Mexico Wind Power Market Size, Share, Trends, and Forecast by Location and Region, 2026-2034

Mexico Wind Power Market Size, Share, Trends & Forecast (2026-2034)

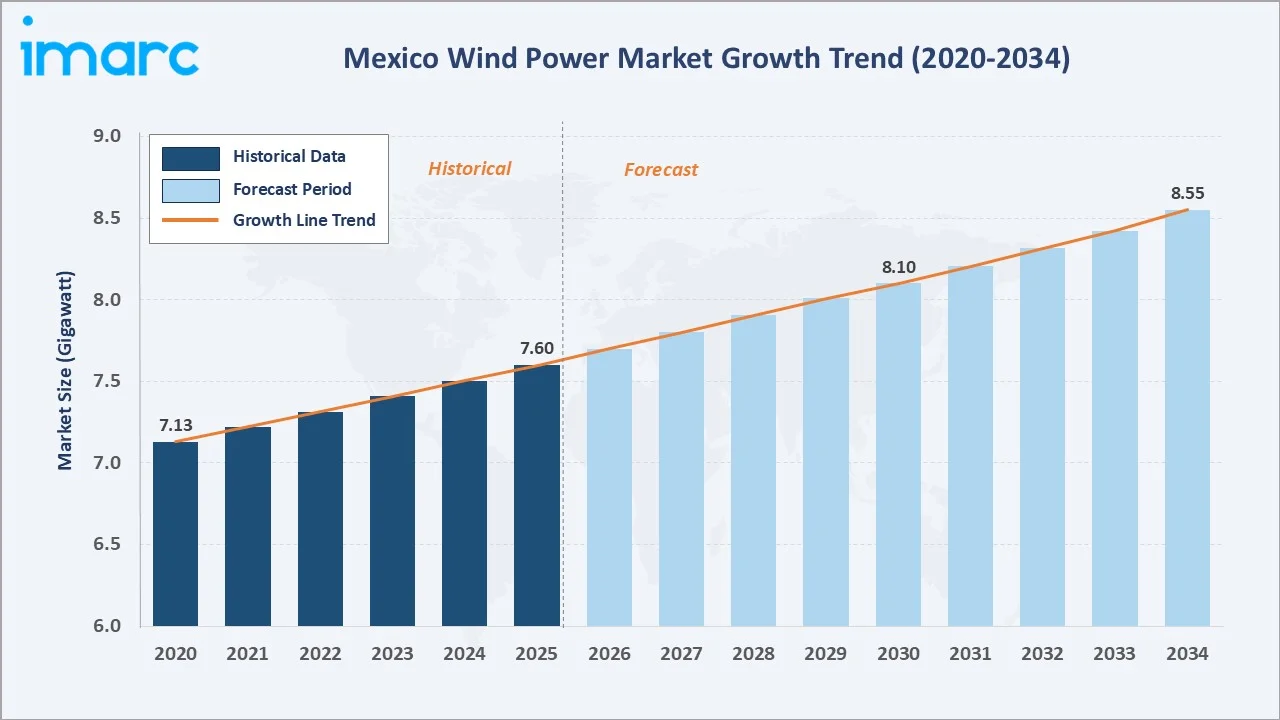

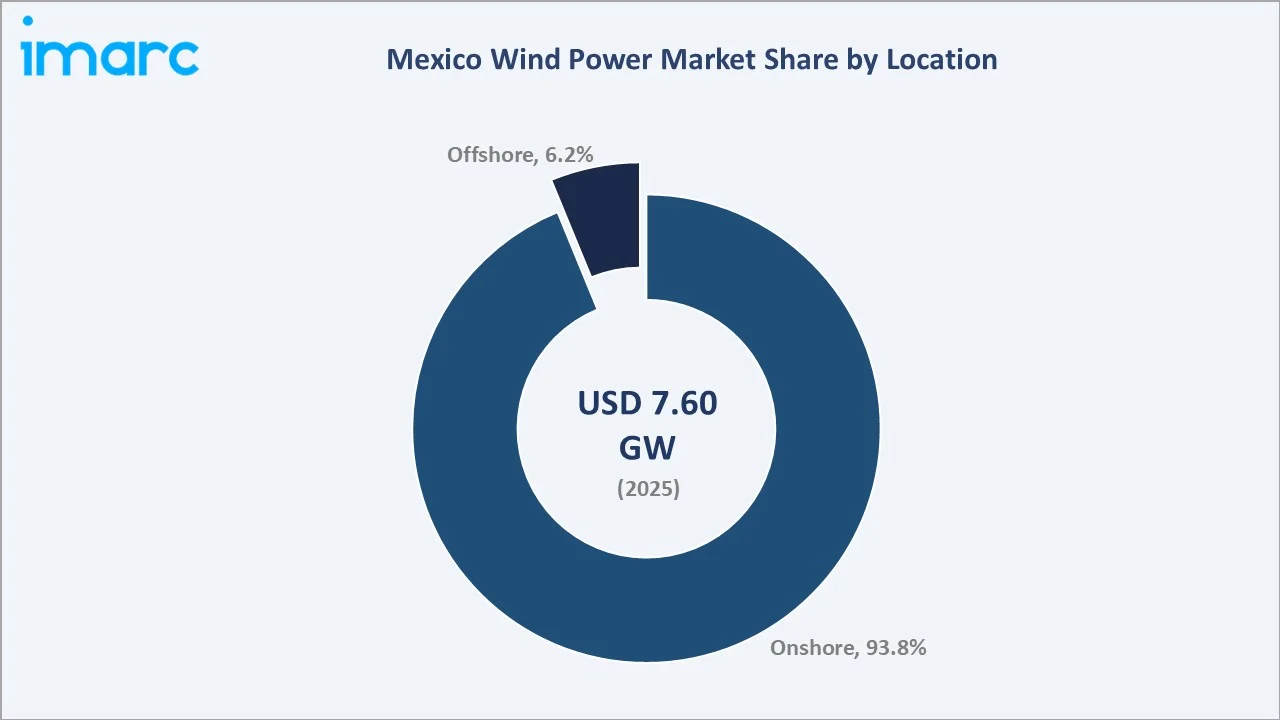

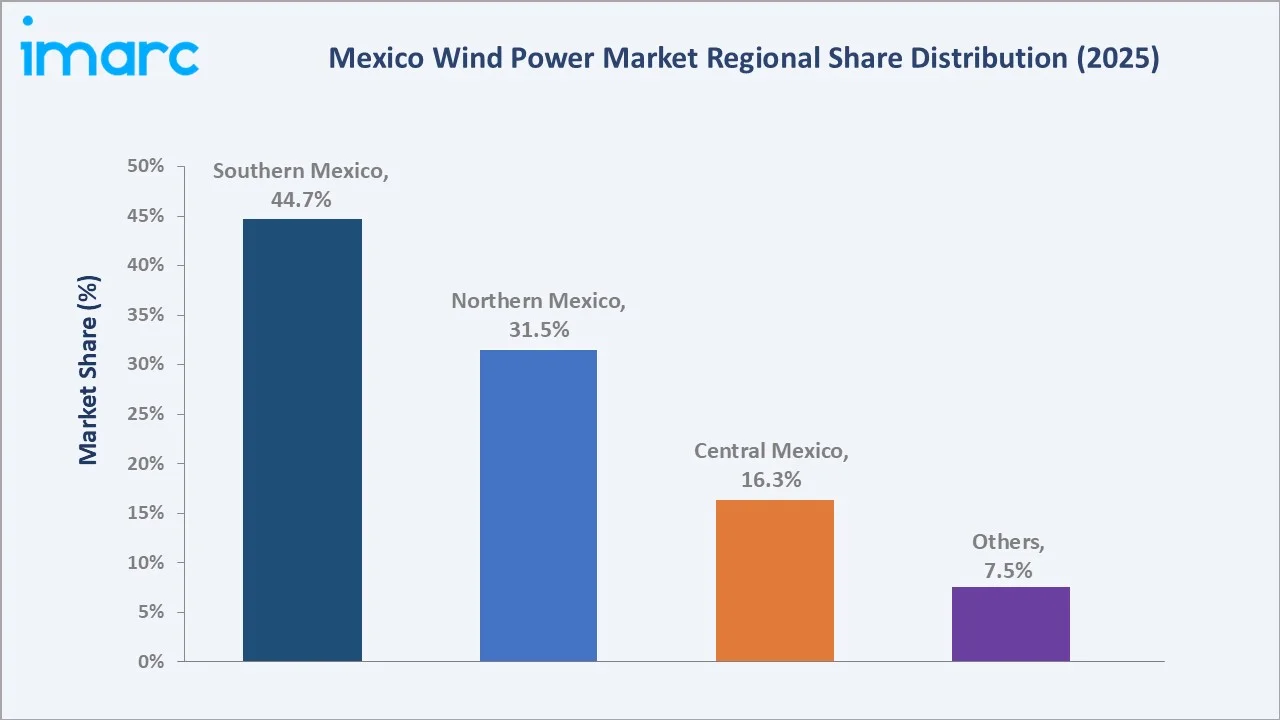

The Mexico wind power market reached 7.60 Gigawatt in 2025 and is projected to reach 8.55 Gigawatt by 2034, expanding at a CAGR of 1.29% during 2026-2034. Growth is supported by the country's renewable capacity expansion targets, rising electricity demand, and declining wind turbine technology costs. Mexico's state-led energy strategy under Plan México aims to add 22 GW of new generation capacity from renewable sources by 2030, with clean technologies, including wind, comprising a significant share of new builds. Onshore installations lead the location segment at 93.8% in 2025, supported by established turbine technology and lower development costs. Southern Mexico leads regionally at 44.7%, reflecting strong wind resource availability and grid access in the region.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

7.60 Gigawatt |

|

Forecast Market Size (2034) |

8.55 Gigawatt |

|

CAGR (2026-2034) |

1.29% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Location |

Onshore (93.8%, 2025) |

|

Leading Region |

Southern Mexico (44.7%, 2025) |

The Mexico wind power market grew from 7.13 Gigawatt in 2020 to 7.60 Gigawatt in 2025, reflecting steady capacity additions despite regulatory pauses affecting private-sector renewable projects during parts of the historical period. It is expected to reach 8.10 Gigawatt by 2030, supported by grid modernization initiatives and renewed state-backed renewable tenders. By 2034, the market is forecast to reach 8.55 Gigawatt, driven by declining technology costs, rising electricity demand, and the gradual resumption of private investment under the 2025 binding planning framework. Overall, the market reflects measured, policy-anchored growth as Mexico balances state control with renewable expansion.

