United States Biostimulants Market Size, Share, Trends and Forecast by Product Type, Crop Type, Form, Origin, Distribution Channel, Application, End User, and Region, 2026-2034

United States Biostimulants Market Size, Share, Trends & Forecast (2026-2034)

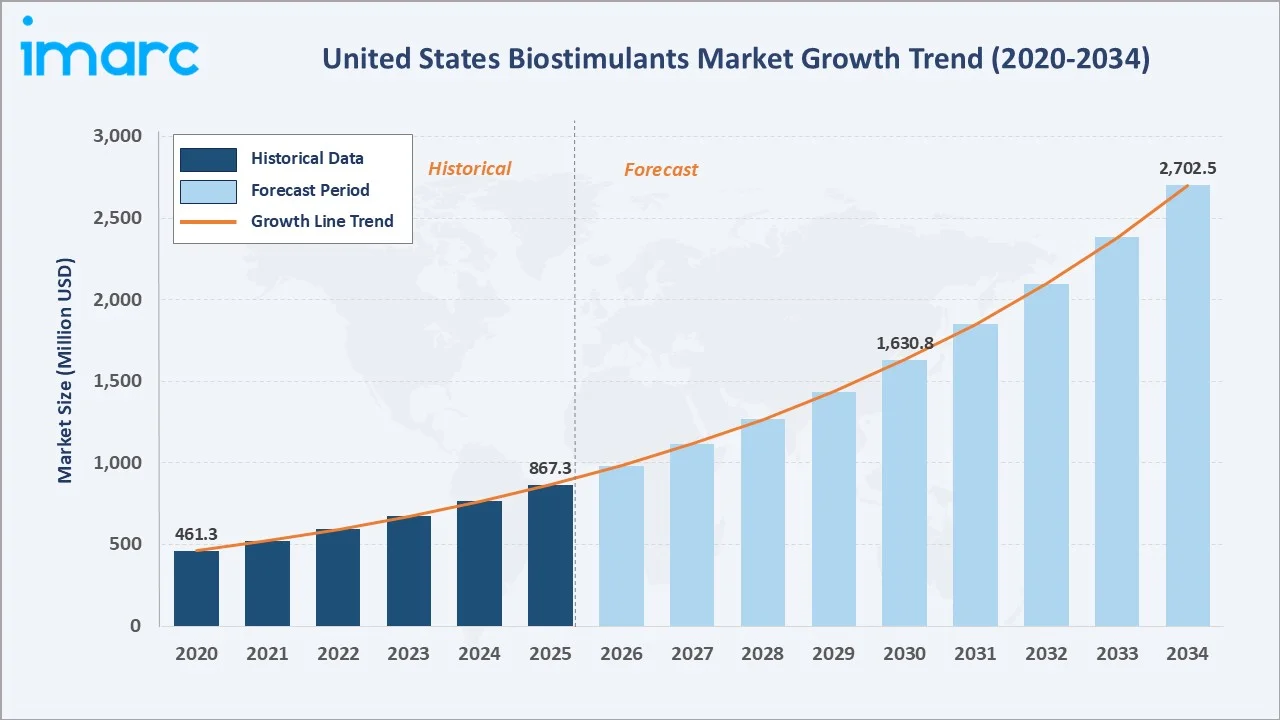

The United States biostimulants market reached USD 867.3 Million in 2025 and is projected to reach USD 2,702.5 Million by 2034, growing at a CAGR of 13.46% during 2026-2034. The market is driven by rising demand for sustainable agriculture, growing organic food preferences, regulatory support for bio-based crop inputs, and integration of precision farming tools.

