Japan Industrial Lubricants Market Size, Share, Trends and Forecast by Product Type, Base Oil, End Use Industry, and Region, 2026-2034

Japan Industrial Lubricants Market Size, Share, Trends & Forecast (2026-2034)

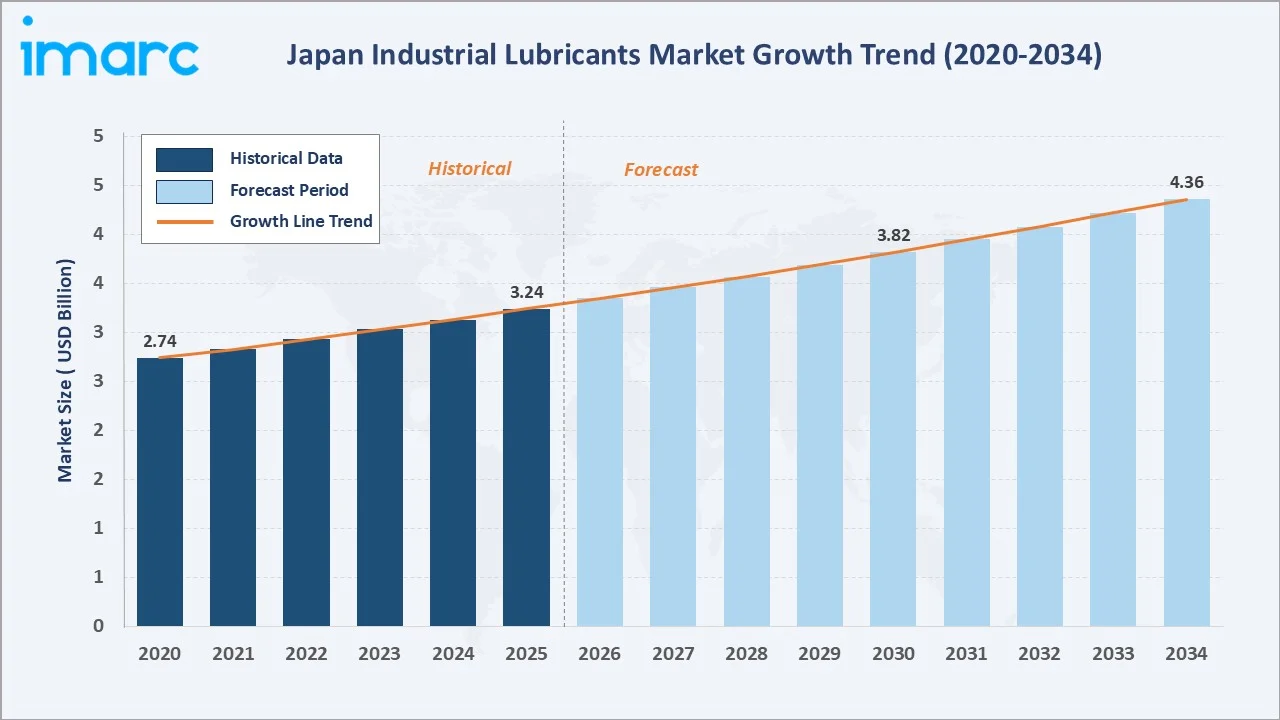

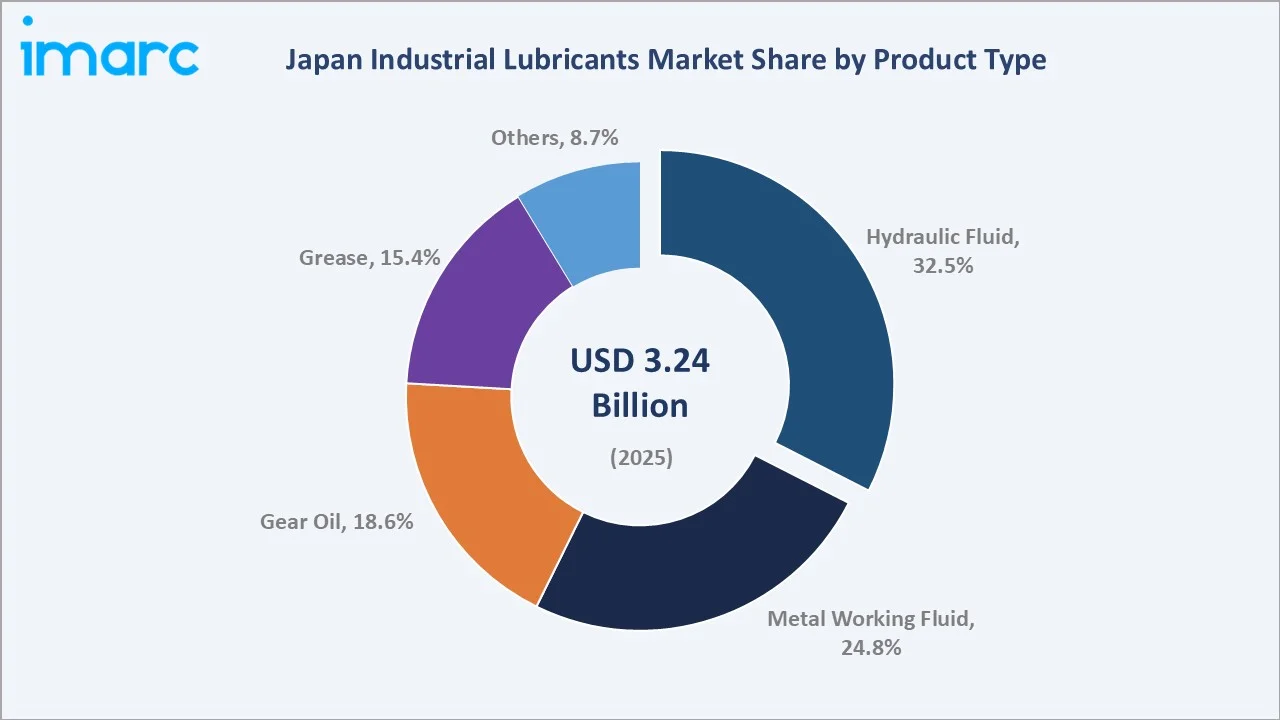

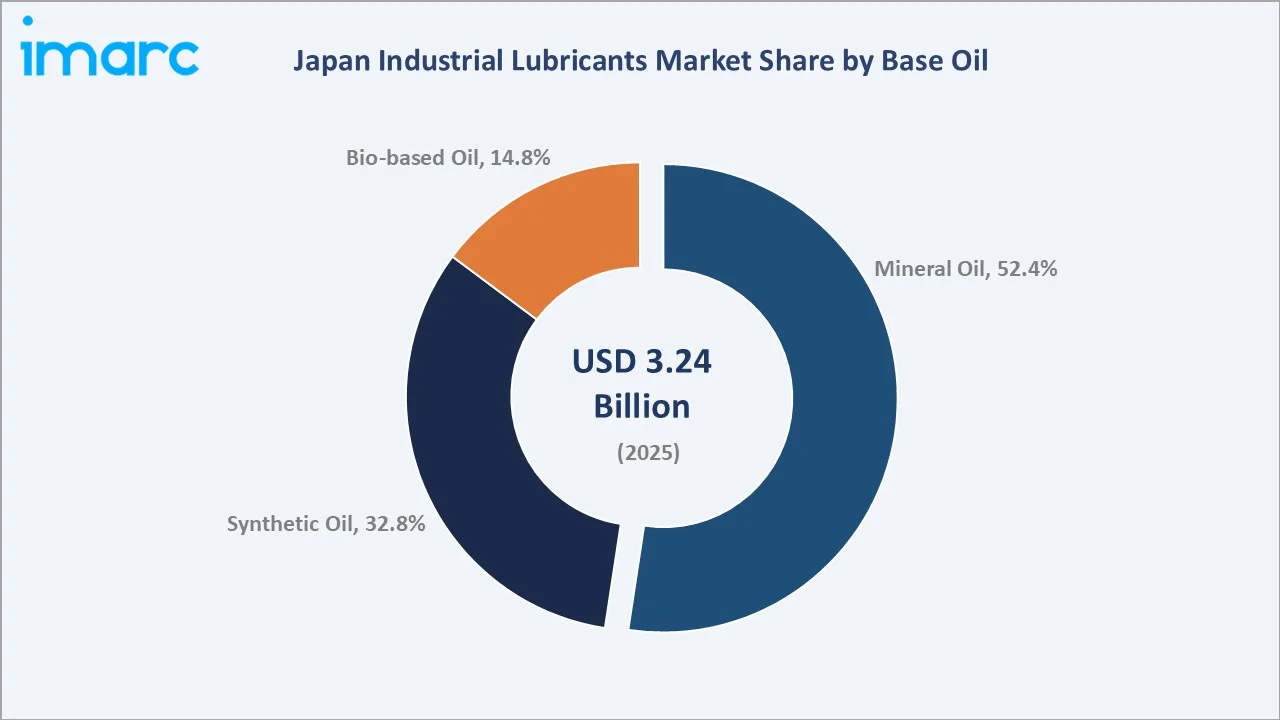

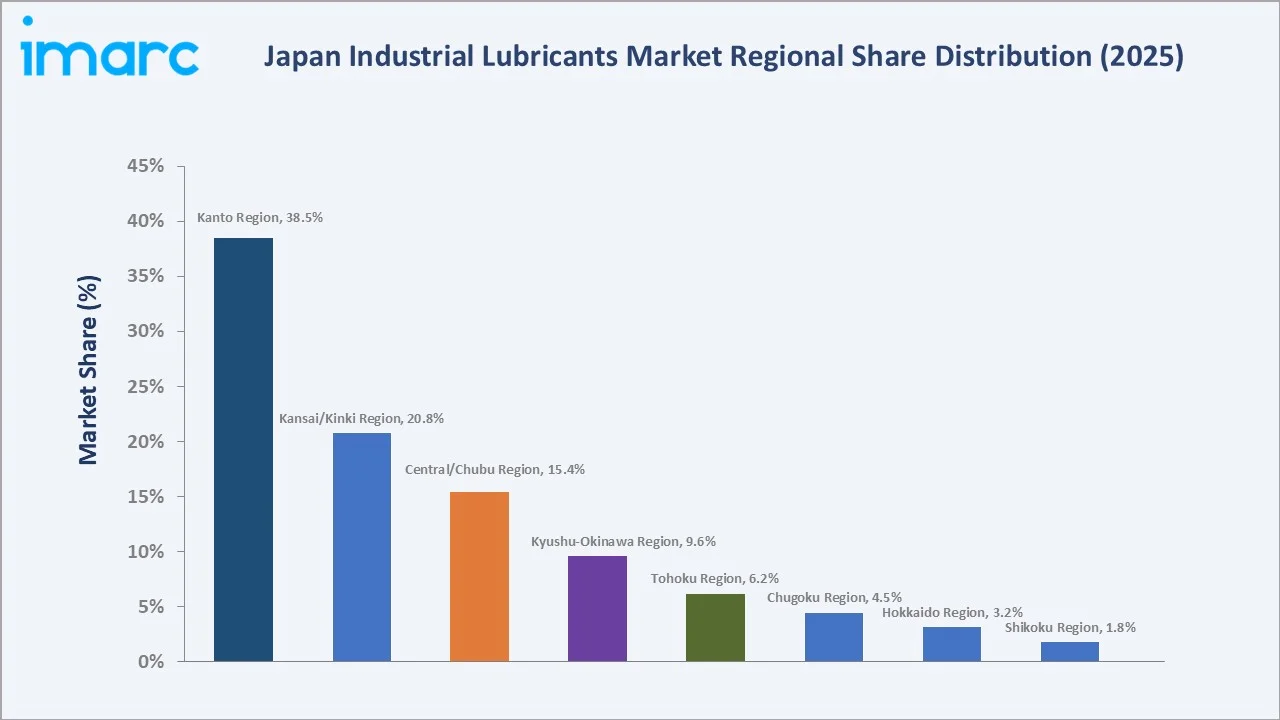

The Japan industrial lubricants market was valued at USD 3.24 Billion in 2025 and is projected to reach USD 4.36 Billion by 2034, expanding at a CAGR of 3.37% during the forecast period (2026-2034). Growth is underpinned by Japan’s manufacturing renaissance, driven by semiconductor reshoring, EV transition creating specialty lubricant demand, and Japan’s GX (Green Transformation) policy, which targets to invest 20 trillion yen in public and private sector decarbonization over the next 10 years, accelerating bio-based and high-performance synthetic lubricant adoption. Hydraulic fluid dominates at 32.5% product type share, while mineral oil leads the base oil at 52.4%. The Kanto region commands 38.5% of the market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.24 Billion |

|

Forecast Market Size (2034) |

USD 4.36 Billion |

|

CAGR (2026-2034) |

3.37% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

Kanto (38.5%, 2025) |

|

Fastest Growing Region |

Kyushu-Okinawa (CAGR ~3.9%, 2026-2034) |

The Japan industrial lubricants market expanded from USD 2.74 Billion in 2020 to USD 3.24 Billion in 2025, reflecting Japan’s post-COVID industrial restart and automation-driven lubricant upgrade demand. Anchored at USD 3.82 Billion in 2030, the forecast is to USD 4.36 Billion by 2034, driven by premium synthetic lubricant transitions, infrastructure spending, and bio-based lubricant adoption.

