Refrigerant Market Size, Share, Trends and Forecast by Product Type, Application, and Region 2026-2034

Refrigerant Market Size, Share, Trends & Forecast (2026-2034)

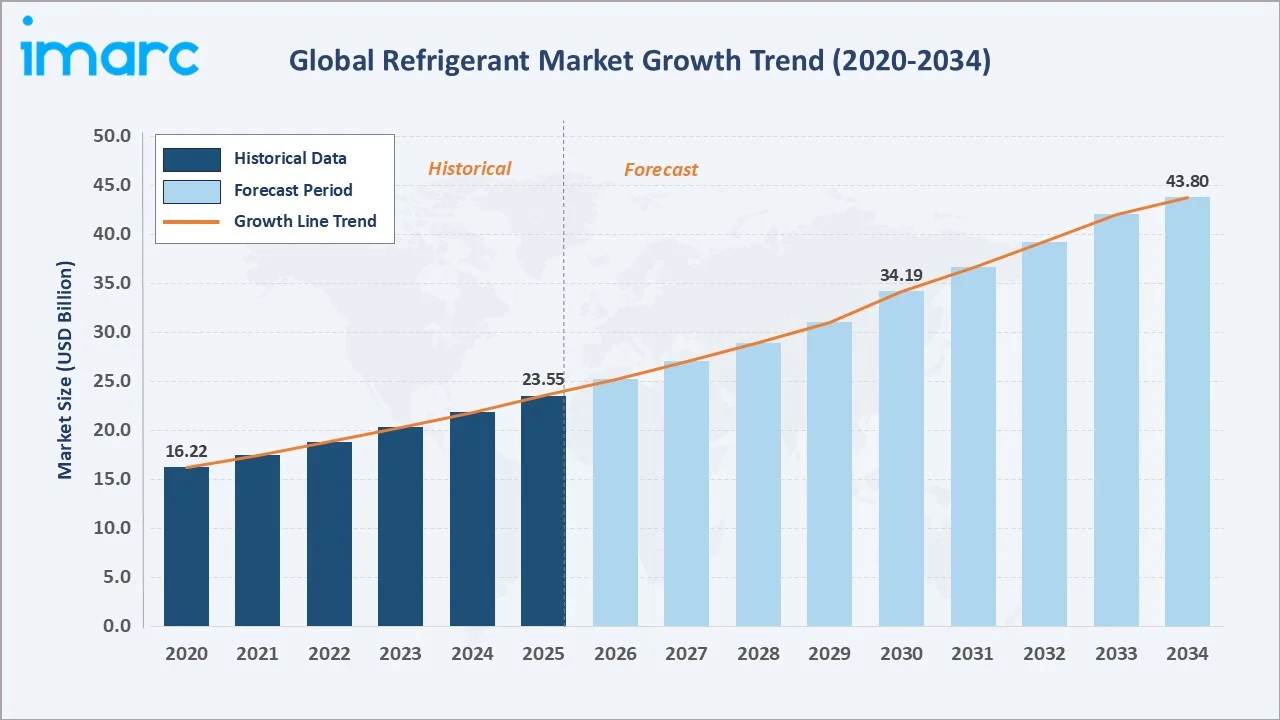

The global refrigerant market was valued at USD 23.55 Billion in 2025 and is projected to reach USD 43.80 Billion by 2034, expanding at a CAGR of 7.74% during the forecast period (2026-2034). The refrigerant market growth is underpinned by surging demand for cooling systems across residential, commercial, and industrial segments, tightening environmental regulations mandating the adoption of low-global-warming-potential (GWP) alternatives, and rapid urbanization across the Asia Pacific.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 23.55 Billion |

