Saudi Arabia Industrial Paints & Coatings Market Size, Share, Trends and Forecast by Product Type, Type, Application, End User, and Region, 2026-2034

Saudi Arabia Industrial Paints & Coatings Market Size, Share, Trends & Forecast (2026-2034)

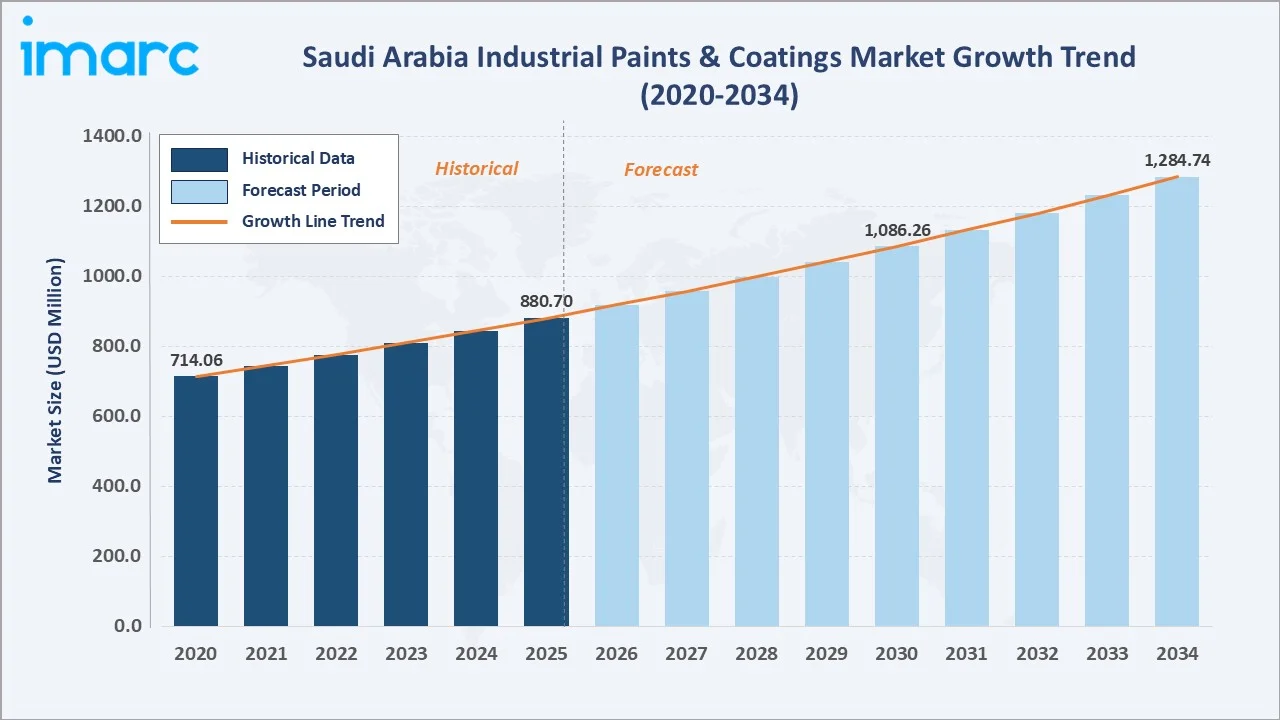

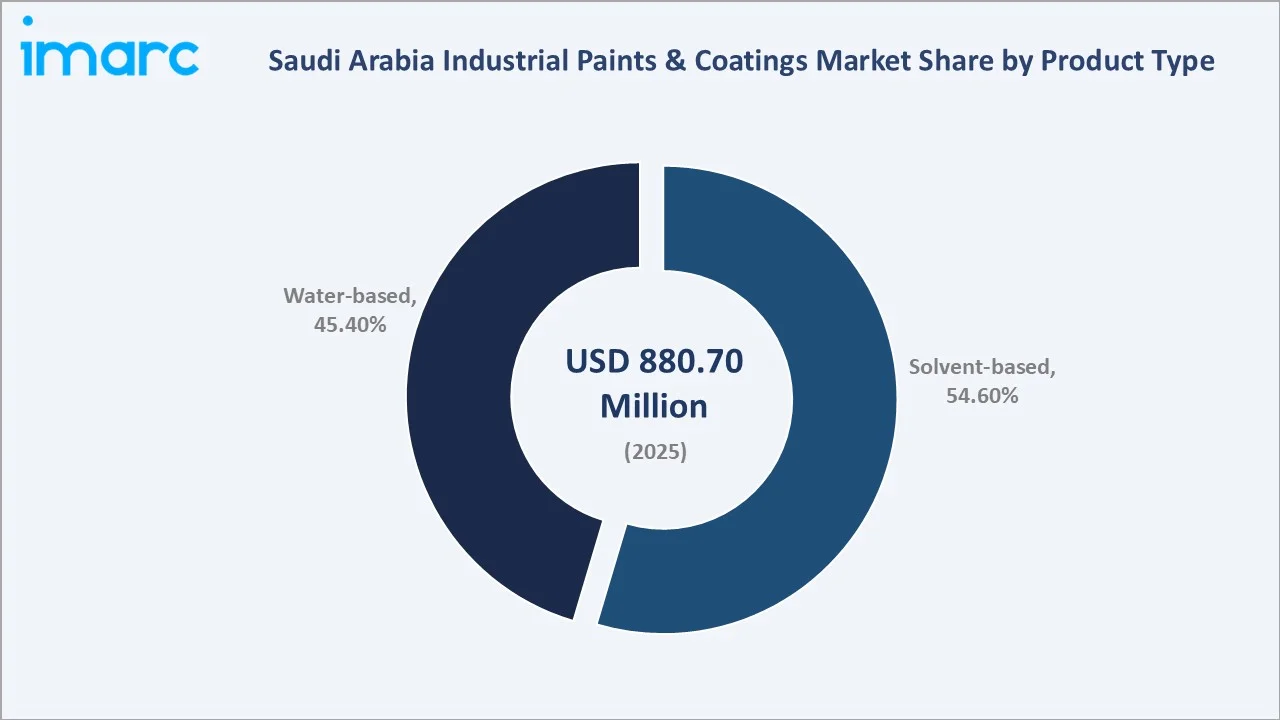

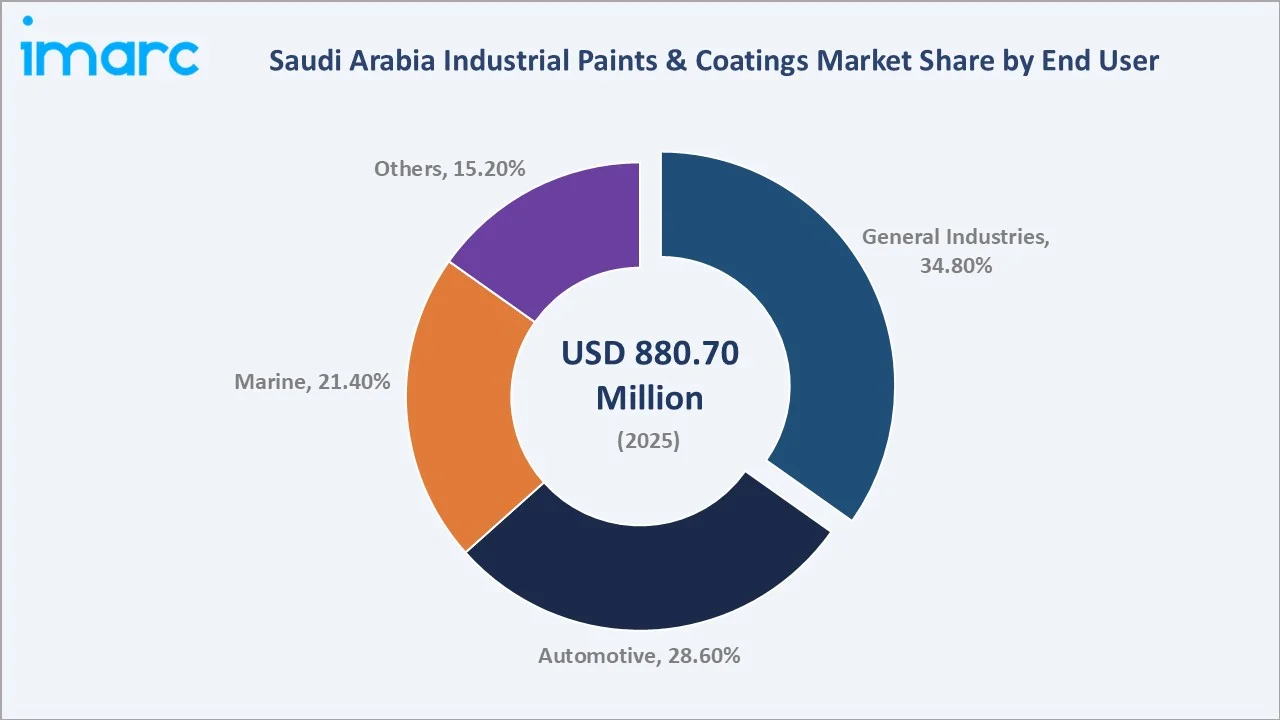

The Saudi Arabia industrial paints & coatings market reached USD 880.70 Million in 2025 and is projected to reach USD 1,284.74 Million by 2034, exhibiting a CAGR of 4.28% during 2026-2034. Robust growth is driven by expanding construction activity under Vision 2030, increasing oil and gas capital expenditure, and rising adoption of high-performance protective and smart coatings across industrial end markets.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 880.70 Million |

|

Forecast Market Size (2034) |

USD 1,284.74 Million |

|

CAGR (2026-2034) |

4.28% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Eastern Region (36.2% share, 2025) |