To get more information on this market, Request Sample

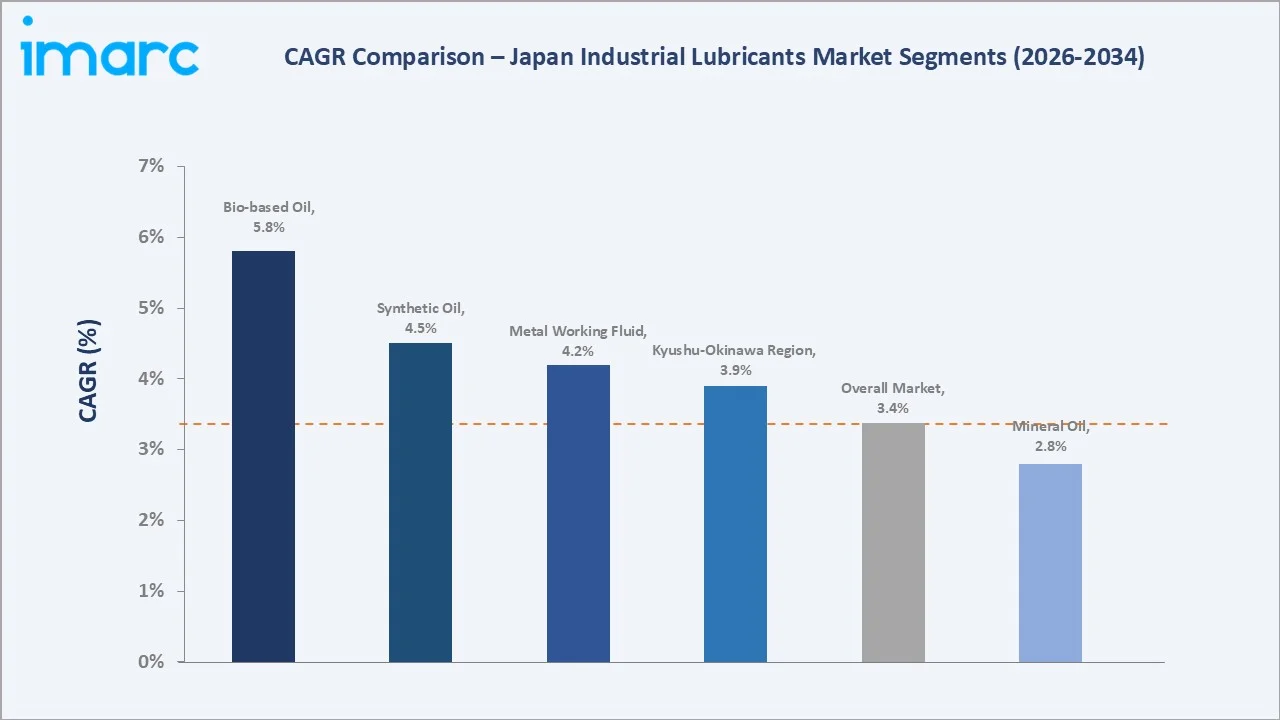

The CAGR across key segments with bio-based oil at ~5.8% CAGR is the fastest-growing base oil segment, reflecting METI’s 2025 industrial bio-lubricant procurement guidelines and Japan’s carbon neutrality 2050 target accelerating eco-friendly lubricant transitions. Synthetic oil at ~4.5% CAGR outpaces mineral oil at ~2.8%, as Japan’s precision manufacturing sector upgrades to high-performance Group III/IV base oil formulations delivering 5–15% energy consumption reduction per industrial machine.

Executive Summary

The Japan industrial lubricants market has grown steadily from USD 2.74 Billion in 2020 to USD 3.24 Billion in 2025. The forecast trajectory to USD 4.36 Billion by 2034 at a 3.37% CAGR reflects the positive offset from three powerful demand drivers: Japan’s semiconductor manufacturing renaissance creating new high-purity metalworking fluid and specialty lubricant demand; Japan’s EV transition requiring new specialty e-drive transmission fluids, electric motor greases, and thermal management lubricants fundamentally different from conventional ICE lubricants; and Japan’s GX policy framework mandating green procurement targets that are systematically shifting industrial lubricant specifications toward bio-based and synthetic formulations commanding price premiums over conventional mineral oil products.

Hydraulic fluid’s 32.5% dominance reflects the breadth of Japan’s hydraulic equipment base spanning construction machinery, industrial press and forming equipment, injection moulding machines, and factory automation servo-hydraulic systems. Metal working fluid at 24.8% is growing fastest at ~4.2% CAGR, driven by semiconductor fab metalworking fluid requirements, automotive EV component precision machining, and Japan’s world-leading machine tool industry requiring ISO-compliant metalworking fluid specifications. Mineral oil’s 52.4% base oil dominance reflects established supply chain relationships, cost competitiveness, and proven performance in traditional industrial applications, while synthetic oil at 32.8% and bio-based oil at 14.8% represent Japan’s systematic base oil premiumization trend.

The Kanto region’s 38.5% dominance reflects Greater Tokyo’s role as Japan’s primary industrial hub, combining Tokyo’s advanced manufacturing, Kanagawa’s automotive and chemical industries, and the expanding semiconductor corridor from Ibaraki to Yamanashi. The Chubu region’s 15.4% share underscores Toyota City’s global significance as the most concentrated automotive manufacturing cluster in the world.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Hydraulic Fluid – 32.5% revenue share (2025) |

|

Dominant Base Oil |

Mineral Oil – 52.4% revenue share (2025) |

|

Leading Region |

Kanto – 38.5% revenue share (2025) |

|

Fastest Growing Region |

Kyushu-Okinawa (CAGR ~3.9%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Hydraulic fluid at 32.5% (2025) leads Japan’s industrial lubricants by product volume because of the extraordinary density of hydraulic-powered machinery across Japan’s manufacturing ecosystem. As of September 2024, the World Robotics report recorded 435,299 industrial robots working in Japan's factories, each requiring 5–20 liters of high-performance hydraulic fluid annually.

- Mineral oil’s 52.4% (2025) dominance reflects Japan’s large installed base of conventional industrial equipment, where JASO-specified mineral oil products deliver adequate performance at lower cost than equivalent synthetic formulations.

- The Kanto Region’s 38.5% dominance represents the industrial gravity of Greater Tokyo. There are more than 660,000 businesses in Tokyo, with Kawasaki’s Chemical Industry Belt and Yokohama’s precision manufacturing clusters representing the highest density of industrial lubricant consumption per square kilometer in Japan.

- Kyushu-Okinawa at 9.6% is the fastest-growing region at ~3.9% CAGR, driven by the TSMC Japan semiconductor manufacturing complex in Kumamoto and subsequent supply chain manufacturing investment in Kyushu’s Kumamoto and Fukuoka prefectures.

Japan Industrial Lubricants Market Overview

Japan’s industrial lubricants market encompasses the manufacture, blending, distribution, and sale of petroleum-derived, synthetic, and bio-based lubricating oils, greases, metalworking fluids, and specialty process fluids used in industrial machinery, manufacturing processes, and power generation across Japan’s 47 prefectures. The ecosystem integrates domestic refiner-manufacturers, international majors with Japan operations, German specialty lubricant specialists, and Japan-origin specialty manufacturers.

Applications span hydraulic systems, metalworking and machining, gear lubrication, bearing greases, and process fluids. Macroeconomic influences include Japan’s manufacturing output, yen exchange rate, Japan’s GX policy investment targets, and JIS/JASO industrial lubricant quality standards.