|

Forecast Market Size (2034) |

USD 43.80 Billion |

|

CAGR (2026-2034) |

7.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

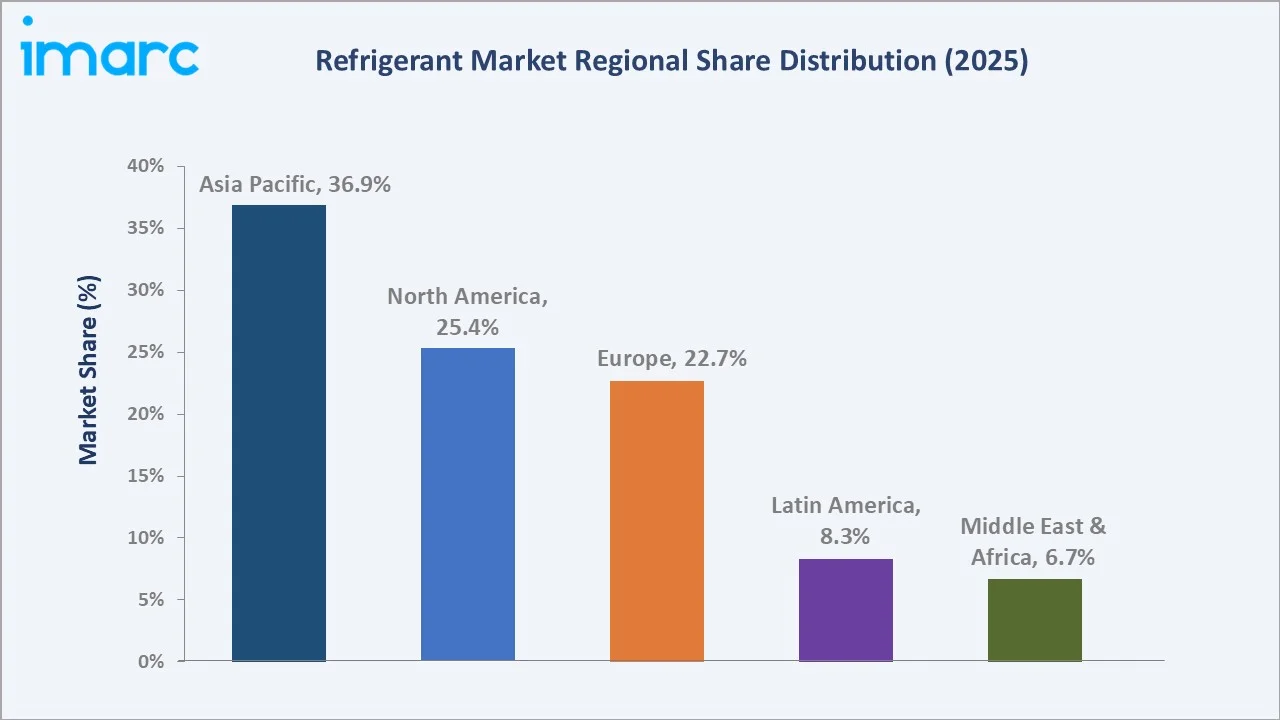

Asia Pacific – 36.9% |

|

Fastest Growing Region |

Asia Pacific |

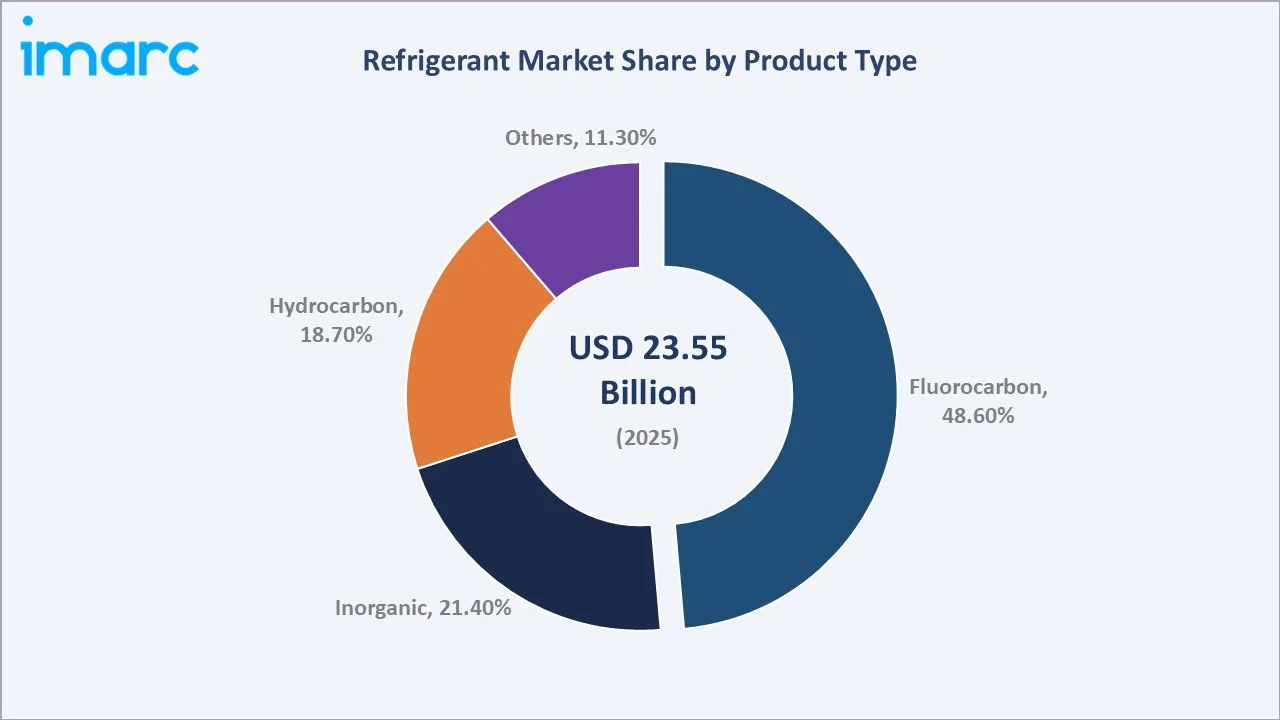

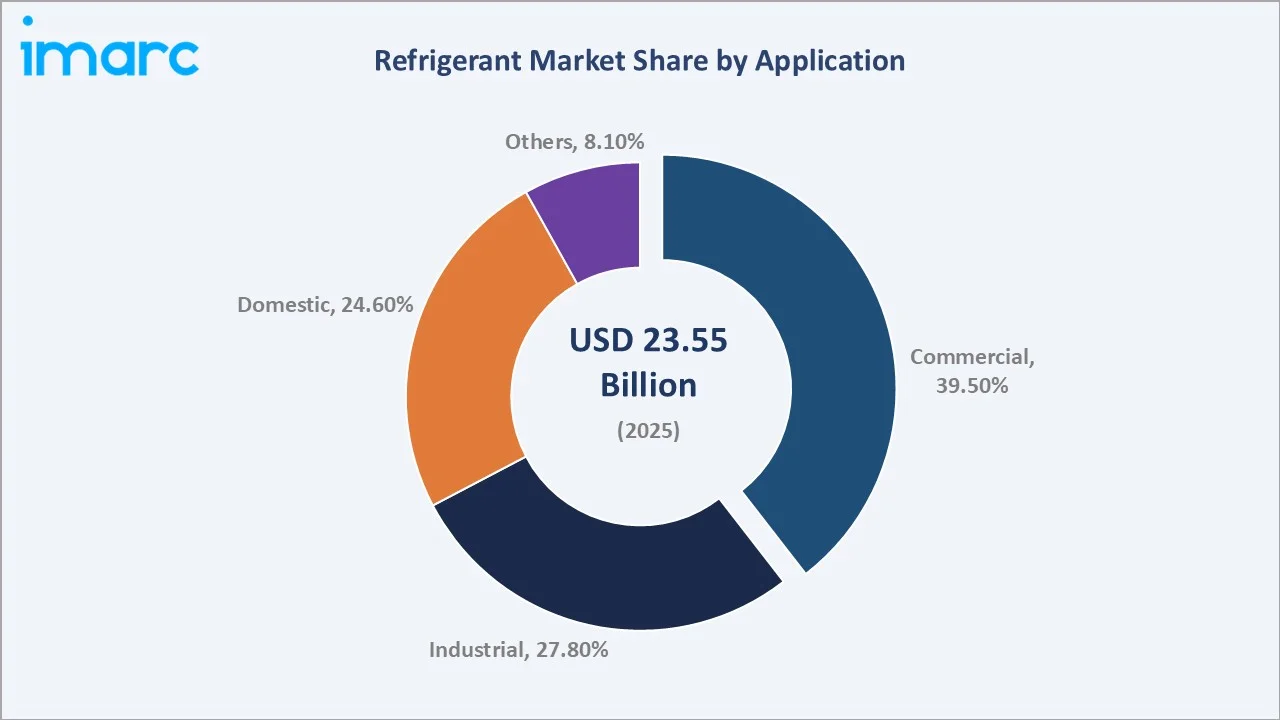

Fluorocarbon refrigerants continue to lead by product type, holding a 48.6% share in 2025, while the commercial application segment dominates with 39.5% of total market revenue. Asia Pacific accounts for the largest regional share at 36.9% in 2025.