|

Fastest Growing Region |

Western Region (Vision 2030 mega-project pipeline) |

To get more information on this market, Request Sample

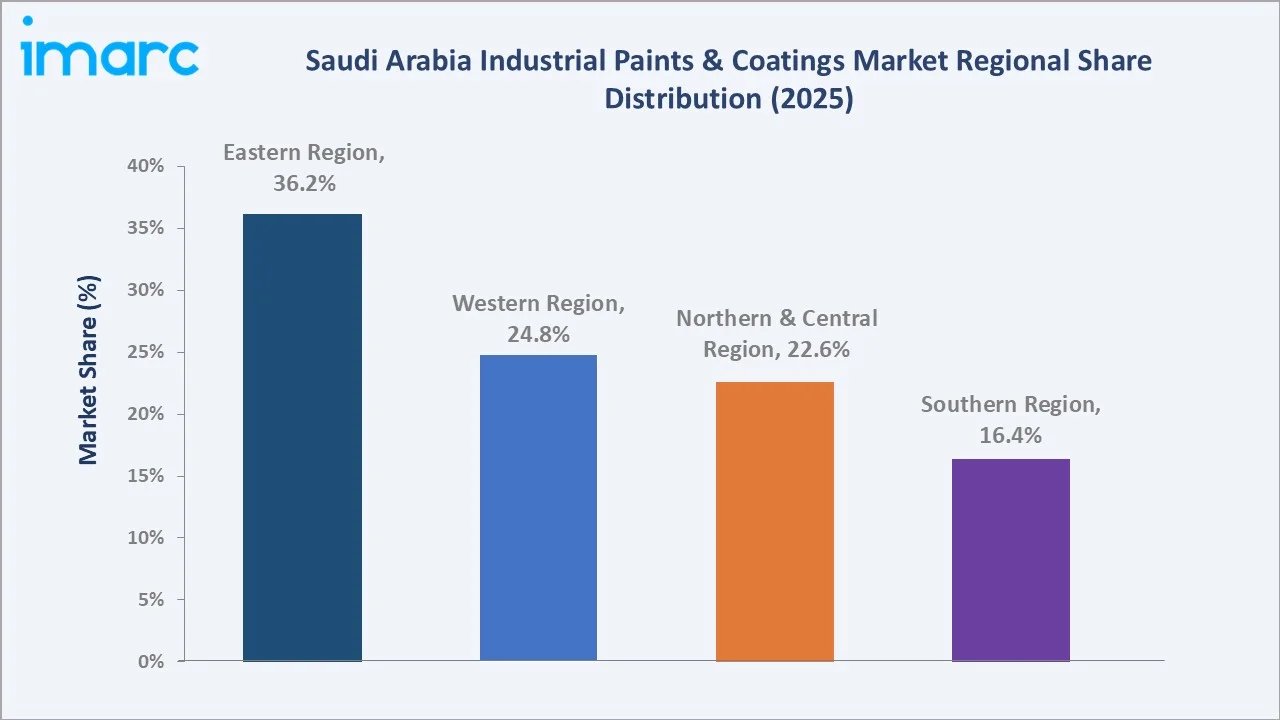

The Eastern region dominates with a 36.2% share, anchored by Dammam and Jubail's dense petrochemical and manufacturing corridors, while solvent-based coatings retain the largest product share at 54.6%.

The Saudi Arabia Industrial Paints & Coatings market is experiencing robust growth, driven by the country's expanding manufacturing sector, construction boom, and increasing demand for durable and high-performance coatings across various industries. The market is supported by a strong focus on infrastructure development, particularly in sectors such as oil & gas, automotive, and construction, along with government initiatives aimed at diversifying the economy under the Vision 2030 plan.

Executive Summary

The Saudi Arabia industrial paints & coatings market is on a sustained growth trajectory, fueled by transformative infrastructure investments, the accelerating rollout of Vision 2030 giga-projects, and deepening industrialization across petrochemicals, marine, and automotive sectors. The market registered USD 880.70 Million in 2025, and the market is projected to reach USD 1,284.74 Million by 2034.

Solvent-based coatings retain dominance with a 54.6% share in 2025, underpinned by superior adhesion and corrosion resistance in extreme heat and humidity conditions prevalent across Saudi Arabia's industrial zones. However, water-based formulations are gaining traction at 45.4%, driven by tightening environmental regulations on volatile organic compound (VOC) emissions and increased corporate sustainability commitments.

Geographically, the Eastern region accounts for 36.2% of revenues, concentrated around ARAMCO and SABIC supply chains in Jubail Industrial City. The Western region (24.8%) is emerging as the second-largest market, buoyed by the Red Sea Project, NEOM, and expanding Jeddah port infrastructure. The Northern and Central region holds 22.6%, primarily driven by Riyadh's construction-related demand, while the Southern Region accounts for 16.4%, supported by agricultural-industrial activities.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Solvent-based – 54.6% share (2025) |

|

Largest Segment (End User) |

General Industries – 34.8% share (2025) |

|

Leading Region |

Eastern Region – 36.2% revenue share (2025) |

|

Fastest Growing Region |

Western Region (Vision 2030 projects) |

|

Top Companies |

JOTUN A/S, Akzo Nobel N.V., Hempel A/S, Sherwin-Williams Company, and PPG Industries Inc. |

|

Market Opportunity |

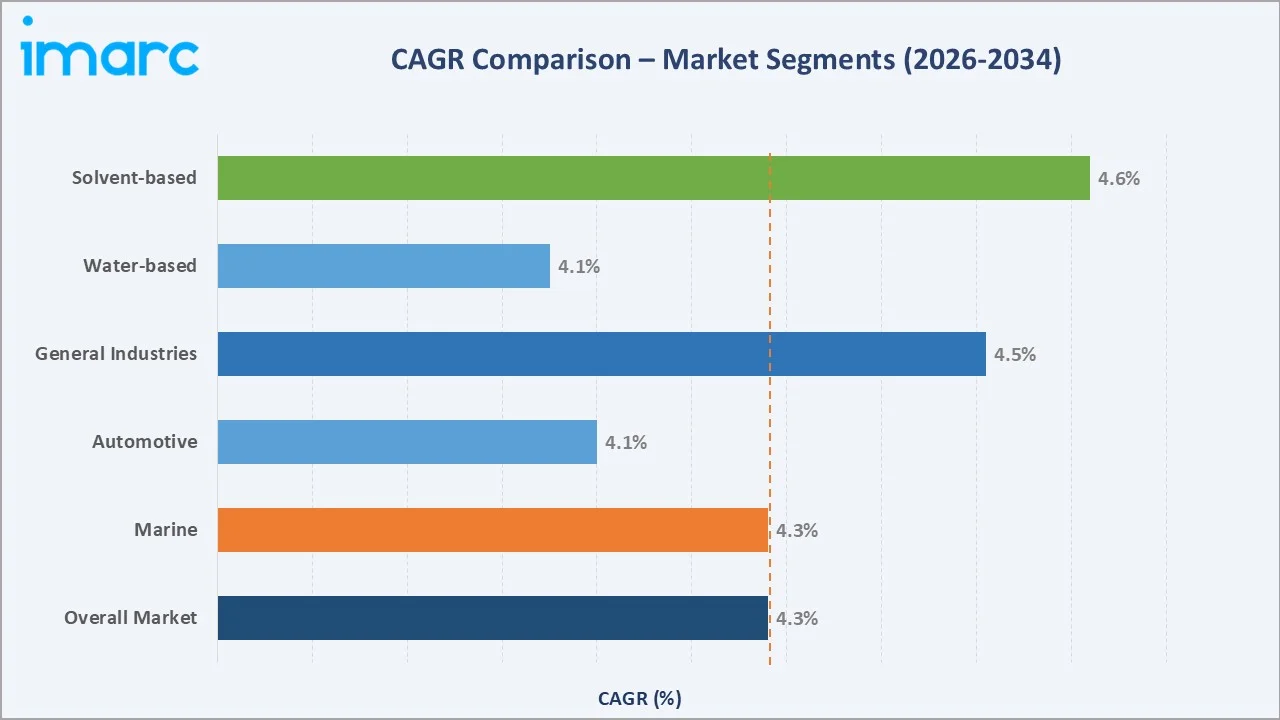

Water-based coatings projected the fastest growth at a CAGR 4.51% |

Key Analytical Observations Supporting the Above Data:

- Solvent-based coatings represent 54.6% of the market in 2025, preferred for high-performance industrial applications requiring corrosion, heat, and chemical resistance in Saudi Arabia's petrochemical and offshore environments.

