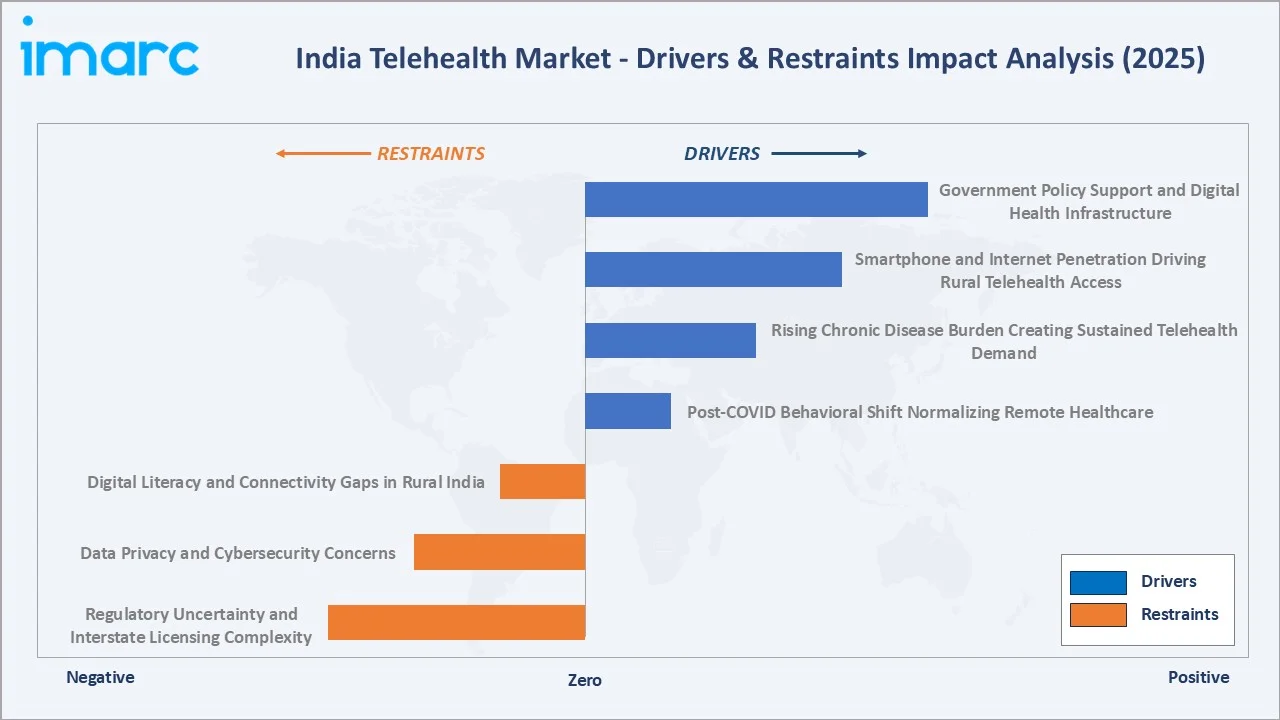

Market Drivers

- Government Policy Support and Digital Health Infrastructure: India's Ministry of Health and Family Welfare launched the Telemedicine Practice Guidelines in 2020 and the Ayushman Bharat Digital Mission in 2021. The ABDM has registered 90 crore health IDs, creating a unique digital patient identity infrastructure that enables cross-platform telehealth service delivery. The eSanjeevani platform, deployed across 1,55,000 public health facilities, facilitates 90,000 to 2,50,000 consultations daily, anchoring telehealth as a national health delivery channel. This government-led infrastructure creates demand certainty and regulatory clarity that supports private platform investment.

- Smartphone and Internet Penetration Driving Rural Telehealth Access: India's 1 billion internet users and among the world's lowest mobile data costs have democratized telehealth access beyond metropolitan boundaries. Tata 1mg's video consultation expansion across 20+ specialties targets Tier-3 cities, leveraging high smartphone penetration in semi-urban India. Rural connectivity improvements under BharatNet and 5G rollouts are expanding the addressable patient base for telehealth platforms, adding approximately 150 million potential new telehealth users from rural and semi-urban households.

- Rising Chronic Disease Burden Creating Sustained Telehealth Demand: India has over 100 million diabetic patients and 300 million hypertensive individuals, creating the world's largest addressable chronic disease management market. Telehealth platforms offering remote patient monitoring, medication adherence tracking, and AI-assisted diagnostic tools address this population efficiently. Chronic disease management platforms generate higher patient lifetime values than acute care consultations, improving unit economics for telehealth operators.