To get more information on this market, Request Sample

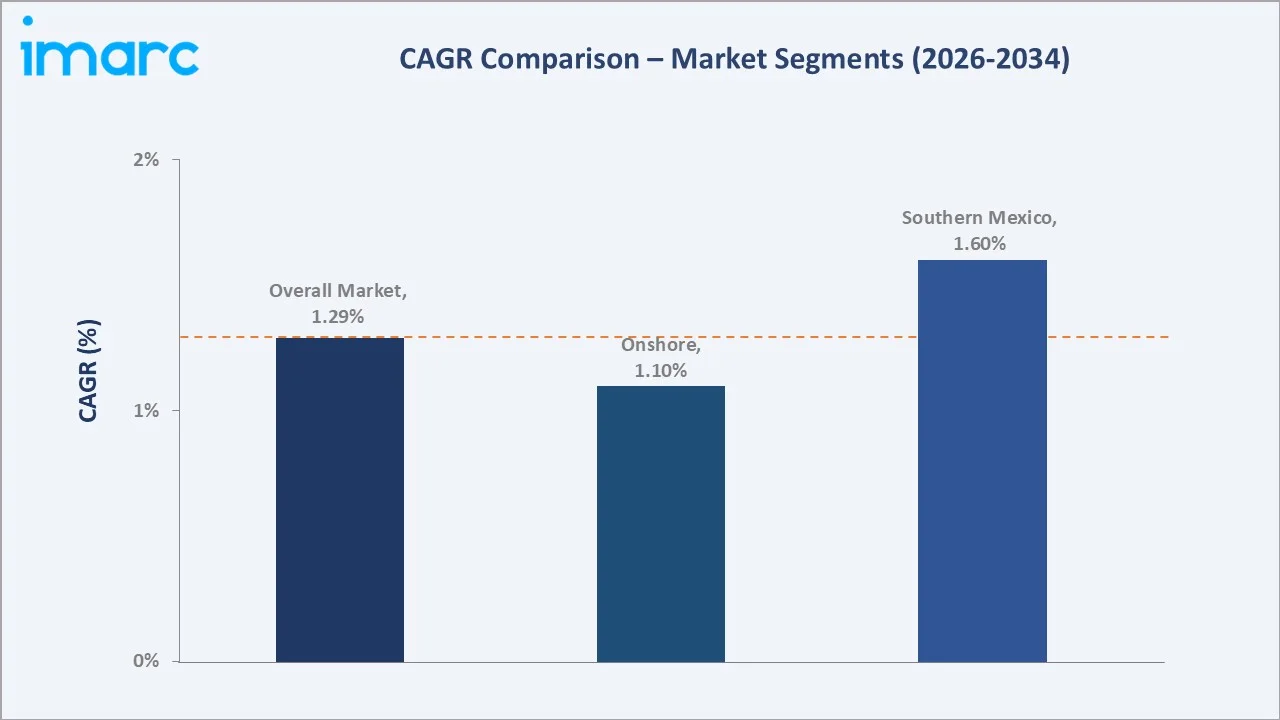

Offshore wind is forecast to grow fastest at ~2.8% CAGR through 2034 as Mexico's coastal wind resource gains early-stage developer interest. Southern Mexico is projected to expand at ~1.6% CAGR, supported by strong wind corridors in Oaxaca. Onshore capacity continues to grow steadily at ~1.1% CAGR through established turbine technology and lower interconnection costs.

Executive Summary

The Mexico wind power market is progressing at a measured pace, shaped by the country's evolving energy policy landscape and its emphasis on state-led generation. Rising electricity demand across industrial and commercial sectors is increasing the need for diversified, reliable power sources, including wind. Onshore wind continues to dominate installed capacity given its mature technology base and comparatively lower development costs, while offshore wind remains nascent but increasingly discussed amid Mexico's extensive coastline.

Market growth is also influenced by Mexico's March 2025 energy reform, which requires at least 54% of dispatched electricity to originate from CFE-owned plants, reshaping the role of private wind developers. Despite this shift, SENER's binding planning framework has approved new wind projects as part of a broader renewable buildout. Grid interconnection constraints and permitting delays remain key restraints on faster expansion.

Onshore installations hold 93.8% share in 2025, while Southern Mexico leads regionally at 44.7%, driven by strong wind resources in Oaxaca's Isthmus of Tehuantepec corridor. The market outlook through 2034 reflects steady, policy-anchored growth supported by grid modernization and gradual private-sector re-engagement.

Key Market Insights

|

Insight |

Data |

|

Dominant Location |

Onshore - 93.8% share (2025) |

|

Leading Region |

Southern Mexico - 44.7% share (2025) |

|

Fastest Growing Location |

Offshore - ~2.8% CAGR (2026-2034) |

|

Top Companies |

Acciona, S.A., Vestas Wind Systems A/S, Enel S.p.A., and EDF S.A. |

|

Market Opportunity |

Grid modernization-linked wind tenders; repowering of aging onshore wind farms; offshore wind feasibility studies; hybrid wind-storage pairing; turbine component localization |

Key Analytical Observations Supporting The Above Data:

- Onshore at 93.8%: Onshore wind dominates due to its established technology base, lower capital costs, and decades of operating history in wind corridors such as Oaxaca and Tamaulipas. Mature turbine supply chains and existing interconnection infrastructure continue to favor onshore development over emerging offshore alternatives.