- Water-based formulations account for 45.4% (2025), growing at the fastest rate among product types as environmental regulations on VOC emissions tighten and manufacturers respond with low-emission product lines.

- General Industries led end-user demand at 34.8% (2025), covering manufacturing plants, warehouses, storage tanks, and pipelines, sectors expanding rapidly under Saudi Arabia's industrial diversification agenda.

- Automotive accounts for 28.6% of demand, driven by OEM coating requirements at assembly facilities and a robust vehicle refinish market across major urban centers, including Riyadh, Jeddah, and Dammam.

- Marine coatings represent 21.4%, supported by Saudi Arabia's strategic Red Sea and Arabian Gulf maritime infrastructure, including ARAMCO offshore installations and commercial port expansions at Jeddah and Ras Al-Khair.

- The Eastern Region's 36.2% share reflects the highest concentration of petrochemical plants, refineries, and industrial estates, making it the primary consumption hub for protective and specialty coatings.

Saudi Arabia Industrial Paints & Coatings Market Overview

Industrial paints and coatings are engineered surface treatment systems applied to protect, decorate, or enhance the functional performance of substrates across metal, concrete, and composite structures. In Saudi Arabia, the market ecosystem spans raw polymer and resin suppliers, pigment manufacturers, paint formulators, distribution networks, and specialized application service providers.

The kingdom's unique climatic conditions – extreme ambient temperatures frequently exceeding 45°C, high UV radiation, and coastal salinity along both the Red Sea and Arabian Gulf coasts – create structural demand for high-performance, durable coatings not typically required in temperate markets.

Vision 2030 is the most transformative catalyst reshaping demand. The program's USD 1 trillion investment pipeline across NEOM, the Red Sea Project, Diriyah Gate, and the expansion of King Salman Energy Park (SPARK) directly drives procurement of industrial coatings for structural steel, pipelines, water infrastructure, and industrial facilities.

Market Dynamics

To evaluate market opportunities, Request Sample

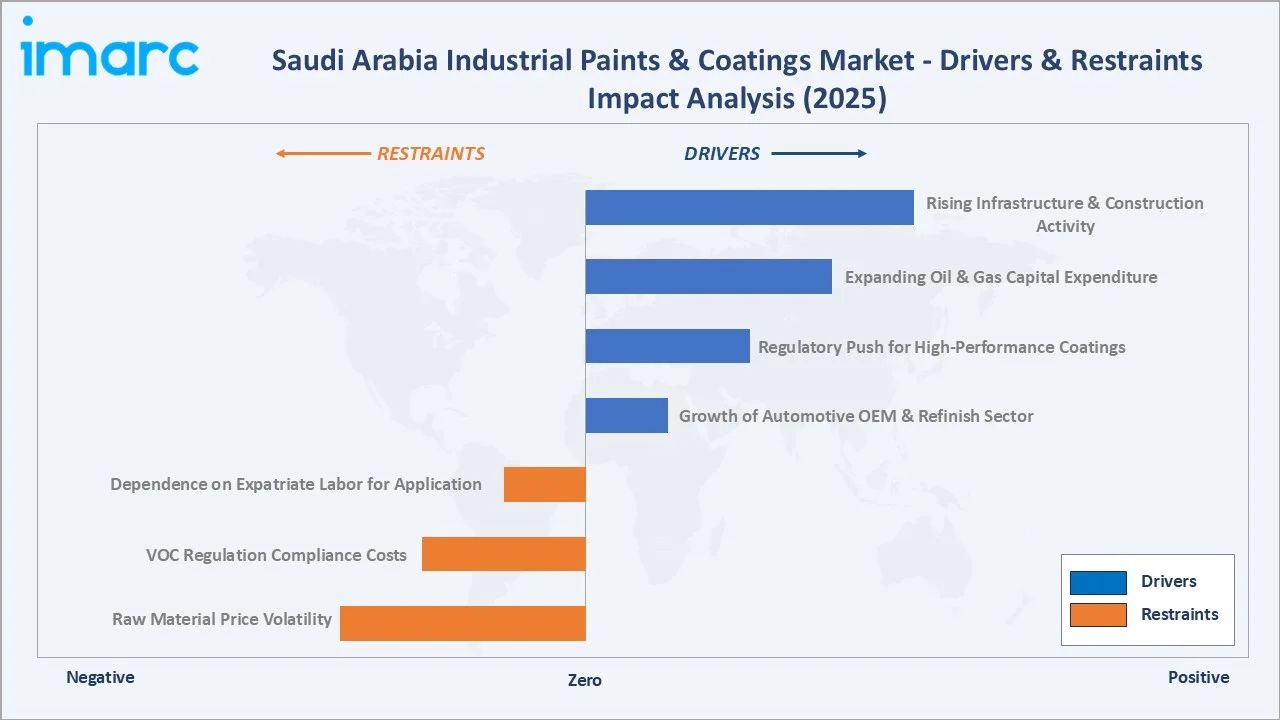

Market Drivers

- Rising Infrastructure and Construction Activity: Saudi Arabia's construction market has become a leader in the Middle East and North Africa, with an estimated value of USD 70.33 billion in 2024, and is expected to grow to USD 91.36 billion by 2029.