- Post-COVID Behavioral Shift Normalizing Remote Healthcare: Online consultations surged 300% during India's COVID-19 lockdowns in 2020, permanently shifting patient acceptance of digital healthcare. The behavioral change has persisted beyond the pandemic, with patients demonstrating willingness to pay for teleconsultation convenience for follow-up care, prescription renewal, and mental health services. India in mid-2025 has approximately 1 billion internet users, setting a robust stage for sustained digital health adoption.

Market Restraints

- Digital Literacy and Connectivity Gaps in Rural India: Despite strong smartphone penetration in urban areas, approximately 450 million rural Indians lack the digital literacy skills needed to navigate telehealth platforms independently. Last-mile connectivity gaps in remote states, combined with the inability to self-administer clinical assessments, limit the quality of care deliverable via telehealth to rural populations. This structural limitation constrains the market's addressable revenue from rural India below the nominal population size potential.

- Data Privacy and Cybersecurity Concerns: India's Digital Personal Data Protection Act (2023) introduces compliance requirements for telehealth platforms processing sensitive health data. Patient reluctance to share medical records on digital platforms, particularly for mental health and reproductive health conditions, reduces willingness to use telehealth for sensitive consultations. Cybersecurity incidents in health IT globally create patient hesitation around data storage and sharing on telehealth platforms.

- Regulatory Uncertainty and Interstate Licensing Complexity: Telemedicine Practice Guidelines permit cross-state teleconsultation, but the regulatory environment for AI-assisted diagnosis, prescription delivery, and cross-border telemedicine remains evolving. Platform operators face compliance uncertainty around AI-generated diagnostic recommendations, limiting the commercial deployment of AI diagnostic tools in teleconsultation settings.

Market Opportunities

- AI-Driven Diagnostics and Remote Patient Monitoring: AI-powered diagnostic platforms achieving 95% sensitivity in ECG interpretation in under 30 seconds represent the next frontier of telehealth value creation. Remote patient monitoring for chronic disease management, integrating IoT-enabled glucometers, blood pressure monitors, and wearables with telehealth platforms, creates recurring revenue streams above episodic consultation models.

- Mental Health Teleconsultation: India has fewer than 0.3 psychiatrists per 100,000 population, creating a structural specialist shortage that telehealth can address at scale. Private mental health telehealth platforms are growing above the overall market CAGR, with low physical infrastructure requirements making this segment attractive for new platform operators.

- Tier-2 and Tier-3 City Telehealth Expansion: India's secondary cities with growing affluence and inadequate specialist infrastructure represent the highest-growth geographic opportunity. A patient in rural Chhattisgarh historically faced barriers of travel distance, time, and cost when seeking specialist consultation, telehealth eliminates these barriers, creating a commercially accessible market in geographically underserved areas.

Market Challenges

- Physician Resistance and Clinical Quality Concerns: A section of India's medical community remains cautious about telehealth's clinical quality standards, particularly for conditions requiring physical examination. Resistance from traditional healthcare providers, concerns about misdiagnosis in teleconsultation, and the difficulty of replicating clinical examination through digital interfaces limit the scope of conditions addressable via telehealth, constraining market penetration in complex diagnostic and specialist segments.

- Platform Fragmentation and Revenue Sustainability: India's telehealth market comprises over 200 active platforms, creating intense competition for patient acquisition. High customer acquisition costs, low consultation price points driven by competition, and the challenge of converting free consultation users to paid services create revenue sustainability challenges for smaller platforms. Market consolidation through M&A, evidenced by Apollo HealthCo's merger strategy and Tata Digital's 1mg acquisition, is an ongoing structural response to this challenge.

