Saudi Arabia Potato Chips Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

Saudi Arabia Potato Chips Market Size, Share, Trends & Forecast (2026-2034)

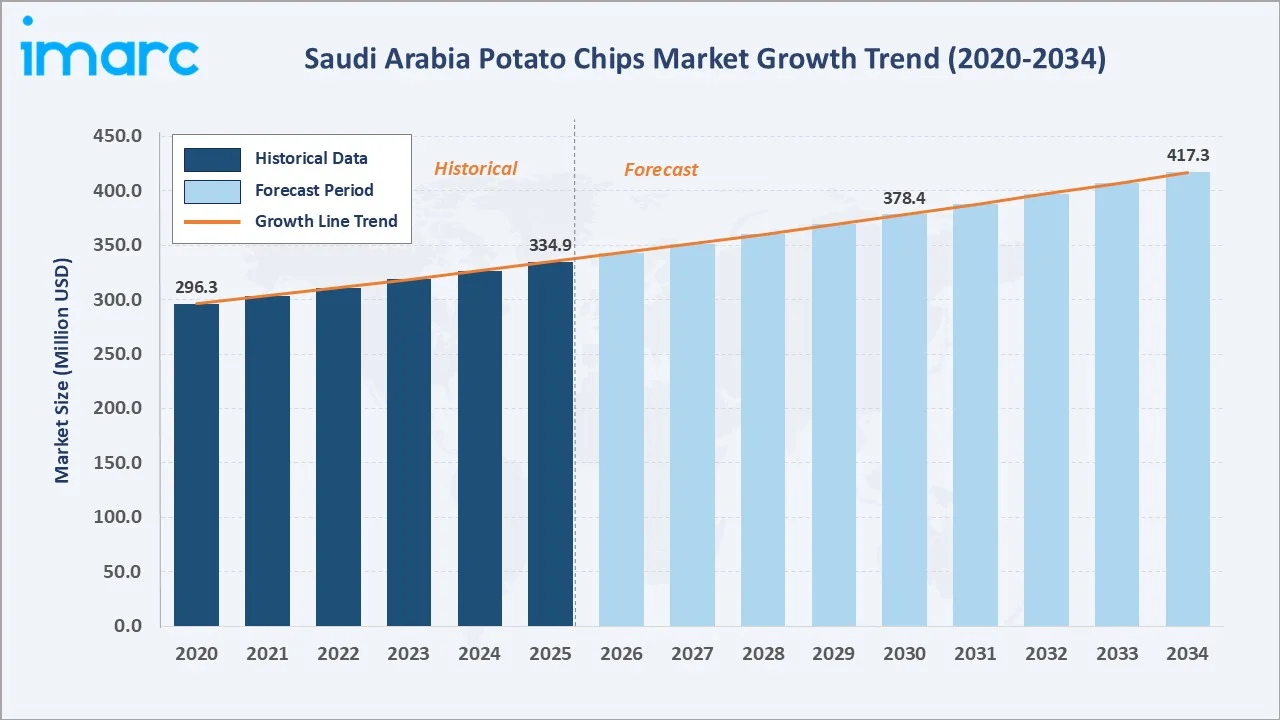

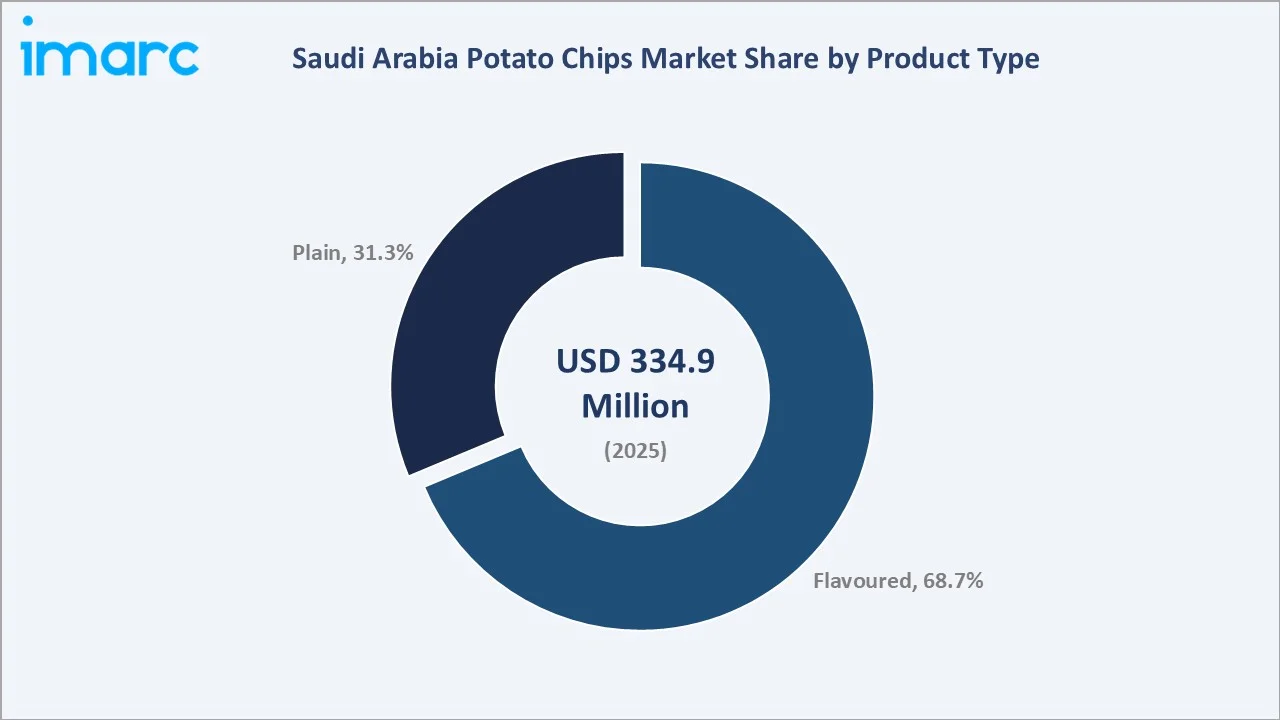

The Saudi Arabia potato chips market size reached USD 334.9 Million in 2025 and is projected to reach USD 417.3 Million by 2034, exhibiting a CAGR of 2.48% during 2026-2034. Rapid urbanisation, rising disposable incomes, and sustained demand for convenient ready-to-eat (RTE) snacks are the central growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 334.9 Million |