- Expanding Oil and Gas Capital Expenditure: Saudi Aramco's planned capacity expansion to 13 MMBPD by 2027 and ongoing SHAYBAH and Hasbah upstream projects necessitate large-volume application of epoxy, polyurethane, and intumescent fire-protection coatings across upstream, midstream, and downstream assets.

- Regulatory Push for High-Performance Coatings: SASO (Saudi Standards, Metrology and Quality Organization) has progressively tightened performance standards for industrial coatings, incentivizing adoption of certified, higher-margin products and disadvantaging cheaper non-compliant substitutes.

- Growth of Automotive OEM and Refinish Sector: Saudi Arabia's automotive sector is expanding, with new assembly ventures announced under Vision 2030, including Lucid Motors' Jeddah facility. OEM coating requirements and a robust insurance-driven refinish market support consistent demand from coating manufacturers.

Market Restraints

- Raw Material Price Volatility: Key inputs, including epoxy resins, titanium dioxide, and petrochemical-derived solvents, are subject to global commodity price fluctuations. TiO₂ prices surged approximately 22% between 2021 and 2023, compressing manufacturer margins and reducing affordability for price-sensitive buyers.

- VOC Regulation Compliance Costs: Transitioning solvent-based product lines to low-VOC or waterborne formulations requires significant R&D investment, re-testing against SASO standards, and capex upgrades, burdens more easily absorbed by global multinationals than local formulators.

- Dependence on Expatriate Labor for Application: Skilled surface treatment applicators remain predominantly expatriate workers. Nitaqat localization quotas and periodic labor market disruptions create supply chain uncertainties for installation-dependent coating demand.

Market Opportunities

- Smart and Functional Coatings: Self-healing, anti-fouling, heat-reflective, and IoT-compatible monitoring coatings represent a high-growth niche, with Saudi Aramco and SABIC piloting smart coating trials in Dammam and Yanbu refineries to reduce re-coating frequency and maintenance shutdowns.

- Green Building and LEED Compliance: Saudi Arabia's Green Building Code, effective from 2025, mandates low-VOC interior coatings in commercial and government buildings, opening a new regulatory compliance-driven market for water-based industrial formulators.

- Localization Under Vision 2030: The In-Kingdom Total Value Add (IKTVA) program incentivizes local manufacturing of industrial inputs, providing tariff advantages and preferred procurement status for coating companies establishing local blending or full production operations.

Market Challenges

- Counterfeit and Sub-Standard Products: Non-compliant coating imports from Southeast Asian markets undercut premium suppliers on price, particularly in smaller industrial and commercial projects where end-user technical literacy is limited.

- Project Delivery Delays: Infrastructure mega-project timelines are subject to execution risk. Delays in NEOM phases, for example, create lumpy, front-loaded demand, complicating inventory planning for coating distributors.

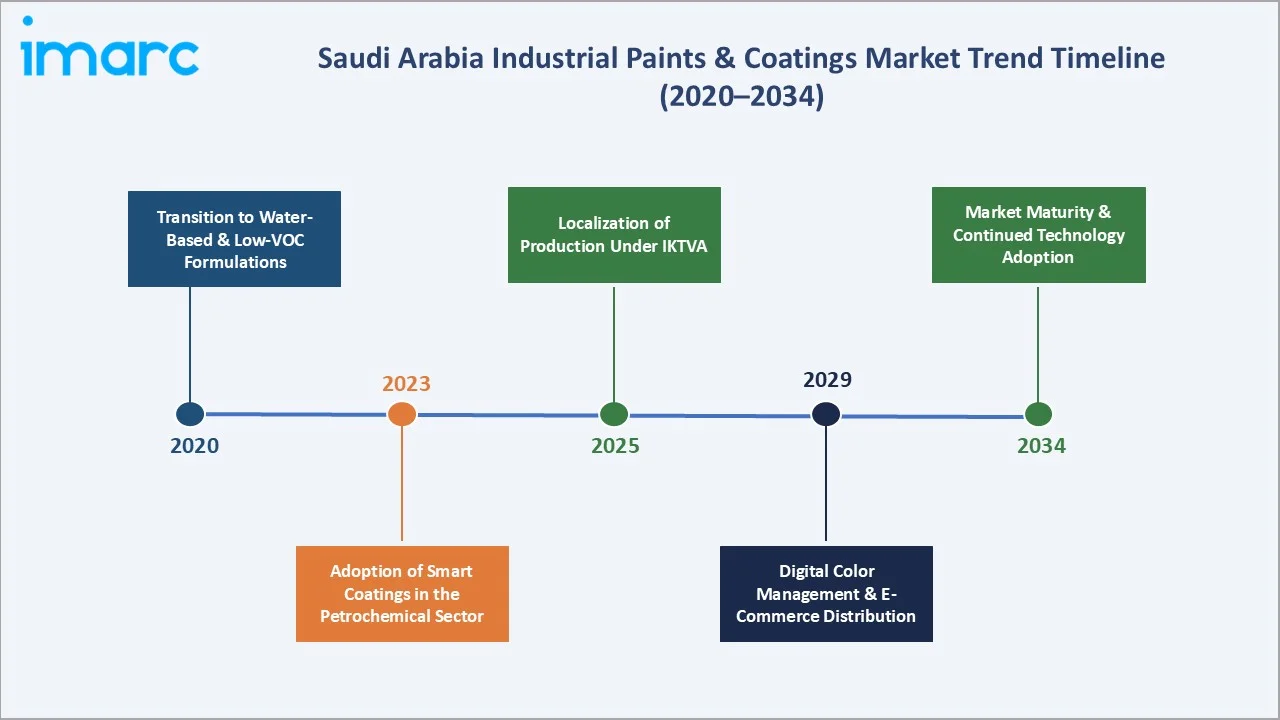

Emerging Market Trends

1. Transition to Water-Based and Low-VOC Formulations

SASO's progressive alignment with EU REACH standards is accelerating reformulation across the industry. Water-based coatings grew from 40.1% of market share in 2020 to 45.4% in 2025, a gain of 5.3 percentage points, reflecting structural, regulatory, and sustainability-driven demand shift.