Market Dynamics

To evaluate market opportunities, Request Sample

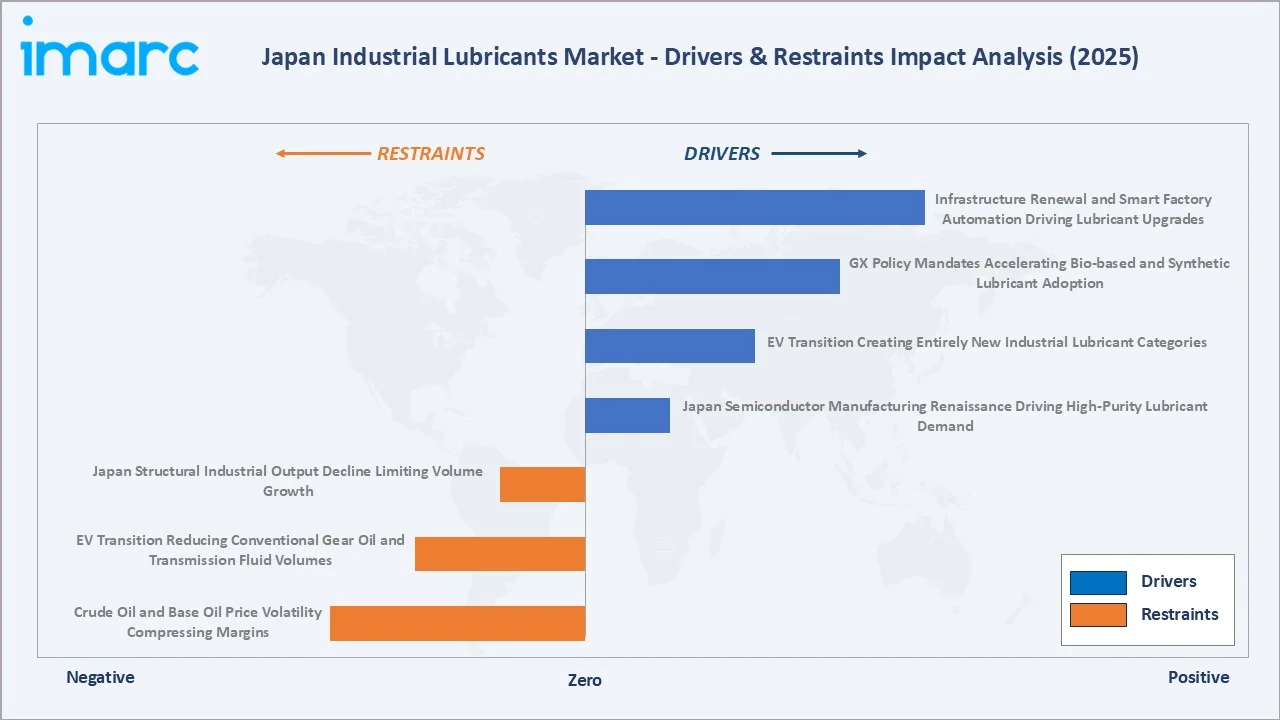

Market Drivers

- Japan’s Semiconductor Manufacturing Renaissance Driving High-Purity Lubricant Demand: The Japanese government allocated an additional 631.5 billion yen in subsidies to Rapidus, a semiconductor foundry company it is supporting to revive the country's domestic semiconductor industry and recover from the "lost 30 years” which has triggered the largest wave of new fab construction in Japan.

- EV Transition Creating Entirely New Industrial Lubricant Categories: Japan’s automotive industry, the world’s fourth-largest automotive market, with 4,421,494 new passenger vehicles sold in Japan in 2024. E-drive fluid requirements, EV battery thermal management oil, and electric motor bearing grease represent fundamentally different formulation requirements than conventional ICE lubricants, commanding price premiums.

- GX Policy Mandates Accelerating Bio-based and Synthetic Lubricant Adoption: Japan’s GX (Green Transformation) policy, which targets to invest 20 trillion yen in public and private sector decarbonization over the next 10 years, includes mandatory green procurement requirements for public infrastructure machinery lubricants, biodegradable lubricant specifications for forestry and waterway maintenance machinery, and industrial carbon footprint reporting that incentivizes lower-emission synthetic and bio-based lubricants.

Market Restraints

- Japan’s Structural Industrial Output Decline Limiting Volume Growth: Japan Industrial output decreased by 1.6% year-on-year, a significant acceleration from the 0.4% decline in July 2025. This structural volume decline limits Japan’s industrial lubricant market’s total volume growth regardless of price premiumization trends.

- EV Transition Reducing Conventional Gear Oil and Transmission Fluid Volumes: Japan’s BEVs’ single-speed reduction gear eliminates 5–10-speed ICE transmission, reducing per-vehicle gear oil consumption.

- Crude Oil and Base Oil Price Volatility Compressing Margins: In 2024, Japan relies on imports for nearly all of its crude oil, with 95% sourced from the Middle East. The oil is primarily imported from the United Arab Emirates (UAE) at 44%, Saudi Arabia at 40%, Kuwait at 7%, and Qatar at 4%, making domestic lubricant base oil prices directly correlated with global crude price cycles.

Market Opportunities

- Predictive Lubrication and IoT Oil Condition Monitoring: Industry 4.0 factories in Japan’s Kanto and Chubu regions are deploying IoT oil condition monitoring systems, inline viscosity sensors, particle counters, and moisture analyzers, that enable condition-based oil drain intervals, extending lubricant service life and creating data-driven lubricant performance services revenue.

- Food-Grade and NSF H1 Lubricant Premium Market Expansion: Japan exports of agriculture, forestry and fishery products and foods rose to over 1.7 trillion yen ($10.9 billion) in 2025, and is systematically upgrading to NSF H1/H2 certified lubricants to meet increasingly stringent food safety regulations under the Food Sanitation Act 2018 revision and FSSC 22000 certification requirements adopted by companies.

Market Challenges

- Regulatory Complexity of Green Procurement Compliance: Japan’s Green Procurement Law (Law Concerning the Promotion of Procurement of Eco-Friendly Goods and Services by the State) and MLIT’s public works procurement specifications create complex, evolving compliance requirements for lubricant suppliers serving government infrastructure projects.

- Intensifying Price Competition from Import Products: Chinese lubricant manufacturers are aggressively entering Japan’s lower-tier industrial lubricant market through local distributors, offering Group II mineral oil lubricants at 20–30% below ENEOS and Idemitsu domestic pricing.