|

Forecast Market Size (2034) |

USD 417.3 Million |

|

CAGR (2026-2034) |

2.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

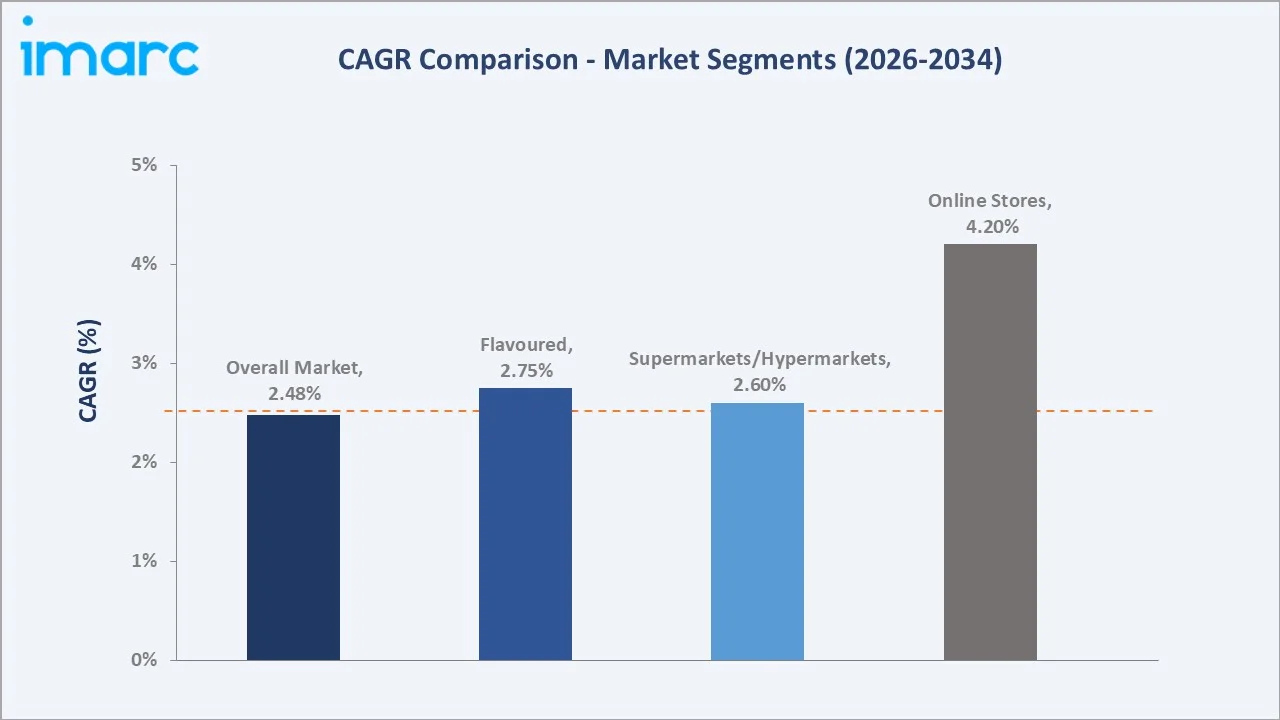

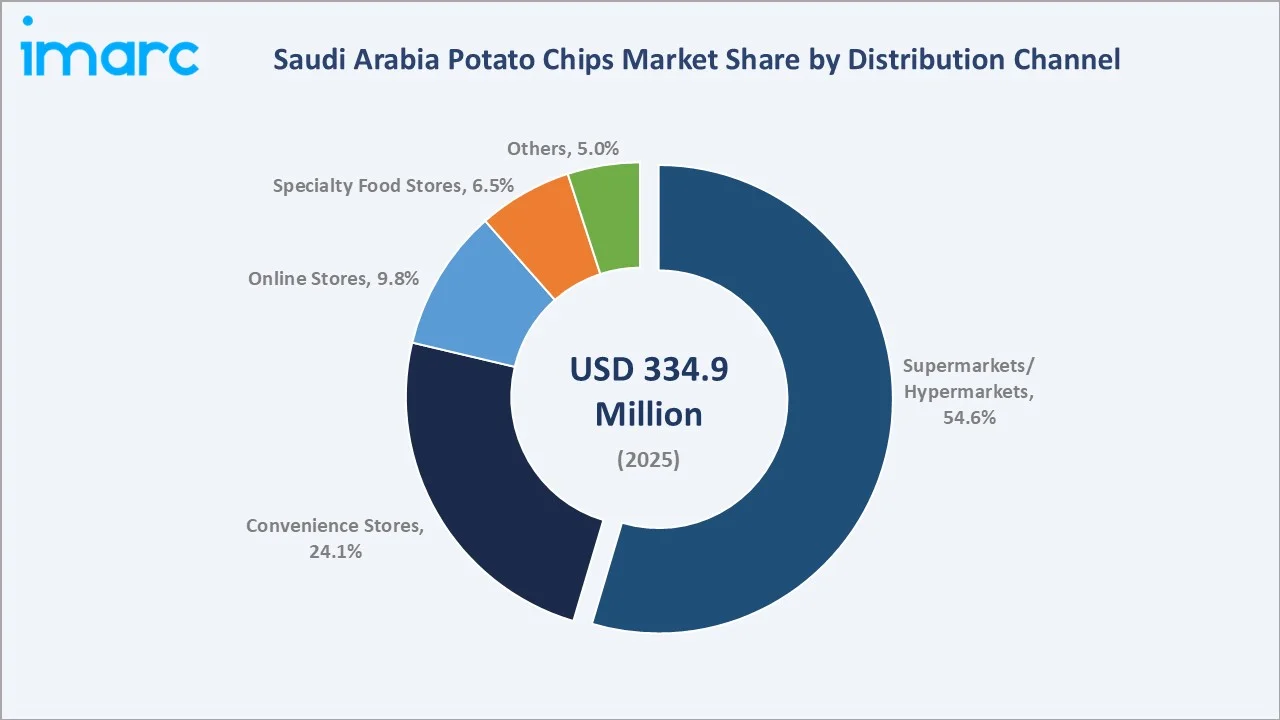

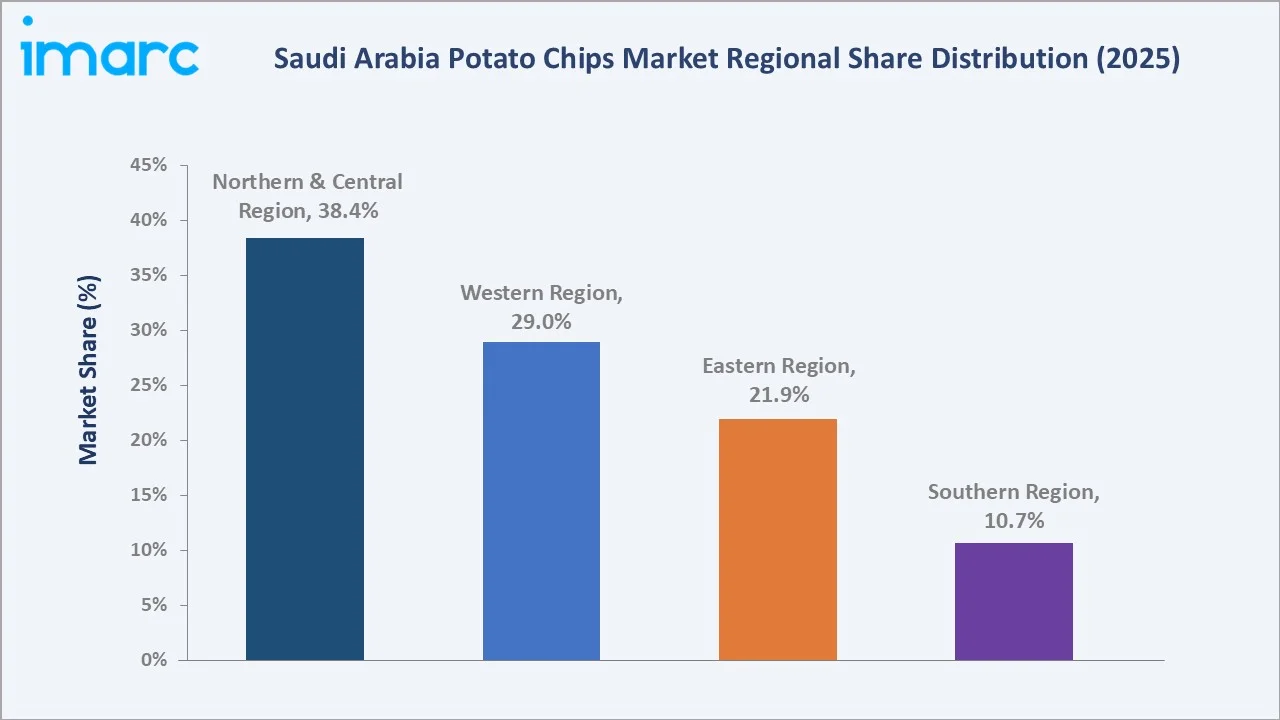

Expanding modern retail formats, a youthful demographic base where over 71% of the population is below 35 years, and surging e-commerce penetration are reshaping purchase behaviour. Flavoured chips dominate at 68.7% share (2025), supermarkets and hypermarkets lead distribution at 54.6%, and the Northern and Central Region holds 38.4% of market revenue.

To get more information on this market, Request Sample

Online stores represent the fastest-growing distribution channel at an estimated 4.20% CAGR during 2026-2034, driven by the rapid rise of digital grocery platforms, influencer-led marketing, and convenient home delivery services. Flavoured chips maintain dominant growth at ~2.75% CAGR versus plain chips at ~1.95%, underpinned by local taste preferences and continuous product innovation in regional and international seasonings.

Executive Summary

The Saudi Arabia potato chips market reached USD 334.9 Million in 2025, propelled by rising consumer preference for convenient snacking, expanding retail channels, and a young urban demographic. Saudi Arabia's food retail sales surpassed USD 51 billion in 2023, with projected annual growth exceeding 5%, reflecting strong consumer spending momentum. The market is projected to reach USD 417.3 Million by 2034 at a 2.48% CAGR, supported by ongoing retail infrastructure expansion, premiumisation trends, and increased health-oriented product launches.

Flavoured chips command 68.7% of the 2025 market, reflecting deep consumer affinity for locally inspired seasonings such as za'atar, kabsa, and chili-lime. Supermarkets and hypermarkets retain 54.6% distribution share, anchored by Saudi Arabia's expanding modern trade ecosystem, while online stores are emerging as the fastest-growing channel. The Northern and Central Region leads at 38.4% due to Riyadh's economic dominance, high population density, and concentration of modern retail formats.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Flavoured - 68.7% revenue share (2025) |