- Southern Mexico at 44.7%: Southern Mexico leads regionally due to exceptionally strong and consistent wind speeds across the Isthmus of Tehuantepec, one of the most wind-rich corridors globally. This natural advantage, combined with established transmission links, has anchored the bulk of the country's installed wind capacity in this region.

- Offshore at ~2.8% CAGR: Offshore wind is forecast to grow fastest, albeit from a small base, as developers begin assessing Mexico's Gulf and Pacific coastlines for future utility-scale projects, supported by global cost declines in offshore turbine technology.

Mexico Wind Power Market Overview

The Mexico wind power market encompasses the generation of electricity from onshore and offshore wind turbines across the country's grid-connected and emerging coastal wind resources. It includes utility-scale wind farms, turbine supply chains, project development, and grid interconnection infrastructure that serve industrial, commercial, and residential electricity demand. Growth is shaped by Mexico's evolving energy policy, which balances state-majority generation requirements with continued private investment in renewables. Macroeconomic factors include rising electricity consumption, Plan México's 22-GW capacity expansion target by 2030, and ongoing transmission grid modernization investments exceeding USD 8 billion.

Market Dynamics

To evaluate market opportunities, Request Sample

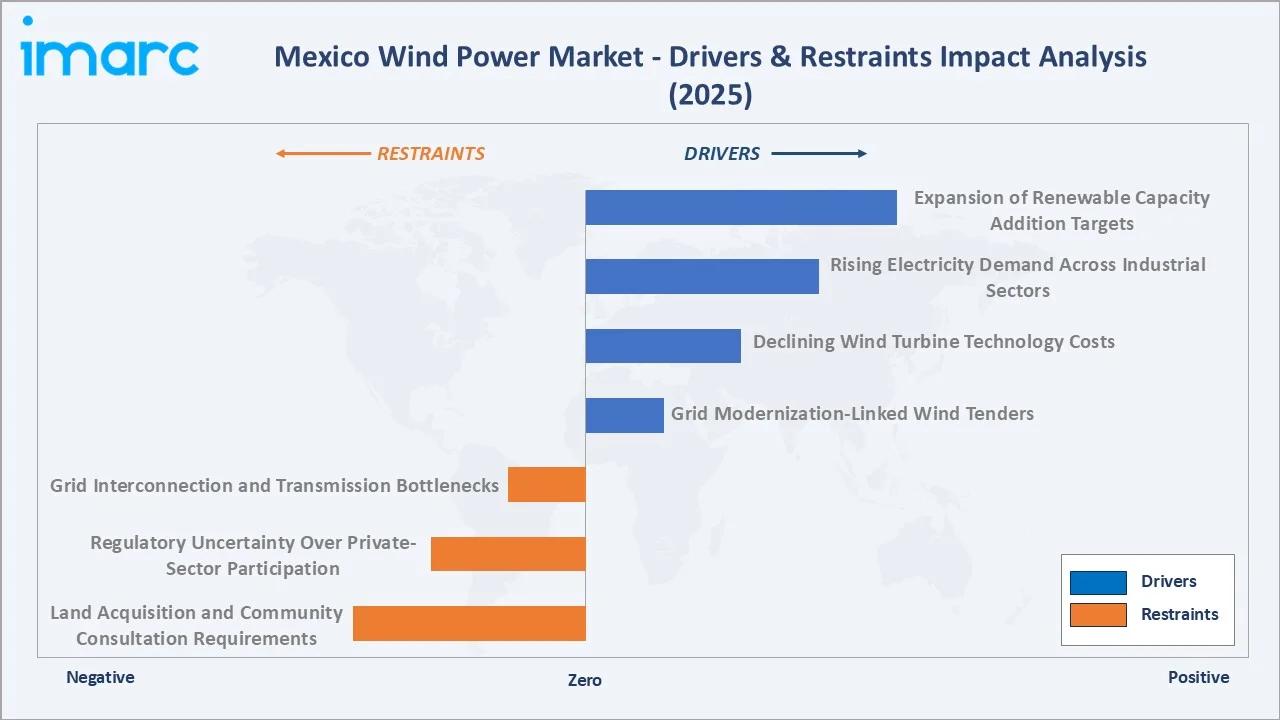

Market Drivers

- Expansion of Renewable Capacity Addition Targets: Mexico's Plan México targets 22 GW of new generation capacity by 2030, with SENER's binding planning scheme approving 3,320 MW of renewable capacity, including five wind projects, in December 2025 alone. This state-backed pipeline is creating a structured pathway for new wind capacity even within a more centralized regulatory environment.

- Rising Electricity Demand Across Industrial Sectors: Mexico's net electricity consumption is projected to rise 38.2% between 2024 and 2038, reaching 495,781 GWh, according to SENER's national planning program. Industrial and commercial sectors account for the largest share of this demand growth, increasing the need for diversified generation sources including wind.

