Mexico Excavators Market Size, Share, Trends and Forecast by Product, Mechanism Type, Power Range, Application, and Region, 2026-2034

Mexico Excavators Market Size, Share, Trends & Forecast (2026-2034)

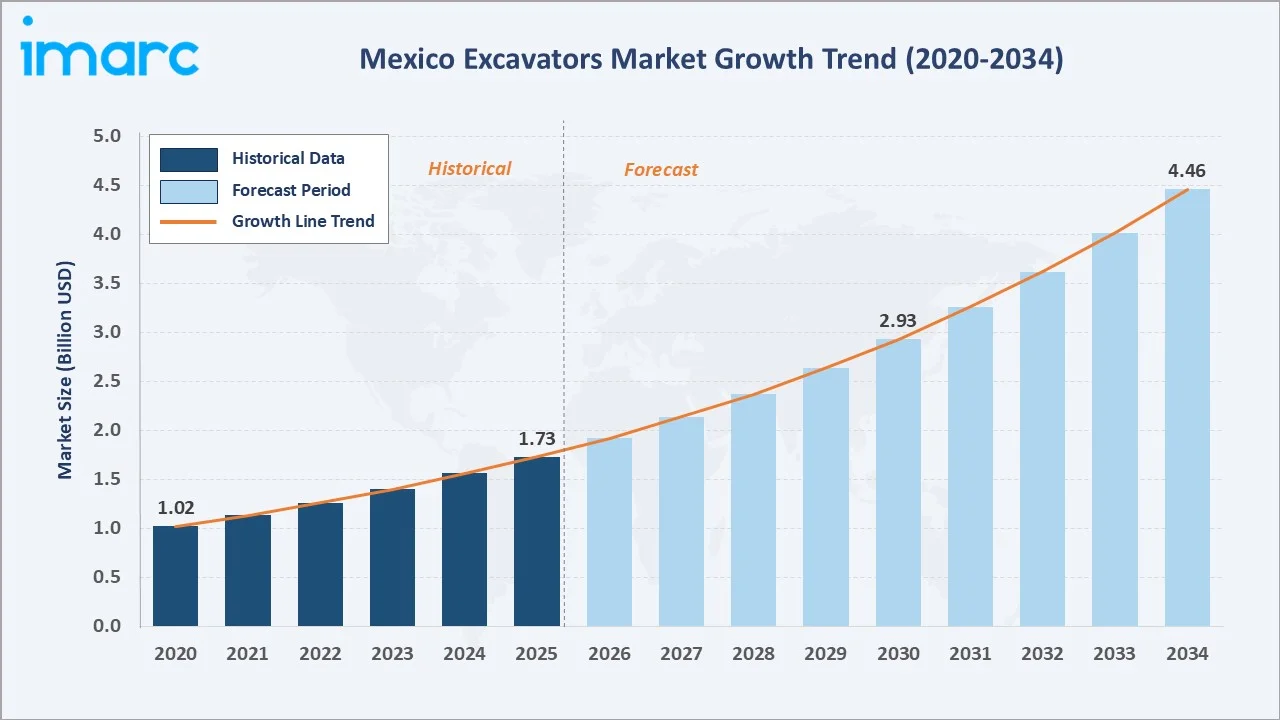

The Mexico excavators market was valued at USD 1.73 Billion in 2025 and is projected to reach USD 4.46 Billion by 2034, exhibiting a CAGR of 11.12% during 2026-2034. Rapid urbanization, expanding mining operations, and increasing adoption of hydraulic and hybrid excavator technologies are the primary drivers shaping the market growth. Government infrastructure investments, rising construction activity, and nearshoring-driven industrial development are further strengthening demand for excavators across residential, commercial, and heavy civil engineering projects.