|

Second Largest Product Type |

Plain - 31.3% revenue share (2025) |

|

Dominant Distribution Channel |

Supermarkets/Hypermarkets - 54.6% share (2025) |

|

Fastest Growing Distribution Channel |

Online Stores (~4.20% CAGR, 2026-2034) |

|

Dominant Region |

Northern & Central Region - 38.4% share (2025) |

|

Top Companies |

PepsiCo, Inc. and Mars, Incorporated |

Key Analytical Observations Supporting The Above Data:

- Flavoured chips at 68.7% share (2025): Consumer preference for variety, bold tastes, and culturally inspired seasonings such as kabsa and za'atar drives flavoured chip dominance. Brands continuously launch limited-edition regional flavours tied to Ramadan and Saudi National Day events to sustain interest and trial.

- Supermarkets and hypermarkets at 54.6% (2025): Saudi Arabia's expanding modern trade network, including major chains such as Panda, Carrefour, and Al-Othaim, provides high product visibility, promotional opportunities, and cross-category impulse purchasing, solidifying their distribution leadership.

- Online stores growing at ~4.20% CAGR (2026-2034): Saudi Arabia's e-commerce food retail is expanding rapidly, fuelled by high smartphone penetration, digital-native consumers, and grocery platforms offering same-day delivery and targeted promotional campaigns.

- Northern and Central Region dominates at 38.4% (2025): Riyadh and surrounding urban hubs host the highest population density, purchasing power, and modern retail concentration, creating the most significant revenue base for snack food consumption.

- Health and wellness reshaping demand: Growing consumer awareness of nutrition, driven by Saudi Arabia's National Transformation Program initiatives promoting healthy lifestyles, is accelerating demand for baked, reduced-fat, and fortified potato chip variants.

- Localisation as a strategic growth driver: International brands are increasingly partnering with Saudi distributors to develop region-specific flavour profiles, packaging sizes catering to family consumption occasions, and Ramadan-themed marketing campaigns.