Emerging Market Trends

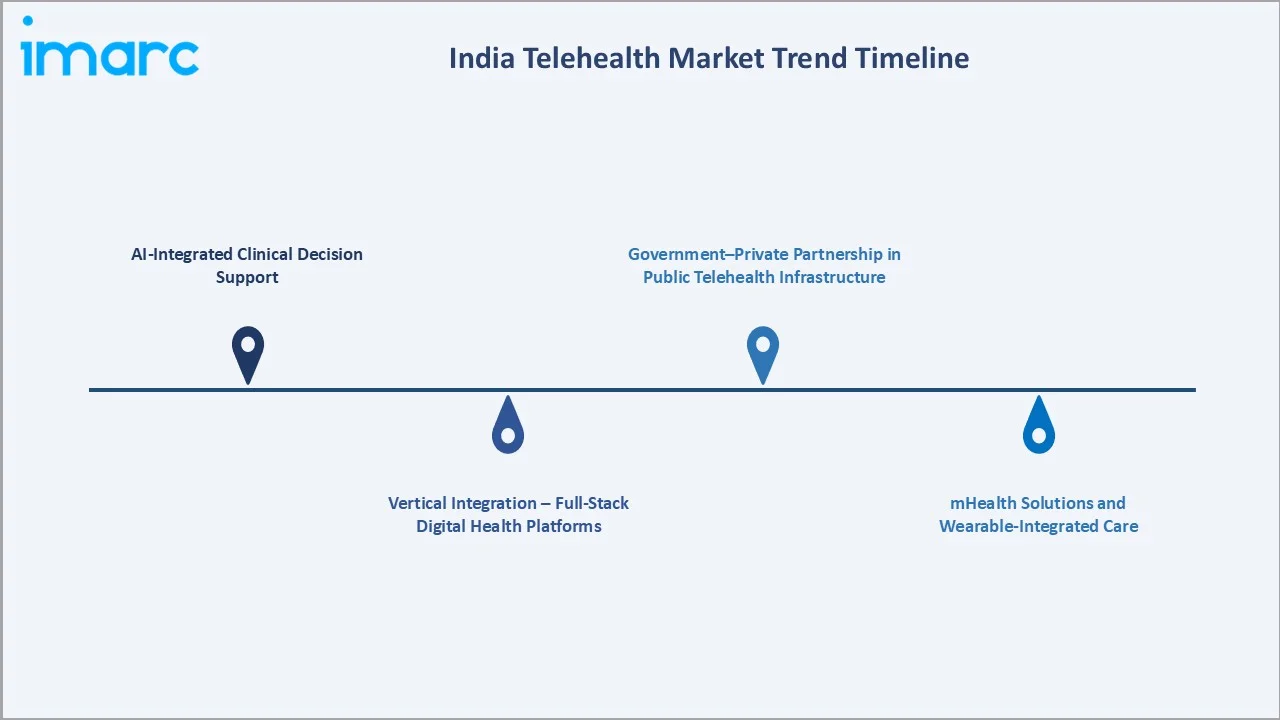

The following structural trends are reshaping the India telehealth market through 2034:

1. AI-Integrated Clinical Decision Support

The government of India's eSanjeevani AI-based Clinical Decision Support System (CDSS), developed between 2022-2024, has supported over 282 million consultations with standardised data capture and AI-generated diagnostic recommendations. Private platforms are deploying proprietary AI diagnostic engines, including cloud-based ECG interpretation and AI-driven triage algorithms, to differentiate clinically and improve consultation outcomes. This trend is accelerating the commercialisation of AI in primary care delivery.

2. Vertical Integration – Full-Stack Digital Health Platforms

Platform operators are moving beyond single-service teleconsultation to full-stack health ecosystems integrating teleconsultation, e-pharmacy, diagnostics, and health insurance. Tata 1mg's integrated platform bundles e-pharmacy, lab tests, and video consultations, targeting a closed-loop healthcare journey. Apollo Hospitals' partnership with Microsoft announced four AI healthcare copilots under a 'Hospital of the Future' vision in January 2025. This vertical integration trend creates higher patient lifetime values and deeper switching costs.

3. Government–Private Partnership in Public Telehealth Infrastructure

India's inclusion of eSanjeevani in IndiaStack as a global digital public good has created a model for government-private telehealth co-investment. The platform's integration across 1,55,000 Health and Wellness Centres creates a distribution network that private platforms can complement through specialty care layers above primary care coverage. The Tele-MANAS mental health helpline, operational since 2022, creates a template for public mental health telehealth that private platforms can build on commercially.

4. mHealth Solutions and Wearable-Integrated Care

The mHealth solutions segment, representing 27.9% of communication technology revenue in 2025, is growing above the overall market CAGR. Wearable health devices integrated with telehealth platforms create continuous patient monitoring capabilities, particularly for chronic disease management. HealthifyMe and similar fitness-health platforms are bridging the wellness-healthcare continuum, expanding the telehealth addressable market to preventive care and health optimisation services.

5. 5G-Enabled Telehealth and Remote Surgery Capabilities

India's 5G rollout, accelerating through 2024-2025, is enabling high-bandwidth telehealth applications including HD video consultations, real-time diagnostic imaging transfer, and IoT-enabled remote patient monitoring at scale. 5G's ultra-low latency is creating commercial viability for remote surgical assistance and tele-robotics in India's tertiary care segment, positioning India's telehealth market for capability expansion beyond consultation-only services through 2034.