- Declining Wind Turbine Technology Costs: Continued global declines in wind turbine manufacturing and installation costs are improving project economics in Mexico. Lower per-megawatt costs support both new installations and the repowering of older turbines, particularly across established wind corridors in Oaxaca and Tamaulipas.

Market Restraints

- Grid Interconnection and Transmission Bottlenecks: Insufficient transmission infrastructure has historically delayed wind project commissioning. Industry associations have noted billions of dollars in stalled wind investment tied to transmission line shortages, even as SENER's USD 8.1 billion grid strengthening plan targets these gaps through 2030.

- Regulatory Uncertainty Over Private-Sector Participation: Mexico's March 2025 energy reform requires at least 54% of dispatched electricity to come from CFE-owned plants, narrowing the addressable opportunity for private wind developers and prompting some companies to reassess their Mexican asset portfolios.

Market Opportunities

- Grid Modernization-Linked Wind Tenders: SENER and FONADIN are advancing studies for new wind power generation capacity as part of the portfolio of projects acquired from a major utility in 2024, creating opportunities for turbine suppliers and EPC contractors aligned with state-led development.

- Repowering of Aging Onshore Wind Farms: Many of Mexico's earliest wind farms, commissioned over a decade ago in Oaxaca, are approaching the end of their original turbine design life, creating opportunities for repowering with larger, more efficient turbines that increase output without expanding land footprint.

Market Challenges

- Land Acquisition and Community Consultation Requirements: Wind project developers in Mexico must navigate complex land-use agreements and community consultation processes, particularly in indigenous territories within key wind corridors, which can extend project development timelines.

- Curtailment Risk Amid Grid Constraints: Periods of transmission congestion have historically led to wind curtailment in high-resource regions, reducing realized output relative to installed capacity and affecting the economics of new and existing wind farms.

Emerging Market Trends

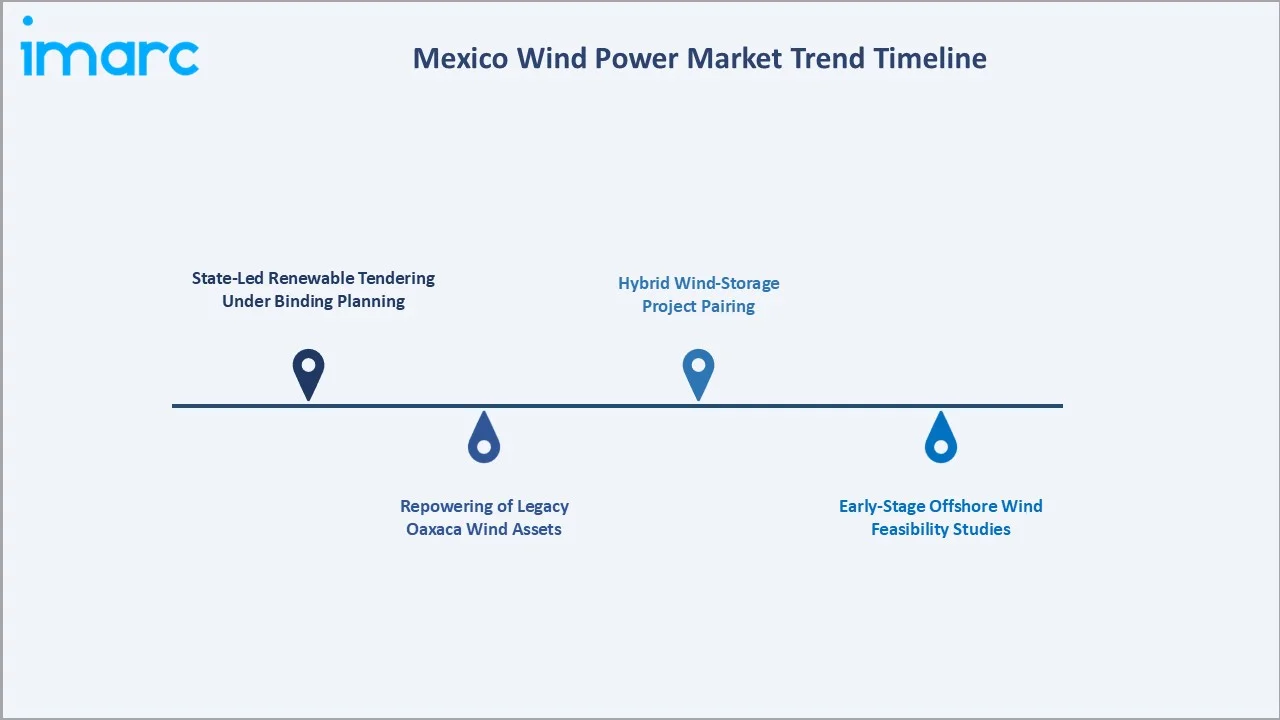

1. State-Led Renewable Tendering Under Binding Planning

Mexico's new binding planning scheme, introduced in late 2025, is reshaping how wind projects move from proposal to construction. Private developers can still participate, but projects must align with SENER's centrally coordinated capacity additions. This trend is increasing the importance of early engagement with national planning processes for wind project sponsors.