Emerging Market Trends

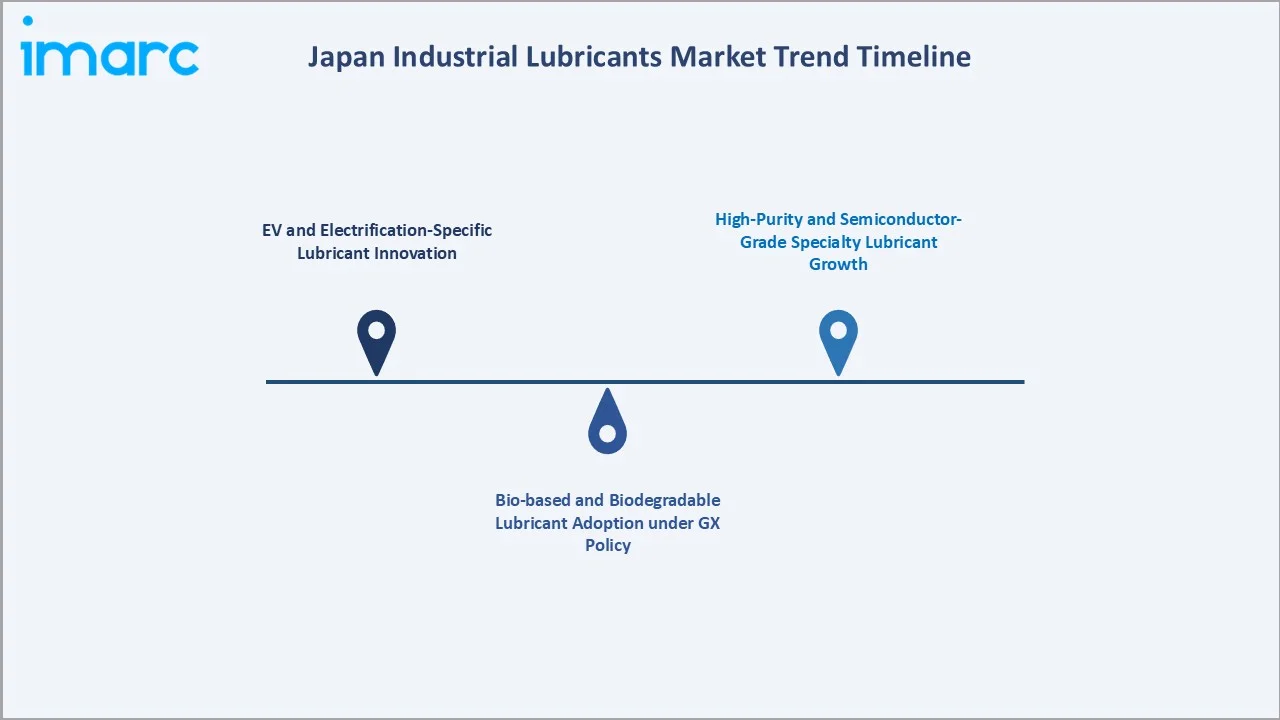

1. EV and Electrification-Specific Lubricant Innovation

Japan’s automotive electrification is generating an entirely new industrial lubricant category, e-Fluids, encompassing e-drive transmission fluid, dielectric battery cooling oil, and electric motor bearing grease. In July 2025, Shell and the Nissan Formula E Team revealed the extension of their ongoing technical collaboration in the FIA Formula E World Championship and co-developed a specialized series of E-Thermal fluids.

2. Bio-based and Biodegradable Lubricant Adoption under GX Policy

Japan’s GX Green Transformation policy is creating mandatory bio-based lubricant demand in public infrastructure sectors. MLIT’s 2024 updated construction machinery procurement specifications now require EU Ecolabel-equivalent biodegradable hydraulic fluid for all public works machinery operating near waterways, forests, and drinking water sources, covering construction machines.

3. High-Purity and Semiconductor-Grade Specialty Lubricant Growth

Japan’s semiconductor manufacturing expansion is creating demand for a new category of ultra-high-purity industrial lubricants where specifications are measured in ppb (parts per billion) contamination levels versus conventional industrial lubricant ppm (parts per million) standards.

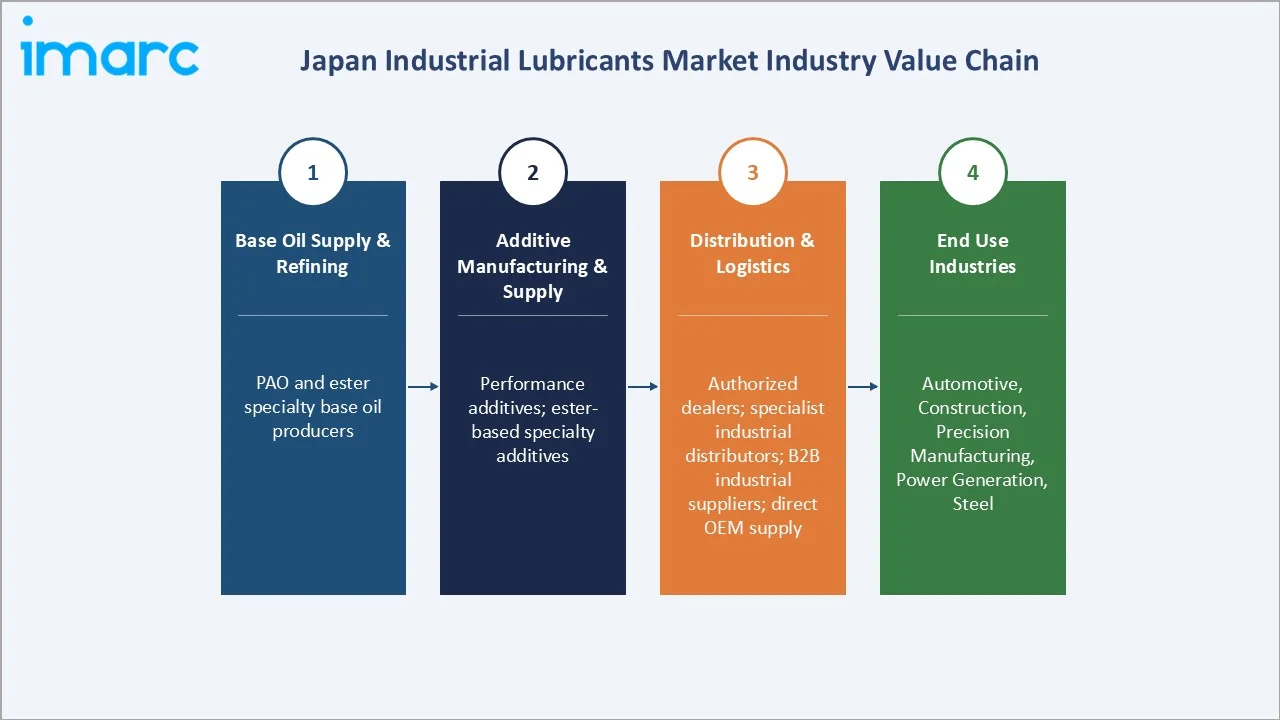

Industry Value Chain Analysis

Japan’s industrial lubricants value chain integrates domestic crude oil refining, base oil production, additive supply, blending and formulation, multi-tier distribution, and specialized industrial end-user applications across the country’s 47 prefectures.

|

Stage |

Key Participants |

|

Base Oil Supply & Refining |

PAO and ester specialty base oils |

|

Additive Manufacturing & Supply |

Performance additives, fuel and lubricant additives, ester-based additives, specialty lubricant additives, phosphate ester-based additives |

|

Distribution & Logistics |

Authorized dealers network, specialist industrial lubricant distributors, B2B industrial supplies, and direct OEM supply |

|

End Use Industries |

Automotive, Construction, Precision Manufacturing, Power Generation, Steel |

ENEOS and Idemitsu’s vertically integrated refining-blending-distribution model gives domestic producers a structural cost advantage, as Group I/II base oil from domestic refineries combined with direct industrial sales forces generates gross margins 5–8 percentage points higher than international majors’ blending-only Japan operations.