Saudi Arabia Potato Chips Market Overview

The Saudi Arabia potato chips market encompasses all forms of potato-based crisp and chip products sold through retail and food service channels within the Kingdom. The market spans plain salted, flavoured, and specialty variants distributed via modern trade, convenience retail, specialty stores, and growing online platforms. Saudi Arabia's Food and Drug Authority (SFDA) governs food product safety, registration, and labelling standards for all imported and locally manufactured snack products.

The ecosystem is import-led at the premium end, with international brands such as Lay's and Pringles manufactured locally and internationally and distributed through established networks. Macro influences include Vision 2030's economic diversification, a youthful population with high snacking propensity, Saudi Arabia's GDP growth in non-oil sectors, and expanding female workforce participation increasing household snack expenditure. The market is structurally supported by Saudi Arabia's USD 51 billion-plus food retail sector (2023) and sustained urbanisation across major cities.

Market Dynamics

To evaluate market opportunities, Request Sample

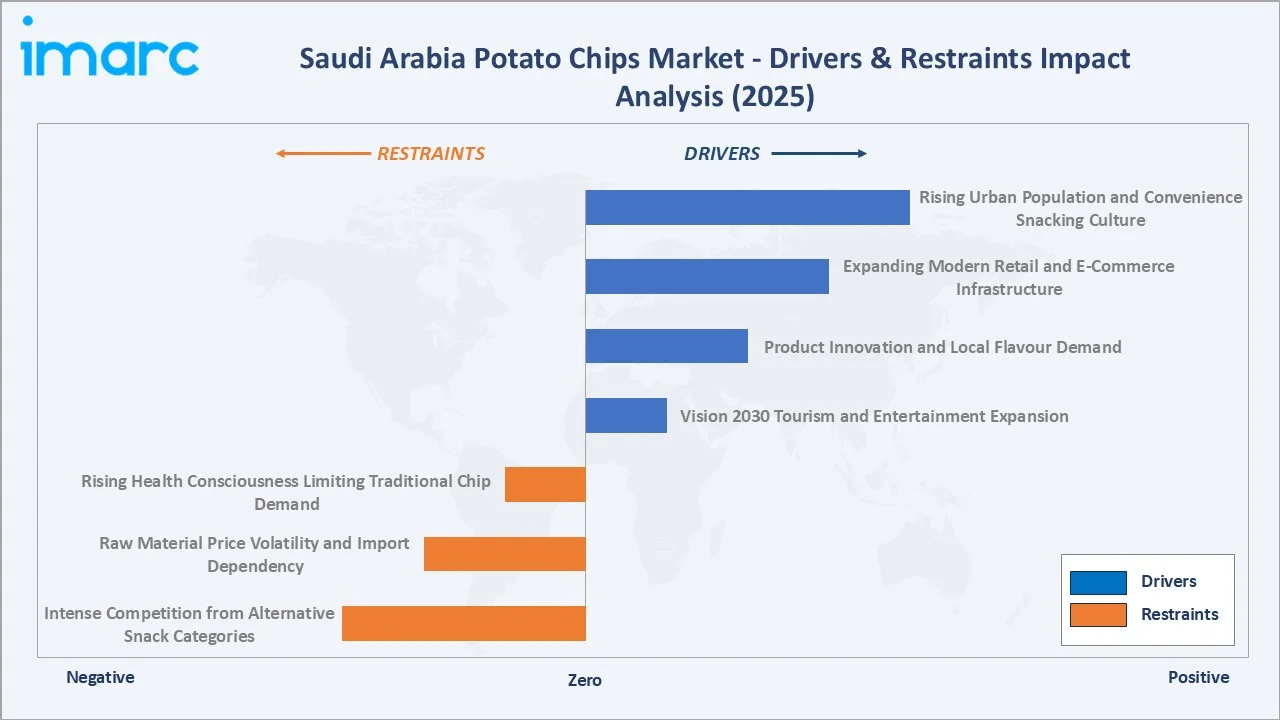

Market Drivers

- Rising Urban Population and Convenience Snacking Culture: Saudi Arabia's rapid urbanisation, with over 85% of the population residing in urban areas, drives demand for on-the-go, convenient snack options. Busy urban lifestyles and dual-income households increase reliance on packaged snacks as between-meal consumption occasions.

- Expanding Modern Retail and E-Commerce Infrastructure: Saudi Arabia's food retail sales exceeded USD 51 billion in 2023, driven by rapid expansion of hypermarkets, supermarkets, and convenience chains across Tier-1 and Tier-2 cities. Online grocery platforms such as Noon, HungerStation, and Carrefour's digital arm are creating new volume drivers through digital promotions and home delivery.

- Product Innovation and Local Flavour Demand: Consumer appetite for novel, culturally relevant flavours drives continuous new product development. Brands are launching chips seasoned with traditional Arabic spices including za'atar, kabsa, sumac, and chili-lime to align with national taste preferences.

- Vision 2030 Tourism and Entertainment Expansion: Saudi Arabia's Vision 2030 targets 150 million tourists annually, with mega-entertainment projects such as Qiddiya City, Red Sea Global resorts, and NEOM generating new snack consumption occasions in hospitality and food service settings. PepsiCo, Inc.'s 10-year partnership as exclusive snack partner for Six Flags exemplifies how entertainment expansion is directly tied to snack brand visibility.

Market Restraints

- Rising Health Consciousness Limiting Traditional Chip Demand: Increasing awareness of obesity, diabetes, and cardiovascular risk is prompting Saudi consumers to reduce high-fat, high-sodium snack consumption. Approximately 60% of GCC consumers are becoming more mindful of their snacking habits, per industry surveys, creating headwinds for conventional potato chips in the health-conscious premium segment.

- Raw Material Price Volatility and Import Dependency: Potatoes, vegetable oils, and flavouring ingredients are subject to global commodity price fluctuations affecting production costs. Saudi Arabia's reliance on imported raw materials and finished goods exposes manufacturers and distributors to foreign currency fluctuations and international freight cost volatility, compressing margins in periods of commodity cycle stress.

- Intense Competition from Alternative Snack Categories: Nuts, popcorn, rice cakes, and health-oriented snack bars are competing with potato chips for the same snacking occasions. The alternative snacks segment is growing faster in premium positioning, and investments by international players in healthier snack portfolios create substitution risk for traditional potato chips.

Market Opportunities

- Premiumisation and Health-Oriented Variant Launches: Consumer willingness to pay a premium for baked, air-popped, reduced-sodium, organic, and fortified chip variants creates a high-margin product opportunity. Front-of-pack 'free-from' labelling - gluten-free, GMO-free - is particularly compelling for the growing health-aware segment.