2. Repowering of Legacy Oaxaca Wind Assets

Operators are increasingly evaluating repowering opportunities across Oaxaca's wind corridor, where many turbines installed in the 2010s are nearing the end of their design life. Replacing older, smaller turbines with modern, higher-capacity units allows developers to increase output from existing sites without new land acquisition.

3. Hybrid Wind-Storage Project Pairing

Developers are beginning to pair wind capacity with battery energy storage systems to improve dispatchability and reduce curtailment risk in transmission-constrained regions. This trend aligns with SENER's broader push for storage-backed renewable integration under the 2025-2030 planning cycle.

4. Early-Stage Offshore Wind Feasibility Studies

While offshore wind remains a small share of the market, developers and research institutions have begun preliminary feasibility assessments along Mexico's Gulf and Pacific coastlines, drawing on cost declines and technology maturity seen in other offshore wind markets globally.

Industry Value Chain Analysis

Mexico's wind power value chain integrates raw material and component supply, turbine manufacturing, permitting and interconnection, project development and EPC execution, ongoing operations and maintenance, and power sale through grid dispatch.

|

Stage |

Key Participants |

|

Raw Material & Component Supply |

Steel, composite material, and electrical component suppliers |

|

Turbine Manufacturing |

Wind turbine OEMs, blade and gearbox manufacturers |

|

Permitting & Interconnection |

National energy regulators, grid operators, environmental authorities |

|

Project Development & EPC |

Project developers, engineering and construction contractors |

|

Operations & Maintenance |

O&M service providers, technical inspection firms |

|

Power Sale & Grid Dispatch |

Utilities, grid operators, wholesale electricity market participants |

The project development and EPC stage is the most value-added stage in the Mexico wind power value chain. This stage transforms permitted sites into operating assets through site engineering, turbine procurement, civil works, and grid connection, requiring substantial technical and financial capability. Companies that can navigate Mexico's evolving permitting framework while managing construction risk are best positioned to capture value across the project lifecycle.

Technology Landscape in the Mexico Wind Power Industry

Advanced Turbine Technology

Modern wind turbines with larger rotor diameters and higher hub heights are enabling greater energy capture per installation, improving project economics across Mexico's established wind corridors. These advances support repowering initiatives at legacy sites in Oaxaca and Tamaulipas.

Grid Integration and Storage Pairing

Battery storage integration alongside wind capacity is emerging as a technology priority, helping manage intermittency and reduce curtailment in transmission-constrained regions. SENER's 2025-2030 planning cycle explicitly incorporates storage alongside renewable capacity additions.

Digital Monitoring and Predictive Maintenance

Remote monitoring platforms and predictive maintenance tools are improving turbine uptime and reducing unplanned outages across Mexico's wind fleet, supporting operators in maximizing output from existing assets amid permitting constraints on new capacity.

Offshore Wind Feasibility Technology

Floating and fixed-bottom offshore turbine technologies, proven in other global markets, are increasingly referenced in early Mexican feasibility studies as developers assess the country's coastal wind resource potential for future utility-scale deployment.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Location |

Onshore |

93.8% |

2025 |

|

Region |

Southern Mexico |

44.7% |

2025 |

By Location

Onshore wind leads at 93.8% (2025), reflecting decades of development across the Isthmus of Tehuantepec, Tamaulipas, and Nuevo León, supported by mature turbine technology, established grid connections, and lower capital intensity compared to offshore alternatives.

To access detailed market analysis, Request Sample

Offshore wind, at 6.2% share in 2025, remains an emerging segment with limited installed capacity but growing developer interest, supported by Mexico's extensive Gulf and Pacific coastlines and global cost declines in offshore turbine technology.

Regional Market Insights

|

Region |

Share (2025) |

Key Mexico Wind Power Market Drivers & Characteristics |

|

Southern Mexico |

44.7% |

Anchored by the Isthmus of Tehuantepec's exceptional wind resource, supported by established transmission infrastructure and a long operating history of utility-scale wind farms. |

|

Northern Mexico |

31.5% |

Reflects strong wind resources in Tamaulipas and Nuevo León, supported by industrial electricity demand and proximity to cross-border transmission links. |

|

Central Mexico |

16.3% |

Supported by moderate wind resources and proximity to major demand centers, with growth linked to grid modernization and state-led capacity tenders. |

|

Others |

7.5% |

Other regions, including the Yucatán Peninsula and Baja California, contribute through smaller, geographically dispersed wind installations and emerging project pipelines. |

Southern Mexico's 44.7% dominance is supported by the Isthmus of Tehuantepec's globally recognized wind corridor, where consistent, high-velocity winds have anchored the bulk of the country's installed wind capacity for over a decade. Northern Mexico's 31.5% share follows, driven by industrial demand and established wind resources in Tamaulipas.

Central Mexico's 16.3% reflects moderate wind resources balanced against proximity to demand centers, while Others at 7.5%, spanning the Yucatán Peninsula and Baja California, contribute through smaller and more dispersed wind project pipelines.