Technology Landscape in the Japan Industrial Lubricants Industry

Advanced Synthetic Base Oil Technologies: PAO, Ester, and Group III+

Japan’s industrial lubricant market’s premiumization is driven by advances in synthetic base oil technology. Polyalphaolefin (PAO) base oils offer -60+°C pour points and 130-270°C+ flash points, enabling year-round operation. These premium base oils are enabling ISO VG 15–22 ultra-low-viscosity formulations for energy-efficient industrial gear oils, a rapidly growing segment in Japan’s energy conservation-mandated manufacturing sector.

Additive Technology for EV and Electrified Drivetrain Applications

EV lubricant formulation requires entirely new additive packages that avoid copper corrosion, withstand high-frequency (kHz range) alternating electric fields without electrostatic discharge, and maintain thermal stability under 800V battery pack thermal management operating conditions.

Digital Oil Condition Monitoring and IoT Lubrication Management

MEMS (Micro-Electromechanical Systems) oil condition sensors measuring viscosity, water content, oxidation products, and particle contamination in real time are being integrated into Japan’s KPK (Konomi Production Kaizen) smart factory systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Hydraulic Fluid |

32.5% |

2025 |

|

Base Oil |

Mineral Oil |

52.4% |

2025 |

|

End Use Industry |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

38.5% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Hydraulic fluid leads at 32.5% market share (2025). This category’s dominance reflects Japan’s massive hydraulic machinery base and Japan’s extensive industrial press infrastructure for automotive and aerospace component forming. Komatsu is the largest Japanese construction OEM and the second-largest global construction OEM by market share. The hydraulic fluid segment is growing, as energy-efficient, lower-viscosity formulations increase value per litre, while volume growth is constrained by the EV transition, reducing hydraulic transmission applications in automotive manufacturing.

Metal working fluid at 24.8% is growing fastest at ~4.2% CAGR, driven by semiconductor fab expansion, precision EV component machining, and Japan’s world-class machine tool industry’s own demonstration machining requirements. Gear oil at 18.6% serves industrial gearboxes, wind turbines, and maritime applications. Grease at 15.4% is dominated by Kyodo Yushi’s Multemp series and specialty greases for precision bearings, electric motors, and high-temperature applications. Others (8.7%) include compressor oil, turbine oil, heat transfer oil, and process oil.

By Base Oil

Mineral oil leads at 52.4% market share (2025). This segment encompasses Group I (paraffinic SN grades), Group II (hydroprocessed), and Group III (severely hydroprocessed/VHVI) mineral base oils used across all product categories. Mineral oil’s dominance persists because Japan’s manufacturing culture of rigorous equipment maintenance and OEM specification compliance creates predictable, consistent demand for proven mineral oil grades with long performance track records.

Synthetic oil at 32.8% encompasses PAO, ester, polyalkylene glycol (PAG), and silicone-based lubricants used in high-performance applications requiring wide-temperature performance, extended drain intervals, or special material compatibility. Bio-based oil at 14.8% is driving, as Japan’s GX policy framework creates systematic specification and procurement incentives for bio-based lubricants across public infrastructure and food processing applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto |

38.5% |

Japan’s largest industrial cluster covering Greater Tokyo, Kanagawa (Yokohama, Kawasaki), Saitama, and Ibaraki |

|

Kansai/Kinki |

20.8% |

Osaka-Kobe-Kyoto industrial triangle covering steel, chemicals, precision machinery, and shipbuilding |

|

Central/Chubu |

15.4% |

Toyota City automotive cluster, Toyota Motor Corporation’s headquarters and primary manufacturing |

|

Kyushu-Okinawa |

9.6% |

TSMC Japan fab and Sony Semiconductor Kumamoto semiconductor cluster creating new high-purity metalworking fluid and specialty grease demand |

|

Tohoku |

6.2% |

Post-earthquake reconstruction industrial recovery, Tohoku Expressway logistics network industrial expansion |

|

Chugoku |

4.5% |

Mazda Motor Hiroshima primary manufacturing complex, Japan’s most lubricant-intensive single automotive site |

|

Hokkaido |

3.2% |

Hokkaido agricultural mechanization (tractors, harvesters) requiring agricultural lubricants for Hokkaido’s arable land |

|

Shikoku |

1.8% |

Ehime Prefecture petrochemical complex requiring specialty process oil and hydraulic fluids, specialty fishing boat engine lubricants |

Kanto’s 38.5% dominance is reinforced by ENEOS’ Kawasaki lubricant blending plantl establishment. The Kanto region’s semiconductor corridor, from Yamanashi through Ibaraki to Kanagawa, is generating the fastest-growing segment of premium metalworking fluid and specialty lubricant demand within the region.

Chubu’s 15.4% share is overwhelmingly driven by Toyota City’s automotive complex. Kyushu-Okinawa’s above-average CAGR (~3.9%) reflects the transformative impact of the Kumamoto semiconductor cluster. TSMC received 770 billion yen (approximately $4.6 billion) to build its second chip manufacturing facility in Kumamoto prefecture.