To get more information on this market, Request Sample

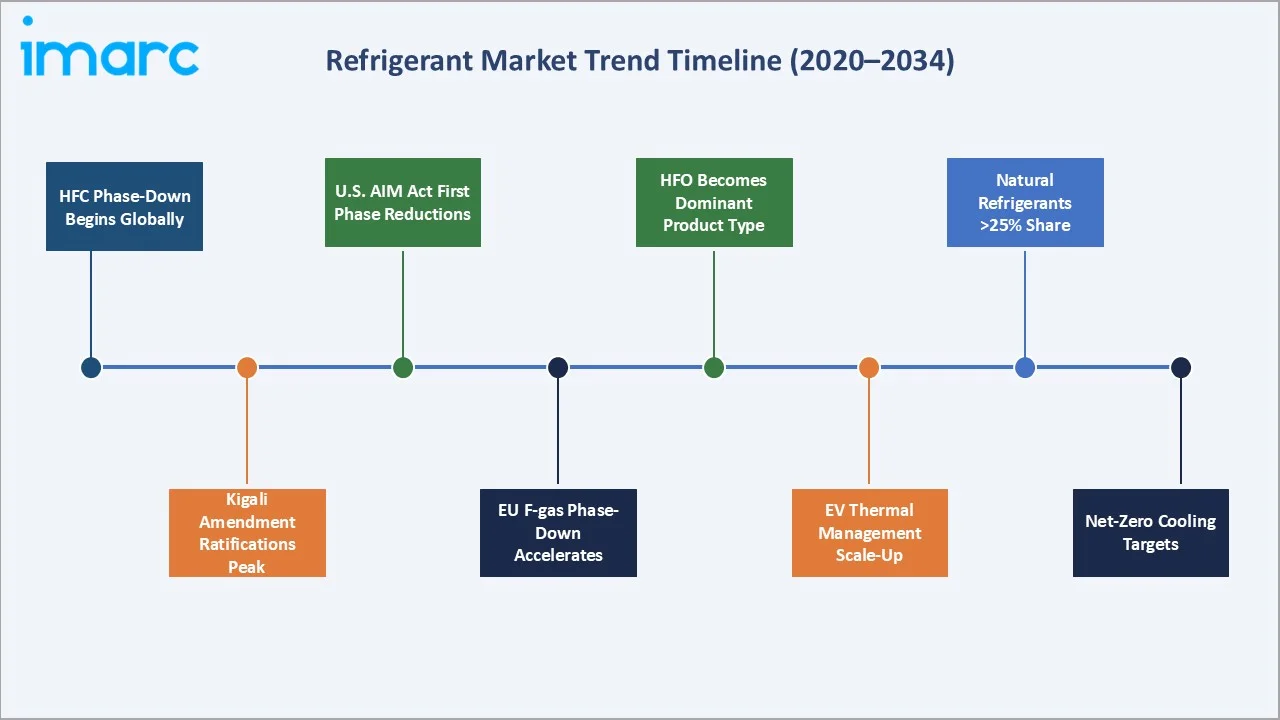

The industry is undergoing a major transition toward low-global-warming-potential (GWP) and environmentally friendly refrigerants, influenced by stringent regulations such as the Kigali Amendment and regional phase-down policies. Technological advancements, along with the adoption of natural refrigerants and energy-efficient systems, are reshaping the competitive landscape and driving innovation across the value chain.

Executive Summary

The global refrigerant market continues to expand at a robust pace, driven by intensifying demand for air conditioning, industrial refrigeration, and cold-chain infrastructure across the globe. Valued at USD 23.55 Billion in 2025, the market is forecast to reach USD 43.80 Billion by 2034, reflecting a steady CAGR of 7.74%.

Key growth drivers include the accelerating phase-out of high-GWP hydrofluorocarbons (HFCs) under the Kigali Amendment, which is steering manufacturers and end-users toward next-generation hydrofluoroolefin (HFO) and natural refrigerant alternatives. Fluorocarbon refrigerants remain dominant in 2025, yet investment in hydrocarbon and inorganic variants is rising sharply as environmental compliance requirements tighten across the European Union, North America, and the Asia Pacific.

From a regional standpoint, Asia Pacific leads global demand with a 36.9% share, supported by China and India's construction booms and expanding cold-chain networks. North America follows with 25.4%, while Europe holds 22.7%, propelled by the EU's stringent F-gas regulations. The competitive landscape is moderately consolidated, with Solstice Advanced Materials Inc., Daikin Industries Ltd, The Chemours Company, Arkema S.A., and Linde plc among the key market participants driving product innovation and geographic expansion.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Fluorocarbon – 48.6% share (2025) |

|

Largest Application Segment |

Commercial – 39.5% share (2025) |

|

Leading Region |

Asia Pacific – 36.9% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – CAGR 7.74% (2026–2034) |

|

Top Companies |

Solstice Advanced Materials Inc., Daikin Industries Ltd, The Chemours Company, Arkema S.A., Linde plc |

|

Market Opportunity |

Transition to low-GWP refrigerants: >USD 20B incremental value by 2034 |

Key Analytical Observations Supporting The Above Data:

- Fluorocarbon refrigerants dominate with a 48.6% share (2025), owing to their wide compatibility with existing HVAC-R equipment and well-established supply chains globally.

- Commercial applications lead with 39.5% of total market revenue (2025), reflecting strong demand from supermarkets, cold-storage warehouses, and hospitality facilities.

- Asia Pacific accounts for 36.9% of global refrigerant demand (2025), driven by rapid urbanization and expanding food and beverage cold chains in China and India.

- The Kigali Amendment is reshaping the competitive landscape, accelerating adoption of HFO and natural refrigerants that offer substantially lower GWP profiles.

- Electric vehicle proliferation is creating significant new demand for specialized refrigerants used in battery thermal management systems.

- Low-GWP refrigerant innovation represents the largest market opportunity through 2034, with governments worldwide committing billions in incentives for eco-compliant cooling transitions.

Global Refrigerant Market Overview

The global refrigerant industry encompasses the production, distribution, and end-use application of chemical compounds used in refrigeration cycles, air conditioning systems, and heat pumps. Refrigerants serve as the thermodynamic medium that absorbs heat at low temperatures and releases it at high temperatures, enabling temperature-controlled environments across residential, commercial, industrial, and automotive sectors.