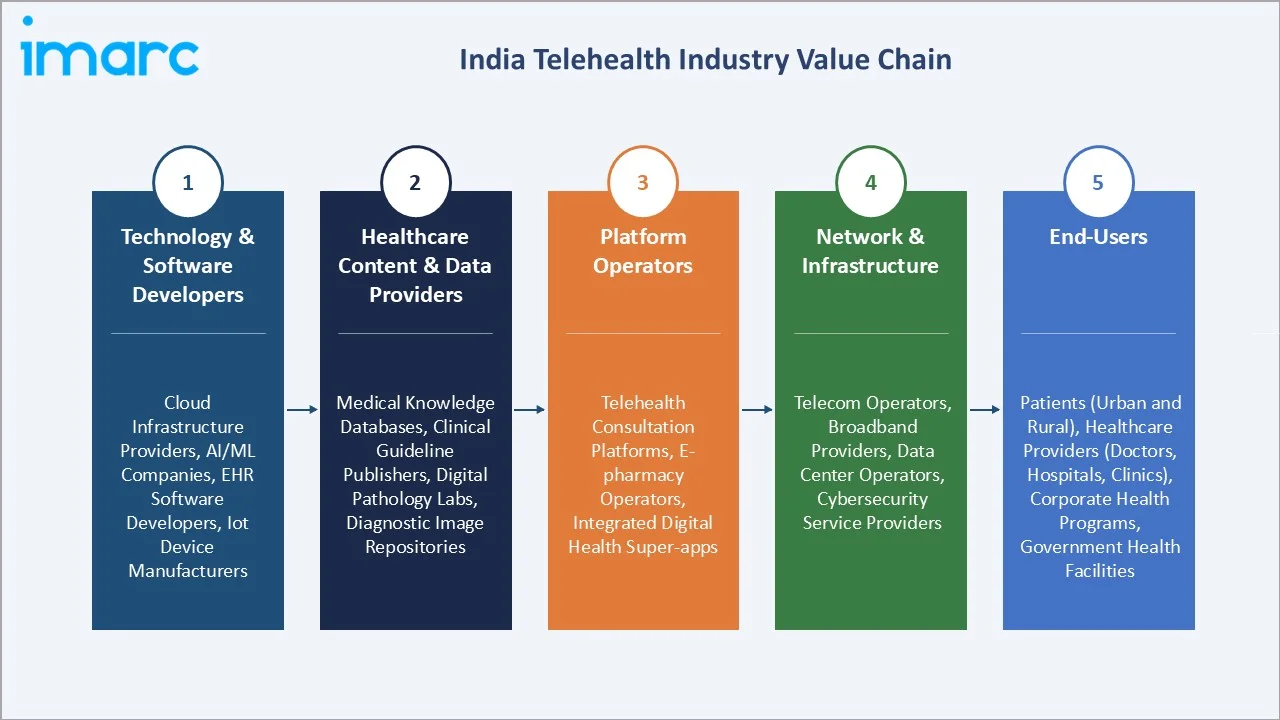

Industry Value Chain Analysis

India telehealth value chain integrates technology development, clinical content, platform operations, digital infrastructure, and patient-provider connectivity. Each stage contributes distinct capabilities to the overall service delivery model, creating a digitally integrated healthcare ecosystem.

|

Stage |

Key Participants |

|

Technology & Software Developers |

Cloud infrastructure providers, AI/ML companies, EHR software developers, IoT device manufacturers |

|

Healthcare Content & Data Providers |

Medical knowledge databases, clinical guideline publishers, digital pathology labs, diagnostic image repositories |

|

Platform Operators |

Telehealth consultation platforms, e-pharmacy operators, integrated digital health super-apps |

|

Network & Infrastructure |

Telecom operators, broadband providers, data center operators, cybersecurity service providers |

|

End-Users |

Patients (urban and rural), healthcare providers (doctors, hospitals, clinics), corporate health programs, government health facilities |

The platform operations stage is India telehealth value chain's most commercially consequential segment, where platform operators invest 20-30% of revenues in patient acquisition, technology development, and clinical network building. Government-provided infrastructure through eSanjeevani and ABDM health IDs reduces the fixed investment required for public-sector-facing telehealth deployments, improving unit economics for private operators building services on government digital health infrastructure.

Technology Landscape in the India Telehealth Industry

Artificial Intelligence and Clinical Decision Support

AI is the most commercially transformative technology in India's telehealth landscape. The government's AI-based CDSS deployed on eSanjeevani has processed data from over 282 million consultations, training machine learning models on India-specific disease patterns and treatment protocols. Commercial platforms are deploying AI diagnostic engines for dermatology, ophthalmology, radiology, and ECG interpretation, with some platforms achieving 95% diagnostic sensitivity. Natural Language Processing (NLP) models enabling multilingual consultation documentation are addressing India's linguistic diversity barrier.

Video Conferencing and Communication Infrastructure

Video conferencing infrastructure, representing 63.4% of communication technology revenue, has matured to support HD video at low-bandwidth conditions common in semi-urban India. WebRTC-based platforms enable browser-based teleconsultation without app downloads, reducing friction for first-time users. End-to-end encryption, HIPAA-equivalent security standards, and session recording capabilities are becoming standard features, improving clinical governance and regulatory compliance for telehealth platforms.