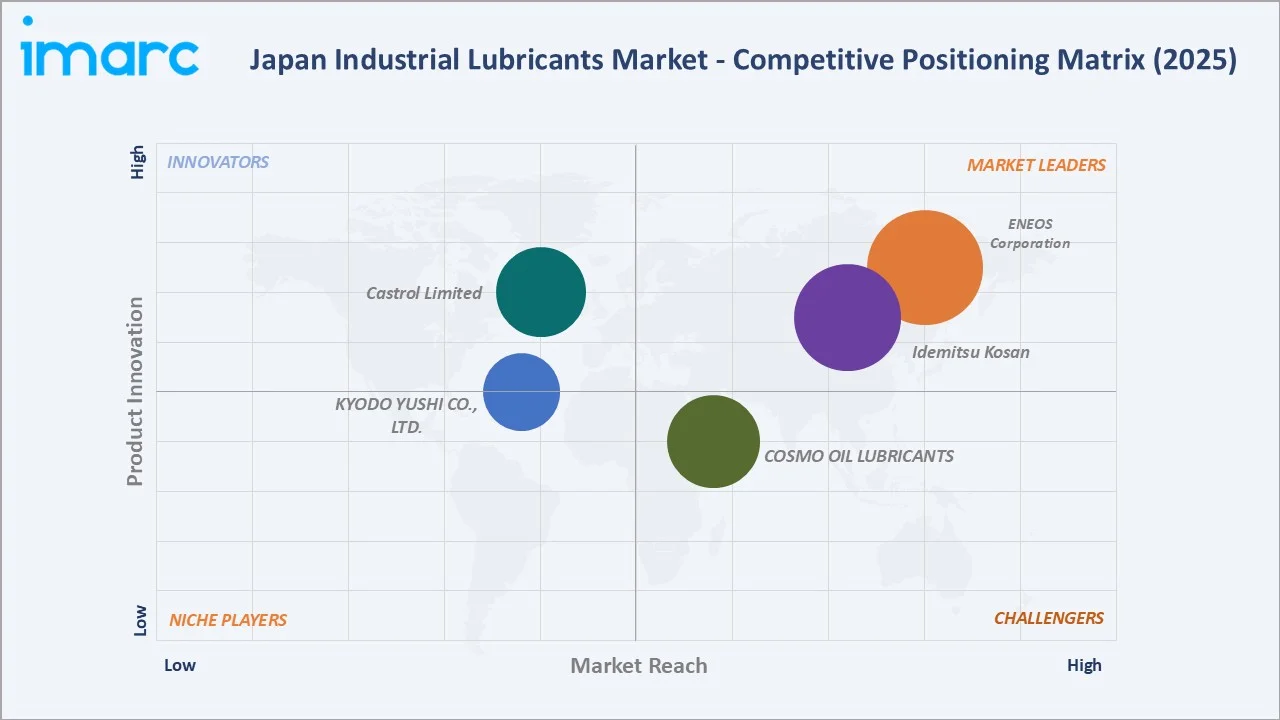

Competitive Landscape

The Japan industrial lubricants market is moderately concentrated, with ENEOS Corporation and Idemitsu Kosan collectively accounting for approximately 45–50% of total market revenue.

|

Company Name |

Product Line |

Market Position |

Core Strength |

|

ENEOS Corporation |

Hydraulic Oils, Turbine Oils, General Purpose Oils, Multi-Purpose Oils, Sewing Machine Oils, Bearing Oil for Machine Tools, Slideway Oils, Gear Oils, Mist Oils, Compressor Oils, Immersion Cooling Fluid, Vacuum Pump Oils, Refrigerating Machine Oils, Heat Transfer Oils, Film-Type Bearing Oils, Food Machinery Lubricants, Electrical Insulating Oils |

Dominant Market Leader |

Japan’s largest energy company; dominant market share across hydraulic fluid, gear oil, and grease categories |

|

Idemitsu Kosan Co., Ltd. |

Engine Oil, Transmission Fluid, Power Steering Fluid (PSF), PAG Oil, Racing Oil, and EV Fluid |

Market Leader |

Japan’s one of the petroleum companies, semiconductor-grade lubricant R&D |

|

COSMO OIL LUBRICANTS Co.,Ltd. |

Hydraulic oils, Multi-purpose machining tool lubricants, Exclusive slideway oil, Gear oil, Mist oil, Turbine oil, Compression lubricants, Vacuum pump oil, Refrigerator lubricants, Rock drill oils, Chain saw oils, Heat medium oil, Electric insulation oil, Film bearing oil |

Strong Challenger |

One of Japan’s most specified hydraulic fluids for construction equipment; growing GX-aligned bio-based product range |

|

Castrol Limited |

Metalworking fluids, Chain oil, Compressor oil, Gear oil, Grease, Hydraulic fluid, Turbine Oil |

Established |

Castrol is dominant in precision machining, metalworking fluids, and lubricant oils |

|

KYODO YUSHI CO., LTD. |

Automotive Grease, Mill Grease, Rolling Bearing Grease, Grease for Electromechanical Parts, Special-Purpose Grease |

Established |

Japan’s dedicated grease specialist with a high industrial grease market share |

The top five combined share is approximately 65–70%. The remaining 30–35% is distributed across specialty companies and Japan-origin specialists

Key Company Profiles

ENEOS Corporation

ENEOS Corporation is Japan’s largest energy company and the dominant industrial lubricant manufacturer, providing deep Group I/II/III base oil supply security for its lubricant blending operations.

- Product Portfolio: Hydraulic Oils, Turbine Oils, General Purpose Oils, Multi-Purpose Oils, Sewing Machine Oils, Bearing Oil for Machine Tools, Slideway Oils, Gear Oils, Mist Oils, Compressor Oils, Immersion Cooling Fluid, Vacuum Pump Oils, Refrigerating Machine Oils, Heat Transfer Oils, Film-Type Bearing Oils, Food Machinery Lubricants, Electrical Insulating Oils.

- Recent Developments: In March 2025, ENEOS Corporation collaborated with NVIDIA and Preferred Computational Chemistry Inc. (PFCC) to accelerate the AI-driven discovery and optimisation of new lubricants and immersion cooling fluids.

- Strategic Focus: EV fluid leadership through Toyota OEM partnership; GX-aligned bio-based lubricant portfolio expansion to capture MLIT green procurement market.

Idemitsu Kosan Co., Ltd.

Idemitsu Kosan is Japan’s second-largest petroleum company and second-largest industrial lubricant manufacturer.

- Product Portfolio: Engine Oil, Transmission Fluid, Power Steering Fluid (PSF), PAG Oil, Racing Oil, and EV Fluid.

- Recent Developments: In December 2024, Idemitsu Kosan Co., Ltd. created the world’s first plant-based motor oil specifically designed for racing.

- Strategic Focus: Honda OEM EV fluid partnership as Chubu region automotive growth anchor; Zepro semiconductor-grade metalworking fluid market penetration in Kumamoto and Yamanashi fab clusters.

COSMO OIL LUBRICANTS Co., Ltd.

Cosmo Oil Lubricants is the dedicated lubricant company. Cosmo Hydro hydraulic fluid series holds major share of Japan’s industrial hydraulic fluid market, particularly strong in construction machinery and agricultural equipment sectors.

- Product Portfolio: Hydraulic oils, Multi-purpose machining tool lubricants, Exclusive slideway oil, Gear oil, Mist oil, Turbine oil, Compression lubricants, Vacuum pump oil, Refrigerator lubricants, Rock drill oils, Chain saw oils, Heat medium oil, Electric insulation oil, Film bearing oil.

- Recent Developments: In May 2022, Cosmo Oil Lubricants received Biomass Mark certification for its bio-based diesel engine oil, COSMO DIESEL CARBONEUT 10W-30. With over 80% plant-derived base oil, it is the first diesel engine oil in Japan to earn this certification.

- Strategic Focus: GX bio-based lubricant market capture through MLIT and METI green procurement programs; premium synthetic gear oil growth targeting wind turbine and industrial gearbox replacement market.

Market Concentration Analysis

The Japan industrial lubricants market is moderately concentrated at the domestic tier. ENEOS and Idemitsu Kosan together account for an estimated 45–50% of total market revenue, underpinned by their vertically integrated refining-blending-distribution structures, long-term OEM supply agreements with nationwide dealer networks providing delivery infrastructure unavailable to international competitors. The top-five participants represent approximately 65–70% of total Japan industrial lubricant market value.