The ecosystem spans raw material producers, chemical manufacturers, HVAC equipment OEMs, cold-chain logistics providers, and end-use industries, including food processing, retail, pharmaceuticals, and data centers.

Macroeconomic influences such as rising per capita incomes, increasing urbanization rates, and escalating ambient temperatures driven by climate change are creating sustained structural demand for refrigerants. Global average temperatures continue to set records, reinforcing the essential nature of cooling infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

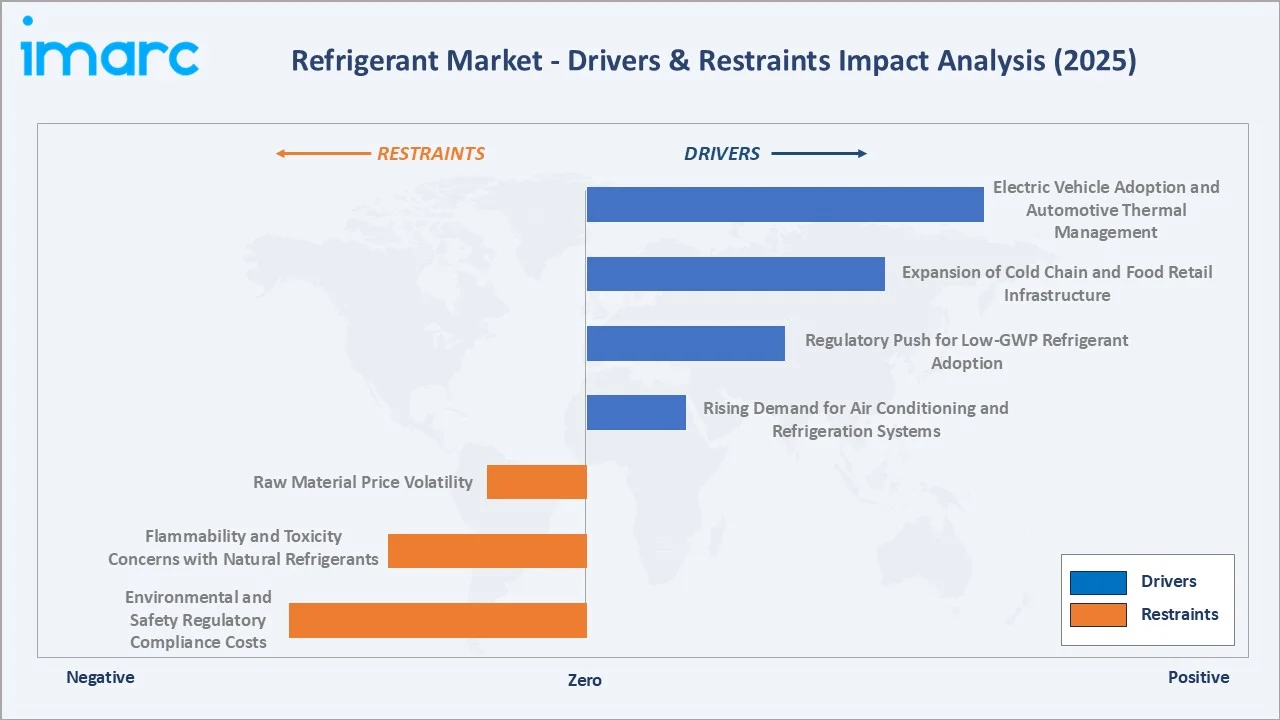

Market Drivers

- Rising Demand for Air Conditioning and Refrigeration Systems: Air conditioning alone accounts for approximately 55% of total refrigerant consumption, with demand accelerating in tropical and emerging markets. Urbanization rates exceeding 55% globally and rising disposable incomes in developing economies are fueling HVAC system adoption across residential and commercial buildings.

- Regulatory Push for Low-GWP Refrigerant Adoption: The Kigali Amendment to the Montreal Protocol and the EU's revised F-gas Regulation are driving a major transition away from HFCs. The U.S. AIM Act mandates an 85% reduction in HFC production by 2036, stimulating substantial demand for HFO alternatives such as R-1234yf and R-1234ze.

- Expansion of Cold Chain and Food Retail Infrastructure: The pharmaceutical sector's growing need for temperature-controlled logistics for vaccines and biologics is adding a premium demand segment. Cold-chain market in India exceeded USD 26.60 billion in 2024, underpinning growth in refrigerant demand.

- Electric Vehicle Adoption and Automotive Thermal Management: EVs require advanced refrigerant-based thermal management systems for battery temperature control. Global EV sales surpassed 4 million units in Q1 2025, a 35% increase over the first quarter of 2024, with each vehicle requiring specialized refrigerants for both cabin conditioning and battery cooling, creating a rapidly expanding end-use application vertical.

Market Restraints

- Environmental and Safety Regulatory Compliance Costs: Transitioning to new low-GWP refrigerant formulations requires substantial R&D investment, equipment retrofitting, and workforce training. Small and medium-sized operators in developing markets face disproportionate compliance burdens.

- Flammability and Toxicity Concerns with Natural Refrigerants: While hydrocarbons and ammonia offer excellent environmental profiles, their flammability (A2L and A3 classifications) and toxicity characteristics create safety complexities in densely populated or consumer-facing applications, limiting adoption in certain segments.

- Raw Material Price Volatility: Key feedstocks for fluorinated refrigerant production, including hydrofluoric acid and fluorspar, are subject to significant price fluctuations due to geopolitical supply concentrations and environmental extraction constraints.