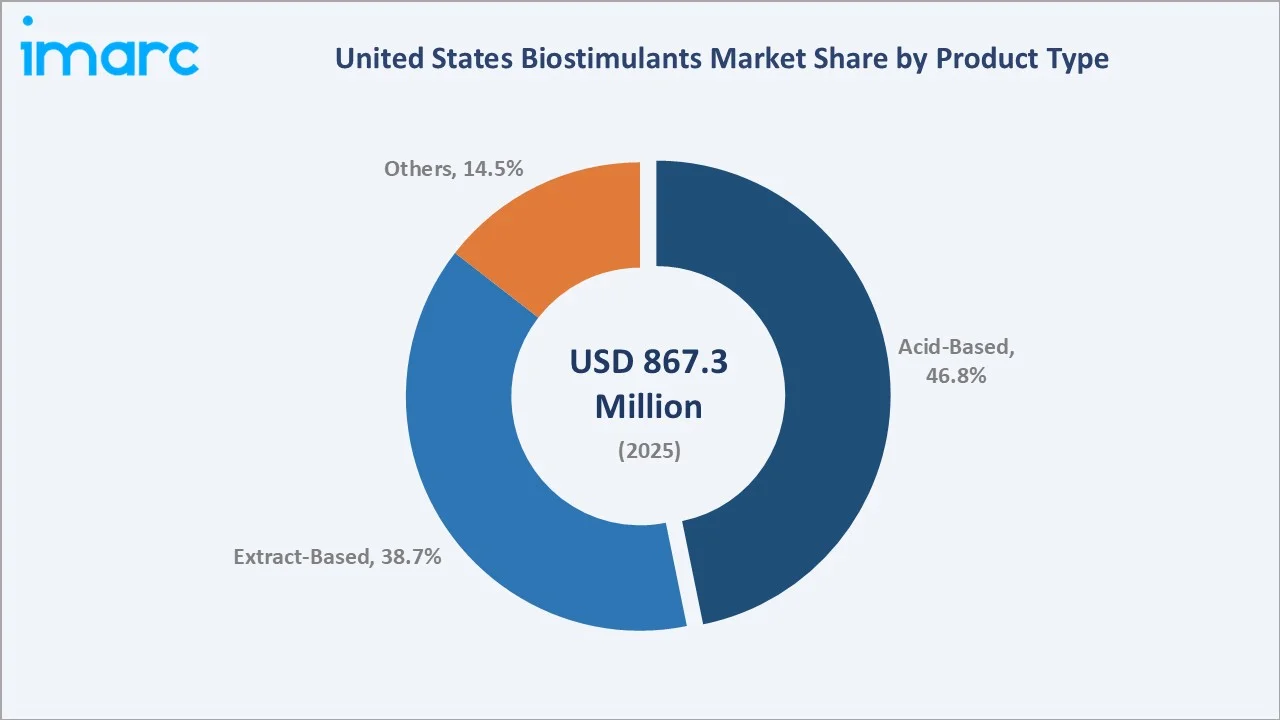

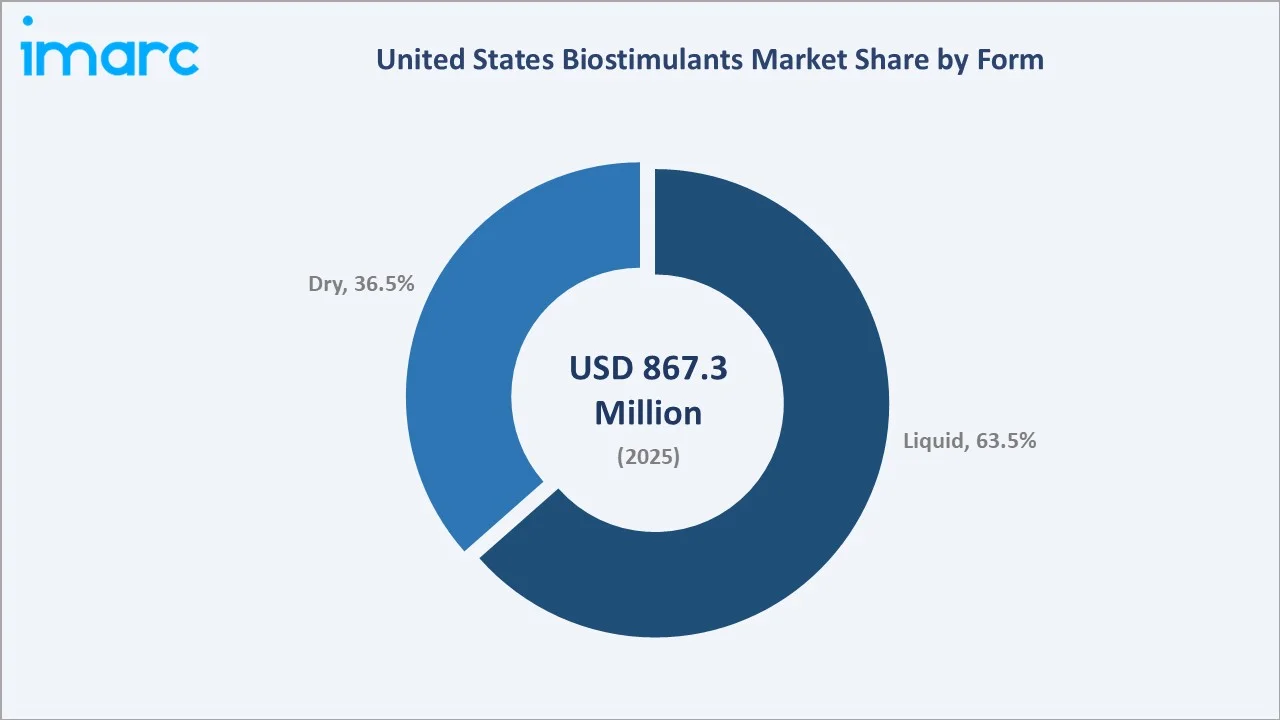

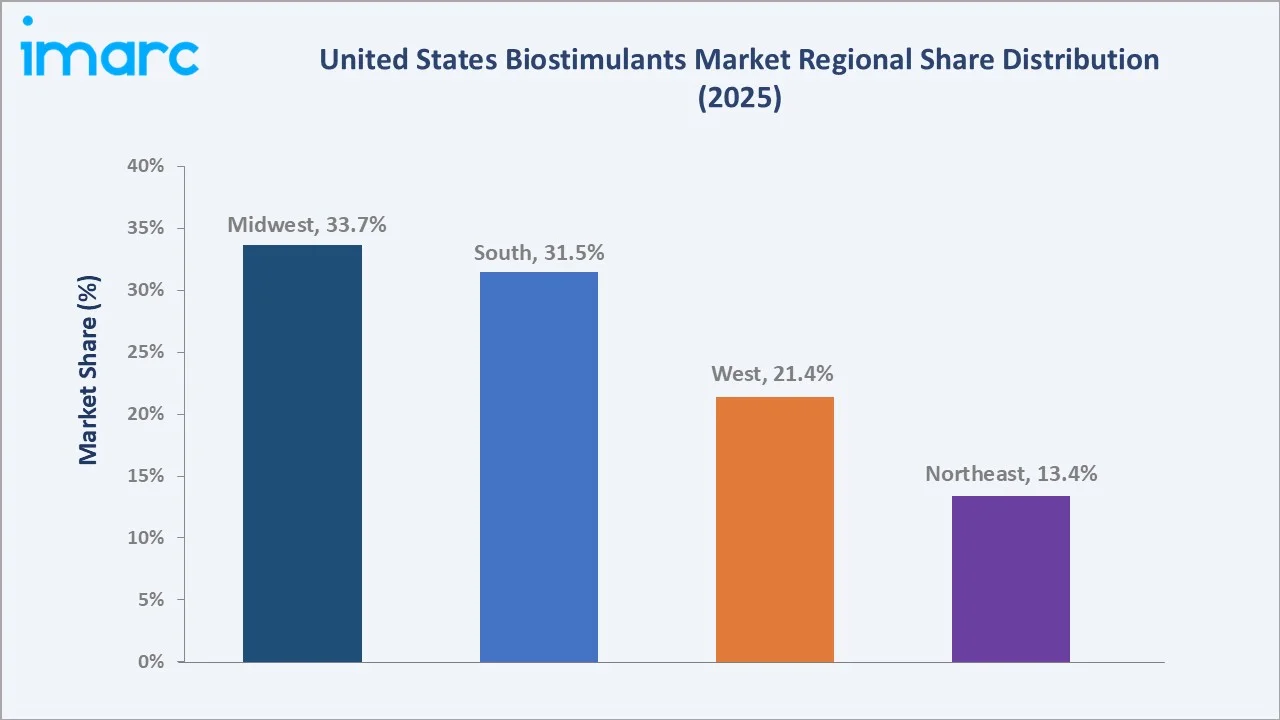

Acid-Based product types dominate at 46.8%, Liquid form leads at 63.5%, and the Midwest commands 33.7% of regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 867.3 Million |

|

Forecast Market Size (2034) |

USD 2,702.5 Million |

|

CAGR (2026-2034) |

13.46% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Acid-Based (46.8%, 2025) |

|

Dominant Form |

Liquid (63.5%, 2025) |

|

Leading Region |

Midwest (33.7%, 2025) |

The market expanded from USD 461.3 Million in 2020 to USD 867.3 Million in 2025, nearly doubling in five years, anchored at USD 1,630.8 Million in 2030 and forecast to reach USD 2,702.5 Million by 2034. Growing awareness of soil health, supportive USDA incentive programs, and rising adoption among large-scale commercial row crop growers underpinned the strong historical growth trajectory.