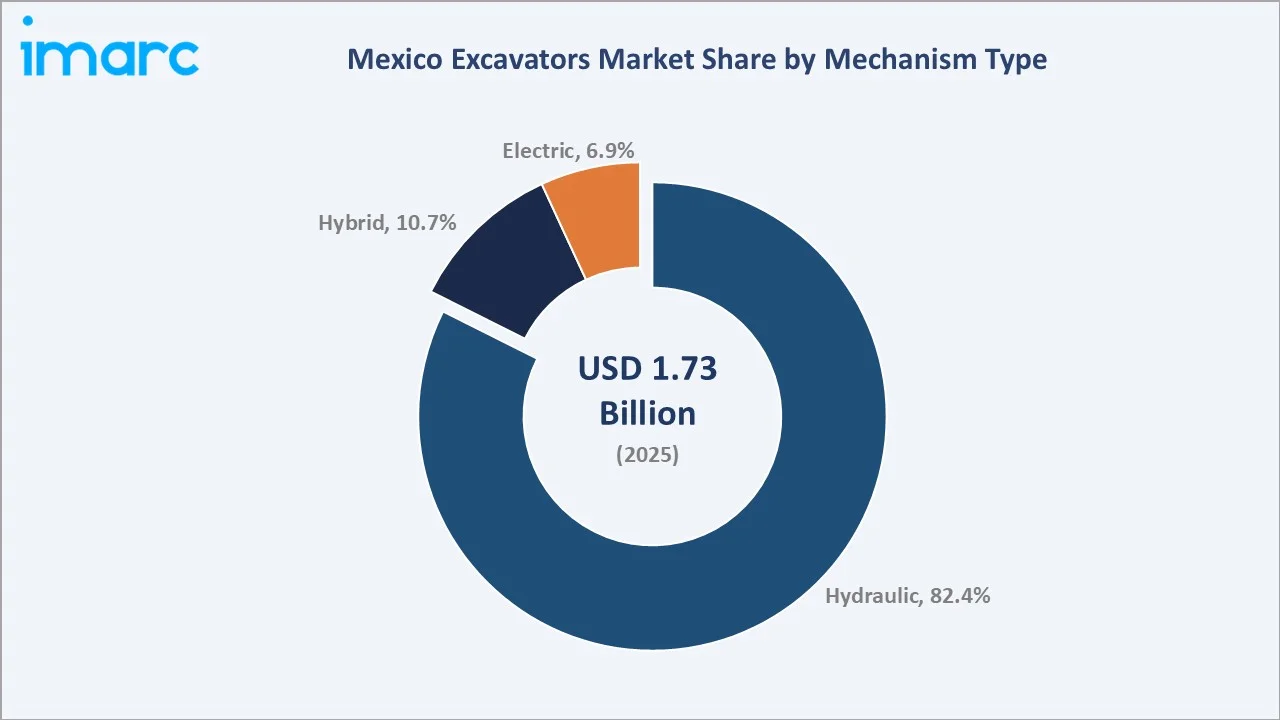

Crawler leads the product segment at 46.8%, hydraulic dominates the mechanism type segment at 82.4%, and Central Mexico commands 39.7% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.73 Billion |

|

Forecast Market Size (2034) |

USD 4.46 Billion |

|

CAGR (2026-2034) |

11.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Central Mexico (39.7%, 2025) |

|

Second Largest Region |

Northern Mexico (31.8%, 2025) |

|

Leading Product |

Crawler (46.8%, 2025) |

|

Leading Mechanism Type |

Hydraulic (82.4%, 2025) |

The Mexico excavators market expanded from USD 1.02 Billion in 2020 to USD 1.73 Billion in 2025, driven by growing construction activity, expanding infrastructure budgets, and increasing mechanization across the mining and energy sectors. Anchored at USD 2.93 Billion in 2030, the forecast to USD 4.46 Billion by 2034 is supported by accelerating investment in rail and highway corridors, nearshoring-driven industrial construction, and growing demand for fuel-efficient and hybrid excavator platforms.