Remote Patient Monitoring (RPM) and IoT Integration

IoT-enabled remote patient monitoring devices, including Bluetooth-connected glucometers, blood pressure monitors, pulse oximeters, and ECG patches, are being integrated with telehealth platforms to enable continuous chronic disease management. The mHealth solutions segment (27.9% of communication technology in 2025) is the fastest-growing component of this trend. Platform operators integrating hardware devices with software consultation services are capturing higher per-patient revenue than consultation-only models.

Cloud Infrastructure and Data Security

Cloud-native architecture enables telehealth platforms to scale consultation capacity dynamically, a critical requirement given demand surges during health emergencies. India's domestic cloud providers (AWS India, Azure India, Google Cloud India) enable health data sovereignty compliance with India's Digital Personal Data Protection Act (2023). Blockchain-based patient health record management is being piloted to enable patient-controlled, portable health records that support multi-platform telehealth service utilisation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Software |

52.6% |

2025 |

|

Communication Technology |

Video Conferencing |

63.4% |

2025 |

|

Hosting Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

South India |

30.9% |

2025 |

By Component

Software leads the India telehealth market at 52.6% in 2025, driven by the platform-centric architecture of India's digital health ecosystem. Telehealth software includes consultation management systems, electronic health records, AI diagnostic tools, and patient engagement platforms. Service at 30.8% reflects the growing demand for managed telehealth services, including virtual ICU management and remote patient monitoring service contracts. Hardware at 16.6% covers medical devices, diagnostic equipment, and monitoring devices deployed in telehealth settings.

To access detailed market analysis, Request Sample

Software segment growth is further supported by India's domestic IT sector expertise in SaaS product development, creating a competitive cost advantage for Indian telehealth software platforms versus imported alternatives. The service segment is growing as hospital networks outsource telehealth operations management to specialized service providers, creating a B2B service layer above direct-to-consumer platform models.

By Communication Technology

Video conferencing dominates at 63.4% in 2025, reflecting its clinical effectiveness for specialist teleconsultation and its equivalency with in-person clinical interaction for history-taking and visual assessment. eSanjeevani's hub-and-spoke video consultation model, connecting over 1,55,000 village-level clinics with urban specialist hubs, operationalises video conferencing at national scale. mHealth Solutions at 27.9% represents mobile-app-based asynchronous consultation, prescription management, and health monitoring services. Others at 8.7% includes telephone-based consultations and text-based clinical communication platforms.

mHealth solutions are growing fastest within the communication technology segment, driven by the convenience of asynchronous mobile-app-based care and the integration of wearable health monitoring devices with platform consultation workflows. The Others segment, while smallest, includes telephonic consultation services that serve digitally excluded rural populations through ASHA health worker-assisted access models.

Regional Market Insights

|

Region |

Share (2025) |

Key Telehealth Market Drivers & Characteristics |

|

South India |

30.9% |

Driven by Bengaluru and Chennai's IT-sector workforce, high digital literacy, and strong healthcare infrastructure. Advanced specialist availability and high per-capita income support premium telehealth adoption. |

|

North India |

28.7% |

Supported by Delhi-NCR's high disposable income, well-developed healthcare ecosystem, and strong corporate health program adoption. Large patient population in Uttar Pradesh drives eSanjeevani utilisation. |

|

West & Central India |

24.6% |

Mumbai and Pune's financial sector concentration and Gujarat's entrepreneurial economy drive corporate and consumer telehealth adoption. Maharashtra is among India's top states for eSanjeevani consultations. |

|

East India |

15.8% |

Rising internet penetration, growing urban professional class in Kolkata, and improving connectivity in Odisha and Northeast India are supporting above-market-average growth from a lower base. |

South India's 30.9% market leadership reflects Bengaluru's position as India's technology capital, combining high digital literacy among IT professionals with access to premium specialist care. Andhra Pradesh is the leading state on eSanjeevani consultations as of March 2025, demonstrating South India's depth of telehealth adoption across urban and rural populations. Tamil Nadu's manufacturing-based economic strength supports corporate health program adoption for factory worker telehealth access.

North India's 28.7% reflects Uttar Pradesh's large rural patient population accessing eSanjeevani government services, combined with Delhi-NCR's premium private telehealth consumption. East India at 15.8% represents the highest-growth geographic opportunity, with digital infrastructure improvements and rising urban incomes creating first-generation telehealth demand from a comparatively lower adoption base.