To get more information on this market, Request Sample

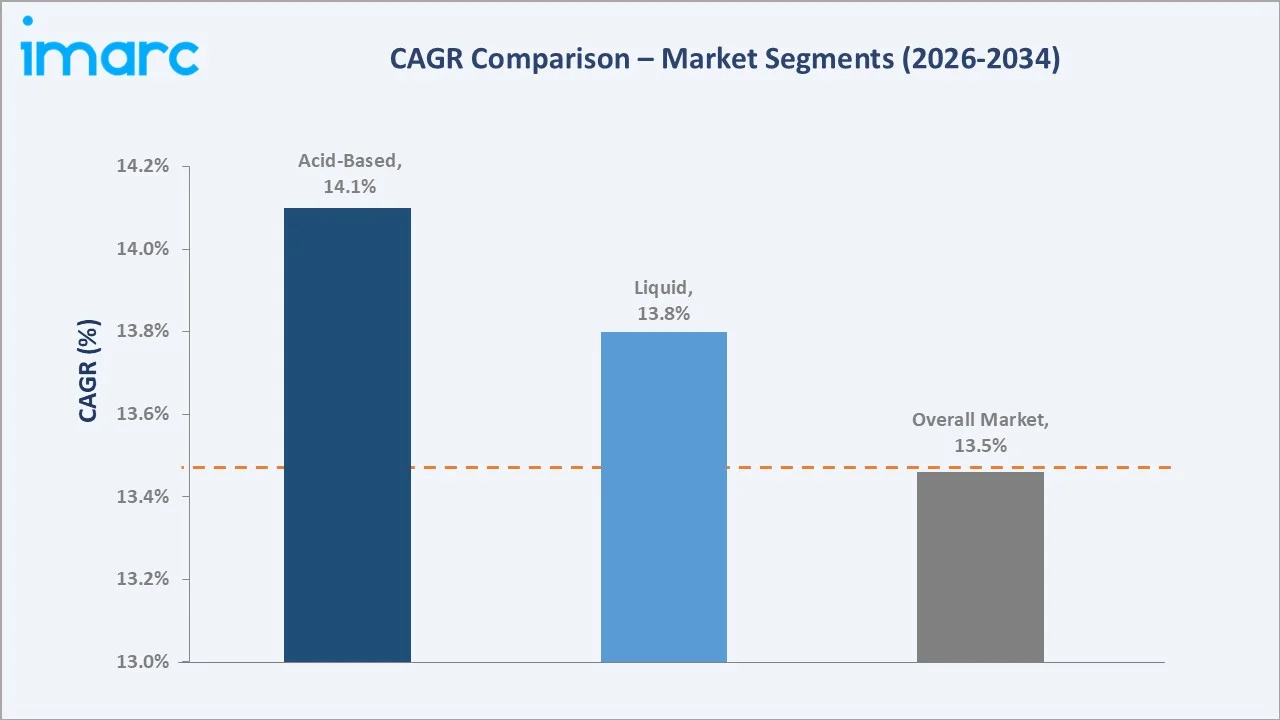

The Acid-Based segment grows at ~14.1% CAGR as humic and fulvic acid formulations gain traction across US corn belt row crops and specialty horticulture. The Liquid form grows at ~13.8% CAGR as ease of application via foliar sprays and fertigation systems accelerates adoption across both conventional and organic farming systems.

Executive Summary

The United States biostimulants market reached USD 867.3 Million in 2025, representing one of agriculture's fastest-growing specialty input categories, driven by the fundamental shift toward sustainable and regenerative farming practices across US crop systems. The market is projected to reach USD 2,702.5 Million by 2034.

Acid-Based biostimulants at 46.8% dominate by capturing humic acid, fulvic acid, and amino acid segments widely adopted in corn, soybean, wheat, and specialty vegetable production. Liquid form at 63.5% leads through compatibility with standard crop management equipment and versatility across diverse crop types. The Midwest at 33.7% commands the largest regional share through its extensive row crop acreage and established biostimulant distribution networks.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Acid-Based - 46.8% share (2025) |

|

Dominant Form |

Liquid - 63.5% market share (2025) |

|

Leading Region |

Midwest - 33.7% market share (2025) |

|

Market Opportunity |

Humic acid controlled-release formats; seaweed extract specialty crops; microbial consortia for soil carbon programs; precision agriculture-integrated biostimulant platforms |

Key Analytical Observations Supporting The Above Data:

- Acid-Based at 46.8%: Humic and fulvic acid biostimulants demonstrate proven efficacy in improving nutrient uptake and soil structure across US row crops. Their compatibility with standard fertilizer programs, cost-effectiveness, and availability in granular and liquid formats for in-furrow and fertigation application cement segment dominance. Key suppliers including BASF SE and Humic Growth Solutions maintain established distribution networks across major corn belt states.

- Liquid at 63.5%: Liquid biostimulants enable precise, uniform application via foliar sprays, fertigation systems, or seed treatment delivery, ensuring rapid bioactive compound delivery to plants. Their versatility across cereals, vegetables, fruits, and specialty crops, combined with formulation advances that enhance stability and shelf life, makes them the preferred format for commercial farming operations across the United States.

- Midwest at 33.7%: The Midwest leads through its extensive corn, soybean, and wheat acreage, where even modest per-acre yield improvements from biostimulants generate significant aggregate revenue impact for growers. The region's adoption of precision agriculture platforms, established agri-retail distribution networks, and USDA program funding for soil health improvements collectively reinforce biostimulant penetration across large commercial farm operations.

United States Biostimulants Market Overview

The United States biostimulants market encompasses the development, manufacture, and supply of all biostimulant products applied to agricultural, horticultural, and turf systems to enhance plant growth, nutrient uptake, stress tolerance, and overall crop productivity through mechanisms distinct from conventional plant nutrition inputs.

The ecosystem integrates biostimulant manufacturers, raw material suppliers including seaweed harvesters, humic substance extractors, and amino acid producers, formulators, agri-retail distributors, precision agriculture technology providers, and regulatory bodies including the EPA and USDA. Macroeconomic factors include rising organic food demand, government sustainability incentive programs, climate change-driven abiotic stress, and increasing farmer awareness of soil health and regenerative agriculture.