To get more information on this market, Request Sample

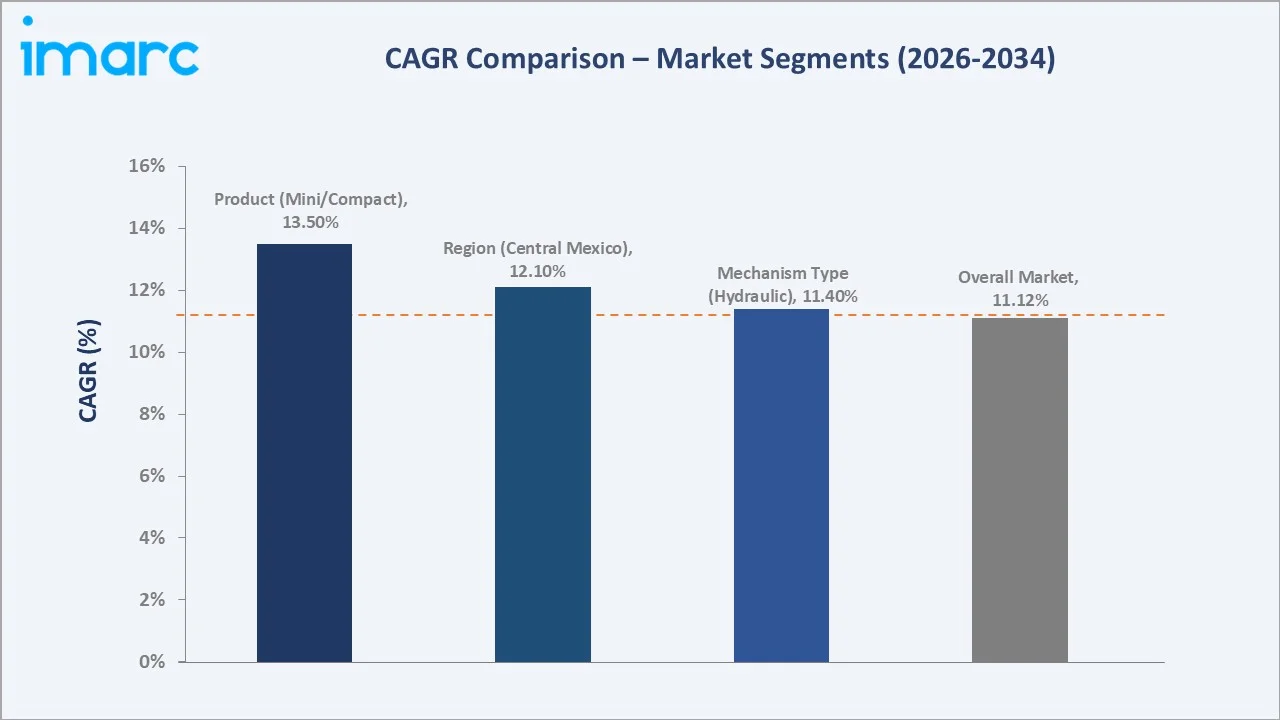

CAGR trajectories across product and mechanism type sub-segments show mini/compact and electric expanding faster than the overall 11.12% market CAGR, driven by urban construction adoption, tighter emission standards, and increasing contractor preference for versatile, lower-footprint equipment.

Executive Summary

The Mexico excavators market is on a strong growth trajectory from USD 1.02 Billion in 2020 to USD 4.46 Billion by 2034. The sector has transitioned from a predominantly import-dependent, project-driven market to one anchored by sustained infrastructure programs, nearshoring-led industrial construction, and a deepening base of domestic rental and leasing activity. Growing government investment in road, rail, water, and energy infrastructure is creating steady, multi-year demand cycles for contractors and equipment operators.

Crawler leads the product segment at 46.8% in 2025, driven by its versatility across heavy earthmoving, foundation work, and mining extraction. Hydraulic dominates the mechanism type segment at 82.4%, reflecting the established serviceability networks, operator familiarity, and proven productivity of diesel-hydraulic systems across Mexico's diverse project environments. Central Mexico at 39.7% leads regional share, anchored by Mexico City metropolitan infrastructure investment, the Bajio industrial corridor, and high density of construction and manufacturing activity.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Crawler - 46.8% share (2025) |

|

Second Largest Product |

Mini/Compact - 24.7% share (2025) |

|

Leading Mechanism Type |

Hydraulic - 82.4% share (2025) |

|

Second Largest Mechanism Type |

Hybrid - 10.7% share (2025) |

|

Leading Region |

Central Mexico - 39.7% share (2025) |

|

Second Largest Region |

Northern Mexico - 31.8% share (2025) |

|

Top Companies |

Caterpillar, Komatsu Ltd., AB Volvo, Hitachi Construction Machinery Co., Ltd., Deere & Company |

Key Analytical Observations Supporting The Above Data:

- Crawler dominance at 46.8% is supported by superior stability on uneven terrain, higher lifting capacity for demanding excavation activities, and strong suitability for large-scale infrastructure, mining, and construction projects. The segment benefits from sustained investment in transportation, industrial, and public infrastructure developments across Mexico.

- Mini/compact at 24.7% is gaining traction in urban construction projects where limited working space and lower equipment weight improve operational flexibility. The segment is supported by increasing adoption among small and medium-sized contractors seeking cost-effective and versatile equipment.

- Hydraulic leadership at 82.4% reflects established service infrastructure, broad operator familiarity, and reliable performance across a wide range of excavation applications. The segment continues to benefit from its cost-effective operation and extensive availability throughout the Mexican construction equipment market.

- Hybrid at 10.7% is gaining momentum as contractors seek improved fuel efficiency, lower operating costs, and reduced emissions. Growing product availability and increasing emphasis on sustainable construction practices continue to support adoption of hybrid excavators.

- Central Mexico at 39.7% leads the regional landscape, driven by the Mexico City metropolitan area, the Bajio manufacturing corridor, and expanding industrial and infrastructure development. The region also benefits from a high concentration of construction activity, equipment dealers, and rental service providers.

Mexico Excavators Market Overview

Excavators are self-propelled earthmoving machines equipped with a boom, dipper arm, and bucket attachment mounted on a rotating upper structure, used for digging, trenching, material handling, demolition, and grading operations. The Mexico market encompasses crawler, mini/compact, heavy-duty, and wheeled configurations, powered by hydraulic, hybrid, and electric drivetrains, and deployed across construction, mining, utilities, and industrial applications.