Market Opportunities

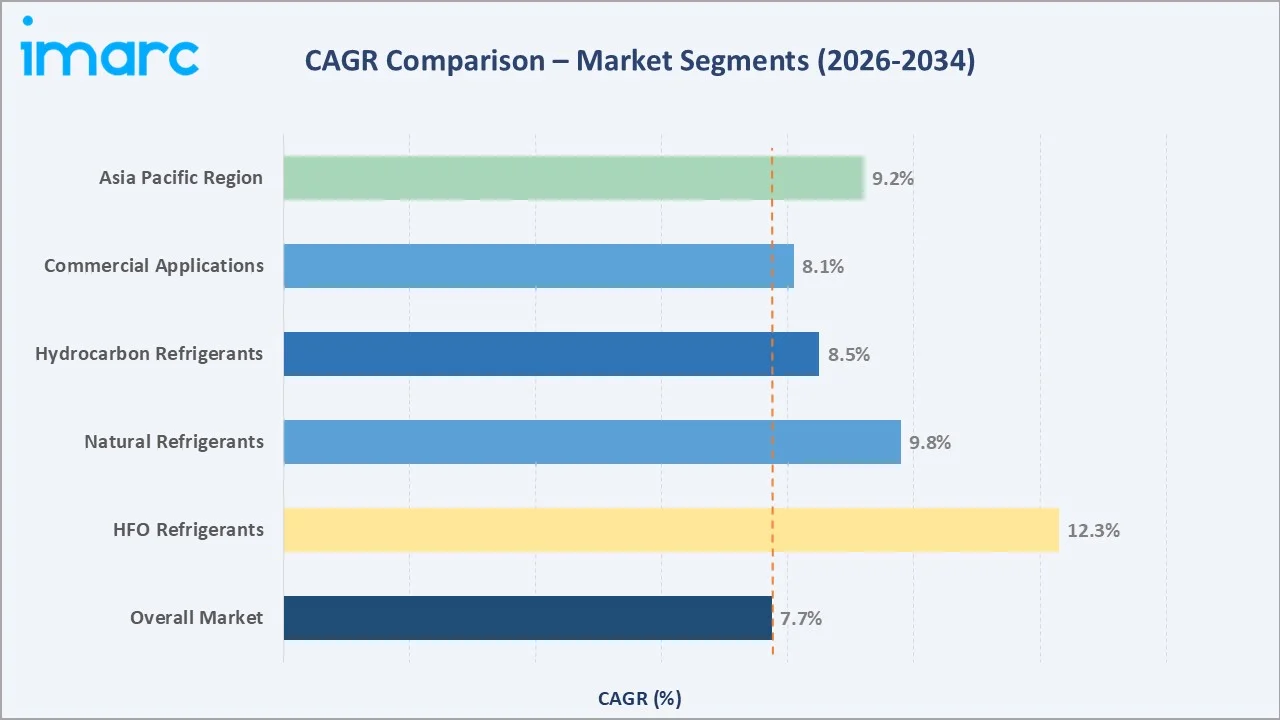

- HFO and Next-Generation Refrigerant Development: The global HFO refrigerant market is projected to grow at a CAGR exceeding 12% through 2034, representing the most significant growth opportunity. Manufacturers investing in HFO capacity and formulation capabilities stand to capture premium margins amid the regulatory-driven transition.

- Emerging Market Cold Chain Buildout: Southeast Asia, Africa, and Latin America represent multi-billion-dollar greenfield opportunities for cold-chain refrigerant demand as food safety standards and pharmaceutical distribution networks expand.

- IoT-Enabled Smart Refrigeration Systems: Integration of IoT sensors and predictive maintenance platforms into refrigeration systems is creating demand for specialized refrigerants compatible with precision-controlled, energy-efficient smart cooling architectures.

Emerging Refrigerant Market Trends

1. Accelerated Transition to HFO and Natural Refrigerants

Honeywell International Inc. launched a new low-GWP refrigerant specifically engineered for commercial cooling, underscoring the pace of product innovation. The EU F-gas phase-out roadmap, targeting a near-complete elimination of high-GWP fluorinated gases by 2050, is compelling equipment manufacturers and service operators across Europe to accelerate transitions that are subsequently cascading into global supply chains and procurement specifications.

2. Smart and IoT-Integrated Refrigeration Technologies

Smart refrigeration platforms enable real-time monitoring of refrigerant charge levels, leak detection, energy consumption optimization, and predictive maintenance scheduling. These capabilities are particularly valuable in commercial supermarket refrigeration, where refrigerant leaks account for estimated losses of 15-25% annually.

3. Expanding Pharmaceutical Cold Chain Demand

U.S. imports of cold chain-dependent food and pharmaceuticals total approximately USD 228 billion annually, supported by refrigerant-dependent systems that form the backbone of temperature-controlled warehousing and last-mile delivery. Factors, including the increasing focus on biologics, specialty pharmaceuticals, insulin products, and expanded immunization programs in developing Asian and African economies, are driving robust adoption of industrial refrigeration systems.