2. Adoption of Smart Coatings in the Petrochemical Sector

In 2023, ARAMCO established 32 new local manufacturers, leading to the introduction of products previously manufactured outside the Kingdom, including specialty coatings for drilling equipment.

3. Localization of Production Under IKTVA

Jotun expanded its powder coatings production facility in Dammam to significantly boost capacity, increasing output by over 37%, storage by more than 28%, and operational scale by 45%, strengthening its position as a leading paint and coatings manufacturer in Saudi Arabia.

4. Digital Color Management and E-Commerce Distribution

Leading distributors are deploying AI-assisted color matching platforms and B2B e-procurement portals to improve order accuracy and reduce delivery lead times. Online and direct procurement channels are estimated to represent 12–15% of total coating sales volume in Saudi Arabia by 2025.

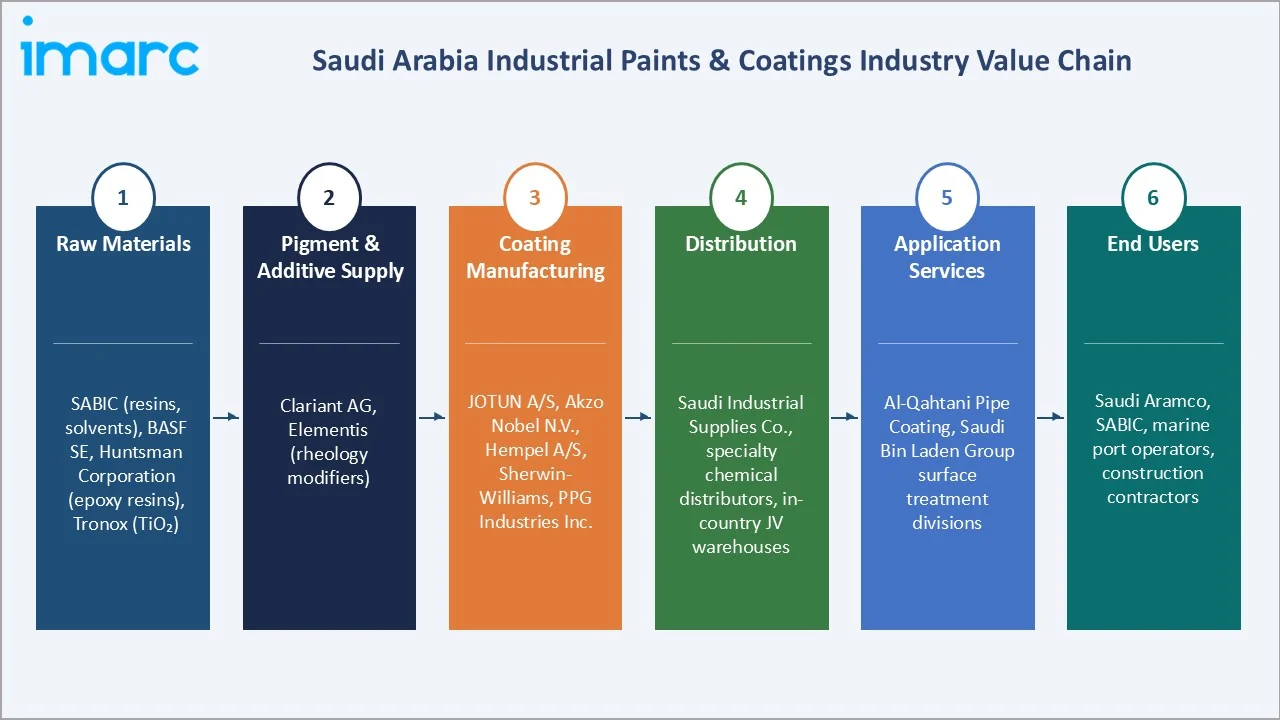

Industry Value Chain Analysis

The Saudi Arabian industrial paints and coatings value chain spans raw material production through end-consumer application, with distinct specialization at each stage:

|

Stage |

Key Players / Examples |

|

Raw Materials |

SABIC (resins, solvents), BASF SE, Huntsman Corporation (epoxy resins), Tronox (TiO₂) |

|

Pigment & Additive Supply |

Clariant AG, Elementis (rheology modifiers) |

|

Coating Manufacturing |

JOTUN A/S, Akzo Nobel N.V., Hempel A/S, Sherwin-Williams, PPG Industries Inc. |

|

Distribution |

Saudi Industrial Supplies Co., specialty chemical distributors, in-country JV warehouses |

|

Application Services |

Al-Qahtani Pipe Coating, Saudi Bin Laden Group surface treatment divisions |

|

End Users |

Saudi Aramco, SABIC, marine port operators, construction contractors |

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Solvent-based |

54.6% |

2025 |

|

Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

General Industries |

34.8% |

2025 |

|

Region |

Eastern Region |

36.2% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Solvent-based coatings dominate the Saudi Arabia market with a 54.6% share in 2025. Their dominance reflects the technical requirements of Saudi Arabia's primary industrial sectors, petrochemicals, offshore platforms, and high-temperature processing facilities, where solvent-based epoxy and polyurethane systems offer superior adhesion, chemical resistance, and application performance in extreme ambient conditions.

Water-based coatings account for 45.4% and are the fastest-growing category, driven by tightening VOC regulations, green building mandates, and improvements in waterborne formulation technology that now match solvent-based performance in many applications.

By End User

General industries represent the largest end-user segment at 34.8%, encompassing manufacturing plants, food processing facilities, water treatment infrastructure, storage terminals, and power generation assets. The segment's breadth ensures consistent baseline demand independent of oil price cycles.