Market Dynamics

To evaluate market opportunities, Request Sample

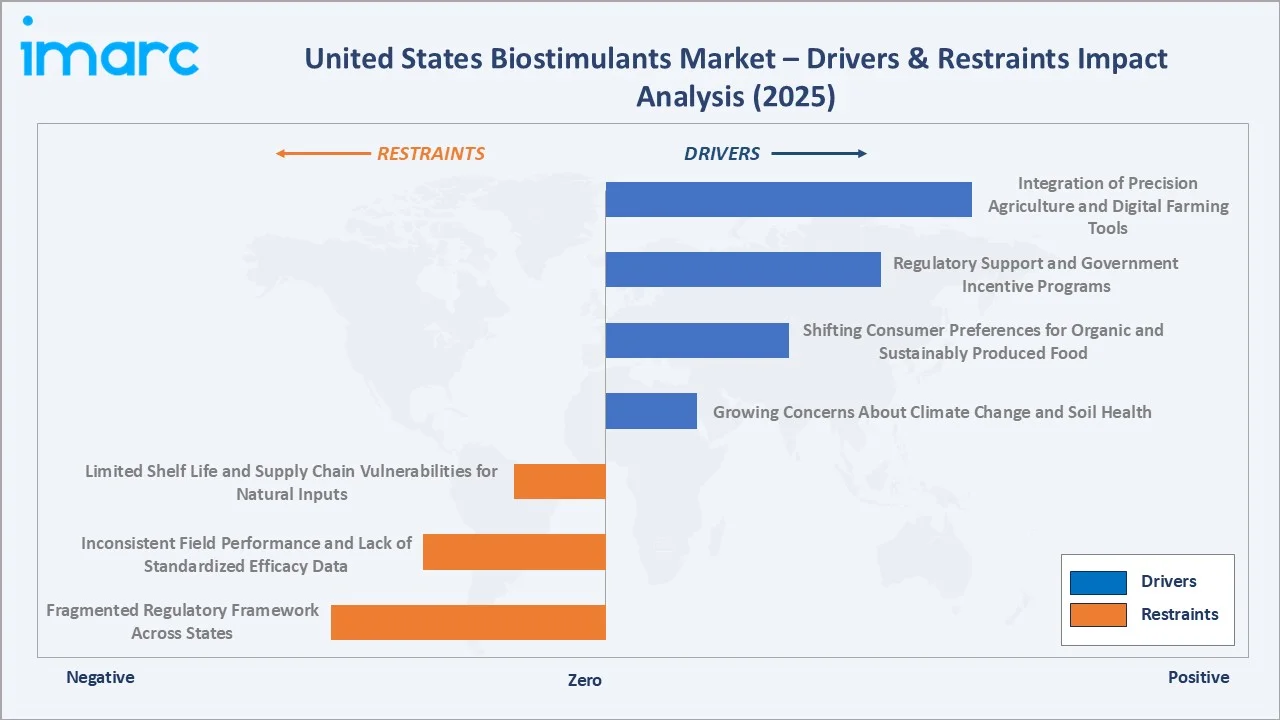

Market Drivers

- Growing Concerns About Climate Change and Soil Health: Rising incidence of drought, heat stress, and soil degradation is compelling US farmers to adopt biostimulants as crop resilience tools. Biostimulants enhance root development, nutrient absorption, and physiological stress resistance, making them essential components of climate-adaptive crop management. Over 5.6 million acres of certified organic farmland in the US creates a structurally growing captive biostimulant demand pool insulated from synthetic input competition.

- Shifting Consumer Preferences for Organic and Sustainably Produced Food: US organic food demand is increasing, outpacing total grocery growth and creating pull-through demand for certified bio-based crop inputs. Retailers increasingly require full input transparency, prompting growers to adopt biostimulants that enhance yield while maintaining strong environmental and sustainability credentials.

- Regulatory Support and Government Incentive Programs: The USDA Environmental Quality Incentives Program reimburses up to 75% of costs for biological amendments that improve soil organic matter. California's Healthy Soils Program disbursed USD 75 million to encourage humic and fulvic acid use on specialty crops. The Plant Biostimulant Act and the EPA's expanding biostimulant definition framework provide regulatory clarity that reduces market entry costs and accelerates commercial product registrations.

- Integration of Precision Agriculture and Digital Farming Tools: Biostimulant products are increasingly developed and applied alongside data-driven agronomy, soil analytics, and variable-rate application technologies, enabling growers to achieve more consistent performance and higher return on investment. Biostimulant manufacturers, agritech platforms, and input distributors are forming strategic partnerships creating new go-to-market models for farmer outreach and product differentiation across diverse US crop systems.

Market Restraints

- Fragmented Regulatory Framework Across States: Inconsistent federal and state-level definitions of biostimulant products create complex multi-state compliance pathways that increase product launch costs for manufacturers. The absence of a unified national biostimulant regulatory framework limits the speed at which new products can achieve market-wide commercial deployment, constraining supply-side growth velocity despite strong underlying demand signals across multiple crop segments.

- Inconsistent Field Performance and Lack of Standardized Efficacy Data: Variability in biostimulant performance across different soil types, climate conditions, crop varieties, and application timings creates farmer hesitation in adopting these products at commercial scale. Unlike synthetic fertilizers with predictable response curves, biostimulant field outcomes can vary significantly, making large-scale commercial farmer adoption contingent on localized, crop-specific, and scientifically validated performance data and demonstration trials.

- Limited Shelf Life and Supply Chain Vulnerabilities for Natural Inputs: Biostimulants derived from biological sources, particularly microbial consortia and seaweed extracts, have inherent shelf-life limitations and require cold-chain management that increases distribution costs and logistics complexity. West Coast kelp harvest quotas are raising raw material costs and pushing seaweed extract manufacturers to explore synthetic or farmed alternatives, introducing supply chain complexity and price volatility into the value chain.

Market Opportunities

- Humic Acid Controlled-Release Granular Formats for Row Crop Programs: Granulated humic and fulvic acid biostimulants that align with standard dry fertilizer application passes represent a large addressable opportunity in the US corn belt, eliminating the need for additional equipment or application passes while delivering consistent agronomic performance across large row crop acreage in corn, soybean, and wheat production systems.

- Seaweed Extract Expansion in High-Value Specialty Crops: Growing demand for biostimulants in California's specialty crop sector, including berries, tree nuts, vegetables, and citrus, creates premium-priced application opportunities for seaweed extract and amino acid biostimulants. Academic field trials in processing tomatoes across California demonstrated yield improvements of 12-18%, validating the commercial payback case for specialty growers and supporting broader adoption across the Western US.