The Mexican ecosystem integrates global OEM brands with domestic dealers, independent rental fleets, component importers, after-sales service providers, finance and leasing institutions, and government procurement agencies. Demand is shaped by federal and state infrastructure budgets, private construction investment, commodity price cycles in mining, and the pace of nearshoring-driven industrial development across border and Bajio regions.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

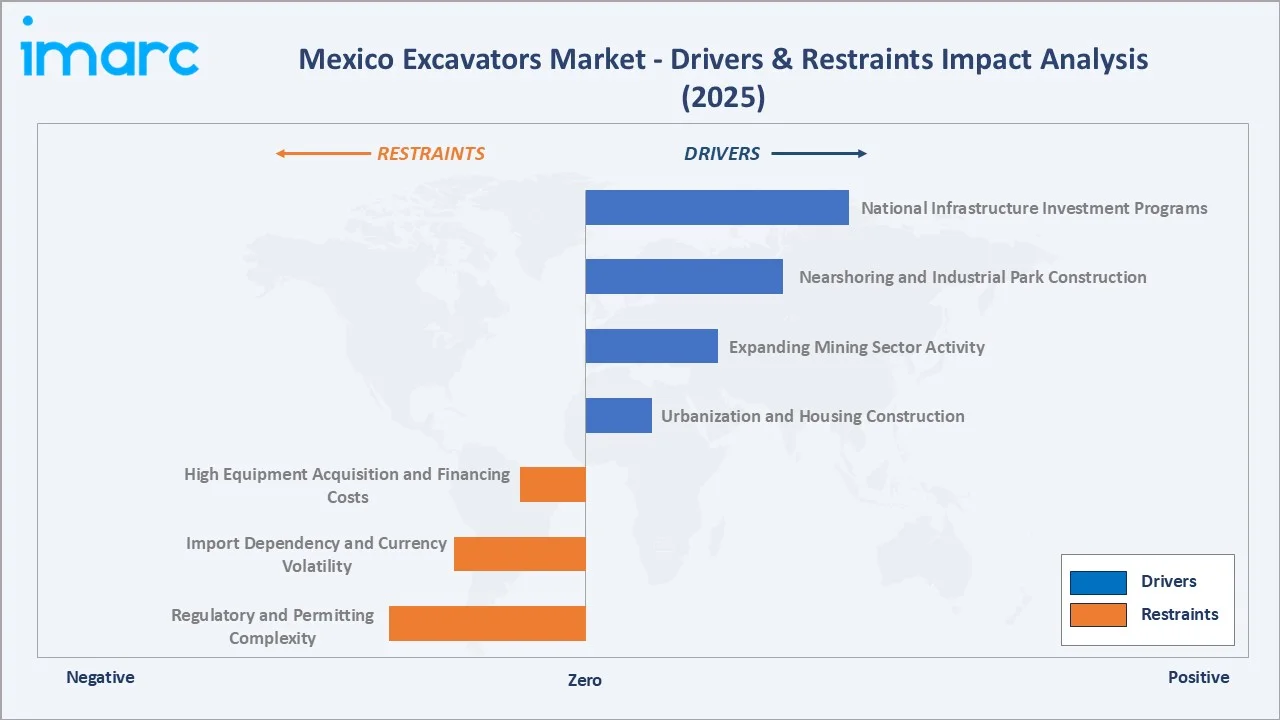

- National Infrastructure Investment Programs: Mexico's sustained public infrastructure spend across successive national infrastructure programs is driving multi-year demand for excavators on road, rail, airport, port, and water projects.

- Nearshoring and Industrial Park Construction: The accelerating relocation of manufacturing supply chains from Asia to Mexico is fueling rapid industrial park and logistics hub development across Nuevo Leon, Coahuila, Guanajuato, and Queretaro.

- Expanding Mining Sector Activity: Mexico ranks among the world's top silver and gold producers, and growing domestic and foreign investment in open-pit and underground mining operations across Sonora, Zacatecas, and Chihuahua is driving sustained demand for heavy and crawler excavator deployments.

- Urbanization and Housing Construction: Rising urbanization rates, growing middle-class housing demand, and sustained private residential and commercial construction activity in major metropolitan areas support baseline demand for smaller and medium-tonnage excavators across urban project environments. Urban population (% of total population) in Mexico stood at 81.86% in 2024, according to the World Bank collection of development indicators.

Market Restraints

- High Equipment Acquisition and Financing Costs: The purchase price of large crawler and heavy excavators, combined with elevated financing costs for small and medium contractors, limits fleet expansion among the broad base of independent operators that account for a significant share of Mexico's construction industry.

- Import Dependency and Currency Volatility: Mexico relies heavily on imported excavators and critical components from international manufacturers. Fluctuations in exchange rates can increase equipment acquisition costs, raise operating expenses for contractors, and delay fleet expansion or replacement decisions, particularly among price-sensitive buyers.

- Regulatory and Permitting Complexity: Overlapping federal, state, and municipal permitting requirements for construction and mining projects create delays that affect project start dates and, consequently, excavator mobilization and utilization timelines.

Market Opportunities

- Rental and Leasing Fleet Expansion: Growing contractor preference for renting rather than owning heavy equipment is creating significant growth opportunities for rental fleet operators investing in newer, fuel-efficient excavator platforms.

- Electric and Hybrid Excavator Adoption: Increasing OEM availability of hybrid and battery-electric excavators, supported by tightening emission norms in Mexico City and other major urban centers, creates a differentiated market opportunity for early movers in alternative-drivetrain equipment.