- Digital Retail and D2C Channel Expansion: Saudi Arabia's digital grocery market is growing at double-digit rates, with online snack purchasing accelerating post-COVID-19. Direct-to-consumer channels and social commerce via Instagram and TikTok are emerging as cost-effective brand-building platforms targeting Saudi Arabia's digitally engaged youth population. Influencer marketing campaigns, digital loyalty programs, and personalized product recommendations are enhancing conversion rates in the online snack category.

Market Challenges

- SFDA Regulatory Compliance and Labelling Requirements: Saudi Arabia's Food and Drug Authority (SFDA) enforces strict product registration, nutritional labelling, and halal certification requirements for all snack food products. Evolving sodium and sugar content regulations impose reformulation costs on manufacturers, while the Halal certification requirement adds supply chain compliance complexity for international brands entering the Saudi market.

- Private Label Competition in Mass Retail: Major Saudi retailers including Panda and Al-Othaim are expanding private label snack product ranges offering competitive pricing versus branded offerings. Private label potato chips, positioned at 20-30% lower price points than branded equivalents, exert price pressure particularly in the value segment and may limit branded manufacturers' volume growth in mass retail channels.

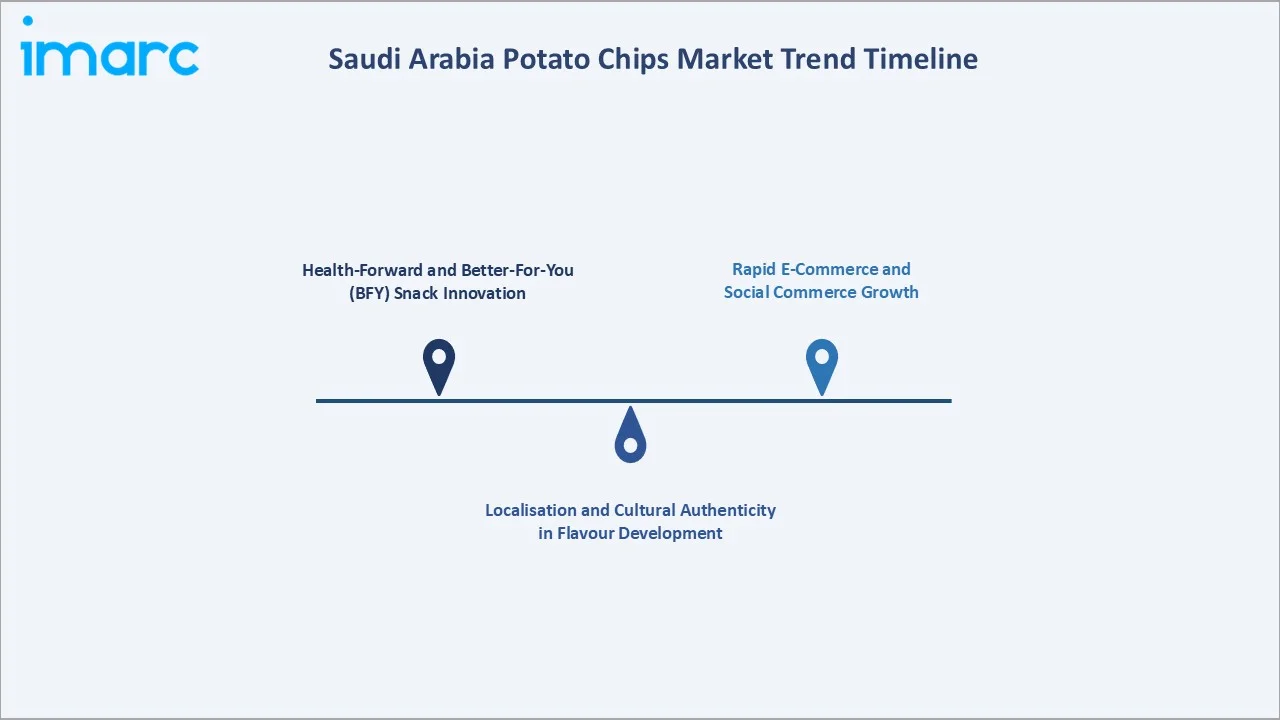

Emerging Market Trends

1. Health-Forward and Better-For-You (BFY) Snack Innovation

Saudi consumers are actively seeking snack options that balance taste enjoyment with nutritional merit. Baked potato chips, low-fat variants, and chips enriched with fiber or vitamins are growing faster than conventional full-fat products. Brands investing in clean-label formulations, natural flavours, and functional ingredient enrichment are capturing disproportionate shelf space in premium retail.

2. Localisation and Cultural Authenticity in Flavour Development

Localization has emerged as a defining competitive strategy as Saudi consumers favor products that reflect regional taste identities. Seasonal limited-edition flavours aligned with Ramadan, Saudi National Day, and FIFA events are creating trial-driving innovations that boost brand equity and repeat purchase. Local snack manufacturers leverage deep knowledge of domestic flavour preferences, creating competitive pressure for international brands to invest in local R&D.

3. Rapid E-Commerce and Social Commerce Growth

Online grocery platforms are fundamentally reshaping the potato chips purchase journey. Post-COVID-19 behavioural shifts toward digital grocery purchasing have proven durable, with Saudi e-commerce food retail expanding at high single-digit CAGR. Social media influencers and unboxing culture are amplifying snack brand discovery, with TikTok food content creating viral moments for new flavour launches among Saudi youth consumers.