Automotive follows at 28.6%, driven by OEM facilities and a substantial refinish market across Saudi Arabia's large registered vehicle fleet of over 16 million units (2024). Marine coatings account for 21.4% with critical demand from ARAMCO offshore installations, commercial shipping, and naval vessel maintenance at Jubail and Jeddah dry docks.

Regional Market Insights

The Eastern region's market leadership (36.2%, 2025) is structurally entrenched. Jubail Industrial City, the largest single industrial development project globally, is situated in Saudi Arabia's Eastern Province. Spanning 1,016 square kilometers, the city houses various industrial complexes and significant harbor and port facilities, contributing approximately 7% to Saudi Arabia's GDP.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

Eastern Region |

36.2% |

Petrochemical belt, ARAMCO/SABIC supply chain, offshore platforms |

SASO corrosion-resistance standards; Aramco contractor specifications |

JOTUN, Akzo Nobel |

|

Western Region |

24.8% |

NEOM, Red Sea Project, Jeddah Islamic Port expansion, tourism infrastructure |

Green Building Code 2025 (low-VOC) |

Sherwin-Williams, PPG Industries |

|

Northern & Central Region |

22.6% |

Riyadh construction boom, King Salman Park, government facilities |

Ministry of Municipal Affairs specifications |

Akzo Nobel, JOTUN (Riyadh branch) |

|

Southern Region |

16.4% |

Agricultural-industrial zones, Jizan Economic City, and military infrastructure |

General SASO standards |

JOTUN, regional distributors |

The Western region (24.8%) is the most dynamic growth market through the forecast period. The Red Sea Gateway Terminal Phase 1 expansion involves extending the main and feeder berths at the container terminal in Jeddah Islamic Port, Saudi Arabia, to accommodate larger vessels (up to 19,000 TEU), deepen access channels, and expand container stacking and support infrastructure.

Competitive Landscape

The Saudi Arabian industrial paints and coatings market is moderately concentrated. The top five global suppliers – JOTUN A/S, Akzo Nobel N.V., Hempel A/S, Sherwin-Williams Company, and PPG Industries Inc. – collectively hold approximately 55–60% of industrial coating revenues in 2025. The balance is distributed among regional formulators, private-label blenders, and specialist niche players.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

JOTUN A/S |

Jotamastic, Jotachar, Jotafloor, SeaQuantum, Jotatemp |

Market Leader |

Dominant protective & marine coatings; Yanbu, Dammam, and Jeddah production plant |

|

Akzo Nobel N.V. |

International, Interzone, Interthane, Interzinc, Interseal |

Market Leader |

Broadest product portfolio; Industrial Coatings and Protective Coatings divisions |

|

Hempel A/S |

Hempadur, Hempaprime, Hempathane, Hempasil, Hempafire |

Strong Challenger |

Marine anti-fouling leadership: Saudi Aramco approved supplier |

|

Sherwin-Williams Company |

Macropoxy, Dura-Plate, FIRETEX, Acrolon, Zinc Clad |

Strong Challenger |

OEM and automotive refinish coatings |

|

PPG Industries Inc. |

Amercoat, SigmaCover, SigmaDur, SigmaGuard, Steelguard |

Challenger |

Aerospace and automotive OEM coatings; waterborne reformulation leadership |

|

BASF Coatings |

Chemetall, baslac, Glasurit, R-M |

Challenger |

Specialty automotive OEM; eco-efficient waterborne systems |

|

Sika AG |

Sikafloor, Sikagard, Sikalastic, SikaCor, Sikadur |

Niche Player |

Concrete protective coatings and flooring systems for construction |

Local manufacturer SAUDCOLOR and Al-Jazeera Paints serve primarily the architectural and decorative segment, with limited penetration in high-performance industrial applications requiring global certification support.

Key Company Profiles

JOTUN A/S

JOTUN A/S is the market leader in Saudi Arabia's industrial and marine coatings segment, operating two production plants located in Yanbu, Dammam, and Jeddah.

- Product Portfolio: Jotafloor industrial floor coatings, Jotamastic epoxy systems, SeaQuantum anti-fouling for marine, Jotatemp heat-resistant coatings for petrochemical applications.

- Recent Developments: IKTVA compliance through local manufacturing expansion.

- Strategic Focus: Marine and offshore protective coating leadership; digital color management platform deployment.

Akzo Nobel N.V.

Akzo Nobel operates through its International and Sikkens brands in Saudi Arabia, focusing on protective, marine, and industrial coatings across the kingdom's oil & gas, construction, and infrastructure sectors.

- Product Portfolio: Interthane polyurethane topcoats, Interzinc zinc-rich primers, Interline pipeline coatings.

- Recent Developments: Launched low-VOC Intergard primers meeting Green Building Code requirements.

- Strategic Focus: Project specification selling into giga-projects; sustainable low-VOC product line expansion; talent localization under Vision 2030 Nitaqat program.

Hempel A/S

Hempel is a global coating specialist with strong Saudi market positioning in marine anti-fouling and protective coatings. The Danish company is an approved supplier to Saudi Aramco for offshore platform maintenance and holds supply agreements with major shipping lines operating through Saudi ports.

- Product Portfolio: Hempadur Mastic 45880 epoxy coating and Hempadur multi-strength epoxy systems.

- Recent Developments: Launched bio-based epoxy coatings for Saudi infrastructure projects.

- Strategic Focus: Marine and offshore market leadership; carbon footprint reduction through bio-based formulations; expansion of Saudi service team for rapid application support.

Market Concentration Analysis

The Saudi Arabian industrial paints and coatings market exhibits moderate-to-high concentration in the high-performance industrial tier. The top five global suppliers account for approximately 55–60% of revenues in 2025, while the remaining 40–45% is distributed among regional formulators, private-label blenders, and imported products.

Consolidation pressure is building. Local formulators serving the residential and light industrial segment face margin compression from global players adopting more competitive pricing in pursuit of IKTVA compliance and market share.