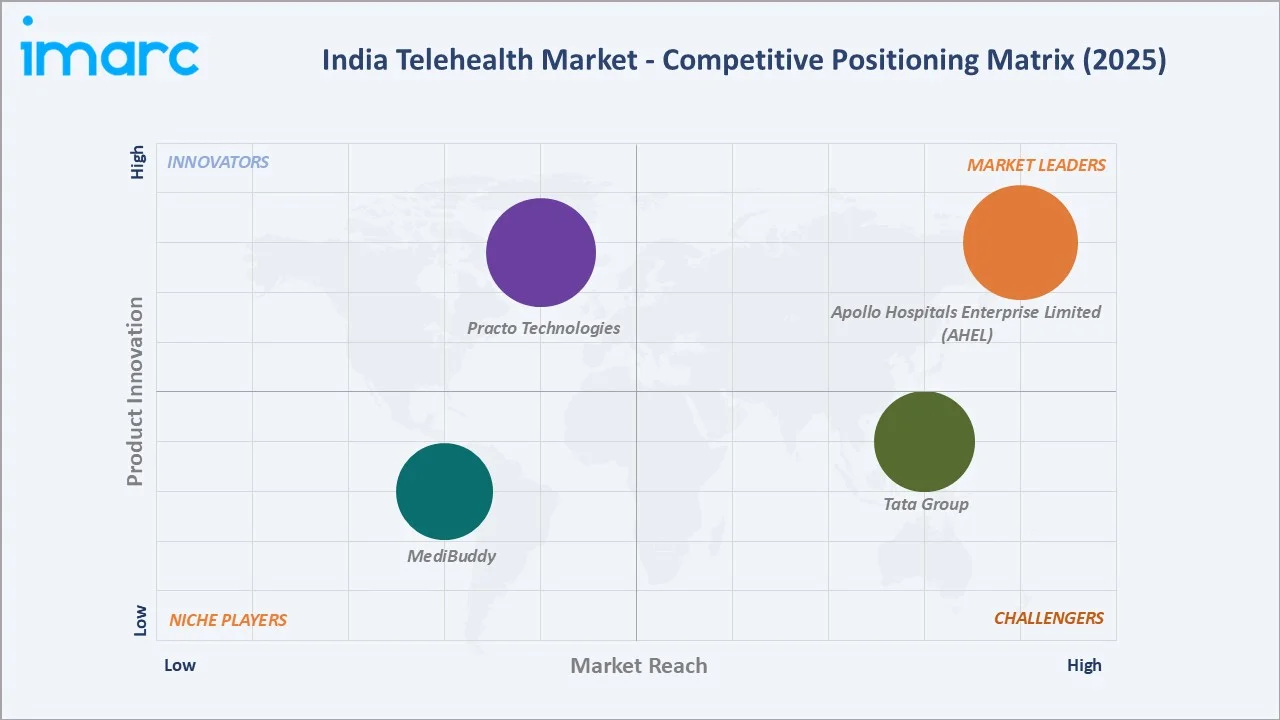

Competitive Landscape

India telehealth competitive landscape is moderately fragmented, with over 200 active platforms spanning e-consultation, e-pharmacy, and remote patient monitoring niches. Apollo TeleHealth, Tata 1mg, and Practo represent the top three by user engagement and revenue scale. The government's eSanjeevani platform, operating on a non-commercial public service model, creates a parallel public-sector telehealth layer that private operators build specialist and premium care services above.

|

Company |

Key Platforms/Brands |

Market Position |

Core Strength |

|

Apollo Hospitals Enterprise Limited (AHEL) |

Apollo 24|7, Apollo TeleHealth |

Market Leader |

Large-scale, technology-enabled rural and remote healthcare delivery. |

|

Tata Group |

Tata 1mg |

Strong Challenger |

Integrated full-stack ecosystem, allowing users to seamlessly transition from an online doctor consultation to e-pharmacy delivery and at-home diagnostics. |

|

Practo Technologies |

Practo |

Innovator |

Integrated digital ecosystem, pairing a massive consumer base with SaaS solutions that digitize local clinics and hospitals. |

|

MediBuddy |

MediBuddy |

Niche Player |

Massive, technology-driven "phygital" ecosystem; hyper-localized care covering over 95% of Indian pin codes. |

The competitive dynamic is defined by vertical integration as the primary strategy for market leadership consolidation. Tata Digital's acquisition of 1mg combined e-commerce depth with healthcare service delivery. Niche AI-driven disruptors are building defensible IP through proprietary clinical algorithms that create competitive moats against larger full-stack platforms.

Key Company Profiles

Apollo Hospitals Enterprise Limited (AHEL)

Apollo TeleHealth Services, a subsidiary of Apollo Hospitals Enterprise Ltd., is India's pioneer and leading commercial telehealth operator. The company operates across teleconsultation, remote patient monitoring, and hospital telehealth infrastructure management.