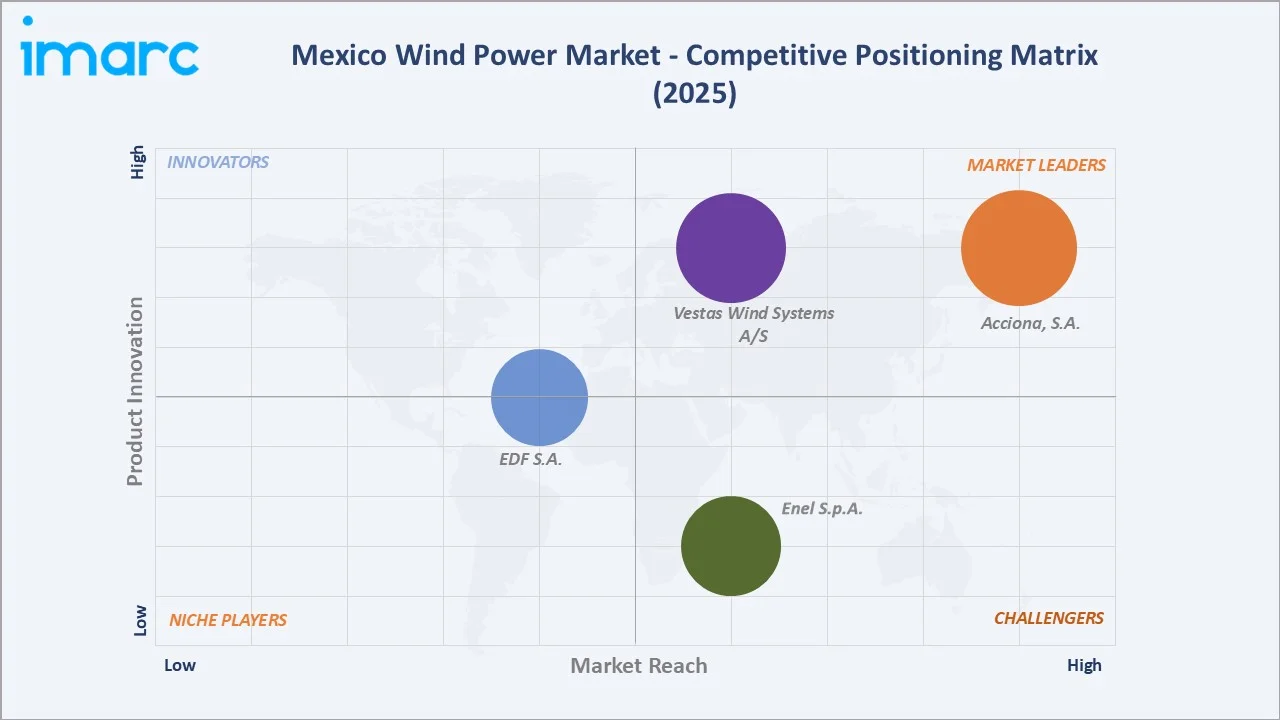

Competitive Landscape

The Mexico wind power market is moderately competitive, with multinational utilities and turbine manufacturers operating alongside regional developers. Key firms focus on project development, turbine supply, and long-term operations and maintenance contracts. Competition is shaped by grid access, regulatory alignment with state-majority requirements, and technical execution capability.

|

Company |

Subsidiary |

Market Position |

Core Strength |

|

Acciona, S.A. |

ACCIONA Energía México |

Market Leader |

End-to-end value chain integration, leadership in total operational capacity, and its pioneering use of advanced, in-house wind turbine technologies like 120-meter-high concrete towers |

|

Vestas Wind Systems A/S |

Vestas WTG México S.A. de C.V. |

Market Leader |

Large-scale project execution, an installed base exceeding 2.7 GW, and long-term Active Output Management (AOM) service contracts |

|

Enel S.p.A. |

Enel Green Power México |

Strong Challenger |

Operates a robust, multi-state portfolio with over 1.6 GW of wind power capacity across Mexico |

|

EDF S.A. |

EDF Renewables Mexico |

Established Player |

Ability to originate, develop, and operate large-scale, private off-taker wind projects, primarily concentrated in the highly windy Oaxaca (Isthmus of Tehuantepec) region |

Companies are increasingly focused on portfolio realignment amid Mexico's 2025 regulatory reforms, with several developers reviewing asset structures to balance state-majority requirements with continued operations. Turbine manufacturers are also strengthening long-term service agreements to capture recurring revenue from Mexico's existing wind fleet.

Key Company Profiles

Acciona, S.A.

Acciona Energía operates a significant wind generation portfolio in Mexico, including 198 MW San Carlos wind farm in Tamaulipas. Acciona also develops cutting-edge wind turbines and provides EPC services for major projects across the country.

- Regional Subsidiary: ACCIONA Energía México

- Strategic Focus: Balancing capital recycling through selective asset sales with continued development optionality in Mexico's wind sector.

Vestas Wind Systems A/S

Vestas is a prominent turbine supplier to the Mexico wind power market, since 1994 when they installed the country's first commercial wind turbine. With regional headquarters in Mexico City, the company has accumulated over 2.7 GW of operational wind power capacity in the region.

- Regional Subsidiary: Vestas WTG México S.A. de C.V.

- Strategic Focus: Expanding turbine deliveries and service agreements as Mexico's wind fleet matures and repowering opportunities increase.

Enel S.p.A.