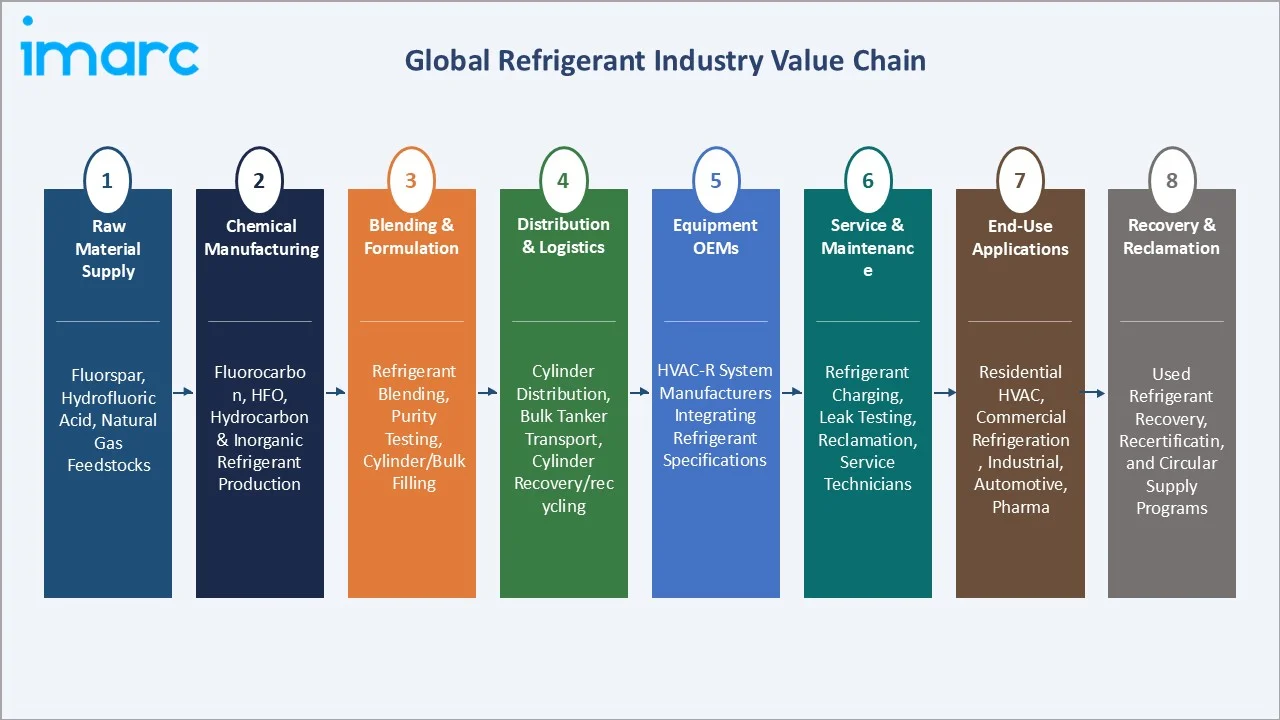

Industry Value Chain Analysis

The refrigerant value chain spans multiple interconnected stages, from upstream raw material extraction through chemical manufacturing and blending to downstream end-use application and post-use recovery. Each stage involves specialized operators whose collective performance shapes product quality, regulatory compliance, supply security, and the ultimate commercial availability of refrigerants across global HVAC-R markets.

|

Value Chain Stage |

Key Activities / Examples |

|

Raw Material Supply |

Fluorspar, hydrofluoric acid, natural gas feedstocks |

|

Chemical Manufacturing |

Fluorocarbon, HFO, hydrocarbon & inorganic refrigerant production |

|

Blending & Formulation |

Refrigerant blending, purity testing, cylinder/bulk filling |

|

Distribution & Logistics |

Cylinder distribution, bulk tanker transport, cylinder recovery/recycling |

|

Equipment OEMs |

HVAC-R system manufacturers integrating refrigerant specifications |

|

Service & Maintenance |

Refrigerant charging, leak testing, reclamation, service technicians |

|

End-Use Applications |

Residential HVAC, commercial refrigeration, industrial, automotive, pharma |

|

Recovery & Reclamation |

Used refrigerant recovery, recertification, and circular supply programs |

Technology Landscape in the Refrigerant Industry

XLPE and Advanced Insulation Materials for Refrigerant Systems

Compared to conventional heat exchangers, microchannel systems deliver measurable gains, including a 30–50% reduction in thermal resistance, a 40–60% decrease in system volume, and 20–40% lower material usage. These system-level material innovations directly influence refrigerant demand profiles, favoring lower-GWP, lower-charge alternatives.

Smart Monitoring and AI-Powered Refrigerant Management

AI-powered refrigerant monitoring systems are enabling predictive maintenance by analyzing real-time performance data from embedded sensors tracking temperature, pressure, superheat, and subcooling. Commercial supermarket operators deploying smart refrigerant monitoring have reported reductions in annual refrigerant leak rates of 30–50%, generating meaningful compliance and cost benefits under tightening F-gas and EPA reporting requirements.

Pre-Molded and Cold-Shrink Component Innovation

The refrigerant accessories and system connection segment is undergoing a materials transition driven by the shift to lower-GWP refrigerants. Pre-molded gaskets, O-ring seal assemblies, and cold-shrink terminations are being re-engineered in HNBR, EPDM, and PTFE compounds compatible with HFO and hydrocarbon refrigerants, which exhibit different swell and permeation characteristics compared to legacy HFCs.

Sustainable and Eco-Friendly Refrigerant Technology

In Europe, CO2 trans critical systems now account for over 30% of new commercial refrigeration installations in food retail, up from less than 5% a decade ago. Honeywell’s Solstice ze refrigerant, recognized for its exceptionally low global warming potential, was selected as the working fluid for Ireland’s first low-carbon district heating network in Dublin, demonstrating HFO technology’s expanding application beyond traditional HVAC-R into decarbonized thermal energy systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Fluorocarbon |

48.6% |

2025 |

|

Application |

Commercial |

39.5% |

2025 |

|

Region |

Asia Pacific |

36.9% |

2025 |

By Product Type

Fluorocarbon refrigerants dominate the global refrigerant market with a 48.6% share in 2025, reflecting their entrenched position across HVAC-R applications worldwide. These include hydrochlorofluorocarbons (HCFCs), hydrofluorocarbons (HFCs), and the emerging hydrofluoroolefins (HFOs), which represent the fastest-growing sub-category within fluorocarbons.

To access detailed market analysis, Request Sample

Inorganic refrigerants, primarily ammonia (R-717) and carbon dioxide (R-744), hold 21.4% of the market, finding particular strength in industrial refrigeration due to superior energy efficiency. Hydrocarbon refrigerants, including propane (R-290) and isobutane (R-600a), account for 18.7%, increasingly adopted in domestic appliances across Europe and Asia, given zero ODP and near-zero GWP profiles.

By Application

The commercial application segment leads the refrigerant market with a 39.5% revenue share in 2025, encompassing supermarkets, hypermarkets, convenience stores, hospitality facilities, and commercial HVAC systems. Commercial refrigeration systems in modern supermarkets typically contain 500-2,000 kg of refrigerant charge, representing significant recurring demand through maintenance and leak replenishment cycles.

The industrial application segment holds 27.8% of market share, spanning food processing facilities, chemical plants, pharmaceutical manufacturing, and large-scale cold storage warehouses. The domestic segment at 24.6% is witnessing robust growth, particularly in Asia Pacific and Africa, driven by rising household incomes and increasing refrigerator and air conditioner ownership rates.

Regional Market Insights

Asia Pacific dominates the global refrigerant market with a 36.9% revenue share in 2025. According to ICRA, the Indian room air conditioner market expanded by 20–25% year-on-year in FY25, achieving record sales of around 12.5 million units. China's implementation of F-gas management controls and India's HCFC phase-out schedule under the Montreal Protocol are simultaneously creating significant demand for compliant HFC and HFO alternatives.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Key Players |

|

Asia Pacific |

36.9% |

Urbanization, construction boom, cold chain expansion |

China F-gas controls, India HCFC phase-out |

Daikin, Dongyue, AGC, SRF |

|

North America |

25.4% |

AIM Act compliance, EV adoption, data center cooling |

U.S. AIM Act HFC reduction mandates |

Honeywell, Chemours, Linde |

|

Europe |

22.7% |

F-gas regulation, green building mandates, retail cold chain |

EU F-gas phase-down schedule |

Arkema, Air Liquide, Orbia |

|

Latin America |

8.3% |

Expanding retail refrigeration, rising temperatures |

HCFC phase-out, growing HFC regulations |

Orbia, SRF, regional distributors |

|

Middle East & Africa |

6.7% |

District cooling expansion, pharmaceutical cold chain |

GCC HVAC standards, Kigali ratification |

Honeywell, Air Liquide, Linde |

North America holds a 25.4% share of the global refrigerant market in 2025. The U.S. has emerged as a major region in the refrigerant market owing to many factors, including the implementation of the American Innovation and Manufacturing (AIM) Act, which mandates an 85% reduction in HFC production and consumption by 2036. This regulatory framework is driving substantial procurement of R-410A replacements such as R-454B and R-32 across residential and commercial HVAC applications.