- Key Platforms: Apollo 24|7, Apollo TeleHealth

- Recent Developments: In January 2025, Apollo Hospitals and Microsoft announced four AI healthcare copilots under a 'Hospital of the Future' vision, integrating AI into clinical workflows and teleconsultation.

- Strategic Focus: Leveraging hybrid physical-digital care delivery model, combining India's largest private hospital network with digital teleconsultation to create a comprehensive healthcare ecosystem.

Tata Group

Tata 1mg, acquired by Tata Digital and operating as part of the Tata Group's consumer digital ecosystem, is India's leading integrated digital health platform combining e-pharmacy, lab test booking, and video teleconsultation.

- Key Platforms: Tata 1mg, 1mg Healthcare Solutions.

- Recent Developments: In April 2025, Tata 1mg planned to raise USD 300 million to expand its integrated platform capabilities. The company launched video consultations across 20+ specialties, targeting Tier-3 cities and semi-urban populations.

- Strategic Focus: Full-stack health ecosystem strategy combining e-pharmacy depth with teleconsultation and diagnostics for a closed-loop patient journey, leveraging Tata Group's consumer trust and digital distribution.

Practo Technologies

Practo is India's largest healthcare discovery and appointment-booking platform, expanding into teleconsultation with a vertically integrated B2C and B2B SaaS model. Practo is the only profitable startup in India's leading telehealth segment.

- Key Platforms: Practo (consumer app), Practo Ray (clinic management SaaS).

- Recent Developments: In December 2024, Practo launched Practo Assured, a verified network of high-quality hospitals and clinics designed to make it easier for patients to find and choose trustworthy care providers.

- Strategic Focus: Dual B2C (patient) and B2B SaaS (clinic) model creating dual revenue streams; continuing profitable growth above capital-intensive competitors.

Market Concentration Analysis

India telehealth market is moderately fragmented at the platform layer, with over 200 active platforms competing across consultation, e-pharmacy, and remote monitoring niches. No single private operator commands above 20-25% of India's total telehealth market by transaction volume, creating a competitive market structure that sustains innovation and pricing competition. The government's eSanjeevani platform, while dominant in consultation volume at 0.4-0.45 million consultations daily, operates in the public-access non-commercial segment.

The top three private operators – Apollo TeleHealth, Tata 1mg, and Practo – collectively represent an estimated 35-45% of India's organized private telehealth market revenue in 2025. Market concentration is increasing through a dual process: Tata 1mg's vertical integration and Apollo's hybrid model are consolidating the premium urban segment, while government expansion of eSanjeevani is consolidating the public rural primary care segment. Smaller single-service platforms face margin compression as full-stack operators leverage bundled service economics.

Investment & Growth Opportunities

Highest Growth Segments

AI-powered diagnostics (above 30% CAGR from a small base), mental health teleconsultation (above 25% CAGR driven by India's 197 million people with mental health conditions and fewer than 0.3 psychiatrists per 100,000 population), remote patient monitoring for chronic diseases, and Tier-2/3 city telehealth expansion (above 28% CAGR as connectivity and digital literacy improvements expand the addressable market) represent India's highest-growth telehealth investment vectors through 2034.

Emerging Investment Opportunities

India's AI clinical decision support market for primary care, growing above 30% annually, represents the highest-CAGR sub-segment. The deployment of indigenous AI models trained on India's disease epidemiology, rather than Western clinical data, creates a defensible IP moat for platforms that invest in proprietary model development. The government's inclusion of eSanjeevani in IndiaStack, positioning it as a global digital public good, creates an international market opportunity for India's telehealth technology platforms.

Investment Themes

- AI Diagnostic Platform Investment for India's Chronic Disease Management Market: India's 100 million+ diabetic patients and 300 million+ hypertensive individuals create the world's largest addressable chronic disease management opportunity for AI-integrated remote monitoring platforms. Platforms combining IoT devices, AI diagnostic algorithms, and teleconsultation into subscription-based chronic care programs generate above-market unit economics.

- Tier-2 City Telehealth Platform Investment for India's Most Underserved High-Growth Demographic: India's secondary cities combining rising income levels with inadequate specialist infrastructure represent the geographic sweet spot for telehealth platform investment – large addressable markets, lower competition, and higher willingness to pay for quality remote specialist access than rural populations.

Future Market Outlook (2026-2034)

India telehealth market is projected to grow from USD 911.9 Million in 2025 to USD 5,858.9 Million by 2034, delivering a 22.04% CAGR over the forecast period. The market's anchor value of USD 2,468.8 Million in 2030 represents India's telehealth industry at a structural inflection, where AI-integrated platforms, chronic disease management subscriptions, and Tier-2 city penetration create diversified revenue streams above the episodic consultation model that defined the market's first phase.