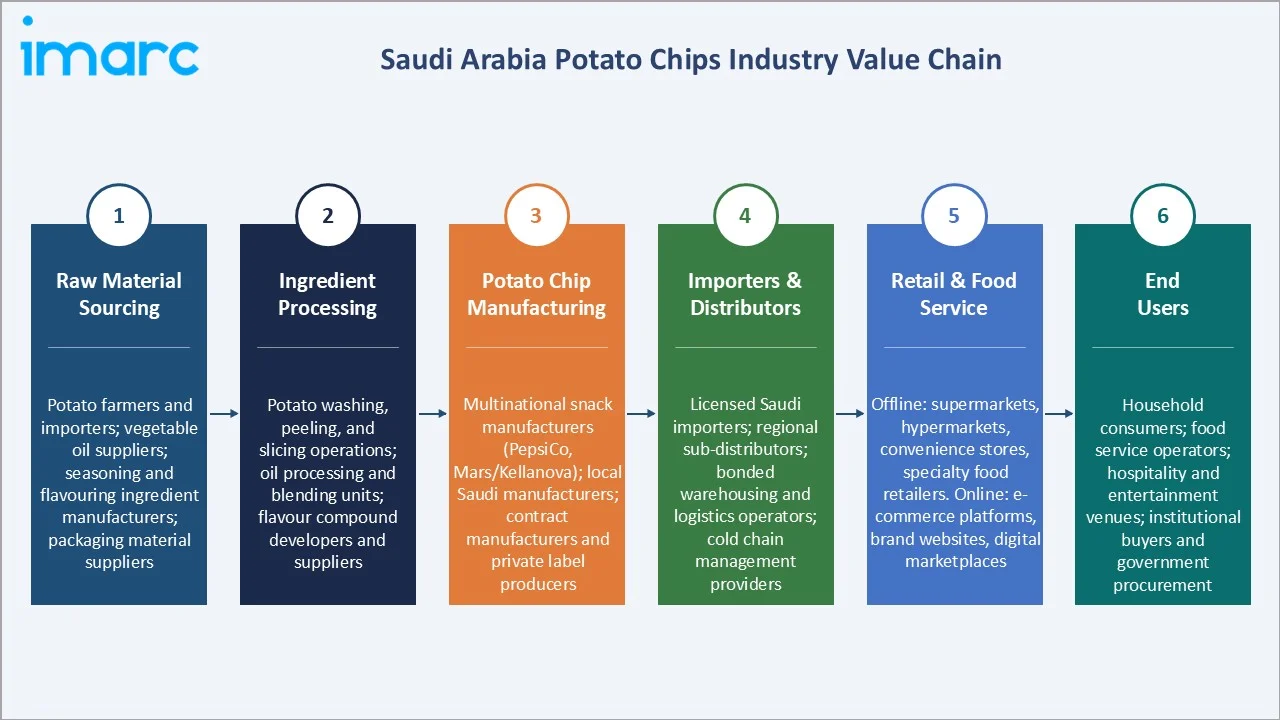

Industry Value Chain Analysis

The Saudi Arabia potato chips market value chain spans agricultural sourcing of raw potatoes and ingredients through manufacturing operations, SFDA regulatory compliance, multi-tier distribution networks, and end-consumer retail across offline and digital channels.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Potato farmers and importers; vegetable oil suppliers; seasoning and flavouring ingredient manufacturers; packaging material suppliers |

|

Ingredient Processing |

Potato washing, peeling, and slicing operations; oil processing and blending units; flavour compound developers and suppliers |

|

Potato Chip Manufacturing |

Multinational snack manufacturers; local Saudi manufacturers; contract manufacturers and private label producers |

|

Importers & Distributors |

Licensed Saudi importers; regional sub-distributors; bonded warehousing and logistics operators; cold chain management providers |

|

Retail & Food Service |

Offline: supermarkets, hypermarkets, convenience stores, specialty food retailers. Online: e-commerce platforms, brand websites, digital marketplaces |

|

End Users |

Household consumers; food service operators; hospitality and entertainment venues; institutional buyers and government procurement |

The distribution structure follows a two-tier model. International manufacturers supply licensed Saudi importers and distributors, who in turn supply modern trade retailers and sub-regional distributors. PepsiCo, Inc.'s Dammam and Riyadh manufacturing plants compress the distribution chain for Lay's brand products, enabling faster route-to-market and fresher product delivery across Saudi Arabia.

Technology Landscape in the Saudi Arabia Potato Chips Industry

Advanced Continuous Frying Technology

Modern potato chip production facilities deploy continuous frying systems with precise oil temperature control, reducing oil degradation and improving product consistency. PepsiCo, Inc.'s Dammam plant expansion incorporated state-of-the-art manufacturing lines improving energy efficiency and production throughput. Nitrogen flushing and modified atmosphere packaging technology extend shelf life without additional preservatives, supporting clean-label positioning.

Baked and Air-Popped Production Technology

Consumer demand for lower-fat alternatives is driving investment in baked chip production technology - air impingement ovens and hot-air roasting systems that reduce oil content by 50-70% versus traditional frying. Air-popped chip technology using dry heat chambers delivers ultra-low-fat products that meet evolving SFDA nutritional guidelines and align with Saudi Arabia's health promotion agenda.

Digital Supply Chain and Demand Planning

AI-driven demand forecasting tools are being deployed by leading FMCG players in Saudi Arabia to optimize inventory levels across the snack category. Real-time point-of-sale data integration from hypermarket partners enables dynamic promotional planning and shelf replenishment optimization.

Sustainable Packaging Technology

Recyclable mono-material flexible packaging, bio-based film laminates, and reduced-weight packaging structures are being piloted by major snack brands in Saudi Arabia. PepsiCo, Inc. introduced rPET bottles and collaborated with SABIC on recyclable packaging solutions in the Saudi market in 2023. Digitally printed packaging enabling rapid flavour variant introduction and limited-edition design launches is improving brand responsiveness to cultural and seasonal marketing moments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Flavoured |

68.7% |

2025 |

|

Distribution Channel |

Supermarkets/Hypermarkets |

54.6% |

2025 |

|

Region |

Northern and Central Region |

38.4% |

2025 |

By Product Type

Flavoured chips dominate at 68.7% market share (2025), driven by Saudi consumer preference for bold, complex taste profiles and the success of localised seasoning innovations. International brands and local manufacturers compete vigorously in the flavoured segment through continuous new product launches, seasonal limited editions, and culturally inspired seasoning strategies.

To access detailed market analysis, Request Sample

Plain chips represent 31.3% of the 2025 market, maintaining steady demand as a classic, versatile snack option favoured for on-the-go consumption and pairing with dips and condiments. The plain segment is supported by household purchasing occasions and remains a gateway category for price-sensitive consumers.

By Distribution Channel

Supermarkets/hypermarkets lead at 54.6% market share (2025), anchored by Saudi Arabia's expanding modern trade ecosystem and consumer preference for consolidated grocery shopping. Major retail chains including Panda Retail, Carrefour, Al-Othaim, and LuLu Hypermarket provide extensive shelf space, promotional visibility, and cross-category impulse purchase opportunities for potato chip brands.