Market fragmentation exists in specialty and high-performance segments, hold dominant positions in specific application niches, precision bearing grease, solid lubricants, food-grade lubricants, and semiconductor specialty products that domestic generalists cannot easily contest. The specialty niche segment represents approximately 15–20% of total Japan industrial lubricant market value but commands 40–50% of total market gross profit, explaining premium companies’ strategic focus on niche penetration over volume growth.

Investment & Growth Opportunities

Fastest Growing Segments

Bio-based oil (~5.8% CAGR), metalworking fluid (~4.2% CAGR), synthetic oil (~4.5% CAGR), and EV-specialty fluids (~25–35% CAGR from 2025 base) represent the four highest-growth investment vectors through 2034. The semiconductor-grade specialty lubricant sub-segment (ultra-high-purity bearing grease, PFPE vacuum lubricants, cleanroom compressor oils) represents the highest absolute margin opportunity despite its small volume, creating disproportionate revenue from minimal volume market share.

Emerging Segment and Geographic Opportunities

Kyushu-Okinawa’s semiconductor cluster (TSMC, Sony Semiconductor, Hitachi Hi-Tech) represents Japan’s fastest-growing regional industrial lubricant opportunity. Tohoku’s food processing industry expansion and NSF H1 food-grade lubricant adoption; Hokkaido’s cold-climate specialty lubricant market for agriculture and infrastructure; and Okinawa’s marine and tourism-related lubricant applications represent geographic expansion opportunities for specialty lubricant providers.

Investment Themes

Japan’s GX investment program, METI’s semiconductor industry support, and MLIT’s infrastructure renewal collectively create high investment that directly drives industrial lubricant demand in construction, semiconductor manufacturing, and energy infrastructure over the next 10 years.

- Key investment themes: EV specialty fluid manufacturing capacity expansion, bio-based ester synthesis plant development (aligned with GX policy), semiconductor cleanroom lubricant R&D, IoT oil condition monitoring platform scaling, and NSF H1 food-grade lubricant blending capacity for Japan’s food processing sector.

- Corporate partnership opportunities: International lubricant companies seeking Japan market access through OEM partnership programs represent the most capital-efficient market entry route versus direct distribution investment in Japan’s relationship-intensive industrial procurement culture.

Future Market Outlook (2026-2034)

The Japan industrial lubricants market is positioned for consistent, structurally supported growth through 2034. From USD 3.24 Billion in 2025, the market will reach USD 4.36 Billion by 2034, at a 3.37% CAGR. While this growth rate is modest compared to emerging market lubricant markets, Japan’s industrial lubricant market’s value creation will outpace volume growth significantly: the systematic shift from conventional mineral oil to premium synthetics. This premiumization trajectory is locked in by Japan’s GX policy, EV transition, and semiconductor expansion (requiring ultra-premium specialty lubricants).

Research Methodology

Primary Research

Primary research included structured interviews with 120+ industry stakeholders in 2025, comprising lubricant blending plant managers, industrial procurement engineers at Toyota, Komatsu, and Hitachi, regional sales directors, distributor network managers across Japan’s eight regional markets, METI industrial chemicals policy officials, and JAST (Japan Society of Tribologists) academic researchers.

Secondary Research

Secondary research encompassed METI Petroleum Supply Monthly Statistics, JLMS lubricant market survey data, JAST tribology research publications, Japan Petroleum Institute annual reports, company financial reports and investor presentations, Bloomberg industry data for Japan specialty chemicals, and European Lubricants Industry Market Data and Analysis (ELGI). Over 180 secondary sources were reviewed and synthesized.

Forecasting Models

Market forecasts were developed using a bottom-up product-region aggregation validated against top-down. Key inputs include METI industrial production projections, Japan Cabinet Office GDP growth forecasts, EV production ramp schedules (JAMA), semiconductor fab capital expenditure programs, GX policy implementation timeline, and base oil price futures from S&P Global Platts.

Japan Industrial Lubricants Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Hydraulic Fluid, Metal Working Fluid, Gear Oil, Grease, Others |

| Base Oils Covered | Mineral Oil, Synthetic Oil, Bio-based Oil |

| End Use Industries Covered | Construction, Metal and Mining, Cement Production, Power Generation, Automotive, Chemical Production, Oil and Gas, Textile Manufacturing, Food Processing, Agriculture, Pulp and Paper, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | ENEOS Corporation, Idemitsu Kosan Co., Ltd., COSMO OIL LUBRICANTS Co.,Ltd., Castrol Limited, KYODO YUSHI CO., LTD., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan industrial lubricants market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan industrial lubricants market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan industrial lubricants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Industrial Lubricants Market Report

The Japan industrial lubricants market was valued at USD 3.24 Billion in 2025 and is projected to reach USD 4.36 Billion by 2034.

The Japan industrial lubricants market is forecast to grow at a CAGR of 3.37% during 2026-2034, driven by semiconductor manufacturing expansion, EV specialty fluid demand, and GX bio-based lubricant policy mandates.

Hydraulic fluid leads with 32.5% revenue share (2025), driven by Japan’s world-class construction machinery sector and industrial robots incorporating servo-hydraulic systems.

Mineral oil leads with 52.4% market share (2025). Synthetic oil at 32.8% is growing steadily, while bio-based oil at 14.8% is growing fastest under Japan’s GX green transformation policy mandates.

Kanto dominates with 38.5% market share (2025), driven by Greater Tokyo’s manufacturing establishments in Kanagawa, Saitama, Ibaraki, and Chiba, hosting Japan’s largest industrial lubricant consumption cluster.

Key companies include ENEOS Corporation, Idemitsu Kosan Co., Ltd., COSMO OIL LUBRICANTS Co.,Ltd., Castrol Limited, KYODO YUSHI CO., LTD.

Key drivers include Japan’s semiconductor manufacturing renaissance (TSMC Kumamoto), EV transition creating specialty e-fluid demand, GX policy mandating bio-based lubricants, infrastructure renewal investment, and IoT predictive lubrication adoption.

Key trends include EV electrification-specific lubricants, bio-based hydraulic fluid GX adoption, IoT lubrication-as-a-service, semiconductor ultra-high-purity lubricants, and low-viscosity energy-efficient formulations for factory energy conservation.

Japan’s GX Green Transformation policy mandates bio-based hydraulic fluid for public works machinery near waterways, incentivizes biodegradable lubricants, and drives green procurement specifications, creating annual bio-based lubricant demand.

Key challenges include structural manufacturing output decline, EV transition reducing conventional gear oil volumes, crude oil price volatility affecting mineral base oil costs, workforce shortage for lubrication engineering, and competition from lower-priced Chinese imports.

Top opportunities include EV specialty fluid manufacturing, bio-based ester synthesis facilities, semiconductor cleanroom lubricant R&D, IoT lubrication management services, NSF H1 food-grade blending capacity, and cold-climate specialty formulation for Hokkaido.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)