Enel Green Power México maintains a renewable generation presence in Mexico spanning wind and solar assets. The company continues to operate within Mexico's evolving regulatory framework, balancing existing generation contracts with the state-majority dispatch requirements introduced in 2025.

- Regional Subsidiary: Enel Green Power México

- Strategic Focus: Maintaining operational continuity across its existing Mexican renewable portfolio while assessing opportunities aligned with state-led planning.

Market Concentration Analysis

The Mexico wind power market shows moderate concentration, with a handful of multinational utilities and turbine manufacturers accounting for the majority of installed capacity, particularly across the Isthmus of Tehuantepec corridor. Mexico's 2025 energy reform, requiring at least 54% of dispatched electricity from CFE-owned plants, is reshaping the competitive structure by limiting the addressable opportunity for purely private generation. At the same time, turbine supply and operations and maintenance services remain moderately fragmented, with multiple international vendors competing for service contracts across the country's aging wind fleet. Consolidation pressure is evident among some private developers reassessing their Mexican holdings amid the regulatory transition.

Investment & Growth Opportunities

Highest Growth Segments

Offshore wind (~2.8% CAGR), Southern Mexico (~1.6% CAGR), and turbine repowering services represent the Mexico wind power market's highest-growth investment vectors through 2034, even as overall market expansion remains measured under the current regulatory framework.

Investment Themes

- State-Aligned Wind Tenders: SENER's binding planning scheme is creating a structured pipeline of wind project opportunities for developers able to align with CFE's 54% dispatch requirement, supported by approved capacity additions and grid strengthening investment exceeding USD 8 billion.

- Repowering and O&M Services: Aging turbines across Oaxaca's wind corridor are creating recurring investment opportunities in repowering, component supply, and long-term operations and maintenance contracts as operators seek to extend asset life and improve output.

Future Market Outlook (2026-2034)

The Mexico wind power market is projected to grow from 7.60 Gigawatt in 2025 to 8.55 Gigawatt by 2034, delivering a 1.29% CAGR over the forecast period through grid modernization, state-aligned renewable tendering, and gradual private-sector re-engagement. The market's anchor size of 8.10 Gigawatt in 2030 reflects the midpoint of Mexico's transition toward its expanded capacity targets under Plan México.

Three structural forces define Mexico wind power market growth through 2034. First, continued grid transmission investment exceeding USD 8 billion is expected to ease historical interconnection bottlenecks that have constrained wind capacity additions. Second, the binding planning framework introduced in 2025 is creating a more predictable, state-coordinated pipeline for new wind projects, even as it narrows the role of fully private developers. Third, the repowering of legacy wind assets in Oaxaca and Tamaulipas is expected to add incremental capacity without requiring new land acquisition, supporting steady output growth across the forecast period.

Research Methodology

Primary Research

Primary research comprised structured discussions with wind project developers, turbine suppliers, grid operators, and energy policy specialists across Mexico. Inputs were gathered on installed capacity trends, regulatory impact, regional development patterns, and competitive positioning to validate market estimates and qualitative findings.

Secondary Research

Secondary research encompassed government energy planning documents, including SENER's national development programs, utility company disclosures, and industry association data. Public sources on installed capacity, regional wind resource assessments, and regulatory developments were reviewed to map market structure and competitive dynamics.

Forecasting Models

Forecasting models combined historical capacity addition trends, government capacity expansion targets, and regulatory scenario analysis to project future market size. The analysis incorporated expected grid investment, repowering activity, and the impact of Mexico's 2025 energy reform on private-sector participation, validated through triangulation of primary and secondary research.

Mexico Wind Power Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Gigawatt |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Location Covered | Onshore, Offshore |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Acciona, S.A., Vestas Wind Systems A/S, Enel S.p.A., EDF S.A., etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico wind power market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico wind power market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico wind power industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Wind Power Market Report Report

The Mexico wind power market reached 7.60 Gigawatt in 2025, supported by rising electricity demand, declining turbine technology costs, and Mexico's renewable capacity expansion targets under Plan México.

The Mexico wind power market grows at 1.29% CAGR during 2026-2034, reaching 8.55 Gigawatt by 2034, reflecting steady, policy-anchored expansion.

Onshore wind leads at 93.8% share in 2025, supported by mature turbine technology and established grid connections across Oaxaca and Tamaulipas.

Southern Mexico leads at 44.7% share in 2025, anchored by the Isthmus of Tehuantepec's exceptionally strong and consistent wind resource.

Leading companies include Acciona, S.A., Vestas Wind Systems A/S, Enel S.p.A., and EDF S.A., among others.

The market is projected to reach approximately 8.10 Gigawatt by 2030, supported by grid modernization investment and state-aligned renewable tendering.

The reform requires at least 54% of dispatched electricity from CFE-owned plants, narrowing the opportunity for fully private wind developers while creating a structured, state-coordinated project pipeline.

Key drivers include renewable capacity expansion targets, rising industrial electricity demand, and declining wind turbine technology costs.

Grid interconnection bottlenecks and regulatory uncertainty over private-sector participation remain the primary restraints on faster market expansion.

Key opportunities include state-aligned wind tenders under the binding planning scheme and repowering of aging onshore wind farms in Oaxaca and Tamaulipas.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)