Market Challenges

- Farmer Education and Adoption Barriers in Conventional Agriculture: Converting large-scale conventional commodity crop farmers, particularly across the Corn Belt and Great Plains, to biostimulant use requires demonstrating clear, financially quantifiable return on investment under their specific agronomic conditions. This demands sustained field demonstration investments, robust agronomic advisory capability, and localized trial data that smaller specialized biostimulant companies may struggle to maintain competitively against established agrichemical majors.

- Competitive Pressure from Synthetic Inputs in Cost-Constrained Farm Environments: During periods of commodity price pressure or elevated input costs, biostimulants face substitution risk as farmers prioritize economically essential inputs such as herbicides, fungicides, and NPK fertilizers over performance-enhancement biologicals. The absence of mandatory regulatory requirements for biostimulant use, unlike certain crop protection inputs, means demand can compress cyclically during farm economic downturns, creating revenue volatility for manufacturers.

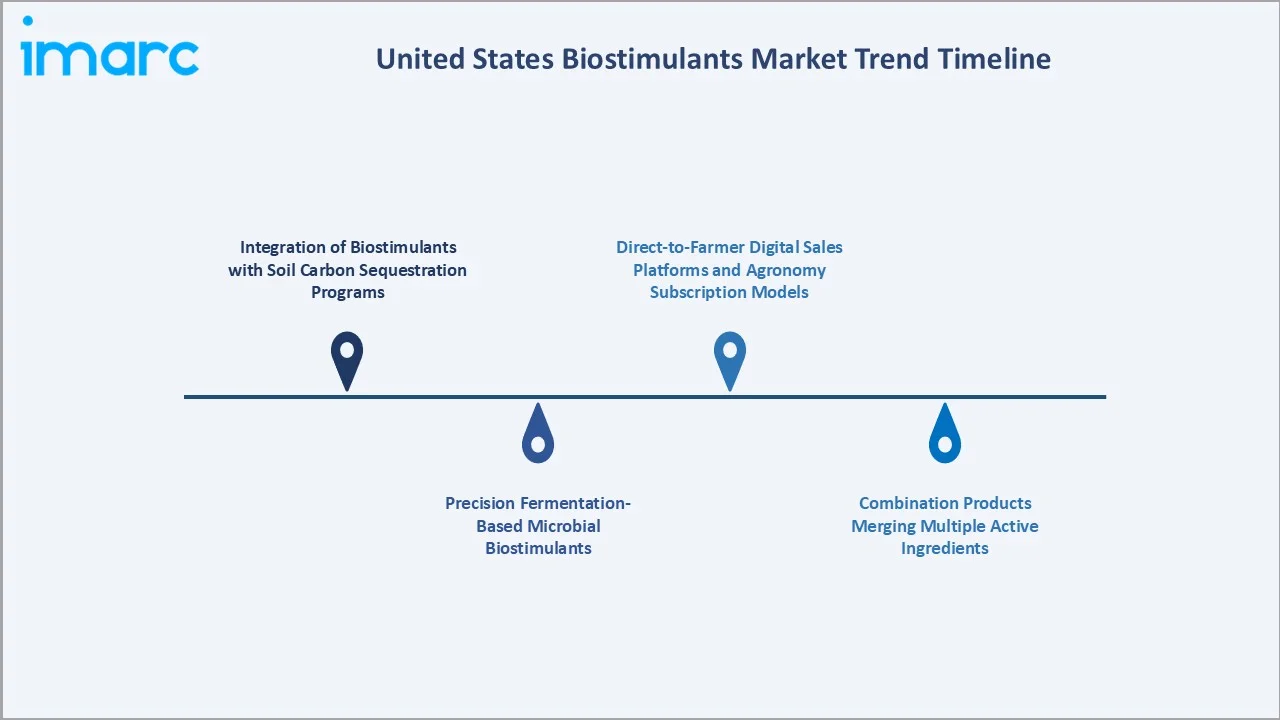

Emerging Market Trends

1. Integration of Biostimulants with Soil Carbon Sequestration Programs

Biostimulants, particularly humic substances and microbial consortia, are gaining significant traction as tools for improving soil carbon content and qualifying participating farmers for voluntary carbon credit programs. The alignment of biostimulant agronomic benefits with emerging agricultural carbon markets creates a dual value proposition of crop performance improvement plus carbon credit revenue, attracting institutional investment into biostimulant product development from sustainability-focused agri-investors and corporate sustainability buyers.

2. Precision Fermentation-Based Microbial Biostimulants

Advances in precision fermentation are enabling the production of highly consistent, standardized microbial biostimulant products at commercially scalable volumes and costs. Unlike traditional fermentation processes, precision fermentation allows targeted production of specific bioactive compounds, improving efficacy predictability and shelf stability while directly addressing the consistency concerns that have historically limited large-scale commercial farmer adoption of microbial biological inputs across US row crop systems.

3. Combination Products Merging Multiple Active Ingredients

Biostimulant manufacturers are increasingly developing combination formulations that merge humic acids, seaweed extracts, amino acids, and microbial components into single-application products that deliver multiple modes of action simultaneously. These multi-function biostimulants reduce application complexity for growers, improve compliance with multi-mode-of-action recommendations, and command premium pricing above single-ingredient products, supporting margin expansion for innovative formulators.

4. Direct-to-Farmer Digital Sales Platforms and Agronomy Subscription Models

Digital agriculture platforms are creating new direct-to-farmer channels for biostimulant manufacturers, bypassing traditional agri-retail intermediaries and enabling more cost-effective customer acquisition and retention. Subscription-based agronomy models that bundle biostimulant products with precision application guidance, soil health monitoring, and performance guarantees are emerging as differentiated go-to-market strategies that create recurring revenue streams and deeper farmer relationships.