- Digital Telematics and Fleet Management Services: Demand for productivity tracking, fuel optimization, preventive maintenance scheduling, and remote equipment diagnostics is growing among large rental fleets and tier-one contractors.

Market Challenges

- Security and Theft Risks in Remote Sites: Equipment theft and operational security challenges in certain mining and infrastructure regions create insurance cost pressures and deter investment in high-value machinery deployment without robust asset protection measures.

- Skilled Operator Shortages: A shortage of trained excavator operators, particularly for advanced hydraulic and GPS-guided machine control systems, limits productivity gains and constrains project execution capacity across some regional markets.

Emerging Market Trends

1. Electrification and Hybrid Drivetrain Adoption

Global OEMs are progressively introducing hybrid and battery-electric excavator models into the Latin American market. Growing emphasis on fuel efficiency, lower emissions, and reduced operating costs is encouraging the adoption of hybrid and electric excavators.

2. Machine Control, GPS Grading, and Digital Telematics

Advanced machine control systems incorporating GPS-based grade guidance, 3D terrain modeling, and real-time productivity reporting are gaining adoption among larger contractors executing precision infrastructure projects. These technologies improve operational accuracy, reduce material wastage, and enhance overall project efficiency.

3. Nearshoring-Driven Industrial Construction Surge

The structural realignment of global manufacturing supply chains toward Mexico is creating a sustained pipeline of industrial park, warehouse, logistics hub, and utility infrastructure projects across the Bajio corridor and northern border states. This wave of foreign direct investment-led construction is generating demand for mid-sized and heavy crawler excavators for site preparation, foundation work, and utility installation.

4. Rental Market Formalization and Fleet Standardization

Mexico's equipment rental market is undergoing consolidation and formalization, with regional and national fleet operators displacing informal single-unit operators in tendering for major project contracts. Standardization of rental fleet specifications, GPS-enabled asset tracking, and contractual service level requirements are raising the bar for equipment condition, accelerating fleet renewal cycles and supporting demand for newer excavator models.

Industry Value Chain Analysis

The Mexico excavators value chain spans six stages from raw material supply through end-use and lifecycle management. OEM assembly, dealer distribution, and aftermarket services capture the highest value-add, while digital telematics and rental fleet management capabilities increasingly determine competitive position in downstream segments.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Steel producers, hydraulic fluid suppliers, rubber and polymer component manufacturers, and electronic component fabricators supplying global OEM supply chains |

|

Components |

Hydraulic pump and valve manufacturers, engine suppliers, undercarriage component producers, and cab and attachment fabricators serving OEM assembly plants globally |

|

Manufacturing |

Global OEM assembly facilities producing crawler, mini/compact, heavy, and wheeled excavators for the Mexican and Latin American market |

|

Distribution |

Authorized dealer networks, independent equipment distributors, and import agents operating across major Mexican cities and mining regions |

|

Rental & Leasing |

National and regional rental fleet operators, construction equipment leasing companies, and project-based equipment hire service providers |

|

End Use & Lifecycle |

Construction contractors, mining operators, utility companies, government project agencies, and aftermarket parts and service providers supporting equipment lifecycle |

Vertically integrated dealers that combine sales, rental, parts distribution, and service delivery are positioned to capture significantly greater value than pure-play equipment importers reliant on third-party service networks.

Technology Landscape in the Mexico Excavators Industry

Hydraulic System Innovation

Advanced hydraulic system architectures incorporating variable displacement pumps, electronically controlled valves, and energy recovery circuits are progressively improving fuel efficiency and cycle-time productivity across the hydraulic excavator segment. OEMs are deploying load-sensing hydraulics and intelligent power management software that optimize engine and hydraulic system output to match task demands in real time, reducing fuel consumption while enhancing machine performance and productivity.

Hybrid and Electric Drivetrain Platforms

Hybrid excavators combining diesel engines with electric swing motors and capacitor or battery energy storage systems are achieving fuel savings and emissions reductions while maintaining productivity parity with diesel equivalents. Battery-electric compact excavators, already commercially available from multiple OEMs, are enabling zero-emission urban construction and interior demolition applications that were previously incompatible with combustion-engine equipment.

Machine Control and GPS Grade Guidance

Three-dimensional machine control systems integrating GPS receivers, inertial measurement units, and grade control software are enabling semi-automated bucket positioning and precision earthmoving on road, runway, and site preparation projects. These systems reduce survey costs, improve grade accuracy, and enable less experienced operators to achieve precision outcomes previously requiring manual guidance.