Between 2020 and 2025, at least three Saudi regional coating distributors were acquired by or entered distribution agreements with international coating manufacturers seeking to consolidate their in-kingdom supply chains. PE interest in mid-tier coating distributors remains elevated, targeting companies with established project specification relationships and Aramco-approved supplier status.

Investment & Growth Opportunities

Fastest Growing Segments

Water-based coatings represent the single highest-growth investment vector through 2034, expanding at a CAGR of 4.51% and gaining structural market share from 45.4% in 2025 toward an estimated 50–53% by 2034. This outperformance versus the overall market CAGR of 4.28% reflects a structural shift driven by SASO’s progressive alignment with EU REACH VOC emission limits and Saudi Arabia’s Green Building Code (effective 2025), which mandates low-VOC interior coatings in all new commercial and government buildings. Formulators with established water-based epoxy and polyurethane product lines are best positioned to capture this regulatory-driven demand uplift.

Emerging Regional Opportunities

The Western region, currently holding 24.8% of national revenues in 2025, is positioned as the highest-growth regional market through 2034, fueled by the largest concentration of Vision 2030 giga-project construction activity. NEOM’s multiple phases (THE LINE, Sindalah, Oxagon), the Red Sea Project’s resort and hospitality infrastructure, Diriyah Gate’s heritage development, and the ongoing Jeddah Islamic Port expansion collectively represent a multi-decade pipeline of structural steel, marine, and protective coating procurement.

Venture and Institutional Investment Trends

- The In-Kingdom Total Value Add (IKTVA) program creates strong structural incentives for international coating manufacturers to establish local blending or full production operations, providing preferential procurement status in Aramco and SABIC supply chains, tariff advantages, and eligibility for government-linked project specifications.

- Private equity interest in Saudi coating distributors with Aramco-approved supplier status and established project specification relationships remains elevated. Consolidation is expected to continue as global players compete to build scale, reduce distribution costs, and deepen their IKTVA compliance ratios ahead of mandatory procurement thresholds.

- Key investment themes identified through the forecast period include: water-based and low-VOC coating formulation capacity expansion (compliance-driven demand); smart coating R&D partnerships with Saudi Aramco Technology Company (SATCO); localized blending facilities qualifying for IKTVA preferential procurement; and digital distribution infrastructure targeting the estimated 12–15% of coating sales volume transacted through digital channels by 2025.

Future Market Outlook (2026-2034)

The Saudi Arabia industrial paints & coatings market is positioned for sustained, broad-based growth through 2034. From a base of USD 880.70 Million in 2025, the market is projected to reach USD 1,284.74 Million by 2034, representing total incremental value creation of approximately USD 404.0 Million over the forecast decade at a CAGR of 4.28%.

Regulatory evolution will be a defining force across the forecast period. Saudi Arabia’s Green Building Code (effective 2025) mandating low-VOC coatings, SASO’s progressive alignment with EU REACH VOC emission standards, and the intensifying sustainability procurement requirements embedded in Aramco and SABIC vendor qualification frameworks will together drive an accelerated transition toward water-based, low-emission, and high-durability smart coating technologies.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 120 industry participants in 2024–2025, including coating manufacturers, distributors, industrial project procurement managers, and end-user facilities engineers across the Eastern, Western, and Central regions of Saudi Arabia.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, SASO regulatory publications, Vision 2030 project documentation, ARAMCO and SABIC procurement guidelines, and industry databases, including Euromonitor and Chemical Week. Over 200 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations were derived using bottom-up and top-down approaches, incorporating GDP growth, industrial sector capex trends, construction activity indices, and historical coating consumption data. A base-case CAGR of 4.28% reflects consensus estimates validated against regional project pipeline data.

Saudi Arabia Industrial Paints & Coatings Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Water-Based, Solvent-Based |

| Types Covered | Automotive and Refinish Coating, Protective Coating, Powder Coating, General Industrial Coating, Others |

| Applications Covered | OEM and Special Purpose, Architectural, Others |

| End Users Covered | Automotive, Marine, General Industries, Others |

| Companies Covered | JOTUN A/S, Akzo Nobel N.V., Hempel A/S, Sherwin-Williams Company, PPG Industries Inc., BASF Coatings, Sika AG, etc. |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia industrial paints & coatings market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia industrial paints & coatings market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia industrial paints & coatings industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Industrial Paints & Coatings Market Report

The market reached USD 880.70 Million in 2025 and is projected to reach USD 1,284.74 Million by 2034, growing at a CAGR of 4.28% during 2026-2034.

Solvent-based coatings dominate with a 54.6% share in 2025, favored for their superior corrosion resistance and performance in high-temperature and chemically aggressive industrial environments.

The general industries segment leads with a 34.8% share in 2025, driven by the kingdom's extensive petrochemical manufacturing, water infrastructure, and power generation asset base.

The Eastern region leads with a 36.2% share in 2025, anchored by Jubail Industrial City's petrochemical complex and Saudi Aramco's upstream and downstream operations.

Key players include JOTUN A/S, Akzo Nobel N.V., Hempel A/S, Sherwin-Williams Company, PPG Industries Inc., BASF Coatings, and Sika AG.

Key drivers include Vision 2030 mega-project infrastructure investment, expanding Saudi Aramco capital expenditure, growth in automotive OEM and marine sectors, and tightening environmental standards, accelerating water-based coating adoption.

Key drivers include the growing demand for coatings in construction, automotive, and oil & gas industries, increased infrastructure development under Vision 2030, rising demand for protective and high-performance coatings, and government initiatives promoting industrial growth.

Key challenges include fluctuations in raw material prices, regulatory pressures regarding environmental standards, high competition from international brands, and the need for continuous innovation to meet market demands for sustainable and eco-friendly coatings.

High-growth investment opportunities exist in the development of environmentally friendly coatings, such as low-VOC and water-based paints, technological advancements in coating formulations, and expanding production capabilities to meet rising demand from local industries.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)