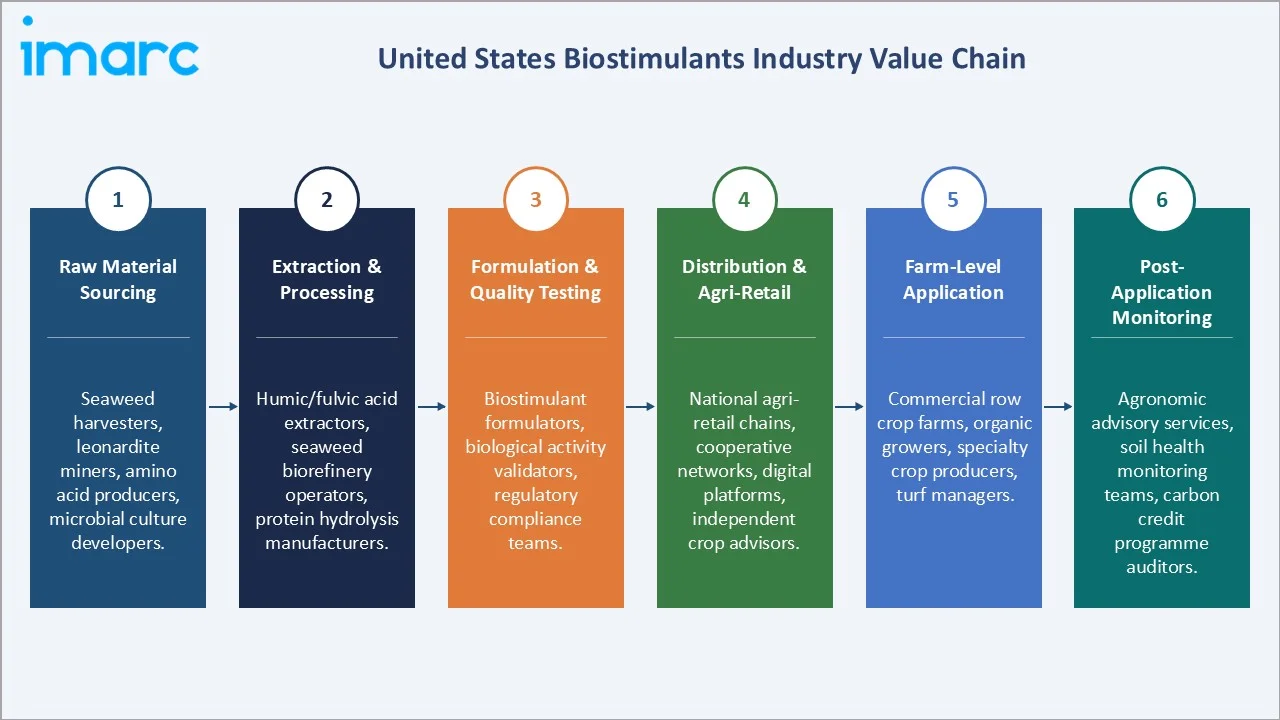

Industry Value Chain Analysis

The United States biostimulants industry value chain integrates raw material sourcing and extraction, active ingredient formulation and quality testing, distribution through agri-retail networks and digital platforms, farm-level application, and post-application agronomic monitoring. The value chain architecture is progressively integrating digital agronomy advisory services as a value-added layer above physical product supply, creating new competitive differentiation opportunities for manufacturers with strong technical expertise.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Seaweed harvesters, leonardite miners, amino acid producers, microbial culture developers. |

|

Extraction & Processing |

Humic/fulvic acid extractors, seaweed biorefinery operators, protein hydrolysis manufacturers. |

|

Formulation & Quality Testing |

Biostimulant formulators, biological activity validators, regulatory compliance teams. |

|

Distribution & Agri-Retail |

National agri-retail chains, cooperative networks, digital platforms, independent crop advisors. |

|

Farm-Level Application |

Commercial row crop farms, organic growers, specialty crop producers, turf managers. |

|

Post-Application Monitoring |

Agronomic advisory services, soil health monitoring teams, carbon credit programme auditors. |

The raw material and extraction tier faces the most significant structural cost pressure through seaweed harvest quota constraints on the Pacific Coast and competition for leonardite humic substance deposits. The formulation tier is experiencing the fastest technology transition as precision fermentation platforms improve product consistency, shelf stability, and regulatory compliance, enabling manufacturers to command premium pricing for standardized biological products.

Technology Landscape in the United States Biostimulants Industry

Humic and Fulvic Acid Extraction and Stabilization Technology

Advanced extraction technologies using alkaline and acid precipitation methods are improving the purity, consistency, and bioavailability of humic and fulvic acid biostimulants derived from leonardite and lignite deposits across the US and imported sources. Modern controlled-release stabilization formulations are extending product shelf life and enabling precision delivery aligned with standard row crop fertilizer application schedules, reducing farm labor requirements and improving adoption economics for large-scale commercial growers.

Seaweed Biorefinery and Extract Standardization

Seaweed biorefinery approaches are enabling the simultaneous extraction of multiple bioactive fractions from kelp and other marine algae sources, including alginates, laminarin, betaines, and cytokinin-like compounds, in a single integrated process. Advanced analytical chemistry standardization of active compound concentrations is improving biostimulant product consistency and agronomic performance predictability, directly addressing the efficacy variability concerns that limit commercial farmer adoption in large-scale row crop systems.

Microbial Formulation and Delivery Technology

In November 2025, Novozymes launched an enhanced microbial biostimulant consortium for US corn and soybean systems, demonstrating 6-9% yield improvement in multi-location trials through improved phosphate solubilization and nitrogen fixation efficiency. Encapsulation technology advances are extending microbial viability through the distribution chain and in soil environments subject to extreme temperature fluctuations, improving product performance reliability and enabling broader geographic deployment across diverse US agricultural regions.

Market Segmentation Analysis

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Acid-Based |

46.8% |

2025 |

|

Crop Type |

🔒 |

🔒 |

2025 |

|

Form |

Liquid |

63.5% |

2025 |

|

Origin |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Midwest |

33.7% |

2025 |

By Product Type

The Acid-Based segment leads at 46.8% in 2025, capturing the humic acid, fulvic acid, and amino acid product categories that collectively serve the US row crop and specialty horticulture markets with well-established, scientifically validated biostimulant products.

To access detailed market analysis, Request Sample

The Extract-Based segment at 38.7% captures seaweed extract and botanical biostimulants experiencing strong adoption in specialty crops and certified organic farming systems. Others at 14.5% includes microbial consortia, protein hydrolysate-based products, and emerging combination formulations gaining commercial momentum through precision fermentation capacity scale-up and increasing grower awareness of multifunctional biological inputs.

By Form

Liquid form leads at 63.5% through compatibility with standard foliar spray, fertigation, and seed treatment application equipment widely deployed across US commercial farms of all scales. Liquid biostimulants enable rapid and uniform bioactive compound delivery to plant root zones and foliar surfaces, making them the dominant commercial format across both row crop and high-value specialty crop applications in the United States biostimulants market.