Telematics, Connectivity, and Predictive Maintenance

Factory-installed telematics systems providing real-time fuel consumption, engine hours, geofencing alerts, and diagnostic code reporting are now standard on most new excavator models sold in Mexico. Predictive maintenance analytics platforms that model component wear from telematics data streams are helping large fleet operators reduce unplanned downtime and optimize planned maintenance intervals.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Crawler |

46.8% |

2025 |

|

Mechanism Type |

Hydraulic |

82.4% |

2025 |

|

Power Range |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

39.7% |

2025 |

By Product

Crawler commands a 46.8% majority share in 2025, driven by its superior traction on soft and uneven terrain, high digging force, and versatility across heavy infrastructure, mining, and deep foundation applications that characterize many of Mexico's major project types.

To access detailed market analysis, Request Sample

Mini/compact at 24.7% represents the second largest product segment in 2025, supported by expanding urban construction activity, wider adoption by small and medium contractors, and increasing versatility through hydraulic attachment compatibility.

By Mechanism Type

Hydraulic dominates with 82.4% share in 2025, reflecting the established cost-effectiveness, proven productivity, and broad service network support of diesel-hydraulic systems across Mexico's contractor and rental fleet base. The format remains the default entry point for most project categories due to operator familiarity, parts availability, and competitive purchase price.

Hybrid at 10.7% is gaining ground among larger rental fleet operators and tier-one contractors, attracted by fuel savings and reduced lifecycle operating costs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Central Mexico |

39.7% |

Dense infrastructure project pipeline, established industrial corridor activity, large contractor base, and proximity to major equipment dealer and service networks |

|

Northern Mexico |

31.8% |

Rapid nearshoring-driven industrial construction, expanding mining operations, border infrastructure investment, and large-scale logistics and manufacturing hub development |

|

Southern Mexico |

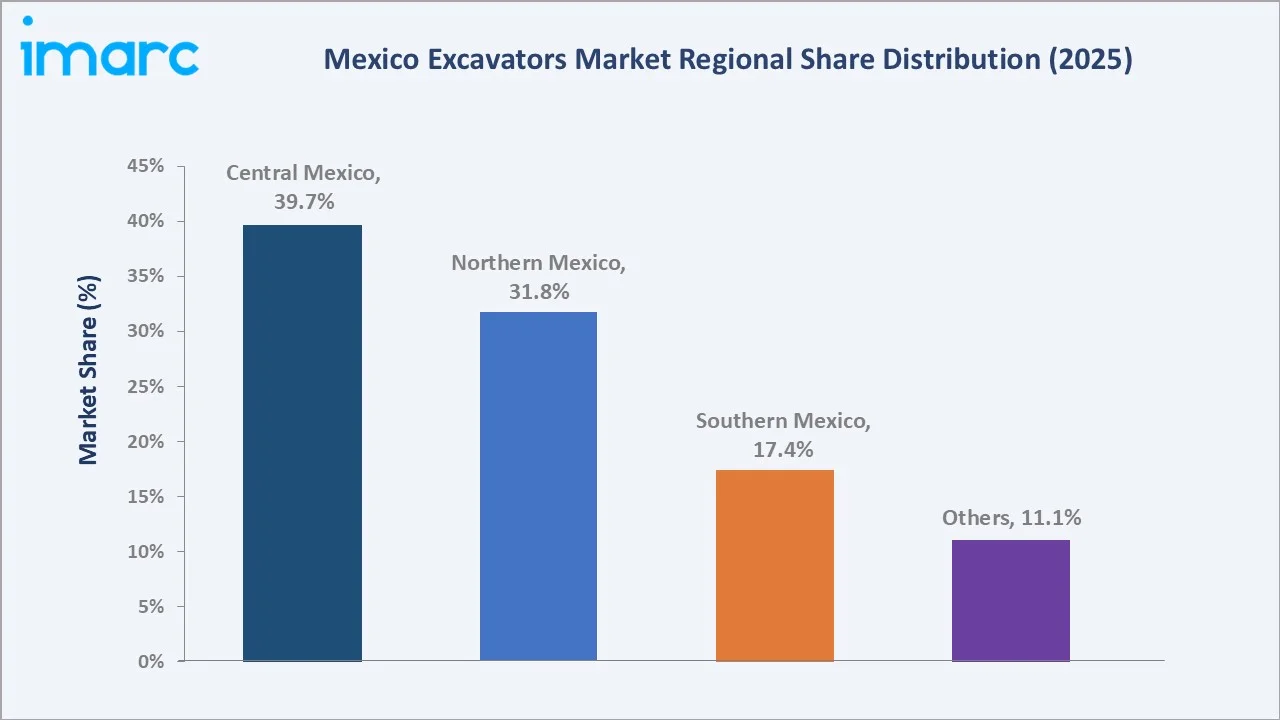

17.4% |

Energy infrastructure projects, expanding tourism and resort development, and growing agricultural and utility sector activity |

|

Others |

11.1% |

Regional highway and road upgrading programs, utility infrastructure development, growing private real estate construction, and gradual mechanization of smaller-scale earthmoving operations |

Central Mexico at 39.7% in 2025 leads the regional landscape, anchored by the Mexico City metropolitan area, Bajio manufacturing corridor, and Puebla-Tlaxcala industrial zone. Dense construction project pipelines, a high concentration of authorized OEM dealer and service points, and established contractor networks support sustained regional leadership across all product categories.