Competitive Landscape

The global refrigerant market exhibits a moderately consolidated competitive structure, with the top six to eight players collectively controlling an estimated 55–60% of global market revenues. Leading companies are differentiated by their proprietary low-GWP formulation capabilities, fluorochemical manufacturing scale, global distribution networks, and regulatory affairs expertise.

|

Company Name |

Brand / Division |

Market Position |

Core Strength |

|

Solstice Advanced Materials Inc. |

Solstice / Genetron |

Market Leader |

HFO innovation, Solstice portfolio |

|

Daikin Industries Ltd |

Daikin Refrigerants |

Market Leader |

Vertically integrated HVAC-R |

|

The Chemours Company |

Freon/ Opteon |

Market Leader |

HFO scale, OEM partnerships |

|

Arkema S.A. |

Forane |

Strong Challenger |

European F-gas compliance |

|

Linde plc |

Linde Industrial Gases |

Strong Challenger |

Industrial & cryogenic refrigerants |

|

Air Liquide |

Airgas Refrigerants |

Strong Challenger |

Industrial gas distribution |

|

Dongyue Group |

Dongyue |

Cost Leader |

Chinese fluorochemical scale |

|

Orbia Advance Corporation S.A.B. de CV |

Klea |

Challenger |

Latin America distribution |

|

Sinochem Group |

Sinochem |

Challenger |

Chinese market penetration |

|

AGC Group |

AMOLEA |

Specialist |

Specialty fluorochemicals |

|

SRF Limited |

FLORON |

Regional Leader |

India & emerging market focus |

|

Gujarat Fluorochemicals Limited |

GFL |

Emerging |

India capacity scale-up |

Innovation in HFO refrigerants, natural refrigerant system solutions, and digital refrigerant management platforms represents the primary competitive frontier. Strategic partnerships between refrigerant chemical producers and HVAC equipment OEMs are accelerating the commercialization of next-generation formulations.

Key Company Profiles

Daikin Industries Ltd.

Daikin Industries Ltd., headquartered in Osaka, Japan, is the world’s largest air conditioning manufacturer and a fully vertically integrated refrigerant producer. Its unique vertical integration from refrigerant chemistry through finished HVAC equipment gives it unmatched control over product compatibility and market positioning.

- Product Portfolio: HFC and HFO refrigerants (R-32, R-410A, R-452B); residential and commercial air conditioner systems; industrial refrigeration solutions; fluorochemical intermediates and specialty fluids.

- Recent Developments: In June 2025, Daikin Industries Ltd. entered a strategic partnership with The Chemours Company to co-develop next-generation, environmentally friendly refrigerants optimized for high-efficiency smart HVAC systems, targeting HFO-based blends with ultra-low GWP profiles for residential and commercial applications.

- Strategic Focus: Driving global adoption of R-32 (a lower-GWP HFC) as a transitional refrigerant, advancing direct R-32 and R-452B adoption across Asia Pacific and Europe, expanding proprietary HFO development capabilities, and leveraging HVAC system integration to secure refrigerant specification advantages.

The Chemours Company

The Chemours Company, spun off from DuPont in 2015 and headquartered in Wilmington, Delaware, is one of the world’s largest fluorochemicals producers. Chemours markets its refrigerant portfolio under the iconic Freon (legacy HFCs) and Opteon (next-generation HFOs) brand families.

- Product Portfolio: Opteon™ HFO refrigerants (R-1234yf, R-1234ze, R-454B, R-466A); Freon™ legacy HFC and HCFC refrigerants; specialty fluoropolymers; chemical intermediates.

- Recent Developments: The Chemours Company entered into an agreement with Zhejiang Juhua Group, Ltd. to expand production capacity of its ultra-low GWP HFO foam blowing agent Opteon 1100 and specialty fluids Opteon SF33, with expansion expected to triple the capacity of HFO-1336MZZZ.

- Strategic Focus: Expanding Opteon HFO production scale to meet accelerating global demand from automotive and commercial HVAC OEMs, securing long-term supply agreements with major HVAC equipment manufacturers, and deepening sustainability credentials through third-party verified low-GWP refrigerant certifications.

Arkema S.A.

Arkema S.A. is a French specialty chemicals and advanced materials company headquartered in La Défense, France. Arkema produces and markets refrigerants under the Forane® brand, with particular strength in European markets navigating the EU F-gas phase-down regulation.

- Product Portfolio: Forane HFO and HFC refrigerants (R-32, R-452B, R-454B, R-1234yf); specialty fluoropolymers; PVDF materials; refrigerant reclamation and recertification services.

- Recent Developments: Arkema has continued to expand its Forane next-generation refrigerant portfolio in response to the EU F-gas Regulation’s accelerated phase-down schedule, with growing sales across European commercial refrigeration and heat pump markets.

- Strategic Focus: European market leadership in F-gas compliant refrigerants, positioning Forane® HFO products as the preferred solution for European HVAC-R operators undergoing mandatory refrigerant transitions, and expanding heat pump refrigerant supply as European heat pump adoption accelerates under the REPowerEU framework.

Linde plc

Linde plc, headquartered in UK, is the world’s largest industrial gas company by revenue. Linde supplies industrial-grade refrigerants, primarily carbon dioxide (R-744) and ammonia (R-717), alongside specialty refrigerant gas blends for industrial and commercial applications.

- Product Portfolio: Carbon dioxide (R-744) for transcritical and cascade refrigeration; ammonia (R-717) for industrial cold storage; specialty refrigerant gas blends; cryogenic cooling solutions; gas handling equipment and services.

- Recent Developments: Linde has expanded its CO2 supply capabilities in response to the rapid growth of transcritical CO2 refrigeration in European food retail, where regulatory mandates are accelerating the replacement of high-GWP HFC systems.

- Strategic Focus: Capitalizing on the structural shift toward natural refrigerants (CO2 and ammonia) by expanding industrial gas distribution networks, developing turnkey natural refrigerant supply solutions for food retail and cold chain operators, and leveraging its existing global gas infrastructure to serve new high-growth refrigerant demand verticals.