Dry biostimulants at 36.5%, including granular and powder formats, are gaining market share in the row crop segment through their alignment with standard dry fertilizer application equipment and controlled-release delivery advantages for sustained soil bioactivity.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

Midwest |

33.7% |

Extensive row crop acreage, USDA EQIP program support, precision ag infrastructure, strong agri-retail distribution networks. |

|

South |

31.5% |

Cotton, peanut and vegetable production, growing organic sector, heat and humidity stress driving biostimulant adoption. |

|

West |

21.4% |

High-value specialty crops, California Healthy Soils Program, organic certification requirements, premium produce pricing. |

|

Northeast |

13.4% |

Specialty horticulture, turf management, organic vegetable farming, proximity to major consumer markets. |

The Midwest, at 33.7%, leads through its vast corn and soybean acreage anchoring the US row crop biostimulant market, with precision agriculture integration enabling variable-rate biostimulant application that improves return on investment documentation. The South, at 31.5%, reflects growing biostimulant adoption across cotton, peanuts, and an expanding specialty vegetable production base driven by climate-adaptive farming investments.

The West, at 21.4%, is driven by California's specialty crop sector, the highest per-acre value biostimulant application market in the US, where organic certification requirements and retail residue-free mandates structurally mandate bio-based input adoption. The Northeast, at 13.4%, reflects specialty horticulture, premium turf management, and organic vegetable production serving major metropolitan consumer markets with stringent sustainability procurement standards.

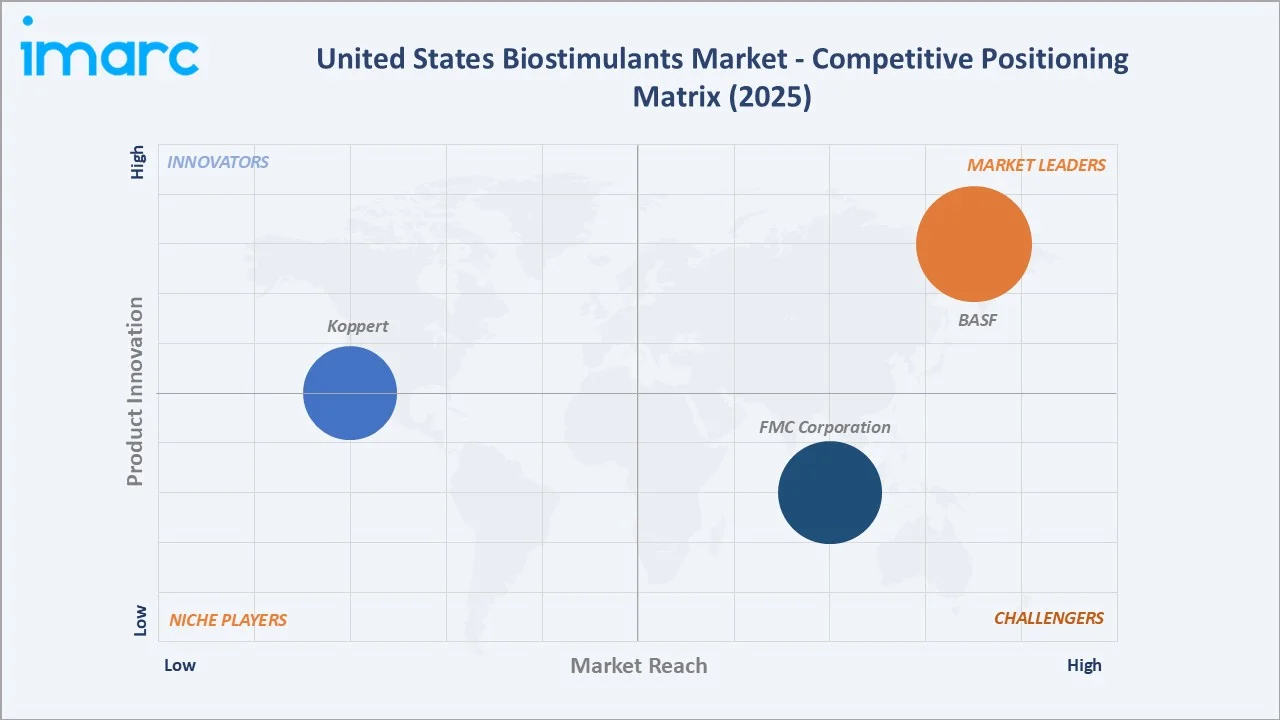

Competitive Landscape

The United States biostimulants market competitive landscape is highly fragmented, with no single company holding a dominant position. Three competitive tiers characterize the market: global agribusiness majors leveraging integrated portfolios and distribution scale, specialized biostimulant companies with deep technical expertise in specific product categories, and emerging domestic players targeting regional crops and sustainability-focused grower segments with differentiated biological solutions.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

BASF |

Optimax biostimulant range; BioSolutions portfolio |

Market Leader |

BASF SE leverages global R&D infrastructure and integrated agricultural solutions to deliver acid-based and microbial biostimulants for US row crops and specialty applications across conventional and organic farming systems. |

|

FMC Corporation |

Biological plant nutrition programs, Zironar |

Strong Challenger |

FMC Corporation focuses on biostimulant programs integrated with its crop protection product portfolio, offering comprehensive crop management solutions to commercial farmers across diverse US agricultural regions. |

|

Koppert |

Vidi Fortum seaweed extract biostimulant; Stingray 25; Vidi Fol fulvic acid biostimulant |

Emerging Player |

Koppert Biological Systems delivers mycorrhizal fungi and Trichoderma-based biostimulants for organic and specialty crop production, with deep expertise in soil biology and integrated biological crop management systems. |

Key players include BASF, FMC Corporation, Koppert, and others.

Key Company Profiles

BASF

BASF is a Germany-based global chemical company with a significant presence in the United States biostimulants market through its agricultural solutions division, offering humic acid, amino acid, and botanical biostimulant products for row crop and specialty horticultural applications across conventional and organic farming systems.

- Key Products: Optimax biostimulant range; BioSolutions portfolio

- Strategic Focus: Expanding integrated biostimulant and crop protection programs for large-scale US commercial farmers, with an emphasis on agronomic services, field trial data generation, and performance guarantees to differentiate from commodity biostimulant suppliers and strengthen farmer retention within the BASF agronomy ecosystem.

FMC Corporation

FMC Corporation is a United States-based agricultural sciences company with a growing presence in the biostimulants market, leveraging its established crop protection distribution network to offer biological and biostimulant solutions targeting row crop, fruit, and vegetable growers across conventional and specialty farming systems in the US.

- Key Products: Biological plant nutrition programs, Zironar

- Strategic Focus: Integrating biostimulant offerings within its broader crop protection and biologicals platform to deliver bundled agronomic solutions for US growers, with emphasis on distribution channel leverage, retailer partnerships, and field performance data to accelerate adoption and reinforce FMC's positioning as a full-spectrum crop input provider across key US agricultural regions.