Three structural forces define India telehealth market growth through 2034: India's digital infrastructure maturation (5G, cloud, AI) expanding the technical scope of deliverable care above consultation-only services; India's demographic dividend creating the world's largest new digital health consumer class; and government policy continuity through ABDM, eSanjeevani, and Tele-MANAS creating institutional infrastructure that sustains telehealth adoption above discretionary consumer demand cyclicality.

The software segment will maintain its dominant share as platform operators invest in AI, clinical governance technology, and integrated health ecosystem architecture. Video conferencing will remain the primary communication modality while mHealth solutions grow fastest as wearable integration and asynchronous care management gain clinical acceptance. South India will sustain regional leadership while East India delivers above-national-average growth from its current underrepresented position.

Research Methodology

Primary Research

Primary research comprised structured interviews with India telehealth industry stakeholders, including CEOs of telehealth platforms, Chief Digital Health Officers at leading hospital groups, technology investors active in India's digital health sector, government health IT officials, corporate HR executives managing employee health benefits, and patient survey data from urban and semi-urban telehealth users across South, North, West, and East India.

Secondary Research

Secondary research encompassed India Ministry of Health and Family Welfare eSanjeevani operational data, ABDM health ID registration data, National Health Mission reports, company annual reports and investor presentations (Apollo Hospitals, Tata Digital), regulatory publications from the Indian Medical Council and National Medical Commission, and industry association data from the Digital Health Association of India. Over 60 secondary sources reviewed. Government data from pib.gov.in, mohfw.gov.in, and abdm.gov.in were primary data sources.

Forecasting Models

Market revenue forecasts were developed using a bottom-up patient-need stratification model: India's addressable patient population by disease category multiplied by teleconsultation adoption rate, average consultation frequency, and average revenue per consultation. Adoption rate curves were calibrated against eSanjeevani's public consultation growth trajectory (2019-2025) and private platform growth benchmarks. CAGR validation was performed against comparable emerging market telehealth trajectories (China 2015-2020, Brazil 2018-2023).

India Telehealth Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Software, Hardware, Service |

| Communication Technologies Covered | Video Conferencing, mHealth Solutions, Others |

| Hosting Types Covered | Cloud-Based and Web-Based, On-Premises |

| Applications Covered | Teleconsultation and Telementoring, Medial Education and Training, Teleradiology, Telecardiology, Tele-ICU, Tele-Psychiatry, Tele-Dermatology, Others |

| End Users Covered | Providers, Patients, Payers, Others |

| Regions Covered | South India, East India, West and Central India, North India |

| Companies Covered | Apollo Hospitals Enterprise Limited (AHEL), Tata Group, Practo Technologies, MediBuddy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India telehealth market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India telehealth market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India telehealth industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Telehealth Market Report

India telehealth market reached USD 911.9 Million in 2025, driven by smartphone adoption, government digital health initiatives, post-COVID behavioral shift toward remote care, and India's structural doctor shortage.

India telehealth market grows at a 22.04% CAGR during 2026-2034, reaching USD 5,858.9 Million by 2034, supported by AI integration, 5G rollout, chronic disease burden, and expanding rural digital access.

Software leads at 52.6% in 2025, driven by platform-centric telehealth ecosystems integrating teleconsultation, EHR, AI diagnostics, and e-pharmacy into unified digital health products.

Video conferencing leads at 63.4% in 2025, reflecting its clinical equivalence to in-person consultation for specialist care. Government platform eSanjeevani facilitates 0.4-0.45 million video consultations daily.

South India leads at 30.9% in 2025, driven by Bengaluru and Chennai's IT workforce, high digital literacy, premium healthcare demand, and Andhra Pradesh's strong eSanjeevani utilisation.

India telehealth market is projected to reach approximately USD 2,468.8 Million by 2030, anchoring mid-period growth at AI-integrated care platform expansion and Tier-2 city market development.

Leading companies include Apollo Hospitals Enterprise Limited (AHEL), Tata Group, Practo Technologies, and MediBuddy, alongside government platform eSanjeevani.

Growth is driven by 1 billion internet users, government ABDM infrastructure, 22.04% CAGR from 2026-2034, chronic disease burden, and post-COVID patient acceptance of remote healthcare delivery.

AI diagnostics, mental health teleconsultation, chronic disease remote monitoring, and Tier-2 city platform expansion represent the highest-growth investment opportunities in India's telehealth market.

AI enables clinical decision support, diagnostic imaging analysis, and remote triage at scale. eSanjeevani's AI-CDSS has supported over 282 million consultations, improving diagnostic accuracy in primary care.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)