Northern Mexico at 31.8% is the second largest region, with accelerating nearshoring-driven industrial park construction, expanding mining operations across Sonora and Chihuahua, and sustained border infrastructure investment creating strong multi-year demand for crawler and heavy excavators through 2034.

Competitive Landscape

The Mexico excavators market is moderately concentrated, with global OEM brands dominating the dealer-sold and rental segments while regional importers serve niche and price-sensitive contractor cohorts. Brand reputation, parts availability, dealer network density, and total cost of ownership form the key competitive differentiators.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Caterpillar |

Cat Excavators |

Leader |

Full product range with strong dealer and service network across Mexico |

|

Komatsu Ltd. |

Komatsu PC Series |

Leader |

Expanding hybrid lineup and digital telematics integration for fleet operators |

|

AB Volvo |

Volvo EWR Series, Volvo EC Series |

Leader |

Sustainability-led product portfolio with electric and hybrid excavator expansion |

|

Hitachi Construction Machinery Co., Ltd. |

Hitachi Zaxis-7 Excavators |

Challenger |

Independent OEM focusing on precision hydraulic performance, telematics, and flexible equipment financing |

|

Deere & Company |

John Deere P-Tier Excavators |

Challenger |

Integrated dealer network leveraging agricultural channel for construction segment |

Key players include Caterpillar, Komatsu Ltd., AB Volvo, Hitachi Construction Machinery Co., Ltd., and Deere & Company, among others.

Key Company Profiles

Caterpillar

Caterpillar is a United States based industrial equipment manufacturer and one of the world's leading producers of construction and mining machinery, diesel and natural gas engines, and industrial gas turbines. The company operates through an extensive authorized dealer network across Mexico and Latin America, offering a comprehensive range of excavators spanning compact mini models through to large production-class machines for construction, infrastructure, and mining applications.

- Product Portfolio: Cat Excavators covering mini, small, medium, large, and wheeled configurations, supported by a full range of construction attachments and services.

- Recent Developments: The company has continued to expand its equipment portfolio, strengthen dealer capabilities, and enhance digital machine technologies to support evolving customer requirements across construction and mining applications.

- Strategic Focus: Expanding full-range product availability across all excavator size classes, advancing telematics and machine control adoption, and strengthening dealer-led service and uptime capability across Mexico.

Komatsu Ltd.

Komatsu Ltd. is a Japanese multinational corporation and one of the world's largest manufacturers of construction, mining, and utility equipment. The company serves the Mexico market through a regional dealer network.

- Product Portfolio: Komatsu PC Series hydraulic excavators spanning mini, small, medium, large, and mining-class configurations.

- Recent Developments: The firm has continued to expand its equipment portfolio, strengthen dealer capabilities, and enhance digital machine technologies to support evolving construction and mining requirements. It has also focused on improving equipment efficiency, operator productivity, and after-sales support.

- Strategic Focus: Advancing hybrid and intelligent machine control excavator availability and growing dealer support capability across Mexico.

Hitachi Construction Machinery Co., Ltd.

Hitachi Construction Machinery Co., Ltd. is an independent, publicly listed Japanese construction equipment manufacturer. The company designs, manufactures, and sells a broad range of hydraulic excavators for construction, mining, and infrastructure applications globally, and serves the Mexico market through its Americas distribution and dealer network.

- Product Portfolio: Hitachi Zaxis-7 Excavators spanning compact, medium, large, and ultra-large classes.

- Recent Developments: The company has been expanding its excavator portfolio through product enhancements, greater digital technology integration, and investments in dealer support capabilities. It has also been strengthening equipment performance, operational efficiency, and lifecycle support across construction and mining applications.

- Strategic Focus: Expanding Zaxis-7 model availability and aftermarket service coverage, advancing telematics and remote monitoring services, and growing flexible leasing and financing solutions for contractors across the Mexico market.

Market Concentration Analysis

The Mexico excavators market is moderately concentrated, with the top three OEM brands - Caterpillar, Komatsu Ltd., and AB Volvo - collectively commanding the majority of dealer-sold new excavator volume across crawler, mid-size, and heavy product categories. Their combined competitive strength is reinforced by the widest authorized service and parts networks in the country, supporting total cost of ownership advantages that smaller importers and niche brands cannot easily replicate.

Barriers to entry include the capital requirement for establishing dealer and service networks across Mexico's geographically diverse regions, the need for certified technician training programs, spare parts inventory investment, and OEM authorization relationships. These factors strongly favor established incumbents with decades of dealer relationship and brand equity in the market.

Consolidation is gradually progressing as smaller regional importers lose share to OEM-authorized dealers offering integrated financing, service guarantee, and telematics packages. Strategic partnerships between OEMs and rental fleet operators are further reinforcing competitive positioning, as fleet standardization decisions create long-term equipment procurement continuity for the largest volume buyers in the market.