Market Concentration Analysis

The global refrigerant market exhibits moderate to high concentration at the top end, with the leading five players—Honeywell International Inc., The Chemours Company, Daikin Industries Ltd., Arkema S.A., and Linde plc, collectively accounting for an estimated 50–55% of global revenues in 2025. The remainder of the market is distributed among regional chemical producers, specialty gas distributors, and Chinese fluorochemical manufacturers.

The HFO sub-segment demonstrates significantly higher concentration than the broader refrigerant market, as proprietary formulation patents and capital-intensive manufacturing requirements create substantial barriers to entry. Solstice Advanced Materials Inc. and The Chemours Company together hold the dominant share of commercially available HFO capacity globally, with Arkema S.A. as the leading European HFO producer.

Entry barriers remain substantial, given the capital intensity of fluorochemical manufacturing, stringent environmental permitting requirements, and the long qualification cycles demanded by major HVAC-R OEMs before adopting new refrigerant suppliers.

Investment & Growth Opportunities

Fastest Growing Segments

HFO refrigerants, CO2-based transcritical systems, and hydrocarbon refrigerants for domestic appliances represent the three highest-growth investment vectors in the global refrigerant market through 2034. The HFO segment alone is forecast to grow at a CAGR exceeding 12% during the forecast period, driven by regulatory mandates and OEM adoption. These segments collectively address an incremental total addressable market opportunity of over USD 20 billion by 2034.

Emerging Market Expansion

Southeast Asia, Sub-Saharan Africa, and the Indian subcontinent represent the most compelling geographic investment opportunities through 2034. India's refrigerant market is growing at a rate significantly above the global average, with urbanization, rising incomes, and expanding pharma cold-chain infrastructure as primary catalysts. Indonesia and Vietnam are also high-priority emerging markets for refrigerant capacity investment and distribution partnerships.

Venture and Strategic Investment Trends

Strategic investment activity is intensifying across the refrigerant value chain, with major chemical companies allocating substantial capital toward HFO production capacity expansion. Key investment themes include natural refrigerant system engineering, IoT-integrated refrigerant management platforms, and circular economy models for refrigerant recovery and reclamation. Private equity interest in specialty refrigerant distribution and service businesses is growing as regulatory transitions create premium service opportunities.

Future Refrigerant Market Outlook (2026-2034)

The global refrigerant market is positioned for sustained, robust growth through 2034, anchored by the convergence of climate-driven cooling demand growth, regulatory-mandated product transitions, and technological innovation in low-GWP formulations. From its 2025 base of USD 23.55 Billion, the market is forecast to reach USD 43.80 Billion by 2034, representing an absolute incremental value of approximately USD 20.25 billion.

The next decade will be defined by the decisive phase-out of HFCs across major economies, with HFOs and natural refrigerants capturing the majority of replacement demand. Manufacturers that invest early in next-generation formulation capabilities, strategic OEM partnerships, and global distribution infrastructure will achieve disproportionate competitive positioning.

Asia Pacific will continue to expand its dominant market share as urbanization deepens across China, India, and Southeast Asia, while North America and Europe will be shaped primarily by regulatory compliance timelines and green building mandates. The refrigerant market forecast to 2034 reflects one of the most significant mandated industrial transitions of the current decade.

Research Methodology

Primary Research

Primary research for this report included structured interviews with industry executives, procurement managers, HVAC equipment OEM representatives, refrigerant distributors, service technicians, and end-users across North America, Europe, and the Asia Pacific. Expert consultations with regulatory affairs specialists and environmental scientists informed the regulatory analysis and product transition timeline assessments.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, patent databases, trade publications (ASHRAE Journal, Cooling Post, ACR News), industry associations (EPEE, ACCA, AHRI), government databases (EPA, UN Environment Programme), and peer-reviewed scientific literature.

Forecasting Models

Market size estimations and growth projections were derived using both top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, refrigerant consumption per cooling unit, cooling equipment installation data, regulatory phase-down schedules, and historical compound annual growth patterns. Scenario analysis was conducted across base, optimistic, and conservative cases to account for uncertainty in regulatory implementation timelines and raw material pricing.

Refrigerant Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Fluorocarbon, Inorganic, Hydrocarbon, Others |

| Applications Covered | Commercial, Industrial, Domestic, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Solstice Advanced Materials Inc., Daikin Industries Ltd, The Chemours Company, Arkema S.A., Linde plc, Air Liquide, Dongyue Group, Orbia Advance Corporation S.A.B. de CV, Sinochem Group, AGC Group, SRF Limited, Gujarat Fluorochemicals Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the refrigerant market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global refrigerant market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the refrigerant industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Refrigerant Market Report

The global refrigerant market was valued at USD 23.55 Billion in 2025.

The refrigerant market is projected to reach USD 43.80 Billion by 2034, exhibiting a CAGR of 7.74% during 2026-2034.

Key drivers include rising global cooling demand, the Kigali Amendment HFC phase-down, expansion of cold-chain infrastructure, and growing EV adoption requiring thermal management refrigerants.

Asia Pacific dominates the refrigerant market with a 36.9% share in 2025, driven by urbanization, construction growth, and expanding cold-chain infrastructure in China and India.

Fluorocarbon refrigerants lead the market with a 48.6% share in 2025, though HFOs within this category are the fastest-growing sub-segment amid regulatory transitions.

Commercial applications hold the largest share at 39.5% in 2025, encompassing supermarkets, commercial HVAC systems, cold-storage warehouses, and hospitality facilities.

The Kigali Amendment is driving a rapid global transition from high-GWP HFCs to HFOs and natural refrigerants, reshaping product portfolios and procurement strategies across the value chain.

Leading companies include Solstice Advanced Materials Inc., Daikin Industries Ltd, The Chemours Company, Arkema S.A., Linde plc., Air Liquide, Dongyue Group, Orbia Advance Corporation S.A.B. de CV, Sinochem Group, AGC Group, SRF Limited, and Gujarat Fluorochemicals Limited.

Key trends include the transition to HFO and natural refrigerants, IoT-integrated smart refrigeration systems, pharmaceutical cold-chain expansion, and electric vehicle thermal management applications.

North America accounts for 25.4% of the global refrigerant market in 2025, driven by the U.S. AIM Act compliance cycle and growing EV and data center cooling demand.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)