Convenience stores hold 24.1% share (2025), driven by on-the-go snacking occasions, petrol station retail formats, and proximity to residential areas, particularly in tier-1 cities. Online stores represent 9.8% of distribution (2025) and are the fastest-growing channel at approximately 4.20% CAGR, fuelled by Saudi Arabia's young digital consumer base and expanding grocery e-commerce ecosystem.

Regional Market Insights

The Northern and Central Region's 38.4% dominance reflects Riyadh's status as Saudi Arabia's economic and administrative capital, home to the largest concentration of modern retail formats, highest per-capita snack expenditure, and the greatest density of young, urban consumers driving snack category growth.

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Northern & Central Region |

38.4% |

Riyadh's dominance as Saudi Arabia's economic capital; highest vehicle registration and household consumption density; major modern retail concentration including flagship hypermarkets and convenience chains |

|

Western Region |

29.0% |

Jeddah's commercial activity and Red Sea port logistics infrastructure; Makkah and Madinah's year-round pilgrimage tourism creating sustained food service snack demand |

|

Eastern Region |

21.9% |

Dammam and Al-Khobar's industrial and petrochemical sector concentration; expatriate workforce population driving diverse snack brand demand; proximity to PepsiCo, Inc.'s Dammam manufacturing plant supporting efficient distribution |

|

Southern Region |

10.7% |

Emerging infrastructure development under Vision 2030's regional connectivity programs; growing domestic tourism toward Asir highlands and Jizan; gradual modern retail expansion |

The Western Region's 29.0% share is reinforced by Jeddah's role as Saudi Arabia's largest commercial port, supporting efficient product import and distribution, alongside sustained snacking demand from the Hajj and Umrah pilgrimage food service ecosystem.

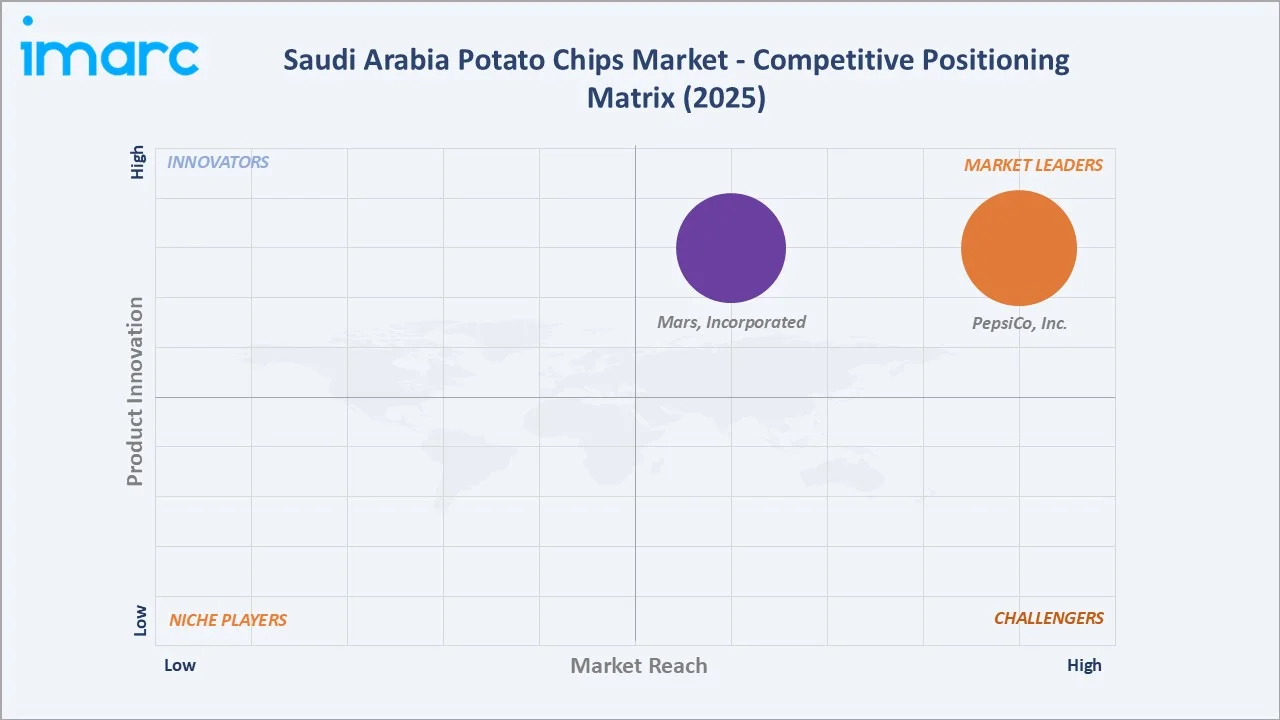

Competitive Landscape

Saudi Arabia's potato chips market is moderately concentrated, with PepsiCo, Inc.'s Lay's brand holding dominant market leadership through local manufacturing, deep distribution, and strong brand equity. Mars, Incorporated's Pringles holds the second-strongest branded position, commanding the premium stackable chip segment.

|

Company Name |

Brands/Products |

Market Position |

Core Strength |

|

PepsiCo, Inc. |

Lay's, Cheetos, Doritos |

Market Leader |

Established local manufacturing presence; long-standing market heritage; substantial sustained capital investment in regional production and distribution infrastructure |

|

Mars, Incorporated |

Pringles |

Market Leader |

Premium stackable chip positioning with strong global brand equity; large-scale strategic acquisition expanding snacking portfolio breadth; extensive international market distribution network |

The competitive landscape is bifurcated: the branded premium segment is dominated by PepsiCo, Inc. and Mars, Incorporated through established distribution, large-scale marketing, and continuous flavour innovation, while the value and mid-tier segments see active competition from local manufacturers and regional private label products at 20-30% lower price points.

Key Company Profiles

PepsiCo, Inc.

PepsiCo, Inc. is the undisputed market leader in Saudi Arabia's potato chips and salty snacks category, operating local manufacturing facilities in Riyadh and Dammam.

- Product Portfolio: Lay's (flavoured, plain, baked variants), Cheetos, Doritos, Ruffles.

- Recent Developments: In April 2025, PepsiCo, Inc. announced the inaugurated a new regional headquarters and an USD 8 million R&D center in Riyadh, its largest innovation facility in the Gulf, to develop products tailored to regional preferences.

- Strategic Focus: Localised manufacturing for fresher product delivery; sustainability integration through solar panel installation at Riyadh and Dammam facilities; Saudi youth workforce development aligned with Vision 2030.