Market Concentration Analysis

The United States biostimulants market is highly fragmented, with the top five companies holding approximately 6.66% combined revenue share, reflecting the diverse product categories, application methods, and crop types that no single company has yet commercially integrated into a dominant full portfolio offering.

Market concentration is gradually increasing through M&A activity, as large players recognize biostimulants as a structural growth vector within sustainable agriculture. Specialized biostimulant companies and regional distributors with deep agronomic expertise and localized farmer relationships maintain competitive strength through differentiated product development and high-quality technical service delivery.

Investment & Growth Opportunities

Highest Growth Segments

The Acid-Based segment at ~14.1% CAGR, Liquid form at ~13.8% CAGR, West region specialty crops at ~14.5% CAGR from premium per-acre pricing, Midwest large-scale row crop biostimulant programs at ~13.5% CAGR, microbial biostimulants for soil carbon sequestration programs at ~16% CAGR from a smaller base, and precision fermentation-based standardized biological products at ~18% CAGR represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Specialty crop biostimulant programs in California's high-value horticultural production systems represent the highest per-acre value emerging investment opportunity, with premium crops generating 5-10x the per-acre biostimulant revenue of row crop applications. California's Healthy Soils Program, USDA organic certification requirements, and retailer residue-free sourcing mandates create structurally growing demand for validated bio-based crop inputs through 2034 and beyond.

Investment Themes

- Soil carbon program integration for biostimulant products qualifying for voluntary carbon credit revenue: The convergence of agronomic biostimulant benefits with soil carbon sequestration measurement creates a dual monetization pathway of direct crop performance revenue plus carbon credit revenue that fundamentally improves farmer return on investment economics and accelerates large-scale biostimulant adoption across the US Corn Belt and Great Plains.

- Precision fermentation-based microbial biostimulants targeting product consistency limitations: Investment in precision fermentation manufacturing for standardized high-efficacy microbial biostimulants directly addresses the primary large-scale farmer adoption barrier of performance consistency, creating a differentiated premium product tier that commands pricing above traditional biological inputs and builds structural competitive advantage through proprietary strain libraries and manufacturing know-how.

Future Market Outlook (2026-2034)

The United States biostimulants market is projected to grow from USD 867.3 Million in 2025 to USD 2,702.5 Million by 2034, delivering a 13.46% CAGR over the forecast period. The anchor value of USD 1,630.8 Million in 2030 represents the market at a critical commercial inflection where biostimulants transition from supplemental performance inputs to essential components of sustainable crop management programs across both conventional and organic US farming systems.

The precision agriculture and biostimulant convergence creates an additive data-driven demand pool above simple agricultural acreage growth by enabling ROI quantification that justifies adoption by cost-conscious commercial farmers. The soil carbon credit market development creates a third-party economic incentive for biostimulant adoption independent of direct crop yield return on investment, materially improving the adoption economics across large-scale conventional farming operations.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders conducted in 2025, including Chief Agronomists at biostimulant manufacturing companies, commercial row crop farm managers across key Midwest production states, specialty crop growers in California and Florida, agri-retail distribution executives, and USDA program administrators managing biostimulant-eligible conservation and sustainability funding programs across multiple US agricultural regions.

Secondary Research

Secondary research encompassed company annual reports and product launch announcements, USDA National Organic Program certification and acreage data, USDA Economic Research Service farm input adoption surveys, EPA biostimulant regulatory filings and guidance documents, Organic Trade Association annual industry surveys, state agricultural department biostimulant program documentation, and peer-reviewed agronomic field trial publications from major US land-grant universities. Over 50 secondary sources were reviewed and triangulated.

Forecasting Models

Market revenue forecasts were developed using a bottom-up modeling approach incorporating: US agricultural acreage by crop type and farming system projections, biostimulant penetration rate assumptions by crop type and organic versus conventional system, average biostimulant spend per treated acre by product type and application method, and product mix adjustment factors reflecting the observed premiumization trend toward liquid formulations, combination products, and precision fermentation-derived biological inputs.

United States Biostimulants Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered |

|

| Crop Types Covered | Cereals and Grains, Fruits and Vegetables, Turf and Ornamentals, Oilseeds and Pulses, Others |

| Forms Covered | Dry, Liquid |

| Origins Covered | Natural, Synthetic |

| Distribution Channels Covered | Direct, Indirect |

| Applications Covered | Foliar Treatment, Soil Treatment, Seed Treatment |

| End Users Covered | Farmers, Research Organizations, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | BASF, FMC Corporation, Koppert, etc. |

| Customization Scope | 10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States biostimulants market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States biostimulants market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States biostimulants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Biostimulants Market Report

The US biostimulants market reached USD 867.3 Million in 2025, driven by the Acid-Based product type dominant at 46.8%, Liquid form leading at 63.5%, Midwest regional share at 33.7%, growing organic food demand, USDA incentive programs, and the integration of precision agriculture platforms with biostimulant application programs across commercial row crop and specialty farming systems.

The US biostimulants market grows at 13.46% CAGR during 2026-2034, reaching USD 2,702.5 Million by 2034. This growth reflects organic farming expansion, soil carbon program development, biostimulant integration with precision agriculture platforms, and increasing large-scale commercial farmer adoption across row crops and specialty horticultural production systems.

Acid-Based biostimulants lead at 46.8%, capturing humic acid, fulvic acid, and amino acid products widely adopted across US corn, soybean, wheat, and specialty vegetable production. The segment grows at ~14.1% CAGR through controlled-release granular format expansion in the Corn Belt and amino acid biostimulant adoption in high-value specialty horticultural crops.

Liquid form leads at 63.5% through compatibility with standard foliar spray, fertigation, and seed treatment equipment widely deployed across commercial US farms. Liquid biostimulants enable rapid bioactive compound delivery and grow at ~13.8% CAGR. Dry granular formats are gaining market share through Corn Belt row crop program integration alongside NPK fertilizer applications.

The Midwest leads at 33.7% through extensive corn and soybean acreage, strong agri-retail distribution networks, USDA EQIP program funding, and established precision agriculture infrastructure enabling biostimulant integration with variable-rate application systems across large commercial farming operations.

Leading companies include BASF, FMC Corporation, Koppert, and others.

The US biostimulants market is projected to reach approximately USD 1,630.8 Million by 2030, with liquid biostimulants integrated with precision fertigation becoming standard practice in commercial row crop systems, California specialty crop programs representing the highest per-acre value market, and soil carbon sequestration programs providing additional economic incentives for biostimulant adoption across conventional farming operations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)