Investment & Growth Opportunities

Fastest-Growing Segments

Mini/compact is the fastest-growing product segment, supported by urban construction demand, small contractor adoption, and attachment versatility. Northern Mexico is growing fastest among geographies, driven by nearshoring-led industrial construction and expanding mining sector activity.

Emerging Markets

Southern Mexico represents a significant emerging market opportunity, anchored by energy infrastructure projects and growing tourism and resort development across the Yucatan Peninsula and Gulf Coast states. The region is transitioning from minimal mechanization to structured heavy equipment adoption, creating substantial demand for first-time equipment acquisition by local contractors.

Venture & Investment Trends

Investment is concentrated in rental fleet modernization, digital telematics platform development, hybrid and electric drivetrain aftermarket service capability, and dealer network expansion in underserved regional markets. OEMs and private equity-backed rental operators are actively investing in fleet management software, operator training programs, and extended warranty and service contracts that generate recurring revenue streams beyond the initial equipment sale.

Future Market Outlook (2026-2034)

The Mexico excavators market is forecast to expand from USD 1.73 Billion in 2025 to USD 4.46 Billion by 2034 at a CAGR of 11.12%, adding approximately USD 2.73 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: sustained public infrastructure investment under successive national programs; nearshoring-driven industrial construction creating multi-year private sector demand; accelerating adoption of hybrid, electric, and digitally connected excavator platforms; and continued rental market formalization driving fleet standardization and renewal cycles.

By 2034, the Mexico excavators market is expected to feature a materially higher share of hybrid and electric models, widespread telematics adoption across rental and contractor fleets, and deeper OEM investment in localized service infrastructure. Regional diversification toward Northern and Southern Mexico will reduce Central Mexico's dominance as infrastructure investment and industrial activity spread across the country.

Research Methodology

Primary Research

Primary research included structured interviews with construction equipment dealers, rental fleet operators, infrastructure contractors, mining sector procurement managers, and OEM regional sales executives, validating market sizing, product mix, rental penetration, and technology adoption trends across Mexico's major regional markets.

Secondary Research

Secondary sources included the Mexican Chamber of the Construction Industry (CMIC) annual statistics, INEGI construction and manufacturing sector data, OEM investor presentations and annual reports, and industry association publications from CANACINTRA and COPARMEX.

Forecasting Models

Market forecasts used top-down and bottom-up models combining construction sector GDP contribution, infrastructure investment budget projections, equipment fleet renewal cycles, rental market penetration rates, and OEM product introduction timelines. Scenario analysis addressed infrastructure budget continuity, nearshoring investment pace, and alternative drivetrain adoption trajectories.

Mexico Excavators Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Mini/Compact, Crawler, Wheeled, Heavy |

| Mechanism Types Covered | Electric, Hydraulic, Hybrid |

| Power Ranges Covered | Up to 300 HP, 301-500 HP, 501 HP and Above |

| Applications Covered | Mining, Construction, Waste Management, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Caterpillar, Komatsu Ltd., AB Volvo, Hitachi Construction Machinery Co., Ltd., Deere & Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico excavators market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico excavators market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico excavators industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Excavators Market Report

The Mexico excavators market was valued at USD 1.73 Billion in 2025, driven by sustained public infrastructure investment, nearshoring-led industrial construction, and growing adoption of mechanized earthmoving equipment across construction and mining sectors.

The market is projected to grow at a CAGR of 11.12% from 2026-2034, reaching USD 4.46 Billion, supported by accelerating nearshoring-driven construction, public infrastructure programs, and adoption of hybrid and electric excavator platforms.

Crawler leads at 46.8% in 2025, driven by its versatility across heavy earthmoving, foundation work, and mining extraction. Its superior stability and ability to operate efficiently across challenging terrain further support widespread adoption.

Hydraulic dominates at 82.4% in 2025, reflecting established serviceability networks and operator familiarity. Its broad availability across multiple excavator classes and suitability for diverse construction, mining, and infrastructure applications further reinforce its market leadership.

Central Mexico commands 39.7% in 2025, led by the Mexico City metropolitan area, Bajio industrial corridor, and Puebla-Tlaxcala zone.

Leading players include Caterpillar, Komatsu Ltd., AB Volvo, Hitachi Construction Machinery Co., Ltd., and Deere & Company, among others.

The primary drivers include increasing infrastructure investments, accelerating nearshoring-driven industrial park construction, expanding mining operations, rising urbanization, and growing rental market formalization supporting fleet renewal cycles.

Advanced hydraulic systems, hybrid and electric drivetrains, GPS machine control, and telematics platforms are progressively reshaping the market, improving fuel efficiency, operator productivity, and fleet management capability across contractor and rental segments.

Key challenges include high equipment acquisition and financing costs for small and medium contractors, peso-dollar exchange rate volatility affecting import costs, skilled operator shortages for advanced machine control systems, and security risks at remote project sites.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)