Mars, Incorporated

Mars, Incorporated has made Pringles a core brand within Mars Snacking's global portfolio alongside Snickers, Twix, and M&M's. Pringles holds strong market recognition in Saudi Arabia's premium stackable chip segment, leveraging distinctive packaging and broad flavour variety.

- Product Portfolio: Pringles Original, Sour Cream & Onion, BBQ, Smoky Bacon, Paprika, and seasonal limited editions.

- Strategic Focus: Leveraging combined Mars and Kellanova distribution scale; Pringles flavour innovation pipeline aligned with global and regional taste preferences; maintaining premium brand positioning in GCC snack markets.

Market Concentration Analysis

Saudi Arabia's potato chips market exhibits moderate-to-high concentration at the branded value level. PepsiCo, Inc,, through its Lay's brand and local manufacturing capability, commands an estimated 40-50% of branded potato chip market value (2025). Mars, Incorporated contributes an estimated 15-20% in the premium segment. The top two branded players collectively hold approximately 55-70% of market value.

Below the top-tier branded players, the market fragments significantly across local Saudi manufacturers, regional snack producers, and imported specialty brands. Local brands offer competitive pricing at 20-35% below international equivalents, capturing cost-sensitive consumer segments. Private label products from major retailers are growing but remain below 10% of total market share.

Investment & Growth Opportunities

Fastest Growing Segments

Online stores (~4.20% CAGR), premium and artisanal chip formats, health-oriented 'better-for-you' variants (baked, reduced-fat, organic), and localised limited-edition flavour lines represent Saudi Arabia's highest-growth investment vectors through 2034. Health-forward product lines represent the highest revenue-per-unit opportunity, targeting premium consumer spending in a market where affordability barriers are lower than most emerging markets.

Emerging Market Opportunities

- Digital grocery investment: Saudi Arabia's e-commerce food retail is expanding at high single-digit growth, creating first-mover advantage for snack brands investing in digital shelf space, influencer partnerships, and subscription grocery programs.

- Healthier snack portfolio development: Launch of baked, air-popped, and functional ingredient-enriched potato chips aligned with Saudi Arabia's health promotion agenda and SFDA nutritional labelling requirements.

Investment Themes

- Local flavour R&D investment: Developing proprietary Saudi and GCC-specific seasoning platforms creates defensible flavour-led competitive advantages that international players find difficult to replicate quickly.

- Sustainability differentiation: Early investment in recyclable mono-material packaging and sustainable sourcing credentials creates regulatory readiness and consumer brand equity aligned with Vision 2030's environmental targets.

- Social commerce marketing: Allocating marketing budgets toward Saudi TikTok, Instagram, and Snapchat channels drives product discovery among the 15-30 year demographic cohort, the core snack consumption driver.

Future Market Outlook (2026-2034)

The Saudi Arabia potato chips market is projected to grow from USD 334.9 Million in 2025 to USD 417.3 Million by 2034, at a 2.48% CAGR, reflecting steady structural growth in one of the GCC's most dynamic consumer markets. The 2030 milestone market size of USD 378.4 Million will be shaped by Vision 2030's economic diversification, expanding modern retail infrastructure, and sustained young consumer demographic driving volume growth.

Health and wellness trends will progressively reshape the product mix. By 2030, better-for-you chip variants are expected to represent a meaningfully larger share of total potato chip revenue, as SFDA labelling requirements, Saudi health promotion programs, and consumer preference evolution collectively incentivize manufacturers to broaden their low-fat and functional snack portfolios. Brands that invest ahead of this structural shift - building health-oriented product credibility while maintaining flavour leadership - will capture disproportionate market share by 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 60+ industry stakeholders (2025), including Saudi FMCG distributors and importers, modern trade category managers from major retail chains, brand managers from key snack companies, SFDA regulatory specialists, and Saudi e-commerce platform snack category managers. Stakeholder inputs validated market sizing, segment share estimates, and emerging trend assessments.

Secondary Research

Secondary research encompassed SFDA product registration databases, Saudi General Authority for Statistics (GaStat) household expenditure surveys, U.S. Department of Agriculture Foreign Agricultural Service Saudi Arabia food retail reports, Saudi Vision 2030 economic reports, company annual reports and press releases for key players, and over 100 secondary sources covering the Saudi FMCG, retail, and snack food landscape.

Forecasting Models

Market value forecasts were developed using bottom-up per-capita snack expenditure models combined with top-down market sizing validation against import trade data and retail sell-out estimates. Key inputs include GaStat population and urbanisation projections, Vision 2030 tourism arrival targets, SFDA regulatory impact assessments, e-commerce penetration adoption curves, and commodity price scenario modeling for raw potato and vegetable oil inputs.

Saudi Arabia Potato Chips Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Pots and Pan, Cooking Racks, Cooking Tools, Microwave Cookware, Pressure Cookers |

| Distribution Channels Covered | Hypermarkets and Supermarkets, Speciality Store, Online, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | PepsiCo Inc., Mars Incorporated, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia potato chips market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia potato chips market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia potato chips industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Potato Chips Market Report

The Saudi Arabia potato chips market reached USD 334.9 Million in 2025, driven by urbanisation, rising disposable incomes, and growing demand for convenient ready-to-eat snacks among Saudi Arabia's youthful population.

The Saudi Arabia potato chips market is projected to grow at a CAGR of 2.48% during 2026-2034, supported by retail expansion, product innovation, and e-commerce channel growth.

Flavoured chips lead at 68.7% market share (2025), reflecting Saudi consumer preference for bold, culturally inspired seasonings including za'atar, kabsa, and chili-lime flavour profiles alongside global classics.

Supermarkets and hypermarkets hold the largest share at 54.6% (2025), anchored by Saudi Arabia's expanding modern trade infrastructure and consumer preference for consolidated grocery shopping in large-format retail.

Online stores are growing fastest at approximately 4.20% CAGR (2026-2034), driven by Saudi Arabia's youthful digital consumer base, grocery e-commerce platforms, and social media-led snack product discovery.

The Northern and Central Region leads with 38.4% market share (2025), anchored by Riyadh's economic dominance, highest population density, and largest concentration of modern retail formats across Saudi Arabia.

Leading companies include PepsiCo, Inc., Mars, Incorporated, and local Saudi snack manufacturers serving regional markets.

Key drivers include Saudi Arabia's youthful urbanising population, expanding modern retail and e-commerce channels, continuous flavour innovation aligned with local tastes, rising disposable incomes, and Vision 2030's economic and tourism expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)